Qualified Clearing Staff

Preparation Material for the Clearer Test

Market Module Securities Lending

Eurex Clearing AG

Clearstream, Eurex, Eurex Clearing, Eurex Bonds, Eurex Repo as well as the Eurex Exchanges and their respective servants and agents (a) do not make any representations or warranties regarding the information contained herein, whether express or implied, including without limitation any implied warranty of merchantability or fitness for a particular purpose or any warranty with respect to the accuracy, correctness, quality, completeness or timeliness of such information, and (b) shall not be responsible or liable for any third party’s use of any information contained herein under any circumstances, including, without limitation, in connection with actual trading or otherwise or for any errors or omissions contained in this publication.

This publication is published for information purposes only and shall not constitute investment advice respectively does not constitute an offer, solicitation or recommendation to acquire or dispose of any investment or to engage in any other transaction. This publication is not intended for solicitation purposes but only for use as general information. All descriptions, examples and calculations contained in this publication are for illustrative purposes only.

Eurex and Eurex Clearing offer services directly to members of the Eurex exchanges respectively to clearing members of Eurex Clearing. Those who desire to trade any products available on the Eurex market or who desire to offer and sell any such products to others or who desire to possess a clearing license of Eurex Clearing in order to participate in the clearing process provided by Eurex Clearing, should consider legal and regulatory requirements of those jurisdictions relevant to them, as well as the risks associated with such products, before doing so.

Eurex derivatives are currently not available for offer, sale or trading in the United States or by United States persons (other than EURO STOXX 50® Index Futures, EURO STOXX® Select Dividend 30 Index Futures, EURO STOXX® Index Futures, EURO STOXX® Large/Mid/Small Index Futures, STOXX® Europe 50 Index Futures, STOXX® Europe 600 Index Futures, STOXX® Europe 600 Banks/Industrial Goods & Services/Insurance/Media/Travel & Leisure/Utilities Futures, STOXX® Europe

Large/Mid/Small 200 Index Futures, Dow Jones Global Titans 50 IndexSM Futures (EUR & USD), DAX®/MDAX®/TecDAX® Futures, SMIM® Futures, SLI Swiss Leader Index® Futures as well as Eurex inflation/commodity/weather/property and interest rate derivatives).

Trademarks and Service Marks

Buxl®, DAX®, DivDAX®, eb.rexx®, Eurex®, Eurex Bonds®, Eurex Repo®, Eurex Strategy WizardSM, Euro GC Pooling®, FDAX®, FWB®, GC Pooling®,,GCPI®, MDAX®, ODAX®, SDAX®, TecDAX®, USD GC Pooling®, VDAX®, VDAX-NEW® and Xetra® are registered trademarks of DBAG.

Phelix Base® and Phelix Peak® are registered trademarks of European Energy Exchange AG (EEX). The service marks MSCI Russia and MSCI Japan are the exclusive property of MSCI Barra. RDX® is a registered trademark of Vienna Stock Exchange AG.

IPD UK Annual All Property Index is a registered trademark of Investment Property Databank Ltd. IPD and has been licensed for the use by Eurex for derivatives.

SLI®, SMI® and SMIM® are registered trademarks of SIX Swiss Exchange AG.

The STOXX® indexes, the data included therein and the trademarks used in the index names are the intellectual property of STOXX Limited and/or its licensors Eurex derivatives based on the STOXX® indexes are in no way sponsored, endorsed, sold or promoted by STOXX and its licensors and neither STOXX nor its licensors shall have any liability with respect thereto.

Dow Jones, Dow Jones Global Titans 50 IndexSM and Dow Jones Sector Titans IndexesSM are service marks of Dow Jones & Company, Inc. Dow Jones-UBS Commodity IndexSM and any related sub-indexes are service marks of Dow Jones & Company, Inc. and UBS AG. All derivatives based on these indexes are not sponsored, endorsed, sold or promoted by Dow Jones & Company, Inc. or UBS AG, and neither party makes any representation regarding the advisability of trading or of investing in such products.

All references to London Gold and Silver Fixing prices are used with the permission of The London Gold Market Fixing Limited as well as The London Silver Market Fixing Limited, which for the avoidance of doubt has no involvement with and accepts no responsibility whatsoever for the underlying product to which the Fixing prices may be referenced.

PCS® and Property Claim Services® are registered trademarks of ISO Services, Inc.

Korea Exchange, KRX, KOSPI and KOSPI 200 are registered trademarks of Korea Exchange Inc.

BSE and SENSEX are trademarks/service marks of Bombay Stock Exchange (BSE) and all rights accruing from the same, statutory or otherwise, wholly vest with BSE. Any violation of the above would constitute an offence under the laws of India and international treaties governing the same.

Table of Contents

Table of Contents 3

Amendments to Preparation Material for the Clearer Test 5

Abbreviations and Glossary of Terms 6

1 Introduction 10

1.1 Structure of the test, question types and evaluation 10

1.2 Contact/Registration 11

2 Introduction to Securities Lending Transactions 12

2.1 Loan Instruments and Flow Providers 14

2.2 Participation and Responsibilities 15

2.3 Trade Capture and Novation 17

2.4 Loan Transaction Types 18

2.4.1 Loan versus Cash Principal Collateral, Loan versus Cash Pool 19 2.4.2 (Financing) Loan versus Non-cash Principal Collateral 19

2.5 Sample Questions 21

3 Clearing Conditions 22

3.1 General Provisions 22

3.2 Clearing License 22

3.2.1 Granting of the Clearing License 22

3.2.2 Prerequisites of Clearing Licenses 23

3.2.3 Prerequisites for granting a Specific Lender License 23

3.3 Conclusion of Transactions 24

3.3.1 Novation 24

3.3.2 Novation Principles and Criteria, Cancellations 25

3.4 Margin Requirement 25

3.5 Sample Questions 26

4 Loan Lifecycle Management 27

4.1 Loan Opening 30

4.1.1 Collection and Distribution Phase 30

4.1.2 Exceptional Processing 30

4.2 Back-loading of Loans 31

4.3 Loan Cancellation 31

4.4 Allocation View versus Street View 32

4.5 Loan Management 32

4.6 Return of an Open-Term Loan 33

4.6.1 Standard Return Processing 33

4.6.2.1 Late Delivery of Loan Securities during Return Processing 34 4.6.2.2 Late Delivery of Cash Principal Collateral during Return Processing 34 4.6.2.3 Late Delivery of Non-cash Principal Collateral during Return Processing 34 4.6.2.4 Forced return of loans at fixed income loan security maturity 35

4.7 Return of a Fixed-Term Loan 35

4.7.1 Standard Return Processing 36

4.7.1.1 Collection and Distribution Phase 36

4.7.2 Exceptional Return Processing 36

4.8 Recall of a Loan 37

4.8.1 Standard Recall Processing 38

4.8.2 Exceptional Recall Processing 39

4.9 Buy-in Processing 39

4.9.1 Forced Returns 39

4.9.2 Buy-in Auction 40

4.10 Re-rate of a Loan 40

4.11 Return Do Not Instruct Request 40

4.12 Lending Fees and Rebates 41

4.13 Reports 43

4.14 Sample Questions 44

5 Delivery Management 46

5.1 Home Market Settlement for Equity Loan Securities 46 5.2 International Market Settlement for Fixed Income Loan Securities 46 5.3 Bridge Settlement for Fixed Income Loan Securities 46

5.4 Corporate Action Handling on loan securities 47

5.4.1 Business Context in the CCP model 47

5.5 Sample Questions 49

6 Risk Management 50

6.1 Principal Exposure and Principal Collateral 50

6.1.1 Mark-to-Market Calculation 50

6.1.2 Handling of Cash Principal Collateral 51

6.1.3 Handling of Non-cash Principal Collateral 51

6.2 Additional Exposure and Margin Collateral 52

6.2.1 Impact of the End-of-Day Mark-to-Market Process 53

Amendments to Preparation Material for the Clearer Test

Date New Version Chapter Changes July 2015 2.0 2, 3 and 4 5 and 6Financing loans (EUR, USD) added revised

Abbreviations and Glossary of Terms

Term Description

Agent Lender (AL)

Service Provider.The Agent Lender (AL) acts as agent in the loan transaction for Beneficial Owners using a Specific Lender License or for Beneficial Owners with a full Clearing Membership.

Allocation View

In case an agent lender acts as account operator for multiple Beneficial Owners each using a dedicated Specific Lender License, individual loan transactions are required from the Agent Lender. This view is called “allocation view”.

Back-loaded loans

An existing portfolio of loan transactions can be ‘back-loaded’ into the CCP system, i.e. handed over to Eurex Clearing for further processing after settlement of the front leg has already taken place outside Eurex Clearing

Beneficial Owner

Lender of loan assets using a Specific Lender License or a full Clearing

Membership. The Beneficial Owner is the “economic” owner of the loan securities, and as such, entitled to the proceeds of the Corporate Action.

Borrower

Market participant in a securities lending transaction who borrows securities for some time from a lender, covering its value with Principal Collateral, and returning the securities at the end of the transaction

Broker Dealer Usually a Borrower acting on behalf of a hedge fund

BYI Buy-in request

CBF Clearstream Banking Frankfurt, a CSD CBF(I) Clearstream Banking International, an (I)CSD

CBL Clearstream Banking Luxembourg, ICSD and TPCA

CCP Central Counterparty

CET Central European Time

CHF Currency Swiss Franc

CM Borrower Clearing Member acting as Borrower CM Lender Clearing Member acting as Lender

CNC Cancel request

Collateral Principal Collateral and Margin Collateral Contractual

settlement date Settlement date initially agreed by the Borrower and Lender CSD Central Securities Depository

DvP Delivery versus Payment

Term Description

EoD End of day: In the context of reporting also referring to a group of reports created at the end of the day

EoM End of month

EONIA Euro Over Night Index Average, a benchmark used for rebate calculation

EUR Currency Euro

Eurex Repo-SecLend Market

A securities lending trading market, also acting as TPFP

ESES Euroclear Settlement for Euronext-zone Securities

ETF Exchange Traded Fund

EURIBOR Euro Interbank Offered Rate, a benchmark used for rebate calculation

Financing loan

Specific type of loan where the Lender provides cash (in EUR or USD) to the Borrower versus non-cash Principal Collateral which will always be pledged to the Lender. Financing loan can be of type Fixed-Term only.

Fixed-Term loan Loan with a defined contractual settlement date of the term leg FoP (delivery) Free of Payment

Front leg Exchange of loan assets against Principal Collateral at loan opening.

FX Foreign currency exchange

HMRC Her Majesty's Revenue and Customs (HMRC), a non-ministerial department of the UK Government responsible for the collection of taxes

ICSD International Central Securities Depository ISIN International Securities Identification Number

Lender

Market participant in a securities lending transaction who lends securities for some time to a borrower, receiving Principal Collateral as coverage, receiving the lent securities back at the end of the transaction

Loan assets Loaned Securities or Loaned Cash in Securities Lending Transactions, together referred to as the “Loaned Assets

Margin Collateral Deposit covering the margin requirement of Eurex Clearing

Margin Markup Markup used to calculate the amount which serves as the basis for lending fee calculation (Fee Margin)

MtM Mark-to-Market, calculation of updating the collateral value to current market value for risk management

Novation Process during loan opening when Eurex Clearing legally steps in as counterparty between Lender and Borrower

Term Description Open Securities

Lending Transaction

Securities Lending Transaction after successful settlement of the front leg (opening) and before its closure (return)

Open-Term loan Contrary to a Fixed-Term loan, an Open-Term loan has no specified settlement date for the term leg

OTC Over-the-Counter

Pending Securities Lending

Transaction

Securities Lending Transaction received by Eurex Clearing and waiting (pending) for settlement of the front leg

Pirum Pirum Systems Limited; Reconciliation platform for lending transactions. See also TPFP

PoA Power of Attorney

Principal Collateral Deposit covering the market value of the loan securities

REC Recall request

RET Return request

RNI Return Do Not Instruct Request

RRT Re-rate request

RTS Real Time Settlement

S Settlement Date

SDS Same Day Settlement

Settlement Date Front Leg

The date, when the loan is opened

Settlement Date Term Leg

The date, when the loan is terminated (and returned)

SIX SIS The national Central Securities Depository (CSD) of the Swiss financial market and also an International Central Securities Depository (ICSD),

SLL

Specific Lending License:

Specific Clearing Membership for the SecLending market. SLL holder is allowed to clear his own lending transactions only (CM limited to lending transactions). Street View During bilateral negotiation Agent Lender and Broker Dealer agree on one loan

comprising the total quantity. This view is called “street view”. SWIFT Society for Worldwide Interbank Financial Telecommunication

T Trading (date), used in schedule calculations to refer to the trading date of the loan Term leg Exchange back of loan assets against Principal Collateral at loan closing.

Term Description

TPFP

Third Party Flow Provider. Provide an interface between Eurex Clearing and securities lending participants. All transactions to Eurex Clearing pass through a TPFP

TPCA Tri-party Collateral Agent, provider of services for collateral management

USD Currency US Dollar

VBK

Voluntary back-load request (The counterparties can send a back-load instruction in the case of an agreement to keep the loan open without redelivery of the underlying loan securities of the existing loan.

1 Introduction

The handbook was developed to help you to prepare for the Clearer Test Market Module Securities Lending.

The handbook summarizes the relevant contents from different sources covered in this test. It describes the different services of the clearing process and is complemented with sample questions for the test. The sources of information for specific topics as well as the preparation material for the Clearer Test Basic Module are referenced where relevant to provide the reader with access to more detailed information which may be of interest, but is not required for this test. The current version can be downloaded via : www.deutsche-boerse.com/qcs_qbo

Please note that there will be regular updates.

1.1 Structure of the test, question types and evaluation

The Clearer Test Market Module Secutities Lending is carried out using a computer program, which randomly selects 20 questions from a question pool for each examination candidate. The test can be taken in English and German.

There are three different types of questions:

• True/False (TF) 2 point

• Multiple choice (MC) 2 points

• Multiple response (MR) 4 points

MC/MR questions which are not answered will consequently not be assessed (0 points).

In case of MR, either one or several answers could be correct and must be marked to get the full number of points.

The following evaluation method is used:

• for marking the correct answer and not marking the wrong answer one point is given

• for marking the wrong answer and not marking the correct answer one point is subtracted So the result could be 4, 2 or 0 points; a negative score will not be given.

The following table provides an overview of the number and types of questions to be selected for each topic:

No. Topic TF MC MR No. of

questions

1.0 Product Overview 1 1 1 3

2.0 Clearing Conditions 1 1 - 2

3.0 Loan Lifecycle Management 3 1 3 7

4.0 Delivery Management 1 - 1 2

5.0 Risk and Collateral Management 2 3 1 6

Total 8 6 6 20

Participants need 75% of the maximum points to pass the test and have 20 minutes to complete the test.

1.2 Contact/Registration

We would like to point out that according to the Clearing Conditions for Eurex Clearing AG (“Clearing Conditions”) each Clearing Member must have at least one Qualified Clearing Staff (QCS). This QCS must have passed the Clearer Test consisting of two modules: the Basic Module and a market module for the particular Clearing License.

Dates (individual online exam is also possible ) and information about the Clearer Test modules can be found under the following link: www.deutsche-boerse.com/qcs_qbo

For further information please contact the Capital Markets Academy: Capital Markets Academy of Deutsche Börse Group

Phone: +49 69 211 13767 Fax: +49 69 211 13763

Homepage: http:// deutsche-boerse.com/cma E-Mail: [email protected]

To register as a QCS please use the Electronic Exchange Admission Service (eXas). eXas can be found in the member section on the website of Eurex Clearing or under the following link:

www.member.eurexclearing.com

For questions about access to the Member Section of Eurex Clearing, please contact the Member Section Team at +49-(0) 69-2 11-1 78 88 or by e-mail to [email protected].

For any questions regarding the features of eXAS, please call the following Member Services & Admission teams:

Location Phone E-Mail

Zurich +41-(0) 58-8 54-29 42 [email protected] Paris +33 (0) 155- 27-67 67 [email protected] London +44 (0) 207-8 62-71 65 [email protected] Chicago +1-312-5 44-11 50 [email protected] Frankfurt +49 (0) 69-2 11-1 16 40 [email protected]

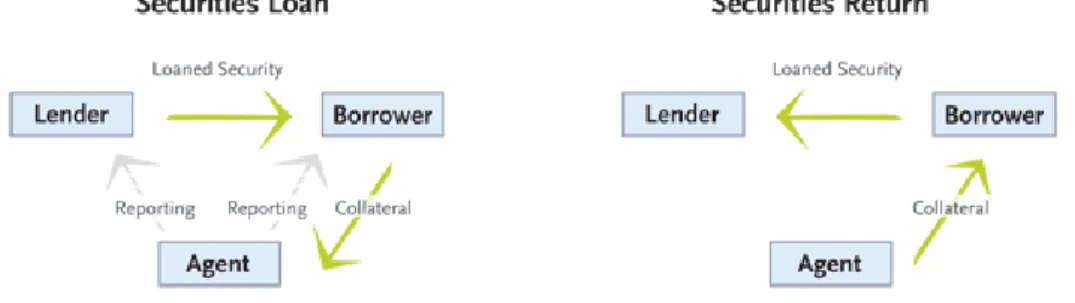

2 Introduction to Securities Lending Transactions

A securities lending transaction in the bilateral market is an agreement between a lender and a borrower to transfer securities on a collateralised basis. A loan transaction consists of

• the opening (front leg):

the exchange of the securities from the lender to the borrower and the exchange of collateral from the borrower to the lender

• the closing (term leg):

the re-exchange of the securities back from the borrower to the lender and the re-exchange of the collateral back from the lender to the borrower

Collateral could be in the form of cash or non-cash.

Securities lending transactions may either be Open Term Loans or Fixed Term Loans. In case of Open Term Loans the lender and borrower have not agreed on a fixed redemption date at contract conclusion. In case of Fixed Term Loans the redemption is made on a specifically agreed maturity date, if not the lender and borrower agree later on a date prior to the originally agreed maturity date.

Investors make short-term loans of their securities while receiving a fee for the use of their securities to generate extra revenues from their portfolios or offsetting expenses while managing the portfolio. Lenders are normally holders of portfolios i.e. mutual funds, insurance companies, endowments or corporate and government pension funds.

Borrowers are the prime brokerage units, the proprietary trading desks of broker/dealers or global banks or hedge funds which are using the securities lending markets to support their trading activities like short selling, hedging, arbitrage trading, trading cross-border strategies or meeting settlement obligations. Custodial agent lenders, third-party agent lenders or broker/dealers acting as principal borrowers (exclusive principal deal) are taking the role of facilitators.

A basic bilateral securities lending transaction is shown in the diagram where cash is the accepted collateral and the collateral is re-invested into a short-term money market investment vehicle. The beneficial owner of the assets will lend the securities to the borrower. The borrower has to provide

collateral in an amount equal to the market value of the securities plus additional margin of 102% to 105%.

The securities lending marketplace has been traditionally a relationship-based business. The offering of Eurex Clearing for the bilateral market maintains this key feature. The interposition of the CCP takes place after the negotiation of the loan which still remains bilateral. A CCP in the securities lending and borrowing market minimizes the counterparty risk and the credit exposures for the participants as well as bringing a considerable reduction in systemic risk for the market in its entirety. Eurex Clearing’s CCP model reduces the potential secondary effects of the failure of a major counterparty because the impact is mitigated and absorbed by Eurex Clearing’s default protections.

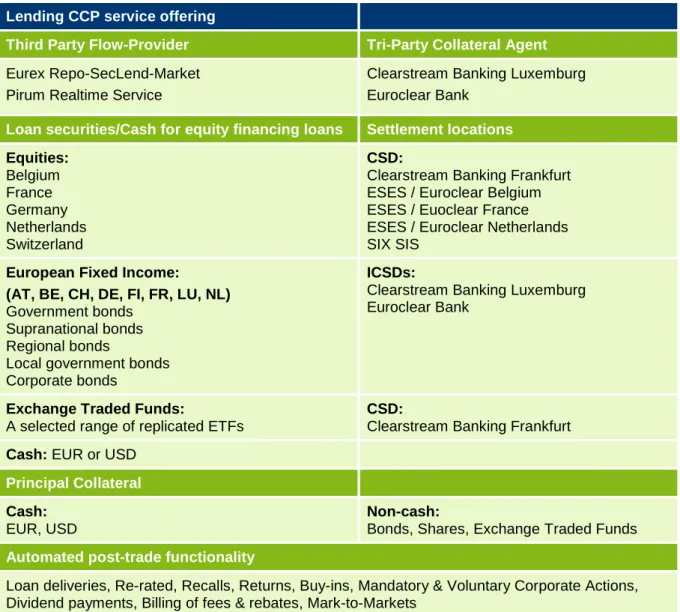

2.1 Loan Instruments and Flow Providers

For the CCP Lending service Eurex Clearing offers central clearing for securities1 or cash lending transactionsand novates loan transactions from the counterparties that reach Eurex Clearing through the following Third Party Flow Providers (TPFP):

Lending CCP service offering

Third Party Flow-Provider Tri-Party Collateral Agent Eurex Repo-SecLend-Market

Pirum Realtime Service

Clearstream Banking Luxemburg Euroclear Bank

Loan securities/Cash for equity financing loans Settlement locations Equities: Belgium France Germany Netherlands Switzerland CSD:

Clearstream Banking Frankfurt ESES / Euroclear Belgium ESES / Euoclear France ESES / Euroclear Netherlands SIX SIS

European Fixed Income:

(AT, BE, CH, DE, FI, FR, LU, NL) Government bonds

Supranational bonds Regional bonds

Local government bonds Corporate bonds

ICSDs:

Clearstream Banking Luxemburg Euroclear Bank

Exchange Traded Funds:

A selected range of replicated ETFs

CSD:

Clearstream Banking Frankfurt Cash: EUR or USD

Principal Collateral Cash:

EUR, USD

Non-cash:

Bonds, Shares, Exchange Traded Funds Automated post-trade functionality

Loan deliveries, Re-rated, Recalls, Returns, Buy-ins, Mandatory & Voluntary Corporate Actions, Dividend payments, Billing of fees & rebates, Mark-to-Markets

Figure 2-2: Lending CCP service offering as of Q2 2015

2.2 Participation and Responsibilities

A clearing license is required in order to participate as a Clearing Member (CM) in the Lending CCP of Eurex Clearing. The license can be combined with other clearing licenses, for which Eurex Clearing is offering CCP services. Market participants owning a clearing license for the Lending CCP are also referred to as CM Lender and CM Borrower in this document.

In order to reflect the specific structure of the securities lending market, Eurex Clearing offers various CM license types to participate in the Lending CCP. The participants can apply for a General Clearing Member (GCM), a Direct Clearing Member (DCM) and a Specific Lender License (SLL).

• A Clearing Member (DCM/GCM) is allowed to clear its own transactions (borrow and/or lend).

• A SLL holder (also called Beneficial Owner) is allowed to clear its own lending transactions only (CM limited to lending transactions).

The detailed requirements for the Clearing Memberships are described in chapter 3.

Eurex Clearing’s CCP system interacts directly with Third Party Flow Providers (TPFP), Clearing Members (CM), (I)CSDs, Payment Locations, and Tri-party Collateral Agents (TPCA).

Basically, their responsibilities with the CCP Service for Securities Lending are:

Party Responsibility Clearing

Member

Fulfill operational and technical requirements

Bilateral loan negotiation and provision of loan requests to TPFP Provide / return Principal Collateral and loan securities

Provide Margin Collateral (when applicable) Receive member reports

Third Party Flow Provider (TPFP)

Collect loan requests from connected agents / brokers Reconcile requests of lender and borrower / match requests Perform validations

Party Responsibility Eurex

Clearing / CCP

Provision of member and static data to facilitate TPFP’s validations Receive requests from the TPFPs

Perform validations

Novate loans, become central counterparty

Process requests on the loans during their lifetime (Re-rates, Recalls, Returns, Buy-ins)

Instruct (I)CSDs, TPCAs, payment locations during settlement Mark-to-market of Principal Collateral

Close loans, including late delivery handling, Buy-in processing Processing of Corporate Actions (on loan securities only) Handle compensation for Corporate Actions proceeds Calculate and instruct lending fees and rebates Calculate and instruct clearing fees and fines Provide reports

Perform risk management (I)CSDs Perform securities settlements Payment

Locations

Perform cash payments

Tri-party Collateral Agent

Perform collateral management for non-cash collateral, including reporting

Eurex Clearing has introduced an Agent Lender role for the Lending CCP. Based on this, the Agent Lender can interact in the following ways in the clearing services.

The Agent Lender (AL) acts as agent in the loan transaction for Beneficial Owners using a Specific Lender License (SLL) or for Beneficial Owners with a full Clearing Membership.

The AL may only support a SLL Holder/CMs performing loans vs. non-cash Principle Collateral (pledged). AL need a Power of Attorney from the SLL Holder/CM so that they can act on behalf of the SLL Holder/CM. This way, the Beneficial Owners can remain principal as they have a direct relationship as restricted Clearing Member with Eurex Clearing and the Agent Lender remains as account operator acting in its current agency role.

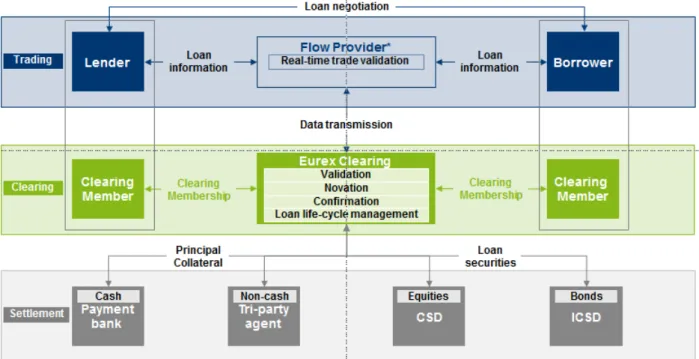

2.3 Trade Capture and Novation

Lender and Borrower bilaterally agree on the terms and condition of a loan. Lender and Borrower provide the agreed loan details via their common Third Party Flow Provider (TPFP). The Third Party Flow Provider reconciles/matches both entries and forwards the loan transaction details to Eurex Clearing`s CCP system.

* Flow Provider used as the entry channel from market participants to Eurex Clearing e.g. for new loan transactions, Re-rates, Recalls, Returns etc.

Figure 2-3: Process Overview

Although trading remains bilateral, on the clearing side Eurex Clearing novates the loan trade and becomes counterparty to the Clearing Members on the borrowing and the lending side, see chapter 3.3.1 Novation. Third Party Flow Provider and related Clearing Members are informed about the novation or the rejection of their transaction. Eurex Clearing then coordinates the stepwise exchange of loan securities versus

Principal Collateral with (I)CSDs, payment locations, and Tri-party Collateral Agents (TPCA).

In case of non-cash Principal Collateral Lender and Borrower have to agree to use the same Tri-party Collateral Agent, either Clearstream Banking Luxembourg (CBL) or Euroclear Bank (EB).

The following picture shows the more specific case where an Agent Lender acts as an agent for a beneficial owner holding a Specific Lending License on the lending side and a Broker Dealer enters the loan information on the borrowing side.

Figure 2-4: Process Overview including Agent Lenders and Broker Dealers

2.4 Loan Transaction Types

In order to mitigate the counterparty risk in the securities lending market, the loan is alwaystransacted against loan collateral (called Principal Collateral). Eurex Clearing supports the following loan types for the Lending CCP:

• Loans versus Cash Principal Collateral: Type of loan where the Lender provides securities to the Borrower in exchange of cash Principal Collateral which will be transferred to the Lender. Loans versus cash Principal Collateral can be of type Open-Term only.

• Loans versus Non-Cash Principal Collateral: Type of loan where the Lender provides securities to the Borrower in exchange of non-cash Principal Collateral which can be pledged or transferred to the Lender. Loans versus non-cash Principal Collateral can be of type Open-Term and Fixed-Term. In case of Fixed-Term non-cash Principal Collateral is always pledged to the Lender.

• Loans versus Cash Pool: Specific type of loan versus cash Principal Collateral where the Lender and Borrower need to agree on a lending fee for the loan security leg and separately a rebate for the cash (pool) collateral leg. Loans versus cash pool can be of type Open-Term only.

• Financing Loans: Specific type of loan where the Lender provides cash (in EUR or USD) to the Borrower versus non-cash Principal Collateral which will always be pledged to the Lender. Financing loan can be of type Fixed-Term only.

The term collateral in the context of a CCP is predefined and is linked to the risk management and margining process of the Clearing House, see chapter 6. In order to avoid ambiguity, the loan collateral is called Principal Collateral and the collateral used to cover exposures vis-à-vis the Clearing House (margin requirements) is called Margin Collateral.

2.4.1 Loan versus Cash Principal Collateral, Loan versus Cash Pool

For loans versus cash Principal Collateral the Principal Collateral will always be transferred via Eurex Clearing to the CM Lender. As the CM Borrower has the obligation to re-deliver the loan securities to Eurex Clearing and the CM Lender (with the transfer of title as a collateral option) has the obligation to re-deliver the cash Principal Collateral, they both have to provide margin to Eurex Clearing.

For Specific Lenders loan versus cash Principal Collateral is not offered by Eurex Clearing.

Figure 2-4: Loan versus Cash Principal Collateral and versus Cash Pool

2.4.2 (Financing) Loan versus Non-cash Principal Collateral

For loans versus non-cash Principal Collateral where the Principal Collateral is transferred by way of title transfer to the CM Lender CM Lender and CM Borrower have to provide margin (Margin Collateral) to Eurex Clearing, see chapter 6 and 6.1.3.

Figure 2-5: Loan versus Non-cash Principal Collateral - Transferred

Transfer of Title Pledge Eurex Clearing Clearing Member Lender Clearing Member Borrower

Non-Cash Principal Collateral

Loan Securities

Margin Collateral Non-Cash Principal Collateral Loan Securities Margin Collateral Transfer of Title Pledge Eurex Clearing Clearing Member Lender Clearing Member Borrower

Cash Principal Collateral

Loan Securities

Margin Collateral Cash Principal Collateral Loan Securities

If the Principal Collateral is pledged in favour of the CM Lender the CM Lender does not have to provide margin to Eurex Clearing. A holder of a Specific Lender License is therefore only allowed to transact loans versus non-cash Principal Collateral - pledged with Eurex Clearing. For Financing Loans the non-cash Principal Collateral must always be pledged to the CM Lender.

Figure 2-6: Loan versus Non-cash Principal Collateral - Pledged

Non-cash Principal Collateral is managed by Tri-party Collateral Agents Clearstream Banking Luxembourg and Euroclear Bank. CM Lender and CM Borrower have to agree to use the same Tri-party Collateral Agent, either Clearstream Banking Luxembourg (CBL) or Euroclear Bank (EB).

2.5 Sample Questions

2-001

Eurex Clearing`s CCP service reduces … A: the credit exposures.

B: counterparty risks. C: post-trade-complexity. D: portfolio activity. Correct answer: A|B|C

2-002

With Eurex Clearing`s CCP services no bilateral agreements between lenders and borrowers on the terms and conditions of a loan are possible.

True False Correct answer: False

2-003

Eurex Clearing coordinates… A: calculations of lending fees.

B: the step-wise exchange of loan securities versus Principal Collateral with (I)CSDs. C: the payment locations.

D: the forwarding of loan requests to Eurex Clearing`s CCP system. Correct answer: A|B|C

3 Clearing Conditions

3.1 General Provisions

Eurex Clearing offers the Clearing of securities or cash lending transactions (each a “Securities Lending Transaction”) in accordance with the prerequisites and conditions pursuant to Chapter IX of the Clearing Conditions.

Under a Securities Lending Transaction, one party (the “Lender”) will transfer to the other party (the “Borrower”) either a specified number of a specific financial instrument (the “Loaned Securities”), or a specified amount of a specific currency (the “Loaned Cash” - the Loaned Securities together with the Loaned Cash are referred to as the “Loaned Assets”) with a simultaneous agreement by the Borrower to redeem the Securities Lending Transaction by the transfer to the Lender of Underlying Securities or Underlying Currency equivalent to the Loaned Securities Assets actually delivered (the “Equivalent Loaned Assets”) on a date fixed as maturity and/or on demand at any time before such date, as the case may be. A Securities Lending Transaction where the Loaned Assets are Loaned Securities is herein referred to as a “Securities Loan” and a Securities Lending Transaction where the Loaned Asset is Loaned Cash is herein referred to as a “Financing Loan”.

The terms of the Securities Lending Transactions may either provide for Open Term Loans and Fixed Term Loans. For more information and restrictions please refer to chapter 2.4.

Eurex Clearing acts as Borrower with respect to each CM which is the Lender under a Securities Lending Transaction (the "Lender Clearing Member" – CM Lender) and Eurex Clearing acts as Lender with respect to each CM which is the Borrower under a Securities Lending Transaction (the "Borrower Clearing

Member" – CM Borrower). These Securities Lending Transactions are concluded by way of novation.

3.2 Clearing License

3.2.1 Granting of the Clearing License

A Clearing License is required in order to participate in the Clearing of Securities Lending Transactions, and Eurex Clearing may grant such Clearing License upon written application if the prerequisites are fulfilled. A Clearing License can be restricted to the Clearing of certain classes of Underlying Securities and/or certain Underlying Currencies. The Clearing License entitles the CM to clear Own Transactions as a Borrower or as a Lender.

3.2.2 Prerequisites of Clearing Licenses

Generally the prerequisites to be fulfilled for the granting of the Clearing License are set out in Chapter I, Part I of the Clearing Conditions for Eurex Clearing and can also be found in the Basic Module in chapter 2.3.1. Following additional and/or deviating prerequisites apply for the participation in the Clearing of Securities Lending Transactions.

The applicant shall provide evidence of the compliance with the following requirements:

• Settlement accounts for equities and Exchange Traded Funds (“ETF”) with - Clearstream Banking AG (“CBF”) and/or

- SIX SIS Ltd., Zurich (“SIX SIS”) and/or

- Euroclear France SA, (Euroclear France) and/or

- Caisse Interprofessionnelle de Dépôts et de Virements de Titres SA / Interprofessionnelle Effectendepositen Girokas NV (C.I.K.) (Euroclear Belgium) and/or

- Nederlands Centraal Instituut voor Giraal Effectenverkeer B.V. (NECIGEF) (Euroclear Nederland);

• and/or settlement accounts for fixed income securities with - CBF or

- Clearstream Banking S.A., Luxemburg (“CBL”) or - Euroclear Bank SA/NV

• an additional bank cash account in USD with a bank recognised by Eurex Clearing

• direct access or admission to a Third Party Flow Provider (“TPFP”)

• execution of the specific tripartite documentation, unless the applicant will provide to the Lender Cash Principal Collateral only.

3.2.3 Prerequisites for granting a Specific Lender License

2 Amongst others the following prerequisites have to be fulfilled:• The applicant is licensed as a credit institution, financial institution, insurance undertaking, reinsurance undertaking, investment firm, pension fund, pension scheme or similar arrangement, Incorporated Fund, Unincorporated Fund of Sub Fund and is subject to supervision as determined by Eurex Clearing. (Further details can be found in the Eurex Clearing Conditions).

• The applicant has obtained all necessary approvals that are required to have been obtained by it for the conduct of securities or cash lending business, as relevant, pursuant to the provisions of chapter IX, Clearing Conditions;

• cash accounts pursuant to Chapter I of the Clearing Conditions and a bank cash account in USD with a bank recognised by Eurex Clearing or alternatively a multicurrency cash account with

• Clearstream Banking AG (“CBF”), including a CBF(I) account, and/or

• Clearstream Banking S.A., or

• Euroclear Bank SA/NV;

either accounts opened in the name of the applicant or accounts opened in the name of an Agent Lender for the account of the applicant

• settlement accounts for the loan securities as described in chapter 3.2.2;

22

• direct access to a or admission to a Third Party Flow Provider either by itself or via an Agent Lender

• execution of the specific tripartite documentation for Securities Lending Transactions with Eurex Clearing AG and a Tri-Party Collateral Agent either by itself or by a representative on behalf of the applicant

• access to Eurex Clearing's Common Report Engine (platform to receives reports), unless the applicant will make use of the services of an Agent Lender

The general prerequisites for a Clearing License for the Clearing of Securities Lending Transactions do not apply.

3.3 Conclusion of Transactions

Securities Lending Transactions are concluded by way of novation subject to, and in accordance with, the following provisions:

3.3.1 Novation

Whenever a securities or cash lending transaction (each an "Original Securities Lending Transaction")

• is transmitted to Eurex Clearing by CMs via the TPFP and

• Eurex Clearing accepts such Original Securities Lending Transaction for inclusion in the Clearing, Eurex Clearing will interpose itself by way of novation as central counterparty and the Original Securities Lending Transaction shall be cancelled and replaced by two related Securities Lending Transactions

• between Eurex Clearing AG as the Borrower and the relevant CM as the Lender and

• between Eurex Clearing AG as the Lender and the relevant CM as the Borrower, each in accordance with the Loan Information.

If provided for by the rules of the relevant TPFP, Eurex Clearing may also conduct the novation of

Securities Lending Transactions which have been disbursed and collateralized between the Lender and the Borrower in full or in part prior to the inclusion into the Clearing (the "Settled Original Securities Lending Transactions").

Following the conclusion of Securities Lending Transaction by way of novation Eurex Clearing will on the same Business Day send corresponding confirmations to the CMs. The actual time of conclusion of a Securities Lending Transaction by way of novation is referred to as the "Novation Time".

3.3.2 Novation Principles and Criteria, Cancellations

Original Securities Lending Transactions or Settled Original Securities Lending Transactions have to be transmitted to Eurex Clearing in a standardized form using an established TPFP accepted by Eurex Clearing which will provide information and notices regarding such transactions to Eurex Clearing. Eurex Clearing shall validate any information regarding the Original Securities Lending Transactions or Settled Original Securities Lending Transactions transmitted to it via the TPFP.

Eurex Clearing may reject Original Securities Lending Transactions or Settled Original Securities Lending Transactions for inclusion in the Clearing, if certain conditions (see chapter 4) have not been complied with. Each of the CM Borrower and the CM Lender are entitled to agree with Eurex Clearing on a cancellation of any related Securities Lending Transaction until the end of the Business Day preceding the Value Date. For more details please refer to chapter 4.3.

3.4 Margin Requirement

In addition to the Principal Collateral (loan collateral) that the CM Borrower has to provide to the CM Lender, the CM Borrower and the CM Lender are subject to an own margin requirement (Margin Collateral, except holders of a Specific Lender License). The applicable Margin Types are the Current Liquidating Margin and the Additional Margin. Further information on margin calculations can be found in chapter 6.

3.5 Sample Questions

3-001

Which of the following statements is correct?

A: Eurex Clearing acts as Borrower/Lender with respect to each Clearing Member which is the Lender/Borrower under a Securities Lending Transaction.

B: For the counterparties of a Securities Lending Transaction there is no obligation to provide principal collateral.

C: Securities Lending Transactions can be concluded in any kind of security and are novated by Eurex Clearing.

D: All of the above Correct answer: A 3-002

The counterparties of a Securities Lending Transaction can never achieve a cancellation of their Securities Lending Transaction.

True False Correct answer: False

4 Loan Lifecycle Management

Eurex Clearing will novate new loan requests and open loans that have previously been transacted and settled between the Lender and the Borrower. After novation, during the lifecycle of loans loan requests can be received from the TPFPs. Each loan request is given a unique reference by Eurex Clearing. The following loan requests are provided by TPFPs during loan opening and the loan lifecycle:

• Request to open a new loan (Request Type NEW)

• Request to back-load a loan (Request Type BKL or VBK)

• Request to cancel a loan (Request Type CNC)

• Request to (partially) Return, Recall, Buy-in and Re-rate a loan (Request Types RET, REC, BYI, RRT)

• Withdrawal of a request of type Return, Recall or Buy-in (Request Type WDL)

• Return do not instruct request (Request type RNI)

Lender and Borrower agree on and provide via their common TPFP: Category Details

General Loan Security, Quantity

Mandatory: Definition of an External Order Number (generated and provided by TPFP, used by Eurex Clearing for reporting purposes) Optionally: External Member Order and Trade Number, Free Text Settlement Settlement date front leg (value date)

Contractual settlement date term leg if Fixed-Term loan Member ID, Agent ID, Account type

Collateral Details Cash: Markup Percentage Collateral Currency (EUR or USD)

Non-cash Transferred / Pledged: Markup Percentage

Tri-party Collateral Agent and accounts

Rebate, Fee details

Rebate:

Benchmark incl. spread, or alternatively: fixed rate Billing Currency

Lending fee:

Fee rate, billing currency (EUR or USD) Optionally:

fixed fee, minimum fee, billing margin Payment

Rate

Activities by Third Party Flow Provider

A flow provider reconciles the two transactions provided by the Lender and the Borrower. The loan will only be assigned an External Order Number and forwarded to Eurex Clearing once the trade details and request data of both counterparties match to each other. The reconciliation of the transactions is based on certain criteria defined by Eurex Clearing.The TPFP where the loan was transacted, forwards the loan transaction details to Eurex Clearing.

A trading market, on which the loan was traded electronically, forwards the details to Eurex Clearing as agreed on the market. The reconciliation platform and trading market shall have already validated loan details to avoid the loan being rejected by Eurex Clearing.

For this purpose Eurex Clearing can provide the TPFP with a set of static data:

• Available Trading Members, Agent Lenders and Clearing Members and their relationship, including clearing license

• Tri-party Collateral Agent for non-cash collateral including available collateral accounts

• CCP eligible loan securities and currencies

• Currency exchange rates

Processing by Eurex Clearing

Eurex Clearing receives the loan details electronically and will in all cases acknowledge receipt. In case of a successful validation, Eurex Clearing novates the loan and the processing continues for clearing and settlement, otherwise the corresponding request will be rejected by Eurex Clearing.

The following functional validations are done in addition to a number of technical validations. If any validation fails, the Third Party Flow Provider receives a negative feedback including an error message indication which validation failed, and the loan is not processed further by Eurex Clearing.

Category Field(s) Validation

General Loan Security Must be eligible for securities lending at Eurex Clearing Quantity/Lendable

Cash Amount

In case of Loan Security, quantity must be a multiple of the minimum settlement unit; in case of a Financing Loan, quantity is the lendable cash amount in EUR or USD. Settlement Settlement Date

Front Leg

Must be today or max. 2 years in the future, no holiday at CCP, CSDs, or collateral locations

For fixed Income loan securities the settlement date front leg shall not be later than 12 business days before the maturity date of the securities is reached

Settlement Date Term Leg

If provided at least one business day after settlement date of front leg, max. 2 years in the future, no holiday at CCP, CSDs or collateral locations

For fixed Income loan securities the settlement date term leg shall not be later than 11 business days before the maturity date of the security is reached

Category Field(s) Validation CM Lender

CM Borrower

Must be valid member of the CCP

Matching settlement and cash account available Clearing Members must have a valid clearing license Agent Lender If specified, must have a relationship with CM Lender Collateral Currency Cash Collateral: EUR, USD

Non-cash Collateral: eligible securities in any currency for which Eurex Clearing has an exchange rate.

TPCA Clearstream Banking Luxemburg - CBL, or Euroclear Bank - EB

TPCA Account Both Lender and Borrower accounts are validated and must have a relationship to the same Eurex Clearing account at the TPCA.

The Lender’s account must be a transfer account in case of transferred non-cash collateral, and/or a pledge account in case of pledged non-cash collateral.

Rebate, Lending Fee Benchmark Spread Interest Rate Billing Currency

Cash Principal Collateral and cash pool: benchmark with spread, or alternatively fixed non-negative rate

currency equal to collateral’s currency

(basis for Rebate calculation: Principal Collateral) Non-cash Principal Collateral and cash pool: basis points or a fixed non-negative value optional definition of fixed and/or minimum fee billing currency: EUR or USD

(basis for Lending Fee calculation: Loan Securities) Payment

Rate

Payment Rate Must be positive

Cut-off Times

Verify the trade entry cut-off time requirements

After successful validation Eurex Clearing legally steps in as the counterparty. The loan’s status is now “pending”.

4.1 Loan Opening

The Loan opening for new loans with T+0 settlement (S) of the front leg (novation date) takes place in near-time after novation, for others at the start of day on their contractual settlement date . Eurex Clearing coordinates the exchange of loan assets versus collateral. This happens in two phases, the collection and the distribution phase:

4.1.1 Collection and Distribution Phase

During the collection phase Eurex Clearing instructs the following by Power of Attorney:

• For cash Principal Collateral loans the payment location to transfer the cash Principal Collateral from the CM Borrower account to the Eurex Clearing account at the payment location.

• For non-cash Principal Collateral loans the TPCA to transfer the Principal Collateral from the CM Borrower account to the Eurex Clearing account at the TPCA.

• The (I)CSD to transfer the loan securities from the CM Lender account to the Eurex Clearing account at the (I)CSD.

• For Financing Loans the payment location to transfer the cash amount from the CM Lender account to the Eurex Clearing account at the payment location.

After the collection phase, both, the loanassets and the loan collateral are with Eurex Clearing. In the following distribution phase, Eurex Clearing instructs:

• For cash Principal Collateral loans the payment location to transfer the cash Principal Collateral from the Eurex Clearing account to the CM Lender account at the payment location.

• For non-cash Principal Collateral loans the TPCA to transfer or pledge the Principal Collateral from the Eurex Clearing account to the CM Lender account at the TPCA. The (I)CSD to transfer the loan securities from the Eurex Clearing account to the CM Borrower account at the (I)CSD.

• For Financing Loans the payment location to transfer the cash amount from the Eurex Clearing account to the CM Borrower account at the payment location.

The loan’s status is now “open”.

4.1.2 Exceptional Processing

If any of the above processing steps for loan opening fails, a clean-up process is executed. During the clean-up process the successful steps are cancelled and reversed, so that by the end of the day Eurex Clearing does not hold any positions for pending loans and the CM Lender / CM Borrower have received back the corresponding loan assets / principal collateral.

The failed loan opening process will be attempted again on the next business day. After a total of three unsuccessful attempts (on S, S+1 and S+2) of settlement of the loan opening Eurex Clearing will cancel the pending loan.

Pending fixed income loans with loan security at maturity will be cancelled by Eurex Clearing at the end of the 12th day before the final maturity date of the security.

4.2 Back-loading of Loans

Existing open loans between two counterparties can still be handed over to Eurex Clearing for novation and further processing thereafter. This is called “Back-loading”.

Back-loading differs from regular Loan Opening; in this case Eurex Clearing suppresses the settlement instructions of loan securities, lendable cash and cash Principal Collateral for the loan opening:

• The loan is sent to Eurex Clearing after settlement of the front leg, i.e. involved parties have already exchanged loan securities or lendable cash versus Principal Collateral.

• Eurex Clearing does not instruct exchange of loan securities or lendable cash.

• Eurex Clearing does not instruct exchange of cash Principal Collateral.

• For non-cash Principal Collateral, principal exposure (please refer to chapter 6 for the calculation of principle exposure) is instructed so that Principal Collateral is moved into the systems of the used TPCA. Please note that it remains the responsibility of the Lender and the Borrower to revert any already exchanged non-cash Principal Collateral on back-loaded loans outside of Eurex Clearing’s CCP system. The loan value of back-loaded loans considered by Eurex Clearing is provided by the Borrower and Lender with the back-load request. This value is considered as the ‘Current Principal Exposure’ to compute the ‘Variation Margin’ during the upcoming mark-to market calculation. The required input attributes for market participants are the same as for Loan Opening.

The Third Party Flow Provider validates the Lender’s and Borrower’s input and forwards the back-loaded loans thereafter to Eurex Clearing.

After a successful back loading process the loan’s status becomes “open”. Further processing of back-loaded loans no longer differs from loans opened by Eurex Clearing.

4.3 Loan Cancellation

Pending loans can be cancelled by the Lender and the Borrower before settlement of the front leg. Lender and Borrower agree on the cancellation bilaterally and provide the necessary information (Loan Security, External System Order Number, Trade Date) via the system of their common Third Party Flow Provider. The Third Party Flow Provider validates the Lender’s and Borrower’s input and forwards the cancellation request thereafter to Eurex Clearing.

Eurex Clearing receives the cancellation request and will in all cases acknowledge receipt. In case of a successful validation, the processing of the cancellation continues, otherwise the corresponding request will be rejected by the CCP.

If the loan opening processing is not currently underway the referenced loan will be deleted and the cancellation confirmed by feedback files.

In case the loan opening processing is already underway, the cancellation request will be stored for later processing. Two scenarios are now possible:

• Loan opening succeeds, which means that the loan reached status “Open”. In this scenario a cancellation is no longer possible and the cancellation request will be rejected.

• Loan opening fails, in which case the cancellation request will be processed after the clean-up processing described in chapter 4.1.2 - Exceptional Processing, i.e. the loan will be cancelled.

4.4 Allocation View versus Street View

In the bilateral market, Agent Lenders act as account operators for multiple Beneficial Owners. During the loan negotiation an Agent Lender and a Broker Dealer agree on one loan. In its role as an account operator the Agent Lender allocates loan securities from multiple Beneficial Owners and lends the securities to the Broker Dealer. The legal relationship is established between the Broker Dealer and each Beneficial Owner in the loan chain.

If Eurex Clearing novates a loan trade and an Agent Lender acts as account operator for multiple Beneficial Owners, each using a dedicated Specific Lender License, a legal relationship only exists between each Beneficial Owner using a Specific Lender License and Eurex Clearing. This fact leads to a splitting of the loan, i.e. a difference between “allocation view” and “street view”.

In such cases individual loan transactions are required from the Agent Lender (“allocation view”), even if Agent Lender and Broker Dealer originally agreed on one loan comprising the total quantity (“street view”). The Broker Dealer continues providing one loan transaction comprising the total quantity. It is within the responsibility of the Third Party Flow Provider to match the Broker Dealer loan against the individual loans from the Agent Lender. The Third Party Flow Provider will forward the individual loan requests to Eurex Clearing.

The individual loan transactions will be novated/opened and maintained separately within the CCP system. To allow a combined view after processing by Eurex Clearing the attribute “Common Reference” can be set to the same value in each individual loan transaction.

An example as well as further information regarding the “Common Reference” is provided in the document CCP Services for Securities Lending - Process Manual (chapter 3.4).

4.5 Loan Management

Unlike the pre-novation and new loan request activities, where the corresponding TPFP ensures confirmed novation requests on identical loan details for the Lender and the Borrower, the management of the loan inter-life closing activities might be initiated on a unilateral declaration either by the CM Borrower or the CM Lender. The CM Borrower / CM Lender is entitled to request a return (full or partial) / recall (full or partial) for Open-Term loans on unilateral basis, if the Return request respects the standard settlement cycles for the relevant loan securities settlement market. Bilaterally confirmed requests by CM Borrower and CM Lender are required for all Re-rate requests and Return / Recall requests (full or partial) with a notice period less than the standard settlement cycles.

Coexisting bilateral declarations by CM Lender and CM Borrower are also required for all modification requests of Fixed-Term loans. Notwithstanding, the processing and confirmation of request types are operated according to the rules of the TPFP. In regard to the loan management for outstanding loans, the following requests types are offered by Eurex Clearing:

• Return (full / partial closing) request entitled to CM Borrower.

• Recall (full / partial closing) request entitled to CM Lender.3

• Re-rate request entitled to CM Borrower and CM Lender.

• Buy-in request entitled to CM Lender.

• Withdrawal request (for Return, Recall and Buy-in requests)4.

3

The following requests are not available in case of financing loans: Recall, Buy-in, Withdrawal for Recall or Buy-in, Return-Do-Nnot-Iinstruct (CCP Release 9.2 – Release Notes)

• Return-Do-Not–Instruct request entitled to CM Borrower and CM Lender5

4.6 Return of an Open-Term Loan

The Lender and Borrower may agree on the return of the loan bilaterally. However, a Return request can only be issued by the CM Borrower via the TPFP for open loans after settlement of the front leg. If a Return request issued by the CM Borrower relates to a pending Recall request (please refer to chapter 4.8) already issued by the CM Lender, the Return request details shall be consistent with the Recall request details (e.g. Quantity, Settlement Date have to have the same value). Return requests can be withdrawn by a Return Withdrawal request also via the TPFP. Without a Return request an Open-Term loan stays open (until the theoretical date 31. Dec. 2099) or until it is automatically returned in case of fixed income securities at maturity.

The CM Borrower provides the Return request via his TPFP: Category Details

General Loan Security, External System Order Number, Trade Date to identify the loan to be returned

Quantity to be returned

Optionally: Reference to a Recall request Settlement Intended settlement date term leg

The Third Party Flow Provider validates the Borrower’s Return request and forwards the Return request thereafter to Eurex Clearing.

Eurex Clearing receives this request and will in all cases acknowledge receipt. In case of a successful validation, the processing of this request continues, otherwise it will be rejected with an appropriate error. Return requests can also be withdrawn by a Return Withdrawal request.

4.6.1 Standard Return Processing

Return requests which are received one day or more before the intended contractual settlement date of the term leg defined in the request are validated and stored for later execution on the given date.

Return requests received with the contractual settlement date being the current business day are processed in near time until the instruction cut-off time6 is reached. If the request is received on the contractual settlement date but after the instruction cut-off time, the request is postponed to the next business day.

The standard return processing is performed in two phases, the collection and the distribution phase which are coordinated by Eurex Clearing (see 4.7.1.1. and 4.7.1.2.)”

4

According to the terms of the TPFP, withdrawal requests are only available at TPFP Pirum.

5

Return Do Not Instruct requests are only available at TPFP Pirum.

4.6.2 Exceptional Return Processing

Exceptional processing of a Return request is applied in the following scenarios:

• Loan securities are delivered late

• Cash Principal Collateral is delivered late

• Non-cash Principal Collateral is delivered late

• Final maturity of fixed income loan securities is reached

4.6.2.1 Late Delivery of Loan Securities during Return Processing

If a (partial) return transaction fails because the CM Borrower does not return the loan securities towards the CM Lender, Eurex Clearing cancels the delivery instruction towards the CM Borrower and returns the already delivered Principal Collateral back to the CM Lender.

The loan remains open and the CM Borrower has to keep paying the lending fees/rebates. Thereafter, the Return request is re-instructed each business day until successful settlement or until its withdrawal. The CM Lender has the right to issue a Recall and a Buy-in request for the loan to be returned. 4.6.2.2 Late Delivery of Cash Principal Collateral during Return Processing

If a (partial) return transaction fails because the CM Lender does not return the cash Principal Collateral towards the CM Borrower, Eurex Clearing cancels the delivery instruction towards the CM Lender and returns the already delivered loan securities back to the CM Borrower. Eurex Clearing may grant an extension to the payment obligation until 09:30 (CET) the next morning (S+1) to return the cash Principal Collateral and a closing attempt will be performed by Eurex Clearing.

Eurex Clearing considers the non-return of cash Principal Collateral as a ‘failure to pay’, implying a Termination Event for the CM Lender.

Please note that even in case the loan securities are not returned at that particular point in time, the non-delivery of cash Principal Collateral can still be considered and handled as a Termination Event.

4.6.2.3 Late Delivery of Non-cash Principal Collateral during Return Processing

In case the CM Lender does not (fully) return the non-cash Principal Collateral upon closure of the loan, the CM Borrower can request to substitute the delivery obligation of the outstanding non-cash Principal

Collateral by a cash settlement. The cash settlement amount will be defined as a price premium to the last settlement price of the outstanding non-cash Principal Collateral ISINs and will be debited from the CM Lender and credited to the CM Borrower. The loan securities will then be returned to the CM Lender. If the CM Borrower does not request a cash settlement of the outstanding non-cash Principal Collateral within a certain timeframe and does not withdraw the Return request, Eurex Clearing will automatically initiate a cash settlement.

Further details on the late delivery handling of the non-cash Principal Collateral can be found in the Eurex Clearing Conditions chapter IX.

4.6.2.4 Forced return of loans at fixed income loan security maturity

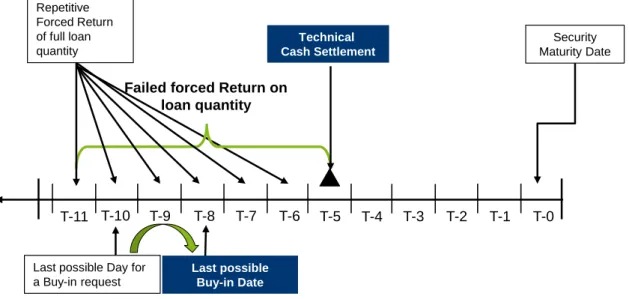

Due to final maturity of fixed income securities, Eurex Clearing will process a forced return of all open loans 11 business days prior to the final maturity date of the respective security (ISINs). During the end of day processing 12 days prior to the final maturity date of a fixed income security, Eurex Clearing will cancel all pending return requests in this ISIN and will replace them by a forced return covering the full pending quantity of the loans in this ISIN.

When the execution of a corresponding forced return is not or only partially successful, Eurex Clearing will continue the attempt to recollect the respective loan quantities and reinstruct the forced return of the open loan quantity for the following business days. If this procedure is not successful until 6 days prior to the final maturity date of the loan security, Eurex Clearing will instruct a “technical cash settlement” 5 days prior to the maturity date.

The latest possible day for a Buy-in request by CM Lender is 5 business days prior to the technical cash settlement (i.e. 10 days prior to the loan security maturity date).

Figure 4-1: Forced Return of Loan at fixed income loan security maturity

4.7 Return of a Fixed-Term Loan

The Fixed-Term loan is characterized by a contractual settlement date, which is agreed between CM Lender and CM Borrower upon opening of the loan. Eurex Clearing reports the settlement dates of open Fixed-Term loans to its Clearing Members on a daily basis.

The market participants had originally agreed on the settlement date. No additional input is required for closing a Fixed-Term loan on its contractual settlement date.

Different to Open-Term loans, CM Lender and CM Borrower are obliged to confirm bilaterally the loan change details provided to the TPFP.

In case of loan modifications for a Fixed-Term loan, the TPFP verifies the bilateral identical declarations of intent by CM Lender and CM Borrower.

Last possible Day for a Buy-in request T-8 T-7 T-6 T-5 T-4 T-3 Technical Cash Settlement Security Maturity Date T-2 T-1 T-0 Failed forced Return on

loan quantity Repetitive Forced Return of full loan quantity T-9 T-10 T-11 Last possible Buy-in Date

4.7.1 Standard Return Processing

Eurex Clearing automatically closes the Fixed-Term loan on its contractual settlement date.

The CCP coordinates the exchange of loan assets versus collateral. This happens in two phases, the collection and the distribution phase.

4.7.1.1 Collection and Distribution Phase

During the collection phase Eurex Clearing instructs by Power of Attorney:

• The payment location for Financing Loans to transfer the cash amount from the CM Borrower to the Eurex Clearing account at the payment location.

• The (I)CSD to transfer the loan securities from the CM Borrower account to the Eurex Clearing account at the (I)CSD.

• The payment agents for cash Principal Collateral loans to transfer the cash Principal Collateral from the CM Lender to the Eurex Clearing account at the payment location.

• The TPCA for non-cash Principal Collateral loans to transfer the Principal Collateral from the CM Lender account/pledge account to the Eurex Clearing account at the TPCA.

In the following distribution phase, Eurex Clearing instructs:

• The payment location for Financing Loans to transfer the cash amount from the Eurex Clearing account to the CM Lender account at the payment location.

• The (I)CSD to transfer the loan securities from the Eurex Clearing account to the CM Lender account at the (I)CSD.

• The payment agents for cash Principal Collateral loans to transfer the cash Principal Collateral from the Eurex Clearing account to the CM Borrower account at the payment location.

• The TPCA for non-cash Principal Collateral loans to transfer the Principal Collateral from the Eurex Clearing account to the CM Borrower account at the TPCA.

4.7.2 Exceptional Return Processing

If on the contractual settlement date either the CM Borrower or CM Lender does not fulfill his obligation to return the loan securities/lendable cash or the Principal Collateral, the loan remains open. Eurex Clearing returns loan securities/lendable cash or Principal Collateral received/collected.

Eurex Clearing automatically attempts to close the loan again on the following two business days. After the CM Borrower fails to deliver the loan securities for the third time, Eurex Clearing automatically executes a Buy-in for the loan securities on S+3 (for more details about the Buy-in process please refer to chapter 4.9).

To avoid the Buy-in for loan securities, CM Lender and CM Borrower can shift the contractual settlement date by providing a respective re-rate request (see chapter 4.10).

If the CM Borrower fails to actually deliver the Loaned Cash to Eurex Clearing AG in full until 9:30 a.m. (Frankfurt am Main time) on the Business Day following the Maturity Date with respect to the Non-Performed Transaction, a Termination Event shall have occurred with respect to the CM Borrower (irrespective of the fact whether a failure to deliver the Equivalent Principal Collateral by the CM Lender occurs at the same time).