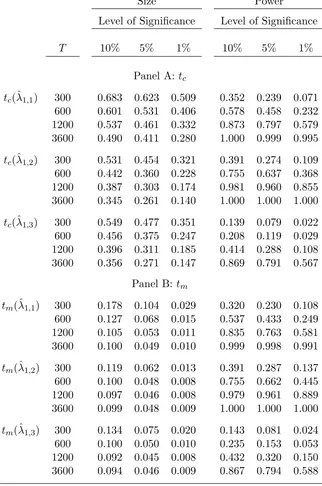

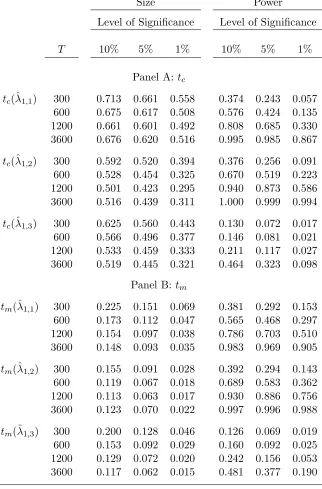

Asymptotic variance approximations for invariant estimators in uncertain asset pricing models

Full text

Figure

Related documents

• FlashCopy to a target (copy pool backup storage group) that is also a PPRC Primary volume sets the secondary volume “duplex pending”. • Secondary site

Such a collegiate cul- ture, like honors cultures everywhere, is best achieved by open and trusting relationships of the students with each other and the instructor, discussions

its wasting time to teaching English when the exam will come in Arabic wasting our time...when I speak in English , student say miss I take the test in Arabic why you

The American legal system offered feminists particular avenues for social change. For instance, in the U.S., judicial precedent has the power of law and American legal rules permit

As highlighted by the present study, the matter of more urgency now is indeed to prioritise doing over knowing as the government (and other actors such as NGO, CSO, donor

The overview of the Italian Health system, described by the data of the Observatory Health Report, shows that the health status of Italian people is good

Instead of using a single thread, multiple threads are used in the data transportation from server to client for some large tables. The initialization time has been

On June 24, 2009, the Senate of WU Vienna University of Economics and Business approved the following resolution of the Committee for Academic Programs dated June