Volume 30, Issue 4

Are Mergers a Solution to Bank Distress in MENA Countries?

Jean-michel Sahut

Amiens School of Management and CEREGE EA 1722 University of Poitiers

Medhi Mili

University of Poitiers & University of Sfax

Abstract

This paper studies bank distress in MENA countries and investigates whether mergers are commonly considered as a solution for resolving individual bank distress. Both specific bank levels and macro variables are deployed to predict banking distress. In line with other recent papers, we challenge the view that specific bank indicators such as CAMEL ratings and bank size are significant determinants of bank distress. Our findings indicate that monetary policy

indicators do not appear to affect bank distress in MENA countries. Overall, we suggest that bank capitalization and regulatory supervision need to be given sufficient consideration to avoid individual distress in the banking sector. Our empirical study shows that 67% of distressed banks in our sample are involved in merger transactions and that poor financial status systematically increases the likelihood of a bank being involved in a merger. Distressed state-owned banks and large-sized banks are less likely to be targets for merger transactions. However, global economic conditions do not seem to affect the decision of distressed banks to initiate a merger policy.

Citation: Jean-michel Sahut and Medhi Mili, (2010) ''Are Mergers a Solution to Bank Distress in MENA Countries? '', Economics Bulletin, Vol. 30 no.4 pp. 2627-2641.

Submitted: Apr 29 2010. Published: October 07, 2010.

1. Introduction

Financial systems in MENA countries are dominated by banks and, in some economies, by state-owned banks. The banking system is one of the most closely supervised industries in the MENA region, reflecting the view that bank distress has a greater adverse impact on economic activity than other business failures. Studies on the health of the banking sector in MENA countries have been a major concern for both bankers and international organisations, including the IMF and the World Bank. The fact that the MENA banking sector is dominated by state-owned banks and characterized by a high degree of government intervention and a lack of independence of the central banks in most countries means that banks are well-protected against failure. This paper focuses on the cases of distressed banks in order to identify specific banking factors and macroeconomic indicators that impact on the probability of bank distress in MENA countries. Bank distress is related to the present weak level of capitalisation, solvency and liquidity. We also look at whether bank mergers in this area may be considered as a solution for distressed banks. Most studies that analyze bank distress at micro and macro level, such as those developed by Altman (1977), Cole and Gunther (1995), Meyer and Pifer (1970), Calomiris and Mason. 2000, Oshinsky and Olin (2006), de Graeve, Koetter and Kick (2008), focus on the developed countries, especially the U.S. banking industry. Relatively little empirical work has examined developing countries. Daley, Matthews and Whitfield (2008) suggest that the failure of banks may be more interesting in the case of developing countries, where banks play a key role in financing the economy. Laeven (1999), Bongini, Classens and Ferri (2001), and Arena (2005), among others, studied bank distress in East Asia following the severe financial crisis experienced in 1997 that led to a number of bank failures. This paper contributes to the literature in this context by developing the first comparative empirical study using micro and macro data that take into account the troubled economic period between 2000-2007 in MENA countries, in order to address the following three questions: (i) To what extent do individual bank conditions explain bank distress? (ii) Is it mainly the macro economic fundamentals that explain bank distress? (iii) Are mergers the commonest solution for distressed banks in the MENA region? As far as we known, no studies have conducted a detailed investigation of individual banking distress in the MENA region to date.

In this paper we examine the determinants of individual bank distress in MENA countries, together with bank merger operations as a solution for troubled banks. We use bank-specific information suggested by the CAMELS rating technique to estimate individual probability of bank distress.1 The CAMELS method encompasses some useful measures of financial performance and includes the five components of a bank's condition in its assessment: Capital adequacy, Asset quality, Management, Earnings, Liquidity and sensitivity to market risk. We apply a cross-sectional multivariate logit model to assess whether specific bank fundamentals are important in explaining bank failures. We find that traditional, CAMELS-type variables, capital to loan loss reserves, loan growth, net interest income to total revenue, return on assets, and loan loss provision can help predict subsequent bank distress.

In the next step, we estimate the individual probabilities of bank failure as a function of both micro and macro variables. We show that economic country fundamentals, such as real interest rate and exchange rate do not significantly impact on the probability of bank distress. This paper assembles a rich disaggregated dataset capable of linking fundamental sources of banking weakness – individual bank portfolios and liability structure and condition, and Macro economic fundamentals – to the process of bank distress. We then look at strategies adopted by distressed banks to resolve distress. We address the issue as to whether mergers are commonly considered as a solution for troubled banks in MENA countries to resolve distress. We show that a distressed bank’s likelihood of being involved in a merger is systematically related to its financial status.

The rest of the paper is organized as follows: section 2 sets out our motivation and reviews the literature on banking distress. Section 3 presents the methodology, describes the data used and provides selection criteria of distressed banks. Section 4 analyzes the contribution of bank specific factors and macro

1 The CAMELS rating system is a method of evaluating the health of credit unions by the National Credit Union Administration.

variables in explaining the probability of individual bank distress through logit models. Section 5 tests the hypothesis that mergers are a solution adopted by troubled banks to resolve distress. Section 6 concludes.

2. Motivation and empirical review

In this section, we present a brief review of the financial literature dedicated to explaining bank distress and we investigate to what extent the literature has explored the adoption of banking merger as a solution to resolve banking distress.

2.1. Bank distress literature

Further to the wave of bank failures since 1990 which have affected many financial centres worldwide, banking distress has been of major interest in the field of economics. Certainly, the interest in banking distress is greater in regions where the banking sector dominates the financial system. In such cases, the banking sector constitutes the prime source of financing economic growth in these regions. In this paper we attempt to characterise the fundamental factors that determine banking distress in MENA countries. We also focus on mergers of troubled banks as a solution for distress.

We began our study by exploring the literature on predicting individual financial institutions' distress and closures. Models have been developed to try to predict the failure of individual financial institution (early warning systems) since the 1970s. Mainly applied to banking systems in developed countries, these studies focus on the early identification of financial institutions developing financial difficulties. From the viewpoint of banking regulators and supervisory agencies, early warning systems can help minimize the use of relatively scarce examination resources, while at the same time introducing as much failure-prevention as possible. Indeed, failure prediction models and early warning systems have proven important tools for supervisory agencies to schedule individual on-site bank examinations and initiate remedial action.

The first generation of financial early warning systems aimed to build screening devices to help schedule bank examinations by flagging institutions in financial distress as early as possible. These studies share a similar approach (Meyer and Pifer 1970; Sinkey 1975; Altman 1977; Martin 1977; Pettaway and Sinkey 1980; see Altman 1981 for a comprehensive survey of the early wave of the literature): on the basis of a set of financial ratios which reflect the different dimensions of a CAMELS rating system,the statistically best subset of variables is chosen to distinguish between potentially financially-troubled and sound financial institutions, within a certain prediction horizon.

A certain number of studies that attempt to empirically identify the causes and origins of banking system2 weakness have mainly focused on the macro-economic factors that can help predict banking crises. Macro-economic variables through factors such as inflation and changes in interest rates may either enhance or distress the financial performance of banks. Cordella and Levy Yeyati (1998) point out that if there are widespread shocks to the economy and banks cannot control their asset portfolio risks, then full transparency of the bank’s risk positions may destabilize the banking system. A country’s macro economic environment may also affect transparency levels, making it difficult to relate to the financial performance of commercial banks.

Early warning systems based on macro variables are important tools for the timely detection of systemic bank distress. However, they do not analyse the impact of individual bank factor weaknesses which contribute to the occurrence of the distress. In particular, they are unlikely to be able to discriminate between the view that distressed banks have been hit by exogenous shocks, or the view that many specific weakness factors may have led to the systemic financial distress.

Wheelock and Wilson (1995), Natalia (2006) and Koetter, de Graeve and Kick (2008), among others, suggest that studies that focus on bank distress from a macro-economic perspective have several limitations. In particular, macro-economic studies leave policymakers with insufficient information as to which banks are the most fragile and vulnerable within the system. This may lead to policymakers dealing

2

See Lee Jong-Kun (2002) for study explaining MENA banking system weakness using macroeconomic fundamentals. See also Corsetti, Pesenti, and Roubini (1998), Kaminsky and Reinhart (1999), Radelet and Sachs (1998), Demirgüç-Kunt and Detragiache (1999) for details about developed banking system with macro-economic variables.

with financial sector problems at aggregate level, introducing policies that might affect both weak and healthy banks in less than optimal ways.

Our study contributes to the existing literature by explaining the reasons for bank distress in MENA countries using both macroeconomic fundamentals and specific bank factors.

Studies that have explored the micro-level and specific factors, looked at bank distress in specific countries or even regions, using cross-section, micro-level data. Wheelock and Wilson (1995) adopted proportional hazard models to study the state-chartered Kansas banks between 1910 and 1928. Together with micro variables, critical for a bank's stability, they include dummy variables for deposit insurance membership and technical efficiency estimates as a proxy for managerial quality. Their findings indicated that insured banks were more likely to fail, supporting the moral hazard hypothesis, while more efficient banks were more likely to stay in business. In a recent study, De Graeve, Kick and Koetter (2008)

suggest an integrated micro–macro approach with two core virtues. First, they measure financial stability directly at the bank level as the probability of distress. Second, they integrate a microeconomic hazard model for bank distress and a standard macroeconomic model. The advantage of this approach is to incorporate micro information, to allow for non-linearities and to permit general feedback effects between financial distress and the real economy. They confirm the existence of a trade-off between monetary and financial stability. An unexpected tightening of monetary policy increases the probability of distress.

2.2. Banking distress and merger

Banking distress is generally the result of banking insolvency and undercapitalization. A strategic decision often needs to be taken by the troubled bank’s government in order to resolve the distress. Financial distress will, for example, often be resolved via mergers that are supervised, encouraged and supported. Mergers are seen as an administrative option that owners may or may not choose to exercise, even when the bank is economically insolvent. Merger and acquisition of distressed banks is a strategic decision largely evoked in the literature as a solution for distress. Berger and Humphrey (1992), Peristiani (1993), and DeYoung (1997) among others indicate that merger and acquisitions tend to be successful in improving the profitability and efficiency of banks.

Banks have different reasons as to why they engage in mergers. Hadlock et al., (1999) and Bliss and Rosen (2001) suggest that business motives play an important role in bank merger transactions. With regard to mergers driven by business motives, Berger (1998) distinguishes between the relative efficiency hypothesis and the low efficiency hypothesis. Under the relative efficiency hypothesis, the acquiring bank tries to bring the target bank back to its own higher level of efficiency by transferring its superior management capacities or its business procedures. Under the low efficiency hypothesis, one or both of the merging banks are inefficient relative to their peers. The merger may therefore serve as a disciplinary device for the banks’ management to improve the banks’ performance or as a means of implementing unpleasant business measures. Hoggarth and Reidhill and Sinclair (2003) note that there is a range of options for resolving insolvent banks. At one extreme, a bank can be kept open through an injection of capital. At the other extreme, a bank can be closed with its assets sold and depositors and possibly other creditors paid off. Between these extremes, a bank’s licence may be removed but with the bank sold off to another bank, in full or in part, to preserve the bank’s activities.

Pasiouras, Tanna and Zopounidis. (2007) develop classification models for the identification of acquisition targets in the EU banking industry, incorporating financial variables that are mostly unique to the banking industry and originate from the CAMELS approach. They state that in general after adjusting for the country where banks operate, acquired banks are less well capitalized and less cost and profit efficient.

In our analysis of the literature on bank mergers we focused on bank merger as a solution to resolving bank distress. We attempted to identify key factors that characterise the distressed banks most likely to be subject to a merger. We considered both bank-specific factors and macro variables to detect which factors affect the merger decisions of distressed banks.

3. Methodology, data and identification of distressed banks

In this paper we estimate two logit models. The first predict the probability of bank distress and the second predict the probability that the distressed banks will be involved in a merger.

3.1. Methodology

Empirical work on bank distress prediction shares the following approach. First, the dependent variable is constructed on the basis of ex-post information on bank distress. Typically, the dependent variable is a dummy variable that distinguishes between distressed and non distressed banks. Second, the explicative variables are a subset of bank-specific indicators that generally refer to the six CAMELS categories and country-specific indicators reflecting the macroeconomic situation of banks.

We use a qualitative response logit model to estimate the probability of the occurrence of distress as a function of a vector of independent variables, X, and a vector of unknown parameters, θ. The specific model we use is:

)] , ( [ ) 1 Pr(Yi = =F H X q (1)

Where Yi is the dependent variable which takes the value of one if the bank has experienced distress and zero otherwise; F is the probability function, which has a logistic functional form, giving rise to the logit model;

å

= + = M j ij j i X H 1 0 q q (2)Xi is the vector of explanatory variables for the i-th individual bank; and θ is the vector of parameters to

be estimated.

The basic equation of the logit model to be estimated can be written as:

i H i i e X H F Y -+ = = = 1 1 )] , ( [ ) 1 Pr( q (3)

We estimate two different logit models using maximum likelihood techniques. In the first model, the dependent variable takes the value of one when a financial intermediary experiences distress and zero otherwise. Here, we have 330 observations,which include 275 non-distressed and 55 distressed banks. In the second model, we only study the strategic decision of distressed institutions. Here we have 55 observations,which include 37 merged and 18 non-merged banks. This model enabled us to estimate the probability of merger with respect to distress. We consider both bank specific indicators and macro variables to investigate which characteristics make a bank more attractive as an acquisition target.

3.2. Data sources and identification of distressed banks

We investigated the distress and subsequent merger decisions for 330 banks from the MENA region during the period 2000-2007. During this period, the MENA region was marked by a highly turbulent political, economic and financial climate, including the Iraq war in 2001 and the Iranian nuclear crises in 2007. These events had both direct and indirect impacts on the banking industry in some countries. We did not exclude countries affected by wars, embargo or political crisis (e.g. Iraq, Iran, etc.) since bank distress is explained in this paper by economic variables. The micro-data of distressed and non-distressed banks used in our sample comes from the Bankscope database, published by the Bureau van Dijk. Macroeconomic data used for each country are collected from the International monetary fund database.

A bank is identified as being in distress when at least one of the following criteria is met according to the information from the BankScope database: bankruptcy, dissolved merger, in liquidation, the fourth quartile of loan loss provision (for two successive years).

To identify distressed banks through the fourth criteria, we constructed quartiles of loan loss provisions in the cross-section of banks on a yearly basis. We define a distressed bank as one which finds itself in the highest quartile of loan loss provisions over two successive years.

4. Prediction of bank distress probabilities

We have tried to analyse both the bank-specific and the macroeconomic conditions that contribute to bank distress. In our bank-specific variables selection we use the financial ratios found extensively in the empirical literature on banking industry and related to the CAMELS rating system.

In this section we develop and estimate a bank distress prediction model for the MENA countries’ banking sector. We use a multivariate logit model to estimate the probability of bank distress and to

identify key explanatory factors that influence it. We include a set of micro and macro-level variables in our estimation. The micro-level variables refer to the six CAMELS categories: Capital adequacy, Asset quality, Management quality, Earnings and Liquidity which are now used extensively by regulators to evaluate a bank’s financial health.

Capital Adequacy: Capital adequacy in banks is measured in relation to the relative risk weights assigned to the different category of assets held both on and off the balance sheet items. We use three ratios to evaluate capital adequacy: Equity/Total Asset, Equity/Total loans, Equity+Loan Loss Reserve/Loans and hypothesize that better capitalised banks are less exposed to distress.

Asset Quality: The solvency of financial institutions is typically at risk when their assets become impaired, so it is important to monitor their asset quality indicators in terms of overexposure to specific risk trends in non-performing loans, and the health and profitability of bank borrowers, especially in the corporate sector. We use two indicators to evaluate Asset Quality, namely, Loan Loss Reserve / Gross Loans ratio, which evaluates the proportion of bad loans over total loans (a high ratio is supposed to mean poor asset quality, but in fact it depends on whether the information on ‘bad loans’ is correctly revealed), and secondly, Loans Growth, which indicates an increase in the misallocation risk of banking asset caused by the growth in loans.

Managerial quality: we use an Efficiency score to assess management quality. We expect more efficient banks to be less likely to be distressed. Following Wheelock and Wilson (1995), we use the non-parametric linear programming approach (DEA) to estimate the individual efficiency of each bank to later be included in a logit model as proxies for managerial quality.

The variables used in the estimation are presented in Table 1. Note that in choosing inputs and outputs, we follow the intermediation approach,3 according to which banks are viewed as intermediaries whose primary objective is to transform deposits into loans. This approach accepts monetary balances rather than physical units as a measure of inputs and outputs.

First, we computed the efficiency scores for each bank in the sample with the help of a Data Envelopment Analysis. We constructed a frontier for each year separately and the resulting scores were then added to the data sets.

Two other indicators are also used to evaluate a bank’s managerial quality. A governance indicator indicates if a bank is state owned or non-state owned. Nakane and Weintraud (2005) suggested that s tate-owned banks face severe agency problems due to their inherent political and social purposes. We consider Total Expenses to Total Revenue ratio as a managerial quality indicator. A higher ratio indicates inefficient bank management and increase the probability of bank distress.

Earnings: Good earnings performance enables a bank to fund its expansion, remain competitive in the market and replenish and /or increase its capital. We use five Earning indicators for banks: Return on Assets (ROA), Return on Equity (ROE), Net Interest Income/Total Revenue, Loan Loss Provision and Personnel Expenses. A number of authors have agued that healthier banks have: higher return on assets (ROA), better return on equity (ROE) and higher net interest income to total revenue.

Liquidity: Initially solvent financial institutions may be driven to closure by poor management of short-term liquidity. We use the Deposit/Total Assets ratio as an indicator of bank liquidity. Perfect liquidity implies that liabilities ranked by maturity be matched by corresponding assets. The size of deposits (short term liabilities) over total assets gives a rough estimate of liquidity risk, associated with deposit withdrawal.

Sensitivity to Market Risk:The sensitivity to market risk is assessed by the degree to which changes in market prices, notably interest rates, exchange rates, commodity prices, and equity prices adversely affect a bank’s earnings and capital. We consider the following ratios to measure the sensitivity of banks to market risk; Net Interest Income/Total Assets, and Foreign Exchange Position/Equity.

We consider size among bank specific explanatory variables other than the non-CAMELS-type. Bongini Claessens and Ferri (2001) argue that in terms of probability of distress, a larger financial institution might

3

There are two widely used approaches to examine a bank's input-output process. In the first, the so-called production approach, banks are treated as firms which employ capital and labour to produce different types of deposit and loan accounts. In the second, the so-called intermediation approach, banks are viewed as intermediates of financial services rather than producers of loan and deposit account services.

have a lower chance of becoming distressed if it is more diversified and less exposed to liquidity shocks. On the other hand, the likelihood of distress probably increases if the bank has been more subject to distortionary effects, including political intervention. As regards closure, we imagine that the authorities would consider large intermediaries “too big to fail.”

With regard to the macroeconomic variables used in our model to predict bank distress, we consider Real interest rate growth (RINT) which could signal that the economy is overheating and there is a possibility of a worsening economic environment in the near future. In this context, the more bad loans there are, the more funds are needed to write them off, in turn making the banks more vulnerable. So we assume that a coefficient in this variable would be a positive sign.

We also include GDP (Gross Domestic Product), CPI (Consumer Price Index) and EXRT (Exchange rate). Rising GDP usually signals a healthy economy and should reduce the probability of distress. Studies have observed that the quality of bank loans deteriorates when the business cycle is in a downward trend. Kaminsky and Reinhart (1999) find that slowdown in output is one of the best indicators of banking crises.

Rising CPI indicates inflation, which often works in a bank's favour - their assets are re-priced faster than their liabilities, and inflation reduces the real value of nonperforming loans. So, we would expect CPI to have a negative effect on distress. Depreciation of domestic currency increases risk exposure, which has a positive impact on the banks’ fragility. Kaminsky and Reinhart (1999) reported that a devaluation of the local currency increases the probability of banking crisis. Thus, the exchange rate coefficient is expected to be positive.

Table 2 summarizes both CAMELS and macroeconomic variables, along with the expected signs of their impact on the likelihood of a bank's distress. Table 3 reports summary statistics of bank specific indicators for all banks in MENA countries. In order to deduce some preliminary results about the banks’ characteristics, we also report descriptive statistics for distressed and non distressed banks. The table suggests that distressed banks showed early signs of vulnerability. Regarding asset risk, distressed banks have lower capitalization while non distressed banks showed a higher ratio of loan loss reserves + equity to total loans, and a higher ratio of equity to total loans, than distressed banks. So, distressed banks are less able to absorb negative shocks given their higher leverage. This preliminary result shows that not only high lending but also bad lending characterizes troubled banks.Non distressed banks are found to have higher personnel expenses and are smaller in size. In contrast with our hypotheses, distressed banks show lower loan growth.

Non distressed banks have a higher efficiency score, which leads us to suggest that management quality is determinant with respect to the probability of bank distress. In addition, distressed banks showed lower profitability (return on assets and return on equity), which makes it more difficult for them to increase their capital base and improve their viability. Regarding liquidity, distressed banks appear less liquid as they have a higher deposit to total assets ratio, which makes them less able to withstand unexpected deposit withdrawals.

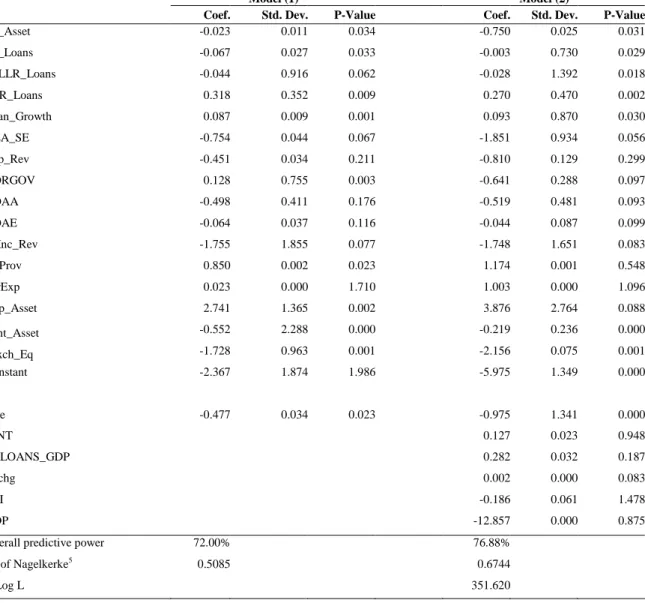

Table 4 summarizes the results of the model used to estimate probability of bank distress in MENA countries. The dependent variable takes the value of 1 if the bank is identified with any of the categories of distress during the periods of study.

Model (1) of Table 2 contains the results of the logit model estimation explaining the probability of bank distress using only bank-specific indicators. The model shows good predictive power, and thus 72% of banks were correctly classified. The results confirm that bank-level fundamentals not only significantly affect the likelihood of bank failure, but also explain a high proportion of the likelihood of distress for distressed banks (over 50%).

All Capital adequacy variables are correctly signed. Eq_TAsset and Eq_Loans variables appear significantly negative, implying that higher capitalization has a negative impact on the probability of distress as the bank will be better able to absorb losses. According to these results, higher capital relative to assets or liabilities is negatively associated with the probability of distress.

The LLR_Loans variable is significantly positive, which implies that a higher share of loan loss reserves in overall capitalization has a positive impact on distress. This result confirms those of Bongini Claessens and Ferri (2001) who suggest that as financial institutions made (albeit inadequate) provisions for loan-losses in response to the riskiness of their loans, the share is a useful predictor of institutions which may run into distress.

Regarding Assets and Management qualities, Model (1) also shows that higher loan growth tends to increase the probability of distress significantly, while a higher ROA, a higher ROE and a higher share of net interest income in total income tends to reduce it. These variables, however, do not impact significantly on the probability of distress.

The ownership variable appears significantly positive. We deduce that privately owned banks are more likely to become distressed, suggesting that flight to safety and access to financing by state-owned banks are mitigating factors. State-owned banks may benefit from depositors' flight to safety-domestic deposits, shifting from non-state-owned to state-owned financial institutions, and may have easier access to financing during a crisis as they are perceived as more likely to receive support in case of distress. Our results confirm those reported by Natalia (2006) for the Russian banking system. He found that higher government securities holdings together with greater profitability were significant determinants of soundness.

The logarithm of total assets, a measure of size, is significant and has a negative sign. The negative significant coefficient probably reflects an actual or perceived size-related diversification benefit. In line with conclusion of Daley, Matthews and Whitfield (2008), we find that larger banks are associated with longer survival, which could be consistent with the “too-big-to-fail” hypothesis.

Quality of management is also associated with a lower probability of distress. As we can see, the efficiency coefficient is negatively significant at 10% level, proving our hypothesis that quality of management is very important in characterizing bank distress.

Our results show that interest income to total revenue and personnel expenses do not significantly impact on the probability of bank distress in MENA countries. Therefore, our results are not exactly the same as those reported by Bongini Claessens and Ferri (2001) who found that Net Interest income to total income were significant determining factors of bank distress, which is not true for our model.

As we can see, deposit to total assets is significantly positive, so liquidity appears to be a significant factor in influencing distress.

As expected, the two variables of sensitivity to market risk appear negatively significant. This implies that the terms of interest rates and exposure to exchange rate significantly affect the financial health of the bank and reduces its probability of distress. The diversification of the portfolio currency of the bank reduces the likelihood of its distress.

In model (2), both bank specific level and macro variables are deployed to predict bank distress. The estimation results reveal that adding macroeconomic variables to the model do not significantly improve it since none of them are statistically significant in the model apart from GDP growth. The predictive power of the model increases by just 4% compared to the model (1).

CPI variables, interest rate and exchange rate are correctly signed but appear insignificant. Our findings are contrary to those of Goldstein, Kaminsky and Reinhart (2000) who found appreciation of real exchange rate to be the best leading indicator of bank distress. However, the sign of total bank loans to the GDP variable is contrary to expectations and tends to have negative, insignificant effects on the probability of distress. As expected, increases in economic activity are associated with a lower probability of distress. This implies that rising GDP signals a healthy economy and reduces the probability of distress. Since any macro analysis of monetary policy issues typically includes at least GDP growth, interest rate and inflation, we deduce that monetary policy do not really impact on bank distress.

Our results are not exactly the same as de Graeve, Kick and Koetter (2008) who confirm the existence of a relationship between monetary policy and bank distress. They argue that a monetary contraction increases the mean probability of distress.

Our findings indicate that a strong banking system is crucial for financial stability and development in MENA countries. This means that the regulatory supervisor, namely central banks, should exercise prudential oversight, ensuring the financial soundness and solvency of individual banks. To this end, the monetary authorities should accelerate the adoption of the Basel II revised capital accord that establishes a spectrum of more risk-sensitive capital allocation and incentives for improving the quality of risk management in banks. In order to reduce the likelihood of individual banking distress, the adoption of Basel II and its three pillars strengthens the security and soundness of the financial system by reinforcing the emphasis on risk-based calculation of capital, the supervisory review process and market discipline. This is achieved by adjusting capital requirements to credit risk and operational risk, and introducing changes in the calculation of capital to cover exposure to risks of losses caused by operational failures.

5. Merger as a solution for distressed banks

In this section we test whether distressed banks in MENA countries adopt merger as a preferred solution to resolving distress. From the 55 distressed banks identified, 37 were involved in mergers (67% of distressed banks). We suggest that distress mergers are observable in MENA countries and that most distressed banks look to bank mergers as a strategy to resolve the financial distress of banks pre-emptively.

We use the same set of specific bank indicators and macro variables to detect the fundamental characteristics of banks most likely to be involved in mergers. In this section, our sample contains only the 55 distressed banks. We estimate a second logit model where the dependent variable equals zero if the distressed bank was not involved in a merger over the observed period, and one if the distressed bank was involved in a merger.

Table 5 reports the results of the logit estimation. Model (1) only considers bank specific variables, while model (2) incorporate both micro and macro variables. Let us begin with the specific bank conditions that precipitate distressed bank merger. Model (1) shows that measures related to bank-specific performances significantly affect the probability of being involved in a merger, apart from loans growth, net interest income to total revenue and personal expenses.

Equity to asset appears significantly negative, implying that under-capitalized banks are more likely to be involved in merger. The attraction of under-capitalised banks may be low acquisition prices because one basis for determining prices is book value, and capital is a major component of book value.

Lower profitability in terms of return on assets (ROA) and return on equity (ROE) increases the probability of becoming a target. These results can be interpreted as evidence of a market for corporate control in which poorly performing firms are acquired. These findings conflict with the evidence of other studies4 examining merger activity in banking as well as the industrial sector.

Taken together, these results suggest that a weak financial situation systematically affects the probability of merger involvement for banks, which is the necessary condition for the distress merger conjecture. The more distressed banks are, the more likely they are to be a target in a merger transaction.

The ownership structure variable appears significantly positive. This implies that state-owned banks are less likely to be involved in merger operations. Distressed state-owned banks have a lower probability of being targeted for merger or acquisition by healthier banks due to the possibility of government recapitalization and direct central bank intervention to reinforce their financial structure and clean up their asset accounts.

While there is weak evidence that the probability of being acquired is related to personal expense, in both models this variable has an insignificant coefficient.

This sensitivity to market risk has a significant impact on the probability of merger. This is supported by the significant coefficients of the two variables; Net Interest Income/Total Assets, and Foreign Exchange Position/Equity.

So remaining in business without a merger is largely defined by bank-specific factors such as large value of assets and CAMELS performance indicators.

Model (2) demonstrates that macroeconomic variables do not significantly affect the probability of an evolving bank merger. Thus, the global economic conjuncture does not appear to affect the decision of distressed banks to trigger a merger policy.

6. Conclusion:

Rapidly growing empirical literature continues to study the causes and consequences of bank distress in diverse economies. The present study developed a logit econometric model to identify a set of specific indicators and macroeconomic factors pertaining to individual bank distress and assessed the likelihood of bank distress in the MENA region. To rationally select bank-specific variables, we extensively adopted financial ratios from the empirical literature on the banking industry and related to the CAMELS rating system. The results of the logit models show that bank specific factors have a significant impact on the probability of bank distress. However from the macro factors used, only GDP growth significantly

increased individual bank distress. Yet, other monetary policy indicators such as real interest rates and CPI as shown do not appear to significantly increase banking distress in MENA countries. Given that global economic development affects the probability and timing of bank failure, banking regulations and supervision should also take into account the influence of macroeconomic developments on individual banks (i.e., assess the financial institution’s exposure to systemic shocks) in order to make the banking system more robust.

In this paper we also tested whether distressed banks in MENA countries looked to mergers as a solution to distress. We tested whether both micro and macro factors accounted for merger in distressed banks and found that 67% of the distressed banks in our sample were involved in merger transactions. The results indicate that a weak financial status significantly increases the likelihood of a bank being involved in a merger. Private distressed banks were found to have a higher likelihood of being involved in a merger. With respect to macroeconomic factors, we deduced that the global economic conjuncture does not affect the decision of distressed banks to initiate a merger policy.

Bibliography

Altman, E.I. (1977). Predicting performance in the Savings and Loan Association Industry. Journal of Monetary Economics, October (3): 443-66.

Altman, E.I. (1981). Application of classification techniques in business, banking and finance.Contemporary Studies in Economic and Financial Analysis. (3): JAI Press Inc.

Berger, Allen N. (1998). The Efficiency Effects of Bank Mergers and Acquisitions: A Preliminary Look at the 1990s Data. In Bank Mergers and Acquisitions. edited by Yakov Amihud and Geoffrey Miller, 79-111. Kluwer Academic Publishers.

Berger, A.N. and Humphrey, D.B. (1992). Megamergers in banking and the use of cost efficiency as an antitrust defense. The Antitrust Bulletin, Fall: 541-600.

Bliss, R. T., and R. J. Rosen. (2001). CEO Compensation and Bank Mergers. Journal of Financial Economics 61 (1). 107–38.

Bongini, P., S. Claessens, and G. Ferri. (2001). The Political Economy of Distress in East Asian Financial Institutions. Journal of Financial Services Research 19(1): 5–25.

Calomiris, C. and J. Mason. (2000). Causes of U.S. Distress During the Depression. NBER Working Paper No. 7919. Cole, R.A., and J.W. Gunther (1995). Separating the likelihood and timing of bank failure. Journal of Banking and

Finance. (19): 1073-1089.

Cordella, T. and Levy Yeyati, E., (1998). Public Disclosure and Bank Failures,. Centre for Economic Policy Research, Discussion Paper, No. 1886.

Corsetti, G., P. Pesenti, and N. Roubini (1998). What caused the Asian currency and financial crises?. Banca d'Italia, Temi di discussione n.343.

Deemirguc-KuntA, ., and E. Detragiache (1999). Monitoring banking sector fragility: a multivariate logit approach with an application to the 1996-97 banking crisis. World Bank, Policy Research working paper No. 2085.

Daley J, K. Matthews and K. Whitfield. (2008). Too-big-to-fail: Bank failure and banking policy in Jamaica, Journal of International Financial Markets, Institutions and Money, 18 (3): 290-303.

DeYoung, R. (1997). Bank mergers, X-efficiency and the market for corporate control. Managerial Finance. ( 23): 32-47. Goldstein, M., G. Kaminsky et C. Reinhart, (2000). Assessing Financial Vulnerability, An Early Warning System for

Emerging Markets. Institute for International Economics, Washington (D.C.).

De Graeve F., T.homas Kick and M. Koetter. (2008). Monetary policy and bank distress: an integrated micro-macro approach. Discussion Paper. Deutsche Bundesbank Series 2: Banking and Financial Studies, No 03/2008

Hadlock, C., J. Houston, and M. Ryngaert, (1999). The Role of Managerial Incentives in Bank Acquisitions. Journal of Banking and Finance. (23): 221–49.

Hoggarth, G, Reidhill, J and P. Sinclair, (2003). Resolution of banking crises: a review. Bank of England Financial Stability Review: 109-123.

Kaminsky, G., and C. Reinhart, (1999). The Twin Crises: the Causes of Banking and Balance-of-Payments problems. American Economic Review. 89. (3): 473-500.

Koetter, M., J. W. B. Bos, F. Heid, J. W. Kolari, C. J. M. Kool, and D. Porath, (2007). Accounting for Distress in Bank Mergers. Journal of Banking and Finance. 31 (10): 3200-3217.

Laeven, L, (1999). Risk and Efficiency in East Asian Banks. World Bank Working Paper No. 2255.

Lee. Jong-Kun, (2002). .Financial Liberalization and Foreign Bank Entry in MEN. Financial sector Strategy and Policy World Bank Working paper.

Arena Marco, (2005). “Bank Failures and Bank Fundamentals: A Comparative Analysis of Latin America and East Asia during the Nineties using Bank-Level Data,” Bank of Canada Working Papers with number 05-19, http://www.bankofcanada.ca/en/res/wp/2005/wp05-19.pdf

Martin, D. (1977). .Early warning of bank failure: a logit regression approach. Journal of Banking and Finance. 1. (3): 249-276.

Meyer, P. and W. Pifer, (1970).Prediction of Bank Failures. Journal of Finance. (25): 853–868.

Nakane M. I. and Weintraub D. B. (2005). Bank Privatization and Productivity: Evidence for Brazil. World Bank Policy Research Working Paper 3666.

Natalia. Konstandina, (2006). Probability of Bank Failure: The Russian Case. EERC Research Network, Russia and CIS with number 06-01e.

Oshinsky, R. and V. Olin, (2006). roubled Banks: Why Don't They All Fail?. FDIC Banking Review. 18. (1): 23-44. F. Pasiouras, S. Tanna and C. Zopounidis. (2007). The identification of acquisition targets in the EU banking industry: An application of multicriteria approaches, International Review of Financial Analysis, 16 (3): 262- -281.

Peristiani, S. (1993). The effects of mergers on bank performance. Federal Reserve Bank of New York Studies on Excess Capacity in the Financial Sector, March 1993.

Pettaway, R.H., and J.F. Sinkey, (1980). Establishing on-site bank examination priorities: an early warning system using accounting and market information. Journal of Finance. (35):137-50.

Radelet, S., and J. Sachs (1998). The East Asian Financial Crisis: Diagnosis, Remedies, Prospects. Brooking Papers on Economic Activity 1:1-90, Washington, D.C., Brookings Institution.

Sinkey, J. (1975). A multivariate statistical analysis of the characteristics of problem banks. Journal of Finance. (30): 21-36.

Wheelock, D. and P. Wilson, (1995). Explaining Bank Failures: Deposit Insurance, Regulation, and Efficiency. Review of Economics and Statistic. (77): 689–700.

Appendix

Table 1. Variables used for DEA model

Variable definition

X1 Personnel Expenses

X2 Total Fixed Assets

X3 Deposits

X4 Other expenses

Y1 Total loans

Y2 Non interest income

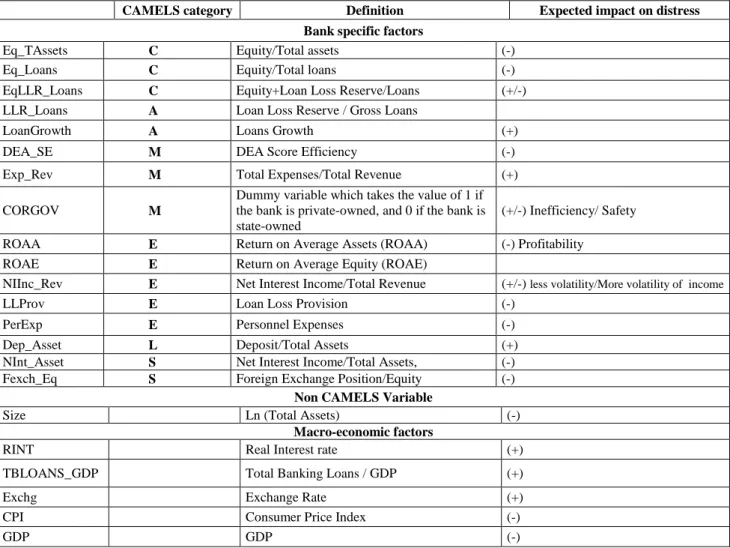

Table 2. Explanatory variables and expected signs for predicting probability of distress

CAMELS category Definition Expected impact on distress Bank specific factors

Eq_TAssets C Equity/Total assets (-) Eq_Loans C Equity/Total loans (-) EqLLR_Loans C Equity+Loan Loss Reserve/Loans (+/-) LLR_Loans A Loan Loss Reserve / Gross Loans

LoanGrowth A Loans Growth (+) DEA_SE M DEA Score Efficiency (-) Exp_Rev M Total Expenses/Total Revenue (+)

CORGOV M

Dummy variable which takes the value of 1 if the bank is private-owned, and 0 if the bank is state-owned

(+/-) Inefficiency/ Safety ROAA E Return on Average Assets (ROAA) (-) Profitability

ROAE E Return on Average Equity (ROAE)

NIInc_Rev E Net Interest Income/Total Revenue (+/-) less volatility/More volatility of income

LLProv E Loan Loss Provision (-) PerExp E Personnel Expenses (-) Dep_Asset L Deposit/Total Assets (+) NInt_Asset S Net Interest Income/Total Assets, (-) Fexch_Eq S Foreign Exchange Position/Equity (-)

Non CAMELS Variable

Size Ln (Total Assets) (-)

Macro-economic factors

RINT Real Interest rate (+) TBLOANS_GDP Total Banking Loans / GDP (+) Exchg Exchange Rate (+) CPI Consumer Price Index (-)

Table 3: Summary statistics of all banks, Non-distressed banks and distressed banks

All Banks Non Distressed Banks Distressed Banks Mean Std. Dev Mean Std. Dev Mean Std. Dev Equity/ Total assets 14,046 59,991 16,841 56,087 11,386 83,975 Equity/Total loans 5,618 76,823 7,622 39,877 3,451 16,512 Equity+Loan Loss Reserve/Loans 19,015 28,579 20,759 30,017 14,257 87,679 Loan Loss Reserve / Loans 8,916 11,156 8,456 10,862 11,345 12,345 Loan Growth 23,771 204,869 25,598 218,332 13,933 106,126 Total Assets 13,172 1,915 13,460 1,932 13,817 1,781 DEA Score Efficiency 0,736 0,153 0,743 0,153 0,697 0,143 Total Expenses/Total Revenue 2,999 30,472 60,139 97,801 44,672 43,336 Return on Average Assets (ROAA) 2,784 4,492 3,058 4,808 1,357 1,586 Return on Average Equity (ROE) 15,668 31,134 18,126 27,971 15,469 46,683 Net Interest Income/Total Revenues 0,795 0,366 0,800 0,394 0,772 0,157 Loan Loss Provision 12,943 1,961 13,013 1,935 12,569 2,057 Personnel Expenses 5720,109 15,734 6026,516 15,691 3934,101 15,535 Deposit/Totat Assets 0,723 0,352 0,706 0,377 0,804 0,159 NInt_Asset 3,182E-4 0.000 9,960E-4 0.003 0,174E-4 0.955 Fexch_Eq 5,914E-5 0.039 6,8410E-5 0.021 3,865E-5 0.037

Table 4: Results of Logit model regression of distress determinants for MENA Banks

Model (1) Model (2)

Coef. Std. Dev. P-Value Coef. Std. Dev. P-Value

Eq_Asset -0.023 0.011 0.034 -0.750 0.025 0.031 Eq_Loans -0.067 0.027 0.033 -0.003 0.730 0.029 EqLLR_Loans -0.044 0.916 0.062 -0.028 1.392 0.018 LLR_Loans 0.318 0.352 0.009 0.270 0.470 0.002 Loan_Growth 0.087 0.009 0.001 0.093 0.870 0.030 DEA_SE -0.754 0.044 0.067 -1.851 0.934 0.056 Exp_Rev -0.451 0.034 0.211 -0.810 0.129 0.299 CORGOV 0.128 0.755 0.003 -0.641 0.288 0.097 ROAA -0.498 0.411 0.176 -0.519 0.481 0.093 ROAE -0.064 0.037 0.116 -0.044 0.087 0.099 NIInc_Rev -1.755 1.855 0.077 -1.748 1.651 0.083 LLProv 0.850 0.002 0.023 1.174 0.001 0.548 PerExp 0.023 0.000 1.710 1.003 0.000 1.096 Dep_Asset 2.741 1.365 0.002 3.876 2.764 0.088 NInt_Asset -0.552 2.288 0.000 -0.219 0.236 0.000 Fexch_Eq -1.728 0.963 0.001 -2.156 0.075 0.001 Constant -2.367 1.874 1.986 -5.975 1.349 0.000 Size -0.477 0.034 0.023 -0.975 1.341 0.000 RINT 0.127 0.023 0.948 TBLOANS_GDP 0.282 0.032 0.187 Exchg 0.002 0.000 0.083 CPI -0.186 0.061 1.478 GDP -12.857 0.000 0.875

Overall predictive power 72.00% 76.88%

R2-of Nagelkerke5 0.5085 0.6744

-2Log L 351.620

5

Table 5. Results of Logit Regressions of Determinants of Bank Merger for MENA banks

Model (1) Model (2)

Coef. Std. Dev. P-Value Coef. Std.Dev. P-Value

Eq_Asset -0.031 0.298 0.002 -0.741 0.186 0.008 Eq_Loans -0.082 0.120 0.027 -0.388 0.172 0.099 EqLLR_Loans 0.268 0.141 0.031 0.778 0.389 0.362 LLR_Loans -0.045 0.000 0.009 0.486 0.000 0.085 Loan_Growth 1.160 1.986 0.061 -1.827 3.967 0.711 DEA_SE -0.001 0.039 0.000 -0.795 0.764 0.882 Exp_Rev 1.037 1.968 0.000 1.875 2.092 0.457 CORGOV 0.893 1.875 0.009 0.799 1.073 0.671 ROAA -3.641 0.673 0.000 -2.8751 3.986 0.000 ROAE -0.098 0.064 0.002 -0.087 0.309 0.816 NIInc_Rev 7.098 3.551 0.892 8.678 1.685 0.772 LLProv 0.004 0.000 0.000 0.001 0.000 0.003 PerExp -0.004 0.006 0.286 -0.805 0.0419 0.891 Dep_Asset -2.785 2.863 0.000 -16.982 9.622 0.071 NInt_Asset -1.502 0.987 0.000 -2.097 0.753 0.006 Fexch_Eq -0.988 3.466 0.004 -1.618 0.443 0.018 Constant -5.316 6.153 0.899 11.154 15.262 0.899 Size 2.994 0.632 0.000 1.356 4.489 0.074 RINT -0.358 0.586 0.077 TBLOANS_GDP -1.865 0.355 0.034 Exchg 0.001 0.005 0.851 CPI 0.277 0.741 0.855 GDP 3.563 0.573 0.765

Overall predictive power 74.12% 79.05% R2-of Nagelkerke6 0.5986 0.6858

-2Log L 643.673

6