Annual Repor

t 2014

Our path –

with resolve and rigour.

Annual Report 2014

Key figures

Operating profit (€m) Return on equity of consolidated profit or loss2, 3(%)

1Prior-year figures restated due to the restatement of credit protection insurance and the tax restatement plus the amended definition of average Group capital attributable to Commerzbank shareholders.

2Insofar as attributable to Commerzbank shareholders.

3The capital base comprises the average Group capital attributable to Commerzbank shareholders.

4The core Tier 1 capital ratio is the ratio of core Tier 1 capital (mainly subscribed capital and reserves) to risk-weighted assets. 2010 2011 2012 2013¹ 2014 1,386 507 1,170 731 684 2010 2011 2012 2013¹ 2014 4.7 2.2 – 0.2 0.3 7 1.0 Income statement 1.1.– 31.12.2014 1.1.– 31.12.20131 Operating profit (€m) 684 731

Operating profit per share (€) 0.60 0.80

Pre-tax profit or loss (€m) 623 238

Consolidated profit or loss2(€m) 264 81

Earnings per share (€) 0.23 0.09

Operating return on equity (%) 2.5 2.7

Cost/income ratio in operating business (%) 79.1 73.3

Return on equity of consolidated profit or loss2, 3(%) 1.0 0.3

Balance sheet 31.12.2014 31.12.20131

Total assets (€bn) 557.6 549.7

Risk-weighted assets (€bn) 215.2 190.6

Equity as shown in balance sheet (€bn) 27.0 26.9

Own funds as shown in balance sheet (€bn) 39.3 40.6

Capital ratios

Tier 1 capital ratio (%) 11.7 13.5

Core Tier 1 capital ratio4(%) 11.7 13.1

Total capital ratio (%) 14.6 19.2

Staff 31.12.2014 31.12.2013

Germany 39,779 41,113

Abroad 12,324 11,831

Total 52,103 52,944

Long/short-term rating

Moody’s Investors Service, New York Baa1/P-2 Baa1/P-2

Standard & Poor’s, New York A-/A-2 A-/A-2

Fitch Ratings, New York/London A+/F1+ A+/F1+

7 May 2015 Interim Report as at 31 March 2015

3 August 2015 Interim Report as at 30 June 2015 2 November 2015 Interim Report as at 30 September 2015

End-March 2016 Annual Report 2015

Commerzbank AG Head Office Kaiserplatz Frankfurt am Main www.commerzbank.com Postal address 60261 Frankfurt am Main Tel. + 49 69 136-20 [email protected] Investor Relations Tel. + 49 69 136-22255 Fax + 49 69 136-29492 [email protected]

Five-year overview

1Prior-year figures restated due to the restatement of credit protection insurance and the tax restatement plus the amended definition of average Group capital attributable to Commerzbank shareholders.

2Prior-year figures restated due to the first-time application of the amended IAS 19, the hedge accounting restatement and other disclosure changes.

3Prior-year figures restated due to the 10-to-1 reverse stock split of Commerzbank shares. 4Insofar as attributable to Commerzbank shareholders.

5The capital base comprises the average Group capital attributable to Commerzbank shareholders.

Income statement | €m 2014 20131 20122 2011 2010

Net interest income 5,607 6,161 6,487 6,724 7,054

Loan loss provisions – 1,144 – 1,747 – 1,660 – 1,390 – 2,499

Net commission income 3,205 3,206 3,249 3,495 3,647

Net trading income and

net income from hedge accounting 393 – 82 73 1,986 1,958

Net investment income 82 17 81 – 3,611 108

Current net income from companies

accounted for using the equity method 44 60 46 42 35

Other income – 577 – 87 – 77 1,253 – 131

Operating expenses 6,926 6,797 7,029 7,992 8,786

Operating profit 684 731 1,170 507 1,386

Restructuring expenses 61 493 43 – 33

Net gain or loss from sale of disposal groups – – – 268 – –

Pre-tax profit or loss 623 238 859 507 1,353

Taxes on income 253 66 803 – 240 – 136

Consolidated profit or loss attributable

to non-controlling interests 106 91 103 109 59

Consolidated profit or loss attributable

to Commerzbank shareholders 264 81 – 47 638 1,430

Key figures

Earnings per share3(€) 0.23 0.09 – 0.48 1.84 12.13

Dividend total (€m) – – – – –

Dividend per share (€) – – – – –

Operating return on equity (%) 2.5 2.7 4.0 1.7 4.5

Return on equity of consolidated profit or loss4, 5(%) 1.0 0.3 – 0.2 2.2 4.7

Cost/income ratio in operating business (%) 79.1 73.3 71.3 80.8 69.3

Balance sheet | €bn 31.12.2014 31.12.2013 31.12.20122 31.12.2011 31.12.2010 Total assets 557.6 549.7 636.0 661.8 754.3 Total lending 240.9 246.7 272.8 303.9 330.3 Liabilities 397.2 418.9 455.5 459.5 531.8 Equity 27.0 26.9 26.3 24.8 28.7 Capital ratios | %

Core capital ratio 11.7 13.5 13.1 11.1 11.9

Total capital ratio 14.6 19.2 17.8 15.5 15.3

Long/short-term rating

Moody’s Investors Service, New York Baa1/P-2 Baa1/P-2 A3/P-2 A2/P-1 A2/P-1

Standard & Poor’s, New York A-/A-2 A-/A-2 A/A-1 A/A-1 A/A-1

Annual Repor

t 2014

Our path –

with resolve and rigour.

Annual Report 2014

Key figures

Operating profit (€m) Return on equity of consolidated profit or loss2, 3(%)

1Prior-year figures restated due to the restatement of credit protection insurance and the tax restatement plus the amended definition of average Group capital attributable to Commerzbank shareholders.

2Insofar as attributable to Commerzbank shareholders.

3The capital base comprises the average Group capital attributable to Commerzbank shareholders.

4The core Tier 1 capital ratio is the ratio of core Tier 1 capital (mainly subscribed capital and reserves) to risk-weighted assets. 2010 2011 2012 2013¹ 2014 1,386 507 1,170 731 684 2010 2011 2012 2013¹ 2014 4.7 2.2 – 0.2 0.3 7 1.0 Income statement 1.1.– 31.12.2014 1.1.– 31.12.20131 Operating profit (€m) 684 731

Operating profit per share (€) 0.60 0.80

Pre-tax profit or loss (€m) 623 238

Consolidated profit or loss2(€m) 264 81

Earnings per share (€) 0.23 0.09

Operating return on equity (%) 2.5 2.7

Cost/income ratio in operating business (%) 79.1 73.3

Return on equity of consolidated profit or loss2, 3(%) 1.0 0.3

Balance sheet 31.12.2014 31.12.20131

Total assets (€bn) 557.6 549.7

Risk-weighted assets (€bn) 215.2 190.6

Equity as shown in balance sheet (€bn) 27.0 26.9

Own funds as shown in balance sheet (€bn) 39.3 40.6

Capital ratios

Tier 1 capital ratio (%) 11.7 13.5

Core Tier 1 capital ratio4(%) 11.7 13.1

Total capital ratio (%) 14.6 19.2

Staff 31.12.2014 31.12.2013

Germany 39,779 41,113

Abroad 12,324 11,831

Total 52,103 52,944

Long/short-term rating

Moody’s Investors Service, New York Baa1/P-2 Baa1/P-2

Standard & Poor’s, New York A-/A-2 A-/A-2

Fitch Ratings, New York/London A+/F1+ A+/F1+

7 May 2015 Interim Report as at 31 March 2015

3 August 2015 Interim Report as at 30 June 2015 2 November 2015 Interim Report as at 30 September 2015

End-March 2016 Annual Report 2015

Commerzbank AG Head Office Kaiserplatz Frankfurt am Main www.commerzbank.com Postal address 60261 Frankfurt am Main Tel. + 49 69 136-20 [email protected] Investor Relations Tel. + 49 69 136-22255 Fax + 49 69 136-29492 [email protected]

Five-year overview

1Prior-year figures restated due to the restatement of credit protection insurance and the tax restatement plus the amended definition of average Group capital attributable to Commerzbank shareholders.

2Prior-year figures restated due to the first-time application of the amended IAS 19, the hedge accounting restatement and other disclosure changes.

3Prior-year figures restated due to the 10-to-1 reverse stock split of Commerzbank shares. 4Insofar as attributable to Commerzbank shareholders.

5The capital base comprises the average Group capital attributable to Commerzbank shareholders.

Income statement | €m 2014 20131 20122 2011 2010

Net interest income 5,607 6,161 6,487 6,724 7,054

Loan loss provisions – 1,144 – 1,747 – 1,660 – 1,390 – 2,499

Net commission income 3,205 3,206 3,249 3,495 3,647

Net trading income and

net income from hedge accounting 393 – 82 73 1,986 1,958

Net investment income 82 17 81 – 3,611 108

Current net income from companies

accounted for using the equity method 44 60 46 42 35

Other income – 577 – 87 – 77 1,253 – 131

Operating expenses 6,926 6,797 7,029 7,992 8,786

Operating profit 684 731 1,170 507 1,386

Restructuring expenses 61 493 43 – 33

Net gain or loss from sale of disposal groups – – – 268 – –

Pre-tax profit or loss 623 238 859 507 1,353

Taxes on income 253 66 803 – 240 – 136

Consolidated profit or loss attributable

to non-controlling interests 106 91 103 109 59

Consolidated profit or loss attributable

to Commerzbank shareholders 264 81 – 47 638 1,430

Key figures

Earnings per share3(€) 0.23 0.09 – 0.48 1.84 12.13

Dividend total (€m) – – – – –

Dividend per share (€) – – – – –

Operating return on equity (%) 2.5 2.7 4.0 1.7 4.5

Return on equity of consolidated profit or loss4, 5(%) 1.0 0.3 – 0.2 2.2 4.7

Cost/income ratio in operating business (%) 79.1 73.3 71.3 80.8 69.3

Balance sheet | €bn 31.12.2014 31.12.2013 31.12.20122 31.12.2011 31.12.2010 Total assets 557.6 549.7 636.0 661.8 754.3 Total lending 240.9 246.7 272.8 303.9 330.3 Liabilities 397.2 418.9 455.5 459.5 531.8 Equity 27.0 26.9 26.3 24.8 28.7 Capital ratios | %

Core capital ratio 11.7 13.5 13.1 11.1 11.9

Total capital ratio 14.6 19.2 17.8 15.5 15.3

Long/short-term rating

Moody’s Investors Service, New York Baa1/P-2 Baa1/P-2 A3/P-2 A2/P-1 A2/P-1

Standard & Poor’s, New York A-/A-2 A-/A-2 A/A-1 A/A-1 A/A-1

world’s most innovative online banks. Commerzbank operates one of the densest networks of any private-sector bank in Germany. It serves a total of around 15 million private customers and 1 million business and corporate customers. The Bank, which was founded in 1870, is represented in all the world’s major financial centres. In 2014, it generated gross income of almost €9bn, with a headcount averaging around 52,000.

Our vision

Our Bank has 145 years of tradition behind it. This tradition is both a commitment and an obligation for the future. We combine modern banking with traditional values such as fair-ness, trust and competence. Our aim is to reinforce our leading position in our core markets of Germany and Poland over the long term. We intend to offer our private and corporate customers the banking and capital market services they need. In the future we shall remain at the side of our customers as a business partner in all markets all over the world. Our busi-ness will always be founded on dealing fairly and competently with customers, investors and employees.

Our mission

The operating environment for banks has changed fundamentally in recent years. Persistently low interest rates, ever-intensifying regulation and shifts in customer behaviour have had a lasting impact on banks’ activities. We will respond robustly to this paradigm shift: we are reducing risks further, optimising our capital base, pursuing a policy of strict cost management and at the same time making long-term investments in the Core Bank’s earnings power, while rigorously orienting our business model towards the needs of our customers and the real economy. Private Customers Private Customers Northern Region Private Customers Eastern Region Private Customers Central Region Private Customers Western Region Private Customers Southern Region Direct Banking Commerz Real Corporate Banking Mittelstandsbank Northern Region Mittelstandsbank Eastern Region Mittelstandsbank Central Region Mittelstandsbank Western Region Mittelstandsbank Southern Region Corporates International Financial Institutions + CTS

mBank Corporate Finance

Equity Markets & Commodities

Fixed Income & Currencies Credit Portfolio Management Client Relationship Management Research Transition London

Commercial Real Estate Deutsche Schiffsbank Public Finance Segments

Operating units

Private Customers Mittelstandsbank Central & Eastern Europe Corporates & Markets Non-Core Assets

All staff and management functions are bundled into the Group Management division.

The support functions of Group Information Technology, Group Organisation & Security, Group Banking Operations, Group Markets Operations, Group Delivery Center and Group Excellence & Support are provided by the Group Services division.

Commerzbank worldwide

As at 31.12.2014

Operative foreign branches 23

Representative offices 35

Group companies and major foreign holdings 6 Domestic branches in private customer business 1,100 Business customer consulting centres 94

Foreign branches 322 Worldwide staff 52,103 International staff 12,324 Domestic staff 39,779 Moscow Kiev Minsk Warsaw Ostrava Brno Prague Plzeň Bratislava Budapest Vienna Bucharest Belgrade Zagreb Istanbul Amsterdam London Brussels Luxembourg Paris Barcelona Madrid Milan Riga Zurich Caracas Panama City São Paulo Lagos Cairo Beirut Dubai Addis Ababa Johannesburg Shanghai Taipei Hong Kong Bangkok

Ho Chi Minh City Singapore Jakarta Dhaka Mumbai Buenos Aires Santiago de Chile Tripoli Melbourne Kuala Lumpur Luanda

world’s most innovative online banks. Commerzbank operates one of the densest networks of any private-sector bank in Germany. It serves a total of around 15 million private customers and 1 million business and corporate customers. The Bank, which was founded in 1870, is represented in all the world’s major financial centres. In 2014, it generated gross income of more than €9bn, with a headcount averaging around 52,000.

Our vision

Our Bank has 145 years of tradition behind it. This tradition is both a commitment and an obligation for the future. We combine modern banking with traditional values such as fair-ness, trust and competence. Our aim is to reinforce our leading position in our core markets of Germany and Poland over the long term. We intend to offer our private and corporate customers the banking and capital market services they need. In the future we shall remain at the side of our customers as a business partner in all markets all over the world. Our busi-ness will always be founded on dealing fairly and competently with customers, investors and employees.

Our mission

The operating environment for banks has changed fundamentally in recent years. Persistently low interest rates, ever-intensifying regulation and shifts in customer behaviour have had a lasting impact on banks’ activities. We will respond robustly to this paradigm shift: we are reducing risks further, optimising our capital base, pursuing a policy of strict cost management and at the same time making long-term investments in the Core Bank’s earnings power, while rigorously orienting our business model towards the needs of our customers and the real economy. Private Customers Private Customers Northern Region Private Customers Eastern Region Private Customers Central Region Private Customers Western Region Private Customers Southern Region Direct Banking Commerz Real Corporate Banking Mittelstandsbank Northern Region Mittelstandsbank Eastern Region Mittelstandsbank Central Region Mittelstandsbank Western Region Mittelstandsbank Southern Region Corporates International Financial Institutions + CTS

mBank Corporate Finance

Equity Markets & Commodities

Fixed Income & Currencies Credit Portfolio Management Client Relationship Management Research Transition London

Commercial Real Estate Deutsche Schiffsbank Public Finance Segments

Operating units

Private Customers Mittelstandsbank Central & Eastern Europe Corporates & Markets Non-Core Assets

All staff and management functions are bundled into the Group Management division.

The support functions of Group Information Technology, Group Organisation & Security, Group Banking Operations, Group Markets Operations, Group Delivery Center and Group Excellence & Support are provided by the Group Services division.

Commerzbank worldwide

As at 31.12.2014

Operative foreign branches 23

Representative offices 35

Group companies and major foreign holdings 6 Domestic branches in private customer business 1,100 Business customer consulting centres 94

Foreign branches 322 Worldwide staff 52,103 International staff 12,324 Domestic staff 39,779 Moscow Kiev Minsk Warsaw Ostrava Brno Prague Plzeň Bratislava Budapest Vienna Bucharest Belgrade Zagreb Istanbul Amsterdam London Brussels Luxembourg Paris Barcelona Madrid Milan Riga Zurich Caracas Panama City São Paulo Lagos Cairo Beirut Dubai Addis Ababa Johannesburg Shanghai Taipei Hong Kong Bangkok

Ho Chi Minh City Singapore Jakarta Dhaka Mumbai Buenos Aires Santiago de Chile Tripoli Melbourne Kuala Lumpur Luanda

Commerzbank remains on its growth pathin the Core Bank – and is pursuing it with resolve and rigour. Against the backdrop of the persistently difficult market environment, the customer-oriented core segments Private Customers, Mittelstandsbank, Central & Eastern Europe and Corporates & Markets achieved total operating profits of €2.7bn, after €2.4bn the previous year. This was aided in no small part by our overhauled product and service offering, which has been brought more closely into line with customer needs. But we are not yet where we want to be – the journey continues. In this section, you

will find extensive information on the steps we took in 2014 in Private

Customer and Mittelstandsbank business.

›

High satisfaction levels

among private customers

Page 70

›

Mittelstandsbank boosts

its lending volume

Page 75›

mBank records growth in

net new customers

Page 80›

Corporates & Markets

enjoys growth in corporate

finance business with

international corporate

customers

Page 84›

Reduction of NCA port

a new way of banking

+ 51%

growth in mandate

investment models

and premium

cus-tody accounts

One of the most modern bank branches in Germany opened its doors in April, just across from Berlin’s landmark Kaiser Wilhelm Memo-rial Church. This flagship branch on the Kurfürstendamm has been completely redesigned and is part of a pilot scheme in Berlin and Stuttgart that Commerzbank is trialling, testing the future of the branch busi-ness, with an expanded range of products and services and a new advisory approach. Surveys have found the concept to be very well received by cus-tomers. Around 80% described it as “startling” and “innovative”.

million downloads of

the Commerzbank apps

Our offering for users of mobile devices such as smartphones and tablets is constantly grow-ing. We launched a new mobile banking app for tablets in 2014. Another innovation was an app for quickly checking account balances without the need for access data to be entered. In total, Commerzbank apps had been downloaded 1.1 million times as at year-end. Under our new business model, we aim to turn digital banking into a pillar of equal significance, closely integrated with the branches.

More and more customers are dele-gating their investment decisions to Commerz bank, entrusting their assets to our all-in, hassle-free packages: the premium custody account, wealth management products or individual wealth management. In so doing, our customers gain access to professional portfolio management with an inde-pendent investment process and trans-parent pricing model. The customer’s needs in terms of investment horizon and portfolio structure are all that count. The highly attractive offering and above-average performance by our mandate investment models drew in another strong increase in volumes in 2014, up from €21bn in 2013 to €32bn last year. This equates to pene-tration of 37% of our securities cus-tody volume.

Modern banking gets a new design:Commerzbank’s flagship branch in Stuttgart.

›

A powerful online banking portal

business. New private and corporate customer gains were helped by the marketing campaign around the Football World Cup, which

they are also fundamental to the corporate culture.

With a home page that customers can customise as they like, the online banking portal was made more modern and user-friendly last year, and also gained addi-tional funcaddi-tionalities. The technical processes were also significantly improved; for example, customers can now place securities orders online quickly and conveniently. Commerzbank is also trialling innovative functions such as legitimising customers by video when concluding sales transactions for selected products. Nearly 140,000 new online con-nections were set up in 2014.

Attracting attention in a World Cup year:Commerzbank’s marketing campaign featuring the German national football squad.

User-friendly and convenient:the new Commerz-bank online Commerz-banking portal.

+ 8%

Growth in lending

to domestic

porate customers

outstrips the market

Strong customer focus and high-quality advice:more than half of high-end medium-sized businesses and 90% of large corporates in Germany place their trust in Commerzbank.

More and more companies

are choosing us

Increasing numbers of small and medium-sized businesses – at both the upper and lower ends of that bracket – are opting for Commerzbank. We significantly grew our customer base last year, with nine out of every ten large corporates in Germany doing business with us. They value our high product expertise and established cus-tomer relationship management approach. For us, a strong cuscus-tomer focus and high-qual-ity advice are at the very heart of the customer relationship. We are also making good progress in Switzerland and Austria. Through efficient processes for the settlement of international documentary business, we are putting ourselves in a position to win new cus-tomers outside our core markets. In Germany, we have 150 locations nationwide serving SMEs and large corporates, on top of our international units in Western Europe, Eastern Europe, Asia and North America.

›

We once again put our claim to sup-port our customers as a strategic partner to the test. We receive con fir-mation of our recognition and high satisfaction among our customers in our annual customer surveys, and once again we managed to improve on our already very good figures. The biggest factors behind the high satisfaction levels were our advisory capabilities and the dedication of our corporate customer advisors and experts. Our customers’ trust is also reflected in our involvement in their growth measures: loan drawdowns have increased in all three Group divisions over the last 12 months. In Germany, despite grow-ing intensity of competition, we suc-ceeded in growing the volume of lending to domestic corporate cus-tomers by 8%, a better performance than the market, which shrank slightly last year. At the same time we also managed to keep risk in our loan port-folio at a moderate level. We also boosted income from other product areas. We particularly impressed our customers in International Business and Corporate Finance.

Driving forward internationalisation: expanding our

successful business model beyond national borders

17%

High market share in export

letters of credit in the eurozone

We support our customers in the relevant markets as they increasingly internationalise their business, applying a proven, internationally standardised customer relationship management approach. But we are also expanding inter -nationally ourselves: last year, we opened another five locations in Switzerland, won local corporate customer business in Austria

and worked intensively on preparations to open a subsidiary in São Paulo (Brazil), scheduled for 2015. We also strengthened our network of partner banks in Asia, adding two Indian banks. With the launch of renminbi clearing in Frankfurt, we now offer our customers access to the only renminbi clearing centre in the eurozone.

The Financial Institutions division bundles together customer responsi -bility and sales expertise for some 5,000 domestic and foreign banks and central banks. In this way, we are strengthening our standing as a major foreign trade bank, covering all key regions of the world. This is also reflected in the way we are further building up our position as one of the leading banks in the processing of export letters of credit in Ger-many – and increasingly in the rest of the eurozone too: SWIFT Watch indicates that we have steadily improved our market share in the eurozone to over 17%.

A driver of growth and employment:we are on hand to partner businesses with our extensive expertise.

›

At the start of last year we received the ac-colade of “Test Winner – Mittelstandsbank” based on a survey conducted by the German Institute for Service Quality (Deutsches Insti tut für Service-Qualität, DISQ). The Mit-tel standsbank came across particularly im-pressively on performance and customer orientation. DISQ said employees “scored on credibility and expertise.” Internal customer surveys bear out this view: we have substan-tially increased our satisfaction among cor-porate customers since 2011.

To our Shareholders

Page 8 to 24

Corporate Responsibility

Page 25 to 54

Group Management Report

Page 55 to 106

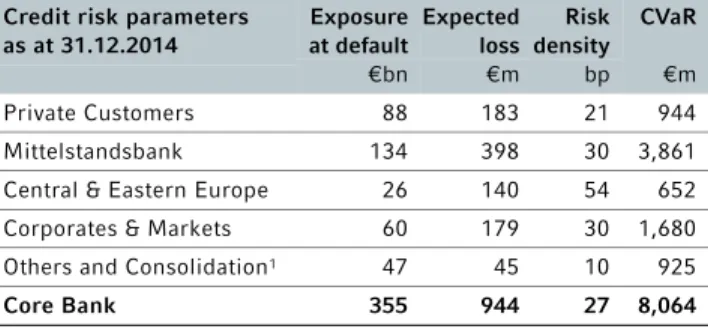

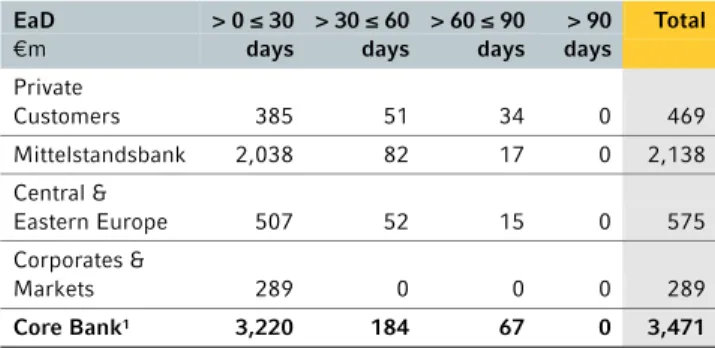

Group Risk Report

Page 107 to 144

Group Financial Statements

Page 145 to 326

Further Information

8 Letter from the Chairman of the Board of Managing Directors 11 The Board of Managing Directors

12 Report of the Supervisory Board 18 Supervisory Board and Committees 21 Our share

27 Corporate governance report 31 Remuneration Report

48 Details pursuant to Art. 315 of the German Commercial Code (HGB) 53 Corporate Responsibility

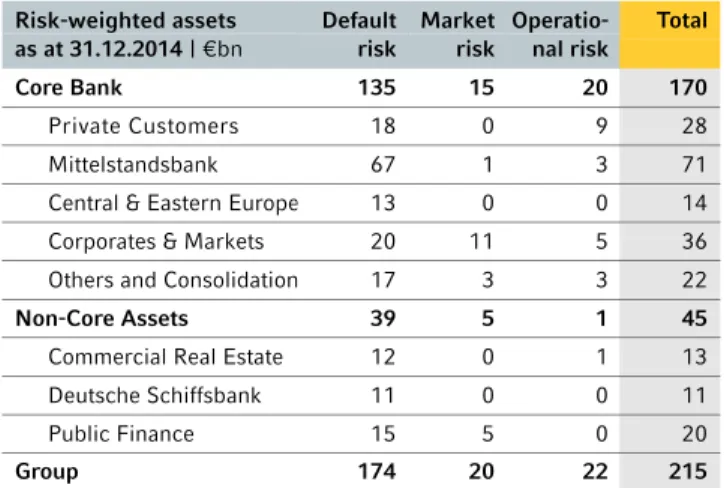

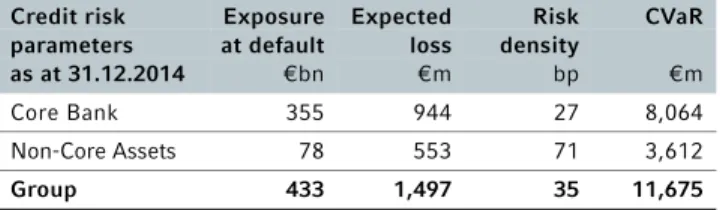

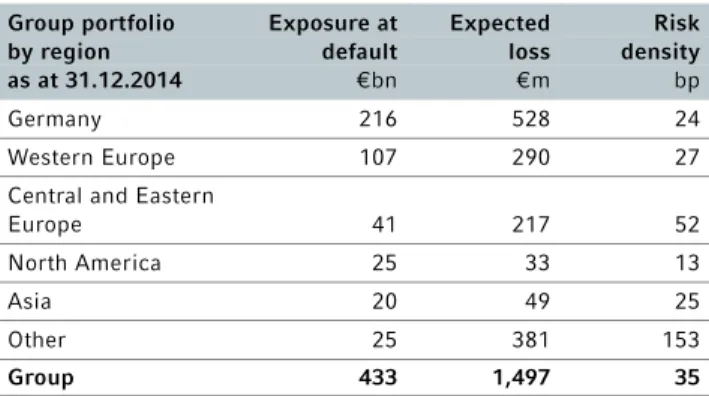

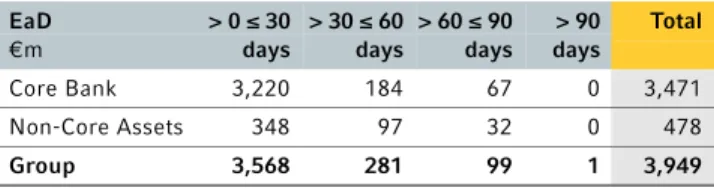

109 Executive summary 2014

110 Risk-oriented overall bank management 116 Default risk

133 Market risk

328 Central Advisory Board 329 Seats on other boards 331 Glossary

335 Information on the encumbrance of assets 336 Index of figures and tables

338 Quarterly results by segment

8 – 24

25 – 54

55 – 106

107 – 144

327 – 339

137 Liquidity risk 139 Operational risk 140 Other risks147 Statement of comprehensive income 150 Balance sheet

152 Statement of changes in equity 154 Cash flow statement

156 Notes

324 Responsibility statement by the Board of Managing Directors 325 Auditors’ report

145 – 326

57 Basis of the Commerzbank Group 62 Economic report

71 Segment performance 71 Private Customers 76 Mittelstandsbank 81 Central & Eastern Europe

85 Corporates & Markets 90 Non-Core Assets 93 Others and Consolidation 94 Our employees

97 Report on events after the reporting period 98 Outlook and opportunities report

T

o our Shar

eholders

Letter from the Chairman of the Board of Managing Directors

Frankfurt am Main, March 2015

2014 was another very challenging year for the entire financial sector, and the market environment remained difficult. The challenges included persistently low interest rates and rising and ever more frequent demands from regulators, placing a significant financial and staffing burden on those af-fected. The relationship between banks and their customers is also changing. Customers’ expectations of their bank and their advisory needs are becoming increasingly complex. They are focused much more heavily than in previous years on their individual requirements and circumstances, or in the case of corporate customers on their competitive situation, and require banks to be highly flexible. The overall conditions for the banking industry are very challenging, and both income and costs are under increasing pressure. This is the situation we have to deal with. Amidst all these changes, however, we also see opportunities we are keen to seize, and we are going about this in a focused manner through the strategic actions now underway or already completed. Dear shareholders, concerning the already known investigations with respect to breaches of US embargo and money laundering regulations, we have reached a settlement – after long negotiations – with the investigating US authorities. With this settlement we are concluding a process which has been protracted and complex for all parties involved. Measures to remedy the deficiencies identified by the US authorities have already been initiated. The earnings figures presented to you on the occa- sion of the annual press conference on 12 February 2015, were adjusted on 3 March 2015 by increas-ing provisions for litigation and recourse risks, in anticipation of a settlement. Nevertheless, and despite the challenges described above, Commerzbank’s operating business performed well in 2014. We achieved further growth in the Core Bank, gaining market share and ex- panding our customer base. Customer satisfaction was up in both the Private Customers and Mittel-standsbank segments, and we were able to increase customer confidence. Commerzbank also

T o our Shar eholders boosted its stability again in 2014 by continuing to reduce risk and strengthen the capital base. Particularly important was the fact that Commerzbank not only passed both the European Central Bank’s Asset Quality Review and the European Banking Authority’s stress test at the end of the year: we were well above the required levels. The good result of the ECB’s Comprehensive Assessment is testimony to the successful restructuring of Commerzbank over the past few years and confirms that we are on the right track with our efforts both to reduce our non-strategic portfolios and to expand our customer-focused business model. Allow me to take a look at the performance of Commerzbank over the past year. The stable to very good results of our core segments during the year show that our strategic measures, our investments and the adaptation of our range of products and services to customer needs and desires are tackling the right levers. In the private customer business we are adapting our advisory model by adding new service and advisory offerings. The opening of our first completely redesigned flagship branches in Berlin and Stuttgart in spring 2014 was a key milestone and a further step in our branch strategy. The expansion of digital offerings such as online and mobile banking is also important, however, if we are to offer our range of products and services as a genuine multi-channel bank. Direct bank capability was achieved at the end of 2014. This means that Commerzbank customers can now carry out all major transactions online – and an increasing number are using this service. The online banking portal was also com-pletely redesigned in 2014. We were guided by the need for user-friendliness and a modern look, and have improved and shortened the technical processes. The complete overhaul of our range of prod-ucts and services as part of the private customers strategy led to continued growth in customers, accounts and assets. New customer gains were helped in 2014 by the successful marketing campaign around the Football World Cup, which focused on the free current account with a satisfaction guaran-tee. The Private Customers segment gained a total of around 288,000 net new customers in 2014. The Mittelstandsbank is still well positioned. We managed to further grow the customer base over the year. In addition to anchor loan products we also provide our corporate customers with custom-fit, efficient solutions geared to their specific requirements, so we can continue to meet all their needs. As part of our aim to be the “leading bank for SMEs”, Commerzbank ensures that Mittelstandsbank customers benefit from a uniform service model worldwide, so both local and cross-border needs of a globally active company are specifically met. Under the expansion of our international strategy we are intensifying our business in selected core markets. We have been operative in six locations in Switzer- land since April 2014, and are seeing pleasing growth in new customers. These offices are now cover-ing small and medium-sized businesses as well as large corporates, giving them access to the full range of products. We support our corporate customers in both their local and their international activities. The pleasingly dynamic performance of the Central & Eastern Europe segment, represented by our mBank subsidiary, the fourth-largest bank in Poland, continued in the year under review. The sus- tained strong growth is also the result of continuous work on innovative products and technical solu-tions. mBank introduced a host of new or updated loan, deposit and investment products in 2014 along with new processes to support sales. The cooperation with Orange Polska, one of the largest telecoms providers in Poland, is one example of this. We have worked with them to develop the Orange Finance project in mobile banking, a new offering for customers who expect to have easy access to their finances wherever they are. In addition, mBank offers Orange Finance customers banking prod-ucts online and through around 900 mobile phone shops in Poland.

T

o our Shar

eholders

Martin Blessing

Chairman of the Board of Managing Directors

The performance of Corporates & Markets in 2014 was driven by a market environment of historically low interest rates and occasional low volatility. The segment’s broad base allowed the impact of lower activity in some areas to be partially offset by strong points elsewhere. This was an instance of our diversified business model paying off. In the Corporate Finance division, performance was mostly good over the year. In Germany and Europe, the equity issuance busi-ness was well up on previous years. However, persistently low interest rates caused customer activity to decline in some areas of the business. One example of the close integration with Mittelstandsbank is the agreement concluded with Bank of China in the year under review for the direct processing of renminbi payments in Frankfurt. Commerzbank now offers renminbi accounts in Asia and Europe, offering corporate customers a reliable way to transfer renminbi payments directly to the Chinese mainland. In the Non-Core Assets segment (NCA), we made further progress in running down the port-folio in 2014. We sold the commercial real estate portfolios in Spain and Japan and a portfolio of non-performing real estate loans in Portugal. We also further reduced the shipping portfolio by selling nine container ships. We are aiming for a volume of €20bn for our real estate and shipping portfolio by 2016. The bottom line as regards all our strategic measures, investments, products and services, whether already implemented or in the pipeline, is that they must also be reflected in our earnings performance. The operating profit achieved in the customer-oriented core segments – Private Customers, Mittelstandsbank, Central & Eastern Europe and Corporates & Markets – in 2014 of €2.7bn, up from €2.4bn the previous year, is a sign that we are on the right path by rigorously gearing our business model to the changed operating environment. Total consoli-dated operating profit for the period was €684m, from €731m last year. Consolidated earnings attributable to Commerzbank shareholders were €264m, against €81m last year. The consistent implementation of our strategic agenda will continue to be a key success fac-tor in Commerzbank’s performance. We are continuing to focus all our efforts on reaching the quantitative objectives announced for 2016. Despite our confidence, however, it would not be prudent to ignore the fact that the operating conditions for banks have changed and the market environment for a broad and profitable banking business has become more difficult. However, the action we have already taken and our plans for the future have laid the foundations for fur-ther growth in 2015 – in customers, market share and assets. I would be delighted if you were to accompany “your Bank” along this challenging path. I am pleased to take this early opportu-nity to invite you to our 2015 Annual General Meeting, and I look forward to seeing you there.

T o our Shar eholders

The Board of Managing Directors

Martin Blessing

Age 51, Chairman Central & Eastern EuropeMember of the Board of Managing Directors since 1.11.2001

Frank Annuscheit

Age 52, Chief Operating Officer Human Resources Member of the Board of Managing Directors since 1.1.2008

Markus Beumer

Age 50, Mittelstandsbank Non-Core Assets (Deutsche Schiffsbank and Commercial Real Estate) Member of the Board of Managing Directors since 1.1.2008Stephan Engels

Age 53, Chief Financial Officer Member of the Board of Managing Directors since 1.4.2012Michael Reuther

Age 55, Corporates & Markets Non-Core Assets (Public Finance) Member of the Board of Managing Directors since 1.10.2006

Dr. Stefan Schmittmann

Age 58, Chief Risk Officer

Member of the Board of Managing Directors since 1.11.2008

Martin Zielke

Age 52, Private Customers Member of the Board of Managing Directors since 5.11.2010T o our Shar eholders during the year under review, we advised the Board of Managing Directors on its conduct of the Bank’s affairs and regularly supervised the way in which Commerzbank was managed. The Board of Managing Directors reported to us at regular intervals, promptly and extensively, in both written and verbal form, on all the main developments at the Bank, including between meetings. We received frequent and regular infor-mation on the company’s business position and the economic situation of its individual business segments, on its corporate planning, on the main legal disputes, on the performance of the share price and on the strategic orientation, including risk strategy, of the Bank, and we advised the Board of Managing Directors on these topics. Between meetings I, as the Chairman of the Supervisory Board, was constantly in touch with the Chairman and other members of the Board of Managing Directors according to a set timetable and kept myself up to date with the current business progress and major business transactions within both the Bank and the Group. The Supervisory Board was involved in all decisions of major importance for the Bank, giving its approval after extensive consultation and examination wherever required.

Meetings of the Supervisory Board

In the year under review there were a total of nine Supervisory Board meetings, of which four were held as conference calls. Two full-day strategy meetings also took place: one for the employee representatives and one for the shareholder representatives. The focus of all ordinary meetings was the Bank’s current business position, which we discussed in detail with the Board of Managing Directors. We considered in depth the Bank’s economic and financial perform- ance, the risk situation, the strategy, the planning, the risk management system and the internal control sys-tem. Another area of emphasis was the economic performance and orientation of the individual business segments. We subjected the reports of the Board of Managing Directors to critical analysis, in some cases requesting supplementary information, which was always provided immediately and to our satisfaction. We also received information on internal and official investigations into the Bank in Germany and other Report of the Supervisory Board

T o our Shar eholders countries, asked questions regarding these and then formed our verdict on them. Drawing on earlier advice from the competent committees, we dealt in several meetings with matters pertaining to the Board of Man- aging Directors, in particular the adjustments to the remuneration system of the Board of Managing Direc-tors to bring it into line with the new regulatory requirements. We also discussed and resolved upon the goal achievement of the individual members of the Board of Managing Directors in financial year 2013 and set the Board of Managing Directors’ targets for 2015. Urgent resolutions of the Supervisory Board were where necessary also passed between meetings by way of circulars. At the meeting of 12 February 2014, our discussions centred, alongside reports on the current business position, the recovery plan and the Private Customers segment, on the provisional results for financial year 2013, the outlook for Commerzbank in 2014 and the upcoming Asset Quality Review. In the ensuing dis -cussion, we satisfied ourselves that the expectations and targets presented were plausible, particularly with regard to the Private Customers segment, and we discussed the various courses of action available. We also considered the declaration of compliance, the Report of the Supervisory Board and the Corporate Govern -ance Report for the Annual Report. We discussed and resolved on the goal achievement of the members of the Board of Managing Directors for 2013 and the ratio of variable to fixed remuneration for 2014. We also reappointed the Nomination Committee. At the accounts review meeting on 19 March 2014, we reviewed the parent company and Group financial statements for 2013 and approved them on the Audit Committee’s recommendation. In addition we approved the proposal for the Annual General Meeting regarding the election of share-holder representatives to the Supervisory Board and the proposed resolutions for the agenda of the 2014 Annual General Meeting, including the proposal for the appropriation of profit. We also considered the Reports of the Supervisory Board for the Annual Report and approved the appointment of the Remuneration Officer. We also extended the terms of office on the Board of Managing Directors of Michael Reuther and Stephan Engels. The meeting on 8 May 2014 was devoted mainly to preparations for the Annual General Meeting that was to follow. We looked at the proceedings for the AGM and the countermotions that had been submitted, and we amended the Rules of Procedure of the Supervisory Board and the Audit Committee in line with regu-latory changes. We were informed of the ruling of the Regional Court of Frankfurt am Main in the case of Sieber versus Commerzbank regarding dismissal from the Board of Managing Directors and resolved to appeal against it. In an extraordinary conference call on 16 June 2014, we considered questions relating to the portfolio of equity holdings. At the meeting of 4 September 2014, the Board of Managing Directors reported to us on the Bank’s business performance and half-year results for 2014. We were also informed about the status of investiga- tions into the Bank relating to breaches of US sanctions and, together with the Board of Managing Direc-tors, received extensive advice on the next steps. We also elected new members to the Risk, Social Welfare, Nomination and Conciliation Committees. The Head of the IT Division reported to us with detailed docu-mentation on Commerzbank’s IT strategy and the status of measures initiated following the Bundesbank’s audit pursuant to Art. 44 of the German Banking Act. The Board of Managing Directors informed us about the new employee remuneration models for the whole Group. We also considered in detail the adjustment of the remuneration system of the Board of Managing Directors to bring it in line with the new regulatory requirements and laid down the parameters pursuant to no. 4.2.2 para. 2 of the German Corporate Gov -ernance Code for vertical comparison as part of checking the appropriateness of the remuneration of the Board of Managing Directors. In addition, we discussed the findings of the Supervisory Board’s 2014 effi-ciency audit.

T o our Shar eholders At two special meetings on 24 and 26 October 2014, we reviewed in depth the results of the ECB’s Com-prehensive Assessment in relation to the findings for Commerzbank, and discussed these in relation to the results for all 130 banks. At the ordinary meeting of 5 November 2014, discussions centred on the report on the business position, including the budget for 2015 and the medium-term planning for the period to 2018. The targets for the Bank and the Group, which were based on the business figures, were presented to us and we discussed them in detail with the Board of Managing Directors. We also held an in-depth discussion with the Board of Managing Directors regarding Commerzbank’s business and risk strategy. The Head of the Compliance Divi- sion also reported on the compliance structure and implementation at the Bank. In this regard, we also re-ceived an update from the Board of Managing Directors on the status of the US investigations in connection with measures by the Bank to prevent money laundering. We also discussed the adjustment of the remunera-tion system of the Board of Managing Directors to bring it into line with the new regulatory requirements, reviewed the appropriateness of the remuneration of the Board of Managing Directors with input from exter-nal remuneration advisors and agreed the members of the Board of Managing Directors’ targets for 2015. Other topics covered at this meeting included the Bank’s corporate governance; in particular, we approved the annual Declaration of Compliance with the German Corporate Governance Code pursuant to Art. 161 of the German Stock Corporation Act and amended the Rules of Procedure of the Supervisory Board and the Board of Managing Directors. More details on corporate governance at Commerzbank can be found on pages 27 to 30 of this Annual Report. At a further extraordinary meeting on 10 December 2014, we again dealt in detail with the new remu- neration model for the Board of Managing Directors. We were also informed about the US attorney’s inves-tigations in connection with measures by the Bank to prevent money laundering.

Committees

To ensure that it can perform its duties efficiently, the Supervisory Board has formed seven committees from its members. The current composition of the committees is shown on page 20 of this Annual Report. The duties and responsibilities of the individual committees are defined in the Supervisory Board’s Rules of Pro-cedure, which can be found online at www.commerzbank.com. The Presiding Committee held five meetings during the year under review, of which one was conducted as a conference call. Its discussions were devoted to preparing for the plenary meetings and in-depth treat- ment of the meeting deliberations, especially with regard to the business situation. It also dealt with the ex-tension of the terms of office on the Board of Managing Directors of Michael Reuther and Stephan Engels. The Presiding Committee also prepared the plenary body’s resolutions and agreed to members of the Board of Managing Directors taking up mandates at other companies. We also looked into loans to employees and officers of the Bank. Urgent resolutions were passed by way of circulars. The Audit Committee met a total of six times in financial year 2014. It also passed urgent resolutions by way of circulars. With the auditors in attendance, it discussed Commerzbank’s parent company and Group financial statements and the auditors’ reports. The Audit Committee obtained the auditors’ declaration of independence pursuant to Section 7.2.1 of the German Corporate Governance Code, submitted proposals for the appointment of the auditors and for their fee to the Supervisory Board and advised the SupervisoryT o our Shar eholders Board on the continuation of the audit mandate. Furthermore, the Audit Committee dealt with requests for the auditors to perform non-audit services; it also received regular reports on the current status and individ-ual findings of the audit of the annual financial statements and discussed the interim reports before they were published. The work of the Bank’s Group Audit and Group Compliance units also formed part of the discussions. The Audit Committee also received regular updates on the status of remediation of the deficien-cies identified by the auditor. In addition, the Audit Committee dealt with the functioning of the ICS and the progress on reputational and compliance risks within the Group. It also examined the effectiveness of the Bank’s risk management system and discussed developments in whistle-blowing cases and the auditor’s re-port on the review of reporting obligations (Art. 9) and rules of conduct (Art. 31 et seq.) under the German Securities Trading Act. Furthermore, the Audit Committee obtained information on internal and external (regulatory) investigations and non-event-related audits by the German Financial Reporting Enforcement Panel. Other areas covered were the ECB’s Asset Quality Review, the Commerzbank Liquidity Project and the Bank’s provisions for legal risks and recourse claims, particularly in relation to investigations into breaches of US sanctions by the Bank. The Audit Committee also gave us an update on current and forth-coming changes to supervisory and accounting law. Representatives of the auditors attended the meetings to report on their audit activities. The Risk Committee convened a total of four times in financial year 2014. At its meetings, the Risk Com-mittee closely examined the Bank’s risk situation and risk management, devoting particular attention to the overall risk strategy for 2015, refinement of the risk strategy and credit, market, liquidity, operational, repu-tational and compliance risks. Significant individual exposures of the Bank were also discussed in detail with the Board of Managing Directors, as were the portfolios in the Non-Core Assets segment, notably the shipping portfolio. The Risk Committee also considered the Bank’s recovery plan. In addition it reviewed whether terms and conditions in customer business are compatible with the Bank’s business model and risk structure. The meetings also addressed the employee remuneration system and the risk assessment of Commerzbank by its regulators. In addition, the Risk Committee considered Commerzbank’s risk-bearing capacity, large exposures and loans to Commerzbank Group companies. The Remuneration Control Committee, set up in 2014, met twice in financial year 2014. It considered the remuneration model for the Board of Managing Directors, its adjustment to bring it into line with the regula-tory requirements and the appropriateness of the remuneration of the Board of Managing Directors. It also dealt with the employee remuneration systems and in particular the appropriateness of their structure. The Remuneration Officer also introduced himself, discussed his mandate and coordinated his cooperation with the committee. The Social Welfare Committee met once in the year under review, with the meeting focusing primarily on human resources policy and staff development. It also looked at progress on headcount reduction, general HR measures, health in the workplace, recruitment and the HR-MOVE-Center. The Nomination Committee held three meetings during the year under review. It covered the composi-tion of the Supervisory Board, proposals for the election of shareholder representatives to the Supervisory Board at the 2014 Annual General Meeting and possible proposals for the 2015 Annual General Meeting. It also performed the duties of the Nomination Committee pursuant to Art. 25d (11) sentence 2 of the Ger-man Banking Act, in particular the assessment of the Supervisory Board and Board of Managing Directors required by that act.

T o our Shar eholders The chairs of the committees regularly reported on their work to the plenary body of the Supervisory Board at the next meetings thereafter. Members of Commerzbank’s Supervisory Board are required pursuant to Art. 3 para. 6 of the Rules of Procedure of the Supervisory Board to disclose potential conflicts of interest to the Chairman of the Super-visory Board or their deputy, who will in turn consult with the Presiding Committee and disclose the conflict of interest to the Supervisory Board. No member of the Supervisory Board declared a conflict of interest during the year under review. The members of the Supervisory Board undertook the training and development measures required for their duties at their own initiative, with appropriate support from Commerzbank. In particular, an internal two-day qualification course was offered for new members of the Supervisory Board. Members of the Super-visory Board were also kept informed about new developments in supervisory law on an ongoing basis. Topics such as compliance, IT security and banking-related projects were also covered in depth. In addition, the members of the Nomination Committee spoke about the duties of their committee under Art. 25d (11) of the German Banking Act. No member of the Supervisory Board attended fewer than half the meetings in financial year 2014.

Parent company and Group financial statements

The auditors and Group auditors appointed by the Annual General Meeting, PricewaterhouseCoopers Aktien - gesellschaft Wirtschaftsprüfungsgesellschaft, Frankfurt am Main, audited the parent company annual finan-cial statements and the consolidated financial statements of Commerzbank Aktiengesellschaft and also the management reports of the parent bank and the Group, giving them their unqualified certification. The par-ent company financial statements were prepared according to the rules of the German Commercial Code (HGB), and the consolidated financial statements according to International Financial Reporting Standards (IFRS). The financial statements and auditors’ reports were sent to all members of the Supervisory Board in good time. In addition, the members of the Audit Committee also received the complete annexes and notes relating to the auditors’ reports, and all members of the Supervisory Board had the opportunity to inspect these documents. The Audit Committee dealt at length with the financial statements at its meeting on 16 March 2015. At our meeting to approve the financial statements held on 17 March 2015, we met as a plenary body and examined and approved the parent company annual financial statements and Group financial statements of Commerzbank Aktiengesellschaft as well as the management reports of the parent company and the Group. The auditors attended both meetings of the Audit Committee and the plenary Supervisory Board meetings, explaining the main findings of their audit and answering questions. At both meetings, the financial statements were discussed at length with the Board of Managing Directors and the representatives of the auditors. Following the final review by the Audit Committee and our own examination, we raised no objections to the parent company and Group financial statements and concurred with the findings of the auditors. The Supervisory Board has approved the financial statements of the parent company and the Group presented by the Board of Managing Directors; the financial statements of the parent company are thus adopted. We concur with the recommendation made by the Board of Managing Directors on the appropriation of profit.

T

o our Shar

eholders

Changes in the Supervisory Board and the Board of Managing Directors

The term of office on the Commerzbank Supervisory Board of Prof. Dr.-Ing. Dr.-Ing. E. h. Hans-Peter Keitel ended with effect from the end of the Annual General Meeting on 8 May 2014. The Annual General Meeting elected Nicholas R. Teller as his successor for the period from the end of the Annual General Meeting of 8 May 2014 until the end of the Annual General Meeting that passes a discharge resolution for financial year 2017. In addition, Dr. Marcus Schenck had earlier completed his term of office on the Supervisory Board on 10 September 2013. His place was taken by Solms U. Wittig as a substitute member of the Supervisory Board with effect from 11 September 2013. The 2014 Annual General Meeting elected Dr. Stefan Lippe as successor to Dr. Marcus Schenck for the period from the end of the Annual General Meeting of 8 May 2014 until the end of the Annual General Meeting that passes a discharge resolution for financial year 2017. With his election, Solms U. Wittig ceased to act as substitute member. Mr Wittig was also elected to the Supervisory Board as a substitute member for Mr Teller and Dr. Lippe by the 2014 Annual General Meeting. We wish to thank Prof. Dr.-Ing. Dr.-Ing. E. h. Keitel for his many years of close association with our bank and his highly dedicated cooperation with our Central Advisory Board and our Supervisory Board. We would like to thank the Board of Managing Directors and all our employees for their tremendous commitment and performance in 2014. For the Supervisory Board Klaus-Peter Müller Chairman

T o our Shar eholders

Klaus-Peter Müller

Age 70, Member of the Supervisory Board since 15.5.2008, Chairman of the Supervisory Board of Commerzbank AktiengesellschaftUwe Tschäge

1 Age 47, Deputy Chairman of the Supervisory Board since 30.5.2003, Banking professionalHans-Hermann Altenschmidt

1 Age 53, Member of the Supervisory Board since 30.5.2003, Banking professionalDr. Nikolaus von Bomhard

Age 58, Member of the Supervisory Board since 16.5.2009, Chairman of the Board of Management of Münchener Rückversicherungs-Gesellschaft AG

Gunnar de Buhr

1 Age 47, Member of the Supervisory Board since 19.4.2013, Banking professionalStefan Burghardt

1 Age 55, Member of the Supervisory Board since 19.4.2013, Head of Mittelstandsbank Bremen branchKarl-Heinz Flöther

Age 62, Member of the Supervisory Board since 19.4.2013, Independent management consultantDr. Markus Kerber

Age 51, Member of the Supervisory Board since 19.4.2013, Chief Executive Director of the Federal Association of German Industry (Bundesverband der Deutschen Industrie)Alexandra Krieger

1 Age 44, Member of the Supervisory Board since 15.5.2008, Head Business Administration/ Corporate Strategy Industrial Union Mining, Chemical and Energy (Industriegewerkschaft Bergbau, Chemie, Energie), Certified Banking Specialist and banking professionalOliver Leiberich

1 Age 58, Member of the Supervisory Board since 19.4.2013, Banking professionalMembers of the Supervisory Board

of Commerzbank Aktiengesellschaft

T o our Shar eholders

Dr. Stefan Lippe

Age 59, Member of the Supervisory Board since 8.5.2014, Former President of the Company Management of Swiss Re AGBeate Mensch

1 Age 52, Member of the Supervisory Board since 19.4.2013, Trade Union Secretary ver.di Region of the Federal State Hessen (Vereinte Dienstleistungsgewerkschaft ver.di), Organizational developmentDr. Roger Müller

Age 54, Member of the Supervisory Board since 3.7.2013, General Counsel Deutsche Börse AGDr. Helmut Perlet

Age 67, Member of the Supervisory Board since 16.5.2009, Chairman of the Supervisory Board of Allianz SEBarbara Priester

1 Age 56, Member of the Supervisory Board since 15.5.2008, Banking professionalMark Roach

1 Age 60, Member of the Supervisory Board since 10.1.2011, Trade Union Secretary ver.di Trade Union National Administration (Vereinte Dienstleistungsgewerkschaft ver.di)Petra Schadeberg-Herrmann

Age 47, Member of the Supervisory Board since 19.4.2013, Managing shareholder of Krombacher Finance GmbHMargit Schoffer

1 Age 58, Member of the Supervisory Board since 19.4.2013, Banking professionalNicholas Teller

Age 55, Member of the Supervisory Board since 8.5.2014, Chairman E.R. Capital Holding GmbH & Cie. KGDr. Gertrude Tumpel-Gugerell

Age 62, Member of the Supervisory Board since 1.6.2012, Former member of the Executive Board of the European Central BankT o our Shar eholders > > > > > > Mediation Committee (Art. 27, (3), German Co-determination Act)

Nomination Committee Social Welfare Committee

Committees of the Supervisory Board

Presiding Committee Compensation Control Committee

Klaus-Peter Müller Chairman

Audit Committee Risk Committee

Dr. Helmut Perlet Chairman

Klaus-Peter Müller Chairman

Hans-Hermann Altenschmidt Hans-Hermann Altenschmidt Gunnar de Buhr

Dr. Markus Kerber Karl-Heinz Flöther Dr. Markus Kerber

Uwe Tschäge Margit Schoffer

Dr. Gertrude Tumpel-Gugerell Dr. Helmut Perlet Dr. Stefan Lippe Klaus-Peter Müller Chairman Klaus-Peter Müller Chairman Klaus-Peter Müller Chairman

Hans-Hermann Altenschmidt Dr. Nikolaus von Bomhard Hans-Hermann Altenschmidt

Dr. Markus Kerber

Nicholas Teller

Uwe Tschäge

Gunnar de Buhr Nicholas Teller

Petra Schadeberg-Herrmann

Stefan Burghardt Uwe Tschäge

T o our Sh a reh ol der s

Development of equity markets and

performance indices

The US and European stock markets reached new record levels in 2014, although full-year gains were not as high as in 2013. The major central banks were once again the biggest driving force behind this stock market performance via their policy actions aimed at supporting global economic growth. The stock markets began heading towards new record highs after the ECB’s meeting in early June, at which it cut its key lending rate to a record low level of 0.15% and imposed a negative interest rate of –0.10% for deposits with the central bank. The DAX hit a new all-time high of 10,051 points on 20 June, with the Dow Jones also reaching a new record at the start of July. The capital markets were unsettled in July by the crisis in Ukraine and the ensuing EU sanctions against Russia. The flare-up of conflict in the Middle East also provoked fears, and the DAX tumbled more than 10% from its record high to 9,009 points. The stock markets rallied again in September, only for the DAX to fall back to a low for the year of 8,571 points in October. The weak state of the economy was once again the

decisive influence on the markets. German business sentiment deteriorated for the sixth successive month in October, as the ifo business climate index fell to its lowest level since December 2012. There was a surprise upturn in German business confidence in November, however, as the weak euro boosted exports and low oil prices also had a positive impact. The ifo business climate index also began to move higher again. The ECB’s expansive monetary policy drove yields on ten-year German government bonds down from 1.95% at the start of January to 0.55% at year-end. In this environment, the DAX set a new record high of 10,087 points on 5 December. On Wall Street, the robust US economy also led the Dow Jones to reach a new record of just under 18,000 points.

However, fears of a fresh economic setback mounted in December. The markets in Europe in particular were disquieted when Greek presidential elections were brought forward and the economic crisis in Russia gathered further speed. There was ultimately no year-end rally, and the DAX hovered below the 10,000-point mark. It ended the year at 9,806 points, up just 2.6% over the previous year, compared with a gain of 25.5% in 2013.

Figure 1 70% 80% 90% 100% 110% 120%

Commerzbank DAX EURO STOXX Banks Commerzbank share vs. Performance indices in 2014 Daily figures, 30.12.2013 = 100

130%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

70% 80% 90% 100% 110% 120%

Commerzbank DAX EURO STOXX Banks Commerzbank share vs. Performance indices in 2014 Daily figures, 30.12.2013 = 100

130%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Positive full-year trend in the average

Commerzbank share price

At the start of 2014, bank stocks benefited from renewed hopes of further monetary policy easing. The ECB gave the financial markets express reassurance that interest rates would be kept low for the long term and remained open to the possibility of further adjusting monetary policy. The banking supervisors also resolved that Europe’s banks would in future need much less capital to back artificial financial products (derivatives), such as equity options and commodity