nthetrade nissue 31 njan-mar 2012 77

The 2012 Algorithmic

Trading Survey

Recognising excellence in the delivery of algorithmic trading solutions

Featuring

n

Market review

n

Broker roll of honour

n

Market feedback

Market review

78 nthetrade nissue 31 njan-mar 2012

Arms race

intensifies

Illustration: iStockphoto

n

The 2012 Algorithmic Trading Survey

O

ver the past 12 months, the response of the buy-side to low volumes and periods of high volatili-ty has been crystal clear. The answer to tougher con-ditions isn’t scaling back your providers. It’s algorith-mic proliferation – making sure you have the right weapons at your disposal, from wherever you can get them.This year, The TRADE’s 5th annual Algorithmic Trading Survey shows trad-ers using more algorithms from an increased number of providers for a lot more volume. Our most compre-hensive survey yet brings over 750 individual views

from more than 150 respondents located in every major trading centre around the globe.

Why I’m a believer

Even though budgets on trading desks are tight, from IT-savvy quant-driv-en algo ‘natives’ to old-school traditionalists, it seems almost everyone is using algorithms and they’re engaging with more providers than ever before.

But when it comes to why they select algos from the available execution options, trader motives aren’t budging, and the top three reasons have

More algos, more often

from more providers

When the going gets tough, buy-side traders

turn to their algos, The TRADE’s 5th annual

Algorithmic Trading Survey reveals.

nthetrade nissue 31 njan-mar 2012 79

remained the same from 2011 to 2012. This year, the most popular reason for using an algo remained the desire to reduce market impact, increasing margin-ally to 13.6% from 13.3% as the buy-side’s primary need. Minimising implicit costs is one of the trader’s core objectives of course, but the desire to reduce market impact is only intensifying at a time when the buy-side is executing an increasing proportion of trades in the dark. Once more, the second most important reason for buy-siders to use algos was ease of use (12.1%, slightly down from 12.3%), fol-lowed by increased trader productivity (11.1% down from 11.3% in 2011).

Consistency of execution performance remained a constant reason for trading electronically, up marginally to 10.7% from 10.5% in 2011, while slightly more respondents recognised the importance of using algos

to enjoy greater anonymity in trading.

But in 2012, fewer trad-ers opted for algos for rea-sons of price improvement.

Just 7.8% – down from 8.3% in 2011 – believed trading via algos was important to find better prices.

Market review

n

The 2012 Algorithmic Trading Survey

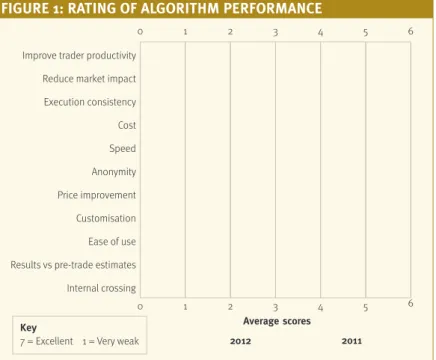

0 1 2 3 4 5 6 0 1 2 3 4 5 6

Internal crossing Results vs pre-trade estimates Ease of use Customisation Price improvement Anonymity Speed Cost Execution consistency Reduce market impact Improve trader productivity

Average scores

2012 2011

Key

7 = Excellent 1 = Very weak

FIgure 1: ratIng oF algorIthm perFormance

Source of all charts: The TRADE Annual Algorithmic Trading Survey

Match pre-trade estimates 2.2% Internal crossing 10.4% Ease of use 12.1% Customisation 7.4% Price improvement 7.8% Anonymity 10.8% Speed 5.4% Commission rates 8.6% Execution consistency 10.7% Reduced market impact 13.6% Trader productivity 11.1%

FIgure 2: reasons For usIng algorIthms

Traders are using

more algorithms

from an increased

number of providers

for a lot more

80 nthetrade nissue 31 njan-mar 2012

Market review

n

The 2012 Algorithmic Trading Survey

relatively low level of importance is offset by comments made by respondents on the addi-tional features they’d like to see introduced by

providers.

Many survey respond-ents expressed a straight-forward desire for “more customisation”, while the majority of those willing

to give their algo provid-ers more of a steer indi-cated a continuing need for algos to be adapted to take advantage of dark trading opportunities (more than one demanded liquidity aggregation and customised SOR settings).

One respondent pro-posed “an option to lift quickly the bid/offer and then to drag the execution into an existing ticket”, while a large institutional investor suggested “the ability to access multiple dark pools under own identity”.

Alongside this, other algo users called for pro-viders to deliver more and faster execution data and analysis across different venues. Still others sought greater levels of ‘in-trade’ service from their brokers, as well as dynamic, respon-sive algos that react “to market signals/technicals, market news, company earnings, macro data etc”.

A sizeable minority requested enhanced And in what may be a

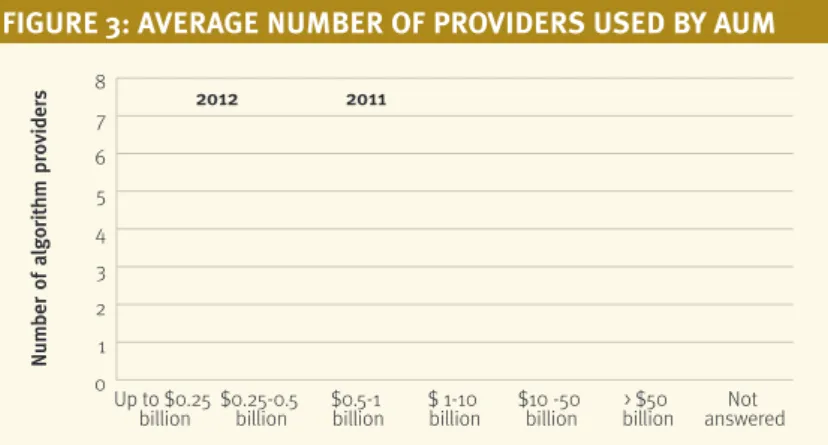

surprise for many provid-ers, being fastest was not seen as important to buy-siders, with only 5.4% list-ing speed as a reason for trading via an algorithm, down from 7.2% last year. Customisation capabilities experienced a slight rise in popularity to 7.4% from 6.9% in 2011 but this 0 1 2 3 4 5 6 7 8 Not answered > $50 billion $10 -50 billion $ 1-10 billion $0.5-1 billion $0.25-0.5 billion Up to $0.25 billion

Number of algorithm providers

Assets under management

2012 2011

FIgure 3: average number oF provIders used by aum

One can only

sympathise with the

trader that made a

plaintive plea for

“Simplicity!”

0 10 20 30 40 50 2012 2011 >12* 8-12* 5-7 3-4 1-2 % of respondents Number of providersFIgure 4: number oF provIders used

* In 2011, respondents could only specify a maximum of ‘five or more’ algo providers

Market review

nthetrade nissue 31 njan-mar 2012 81

Market review

n

The 2012 Algorithmic Trading Survey

Market review

n

The 2012 Algorithmic Trading Survey

In this year’s survey, on average, buy-side traders were most impressed with the ease of use of their algos, scoring them 5.4 out of seven, a slight dip from 2011. Qualities almost equally impressive – all scoring 5.3 out of seven – were the increase in trader productivity algos offered, execution consistency and cost.

one is not enough

While smaller players slightly reduced the number of algorithm providers they used since last year’s survey, the larger houses dramati-cally raised the number of shops on their roster.

On average, buy-siders with assets under manage-ment (AUM) of up to US$250 million dropped providers, with the average number slimming to 2.18 from 2.41. But these were the exception.

Buy-side firms manag-ing between US$500 mil-lion and US$1 bilmil-lion, for example, almost doubled the average number of algo providers they used from 2.36 to 4.12. Houses with AUM of US$1 billion to US$10 billion increased their average number of providers to 4.74 from 3.65, while those with AUM of the “ability to delta hedge

with options” and “better derivative capability”.

One can only sympathise with the trader that made a plaintive plea for “Simplicity!” cross- and multi-asset

capabilities, such as algo-rithms that trade both equities and futures, pairs, portfolios and baskets. One buy-side trader specified

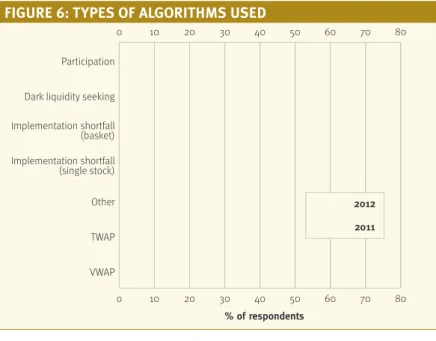

0 10 20 30 40 50 60 70 80 0 10 20 30 40 50 60 70 80 VWAP TWAP Other Implementation shortfall (single stock) Implementation shortfall (basket) Dark liquidity seeking Participation

% of respondents

2012 2011

FIgure 6: types oF algorIthms used

% of respondents

% of value traded using algorithms

0 10 20 30 40 50 Not answered 40% and over 30-40% 20-30% 10-20% 5-10% 0-5% 2012 2011

FIgure 5: algorIthm usage by value traded

Dark liquidity-seeking algorithms remained the

weapon of choice

82 nthetrade nissue 31 njan-mar 2012

Market review

n

The 2012 Algorithmic Trading Survey

Even fewer traders (12.6%) found use for bas-ket implementation shortfall this year, compared to last year (16.1%) and just over a quarter of respondents claimed to be using TWAP.

But algorithm prefer-ences have shifted since 2010. Two years ago, far more buy-siders claimed to use dark liquidity seeking algos (80%), and single stock implementation shortfall was the second-most used algo at alsecond-most 70%. This year, less than half of respondents (48.2%) reported using single stock implementa-tion shortfall.

Temporary market con-ditions will inevitably play some part in the choice of algorithm type but it seems clear that the general trend is toward trusting algorith-mic providers to come up with the right tool regard-less of the circumstances. Should this – and the rise in the average number of pro-viders used – be a source of comfort to the sell-side? The results of The TRADE’s 2012 Algorithmic Trading Survey suggest there is plenty of scope for differen-tiated offerings to capture market share, but ongoing investment is required to stay on top. n

five-plus algo providers and around a third used one-to-two shops.

Yet in some ways, the electronic trading land-scape is dramatically differ-ent from two years ago. In 2010, barely a third of respondents said they used algos for 40-plus per cent of their trading, yet this year almost half of all respondents (46.12%) relied on algos for that same volume of execution. Those using algos the least – for less than 5% of their trading – halved to 6.31% this year. Overall, the trend seems to be for more algo use for more trades. The percentage of respondents using algos for only 10-20% of trades dropped to 10.64% from 18.79% in 2011, while the proportion executing via algo for 20-30% of their trades rose to 18.76% from 13.42% a year earlier.

choose your weapon

In the electronic trader’s arsenal, dark-liquidity seek-ing algorithms remained the weapon of choice for the buy-side in 2012, with 72.1% of respondents claiming to use the algo type. Perennial favourite VWAP held its third-place position this year at 58.7%. US$10 billion to US$50

bil-lion added on average just over one provider to 5.39 from 4.14 in 2011. But the largest buy-siders added the most new algo shops, with firms managing US$50 bil-lion and above signing on average more than two extra providers – from 4.14 in 2011 to 6.59 in 2012. Although 2011’s survey revealed a tailing off in number of providers across most firms, large or small, 2012 generally exceeds even 2011’s highs. For example, the biggest firms were still using just shy of five algo providers on average two years ago.

Increasing appetites?

Almost half of all respond-ents (48.9%) last year said they only used one-to-two providers and only 32.2% used more than five provid-ers. Yet this year, 41% of respondents admitted to using more than five pro-viders – and in fact, 16.5% said they used more than eight algo shops (with 6.1% using more than 12).

But the sharp uptick per-haps belies a return to nor-malcy, as this year respond-ent behaviour was more in line with our 2010 survey results, where over 40% of respondents claimed to use

84 n thetrade n issue 31 njan-mar 2012

Broker Roll of Honour

n

The 2012 Algorithmic Trading Survey

Illustration: iStockphoto

Functional capabilities

The 2012 broker Roll of Honour

IMPROVING TRADER PRODUCTIVITY ROLL OF HONOUR Goldman Sachs Société Générale UBS ONES TO WATCH BNP Paribas Fidelity

In terms of areas that influence the extent and types of algorithms used, trader productivity was ranked the third most important in this year’s survey, mentioned by more than 60% of respondents. In 2011 this question attracted the second most positive scores. But Survey respondents were asked to provide a rating for each algorithm provider

on a numerical scale from 1.0 (very weak) to 7.0 (excellent), covering 11 functional criteria. Data taken from over 750 separate evaluations was used to compile the provider Roll of Honour. In assessing the rankings, the judgements of the various respondents were weighted according to three components: the value of assets under management; the proportion of business done using algorithms; and the number of providers being used. This meant that the most important evaluations were assigned as much as three times the weight of the least important.

In arriving at the overall Roll of Honour the scores received in respect of each of the 11 functional capabilities were further weighted according to the importance attached to each of them by respondents to the survey. The aim is to ensure that in assessing service provision, the greatest impact results from the scores received from the most sophisticated and active market participants in those aspects of service they regard as most important. In addition, there is close scrutiny of individual responses to ensure that individual assessments that are very favourable or unfavourable do not distort average scores unduly.

MEASURING FUNCTIONAL CAPAbILITIES

1 Roll of Honour recipients are listed in alphabetical order throughout the survey.

n thetrade n issue 31 njan-mar 2012 85

Broker Roll of Honour

n

The 2012 Algorithmic Trading Survey

respondents continued to use algorithms for a high proportion of their of trades, than the proportion by value, also suggests that most consider algorithms to be an effective way of dealing with smaller orders.

COSTS AND COMMISSIONS

ROLL OF HONOUR

Bank of America Merrill Lynch ITG

UBS

ONES TO WATCH

Fidelity Société Générale

A key feature of algorithmic trading is the opportunity it offers the buy-side to reduce costs of trading. The most obvious cost component is the lower commission charged by brokers compared with full service offerings.

While improved trader productivity was ranked with equal significance, Credit Suisse. Overall scores were

marginally below those seen in 2011 at 5.24 compared with 5.28.

The level of importance of this aspect of service increased once again. It garnered more mentions from respondents as being a key element in their decision to use algorithms than any other aspect. Together with the growing importance of anonymity, this suggests clients see the ability to trade larger orders more surreptitiously than using sales traders as a key benefit of algorithmic trading. Simply put, most clients see algorithmic trading as being an important way to ‘hide’ their activity from the market as a whole, thereby improving execution performance.

However, the wide range of scores seen even among leading providers suggests that not all clients are convinced about the effectiveness of all algo suites in dealing with large orders. The fact that most this year levels of satisfaction

diminished to a statistically meaningful extent. The average score this year was 5.32, down from 5.47, suggesting that around 15% of respondents gave a lower score this year than in 2011. To some extent this may simply reflect the generally lower level of trading activity seen in the market, which undermines the benefits of automation within the trading process. Growing complexity in the way clients use algorithms may also be a factor in lower scores as ease of use experienced a similar level of decline in satisfaction rates.

Among the leading banks in terms of responses, UBS repeated its position in the Roll of Honour with consistently good scores across the vast majority of clients. Together with Goldman Sachs and Société Générale, UBS saw average scores in excess of 5.50. Among banks with fewer responses, excellent scores were received by BNP Paribas and Fidelity who clearly offer a service that is attractive to clients and may allow them to increase their penetration before next year’s survey.

REDUCING MARKET IMPACT

ROLL OF HONOUR Credit Suisse Goldman Sachs Morgan Stanley ONES TO WATCH Knight Capital Liquidnet

Goldman Sachs repeated its Roll of Honour position this year, joined once again by Morgan Stanley and

Broker Roll of Honour

86 n thetrade n issue 31 njan-mar 2012

n

The 2012 Algorithmic Trading Survey

5.38 they were the second best in the survey, only behind ease of use. This is an area where algorithms continue to meet client expectations. Anonymity is an important factor in why respondents choose to use algorithms and, based on number of mentions, has increased in relevance over the last year.

Evaluation of performance in this area can be rather subjective. To some extent clients will look at slippage and other measures of market impact on individual trades. But while pre-trade cost estimates may be a guide in setting

performance expectations, they are recognised as being only part of the evaluation. In some cases traders may work large orders using algorithms for part of the trade. Even that is an imperfect measure. However, all providers would want to satisfy clients in this area and generally they do. Banks that scored well clearly demonstrated superior performance, including the Ones to Watch who showed either improved scores from a year ago (Citi) or very good scores from a smaller group of respondents (Royal Bank of Canada).

SPEED ROLL OF HONOUR Bloomberg Knight Capital Morgan Stanley ONES TO WATCH Weeden Citi

Smart order routers (SORs) are crucial for effective execution in fragmented markets. These are positive responses. Fidelity is a

relative newcomer to the survey and scored strongly on this question. Société Générale is a well-established provider who scored highly in this area but whose respondent numbers put them in the Ones to Watch category.

ANONYMITY ROLL OF HONOUR Barclays Capital Credit Suisse Instinet ONES TO WATCH Citi

Royal Bank of Canada

Scores for anonymity were marginally higher in 2012 than a year earlier. At different clients and brokers will see

each of these facets as being of different relative importance.

The range of scoring is therefore likely to be quite large and the same buy-side trader may use various brokers for a range of reasons. Good performance here suggests that brokers are aware of one of the key drivers for many clients. Interestingly, in 2012 average scores in this area improved quite noticeably from 5.25 to 5.32, reversing a trend towards weakening scores seen over previous periods.

As well as UBS, good scores were recorded by Bank of America Merrill Lynch, which also performed well in this category last year, and ITG, which received a large number of

n thetrade n issue 31 njan-mar 2012 87

Broker Roll of Honour

n

The 2012 Algorithmic Trading Survey

critical to their evaluation process. This is also an area where it is possible to assess performance with some quantitative analysis. Slippage can be compared to market volatility and performance against any relevant benchmark is easy to assess.

Performance is traditionally dominated by the major service providers. That situation was clear again in this year’s survey. Morgan Stanley repeated its Roll of Honour position from 2011 and was joined this year by Bank of America Merrill Lynch and UBS. Among newer providers with fewer respondents, Fidelity and Liquidnet both scored highly suggesting that they understand the importance of this aspect of service across a broader client base. Overall scores averaged 5.25 in 2012 across the survey, almost exactly the same score that was seen in 2011.

EASE OF USE

ROLL OF HONOUR

Bank of America Merrill Lynch Credit Suisse

Deutsche Bank

ONES TO WATCH

CA Cheuvreux J.P. Morgan

Survey respondents ranked ease of use as the second most important aspect of algorithmic use, behind reducing market impact.

As the number of different strategies and algorithmic providers increases, how easy algorithms are to use becomes more important. Across all respondents the number of mentions this factor received It is also an area where the best

scores seem to have been awarded to newer market participants rather than the more established names, with the notable exception of Morgan Stanley, which appears in the Roll of Honour for the second year in a row.

EXECUTION CONSISTENCY

ROLL OF HONOUR

Bank of America Merrill Lynch Morgan Stanley

UBS

ONES TO WATCH

Fidelity Liquidnet

For clients that use algorithms to handle large numbers of relatively small orders, execution consistency, rather than outperformance, is the key to satisfaction. Compared to last year, this area increased slightly in importance for all respondents but still only ranked fifth.

However, comments suggest that for some clients it is much more typically provided by brokers and

independent software vendors, although some buy-side firms have built their own.

For SORs to work effectively, all need to operate with very low latency. Algorithmic trading now depends heavily on smart order routing and as such there is a dependency on high speed functionality. However, it is not clear that clients appreciate this component of service.

It attracted relatively few mentions as being a decision factor and also declined in importance compared to a year ago. This may reflect the fact that clients find it impossible to assess or analyse latecy. Equally it may reflect an environment where speed is seen as less important, given the buy-side’s focus on anonymity and lower market impact. Scores remain strong in this area; the average was unchanged at 5.35. Clearly clients recognise the value in terms of electronic trading, but perhaps cannot differentiate at a specific provider level.

88 n thetrade n issue 31 njan-mar 2012

Broker Roll of Honour

n

The 2012 Algorithmic Trading Survey

actually decreased marginally over the last year but still accounted for more than 12% of the overall total. Scores remained the best in the survey with an average score of 5.44, but were lower than the 5.60 average recorded in 2011.

None of the Roll of Honour names from 2011 made the list this year, which may reflect the pace of change in an industry where front-end features are increasingly easy and cheap to update. Ease of use can also be impacted by use of different order and execution management options. A level of satisfaction with those delivery mechanisms may affect users’ perception of underlying algorithmic capabilities. There is also the potential trade-off between new features and simplicity of use that could effect change from one year to the next. In any event the Roll of Honour names and the Ones to Watch all demonstrated an ability to be effective in the eyes of a large number of respondents. INTERNAL CROSSING ROLL OF HONOUR ITG Morgan Stanley UBS ONES TO WATCH Citi Sanford Bernstein

For some clients internal crossing is an integral part of reducing the market impact that can result from algorithmic trading. Indeed some brokers offer that as a key advantage, with crossing percentages being used as a differentiator. For other respondents crossing is an undesirable way in which their natural orders may interact with toxic flow. In some cases brokers make a virtue out of not having an internal pool. These views may result in anomalies with some respondents praising brokers without any internal crossing while others regard that as a weakness and score accordingly. This is also

reflected in the fact that at nearly 1.5 points, the range of scores across the top fifteen banks (based on number of responses) is the highest of any question in the survey.

Overall scores had an average of 5.10, slightly lower than in 2011 and among the three lowest scores in the whole survey. But some individual banks performed well, which may reflect clarity in their approach as well as actual performance. Morgan Stanley and UBS both repeated their Roll of Honour mention from 2011 and this year were joined by ITG. Citi has also been getting high praise for its matching services and is joined in the Ones to Watch by Sanford Bernstein. PRICE IMPROVEMENT ROLL OF HONOUR Goldman Sachs Knight Capital UBS ONES TO WATCH BNP Paribas Fidelity

A major objective of investment in ever more sophisticated algorithmic trading services has been the ability to improve the average price achieved on orders, although this can be hard to prove. The average score across the survey was only 5.09, which while better than the 5.05 recorded in 2011 was still poor. Respondents remain less convinced by this aspect of service than any other. Among brokers receiving significant levels of responses, average scores ranged between 4.50 and 5.50.

n thetrade n issue 31 njan-mar 2012 89

Broker Roll of Honour

n

The 2012 Algorithmic Trading Survey

Broker Roll of Honour

n

The 2012 Algorithmic Trading Survey

CONSISTENCY WITH PRE-TRADE ESTIMATES ROLL OF HONOUR Citi ITG Nomura ONES TO WATCH BNP Paribas MacquarieThis question appears to be the hardest for respondents to be enthusiastic about and continues to attract by some way the lowest number of mentions among factors that influence either the use of algorithms or respondent views of service levels. It also has

consistently seen the lowest scores within the survey. The average in 2012 was 5.07. Though better than last year, this still reflected the lowest number of actual evaluations. This conclusion is surprising given the amount of money, time and effort spent by brokers to create models and formulas that seek to create pre-trade estimates.

There is no doubt that every broker uses a different model, and in some cases a different theoretical construct in their process as well as different historic data. Clearly some form of standard needs to be created if banks are not to continue to waste their resources. In the meantime, the banks that have done well deserve particular praise in that they seem to have encouraged their clients to care and understand enough about the process to differentiate between their various providers.

Nor is there much consistency among the more successful providers in this area. The top three Roll of Honour names are to be commended on their scores, with none of the firms that scored highly last year appearing this year.

This suggests that scoring for this category may be more anecdotal, reflecting recent good or bad experience. Consistent performance in this area remains as hard to achieve. The good, or perhaps bad news is that respondents do not appear to value this aspect as being especially important to either their use of algorithms generally or their use of a particular broker specifically. CUSTOMISATION ROLL OF HONOUR Deutsche Bank ITG Morgan Stanley ONE TO WATCH Barclays Capital Citi

Algorithms continue to get more and more sophisticated in terms

of parameterisation, execution aims and objectives. As clients become more familiar with algorithms and expand the number of providers they use, customisation becomes a useful and valued capability and is growing in terms of numbers of mentions from respondents. That it is now seen as being more important than lower latency may surprise some. Average scores are also showing signs of improving. The average of 5.23 in this year’s survey is well ahead of the 5.17 recorded in 2011.

Both ITG and Morgan Stanley repeated their Roll of Honour rankings from 2011. This year they were joined by Deutsche Bank, which replaced UBS from the 2011 list. Perhaps as important was that Barclays Capital again came close to a Roll of Honour position and Citi showed a marked improvement in scores in this area as well. But few banks are being left behind in this particular arms race. The range of scores among the top fifteen providers by number of responses, was the narrowest in the survey at 0.86.

Broker Roll of Honour

90 n thetrade n issue 31 njan-mar 2012

n

The 2012 Algorithmic Trading Survey

scores, then providers can be confident they are doing well. The average scores from this group are generally lower than the survey as a whole reflecting the fact that for the most part they are more demanding and more sophisticated users. It is interesting, but not surprising, that the three Roll of Honour names in 2012 are the same as those in 2011. While many would wish opinions could be changed quickly, the fact is that they cannot. Reputations are established over years not months. Once a bank has established itself with this group of clients it will compete very hard to maintain its position and reputation. However, as the number of responses for newer providers illustrates clients are increasingly willing to test out new alternatives and, where they prove themselves, grow those relationships alongside those that have been around for longer. n trading with algorithms, the number

of providers used and the willingness of the respondent to differentiate between various aspects of service and the strengths and weaknesses of the providers they use.

Some respondents use different providers for different types of business but this does not invalidate the effect of scoring. They form a unique and valuable group against which providers can and should assess their performance. If this group of clients is giving good

LEADING CLIENTS ROLL OF HONOUR Credit Suisse Goldman Sachs UBS ONES TO WATCH Morgan Stanley J.P. Morgan

Leading clients represent a specific category within the survey. Inclusion reflects the extent of business done using algorithms, the breadth of

Overall performance

As well as considering the functional capabilities of algorithm providers, the survey also assessed overall performance as measured across all capabilities. This analysis took account of both un-weighted and weighted scores based on the different levels of importance attached to the various aspects of service covered in the survey.

nthetrade nissue 31 njan-mar 2012 95

Market feedback

A problem shared

Illustration: iStockphoto

n

The 2012 Algorithmic Trading Survey

D

ark liquidity-seeking algorithms were again the most commonly used strategy by respondents to The TRADE’s Algorithmic Trading Survey in 2012, but the underlying story is one of customisation and adaptability.The last year has seen the continued evolution of elec-tronic trading technology and a growing proliferation in the range of venues and channels to market. This may look good for customer choice, but in reality it’s bad for trading in size. To sup-port the buy-side’s search for liquidity, the last 12 months has seen a prolifera-tion of algorithmic trading strategies and order routing permutations offered by sell-side providers, together with an expansion in execu-tion consulting services and an increasing demand for quality quantitative data, research and analytics.

Driven by the dearth of liquidity to derive more value value from their algos,

the trading desks of institu-tional investment firms have reached new levels of insight and expertise. “Buy-side algo usage has moved on from its function as an efficiency tool to a method of preserving alpha as an integral aspect of the invest-ment process. We are look-ing for our algo providers to push forward and take the next steps to demon-strate that these are not just efficiency tools,” says Huw Gronow, director of European equity trading and investment operations at Principal Global Investors (PGI), the invest-ment arm of Principal Financial Group, a US-headquartered retire-ment and investretire-ment man-agement company with US$335.8 billion assets under management.

Brokers recognise and are responding to the grow-ing buy-side sophistication and engagement in the algorithmic trading process, says Duncan Higgins, head

In a market environment that prioritised alpha

capture, buy-side traders engaged in deeper

collaboration with brokers to develop more

tailored and responsive algorithms.

Market feedback

96 nthetrade nissue 31 njan-mar 2012

n

The 2012 Algorithmic Trading Survey

of electronic sales for EMEA at agency-broker ITG. “Investment managers are matching their trading approach and the algos they use to the alpha in the trade. Demand for algo-rithms working in specific ways for specific investment flows has been growing and I expect that to continue to grow over the next 12 months,” he says.

“Clients are much more open to understanding nuances between different algos from different bro-kers and using them when they feel they are the right ones to accomplish a par-ticular strategy,” adds Joe Wald, managing director

at US agency broker Knight Capital.

Volatile reaction

Regular periods of equity market volatility, particular-ly during Q3 2011, trig-gered by political and eco-nomic uncertainties across Europe, had a notable impact on algo selection. “Volatility has provided us with a much more challeng-ing environment, where alpha preservation is a pri-ority and algo usage has been adapted accordingly. We’ve relied a lot less on scheduling strategies and biased our activity to opportunistic liquidity-seeking strategies and

focused on minimising sig-nalling risk,” says Gronow.

Brian Schwieger, head of EMEA algorithmic execu-tion at Bank of America Merrill Lynch, witnessed a divergence in buy-side exe-cution styles as traders sought to counteract volatil-ity. “Clients have migrated towards either long dura-tion VWAP or very short duration implementation shortfall (IS) and liquidity-seeking algorithms. During more ‘relaxed’ times, as have held sway in Q1 2011, we see preferences migrating back towards medium dura-tion IS strategies,” he said.

In volatile conditions, many stay out of the market unless a trade is absolutely necessary. As such a prefer-ence for opportunistic and dark liquidity-seeking algo-rithms in periods of market uncertainty can also be explained by “a greater amount of conviction in investment decisions and therefore in trading deci-sions”, says Higgins.

Emphasising the impor-tance of capturing liquidity quickly and efficiently in vol-atile markets, Wald observes that the make-up of liquidity in many venues (both lit and dark) has become very simi-lar, which places a premium on tools and strategies that

n

“Competition for liquidity amongst both short-term and long-term alpha players has grown more than ever before.”nthetrade nissue 31 njan-mar 2012 97

Market feedback

n

The 2012 Algorithmic Trading Survey

“Competition for liquid-ity amongst both short-term and long-short-term alpha players has grown more than ever before,” explains Wald. “A short-term alpha player is using sophisticated radar technology to scan the markets to find trades they want to do. If you’re a buy-side trader competing against them you need to have tools that basically act as radar jamming tech-niques to prevent them from using your order flow to gain information.”

From an order routing perspective, Gronow says it is incumbent on the buy-side to remain informed about where their orders are being routed – and onward routed. “Collecting and monitoring this information presents a significant chal-lenge and is part and parcel of the buy-side move towards more self-directed trading as a significant part of their overall implementa-tion strategy,” he notes.

Simo Puhakka, head of trading at Helsinki-based Pohjola Asset Management and CEO of Pohjola Asset Management Execution Services, warns of the risks that potential inherent sell-side conflicts of interest and market impact costs pose in the hunt for liquidity across

dark and lit venues. “We all know that smart order routing should try to find liquidity at the right time and minimise market impact, but in many cases we found that our order either doesn’t hit the smart order router at all, because it has been internalised in a broker’s dark pool, perhaps not at the best price, or it hits the smart order, but with some order preferences added by the sell-side,” he says. In 2011, Puhakka joined forces with agency-broker ITG to develop and launch a new buy-side con-trolled smart routing and algorithmic trading service. can efficiently access the right

kind of aggregated liquidity. Undue market impact, he adds, can be mitigated by algorithms with size discov-ery functionality.

Gronow concurs with Wald on the convergence of lit and dark liquidity. “Dark pool activity doesn’t appear to have increased greatly, perhaps due to periods of high volatility, but it may also be a factor of some dark venues appearing more like lit venues, where apart from a small spread capture there appears to be little gained in terms of sig-nificant liquidity capture per fill,” he explains. “The key debate going forward on this topic will be the organised trading facility category under MiFID II and how those venues will operate”. (See p15)

Competing for liquidity

Fragmentation, lower vol-umes and rising competition for liquidity from high-fre-quency trading firms have made access to the right kind of liquidity a funda-mental buy-side concern in recent years. As well as prompting an increase in the use of opportunistic algos, this has made effective smart order routing crucial to achieving best execution.

n

“Demand for algorithms working in specific ways for specific investment flows has been growing.”98 nthetrade nissue 31 njan-mar 2012

Market feedback

n

The 2012 Algorithmic Trading Survey

demanded algos customised to particular styles of trad-ing, for example different tactics for trading large- and small-cap names. “Today, with more intelligent, adap-tive algos, those customisa-tion requirements are gener-ally becoming tweaks,” he says. “This is because adap-tive algos offer a much high-er degree of intelligence, using statistics to under-stand what type of stock it is trading (spreads, volatility, liquidity, etc) and adapting tactics accordingly as well as rapidly identifying market trends through greater use of quantitative signals, and responding appropriately to changes in the market. In

Adapting to circumstances

In keeping with heightened buy-side comparison and analysis of sell-side algo-rithmic trading offerings, 2011 witnessed a growth in consultative working part-nerships to devise tools that suit buy-side desired bench-marks and which are designed to fit the specific alpha profiles of particular types of buy-side partici-pants and overcome liquidi-ty constraints. Based on a high degree of input from users, algo customisation now takes many forms.

In Schwieger’s experi-ence, the buy-side has gener-ally moved on from 12 to 18 months ago, when they

this way, adaptive strategies are adding value to traders by improving trading and reducing the number of algos a trader needs on his or her desktop.”

Puhakka notes, however, that while brokers are increasingly willing to tai-lor trades to meet client needs, a certain opacity may remain in how an order passes through the sell-side’s trading infra-structure. “It’s not about customising algos anymore it’s about customising the liquidity,” he says.

Nevertheless, closer cooperation in pursuit of best execution is apparent in many quarters, with Gronow observing that internal analysis at PGI has demonstrated quantifiable benefits from using algo providers “that can adapt to our trading style”.

Following on from a period of “algo overload” on the buy-side, Wald remarks on a shift in client engage-ment in the developengage-ment and operation of algorith-mic trading strategies and solutions. “It’s a great change and a great dialogue,” he says. “Sharing has become an ingrained part of our modern culture and there is a lot more transparency and sharing of information in

n

“We’ve relied a lot less on scheduling strategies and biased our activity to opportunistic liquidity-seeking strategies and focused on minimising signalling risk.”Huw Gronow, director of European equity trading and investment operations, Principal Global Investors

nthetrade nissue 31 njan-mar 2012 99

Market feedback

n

The 2012 Algorithmic Trading Survey

the lessons learned develop-ing algos for blue-chip stocks to other parts of the market that could yield even more value for inves-tors. “The trend is towards more illiquid stocks in the small- and mid-cap arena, where spreads and depth of book are smaller you natu-rally have more inherent signalling risk. You’re look-ing for the same level of sophistication and efficacy for small- and mid-cap stocks as for large-cap stocks. We see greater demand evolving for algos to execute portfolio baskets, pairs trading and ‘sector switch’ algos to enhance the alpha capture of these algo strategies and bring them in-house,” he said.

At BAML, Schwieger sees algos used by institutional investors becoming more able to interpret a wider range of information, fur-ther improving their ability to ‘think on their feet’. For some time prop traders have used economic data and other news as prompts for trades, but it may not be long before investors also leverage such technologies. “I predict a greater prolifer-ation of these more intelli-gent ‘next generation’ adap-tive algo strategies and a greater reliance on the terms of how the markets

are evolving and hopefully that will lead to better trad-ing and execution decisions being made faster.”

Beyond 2012

For the past 12 months, the evolution of algorithmic trading has been propelled by a more intensive role for the buy-side in the develop-ment and execution of algo-rithmic trading strategies, competition for liquidity and retention of alpha in an unpredictable trading cli-mate. With prevailing mar-ket conditions unlikely to change significantly, these factors are likely to drive algo innovation in 2012 and beyond, with algorithms digesting and responding to more data dynamically, then adjusting tactics on the fly. Our algo sages suggest expect to see progress on a number of fronts.

“The new frontier for execution algos is clearly going to be signal-based algos; I think that is abso-lutely how this market is going to evolve. The perfor-mance of signal-based algos in delivering size discovery is going to be incredibly well received and incredibly effec-tive,” says Wald.

For Gronow, the empha-sis should be on extending

Market feedback

n

The 2012 Algorithmic Trading Survey

market signals which feed them,” says Schwieger. “For example, I would expect to see signals which use digit-ised news feeds and ‘read’ market news to be used more widely in the near future.”

If the buy-side found its voice in 2011, it may begin to test the boundaries of its influence in 2012. Puhakka looks towards a stronger buy-side participation in the development of new prod-ucts and market initiatives building on tangible steps towards buy-side independ-ence in the form of more consultation with exchang-es, buy-side steering com-mittees and information sharing, and increased use of buy-side designed and controlled trading services.

Higgins agrees that buy-side influence will only grow in the medium term, but some will have more say than others. “Buy-side independence will continue to grow but will be limited to firms who are able to invest the time and resourc-es to make that happen,” he says. “Overall we will con-tinue to see buy-side traders taking a much greater involvement in the use of analysis to aid algorithm selection, algorithm design and venue selection.” n