Global Networking in Wireless

Teletechnology Business

Lasse Baldauf, Michael Lovejoy, Jarmo Karesto, Laura Paija

Global Networking

in Wireless Teletechnology Business

Lasse Baldauf Jarmo Karesto Michael Lovejoy Laura Paija Technology Review 114/2001 Helsinki 2001

Tekes – your contact for Finnish technology

Tekes, the National Technology Agency of Finland, is the main financing or-ganisation for applied and industrial R&D in Finland. Funding is granted from the state budget.

Tekes’ primary objective is to promote the competitiveness of Finnish indus-try and the service sector by technological means. Activities aim to diversify production structures, increase productivity and exports, and create a foun-dation for employment and social well-being. Tekes supports applied and industrial R&D in Finland to the extent of some EUR 390 million, annually. The Tekes network in Finland and overseas offers excellent channels for co-operation with Finnish companies, universities and research institutes. Technology programmes – part of the innovation chain

The technology programmes for developing innovative products and cesses are an essential part of the Finnish innovation system. These pro-grammes have proved to be an effective form of cooperation and networking for companies and the research sector. Technology programmes promote development in specific sectors of technology or industry, and the results of the research work are passed on to business systematically. The programmes also serve as excellent frameworks for international R&D cooperation. Cur-rently, a total of about 50 extensive national technology programmes are un-der way.

_ _ _

Finpro – Finnish business solutions worldwide

Finpro is an efficient expert and service organization. Finpro provides ser-vices, support and information to help Finnish companies enter the interna-tional market as swiftly, safely and efficiently as possible.

In addition to Finpro’s operations in Finland, Finpro has 48 Finland Trade Centers in 38 countries worldwide. Finpro´s global expertise areas focus on the most important industry sectors of the Finnish economy. Finpro’s com-petence focuses on the industry sectors and market areas where Finnish companies have a special competitive advantage or that are interesting as potential markets.

ISSN 1239-758X ISBN 952-457-044-0

Cover: LM&CO Page layout: DTPage Oy Printers: Paino-Center Oy, 2001

Foreword

Networks, inter-firm alliances and cooperation between companies and the research community are important elements of today’s business operations. Networking means not only vertical rela-tionships, i.e. buyer-supplier relarela-tionships, but also cooperation in manufacturing, marketing and in research and development. The depth of cooperation varies however, from subcontracting to strategic partnerships.

The driving forces behind networking are access to new markets and, increasingly, a tendency among firms to focus on core competence of the firm, thus leading to outsourcing of non-critical activities. Companies are operating in an industrial ecosystem of mutually supporting, and interde-pendent companies and other partners. To a large extent, today’s competition means competition between these networks.

For the National Technology Agency of Finland, Tekes networking is a strategic objective and a central element of all R&D projects. The Agency has extensive experience and knowledge of net-working and cooperation trough national technology programmes, but its focus has been mainly on strategic R&D partnerships between national players.

Although networking is an important element in private and public sector organizations, the impe-tus behind international networking as well as its mechanisms and benefits are not widely known. This report aims at helping companies initiate international cooperation in the field of mobile com-munications; it is designed as a networking aid providing vital information about networking envi-ronments in the most important mobile communications markets.

This report has been prepared by a Finpro working group supported by ETLA, the Research Insti-tute of the Finnish Economy, and other experts in the field of telecommunications. Tekes wishes to express its warm thanks to the project team for excellent work collecting benchmarking informa-tion on key players in the telecommunicainforma-tions industry and for analysing internainforma-tional networking mechanisms. Special thanks are also given to the steering group, composed of companies, the Finpro team and the Tekes representative. Through benchmarking visits and highly productive dis-cussions this group contributed to gaining a deep understanding of the key elements of networking. We hope you will find this report useful for your international business development.

Table of contents

Foreword

1 Executive summary · · · 1

2 Introduction · · · 3

3 The ICT cluster in the Finnish economy · · · 6

Laura Paija, ETLA 3.1 ICT cluster identification · · · 6

3.1.1 What is a cluster? · · · 6

3.1.2 The ICT cluster environment · · · 6

3.2 The economic relevance of the ICT cluster · · · 7

3.2.1 Domestic market position · · · 7

3.2.2 Foreign trade and international market position · · · 8

3.3 The evolution of the ICT cluster· · · 9

3.3.1 Network operation – a fragmented monopoly market· · · 9

3.3.2 The emergence of the telecommunications industry · · · 11

3.4 The factors of the competitive advantage · · · 13

3.4.1 Firm strategy, structure and rivalry · · · 13

3.4.2 Factor conditions· · · 13

3.4.3 Demand conditions · · · 14

3.4.4 Supporting and related industries · · · 14

3.4.5 Government · · · 15

3.4.6 Coincidental factors· · · 16

3.5 Dynamics in the ICT cluster · · · 16

3.5.1 The government as an early catalyst of cluster development · · · 16

3.5.2 Exceptional demand conditions have offered home-base advantage · 17 3.5.3 Intense firm interaction has induced upgrading · · · 18

3.5.4 Deterioration in labor supply, improvement in capital supply · · · 19

3.5.5 World-wide liberalization – pivotal and perfectly timed for Finland· · · · 19

3.6 Future opportunities and threats · · · 20

3.6.1 Market positions at stake in the third generation competition · · · 20

3.6.2 Globalization behind most of the opportunities and threats · · · 21

3.6.3 Small firm size limits seizure of opportunities · · · 21

3.6.4 Dynamic cluster relations support specialization and upgrading · · · 22

3.6.5 Electronic business will have implications on firm interaction · · · 22

3.6.6 How to guarantee sufficient supply of skilled labor? · · · 23

3.6.7 Will content production grow into the third base of the ICT cluster? · · 23

4 Trends in wireless services and products · · · 25

Jarmo Karesto, Finpro 4.1 Drivers in wireless content· · · 27

4.2 From mobile phones to wireless devices · · · 27

4.3 Customer segmentation · · · 29

4.4 Alternative network connections · · · 29

4.5 Wireless Internet · · · 29

4.7 Personality · · · 30

4.8 Location identity · · · 30

4.9 Safety and security · · · 31

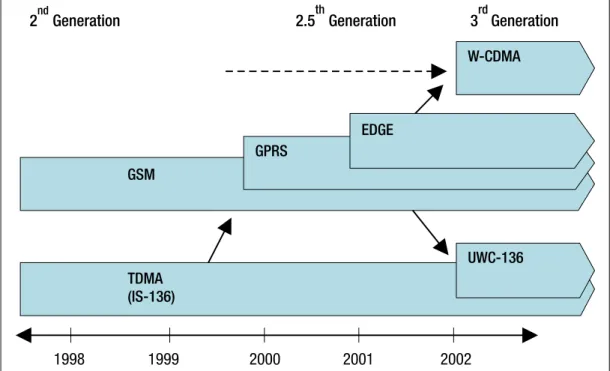

5 Promising standards and technology platforms· · · 33

Jarmo Karesto, Finpro 5.1 The evolution of third generation cellular networks · · · 33

5.2 3G technology strategy plans by operators in major markets· · · 36

5.3 CDMA terminology and definitions · · · 38

5.4 W-CDMA · · · 39

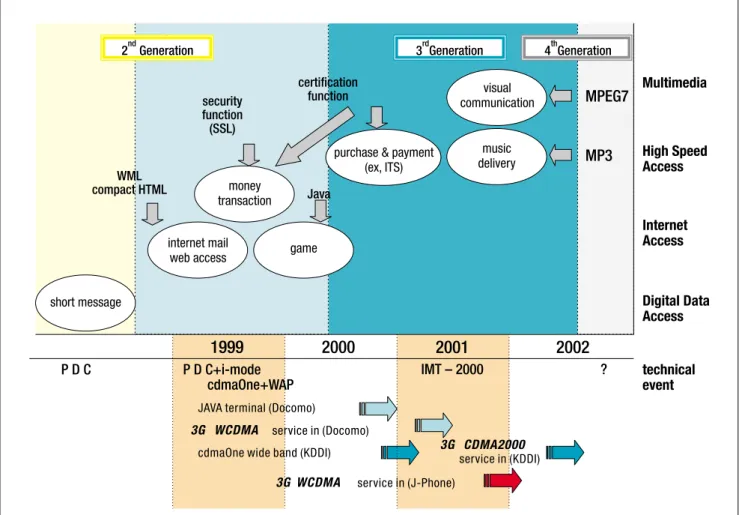

5.5 WAP · · · 39

5.6 I-mode and other Japanese 3G approaches· · · 40

5.7 Bluetooth · · · 41

5.8 Wireless local area networks · · · 41

5.9 Operating systems in mobile devices, EPOC, Palm OS, and Windows CE · · · 41

5.10 Mobile Internet Protocol Version 6 · · · 42

5.11 Major technology suppliers by key categories · · · 43

5.12 Useful links to get more free information: · · · 44

6 Trends in The Global business environment · · · 45

Michael Lovejoy, Finpro 6.1 “Turbulent times” · · · 45 6.2 Convergence · · · 45 6.3 Globalization · · · 46 6.4 Transnationalism · · · 47 6.5 Virtual Integration· · · 47 6.6 Importance of place· · · 50

6.7 New model of production in the ICT industry · · · 52

6.8 Globalization of the EMS model · · · 53

6.9 Types of outsourcing services offered and utilized · · · 55

6.10 Thoughts for the future · · · 57

7 Generic growth strategies for technology companies in the network environment · · · 59

Vipul Chauhan, Helsinki Univeristy of Technology, Jarmo Karesto, Finpro 7.1 Product strategy · · · 60

7.2 Strategic roles of collaboration · · · 61

7.3 Competence leverage in key customer relationship · · · 62

7.4 Key customer-driven growth strategies· · · 63

7.5 Key customer risk · · · 64

7.6 Managing Intellectual Property · · · 64

7.6.1 IP Rights Protection: Strategic Aspect · · · 64

7.6.2 IP Rights in Relationships · · · 64

8 Getting global, road map for technology firms · · · 65

Lasse Baldauf, Finpro 8.1 Which direction? · · · 65

8.2 Needs and requirements for global business · · · 65

8.3 The process for establishing a business abroad · · · 68

8.4 Wireless telecommunications industry value chain · · · 69

8.5 Connections to the business environment · · · 72

8.6 Importance of the cluster for SME’s · · · 73

9 Benchmarked companies · · · 75

Lasse Baldauf, Finpro 9.1 General · · · 75

9.2 Motorola· · · 75

9.2.1 Key figures, major businesses· · · 75

9.2.2 Global map · · · 75

9.2.3 Business strategy · · · 76

9.2.4 Research and development· · · 76

9.2.5 Distributors · · · 76

9.2.6 Contract electronic manufacturers · · · 76

9.3 Siemens · · · 77

9.3.1 Key figures, major businesses· · · 77

9.3.2 Global map · · · 77

9.3.3 Business strategy · · · 77

9.3.4 Research and development· · · 78

9.3.5 Distributors · · · 78

9.3.6 Contract electronic manufacturers · · · 78

9.4 Matsushita (Panasonic) · · · 79

9.4.1 Key figures, major businesses· · · 79

9.4.2 Global map · · · 79

9.4.3 Strategy · · · 79

9.4.4 Research and development· · · 80

9.4.5 Contract manufacturers· · · 80

9.5 Samsung · · · 80

9.5.1 Key figures, major businesses· · · 80

9.5.2 Global map · · · 80

9.5.3 Strategy · · · 80

9.5.4 Research and development· · · 80

9.5.5 Contract electronics manufacturers · · · 80

9.6 Nortel Networks · · · 81

9.6.1 Key figures, major businesses· · · 81

9.6.2 Global map · · · 81

9.6.3 Strategy · · · 82

9.6.4 Research and development· · · 82

9.6.5 Outsourcing, suppliers · · · 82

9.7 Cisco Systems · · · 82

9.7.1 Key figures, major businesses· · · 82

9.7.2 Global map · · · 82

9.7.3 Strategy · · · 82

9.7.4 Research and development· · · 83

9.7.5 Distributors · · · 83

9.7.6 Contract electronic manufacturers · · · 83

9.8 Solectron · · · 83

9.8.1 Key figures, major businesses· · · 83

9.8.2 Global map · · · 83

9.8.3 Strategy · · · 83

9.8.4 Research and development· · · 84

9.9 Celestica · · · 84

9.9.1 Key figures, major businesses· · · 84

9.9.2 Global map · · · 85

9.9.3 Strategy · · · 85

9.9.4 Research and development· · · 85

9.9.5 Key customers· · · 85

9.10 Flextronics · · · 85

9.10.1 Key figures, major businesses· · · 85

9.10.2 Global map · · · 85

9.10.3 Strategy · · · 86

9.10.4 Research and development· · · 86

9.10.5 Key customers· · · 86

10 Conclusion · · · 87

Appendix 1 The NACE codes utilized in the calculation of economic indicators for the ICT cluster · · · 89

Appendix 2 Measuring the export specialization of a country · · · 91

1

Executive summary

Production of Telecommunications equipment in Finland increased from about 5 Billion Fim in 1990 to nearby 80 Billion Fim in 2000. The production incorporates directly several hundred companies in electronics, metal, plastic and software industries and employs approximately 40– 50.000 people. Major part of the production was exported. This miraculous development is a sum of many factors, which have successfully supported each other. Liberaliza-tion of telecom services in early stage, building NMT net-work jointly with the other Nordic countries, great success of mobile phones worldwide, opening of telecom services for competition globally and growth of Nokia are all fac-tors which have contributed to the success and created a very strong telecommunication industry in Finland. As a result the Finnish telecom technology know-how today is world class.

However this blessed situation is extremely fragile and continuous growth is not at all granted. Nokia’s role as a lo-comotive of the whole cluster in Finland will probably not continue forever. Nokia is growing fast outside Finland. More and more decision makers in Nokia’s organization are representing other nationalities than Finns and we all know how important personal relationships are in business. At this moment the most critical issue is the international-ization of the cluster. If the smaller technology and service companies in the cluster can expand their business to new customers globally, it reduces their operational risk and the impact on the whole Finnish economy.

The companies in telecom business face new type of chal-lenges. Technology is developing fast and the future is not at all predictable. The business is much more innovation driven than capital driven. Merge of Internet, mobile phones and computers may create totally new needs for services and products, which are not identified yet. The business environment is moving fast. Earlier several lo-cally operating companies in each business were sharing the market but the trend is to smaller number but globally operating key players. This is a result of globalization. R&D and production are organized globally according to the rules of the business not by following artificial borders and barriers. This new world map shows how R&D and

production are concentrating in few locations. In the “R&D map” Finland and Sweden are centrally located beside USA and Japan. Manufacturing sites are locating near main markets. The other trend is networking. Companies are outsourcing non-critical activities and enhancing col-laboration with partners and even competitors. Nokia is a good example of this. Totally new actors, like global pro-viders of contract manufacturing services, have emerged in the business rebuilding the value chain. Speed has become a crucial competitive edge. Cisco System’s famous slogan “Innovations by acquisitions” describes well the phenome-non. Companies are no longer doing everything by them-selves anymore as it was still few years ago.

Globalization and networking open totally new possibili-ties for smaller technology companies but the old strategies do not work any more. Global approach, focus on cus-tomer, concentration on core competencies, understanding value networks and the progress in business environment, networking with others, speed and capability to finance the fast growth are raw materials in building a successful strat-egy in telecom technology business. A key customer rela-tionship can be a springboard to new customers and even to new businesses as many of the Nokia’s smaller partners have recognized. Innovations, work processes, references, social competencies among many others are gaining im-portance beside technical competencies in new business environment.

What should then be done to ensure that success continues? As mentioned earlier the most critical issue is the interna-tionalization of the cluster. It is important to capitalize on the success with Nokia when entering new markets. This can translate to a speedier access to new customers and ability to manage the business through international net-working. The focus of the national system of innovation should be more on innovativeness, global customer needs and ability to help the smaller companies in organizing their operations in international market environment. The key issue for public supporting organizations involved is to understand the new logic of the global telecom business and develop their services and mutual cooperation accord-ingly.

2

Introduction

This report is an outcome of the Global Networking in Mo-bile Teletech business project conducted by the leading technology companies in mobile business in Finland (CCC Group, Elektrobit Oy, Fortel Invest Oy, JOT Automation Oy, Orbis Oy and Nokia Mobile Phones) Tekes (the Na-tional Technology Agency) and Technopolis Oyj. Finpro has been in charge of managing the project and producing this report.

The goal of the project was to support the strategy process of each participant in the fast transforming business envi-ronment. The major focus was on mobile technology busi-ness, global business environment, corporate strategies, networking and small and medium-sized enterprise ap-proach. Mobile services and applications were just briefly discussed when they had some relevance with technology business (but otherwise they were left out of this study). The project was carried out between fall 2000 and summer 2001. The working methods were workshops, study tours to USA, Germany and Japan and the company bench-marking studies. ETLA (the Research Institute of Finnish Economy) and Helsinki University of Technology were helping by carrying out part of the research work.

The chapter ICT Cluster in Finnish Economy is a brief but an important review of the emergence and development of the telecom industry in Finland. The formation of the clus-ter and the growth of Nokia have mainly taken place in 1990’s but their roots are much deeper in the history. Spe-cial focus is put on cluster analysis to help the reader to un-derstand the importance of various elements in the business environment which are discussed in later chapters. The ICT Cluster in Finnish Economy chapter was written by Laura Paija from ETLA.

The Chapter Trends in Wireless Services and Products summarizes the various thoughts and views about the emerging customer needs defining the direction for the whole business. The chapter is not a comprehensive study of the subject but rather a summary of the those issues on which the leading people in the industry believe today. Customer needs concerning services and physical products are driving the business but hardware products and soft-ware applications make the services possible.

The chapter Emerging Standards and Technology Plat-forms is worked out similar way as the previous chapter. The focus in this chapter has been on identifying those technological standards, either official or de facto, and platforms that are supposed to play important role in the foreseeable future. Standards and platforms create a solid base for fast changing, short time living products and ser-vices aimed at end users. They can also be important corner stones in strategies of small technology companies. The chapter Trends in Global Business environment dis-cuss the forces and development trends, which are redraw-ing the business environment makredraw-ing the old strategies ob-solete. Liberalization of global trade and investments makes it possible for businesses to reorganize globally their activities following the laws of business, not accord-ing to artificial regulations and boundaries. Fast develop-ing information and communication technologies and lo-gistical services greatly support this trend. Global business networks are emerging. Firms focus on their core compe-tencies and grow their added value through alliances and cooperation. Old value chains are redrawn. Nokia, Elcoteq, JOT Automation and Elektrobit are good examples of com-panies, which have understood the ongoing change and have been able to quickly utilize the emerging opportuni-ties in their businesses.

The chapter Generic Growth Strategies for Technology Companies in Network Environment focuses on corporate strategies. This chapter is an introduction to the following chapter Getting global, Road Map for Technology Firms. The chapter introduces and offers generic strategy alterna-tives for small and medium-sized technology enterprises in network environment. This part was created together with the Institute of Strategy and International Business of Helsinki University of Technology. In the chapter Getting global, Road Map for Technology Firms the focus is turned to mobile telecom business in global market envi-ronment. The chapter introduces business cases and mod-els and is created by studying various Finnish and interna-tional companies in Europe, USA and Asia.

The chapter Benchmarked Companies introduces several leading technology companies, their strategies and activi-ties in mobile business. The companies were selected based on their importance for Finnish industry or based on their interesting business models. The benchmarked com-panies were thoroughly studied and interviewed. Summary of strategies, business models and other key findings are presented in this chapter.

The last chapter Conclusions outlines the key findings of this project and gives recommendations to governmental and public business development organizations working closely with the ITC-cluster.

3

The ICT cluster in the Finnish economy

Laura Paija, ETLA

3.1

ICT cluster identification

3.1.1 What is a cluster?

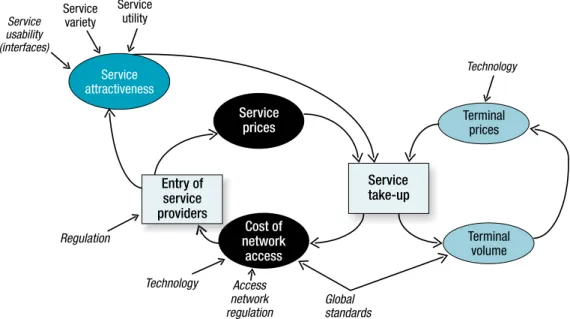

1Clusters are used to describe a network of organizations in which competitive advantage grows from dynamic interac-tion between actors, both public and private. Cluster rela-tions spur innovation and upgrading through spill-overs and knowledge transfers.

There are different environmental determinants influenc-ing the competitiveness of the cluster. These include factor conditions; demand conditions; related and supporting in-dustries; and firm strategy, market structure and rivalry. Clusters are exposed to external forces, like government actions and chance, including changes in firms’ global op-erational environment.

Dynamic interaction between these factors of competitive advantage gives rise to a self-enforcing system – either

vir-tuous or vicious, depending on the state of the factors (fig-ure 3.1).

3.1.2 The ICT cluster environment

The network environment of the firms related to the infor-mation and communications technology (ICT) is depicted in figure 3.2. The ICT term is in general use worldwide but it has different meaning country by country. In Finland the weight is on telecommunication and in this study espe-cially on mobile technology.

The ICT infrastructure, terminals and services constitute a complex regarded as the key industries, whose interactions with other industries differ in their dimensions. There are vertical relationships with suppliers in the supporting in-dustries and with customers; horizontal linkages between competitors within the key industries; and diagonal inter-faces with third-party sectors, or related industries. Recently, the cluster portrait has become increasingly blurred. Three megatrends, namely convergence of net-works, terminals and services, digitalization, and

deregu-Firm strategy,

structure and

rivalry

Demand

conditions

Related and

supporting

industries

Factor

conditions

Government

Chance

Figure 3.1. The dynamic system of factors of competitive advantage. Source: Porter (1990).

lation have lead to a significant restructuring of the clear-cut ‘telecommunications cluster’ that we were able to identify a few years ago.2The actors of the cluster are pene-trating new, and to a large extent one another’s business ar-eas. Vertical mergers across traditional sectoral boundaries are used to strengthen new competitive positions.

These fundamental changes lie behind the need to expand the previously utilized notion of the telecommunications cluster to the ICT cluster, which encloses a wider array of technology enabling digital services hardly existing in the early 1990s.

Owing to the generic nature of the ICT, the cluster has in-numerable interfaces with other industrial clusters. Repre-sentative crossing points are found in the related industries (figure 3.2), in which new sector-specific applications of the ICT are being developed. In addition, manufacturing industries are actively adopting new equipment developed in the interface of the clusters.3

The overall economic impact of the ICT is likely to be even more powerful in the demand-side of the technology than in the supply-side, since innovative applications of the technology are about to revolutionize traditional business models in a number of sectors.

KEY INDUSTRIES

NETWORK OPERATION

NETWORK SERVICES AND

DIGITAL CONTENT

PROVISION

ICT EQUIPMENT

Hardware and

software

Terminals

Fixed and mobile

network systems

Digital-TV

Cable-TV

Internet

Data networks

Fixed and mobile

networks

Content (value added)

services

Basic voice and

data services

SUPPORTING INDUSTRIES

Education

and R&D

Contract

manufacturing

Parts and components

manufacturing

RELATED INDUSTRIES

Advertising

Entertainment

Traditional

media

Health

care

Banking

Booking

services

Education

Public

services

Consumer

electronics

ASSOCIATED SERVICES

CUSTOMERS

Distribution

channels

Venture

capital

Consultancy

Figure 3.2. ICT cluster chart.

2 Luukkainen & Mäenpää (1994) carried out the first telecommunications cluster identification study as part of the initial national cluster research project, coordinated by ETLA (Hernesniemi et al., 1995).

3 Examples of industrial applications of ICT are: remote maintenance of machines in the mechanical engineering, self-supported health monitoring, location techniques in forestry, and intelligent consumer electronics.

3.2

The economic relevance of

the ICT cluster

3.2.1 Domestic market position

The key figures of the ICT cluster for 1998 are presented in table 3.1.4The gross value of the cluster was EUR 17.5 bil-lion. Manufacturing of equipment and their electronic components dominated the cluster, accruing two thirds of the production value, while the share of telecommunica-tions services was one fifth of the value. The significance of software supply and other IT services is underestimated

in the table since ICT equipment include an important amount of software, and the construction of telecommuni-cations networks involves IT services that is included in the sales of equipment manufactures. The value-added gener-ated in the cluster was in average 43 per cent of the gross value, ranging though between the sub-sectors of the clus-ter (see table).

Figure 3.3 reveals the breakthrough of communications products in domestic production. Since Nokia’s recovery (from 1992 onwards), the value-added in ICT manufactur-ing has grown at the average annual rate of 35 per cent. In 1998, the cluster contribution to the GDP was 6.6 per cent.

ICT Manufacturing ICT Services Cluster (total)

Telecom services Software, IT services Euros (millions) Share of prod. Euros (millions) Share of prod. Euros (millions) Share of prod. Euros (millions) Share of prod. Production Value added Labor cost Exports Imports 11,631 3,728 951 9,543 1,694 100% 32% 8% 82% 15% 3,408 2,045 682 110 150 100% 60% 20% 3% 4% 2,500 1,724 706 932 578 100% 69% 28% 37% 23% 17,538 7,497 2,339 10,585 2,422 100% 43% 13% 60% 14%

Table 3.1. Key economic indicators of the ICT cluster in 1998.

Source: Statistics Finland, Ministry of Transport and Communications.

1975 1980 1985 1990 1995 2000 0 % 1 % 2 % 3 % 4 % 5 % Equipment Telecom services

Figure 3.3. The share of ICT value-added on GDP.

Source: Statistics Finland, Ministry of Transport and Communications.

Note:The figure excludes software and IT services as well as computers due to lacking data. There is a slight discontinuity in the data between 1994 and 1995 due a change in statistical classification.

4 Clusters do not follow sectoral boundaries. Sectoral data inevitably includes firms not active in the cluster, and respectively, excludes many important actors. For example, national statistics do not yet enable quantification of digital content production. However, the data on telecom operation and software production include some of these activites. Further, it is necessary to combine the data for electronic components (inputs) and ICT equipment (outputs), since many of the input suppliers are classified under the sector code of their main clients. Despite classification problems, the national data applied here covers the crucial business sectors of the cluster. See Appendix for the NACE codes included.

With its 75,000 employees, the ICT cluster accounted for 3 per cent of the total national employment in 1998. Nokia alone employed 21,000 persons in Finland and thus ac-counted directly for almost 30 per cent of the cluster employ-ment. According to estimations Nokia employed indirectly an additional 14,000 persons through its first-tier subcon-tractor firms.5As production networks go further to sequen-tial tiers, the employment effect of the major firm is signifi-cant, but cannot be readily quantified. However, without the chronic shortage of skilled labor the employment potential of the cluster would allow much higher recruitment.

3.2.2 Foreign trade and international

market position

In 1998, the export share of the total ICT cluster production was 60 per cent (table 3.1). In telecommunications services

exports represented an insignificant share (3 per cent), while in equipment manufacturing about 85 per cent of the sales was accrued abroad. In 1999, ICT product exports represented 20 per cent of the total exports while 1990, the share was only five per cent.

Figure 3.4 of the trade balance in cluster products illus-trates the dominance of telecommunications equipment in the Finnish ICT cluster trade. Despite the persistent rise in ICT exports, the current value of non-telecommunications products has remained virtually constant. The growth in imports, in turn, depicts the dependence of the electronics industry of standard components (semi-conductors) rather than a rise in the demand of foreign telecommunications equipment.

The pace and intensity of the growth in the Finnish elec-tronics industry has been extraordinary throughout the

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 0 1 2 3 4 5 6 7 8 9 Cluster imports Cluster exports Telecom imports Telecom exports

Figure 3.4. Foreign trade in ICT and telecommunications products (millions of Euros).

Source: National Board of Customs.

12 28 14 23 25 31 25 42 40 30 31 23 27 16 15 8 6 16 19 26 18 18

Electronics and electrotechnics industry

Metal and engineering industries

Paper industry

Mechanical wood industry Other

1990 1980

1970

1960 1999

Figure 3.5. Export shares by industry groups 1960–1999.

Source: National Board of Customs.

1990s. It has lead to an industrial restructuring in the for-mer forest and metal based economy, in which knowledge has replaced capital, raw materials and energy as the domi-nant factors of production. During the past decade, Finland became the world leader in high-tech trade surplus (high-tech exports/imports ratio) among indigenous high- (high-tech producers. The share of electronics and electrotechnics ex-ports has almost tripled at the expense of pulp and paper and metals, representing close to 30 per cent of the total manufacturing exports in 1999 (figure 3.5).

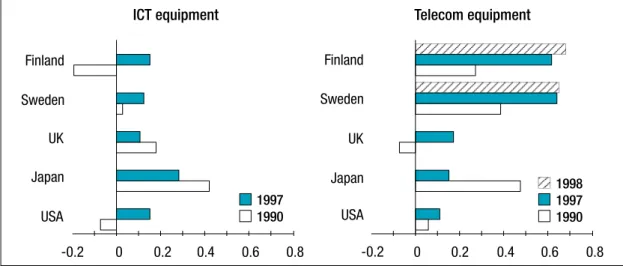

In OECD comparison, Finland ranked the second in ICT exports specialization after Japan in 1997 (figure 3.6 left; see Appendix 2 for the definition). Limiting the compari-son to telecommunications equipment6reveals that Finland had become the most telecommunications-oriented coun-try in its exports in 1998 (figure 3.6 right). During the 1990s, Japan has lost its lead to the two Nordic countries, which have been racing for the leading position. In abso-lute terms, Finland accounted for 4.4 per cent of total OECD telecommunications equipment exports, being in the seventh position in cross-country comparison in 1997.7

3.3

The evolution of

the ICT cluster

3.3.1 Network operation – a fragmented

monopoly market

Despite the prominent role the telecommunications manu-facturing sector has played in the recent industrial struc-tural change in Finland, a glance at the history reveals that it was the advanced network operation – rather than equip-ment manufacturing – that formed the ground for the indus-try to develop.

Since its early days, the Finnish telecommunications mar-ket has had a tendency of early adoption of the latest tech-nology – both in the manufacturing and operator sector. The first indication of this feature was the introduction of the telephone in Finland only a year after its invention in 1876. The first telephone companies were established in 1882, and by the end of the century, all the cities of Finland had a telephone company.

Finland Sweden UK Japan USA 1997 1990 ICT equipment Finland Sweden UK Japan USA 1998 -0.2 0 0.2 0.4 0.6 0.8 -0.2 0 0.2 0.4 0.6 0.8 1997 1990 Telecom equipment

Figure 3.6. Export specialization in 1997 (RSCA index).Source: OECD.

Note:The 1998 data was not yet available for all countries. See Appendix 2 for the definition of the RSCA index.

6 SITC rev3 class 764 (Telecommunications equipment n.e.s & parts n.e.s). 7 Shares of OECD telecommunications exports in 1997 (totalling USD 104 billion):

1. USA 20.5 2. Japan 14.5 3. UK 9.7 4. Sweden 9.5 5. Germany 8.6 6. France 6.1 7. Finland 4.4 8. Korea 4.4 9. Canada 4.2 10. Mexico 4.2

Unlike in most of the European countries, the telephone network ownership was not monopolized by the state. Be-side the national public telecommunications operator (PTO) there was a growing number of private local tele-phone companies that operated in their exclusive conces-sion areas. In the 1930s, their number was no less than 815 (yet it decreased drastically between 1950–65 due to struc-tural regulations). Thus, the market could be characterized as a fragmented monopoly market.

Initially the fragmented market structure was a political outcome. In the turn of the 20th century, when Finland was setting the ground for its telecommunications, it was a Rus-sian Grand Duchy. The Tsar authorized the Finnish Senate to grant licenses in telephony operation. However, there was a threat of seizure of the national telephony by the Tsar, which provoked the Senate to decentralize the net-work ownership to discourage confiscation.

In 1921, the private companies founded the Association of Telephone Companies aiming at administrative coopera-tion and joining forces in face of the PTO, who acted as the regulatory body authorized to redeem poorly performing operators. Indeed, the threat of nationalization worked as an effective means of technical upgrading. Over the years, the Association grew a powerful opponent to the PTO, giv-ing rise to a duopolistic market structure.

There were several intentions throughout the decades to nationalize the private operation, but there was nor enough political coherence neither financial means to realize such endeavours. State redemption of the long distance opera-tion in 1934 was one excepopera-tion to the rule.8

In 1971, the Nordic Telecom Conference, consisting of na-tional Post and Telegraph Administrations, initiated a re-search project on an automatic Nordic mobile telephone (NMT) network, which was going to set the foundation for the consumer-oriented mobile communications. The Con-ference agreed upon the rules on the cross-border roaming, billing and, perhaps most notably, the openness of the tech-nical specifications. Based on their experience, the Confer-ence played an active role in initiating the Groupe Special Mobile (GSM) in 1982, and in designing the pan-European digital mobile network.

The introduction of the NMT in 1981–82 made the Nordic countries the largest mobile market. The number of sub-scribers expanded at an unanticipated rate, exceeding the initial capacity in a short time in all member countries. The mobile market started to attract also private operators, whose license applications were however rejected by the

regulator-PTO that pleaded to the natural monopoly nature of the market.

In fact, the dispute over the PTO’s monopoly rights had its roots in the 1960s. The operative Imperial Telephone De-cree of 1886 could not provide an unambiguous interpreta-tion of the statutory rights to provide novel network ser-vices, such as data transfer, telefax and teletex. As a re-sponse to the intensifying dispute the new Telecommuni-cations Services Act was enacted in 1987, reflecting the start of a new era in the telecommunications regulation. For example, it separated the administrative and opera-tional functions of the PTO, transferring the regulatory au-thority to the Telecommunications Administration Centre, which was established under the Ministry. It also made possible the license of Datatie, a joint venture of private operators and their main corporate clients, in 1988, repre-senting the first major chunk of the public monopolized market allocated to the private sector.

The first amendment to the hundred years old Telephone Decree was followed by a gradual but full liberalization of the telecommunications competition, finalized in 1994. Having been repeatedly denied a license to operate an NMT network, private operators established with their main corporate customers a joint venture, Radiolinja. It was to operate a GSM network that was constructed and leased by local operators. This was made possible by the new Act that authorized full telecom service provision within concession areas. However, in order to provide na-tion-wide services Radiolinja needed a license.

The license application necessitated fundamental changes in the telecommunications regulation provoking a funda-mental political dispute – primarily ideological of nature. In 1991, Radiolinja, as the winner of the regulatory battle, was the first operator in the world to launch commercial GSM services.

The liberalization meant fundamental organizational and regulatory changes for the PTO. In order to be able to re-spond to the competition it was changed into a public cor-poration with no budget obligations to the government. It launched GSM service soon after Radiolinja – thus, among the very first in Europe.

In 1994, the PTO was demerged, and Telecom Finland be-came a limited company with the State as the major share-holder. In 1998, the name of the company was changed to Sonera to pinpoint the change in the strategic focus redi-rected to mobile services and technologies.9

The company

8 There were also occasional acquisitions of operators by the state, motivated by national defence and technical concerns. 9 In 1999, the digital mobile services represented 60 per cent of the turnover.

underwent a quick metamorphosis from a national tele-phony operator to a global pioneer in Internet and mobile applications.10

The Government has reduced its ownership and indicated further privatization in due course.

3.3.2 The emergence of the

telecommunications industry

Unlike in many other countries, in Finland the equipment market has always been open to competition. Up until the 1980s, the market was dominated by leading foreign manu-facturers, like Siemens, Ericsson, and ITT. Attracted by the multi-operator market, they had set up production facilities in Finland. The established, capital-intensive foreign com-panies put a pressure on the emerging domestic industry. To illustrate, in 1970 the turnover of the Siemens Group was EUR 2 billion – almost equaling the total Finnish State budget of EUR 2.5 billion.11

The seeds of the Finnish radiophone industry were planted in three companies, Salora, Suomen Kaapelitehdas, and Valtion Sähköpaja in the 1920s. New radio technology was typically developed in the sideline of main activities by fer-vent engineers, often under suspicion and opposition of conservative colleagues. During a complex organizational evolution process, finalized in 1987, the three companies merged under Nokia’s roof.

Salora (originally Nordell & Korhonen Ltd, established in 1928) was a manufacturer of TV and radio sets, whose brand grew strong beyond national borders. The develop-ment and production of radiophones initiated in 1964 was based on pioneering experiments conducted aside core ac-tivities. Salora’s accumulated experience in serial produc-tion and marketing proved valuable in the later mobile phone business development.

Suomen Kaapelitehdas (lit. Finnish Cable Works, founded in 1917), in turn, was a producer of telecommunications ca-bles. The trade with the Soviet Union, originated during the deliveries of war indemnities, was decisive to the develop-ment of the company’s technical skills. As a demanding but patient customer, the Soviet Ministry of Communica-tions spurred elaboration of modern digital technology. The radio laboratory of the Ministry of Defence (estab-lished in 1925) initiated public development and produc-tion of radio equipment. The wars against the Soviet Union revealed the strategic need for national development of ra-dio technology. After the wars, the activities were industri-alized by founding Valtion Sähköpaja (lit. State Electric

Works), and in 1948, merged with the R&D unit of the PTO. The company was renamed Televa, and in 1976, it became a state-owned limited company serving mostly public establishments for which it was the prime, but not exclusive provider.

In 1963, the Army gave a decisive stimulus to the domestic industry by putting out an invitation for tenders for a radio-phone. This was the first in a series of impulses by which the Government provoked companies to exceed their ca-pacity to meet demanding technology requirements. For the first time the firms were given an economic motive to develop a radiophone, generally regarded as a toy for a marginal group of users. In fact, rather than a business op-portunity, firms regarded the order as a chance to give a physical form to the know-how accumulated in the “back stage” of core operations.

Virtually, the Army did not have the funds to redeem the phone, but for the bidding firms12the prototypes served in developing new portable phones, which soon found their way to export markets.

In 1966, Suomen Kaapelitehdas was merged with Suomen Gummitehdas (lit. Finnish Rubber Works) and Nokia, a 100 year-old wood grinding mill that gave its name to the new corporation. The merger of Suomen Kaapelitehdas with the companies in stable industries secured sustained R&D investments in telecommunications, which was now regarded as one of the strategic business areas of the com-pany.

In the 1970s, it became apparent that the market was too small and resources too scarce for parallel development of digital exchanges in both Televa and Nokia. Consequently, in 1977, the companies combined their R&D and market-ing efforts on digital transfer technology in a joint venture, Telefenno.

Lengthy and laborious R&D in digital technology led fi-nally, in 1982, to the introduction of the first domestic digi-tal exchange – shortly after the leading resource-intensive manufacturers Ericsson, AlcateI, ITT and Siemens. It was the first fully digital exchange installed in the whole Eu-rope, and thus, served in convincing the market of the do-mestic competence vis-à-vis the foreign manufacturers. For years the exchange was the most successful export arti-cle of Nokia.

In 1979, Nokia and Salora, in turn, joined their comple-mentary resources. The fifty-fifty owned Mobira was set up to market and develop radio technology and especially the NMT terminal that was under design in the Nordic

10 For example, in December 2000, Sonera was awarded as the best mobile operator in the World Communication Awards 2000. Sonera was granted the award in recognition of its high-quality service and technological innovations. The company was also regarded as a European forerunner in developing new mobile communications services.

11 Mäkinen (1995).

Telecom Conference. Mobira was the first to launch a ter-minal approved to the NMT network.

The design phase of the NMT standard in the 1970s brought the Nordic telecommunications administrators and companies in close cooperation. While active in terminal development, the Finnish industry was not yet able to con-tribute to network specifications. Fierce pressure from the PTO’s side to engage the industry in cellular exchange de-velopment materialized finally, in 1981, in the base station supplied by Mobira. In the retrospect, it turned out to be crucial in maintaining the company’s position in the emerging market.

The introduction of the NMT in 1981–82 marked the start of a fast-expanding new industry. The specifications were kept open to pursue the objective of the Conference to pro-mote competition in equipment provision. No less than ten manufacturers entered the Nordic market.

Following its vision of global mobile communications, Mobira took substantial risks in investing in large develop-ment projects and pioneering production techniques and in entering markets all over the world.13By 1985, it had

ob-tained a leading position in a number of markets. Between 1982–87, the average annual growth rate of sales was 50 per cent, owing to both general market expansion and to an increased market share.14

In order to intensify foreign market penetration, Mobira al-lied with established local actors.15International coopera-tion taught the company, among other things, the impor-tance of the brand – which was later going to distinguish a Nokia from other mobile phones in the challenging con-sumer market.

Mobira became famous for its “crazy” organizational spirit that referred to the passionate, pioneering and risk-taking style with which is it pursued its ambitious targets.16The same kind of stamina and general enthusiastic – if not fa-natic – attitude towards new radio technology has been seen behind much of the technological progress in the Finnish telecommunications industry.

Virtually in 1986–87, the Finnish telecommunications know-how was organized under one management when Nokia got full ownership of Mobira and the State’s share of Telefenno. 0 10 20 30 40 50 60 70 80 90 100 1967 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 Electronics Cable Forest Rubber

%

Figure 3.7. The structure of Nokia’s sales 1967–1999.

Source: Lemola & Lovio (1996), updated by ETLA.

13 Mobira manufactured equipment for five standards adopted in different countries. Only Motorola supported an equal amount of standards.

14 Koivusalo (1995).

15 Mobira came ashore the US under an OEM agreement with Tandy Corporation, which offered an extensive distribution channel. The alliance with Alcatel and AEG for marketing and system development opened the doors of the French and German PTOs and gave credibility to the emerging mobile manufacturer. Cooperation was gradually terminated after the company was capable of independent supply of a GSM system in 1991.

In the search of rapid growth and global market presence, Nokia ran into serious production and financial difficulties that almost destroyed the company. Towards the end of the decade, it started loosing positions in the export markets. The downturn was aggravated by the severe external chocks, the collapse of the Russian bilateral trade and the abrupt economic recession, which put the future of Nokia at stake.

The crisis gave a stimulus to a drastic dismantling of busi-ness sectors – varying from tissue paper and rubber boots to cable machines and consumer electronics – preserving exclusively the telecommunications activities. The struc-tural changes were coupled with an important redesign of the company governance.

At the same time, however, the world witnessed a wave of telecommunications liberalization. The boost in global de-mand for digital mobile equipment with Nokia’s global po-sition built in the 1980s saved the company from a dive that would probably have destroyed the company.

Owing to the recession hitting hard on consumer demand, it was crucial to dismantle the luxurious image of the porta-ble phone. With the softer aesthetic design and the user-friendlier customer interface Nokia was the first manufac-turer to invent the key to the consumer markets. Since the first consumer-targeted model in 1994, Nokia has high-lighted the life-style feature of communications in brand building – a strategy that explains an important share of its breakthrough in the consumer market. In 2000, Nokia was the fifth most valuable global brand.17

In 1999, Nokia accounted for about a third of the world mo-bile phone market, and the phones represented almost 70 per cent of the turnover. In network systems, the company holds a market stake of close to 20 per cent.

3.4

The factors of the competitive

advantage

In order to provide an analysis of the competitive advan-tage of the ICT cluster as suggested in chapter 3.1.1, the factors involved will be briefly described below.

3.4.1 Firm strategy, structure and rivalry

Nokia dominates the ICT cluster by size and effect. The company accounted for almost 50 per cent of the cluster sales and 66 per cent of the cluster exports in 1998. How-ever, there is a number of other ICT companies that havealso established their positions in international markets. Moreover, many companies with their roots deep in the Finnish cluster have attracted foreign acquisitions (e.g. LK-Products, Martis, NK Cables, Solitra).

In the wake of the ICT boom there has been an intensive emergence of start-ups finding narrow but lucrative niches in the wireless and Internet applications sectors. Important conquests have been made notably in the data security do-main. At the other end of the spectrum, there are estab-lished companies with accumulated world-class compe-tence particularly in network technology.

Despite the global business environment the core activities of companies, namely the headquarters and R&D, are still predominantly located in Finland.18Established tradition in cooperation in the local innovation system and advanced R&D activities anchor companies to their home base. The fertile environment has attracted a number of leading for-eign companies to base their R&D centres in Finland, too (e.g. ICL, IBM, Siemens, Hewlett Packard, Ericsson).

Today, domestic competition has little effect on firm strat-egy. Competitors, regardless of their origins, operate glob-ally determining the scope and perspective of company strategies. Unlike in a host of monopolized markets, the Finnish equipment industry has evolved under competitive pressure from the outset.

In network operation, the fragmented, yet monopolistic market structure has had implications on the market, non-existent in monopoly markets. For example, the pre-conditions for duopolistic competition were in place at the opening of the market, spurring price efficiency and ser-vice improvements that made the Finnish telecommunica-tions very competitive in international comparison.

The liberalization has affected the strategic relationships within the private sector, as well. In the Finnet Group (the newly named Association of Telephone Companies), there have emerged regional alliances to form competing camps, while there are still joint ventures in nation-wide service provision.

3.4.2 Factor conditions

Liberalization of the capital market in Finland at around the turn of the 1990s has revolutionized the institutional envi-ronment of corporate funding. Established structures of power concentrations and cross-ownership were disman-tled, providing firms an access to abundant international resources at market price.

17 Interbrand.

Between 1994–1999, the value of private capital invest-ments grew tenfold, to EUR 286 million.19Perhaps most notably, the weight in risk ownership has been shifting from the public to the private sector. The role of the state is been refocused on carrying the technology risk, while ven-ture capitalists have come to bear the commercial risk of a new company.

Unequalled opportunities for innovative start-ups have opened up in the form of “intelligent” venture capital, which has actually become their most common source of capital. The share of the ICT sector was 30 per cent of the total private capital investments in 1999.20

The level of R&D investments on ICT has been in inten-sive growth. In OECD comparison, the share of private ICT-related R&D of total manufacturing R&D was the highest in Finland in 1998. During the period 1991–97, Finland turned from a below-average investor into the world leader. In the public sector there was an outspoken objective in 1996 to increase systematically the share of R&D expenditure of the GDP. Today it amounts to over 3 per cent being the second highest share in the world after Sweden.

Thus, the critical factor in the development of the cluster is not scarcity in capital but rather in human resources that is virtually impeding full-scale exploitation of the available funds. There is a structural mismatch in available skills not only on the macro level, but also within the cluster, notably in the software industry owing to the fast pace of techno-logical development. Owing to the lengthy lead-time in ed-ucation, the increased intake in the education system has not yet alleviated the shortage of skills. Worse yet, the lack of employees draws both students and personnel from higher education institutions to the industry, eroding se-verely future resources.

3.4.3 Demand conditions

Since 1996, Finland has been the world leader in mobile penetration. All in all, households have adopted mobile phones as consumer products: in 1999, they held more wireless terminals (78.5%) than wired (75.8%). 60 per cent of households have both terminals, while no less than 20 per cent rely solely on mobile communications.21Also in Internet host penetration rate Finland ranked the second af-ter the US, by 121 per thousand inhabitants in 1999.22

Since the full liberalization in 1994, the telecommunica-tions price level has declined by about 25 per cent in real terms. The sharpest reductions have been witnessed in dig-ital mobile and data services making Finland the leader in low-cost telecommunications services in the OECD in 1998.23Reasonable pricing together with the cheaper and consumer-oriented handportables, introduced in the early 1990s, boosted swift expansion of the market. Digital value-added services were soon adopted by consumers and have established their role in every-day communications. The national attraction towards technology together with the high level of basic education has been seen behind much of the communications boom in Finland. All the same, the small home market has served as a test laboratory for the development of new products and services – despite the fact that its importance to Finnish firms is decreasing in monetary terms.

3.4.4 Supporting and related industries

In the recent years, the domestic supporting sector has evolved very specialized for the needs of the original equipment manufacturers (OEM). Customers’ growing re-quirements in production volume and product sophistica-tion have generated a number of new companies, and in-duced redirection of activities in the existing ones. The strength of the domestic supporting sector is in highly customized inputs. Special competence resides in the pro-duction of ASIC, rf-filters, hybrid circuits, silicon wafers, printed circuit boards and their surface mounting technol-ogy, as well as in electronic manufacturing services, auto-mation, and precision mouldings. Standard components, in turn, requiring large scale and effective global distribution channels, are practically fully imported.24In the wake of Nokia, many of the suppliers have learned fast the requirements of global operation and grasped the opportunity of rapid growth.25Domestic partnerships have been stretched to foreign markets to benefit from estab-lished operative processes and trust-based relations. Global extensions of domestic partnerships have involved suppli-ers’ green-field investments as well as acquisitions of the customer’s foreign production facilities.

The versatile and world-class supporting sector has greatly enhanced manufacturers’ possibilities to contract out non-core activities. This has been imperative in the sector in which time-based competition and risks involved in

con-19 Holtron Ltd.

20 Ibid.

21 Ministry of Transport and Communications.

22 EITO 2000.

23 OECD (1999).

24 92% of the electronic component market value is composed of imports (Hienonen, 2000). 25 Eight suppliers, with Nokia as a prime customer, had gone public by the end of 2000.

tinuous technology race call for disintegration of the pro-duction process.

There is a trend towards growing responsibility of suppli-ers in independent product development by which manu-facturers seek to take advantage of specialized external knowledge. Suppliers are being increasingly engaged in early-phase product and production process design to pro-duce more effective and innovative solutions. Indeed, the scope of outsourcing has widened from mere standard outsourcing to R&D activities.

The relative size of Finnish suppliers in global perspective is small. Global operations of customers, most particularly Nokia, put tremendous pressure on suppliers’ capabilities and resources. Any firm aspiring to be connected to the net-work will have to be able to grow in pace with the cus-tomer, which has direct bearing on the firm’s risk leverage and management skills required.

As a general rule, the presence of a competitive industry contributes to the development of related industries.26As a provider of infrastructure technology, the ICT cluster has linkages to a number of industries providing service prod-ucts, or content, complementing basic network services.27 The digital content industry is still in its early phase in Fin-land, yet there are numerous signs of emerging activities. The notion of digital content embraces a whole array of ser-vice concepts, from transaction and information serser-vices to education and entertainment. Yet the borders of the ‘con-tent industry’ are difficult to draw, they can be regarded to include the ‘digitized products’ of a number of traditional sectors (see figure 3.2). Non-fixed definitions severely complicate quantitative valuation of the industry.

In 1999, there was a group of some fifty firms in the games and entertainment software production that generated EUR 10-12 million. Despite advanced technological skills, this group still operates in the fringe of the software sector, lacking sectoral concentration and volume. In addition, the sub-sector tends to have difficulty in attracting profes-sional business skills as it suffers from low credibility as compared with more “serious” software sectors.28 How-ever, technology leadership and new business models en-abled by the Internet (digital mass distribution) provide great opportunities for the Finnish digital entertainment in-dustry.

All in all, it is clear that the most value-adding applications of the Internet and mobile services are still to come. Al-though entertainment will draw the largest demand

vol-umes, applications in, say, education and health care will be likely among those enhancing the efficiency and well-fare of the economy.

3.4.5 Government

The appropriate role of the government with regard to clus-ters is to create a context that encourages upgrading, and establishes a stable economic and political environment.29 Even though all government actions matter for the national competitiveness, competition, technology and education are the domains with most direct effects on the ICT cluster competitiveness.

Competition policy. The competitive conditions in the Finnish telecommunications market – both in manufactur-ing and operation – have differed somewhat from the inter-national tradition. Not only have both the markets been fragmented in ownership, but also there has not been an ex-clusive symbiosis between the PTO and a national cham-pion in equipment provisioning.

Through the Association of Telephone Companies the pri-vate sector grew a counterweight to the national monopoly, non-existent in most markets prior to the worldwide wave of liberalization in the 1990s. Deregulation and the market opening were initiated among the first countries, soon after the UK and the US in the early 1980s. Thereafter, the regula-tory approach has based on pro-competitive, light-handed regulation and technology neutrality. The market is subject to general competition and consumer protection legisla-tion.

The approach is still less interventionist than in many other OECD countries; some mandatory EU requirements have been regarded as regressive to the liberal market function-ing of the Finnish market.30Following the fortifying trend in national telecommunications policies, the Finnish gov-ernment is also looking for an opportunity to withdraw from telecommunications activities.

Technology policy. The purposeful orientation in technol-ogy policy has a twenty-year history, materializing in e.g. continuous growth in the R&D share of the GDP. Between 1985 and 1999, the share doubled reaching EUR 3.75 bil-lion at the end of the period, of which 30 per cent was pub-lic investments. By the 3.1 per cent GDP share Finland po-sitioned the second in the world in R&D intensity after Sweden.

26 Porter (1990).

27 A distinction is made between the industries exploiting the network in digital distribution of service products, and those rationalising their business procedures (electronic business) with the ICT. ‘Related industries’ refer here to the former case. 28 Autere, Lamberg & Tarjanne (1999).

29 Porter (1998) as in Rouvinen & Ylä-Anttila (1999). 30 Ministry of Transport and Communications (2000).

In the 1990s, amidst the general cutback objectives in public expenditure, the government decided, in 1996, to system-atize the increase in public R&D funding to sustain the posi-tive development of the electronics sector discernible by the time. Part of the proceeds from privatization was earmarked for public funding of technology development. The objec-tive for the period 2001–2004 is to connect the increase in public funding to the general growth rate of the economy. Digitized content and enabling software applications, as key factors in the ICT cluster’s future success, have been appointed high status on the national agenda. Concur-rently, there has been a need to redirect the focus in public funding. From traditional technology-oriented product and process development there has been an extension in focus, towards service products and market-orientation to facili-tate the emergence of export-oriented service products. The shift in policy direction has been manifested in a series of digital media technology programs since the mid-1990s.

In addition, there has been a need to re-evaluate the role of the public sector in risk funding altogether. The emergence of abundant private venture capital enables a more focused public strategy in technology risk funding, and a clearer role differentiation with the private sector financiers. In ad-dition, through technology programs, the public sector has been active in practicing the role of a facilitator between firms and venture capitalists.

Education policy. The threat of exhausted labor resources has been attacked by increasing openings in higher educa-tion institueduca-tions. Between 1993–98, the total intake in uni-versities grew nearly twofold and in polytechnics nearly threefold. However, established institutional structures as well as resources lagging behind increased utilization of educational capacity seem to frustrate efficient achieve-ment of policy objectives.

The dialogue between the industry and the government on educational issues has been active since the upsurge of the industry. In the early 1998, the government adopted a pro-gram for increasing education in the information industry fields between 1998–2002. The industry has committed it-self to its implementation by providing internships, but avoiding recruitment of under-graduates, and encouraging graduation of employed students. Moreover, companies aim at increased participation in training and education, and do-nation of equipment for education and research purposes.

3.4.6 Coincidental factors

The turn of the 1990s entailed several external incidents with momentous implications on the Finnish ICT cluster, without which, it is fair to say, the average 30 per cent

an-nual growth rate of the electronics industry would not have materialized.

Following the agreements within the EU and the WTO, the traditionally monopolized telecommunications equipment and service markets were gradually liberalized, starting with terminal equipment in 1988 in Europe. The opening of the East European market gave an additional boost to mo-bile equipment demand.

The effects of liberalization were momentous. Between 1990–98, the value of OECD exports of telecommunica-tions equipment grew almost 2.5-fold, reaching USD 110 billion at the end of the period.31Correspondingly, 96 per cent of the OECD market, as measured by telecommunica-tions revenue, was open to competition by the beginning of 1999.32

In contrast, the collapse of the Soviet Union together with the severe recession in Finland hit hard on the ICT cluster demand in the early 1990s. Without the counterbalancing effects of market liberalization, the Finnish economy would have taken a somewhat different and slower path in its revival process.

3.5

Dynamics in the ICT cluster

The ICT cluster has been evolving for a hundred years. The cluster as we see it today looks like a product of a master plan: a vigorous industrial innovation system with high na-tional competitive advantage. However, it is an outcome of a dynamic self-reinforcing process in which coincidental factors do not play the least consequential role.

In order to get a grasp on the factors behind the ICT cluster development, the most influential dynamic linkages be-tween the factors of competitive advantage will be ana-lyzed within the framework suggested in chapter 3.1.1. It is obvious that the causes and the effects of interactive factors become blurred and ambiguous, but the framework helps in providing some systematic in the analysis.

3.5.1 The government as an early catalyst

of cluster development

The earliest and perhaps most influential factors on cluster development relate to those government policies that have promoted competitive market structure.

The foundation of the developed telephony infrastructure was laid already in the 19th century, under the Tsar’s reign.

31 OECD (1999) and OECD trade statistics.