October 11, 2012

Alpha Pilot – Small/Mid Cap

Same same, but different

Estimate downgrades + mid-point valuation = creative stock-picking

Portfolio suggestions combining value, GARP, yield and quality

Almost time to bet against the negative revisions in consumer stocks

Contents

Table of figures

4

Key highlights

6

Valuation

11

Revisions

19

Quality

26

Implied sales growth

31

Multifactor models

34

Screening methodology

41

Disclaimer

43

Carl Grapenfelt

+46 8 701 33 93

[email protected]

Elias Porse

+46 8 701 34 24

[email protected]

Jan Dworsky

+46 8 701 55 55

[email protected]

This product combines consensus data and our

own estimates, building on our work done in the

Consensus Pilot and our Small/Mid and large cap

pilots for Nordic stocks with a market cap below

EUR 4bn and a daily liquidity of at least EUR

200,000.

Table of figures

Key highlights

Quality yield screening (quality 70%, dividend yield 30% weight) ... 8

Quality GARP screening (50% quality, 50% implied growth) ... 8

HCM multifactor screening 1 (value 30%, yield 20%, quality 30%, growth 20%) ... 9

HCM multifactor screening 2 (value 30%, yield 20%, rev. 10%, quality 40%) ... 10

Valuation

P/E, 12m forward and 12m trailing ... 11

P/B and ROE, 12m forward ... 11

Last 12m dividend yield vs. 10-year yield ... 12

Dividend payout, next 12m vs. last 12m ... 12

Next 12m EV/sales vs. 12m forward EBIT margin ... 12

EV/S model 12m forward, top 25 ... 13

EV/S model 12m forward, bottom 25 ... 13

EV/S model 12m historical, top 25 ... 14

EV/S model 12m historical, bottom 25 ... 14

15 largest 2013e P/E appreciation, -3m (%) ... 15

15 largest 2013e P/E declines, -3m (%) ... 15

15 highest 2012 dividend yields (%) ... 15

Payout ratio – top 25 ... 16

15 lowest forward P/E ... 16

15 lowest trailing P/E ... 17

15 highest forward P/E ... 17

15 lowest 12m forward P/B ... 17

EV/S relative to EW, top decile ... 18

EV/S relative to EW, bottom decile ... 18

Div yielders relative to EW, top decile ... 18

P/BV relative to EW, bottom decile ... 18

Revisions

HCMe EPS revision indicator ... 19

EBIT margin outcome vs. expectations ... 20

Sales growth expectations vs. outcome ... 20

EPS growth trend ... 20

Dispersion in EPS trend (median of universe) ... 21

HCMe sales revision indicator ... 21

Recommendation trend ... 21

Figure 1: Proportion of companies with EBIT margin improvement ... 22

Bottom 15 2013e EPS revisions, -3m ... 22

Top 15 2013e EPS revisions, -3m ... 22

Two-factor revision model, top 25 ... 23

Revision trends, bottom 25 ... 23

Sales revision ratio vs. EPS revision ratio ... 24

Recommendation revision ratio vs. EPS revision ratio ... 24

EPS revisions relative to EW, top decile ... 25

Sales revisions relative to EW, bottom decile ... 25

EPS + recommendation revision combo relative to EW, top decile ... 25

Quality

7-year average ROCE – Top 25 ... 26

EBITDA margin stability – Top 25 ... 27

EBIT margin stability – Top 25 ... 27

Net debt/EBITDA – ranked by lowest for 2012e ... 28

Net debt/EBITDA – ranked by highest for 2012e ... 28

Biggest positive net debt/EBITDA change in units since 2011 ... 29

Biggest negative net debt/EBITDA change in units since 2011 ... 29

Lowest one-year (52w) beta ... 29

Defensive quality screen (high ROCE, margin stability, low beta) top 25 ... 30

ROCE margin stability combo relative to EW, top decile ... 30

Implied sales growth diff vs. CAGR 2005-13e - top 25 (long screen) ... 31

Implied sales growth diff vs. CAGR 2005-13e - bottom 25 (short screen) ... 32

Implied sales growth diff vs. 2014e - top 25 (long screen) ... 32

Implied sales growth diff vs. 2014e - bottom 25 (short screen) ... 33

Multifactor models

Greenblatt – top 25, forward ... 34

Greenblatt – bottom 25, forward ... 35

Greenblatt –top 25, historical ... 35

Greenblatt - bottom 25, historical ... 36

Handelsbanken’s two-factor model (value + revisions), top 25 (forecasts) ... 36

Handelsbanken’s two-factor model (value + revisions), bottom 25 (forecasts) ... 37

Handelsbanken’s two-factor model (value + revisions), top 25 (history) ... 37

Handelsbanken’s two-factor model (value + revisions), bottom 25 (history) ... 38

Three-factor model (value + revisions + quality) – top 25, forward ... 38

Three-factor model (value + revisions + quality) – bottom 25, forward ... 39

Three -factor model (value + revisions + quality) – top 25, historical ... 39

Three -factor model (value + revisions + quality) – bottom 25, historical ... 40

Key highlights

Our view remains generally the same, as we continue to argue that estimates are too high, but valuation

levels have now reached mid-point making for an even more demanding stock-picking environment. The

value normalisation we witnessed in early September came to a screeching halt in conjunction with QE3,

implying that value alone is not enough. Leaning on revisions is also dangerous, as we see estimate

dispersion widening. Recent profit warnings in Net Ent. and Betsson have painfully reminded us what

happens when quality growth stocks disappoints, leaving us advocating a more defensive mix of value,

quality, yield and GARP traits. A contrarian strategy would involve looking for decent yielding Greenblatt

names that have already shown weakness. Many consumer stocks fit this bill, and we are on high alert as

we approach a point when it is time to bet against the negative revision trend.

Valuation

Valuation multiples have expanded on the heels of rising markets and falling estimates, and

now stand just shy of 15x 12-month trailing EPS. This has pushed the yield gap vs. long dated

government bonds down towards 200bp, after peaking at 250bp in late spring, whereas the

earnings yield gap has fallen to around 500bp from its 700bp peak. Equities still imply better

fortunes relative to bonds, though multiples have normalised relative to the historical

averages. This normalisation phase has proven the strongest among value stocks, which have

sharply outperformed the market (8-10 p.p. from summer lows). However, whether using our

normalised value approach (EV/S model) or low quality value approach, the cheapest names

have underperformed the market following the QE3 announcement on September 13. This

development is in line with the conclusions in our latest Small/Mid Cap Pilot, where we

argued that investors should not play a strategy based solely on valuation factors.

Revisions

Estimates have remained under pressure, with our revision indicators deep in negative

territory. We continue to argue that forecast changes will stay on the minus side, as

expectations for 2013e still look exuberant. Just consider that the prevailing consensus

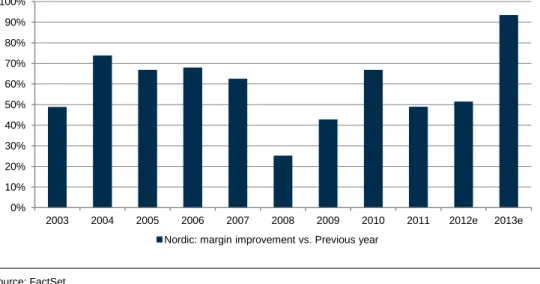

forecasts imply margins improving 150bp on 3% of top-line growth or that 93% of the

universe is expected to post margin improvements in 2013. Further to this, our screenings

show earnings dispersion at extremely low levels, which suggests confidence in

estimates. We find such a scenario very unrealistic and consequently expect dispersion to

widen as we exit the reporting season and, hopefully, analysts take down 2013e

estimates. We maintain our view that during this process it will be unusually difficult to

find earnings upgrade candidates, while simply betting on the stocks currently seeing the

best revision pattern is too risky. The revision factor (top decile) has in fact been flat

since May, though recent weeks have shown some outperformance. The bottom decile

has seen strong alpha generation lately, which in effect could spell trouble for the entire

universe as downgrades have been punished.

Quality

Quality factors have shown an inverse pattern compared to value stocks. That is, this

strategy underperformed until the QE3 announcement, and has outperformed since.

Conclusions

The stock-picking environment is very tricky, as we foresee continued estimate pressure

coupled with valuation levels at mid-point. We continue to argue that it is not as simple as

buying value outright, but also find that the revisions factor carries unusually high risks.

This leaves quality, and GARP characteristics, which we believe should be combined with

value and dividend yield traits. However, as recent profit warnings in Focus List names

Betsson and Net Entertainment have reminded us: it can be very painful when quality

growth stocks disappoint.

Valuation levels

have reached

historical averages…

…but are still

attractive vs. bonds

We remain convinced

that the prevailing

estimate pressure is

here to stay

We believe a

combination of yield,

GARP and quality

should yield is best

Stock calls

A contrarian strategy would involve looking for decent yielding Greenblatt names that have

already shown weakness in both estimates and share prices. Consumer-related stocks

dominate this category, as they are overrepresented in our Greenblatt-inspired rankings. In

this sector, we are approaching a point when it is time to take a bet against the negative

revision trend. Stocks which fit the bill include Axfood, Clas Ohlson, MTG, Bilia,

Oriflame, Betsson, Ekornes, JM, Net Entertainment, CDON and Duni. We are therefore not

exiting MTG, Betsson and Net Entertainment, which all have been downgraded recently (to

ACCUMULATE), though we acknowledge that in the short term they remain triggerless

and risk further de-rating. Additionally, these companies would be among the key

benefactors from the proposed corporate tax cut in Sweden. When it comes to Oriflame,

Clas Ohlson, Bilia, Duni and CDON, we are monitoring their performance closely, but are

not prepared to include them in our Focus List just yet.

Taking into account the above mentioned factor risks, we also highlight groupings of

companies that reflect a particular style or combination thereof from a screening

perspective, thereby leaving our subjectivity out of the equation. Below are some of the

stocks that we think warrant highlighting, illustrating some of the difficulties that we face:

Axfood and Intrum Justitia screen among the most attractive when you combine high

ROCE, margin stability, low beta, and dividend yield. Despite our EV/S model suggesting

that these stocks look fair, we think they warrant a closer look. Axfood’s bottom line could

also see ~6% boost to EPS in 2013 given the proposed corporate tax cuts.

Outotec score highly when we join value, quality and revision traits, but we believe that

mining capex cuts will eventually bleed into sales in 2014, when we expect a 13% y-o-y

drop. Do you trust the short-term revision trend, valuation and historical growth or should

you be afraid of downgrades based on potential peak earnings multiples?

JM looks very cheap, at 0.75x sales, given historical and forecasted profitability well above

10% and a 6% yield. In contrast, the secondary housing market is characterised by high

supply and major home builders have seen bookings fall sharply, potentially signalling risk

in the housing market. We are thus stuck between cheapness and sentiment risk again.

HiQ (part of SHB Focus List)

screens favourably using all our metrics apart from

revisions, with an EV/S of <1x, stable EBIT margins (~15%), high returns, delivery of

>10% top-line growth historically, and about a 7%. Further, it is a beneficiary of the

proposed corporate tax cut. The only caveat is the size of the company and stock liquidity.

The lower-quality value segment merits a mention, where asset plays Songa Offshore (part

of SHB Focus List) and

BW Offshore screen cheaply and did not bounce in line with

stocks with a similar debt level. Patience is running out and the debt pile is cause for

concern, but it is hard to argue that these stocks should remain so depressed.

Our oil service call from three months ago has played out nicely. From this junction, we

note that the upside in our EV/S model in Fred Olsen is now rather limited, potentially

prompting some profit taking. Prosafe screens negatively, with its estimates under pressure

and its share trading at 5x sales, which also suggests good profit taking odds. We remain

more optimistic on subsea and seismic names from a screening perspective.

Schibsted has seen downgrades for over two years, but the share has completely decoupled

from the estimate trend, which at the current valuation implies that the company would

need to outgrow its historical track-record by almost 3x.

Bang Olufsen and Mestsä Board look risky, with unstable profitability and poor ROCE,

in addition to looking very expensive according to our EV/S model.

Approaching an

opportunity to bet

against the revision

trend within the

consumer names

Axfood a great bet if

you are bearish

Outotec and JM

illustrate screening

appeal vs. sentiment

risk

HiQ among the best

cases around – we

just wish the liquidity

was greater

Our screenings imply

profit-taking in

Prosafe and FOE

Take profit in

Schibsted, B&O and

Metsä Board

Screening various investment styles

Quality yield screening (quality 70%, dividend yield 30% weight)

Div. Screening for overw eights Mcap (EURm ) Perf -3m (%) Adj.EV/S Hist Fw d Im plied Hist Fw d Grow th 5y CAGR 05-13 2014e yield 12e % Beta HiQ 204 -8 0.94 16.0 14.5 9.1 68 53 -5.8 11.0 12.8 7.2 0.7 Oriflame 1,419 -6 1.09 12.2 11.9 10.5 20 17 1.1 9.4 4.0 6.9 0.7 Ekornes 439 2 0.98 16.8 14.9 9.5 68 51 -5.8 2.9 3.4 8.6 0.9 Axfood n.m 10 0.37 3.6 3.5 3.6 2 -2 4.0 3.5 2.5 5.0 0.5 Sw eco 744 -5 0.81 9.0 9.0 7.8 16 16 1.2 11.6 4.9 4.7 0.7 Intrum Justitia 880 -4 2.42 20.8 23.2 23.3 -15 0 5.1 5.7 3.5 5.0 0.7 Duni 314 -1 0.84 9.8 11.0 8.1 26 45 -0.9 1.0 4.2 6.3 0.5 Net Entertainment 323 0 4.12 36.5 31.8 39.6 -8 -19 7.0 33.6 17.0 3.4 0.8 Elisa 2,916 9 2.23 17.7 19.6 21.4 -23 -11 6.8 2.0 -1.6 7.7 0.5 Clas Ohlson 646 -13 0.76 10.5 8.7 7.3 44 19 -1.3 9.0 6.0 5.1 0.9 Prosafe 1,512 16 5.00 46.2 47.7 48.1 -5 -1 4.5 7.3 12.6 6.3 0.9 Simcorp 775 32 3.02 23.0 23.5 29.1 -19 -18 8.5 10.3 14.0 2.7 0.5 Securitas 2,124 -8 0.42 5.5 4.5 4.0 57 20 -0.4 0.3 3.1 6.0 1.0 Veidekke 851 10 0.29 3.2 3.8 2.7 17 41 -0.8 5.9 12.4 5.9 0.7 Axis 1,323 12 2.04 17.0 15.9 19.7 -13 -19 7.6 25.1 22.0 3.7 1.2 Mekonomen 819 -1 1.38 12.1 13.2 13.3 -11 -1 5.0 13.8 6.4 4.1 0.8 Indutrade 864 -8 1.00 9.9 9.3 9.6 4 -4 4.1 11.2 4.0 3.6 0.8 Lundbeck 2,796 -12 1.33 23.2 14.7 12.8 78 14 -3.5 6.5 0.8 2.2 0.3 NCC 1,598 3 0.32 4.3 4.0 3.0 54 40 -1.9 1.7 4.7 7.9 1.3 Betsson 802 -17 2.55 24.3 27.5 24.5 -1 12 2.9 42.2 13.7 6.1 1.1 TGS-Nopec 2,760 25 3.33 44.7 43.1 32.1 35 31 -2.1 18.8 10.0 3.4 1.1 Royal Unibrew 661 21 1.47 10.2 15.3 14.2 -30 8 6.1 0.8 1.6 5.1 0.1

Fred. Olsen Energy 2,322 22 2.91 34.2 34.4 28.0 26 26 0.0 11.5 8.7 7.8 0.9

Unibet Group 596 4 1.96 29.7 18.5 18.9 52 -2 -0.8 22.4 11.9 4.5 0.7

Pandora 1,490 58 1.49 36.0 23.4 14.3 144 60 -9.6 n.m 7.0 3.5 1.3

Average 6 1.72 19.1 17.9 16.6 23 15 1.2 11.2 7.6 5.3 0.8

Adj. EBIT-m argin (%) Share Pot. (%) Im pl. Sales gr. (%)

Source: Handelsbanken Capital markets (Quality defined as: 40% ROCE, 30% margin stability and 30% low beta)

Quality GARP screening (50% quality, 50% implied growth)

Screening for overw eights Mcap (EURm ) Perf -3m (%) Adj.EV/S Hist Fw d Im plied Hist Fw d Grow th 5y CAGR 05-13 2014e yield 12e % Beta Net Entertainment 323 0 4.12 36.5 31.8 39.6 -8 -19 7.0 33.6 17.0 3.4 0.8 HiQ 204 -8 0.94 16.0 14.5 9.1 68 53 -5.8 11.0 12.8 7.2 0.7 Axis 1,323 12 2.04 17.0 15.9 19.7 -13 -19 7.6 25.1 22.0 3.7 1.2 TGS-Nopec 2,760 25 3.33 44.7 43.1 32.1 35 31 -2.1 18.8 10.0 3.4 1.1 Pandora 1,490 58 1.49 36.0 23.4 14.3 144 60 -9.6 7.0 3.5 1.3 Ekornes 439 2 0.98 16.8 14.9 9.5 68 51 -5.8 2.9 3.4 8.6 0.9 Sw eco 744 -5 0.81 9.0 9.0 7.8 16 16 1.2 11.6 4.9 4.7 0.7 Unibet Group 596 4 1.96 29.7 18.5 18.9 52 -2 -0.8 22.4 11.9 4.5 0.7 Clas Ohlson 646 -13 0.76 10.5 8.7 7.3 44 19 -1.3 9.0 6.0 5.1 0.9 CDON Group 317 4 0.49 6.0 2.4 4.8 26 -50 6.6 15.0 0.0 0.9 Betsson 802 -17 2.55 24.3 27.5 24.5 -1 12 2.9 42.2 13.7 6.1 1.1 Kongsberg Gruppen 1,788 -1 0.62 11.4 11.3 6.0 75 74 -8.0 14.9 7.5 3.4 1.0 Oriflame 1,419 -6 1.09 12.2 11.9 10.5 20 17 1.1 9.4 4.0 6.9 0.7

Modern Times Group 2,180 -12 1.12 14.7 12.8 10.7 30 16 -0.8 7.2 6.4 3.6 1.3

Hexpol 1,051 13 1.14 11.2 13.0 11.0 3 20 2.1 18.6 4.0 2.3 1.1

Lundbeck 2,796 -12 1.33 23.2 14.7 12.8 78 14 -3.5 6.5 0.8 2.2 0.3

Veidekke 851 10 0.29 3.2 3.8 2.7 17 41 -0.8 5.9 12.4 5.9 0.7

Indutrade 864 -8 1.00 9.9 9.3 9.6 4 -4 4.1 11.2 4.0 3.6 0.8

Transmode 229 -12 1.28 13.0 16.6 12.3 5 29 0.3 10.0 2.5 0.9

Opera Softw are 616 -6 2.57 15.3 23.6 24.7 -35 -4 8.9 36.4 12.1 0.5 0.5

Simcorp 775 32 3.02 23.0 23.5 29.1 -19 -18 8.5 10.3 14.0 2.7 0.5

Mekonomen 819 -1 1.38 12.1 13.2 13.3 -11 -1 5.0 13.8 6.4 4.1 0.8

DSV 3,209 9 0.57 5.2 5.6 5.5 -7 2 4.4 9.9 5.4 1.0 0.9

Fred. Olsen Energy 2,322 22 2.91 34.2 34.4 28.0 26 26 0.0 11.5 8.7 7.8 0.9

AF-Group 549 7 0.77 7.9 9.2 7.4 7 25 1.1 13.3 3.1 3.7 1.1

4 1.54 17.7 16.5 14.8 25 16 0.9 15.7 8.9 4.0 0.9

Adj. EBIT-m argin (%) Share Pot. (%) Im pl. Sales gr. (%)

Source: Handelsbanken Capital markets (quality defined as 50% ROCE. 40% margin stability and 10% Beta)

5.3% yield with 1%

implied growth for

this basket

Intrum and Clas O

knocking on Focus

List door

Is it finally time for

Securitas to shine?

Betsson PW vs. 6%

yield and likely

growth in 2013e

4% yield, beta 0.9

with 1% implied

growth for this

basket

Net Ent, Axis, HiQ,

Betsson, KOG, MTG,

and AF part of our

Focus List

Clas O again

Consumer stocks ex

Pandora have

struggled

HCM multifactor screening 1 (value 30%, yield 20%, quality 30%, growth 20%)

Div. Screening for overw eights Mcap (EURm ) Perf -3m (%) Adj.EV/S Hist Fw d Im plied Hist Fw d Grow th 5y CAGR 05-13 2014e yield 12e % Beta HiQ 204 -8 0.94 16.0 14.5 9.1 68 53 -5.8 11.0 12.8 7.2 0.7 Ekornes 439 2 0.98 16.8 14.9 9.5 68 51 -5.8 2.9 3.4 8.6 0.9 Pandora 1,490 58 1.49 36.0 23.4 14.3 144 60 -9.6 7.0 3.5 1.3 TGS-Nopec 2,760 25 3.33 44.7 43.1 32.1 35 31 -2.1 18.8 10.0 3.4 1.1 NCC 1,598 3 0.32 4.3 4.0 3.0 54 40 -1.9 1.7 4.7 7.9 1.3 JM 1,148 -2 0.73 11.7 12.4 7.0 65 75 -6.3 2.9 10.1 5.6 1.7 Veidekke 851 10 0.29 3.2 3.8 2.7 17 41 -0.8 5.9 12.4 5.9 0.7 Clas Ohlson 646 -13 0.76 10.5 8.7 7.3 44 19 -1.3 9.0 6.0 5.1 0.9 Oriflame 1,419 -6 1.09 12.2 11.9 10.5 20 17 1.1 9.4 4.0 6.9 0.7 Kongsberg Gruppen 1,788 -1 0.62 11.4 11.3 6.0 75 74 -8.0 14.9 7.5 3.4 1.0

Fred. Olsen Energy 2,322 22 2.91 34.2 34.4 28.0 26 26 0.0 11.5 8.7 7.8 0.9

Sw eco 744 -5 0.81 9.0 9.0 7.8 16 16 1.2 11.6 4.9 4.7 0.7 Konecranes 1,511 16 0.62 7.3 7.3 5.9 23 24 0.0 11.3 2.6 4.4 1.9 Securitas 2,124 -8 0.42 5.5 4.5 4.0 57 20 -0.4 0.3 3.1 6.0 1.0 Duni 314 -1 0.84 9.8 11.0 8.1 26 45 -0.9 1.0 4.2 6.3 0.5 Outotec 1,749 8 0.60 7.9 9.1 5.8 26 41 -3.4 18.0 -12.7 2.9 1.5 Betsson 802 -17 2.55 24.3 27.5 24.5 -1 12 2.9 42.2 13.7 6.1 1.1

Modern Times Group 2,180 -12 1.12 14.7 12.8 10.7 30 16 -0.8 7.2 6.4 3.6 1.3

Unibet Group 596 4 1.96 29.7 18.5 18.9 52 -2 -0.8 22.4 11.9 4.5 0.7 Höganäs 919 0 1.14 12.8 15.3 10.9 18 43 -0.9 6.2 4.0 4.4 1.1 Boliden 3,513 13 0.90 13.3 11.3 8.7 64 37 -2.8 8.8 0.6 3.6 1.7 Hexpol 1,051 13 1.14 11.2 13.0 11.0 3 20 2.1 18.6 4.0 2.3 1.1 Tieto 962 3 0.54 6.5 6.8 5.2 27 32 -0.9 1.0 4.9 5.9 0.7 Net Entertainment 323 0 4.12 36.5 31.8 39.6 -8 -19 7.0 33.6 17.0 3.4 0.8 Axfood 1,515 10 0.37 3.6 3.5 3.6 2 -2 4.0 3.5 2.5 5.0 0.5 5 1.22 15.7 14.6 11.8 38 31 -1.4 11.4 6.1 5.1 1.0 Div. Screening for underw eights Mcap (EURm ) Perf -3m (%) Adj.

EV/S Hist Fw d Im plied Hist Fw d Grow th 5y CAGR 05-13 2014e yield 12e % Beta Talvivaara Mining Co 531 13 3.11 n.m. 11.0 29.9 n.m n.m 10.1 0.0 1.7 Outokumpu 1,075 7 0.60 0.0 -0.2 5.8 n.m n.m -1.2 0.3 0.0 1.5 SAS 266 29 0.47 2.6 1.4 4.5 n.m n.m 21.4 -4.2 1.0 0.0 1.2 Norske Skog 130 25 0.43 0.6 3.4 4.1 n.m n.m 19.8 -4.8 -5.0 0.0 1.3 Alk-Abello 509 -3 1.35 9.3 7.6 13.0 -24 -35 12.9 -7.3 7.0 1.3 0.3 Metsä Board 769 16 0.64 1.1 5.1 6.2 n.m -31 18.8 -10.7 0.1 0.0 1.8

Norw egian Air Shuttle 543 6 1.04 2.6 5.6 10.0 n.m n.m 23.5 28.1 13.0 0.0 1.5

Bang & Olufsen 419 36 0.78 2.2 6.5 7.5 -67 -13 15.6 -1.4 9.3 1.3 1.0

Lundin Mining 2,283 17 2.88 21.0 19.7 27.7 -20 -24 10.3 20.5 -0.4 0.0 1.3 SSAB 1,667 -19 0.78 9.7 3.9 7.5 61 n.m 6.1 4.9 2.9 4.3 2.1 Chr. Hansen 3,285 4 4.61 22.3 27.5 44.3 -55 -42 16.3 9.0 2.0 0.3 Stockmann 1,133 1 0.84 5.4 5.1 8.1 -56 -62 13.1 8.5 4.8 3.8 0.9 Schibsted 3,297 20 1.71 9.5 11.2 16.4 -46 -35 13.7 5.8 5.0 1.8 1.1 Nobia 527 31 0.49 5.2 4.5 4.7 12 -6 3.6 -0.8 3.5 1.5 1.6 BW Offshore 364 -41 2.69 -1.8 14.2 25.9 n.m n.m 37.1 40.4 -2.8 11.0 0.8 D/S Norden 871 -2 0.78 11.4 4.2 7.5 37 -32 3.3 -0.7 9.1 2.7 0.7 KappAhl 161 23 0.63 8.9 3.0 6.0 102 n.m 4.3 2.4 2.5 0.0 1.0 Elekta 3,928 16 3.21 16.4 21.5 30.9 -50 -32 14.3 12.6 9.9 1.6 0.5 Petroleum Geo-Services 2,892 37 2.49 19.7 21.9 24.0 -21 -10 6.9 8.8 9.4 1.3 1.1 Archer 405 -28 0.66 5.6 5.5 6.3 -32 -37 6.6 3.4 0.0 1.8 AarhusKarlshamn 1,244 10 0.73 5.3 6.1 7.0 -32 -18 8.3 7.5 7.8 1.9 0.7 Songa Offshore 330 -10 2.34 23.3 20.5 22.5 14 -35 4.5 7.9 0.0 1.5 Vestas 1,000 31 0.28 2.7 2.7 2.7 1 3 3.7 6.4 8.4 0.0 1.5 Amer Sports 1,209 14 0.76 6.1 7.4 7.3 -22 2 5.5 2.6 4.7 3.4 0.7 Stora Enso 3,891 -3 0.60 5.7 6.5 5.8 -2 22 2.9 -2.4 3.3 6.3 1.5 9 1.40 8.1 9.0 13.4 -11 -23 11.8 5.5 5.0 1.8 1.2

Adj. EBIT-m argin (%) Share Pot. (%) Im pl. Sales gr. (%) Adj. EBIT-m argin (%) Share Pot. (%) Im pl. Sales gr. (%)

Source: Handelsbanken Capital markets

5% yield, beta 1 with

-1.4% implied growth

for this basket

If construction

margins improve, the

sector has scope to

normalise

Duni again

Our screenings can’t

get rid of MTG and

Axfood

1% yield, beta 1.2

with 12% implied

growth for this

basket

Metsä Board and

B&O screen poorly

Nobia back at 0.5x

sales

Elekta needs to

match historical

growth for valuation

to be fair

HCM multifactor screening 2 (value 30%, yield 20%, rev. 10%, quality 40%)

Div. Screening for overw eights Mcap (EURm ) Perf -3m (%) Adj.EV/S Hist Fw d Im plied Hist Fw d Grow th 5y CAGR 05-13 2014e yield 12e % Beta Ekornes 439 2 0.98 16.8 14.9 9.5 68 51 -5.8 2.9 3.4 8.6 0.9 TGS-Nopec 2,760 25 3.33 44.7 43.1 32.1 35 31 -2.1 18.8 10.0 3.4 1.1 Oriflame 1,419 -6 1.09 12.2 11.9 10.5 20 17 1.1 9.4 4.0 6.9 0.7 HiQ 204 -8 0.94 16.0 14.5 9.1 68 53 -5.8 11.0 12.8 7.2 0.7 JM 1,148 -2 0.73 11.7 12.4 7.0 65 75 -6.3 2.9 10.1 5.6 1.7 Axfood 1,515 10 0.37 3.6 3.5 3.6 2 -2 4.0 3.5 2.5 5.0 0.5 Pandora 1,490 58 1.49 36.0 23.4 14.3 144 60 -9.6 7.0 3.5 1.3 Sw eco 744 -5 0.81 9.0 9.0 7.8 16 16 1.2 11.6 4.9 4.7 0.7 NCC 1,598 3 0.32 4.3 4.0 3.0 54 40 -1.9 1.7 4.7 7.9 1.3 Duni 314 -1 0.84 9.8 11.0 8.1 26 45 -0.9 1.0 4.2 6.3 0.5 Konecranes 1,511 16 0.62 7.3 7.3 5.9 23 24 0.0 11.3 2.6 4.4 1.9 Outotec 1,749 8 0.60 7.9 9.1 5.8 26 41 -3.4 18.0 -12.7 2.9 1.5 Securitas 2,124 -8 0.42 5.5 4.5 4.0 57 20 -0.4 0.3 3.1 6.0 1.0 Clas Ohlson 646 -13 0.76 10.5 8.7 7.3 44 19 -1.3 9.0 6.0 5.1 0.9 Veidekke 851 10 0.29 3.2 3.8 2.7 17 41 -0.8 5.9 12.4 5.9 0.7

Fred. Olsen Energy 2,322 22 2.91 34.2 34.4 28.0 26 26 0.0 11.5 8.7 7.8 0.9

YIT 1,968 15 0.55 6.0 6.0 5.3 19 17 1.6 6.0 2.7 4.8 1.4

Tieto 962 3 0.54 6.5 6.8 5.2 27 32 -0.9 1.0 4.9 5.9 0.7

Kongsberg Gruppen 1,788 -1 0.62 11.4 11.3 6.0 75 74 -8.0 14.9 7.5 3.4 1.0

Modern Times Group 2,180 -12 1.12 14.7 12.8 10.7 30 16 -0.8 7.2 6.4 3.6 1.3

Lundbeck 2,796 -12 1.33 23.2 14.7 12.8 78 14 -3.5 6.5 0.8 2.2 0.3 Höganäs 919 0 1.14 12.8 15.3 10.9 18 43 -0.9 6.2 4.0 4.4 1.1 Boliden 3,513 13 0.90 13.3 11.3 8.7 64 37 -2.8 8.8 0.6 3.6 1.7 Intrum Justitia 880 -4 2.42 20.8 23.2 23.3 -15 0 5.1 5.7 3.5 5.0 0.7 AF-Group 549 7 0.77 7.9 9.2 7.4 7 25 1.1 13.3 3.1 3.7 1.1 5 1.04 14.0 13.1 10.0 40 33 -1.6 7.9 4.7 5.1 1.0 Div. Screening for underw eights Mcap (EURm ) Perf -3m (%) Adj.

EV/S Hist Fw d Im plied Hist Fw d Grow th 5y CAGR 05-13 2014e yield 12e % Beta SAS 266 29 0.47 n.m. 1.4 4.5 n.m n.m 21.4 -4.2 1.0 0.0 1.2 Talvivaara Mining Co 531 13 3.11 n.m. 11.0 29.9 n.m n.m 10.1 0.0 1.7 Norske Skog 130 25 0.43 0.6 3.4 4.1 n.m n.m 19.8 -4.8 -5.0 0.0 1.3 Outokumpu 1,075 7 0.60 0.0 -0.2 5.8 n.m n.m -1.2 0.3 0.0 1.5

Norw egian Air Shuttle 543 6 1.04 2.6 5.6 10.0 n.m n.m 23.5 28.1 13.0 0.0 1.5

Alk-Abello 509 -3 1.35 9.3 7.6 13.0 -24 -35 12.9 -7.3 7.0 1.3 0.3

Metsä Board 769 16 0.64 1.1 5.1 6.2 n.m -31 18.8 -10.7 0.1 0.0 1.8

Lundin Mining 2,283 17 2.88 21.0 19.7 27.7 -20 -24 10.3 20.5 -0.4 0.0 1.3

Bang & Olufsen 419 36 0.78 2.2 6.5 7.5 -67 -13 15.6 -1.4 9.3 1.3 1.0

Archer 405 -28 0.66 5.6 5.5 6.3 -32 -37 6.6 3.4 0.0 1.8 Songa Offshore 330 -10 2.34 23.3 20.5 22.5 14 -35 4.5 7.9 0.0 1.5 SSAB 1,667 -19 0.78 9.7 3.9 7.5 61 n.m 6.1 4.9 2.9 4.3 2.1 Stockmann 1,133 1 0.84 5.4 5.1 8.1 -56 -62 13.1 8.5 4.8 3.8 0.9 KappAhl 161 23 0.63 8.9 3.0 6.0 102 n.m 4.3 2.4 2.5 0.0 1.0 BW Offshore 364 -41 2.69 -1.8 14.2 25.9 n.m n.m 37.1 40.4 -2.8 11.0 0.8 Vestas 1,000 31 0.28 2.7 2.7 2.7 1 3 3.7 6.4 8.4 0.0 1.5 Nobia 527 31 0.49 5.2 4.5 4.7 12 -6 3.6 -0.8 3.5 1.5 1.6 Schibsted 3,297 20 1.71 9.5 11.2 16.4 -46 -35 13.7 5.8 5.0 1.8 1.1 D/S Norden 871 -2 0.78 11.4 4.2 7.5 37 -32 3.3 -0.7 9.1 2.7 0.7 New Wave 170 -15 0.75 8.3 7.2 7.3 32 -1 2.7 4.3 4.0 2.3 1.6

Opera Softw are 616 -6 2.57 15.3 23.6 24.7 -35 -4 8.9 36.4 12.1 0.5 0.5

North Atlantic Drilling 1,729 15 4.43 43.2 42.6 n.m 3 8.4 9.5 0.6

Chr. Hansen 3,285 4 4.61 22.3 27.5 44.3 -55 -42 16.3 9.0 2.0 0.3

Petroleum Geo-Services 2,892 37 2.49 19.7 21.9 24.0 -21 -10 6.9 8.8 9.4 1.3 1.1

AarhusKarlshamn 1,244 10 0.73 5.3 6.1 7.0 -32 -18 8.3 7.5 7.8 1.9 0.7

8 1.52 8.5 10.6 14.6 -7 -22 11.9 7.2 5.2 1.8 1.2

Adj. EBIT-m argin (%) Share Pot. (%) Im pl. Sales gr. (%) Adj. EBIT-m argin (%) Share Pot. (%) Im pl. Sales gr. (%)

Source: Handelsbanken Capital markets

5% yield, Beta 1 with

-1.6% implied growth

for this basket

Axfood and MTG

again

Konecranes and

Outotec the capital

goods names

Intrum and AF also

makes the cut

1% yield, Beta 1.2

with 12% implied

growth for this

basket

New Wave, Songa

and NKT value bets

in our Focus list

Christian Hansen in

need of >15%

growth assuming

25% sustainable

margins

AAK now trading in

line with historical

growth rates

Valuation

Valuation multiples have expanded to a point just shy of 15x 12-month trailing EPS. This has pushed the yield

gap vs. bonds down towards 200bp (250bp four months ago), while the earnings yield gap has fallen to around

500bp (700bp). Equities still imply better fortunes relative to bonds, but multiples have normalised relative to

historical averages. This normalisation phase has proven the strongest among value stocks, which have

sharply outperformed the market (up 8-10 p.p. from summer lows). However, the cheapest groupings (EV/S

model and P/BV) have underperformed the market since the QE3 announcement on September 13, potentially

marking the end of normalisation. We continue to argue that value cannot stand alone and needs support from

quality, yield and GARP characteristics.

P/E, 12m forward and 12m trailing

6

8

10

12

14

16

18

20

22

24

26

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Next 12 months P/E Last 12 months P/E

Source: FactSet

P/B and ROE, 12m forward

9%

10%

11%

12%

13%

14%

15%

16%

17%

18%

19%

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Next 12 months Price/Book (L) Next 12 months Return on Equity (R)

Source: FactSet

<15x trailing EPS up

from ~12x in May

Forecast cuts set to

drive further forward

P/E expansion

1.5x BV a touch

below historical

midpoint

Last 12m dividend yield vs. 10-year yield

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Last 12 months Net Div Yield 10-Year Yield

Source: FactSet

Dividend payout, next 12m vs. last 12m

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Next 12 months Div. Payout Last 12 months Div. Payout

Source: FactSet

Next 12m EV/sales vs. 12m forward EBIT margin

5%

6%

7%

8%

9%

10%

11%

12%

13%

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

EV/Sales

EBIT Margin Fwd

Source: FactSet

Dividend yield gap of

~200bp...

...but based on a

payout ratio not seen

since 2003, implying

risk of forecast cuts

>10x forward EBIT,

despite estimate risk

EV/S model 12m forward, top 25

Mcap

(EURm )

Perf

-3m (%)

Hist

Fw d Im plied

Adj.

EV/S

Hist

Fw d

Eniro

96

4

19.3

13.9

8.6

0.90

520

260

EAC

199

-18

7.1

4.9

2.9

0.30

293

142

Auriga Industries

308

28

5.3

8.6

6.1

0.64

-27

77

Haldex

164

2

4.6

6.3

3.9

0.41

22

76

JM

1,148

-2

11.7

12.4

7.0

0.73

65

75

Kongsberg Gruppen

1,788

-1

11.4

11.3

6.0

0.62

75

74

Kvaerner

561

20

3.3

4.4

2.3

0.24

32

67

Cermaq

931

-3

10.9

9.1

5.8

0.61

104

66

Concentric

242

-7

13.3

8.1

0.84

n.m

65

Pandora

1,490

58

36.0

23.4

14.3

1.49

144

60

Bilia

244

-7

1.9

2.1

1.5

0.15

36

56

HiQ

204

-8

16.0

14.5

9.1

0.94

68

53

Ekornes

439

2

16.8

14.9

9.5

0.98

68

51

Duni

314

-1

9.8

11.0

8.1

0.84

26

45

Höganäs

919

0

12.8

15.3

10.9

1.14

18

43

Outotec

1,749

8

7.9

9.1

5.8

0.60

26

41

Veidekke

851

10

3.2

3.8

2.7

0.29

17

41

NCC

1,598

3

4.3

4.0

3.0

0.32

54

40

Golden Ocean

256

5

32.3

34.3

30.3

3.15

19

38

Boliden

3,513

13

13.3

11.3

8.7

0.90

64

37

FLSmidth & Co

2,350

1

8.8

9.6

7.3

0.75

23

35

Leroy Seafood Group

865

7

11.4

10.6

8.5

0.89

46

33

Tieto

962

3

6.5

6.8

5.2

0.54

27

32

TGS-Nopec

2,760

25

44.7

43.1

32.1

3.33

35

31

Transmode

229

-12

13.0

16.6

12.3

1.28

5

29

Adj. EBIT-m argin (%)

Share Pot. (%)

Source: Handelsbanken Capital Markets

EV/S model 12m forward, bottom 25

Mcap

(EURm )

Perf

-3m (%)

Hist

Fw d Im plied

Adj.

EV/S

Hist

Fw d

Stockmann

1,133

1

5.4

5.1

8.1

0.84

-56

-62

CDON Group

317

4

6.0

2.4

4.8

0.49

26

-50

Chr. Hansen

3,285

4

22.3

27.5

44.3

4.61

-55

-42

Rautaruukki

732

3

5.8

3.9

4.8

0.50

45

-42

Archer

405

-28

5.6

5.5

6.3

0.66

-32

-37

Songa Offshore

330

-10

23.3

20.5

22.5

2.34

14

-35

Alk-Abello

509

-3

9.3

7.6

13.0

1.35

-24

-35

Schibsted

3,297

20

9.5

11.2

16.4

1.71

-46

-35

Elekta

3,928

16

16.4

21.5

30.9

3.21

-50

-32

D/S Norden

871

-2

11.4

4.2

7.5

0.78

37

-32

Metsä Board

769

16

1.1

5.1

6.2

0.64

n.m

-31

Lundin Mining

2,283

17

21.0

19.7

27.7

2.88

-20

-24

Net Entertainment

323

0

36.5

31.8

39.6

4.12

-8

-19

Axis

1,323

12

17.0

15.9

19.7

2.04

-13

-19

Simcorp

775

32

23.0

23.5

29.1

3.02

-19

-18

AarhusKarlshamn

1,244

10

5.3

6.1

7.0

0.73

-32

-18

Bang & Olufsen

419

36

2.2

6.5

7.5

0.78

-67

-13

Nibe Industrier

1,370

9

11.8

13.2

14.6

1.51

-24

-12

Holmen

1,806

-3

10.0

9.3

10.2

1.06

-2

-11

Elisa

2,916

9

17.7

19.6

21.4

2.23

-23

-11

Husqvarna

2,244

5

7.7

7.3

7.9

0.82

-4

-10

Petroleum Geo-Services

2,892

37

19.7

21.9

24.0

2.49

-21

-10

DFDS

566

0

6.2

4.8

5.0

0.52

36

-8

Nobia

527

31

5.2

4.5

4.7

0.49

12

-6

Indutrade

864

-8

9.9

9.3

9.6

1.00

4

-4

Adj. EBIT-m argin (%)

Share Pot. (%)

Source: Handelsbanken Capital Markets

High upsides are

harder to find, as

several value names

have performed

strongly

Consumer names

Bilia, Duni and JM

climb rankings

following poor

performance

What’s normalised

profitability in

CDON?

Look for strong

performers with big

downsides as

sources of funding

Schibsted, Simcorp,

Elekta, B&O, Nobia

stand out

EV/S model 12m historical, top 25

Mcap

(EURm )

Perf

-3m (%)

Hist

Fw d Im plied

Adj.

EV/S

Hist

Fw d

Eniro

96

4

19.3

13.9

8.6

0.90

520

260

EAC

199

-18

7.1

4.9

2.9

0.30

293

142

Pandora

1,490

58

36.0

23.4

14.3

1.49

144

60

Cermaq

931

-3

10.9

9.1

5.8

0.61

104

66

KappAhl

161

23

8.9

3.0

6.0

0.63

102

n.m

Lundbeck

2,796

-12

23.2

14.7

12.8

1.33

78

14

Kongsberg Gruppen

1,788

-1

11.4

11.3

6.0

0.62

75

74

HiQ

204

-8

16.0

14.5

9.1

0.94

68

53

Ekornes

439

2

16.8

14.9

9.5

0.98

68

51

JM

1,148

-2

11.7

12.4

7.0

0.73

65

75

Boliden

3,513

13

13.3

11.3

8.7

0.90

64

37

SSAB

1,667

-19

9.7

3.9

7.5

0.78

61

n.m

Securitas

2,124

-8

5.5

4.5

4.0

0.42

57

20

NCC

1,598

3

4.3

4.0

3.0

0.32

54

40

Unibet Group

596

4

29.7

18.5

18.9

1.96

52

-2

Cargotec

1,239

5

6.5

5.5

4.7

0.49

47

20

Leroy Seafood Group

865

7

11.4

10.6

8.5

0.89

46

33

Rautaruukki

732

3

5.8

3.9

4.8

0.50

45

-42

Clas Ohlson

646

-13

10.5

8.7

7.3

0.76

44

19

NKT Holding

656

12

4.8

4.4

3.7

0.39

38

25

D/S Norden

871

-2

11.4

4.2

7.5

0.78

37

-32

DFDS

566

0

6.2

4.8

5.0

0.52

36

-8

Bilia

244

-7

1.9

2.1

1.5

0.15

36

56

TGS-Nopec

2,760

25

44.7

43.1

32.1

3.33

35

31

Kvaerner

561

20

3.3

4.4

2.3

0.24

32

67

Adj. EBIT-m argin (%)

Share Pot. (%)

Source: Handelsbanken Capital Markets

EV/S model 12m historical, bottom 25

Mcap

(EURm )

Perf

-3m (%)

Hist

Fw d Im plied

Adj.

EV/S

Hist

Fw d

Bang & Olufsen

419

36

2.2

6.5

7.5

0.78

-67

-13

Stockmann

1,133

1

5.4

5.1

8.1

0.84

-56

-62

Chr. Hansen

3,285

4

22.3

27.5

44.3

4.61

-55

-42

Elekta

3,928

16

16.4

21.5

30.9

3.21

-50

-32

Schibsted

3,297

20

9.5

11.2

16.4

1.71

-46

-35

Opera Softw are

616

-6

15.3

23.6

24.7

2.57

-35

-4

Archer

405

-28

5.6

5.5

6.3

0.66

-32

-37

AarhusKarlshamn

1,244

10

5.3

6.1

7.0

0.73

-32

-18

Nordic Semiconductor

370

-2

14.9

22.1

22.4

2.33

-31

-1

Royal Unibrew

661

21

10.2

15.3

14.2

1.47

-30

8

Auriga Industries

308

28

5.3

8.6

6.1

0.64

-27

77

Nibe Industrier

1,370

9

11.8

13.2

14.6

1.51

-24

-12

Alk-Abello

509

-3

9.3

7.6

13.0

1.35

-24

-35

Elisa

2,916

9

17.7

19.6

21.4

2.23

-23

-11

Amer Sports

1,209

14

6.1

7.4

7.3

0.76

-22

2

Petroleum Geo-Services

2,892

37

19.7

21.9

24.0

2.49

-21

-10

Lundin Mining

2,283

17

21.0

19.7

27.7

2.88

-20

-24

Tomra

1,013

2

14.6

18.4

17.7

1.84

-20

5

Simcorp

775

32

23.0

23.5

29.1

3.02

-19

-18

Trelleborg

2,287

14

7.6

11.2

9.0

0.94

-17

25

Intrum Justitia

880

-4

20.8

23.2

23.3

2.42

-15

0

Axis

1,323

12

17.0

15.9

19.7

2.04

-13

-19

Atea

804

15

2.2

3.1

2.5

0.26

-12

24

Mekonomen

819

-1

12.1

13.2

13.3

1.38

-11

-1

Net Entertainment

323

0

36.5

31.8

39.6

4.12

-8

-19

Adj. EBIT-m argin (%)

Share Pot. (%)

Source: Handelsbanken Capital Markets

Only ~60% upside in

SSAB at 0.8x sales

when you include the

boom years

Clas Ohlson screens

attractively

NKT could rock if

cables profitability

finally improves

Schibsted appears

immune to estimate

downgrades

Royal Unibrew move

makes it fair on

forecasts

Amer – you have to

believe in 10% target

to find solid upside

Tomra above 1.8x

sales – time for a

breather?

Trelleborg: historical

data includes the

automotive division

15 largest 2013e P/E appreciation, -3m (%)

-20

0

20

40

60

80

SAS

O

ut

ok

um

pu

T

al

v

iv

aar

a M

ini

ng

C

o

V

es

tas

R

aut

ar

uuk

k

i

D

/S

N

or

den

D

N

O

I

nt

er

nat

io

nal

A

S

A

E

n

iro

SSAB

P

andor

a

B

ang &

O

luf

s

en

NK

T

Ho

ld

in

g

Lundi

n M

ini

ng

P

ros

af

e

N

obi

a

P/E 13 change, -3M Price ch, -3M

248

234

193

142

Source: FactSet

15 largest 2013e P/E declines, -3m (%)

-50

-40

-30

-20

-10

0

10

20

A

lm

. B

rand

N

or

s

k

e S

k

og

A

lk

-A

bel

lo

T

rans

m

ode

B

W

Offs

h

o

re

M

oder

n

T

im

es

G

roup

Lundbec

k

Or

ifl

a

m

e

K

ongs

ber

g

G

ruppen

C

las

O

hl

s

on

HiQ

F

LS

m

idt

h

&

C

o

S

we

c

o

AF

-G

roup

Int

rum

J

us

ti

ti

a

P/E 13 change, -3M Price ch, -3M

Source: FactSet

15 highest 2012 dividend yields (%)

5

6

7

8

9

10

11

12

B

W

Offs

h

o

re

No

rt

h

A

tla

n

tic

Dr

illin

g

S

anom

a

E

k

or

nes

A

tea

NCC

F

red.

O

ls

en

E

ner

gy

E

lis

a

HiQ

B

ilia

K

v

aer

ner

Or

ifl

a

m

e

P

eab

S

tor

a E

ns

o

D

uni

Source: FactSet

Estimate cuts behind

the majority of these

moves

Significant multiple

expansion for many

names...

...while consumer

stocks HiQ and

Intrum J. have not

re-rated, though the

contraction is small

15 stocks yielding

>6%

Oil service,

consumer and

construction names

dominate

Payout ratio – top 25

Mcap

(EURm )

Perf

-3m (%)

Pay-out r.

12e %

Div Yield

2012e

Net debt /

EBITDA 12e

Net debt /

Equity 12e

BW Offshore

364

-41

-750

11.0

5.2

1.5

Rautaruukki

732

3

-115

5.7

3.8

0.7

Kvaerner

561

20

140

6.9

-3.5

-0.6

Elisa

2,916

9

100

7.7

1.5

0.9

Ekornes

439

2

95

8.6

-0.8

-0.2

Atea

804

15

93

8.5

0.0

0.0

Axis

1,323

12

92

3.7

-0.6

-0.5

SSAB

1,667

-19

87

4.3

5.2

0.6

DFDS

566

0

87

4.9

2.3

0.4

HiQ

204

-8

85

7.2

-0.8

-0.3

Peab

1,076

-5

81

6.7

3.6

0.9

Stora Enso

3,891

-3

80

6.3

2.5

0.5

Sanoma

1,118

5

77

8.7

2.2

0.7

Oriflame

1,419

-6

77

6.9

1.2

1.0

Nordic Semiconductor

370

-2

77

3.5

-1.2

-0.5

Stockmann

1,133

1

76

3.8

4.4

0.9

Kesko

2,201

12

75

5.0

0.5

0.1

Betsson

802

-17

74

6.1

0.0

0.0

Clas Ohlson

646

-13

73

5.1

-0.1

0.0

Veidekke

851

10

73

5.9

1.0

0.4

NCC

1,598

3

73

7.9

1.6

0.5

Axfood

1,515

10

73

5.0

0.4

0.2

Fred. Olsen Energy

2,322

22

72

7.8

0.8

0.3

North Atlantic Drilling

1,729

15

71

9.5

3.9

2.6

Royal Unibrew

661

21

70

5.1

0.9

0.4

Source: FactSet/Handelsbanken Capital Markets

15 lowest forward P/E

3

4

5

6

7

8

9

E

n

iro

A

llia

n

c

e

O

il

S

onga O

ff

s

hor

e

G

ol

den O

c

ean

S

tor

ebr

and

DNO

Int

er

nat

ional

…

B

W

Offs

h

o

re

N

or

w

egi

an

A

ir

S

hut

tl

e

N

or

ec

o

B

ilia

P

eab

N

ew

W

av

e

N

or

th A

tl

ant

ic

Dr

illin

g

P

andor

a

P

ros

af

e

Source: FactSet

Will steel companies

really pay out as

expected?

Will Peab pay 81%

of EPS given

gearing?

25 stocks with

payouts above 70%

We say the risk of

cuts have increased

The highly-geared

bunch

15 lowest trailing P/E

3

4

5

6

7

8

9

10

E

n

iro

A

llia

n

c

e

O

il

S

onga O

ff

s

hor

e

G

ol

den O

c

ean

No

rt

h

A

tla

n

tic

Dr

illin

g

S

tor

ebr

and

B

ilia

P

andor

a

S

anom

a

N

ew

W

av

e

C

ar

got

ec

F

red.

O

ls

en

E

ner

gy

B

ol

iden

NCC

S

ec

ur

it

as

Source: FactSet

15 highest forward P/E

15

20

25

30

35

40

45

50

55

V

es

tas

T

al

v

iv

aar

a M

ini

ng

C

o

A

lk

-A

bel

lo

SAS

D

/S

N

or

den

R

aut

ar

uuk

k

i

B

ang &

O

luf

s

en

CDO

N G

ro

u

p

E

lek

ta

C

hr

. H

ans

en

S

c

hi

bs

ted

A

xi

s

O

per

a S

of

tw

ar

e

S

im

c

o

rp

K

appA

hl

Source: FactSet

15 lowest 12m forward P/B

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

P

A

R

es

our

c

es

N

or

s

k

e S

k

og

SAS

E

n

iro

S

onga O

ff

s

hor

e

O

ut

ok

um

pu

N

or

ec

o

A

rc

her

V

es

tas

B

W

Offs

h

o

re

SSAB

S

par

N

or

d

EAC

A

lm

. B

rand

G

ol

den O

c

ean

Source: FactSet

If trailing EPS is a

good reflection of

sustainable earnings

then this group is

way too cheap

Still only a handful

above 20x forward

EPS

Steel, P&P, oil,

renewable and

highly-geared oil

service

EV/S relative to EW, top decile

90 100 110 120 130 140 150 160 170 180 190 200 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 92 94 96 98 100 102 104 Oc t … No v De c … J an … F eb Ma r Ap r Ma y Ju n Ju l Au g Se p Oc t …EV/S relative to EW, bottom decile

20 30 40 50 60 70 80 90 100 110 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 82 84 86 88 90 92 94 96 98 100 102 Oc t … No v De c … J an … F eb Ma r Ap r Ma y Ju n Ju l Au g Se p Oc t …

Div yielders relative to EW, top decile

90 100 110 120 130 140 150 160 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 95 100 105 O c t 2011 No v D ec 2011 J an 2012 F eb Ma r Ap r Ma y Ju n Ju l Au g Se p O c t 2012

P/BV relative to EW, bottom decile

60 70 80 90 100 110 120 130 140 150 160 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 70 75 80 85 90 95 100 105 Oc t … No v De c … J an … F eb Ma r Ap r Ma y Ju n Ju l Au g Se p Oc t …

Source: Handelsbanken Capital Markets, Factset (EW = equally weighted index)

Value rebound

halted when QE3

was announced

Most expensive

decile flat since start

of September

High yielders also

flat in past six weeks

Low-quality value

mirrors normalised

value following QE3

Revisions

Estimates have remained under pressure, with our revision indicators deep in negative territory. We continue

to argue that 2013 estimates look exuberant, given that the prevailing consensus forecasts imply margins

improving 150bp on 3% of top-line growth and that 93% of the universe is expected to post a margin

improvement in 2013. Further, we find earnings dispersion at extremely low levels, signalling confidence in

estimates, in our view falsely. We consequently expect dispersion to widen as we exit the reporting season

and hope that analysts take down 2013e estimates. We maintain that during this process it will be unusually

difficult to find earnings upgrade candidates, while simply betting on the stocks currently seeing the best

revision pattern is too risky. The revision factor (top decile) has in fact been flat since May, though recent

weeks have shown some outperformance. The bottom decile has seen strong alpha generation lately, which

in effect could spell trouble for the entire universe, as downgrades appear to have been punished.

EPS trend (EUR)

14

16

18

20

22

24

26

28

30

Q

4 2009

Q

1 2010

Q

2 2010

Q

3 2010

Q

4 2010

Q

1 2011

Q

2 2011

Q

3 2011

Q

4 2011

Q

1 2012

Q

2 2012

Q

3 2012

Q

4 2012

Earnings Per Share 2011 Earnings Per Share 2012 Earnings Per Share 2013

Source: FactSet

HCMe EPS revision indicator

0.0

0.5

1.0

1.5

2.0

2.5

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Nordics < 4bn

neutral

Source: FactSet

Estimates continue

to slide, but 2013e

cuts are not keeping

pace with 2012e

We expect the

revision pattern to

stay negative

EBIT margin outcome vs. expectations

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

5%

6%

7%

8%

9%

10%

11%

12%

2005

2006

2007

2008

2009

2010

2011

2012

2013

Source: FactSet

Sales growth expectations vs. outcome

2012

2011

2010

2009

2008

2007

2006

2004

2005

2003

2013

-10%

-5%

0%

5%

10%

15%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Source: FactSet

EPS growth trend

0%

5%

10%

15%

20%

25%

30%

H

2 2009

H

1 2010

H

2 2010

H

1 2011

H

2 2011

H

1 2012

H

2 2012

EPS % Change 2012 EPS % Change 2013

Source: FactSet

2013 margins are set

to rise 150bp

2012e margins

below 2011, which

was below 2010

Why is 2013 up

150bp on 3%

top-line growth?

Growth in excess of

5% needed to

sustain >7% EBIT

margin

2013 growth

expectations keep

climbing – now 25%

Dispersion in EPS trend (median of universe)

5%

10%

15%

20%

25%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Nordics < 4bn

Source: FactSet

HCMe sales revision indicator

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Nordics < 4bn

neutral

Source: FactSet

Recommendation trend

1.45

1.50

1.55

1.60

1.65

1.70

1.75

1.80

1.85

1.90

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Source: FactSet

Rating definition: 1 Buy, 2 Hold, 3 Sell

EPS dispersion at

record lows in an

unusually uncertain

economic setting

As it rises, it gets

harder to find EPS

upgrade candidates

Revision indicator at

depressed levels,

implying a

weakening outlook

Analysts getting

more cautions after

being close to record

bullish this summer

Figure 1: Proportion of companies with EBIT margin improvement

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012e

2013e

Nordic: margin improvement vs. Previous year

Source: FactSet

Bottom 15 2013e EPS revisions, -3m

-80%

-43%

-7%

30%

O

ut

ok

um

pu

T

al

v

iv

aar

a M

ini

ng

C

o

SAS

V

es

tas

SSAB

R

aut

ar

uuk

k

i

D

/S

N

or

den

A

rc

her

B

W

Offs

h

o

re

N

or

ec

o

EAC

E

n

iro

N

ew

W

av

e

A

llia

n

c

e

O

il

NK

T

Ho

ld

in

g

EPS revisions Price change -3M

Source: FactSet

Top 15 2013e EPS revisions, -3m

-10%

0%

10%

20%

30%

40%

50%

N

or

s

k

e S

k

og

A

lm

. B

rand

A

ur

iga I

ndus

tr

ies

A

lk

-A

bel

lo

K

e

m

ira

CDO

N G

ro

u

p

S

im

c

o

rp

AF

-G

roup

Ler

oy

S

eaf

ood G

roup

P

et

rol

eum

G

eo

-S

er

v

ic

es

S

par

N

or

d

N

or

w

egi

an

A

ir

S

hut

tl

e

P

andor

a

R

oy

al

U

ni

br

ew

K

ongs

ber

g

G

ruppen

EPS revisions Price change -3M