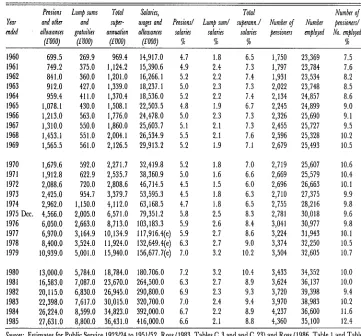

Irish Civil Service Superannuation Scheme

Full text

Figure

Related documents

The assets of the newly-formed company will comprise The Carphone Warehouse’s existing retail business, operating from more than 2,400 stores in nine European

Our results showed a marked increase in c‑fos activity in these amygdala subnuclei both ipsilateral and contralateral to LC electrical stimulation in vivo.. Therefore, our study

In the second step respondents were asked to rank their preferences on a scale ,5 point scale ranging from Highly Important (5) to Not at all Important (1). Using Principal

At the larger urban scale, the chapter investigates the effects of green on heat island mitigation and on the energy demand for cooling, demonstrating the paramount additional

Twenty-two studies (42 %) demonstrated negative effects of habitat conversion, twelve (23 %) showed varia- ble responses (e.g., only some species or ensembles declined,

income mobility reduces inequality in lifetime income by about 25 percent, while heterogeneous (but non-intersecting) age–income profiles contributes to upward (downward)

The study reported in this research brief examined the extent to which organized and unstructured outdoor activity involvement during adolescence predicted postsecondary

When compared with the existing studies in the literature, the key contribution of the proposed work is the development of the first–ever controller that addressed robust control