ABSTRACT

This study is conducted to better understand budgeting practice in Singapore which may be critical for increasing competitiveness and productivity for firms, and increasing value-add contribution for accountants. We obtained 356 valid responses from an online survey administered to members of a professional accounting organization. We found that most firms prepare budget and many (about 30%) incorporate significant strategy assumptions in budgets. The time spend on budgeting (10%-20%) is lower than what was reported in US studies, and more time is spent in preparing than using the budget. Budgeting problems (e.g. ratcheting and sandbagging behaviour) are well recognized, but firms preparing budgets with business plans generally deem pros for budgeting exceeding cons. Firms with annual revenue below $1m prepare budget primarily for forecasting cash flows; larger firms focus more on guiding and coordinating business activities, with increasing importance on variance analysis as firm size increases. For firms that prepare budgets with business plans, employee compensation based on budget performance is not as prevalent as expected. About 70% of the firms set budget targets to monitor strategy execution, about 50% set budget target for employee performance evaluation, and about 43% compensate by budget performance. The implications of these findings are discussed.

Keywords: budgeting process; budget gaming; strategic control; performance measure; time cost of budgeting; use of budget

BUDGETING PRACTICE

IN SINGAPORE – AN EXPLORATORY

STUDY USING A SURVEY

Tan Boon Seng1

Low Kin Yew2

1Institute of Singapore Chartered Accountants, Singapore 2nanyang Business School,

nanyang Technological University, Singapore

ARTICLE InFO Article History:

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

INTRODUCTION

Budgeting is a ubiquitous activity in business that accountants participate – supporting business unit heads in its preparation, assisting controllers and executives in its review, and even preparing and developing the operating budget itself. Businesses generally prepare two types of budgets – the capital budget and the operating budget. But for our purpose, budgeting refers to the preparation of recurring operating budgets. Capital budgeting, also known as investment appraisal, is non-recurring and uses a different set of tools.

There are two related objectives for businesses to prepare operating budgets. First, budgeting is an integral part of a business strategy where the budget assists managers to allocate resources, monitor progress, and provide feedback on how well the strategy is working (i.e., for strategic control and coordination). Second, budgets are used as performance targets to motivate behaviours supporting the strategy (i.e., for performance measurement). These objectives are related but distinct, and have different implications for the practice and research on budgeting.

A literature review on the practice of budgeting by neely, Sutcliff and Heyns (2001) suggests that traditional budgeting is broken: Budgeting is found to take up a substantial amount of management time in preparation, revision, negotiation, and review. Yet, managers complain that budgets are negotiated outcomes that are rarely strategically focused. They appear to be based on implicit but invalid assumptions, reinforce departmental barriers rather than encourage collaboration, and misallocate resources based on positional power rather than strategic needs. Budgeting is perceived by managers to focus on cost reduction, ignore value creation and encourage gaming. Budgeting is found to be simply too inflexible: Planning assumptions are often outdated when budgets are finally completed. However, budgets are seldom revised in response to competitive changes and hence, constrain effective strategic responses.

79

process; Beyond Budget (Hope & Fraser 2003) abandons the traditional budgeting process and replaces it with concepts such as rolling forecast, relative performance measure and decentralization of decision control.

Anecdotally, there are wide variations in the effectiveness and practice of budgeting approaches. These variations indicate opportunities for adoption of best practices that enable accountants to value-add to their firms. Paradoxically, using the budget for performance measurement intensifies budget gaming which will ultimately reduce the effectiveness of budgeting for strategic coordination and control (Jensen, 2003). How firms handle the trade-off have a strong impact on their competitiveness. However, current budgeting practice in Singapore, which may well be the key to help firms unlock greater competitiveness and productivity, is largely unknown. This exploratory study analyses four aspects of budgeting practice: (a) how are budget prepared and used, (b) time spend, (c) usefulness of budgeting in general and for strategic planning and performance measure, and (d) challenges.

DATA: COLLECTION AND PROFILE

We administered an online survey to members of the Institute of Singapore Chartered Accountants from July to August 2015. We obtained 356 responses after eliminating three duplicate responses.

We collected information of the respondent’s profile that may enables meaningful subgroup levels analysis. The information includes firm size (by revenue class), firm types (ownership and participation in equity market), firm structure (diversification and primary activity) and the respondents’ roles in budgeting.

80

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

Respondent Profile

The mix of firms by size (measured by category of annual revenue) is diverse. About a quarter (26.4%) are very large firm with over $1b annual sales, another quarter (25.0%) are large firms with annual sales of $100m – $1b, and the remaining half (48.6%) are Small and Medium Enterprise (SME)1 with annual sales below $100m. The pie chart below summarizes the size distribution with detailed breakdown of the SME:

The res

p

more th

a

be a mul

t

Multinat Governm Local Non-pro SGX Lis Listed O

The bu

d

diversifi

c

goods.).

possible

– genera

l

function

a

2 This classi

pondents wo

a

n 100% (n=

tinational en

Own tional ment Linked ofit sted Overseasd

geting pr

o

cation and

b

Generally,

d

– but rare –

l

ly with mor

a

l departme

n

ification follows

Figure 1: D

o

rk in a wi

d

=356) b

eca

u

n

terprise an

d

Tab

nership and

o

cess may

by the natur

e

d

iversified f

i

case of co

m

re than 70%

n

ts. The distr

s from the strateg

$1m to $ Firm

Distribution

d

e variety o

f

use afirm

can

d

listed in Si

n

ble 1: Respo

Equity Listin

be influen

e

of the pro

d

i

rms are org

mbining bot

h

of the reve

n

ribution of t

h

gic management

$10m to $100m, 19 $10m, 16.0%

Below $1m, 1 m Size (Ann

of Firm Siz

f

firms. The

n

have mult

i

n

gapore). T

h

ondents by

ng

ced by fir

d

uct (wheth

e

anized as pr

h

in a matrix

n

ue arising fr

h

e responde

n

t literature, speci

A $100m o 9.7% 12.9% nual Reven

ze of Respo

tabulated

p

i

ple attribut

e

h

e distributi

o

y Firm Type

rm structur

e

e

r the firm

p

roduct or ge

o

structure. F

rom a single

n

ts’ organis

a

ifically Rumelt ( m to $1b, 25.0%

ue) N= 356

ondents

p

ercentages

e

s (e.g.,an or

o

n is tabulat

e

N 149 31 130 18 48 26

e

arising

f

p

rovides ser

v

o

graphical

d

irms with l

o

business

2–

a

tions (n=3

5

(1974). %

below add u

r

ganisation

m

ed as follow

% 41.9% 8.7% 36.5% 5.1% 13.5% 7.3%

f

rom the

f

v

ices or pro

d

divisions wit

o

w diversifi

c

are organiz

e

5

6) is as fol

l

4

u

p to

m

ight

s:

f

irm’s

d

uces

th the

cation

e

d by

l

ows:

Figure 1: Distribution of Firm Size of RespondentsThe respondents work in a wide variety of firms. The tabulated percentages below add up to more than 100% (n=356) because a firm can have multiple attributes (e.g., an organisation might be a multinational enterprise and listed in Singapore). The distribution is tabulated as follows:

1 SPRInG defines SME in Singapore based on annual sales (below $100m) or employee number (below 200). The definition is used to access eligibility for SME grants. See http://goo.gl/xzAzQn.

81

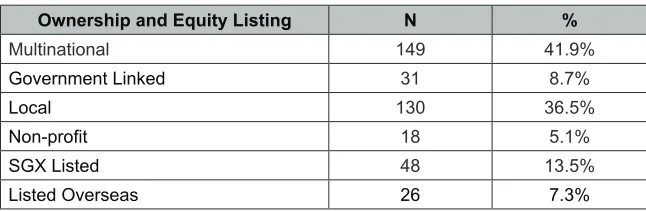

Table 1: Respondents by Firm Type

Ownership and Equity Listing N %

Multinational 149 41.9%

Government Linked 31 8.7%

Local 130 36.5%

Non-profit 18 5.1%

SGX Listed 48 13.5%

Listed Overseas 26 7.3%

The budgeting process may be influenced by firm structure arising from the firm’s diversification and by the nature of the product (whether the firm provides services or produces goods.). Generally, diversified firms are organized as product or geographical divisions with the possible – but rare – case of combining both in a matrix structure. Firms with low diversification – generally with more than 70% of the revenue arising from a single business2 – are organized by functional departments. The distribution of the respondents’ organisations (n=356) is as follows:

Table 2: Respondents by Firm Structure

Firm Structure N %

Diversified Product Divisions 104 29.2%

Diversified Geographic Divisions 56 15.7%

Primarily Manufacturing 41 11.5%

Primarily Service 155 43.5%

HOW ARE BUDGET PREPARED?

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

(63.7% vs. 29.5%). This is consistent with the view that the preparation cost for incremental budgets is lower than zero based budgets. Overall, more budgets are prepared based on a business plan than without (52.5% vs. 40.7%). The summarized data are as follows:

Diversifi Diversifi Primarily Primarily

HOW AR

The maj

o

work do

budgets

t

budget b

adjustin

g

plan as th

zero-b

ase

cost for

prepared

follows:

ed Product D ed Geograph y Manufacturi y Service

RE BUDGE

o

rity offirm

s

not prepar

e

t

hrough ne

g

b

ase on thei

g

from last

y

h

e basis of

p

e

d budgetin

g

incrementa

l

based on a

Fig Table Firm Stru Divisions hic Divisions ing

ET PREPA

s

prepare o

p

e

budgets.

A

gotiation and

i

r business

y

ear’s budg

e

p

reparation.

g

(63.7% v

s

l

budgets i

s

business p

l

gure 2: Dist H

e 2: Respon

ucture

RED?

p

erating bu

d

A

bout40.7%

d

without bu

plans, cons

e

tsand 29.5%

There is a

s

. 29.5%).

T

s

lower th

a

lan than with

ribution of Incremental Last Year Busines Plan, 23.0 Zero Based Business Plan, 29.5% How is the

dents by Fi

dgets - only

% of firmspr

u

siness plans

isting of 23

% preparin

g

clear prefer

e

This is consi

a

n zero bas

e

h

out(52.5%

the Basis o Increm Last Negotia l from r by ss 0% by s % Budget Pre N=356 irm Structu

6.7% of th

e

repares bud

g

s

. About 52.

3

.0% prepar

g

zero base

d

e

nce towar

d

istent with t

e

d budgets.

vs. 40.7%).

of Budget P mental from Year by ation, 40.7% epared? re N 104 56 41 155

e

firmswher

e

g

ets by adju

.5% of the

f

ring increm

e

d

budgets u

s

d

sincrement

a

the view tha

Overall, m

. The summ

reparation Does no Budg % 29.2% 15.7% 11.5% 43.5%

e

the respo

n

u

sting last y

f

irms prepar

e

ntal budge

t

s

ing the bu

s

a

l budgeting

a

t the prepar

more budget

marized data

a

ot Prepare get, 6.7%

5

ndents

y

ear’s

r

e the

t

s by

siness

over

r

ation

s are

a

re as

Figure 2: Distribution of the Basis of Budget Preparation

We examine if subgroup characteristics change the way budgets are prepared. The results are summarized in the following tables:

Table 3: Preparation of Budget – Analysed by Size

Size (Annual Revenue) Above $1b $100m to $1b $10m to $100m $1m to $10m Below $1m

Does not Prepare Budget 2 (2%) 4 (5%) 2 (3%) 4 (7%) 12 (26%) Incremental from Last Year by

Negotiation 41 (44%) 33 (38%) 26 (37%) 27 (47%) 17 (37%)

Incremental from Last Year by

Business Plan 24 (26%) 24 (28%) 17 (24%) 11 (19%) 6 (13%)

Zero Based by Business Plan 27 (29%) 26 (30%) 25 (36%) 15 (26%) 11 (24%) 94

83

While only 6.7% of all firms do not prepare operating budget, this group is heavily weighted towards small firms with annual revenue below $1m (26% vs. 2% to 7% in the other groups). For firms not preparing any budget, the differences between small firms and every other group are statistically significant3.

For firms that prepare budgets, there is no clear indication that size is the cause for any difference in budgeting approach. As such, the sub-group analysis does not provide new insight as compared to aggregate analysis for firms that prepare budgets.

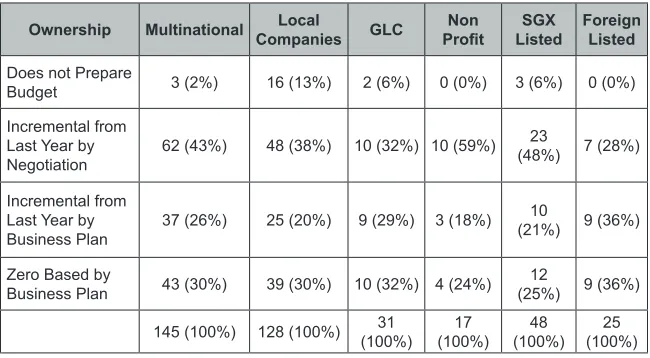

Table 4: Preparation of Budget – Analysed by Ownership

Ownership Multinational CompaniesLocal GLC ProfitNon ListedSGX Foreign Listed

Does not Prepare

Budget 3 (2%) 16 (13%) 2 (6%) 0 (0%) 3 (6%) 0 (0%)

Incremental from Last Year by

Negotiation 62 (43%) 48 (38%) 10 (32%) 10 (59%) 23

(48%) 7 (28%)

Incremental from Last Year by

Business Plan 37 (26%) 25 (20%) 9 (29%) 3 (18%) 10

(21%) 9 (36%)

Zero Based by

Business Plan 43 (30%) 39 (30%) 10 (32%) 4 (24%) (25%)12 9 (36%)

145 (100%) 128 (100%) (100%)31 (100%)17 (100%)48 (100%)25

Comparing multinationals with local companies, local companies are more likely not to prepare a budget (13% vs. 2%; statistically significant). Multinationals are more likely to use incremental budget and equally likely to use the zero-based budget as compared to local companies. As seen from the comparisons of GLC with multinational and local companies which are privately held, the introduction of government shareholding appears to increase the use of business plan in budgeting. The non-profit status of the firm has an opposite effect whereby there is a decreased use of business plan in budgeting, and an increased practice of incremental budgeting by negotiation. Interestingly, when a company is listed in Singapore instead 3 We will use the 5% level throughout this report; see http://www.jerrydallal.com/LHSP/p05.htm

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

of overseas, it appears to increase the probability of using incremental budgeting and reduce the link of the business plan with the budget.

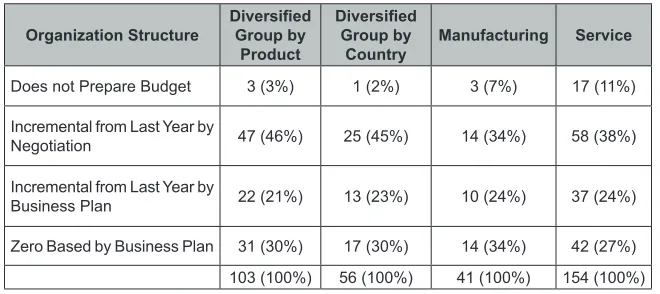

Table 5: Preparation of Budget – Analysed by Firm Structure

Organization Structure Diversified Group by Product

Diversified Group by

Country Manufacturing Service

Does not Prepare Budget 3 (3%) 1 (2%) 3 (7%) 17 (11%)

Incremental from Last Year by

Negotiation 47 (46%) 25 (45%) 14 (34%) 58 (38%)

Incremental from Last Year by

Business Plan 22 (21%) 13 (23%) 10 (24%) 37 (24%)

Zero Based by Business Plan 31 (30%) 17 (30%) 14 (34%) 42 (27%) 103 (100%) 56 (100%) 41 (100%) 154 (100%)

Table 5 shows that diversification affects budgeting in aggregate. The diversification effects are not seen at the detailed level of product or geographical diversification. It also does not extend to the detailed level of whether und iversified firms supply products or services. Diversified firms are less likely not to prepare a budget (2%-3% vs. 7%-11%) and are more likely to use incremental budget by negotiation (45%-46% vs. 34%-38%). There is little difference in the use of business plan for budgeting between the groups.

85

For firms that prepared budget, we examined how the first draft is established by the following three choices:

1. Top-Down Target Setting: Top management sets certain targets and allocates these targets to individual business units to develop their draft budgets

2. Top-Down Budget Setting: Top management prepares the draft budgets and conveys them to the individual business units for their inputs

3. Bottom-Up Approach: Individual business units prepare the draft budgets that are aggregated up the hierarchy

The budget numbers are anchored by the first draft, hence the one who prepares the first draft influences whether the final budget is closer to the ambition of the management or feasibility of the business unit. This outcome is explained by the concept of framing and anchoring in negotiation theory (Bazerman & neale, 1993). For our sample, some firms do not prepare budget (n=24) and others skip this question by choice (n=12), resulting in 320 usable responses. The breakdown of the budgeting approach is as follows:

•

T

th

•

B

ag

The

bud

g

influenc

e

the busi

n

negotiati

(n=24)

a

breakdo

w

The fig

u

approac

h

15.0%) i

than sett

summariz

Top-Down B

h

em to the i

n

Bottom-Up

g

gregated u

p

g

et number

s

e

s whether t

h

n

ess unit.

T

on theory (

B

a

nd others sk

w

n of the bu

d

ure above s

h

h

(57.8% vs

n the top-do

t

ing targets.

z

ed in the fo

Budget Sett

n

dividual bu

Approach:

p

the hierar

c

s

are anchor

h

e final bu

d

T

his outcom

B

azerman &

kip this qu

e

dgeting app

r

Figure 3

hows that th

. 42.2%).

T

o

wn approa

c

We exami

n

o

llowing tab

l

A

A

ting:

Top

m

siness units

Individual

chy

red by the f

i

dget is close

r

me is expla

i

neale, 199

3

e

stion by ch

o

r

oach is as fo

3: Distributi

he top-down

T

arget settin

g

c

h. This resu

n

e if subgr

o

l

es (n=320)

Bu Bottom Up Approach, 42.2%

Approach to

management

for their in

p

business u

n

i

rst draft, h

e

r to the amb

i

i

ned by the

3

). For our s

a

o

ice (n=12)

fo

llows:

on of Budg

n

approach

g

is more

c

ult is expec

t

o

up charact

e

:

Top Dow Setting Top Down udget Setting, 15.0% % o Budgetingprepares th

e

p

uts

n

its prepar

e

ence the one

ition of the

m

concept of

a

mple, som

e

), resulting i

eting Appro

is more pr

c

ommon th

a

ted as setting

e

ristics has

wn Target g, 42.8%

g, N=320

e

draft bud

g

e

the draft

e

who prepar

manageme

n

f

framing

a

e

firms do n

o

n 320 usab

l

oach

r

evalent than

a

n budget s

e

g

budgetsre

q

any impact.

gets and con

budgets th

a

res the first

n

t or feasibil

i

a

nd anchori

n

o

t prepare bu

l

e responses

n

the bottom

e

tting (42.8%

q

uire more

e

. The resul

t

8

nveys

a

t are

draft

ity of

ng in

u

dget

. The

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

The figure above shows that the top-down approach is more prevalent than the bottom up approach (57.8% vs. 42.2%). Target setting is more common than budget setting (42.8% vs. 15.0%) in the top-down approach. This result is expected as setting budgets require more effort than setting targets. We examine if subgroup characteristics has any impact. The results are summarized in the following tables (n=320):

Table 6: Distribution of Budgeting Approach by Firm Size

Size (Annual Revenue) Above $1b $100m to $1b $10m to $100m $1m to $10m Below $1m Top Down Target Setting 36 (43%) 39 (48%) 26 (38%) 18 (35%) 17 (52%) Top Down Budget Setting 7 (8%) 8 (10%) 13 (19%) 10 (19%) 9 (27%) Bottom Up Approach 41 (49%) 34 (42%) 29 (43%) 24 (46%) 7 (21%) 84 (100%) 81 (100%) 68 (100%) 52 (100%) 33 (100%)

Budgeting in companies below $1m annual turnover is distinct from larger companies. About 79% of companies below $1m annual turnover adopt the top-down approach compared to around 50% in larger companies. The results are consistent with the view that management in small companies is more involved in the budgeting process because it is feasible to do so. This hypothesis is supported by the observation that top-down budget setting is observed to decrease with company size in the sample.

Table 7: Distribution of Budgeting Approach by Ownership

Ownership Multinational Companies GLCLocal ProfitNon ListedSGX Foreign Listed Top Down Target

Setting 59 (42%) 55 (50%) 7 (25%) 5 (31%) 14 (33%) 12 (50%) Top Down Budget

Setting 22 (16%) 17 (15%) 2 (7%) 4 (25%) 4 (9%) 3 (13%)

Bottom Up Approach 59 (42%) 39 (35%) (68%) 7 (44%) 25 (58%) 9 (38%)19

140 (100%) 111 (100%) (100%)28 (100%)16 (100%)43 (100%)24

87

Table 8: Distribution of Budgeting Approach by Firm Structure

Organization Structure

Diversified Group by

Product

Diversified Group by

Country Manufacturing Service

Top Down Target

Setting 41 (43%) 25 (45%) 17 (47%) 53 (40%) Top Down Budget

Setting 15 (16%) 7 (13%) 5 (14%) 20 (15%) Bottom Up Approach 40 (42%) 23 (42%) 14 (39%) 58 (44%) 96 (100%) 55 (100%) 36 (100%) 131 (100%)

The results in Table 8 show that the choice of budgeting approach is not affected by whether a firm is diversified or not. Furthermore, the choice of budgeting approach in undiversified firm is not affected by whether the firm is primarily in manufacturing or service industry.

TIME COST OF BUDGETING

There is no doubt that budgeting is time-consuming. Budgeting is reported to take 20%-30% of managers’ time in Hope and Fraser (2003) and 21%-40% in Umapathy (1987). These results are generally accepted as representative of US companies and appear to indicate a trend of reduced time cost over the years. Our survey shows a lower time cost for budgeting where the median lies in the 10%-20% range compared to the US studies. The detailed results are tabulated below.

Table 9: Distribution of Time Spend on Budgeting

N %

None at all 39 12%

Up to 10% 81 24%

10% to below 20% 67 20%

20% to below 30% 59 18%

30% to below 40% 45 14%

40% to below 50% 16 5%

More than 50% 24 7%

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

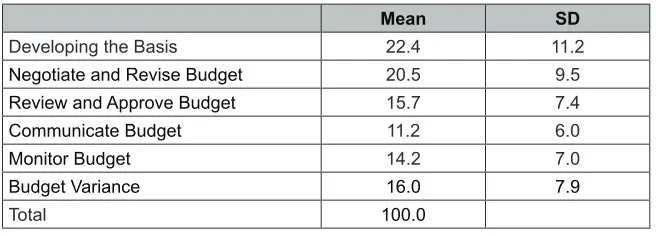

We requested the respondents who prepare the budget with a business plan to allocate their time spent on budgeting activities over a total of 100 points. The results are as follows:

Table 10: Distribution of Mean Time Allocation on Budgeting Activities

Mean SD

Developing the Basis 22.4 11.2

Negotiate and Revise Budget 20.5 9.5

Review and Approve Budget 15.7 7.4

Communicate Budget 11.2 6.0

Monitor Budget 14.2 7.0

Budget Variance 16.0 7.9

Total 100.0

The table illustrates the ratio of time spent in preparing a budget (developing the basis, negotiating and revising, reviewing and approving, communicating the budget) to time spent in using the budget (monitoring budget and analysing variance) is approximately 7:3.

89

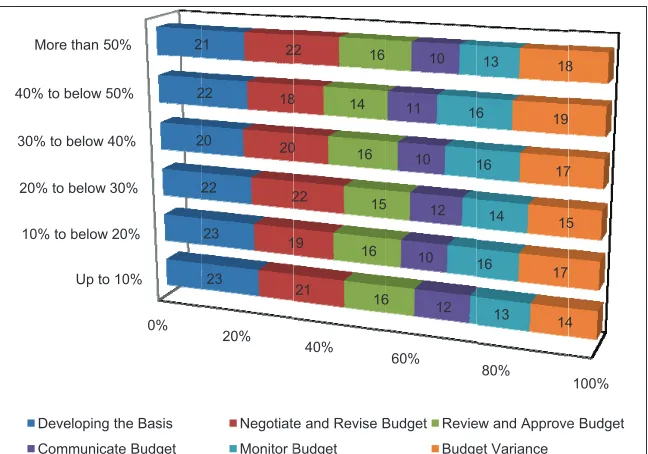

Budgeting Practice in Singapore negotiatin

using the

We inves figure (th

Fig

The resu developin more tim sophistic

USE OF

We surv (n=187) of firms 3 4

ng and revis e budget (mo

stigated if th he vertical ax

gure 4: Anal

ults show th ng the basis me foranalysi cated use of t

F BUDGET

eyed a subs

on how bud

for each usa Up to 10% to below 20% to below 30% to below 4 40% to below 5 More than 5

Developing Communica

sing, review onitoring bud

he activity al xis is the tim

lysis of Tim

at firms spe of the budg ing variances the budget.

WHEN PR

set of the re dgets are use age in brack

0% 10% 20% 30% 40% 50% 50% 2 2 2 2 the Basis ate Budget

wing and app dget and ana

llocation var me spenton b

me Allocatio B

ending less et, andfirms s. Therefore

REPARED W

espondents,th ed for strateg ket) are: fore

20% 23 23 22 20 22 1 1 2 20 18 2 Negotiat Monitor B

proving, com alysing varia

ries with the udgeting):

n of Budge Budgeting

time on bud spending m ,firmsspendi

WITH BUS

he firms tha gic planning ecasting cas 40% 21 9 22 0 8 2 16 16 15 16 14 16

e and Revise B Budget

mmunicating ance) is appro

time spento

ting Activit

dgeting appe more time on

ing more tim

INESS PLA

at prepared

g. The comm

sh flow (70% 60% 6 5 12 10 12 10 11 10 16 Budget Revie Budge the budget) oximately 7

onbudgeting

ies by Time

ear to alloca n budgeting a me in budget

AN

budgets wit mon uses (wi %), guiding 80% 13 16 14 16 6 13 14 17 15 17 19 18

ew and Approve et Variance

) to time spe :3.

g in the follo

e Spend on

ate more tim appear to all ting adopt a

th business ith the propo

and coordin 100% 4 5 7 8 e Budget 11 ent in owing

me in ocate more

plans ortion nating Figure 4: Analysis of Time Allocation of Budgeting

Activities by Time Spend on Budgeting

The results show that firms spending less time on budgeting appear to allocate more time in developing the basis of the budget and firms spending more time on budgeting appear to allocate more time for analysing variances. Therefore, firms spending more time in budgeting adopt a more sophisticated use of the budget.

USE OF BUDGET WHEN PREPARED WITH BUSINESS

PLAN

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

business conditions when necessary (63%), setting performance targets and evaluating subsequent actual performance against the budgets for future planning purposes (71%), setting performance targets and evaluating subsequent actual performance against the budgets for employees’ performance evaluation purposes (51%), and setting performance targets and evaluating subsequent actual performance against the budgets for employees’ performance compensation purposes (43%). We examined whether these uses vary by firm size as shown in the figure below:

business

and wher revising performa planning performa setting pe employee

by firm s

Fig

Forecasti

business $10m (u forecastin

other fore

The bud

implemen revenueb anomaly generally Guide a Budg Set Tar Set T

during the b re necessary

budgets to

ance targets purposes

ance against erformance t es’ performa size as shown

gure 5: Ana

ing cash flow

plans. This

sed by 76%

ng in larger

ecasting met

dget also ser

ntation (used

below $1m, may indica y use the bu

and Coordinate

Manage by

get accommoda

rget to Monitor

Target for Emp

Set Target fo

Above $1

budget period y, following

reflect the and evaluati

(71%), sett

the budget

targets and e ance compen n in the figu

lysis of Use

w is a comm

s use is espe

%-85% of th firms (used thods such a

rves as an d by 73% of

use of bud ate a differ udget to guid

Forecast Cash

Business Activ

y Variance Ana

ate external ch

Strategy Exec

ployee Perform

or Performance

1b $100m

d (73%), ide

up (66%), changed b

ing subseque ting perform s for emplo evaluating su

nsation purp

ure below:

e of Budget

mon use (by 7 ecially impo

e firms). Th d by 62%-71 as regression

important g f all firm). W

dget to guid rent approac de and coord

hflow (Mean 70

vities (Mean 73

alysis (Mean 66

ange (Mean 63

cution (Mean 71

ance (Mean 51

e Pay (Mean 43

m to $1b $

entifying var monitoring usiness con ent actual pe

mance targ oyees’ perfor

ubsequent ac poses (43%)

t in Strategi

70% of all f ortant in sm

he lower im

1% of the fi n models from

guidance an With the exc e strategy a ch used by

dinate busin

0% 10% 0%) 3%) 6%) 3%) 1%) 1%) 3%)

10m to $100m

riances (e.g.,

any change nditions whe

erformance a gets and ev

rmance eval ctual perform ). We exami

c Planning

firms) for fir maller firms mportance of irms) may a

m interim fin

d coordinat eption of ve appears to in

very small ness activitie

% 20% 30% 40

31% 3

29%

24%

$1m to $

, price and v

s in busines en necessary against the b

valuating su

luation purp

mance again ined whether

By Firm Siz

ms that prep

with annual f using budg arise because nancial state

ion mechan

ry small firm

ncrease with l firms. For

es, and large

0% 50% 60%

51% 6 53% 51% 6 6 45% 38% 6 42% 54% 46% % 5% 47% 53% $10m Belo

volume varia ss conditions

y (63%), se

budgets for f

ubsequent a poses (51%) st the budge r these uses

ze (N=187)

pare budgets l turnover b

get for cash

e these firm

ements.

nism for stra

ms earningan h firm size. r example,

er firms are

% 70% 80% 9

65% 78% 69% 78% 82% 63% 71% 75% 78% 61% 67% 62% 67% 62% 67% 79% 85 65% 62% 76% 82% ow $1m 12 ances) s and etting future actual , and ts for vary s with below flow ms use ategy nnual . The

firms more 0% % 5% %

Figure 5: Analysis of Use of Budget in Strategic Planning By Firm Size (N=187)

Forecasting cash flow is a common use (by 70% of all firms) for firms that prepare budgets with business plans. This use is especially important in smaller firms with annual turnover below $10m (used by 76%-85% of the firms). The lower importance of using budget for cash flow forecasting in larger firms (used by 62%-71% of the firms) may arise because these firms use other forecasting methods such as regression models from interim financial statements.

91

the exception of very small firms earning annual revenue below $1m, use of budget to guide strategy appears to increase with firm size. The anomaly may indicate a different approach used by very small firms. For example, firms generally use the budget to guide and coordinate business activities, and larger firms are more proficient in doing so. However, very small firms use budgets to guide and coordinate business activities with liquidity as the primary constraint. This pattern is consistent with the greater focus of using the budget for cash flow forecasting in small firms.

About 66% of the firms that prepare budgets with business plans also use variance analysis. There appears to be two groups – a minority of very small firms earning annual revenue below $1m (35% use variance analysis), and a majority of larger firms (62%-78% use variance analysis). Variance analysis provides insight on the contribution of price and volume variations to budget deviations. When this information is interpreted with known business activities, it helps to explain the outcome of business strategy. The low use of variance analysis in very small firms probably indicates that maintaining liquidity, as opposed to value maximization, is the primary objective of strategy execution in these firms. It is comforting to note that a majority of the larger firms analyse their variances.

Generally, we expect larger firms to be more sophisticated and extensive in using budgets as a strategic planning tool. Our results suggest that as organisation size increases, firms are more likely to monitor changes in business conditions and revise their budgets accordingly. For instance, only 47% of the firms with annual revenue below $1m use budgeting as a strategic planning tool as compared with 78% of the firms with annual revenue above $1b.

Overall, a clear majority of the firms uses budgets to set targets to monitor strategy execution (71%). This happens less in small firms with annual revenue below $10m (53%-54%), and much more when annual revenue is above $10m (67%-82%). The results are generally consistent with expectation.

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

are met. Approximately 30% of the firms that use the budget to set targets for strategy execution do not use the budget to set targets for employee performance evaluation4

About 16% of the firms that use the budget to set targets for employee performance evaluation do not use budgets for employee performance compensation5. Using the budget results to compensate employee performance is less prevalent than expected, only about 43% of the surveyed firms pay for performance based on budget target achievement.

The prevalence of use of budgets for performance compensation varies with firm size. For firms with above $100m annual revenue, 51% compensates performance based on achievement of budget targets; for firms with $1m to $100m annual revenue, it is approximately a third; for firms with below $1m annual revenue, it is about a quarter.

USEFULNESS OF BUDGET PREPARED WITH BUSINESS

PLAN

We use the same subset of respondents whose firms prepare budgets with business plans (n=187) to examine the usefulness of the operating budgets. The results (with the number of respondents in bracket) are summarized as follows:

4 Figure 5 shows that 71% of 187 firms set budget to monitor strategic performance, and 51% of the same 187 firms set target to monitor employee performance. Therefore, of the firms that use budget to monitor strategic performance, 51/71 = 72% also use budget to monitor employee performance. About 30% (more precisely 28%) of the firms that use budget to monitor strategic performance do not use budget to monitor employee performance

93

Budgeting Practice in Singapore

firms wit

USEFUL

We use (n=187) responde

Only abo

takes so while a obsolete, Similarly “budgetin period”.T constrain majority Budg Bu tra Sou cro B S

th below $1m

LNESS OF

the same s

to examine ents in brack

Figure 6

out 40% of long that by

significant

, the majority

y, only abou

ng is too in This result n

n effective r view.

et helps to a (N= udget helps ack planned urce of budg oss function Budget const business c Slow budget obsole

m annual rev

F BUDGET

subset of re e the usefuln

et) are summ

6: Analysis

the respond

y the time th

portion of

y (60%) doe

ut 40% of th nflexible to

ot only show

response to

allocate Res 183) to coordina strategy (N get variance nal effort (N=

trains respo change (N=1 ing makes b ete (N=184)

Strongly D

venue, it is a

PREPARE

espondents w ness of the o

marized as fo

of Respons

ents agree o he budget is

the respond es not think s

he responde

keep up wi ws that a sign

environmen 0% source te and N=184) helps =183) nse to 83) budget 1% 2% 2% 2% Disagree Di

about a quart

ED WITH B

whose firm

operating bu

ollows:

se to Usefu

or strongly a

ready, it is a dents think

so.

ents agree or

ith business

nificant port ntal change,

20% 18% 5% 7% 5% % 10% % % % 8% 13% sagree Ag ter. USINESS P

ms prepare b udgets. The

lness of Op

agree with th already obso that the sl

r strongly a

changes an tion of the re

, but alsobu

40% 26% 26% % 35% 33% ree Strong PLAN

budgets with

results (wit

perating Bud

he statement olete”. This

low process

gree with th nd lock us i

espondents th

usted the m

60% 51% 48%

ly Agree

h business

th the numb

dget

t that “budg

result shows s makes bu

he statement

n for the bu

hink that bu myththat this

80% 68% 72% 70% 14 plans

ber of

geting s that udgets t that udget dgets is a %

Figure 6: Analysis of Response to Usefulness of Operating Budget

Only about 40% of the respondents agree or strongly agree with the statement that “budgeting takes so long that by the time the budget is ready, it is already obsolete”. This result shows that while a significant portion of the respondents think that the slow process makes budgets obsolete, the majority (60%) does not think so.

Similarly, only about 40% of the respondents agree or strongly agree with the statement that “budgeting is too inflexible to keep up with business changes and lock us in for the budget period”. This result not only shows that a significant portion of the respondents think that budgets constrain effective response to environmental change, but also busted the myth that this is a majority view.

The value of variance analysis as a business tool is clearly recognized. About 88% of the respondents agree or strongly agree with the statement that “Identifying the source of budget variances helps to initiate cross-functional effort to solve business problems”.

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

The importance of the budget for resource allocation is well recognized. Approximately 94% of the respondents agree or strongly agree with the statement that “budgeting helps to allocate resources (people and funding) to the departments that need them”.

In conclusion, the majority of the respondents, whose firms prepare budgets with business plans, view operating budgets as generally useful.

USEFULNESS OF BUDGET IN PERFORMANCE

EVALUATION AND REWARD

We surveyed the respondents whose firms prepared budgets (n=332) about the usefulness of budget for performance evaluation and reward, and the prevalence of known problems.

The valu responde

variances

There is

planned

“budgeti

The impo

the respo

resources

In conclu

view ope

USEFUL

We surv budget fo

Budg

Meet

ue of varian ents agree or

s helps to ini

almost una

strategy. Ab

is a useful to

ortance of th ondents agre s (people and

usion, the ma erating budge

LNESS OF

eyed the res or performan

Figure 7:

get is useful for

ting budget is i perfo

Manag

Th

nce analysis

r strongly a itiate cross-f animous agr bout 98% of ool to coordi

he budget fo ee or strong d funding) to

ajority of the ets as genera

F BUDGET

spondents w nce evaluatio

Budget Us

rewarding perf

mportant in eva ormance (N=32

ger sandbag th

ere is budget r

Strongly A

as a busin agree with th

functional ef

reement on

fthe respond inate and trac

or resource a gly agree w o the departm

e responden ally useful.

IN PERFO

whose firms

on and rewar

sefulness fo

formance (N=3

aluating emplo 23)

he budget (N=3

ratcheting (N=3

Agree Agre

ness tool is he statement ffort to solve

the usefuln dents agree o ck the progr

allocation is with the state

ments that ne

nts, whose fir

ORMANCE

prepared bu rd, and the p

or Performa 0% 10 318) oyee 326) 317) 8% 9 1% 2% 1% 3% e Disagree

clearly reco t that “Iden

e business pr

ness of bud or strongly a

ress of plann

well recogn ement that “

eed them”.

rms prepare

EVALUATI

udgets (n=3 prevalence o

ance Evalua

% 20% 30%

% 9% 15% 14% 15% 24% 12% 14% e Strongly

ognized. Ab

tifying the s

roblems”.

dget to coor

agree with th ned strategy”

nized. Appro

“budgeting

budgets wit

ION AND R

332) about t

f known pro

ation and Re

% 40% 50%

Disagree

bout 88% o source of bu

rdinate and he statemen

”.

oximately 94 helps to all

th business p

REWARD

the usefulne oblems.

eward

60% 70% 8

75 64% 72% 69% 15 of the udget track nt that

4% of

ocate plans, ess of 80% 5% %

Figure 7: Budget Usefulness for Performance Evaluation and Reward

95

The importance of meeting the budget in performance evaluation is also well recognized. About 73% of the respondents agree or strongly agree with the statement “Meeting the budget is very important in evaluating and assessing an employee’s performance”.

The problems of budget manipulation are also prevalent. About 87% of the respondents agree or strongly agree with the statement “Managers who develop budget and are responsible for its achievement often build slack into the budget”. This problem is commonly called sandbagging (or padding) the budget which distorts true estimates on revenues and expenses.

Budget ratcheting is related to the sandbagging problem. About 83% of the respondents agree or strongly agree with the statement “Managers who review and approve budget often increase the targets over time when targeted performance has been achieved in the past”. Budget ratcheting not only counters the slacks built into the operating budget, but also promote behaviours such as unnecessary end-of-period spending so that the budgeted amount remains for the following year.

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1 The majo

42% that

almost al The com performa

CHALLE

We surv challenge

F

From the

that “For Pr Bud Budge There Dis Deli

ority (58%) o t claimed oth lways tied to

mmon feature ance (67%) a

ENGES IN

veyed the r

es in prepari

Figure 9: Dis

e survey resu r afirm’s op

Benefit Exc Preparers/ assump Explicit as strat Budget deli surpr reparers/rev (N dget adapts (N et hinders re

change Low buy-consu is ratcheting tortion of ta

(N nk budgetin apprais

of the respon herwise is s o budget perf es of bonus p and bonus pa

BUDGET P

respondents ing them. Th

stribution o

ults, about60

erating budg

ceed Cost (N Reviewers c ptions (N=32 sumption ba egy (N=324 ivers financ rise (N=324) viewers well =321) * to external =314)* esponse to e

(N=316) -in from insu ultation (N=3 g of target ( rget due to N=314) ng and perfo sal (N=321)

Strongly D

ndents indica surprisingas

formance.

plan include ayable after

PREPARA

whose firm

he results are

of Response

0% of the res get to serve

0% N=325)* common 25)* ased on )* ial if no )* trained change external ufficient 316) N=318) politics rmance 1 2 Disagree Di

ates that thei anecdotal ev

e the presenc

exceeding a

TION

ms prepared e as follows:

e to the Cha

spondents ag

as a more

20% 7% 6% 6% 10% 7% 12% 7% 4% 8% 8% 10% 14% 11% 14% 2 3% 3% 1% 2% 3% 3% 5% 6% 3% 6% 9% isagree Ag

ir bonus is li vidence app

ce of a cap ( minimum ta

d budgets

allenges in

gree or stron effective too 40% 22% 22% 26% 30% 21% 30% 31% gree Strong

inked to mee

ears to sugg

(70%), bonu

arget (59%).

(n=332) an

Budget Pre

ngly agree w ol for strate

% 60% 46% 56 50% 44% gly Agree

eting budget gest that bon

us increasing

.

nd explored

eparation

with the state gic planning % 80 68% 69% 64% 72% 59% 68% 6% 17 t. The

nus is

g with d the ement g and 0% 79% 78%

Figure 8: Use of Budget in Bonus Plan

The majority (58%) of the respondents indicates that their bonus is linked to meeting budget. The 42% that claimed otherwise is surprising as anecdotal evidence appears to suggest that bonus is almost always tied to budget performance.

The common features of bonus plan include the presence of a cap (70%), bonus increasing with performance (67%) and bonus payable after exceeding a minimum target (59%).

CHALLENGES IN BUDGET PREPARATION

97

Budgeting Practice in Singapore 42% that

almost al The com performa

CHALLE

We surv challenge

F

From the

that “For Pr Bud Budge There Dis Deli

t claimed oth lways tied to

mmon feature ance (67%) a

ENGES IN

veyed the r

es in prepari

Figure 9: Dis

e survey resu r afirm’s op

Benefit Exc Preparers/ assump Explicit as strat Budget deli surpr reparers/rev (N dget adapts (N et hinders re

change Low buy-consu is ratcheting tortion of ta

(N nk budgetin apprais

herwise is s o budget perf es of bonus p and bonus pa

BUDGET P

respondents ing them. Th

stribution o

ults, about60

erating budg

ceed Cost (N Reviewers c ptions (N=32 sumption ba egy (N=324 ivers financ rise (N=324) viewers well =321) * to external =314)* esponse to e

(N=316) -in from insu ultation (N=3 g of target (

rget due to N=314) ng and perfo sal (N=321)

Strongly D

surprisingas

formance.

plan include ayable after

PREPARA

whose firm

he results are

of Response

0% of the res get to serve

0% N=325)* common 25)* ased on )* ial if no )* trained change external ufficient 316) N=318) politics rmance 1 2 Disagree Di anecdotal ev

e the presenc

exceeding a

TION

ms prepared e as follows:

e to the Cha

spondents ag

as a more

20% 7% 6% 6% 10% 7% 12% 7% 4% 8% 8% 10% 14% 11% 14% 2 3% 3% 1% 2% 3% 3% 5% 6% 3% 6% 9% isagree Ag vidence app

ce of a cap ( minimum ta

d budgets

allenges in

gree or stron effective too 40% 22% 22% 26% 30% 21% 30% 31% gree Strong

ears to sugg

(70%), bonu

arget (59%).

(n=332) an

Budget Pre

ngly agree w ol for strate

% 60% 46% 56 50% 44% gly Agree

gest that bon

us increasing

.

nd explored

eparation

with the state gic planning % 80 68% 69% 64% 72% 59% 68% 6% 17 nus is

g with d the ement g and 0% 79% 78%

Figure 9: Distribution of Response to the Challenges in Budget Preparation

From the survey results, about 60% of the respondents agree or strongly agree with the statement that “For a firm’s operating budget to serve as a more effective tool for strategic planning and coordination, employee compensation should not be linked to budget achievement”. Therefore, a majority of the respondents think that budget should not be linked to performance appraisal.

About 64% of the respondents agree or strongly agree with the statement that “There is often so much politics involved in the budgeting process that render the final budget less than an accurate depiction of what the firm can actually achieve”. This suggests that the problem that politics degrade the reliability of budget estimates is well recognized.

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

The lack of budget buy-in is a common complain. However, only about 50% of the respondents agree or strongly agree with the statement that “There are insufficient consultations and agreement before the budget is finalized, resulting in inadequate buy-in during implementation”.

Changes in the external environment are inevitable and pose a major problem for budgeting as the underlying assumptions may become invalid. For respondents whose firms prepare a budget, a majority perceives the budget to hinder effective response. Approximately 66% agree or strongly agree with the statement that “When there are unexpected changes in business conditions, the budget hinders resource mobilization needed to respond to the changes”. This is a similar question that we asked respondents who prepared budgets with the business plan “Budgeting is too inflexible to keep up with business changes and lock us in for the budget period” of which only about 40% of the respondents agree or strongly agree with the statement.

Another aspect of the effect of external change on budgeting is to revise the budget. This is surprisingly prevalent. About 85% of the respondents that prepare budget agree or strongly agree with the statement that “When there are unexpected changes in business conditions, my firm requires the budget to be revised in light of the changes”. However, only 63% of the respondents who prepare a budget with business plan claimed, “to monitor any changes in business conditions and where necessary, revise budgets to reflect the changed business conditions”. The results captured a subtle difference where approximately two third of the firms actively monitor business changes and make the necessary changes. But a larger 85% of respondents would revise the budget when their organisations know and require changes in budget to changed business conditions.

There is a clear majority view that budget preparers and reviewers are well trained. About 71% of the respondents that prepare budget agree or strongly agree with the statement that “Budget preparers and reviewers are well versed and trained in variance analysis and the use of static/flexible budget”.

99

of the business outcome that will be achieved if things go according to expectations”. This result is surprising given that there is also a clear majority that thinks that budget manipulation is common. A possible explanation is that the business outcome will be achieved with a comfortable surplus when the environment is stable. This means that target ratcheting cannot fully compensate for the effect of sandbagging. The validity of this interpretation requires further research.

There is also a clear majority view that the budget is based on explicit assumption derived from strategy. About 85% of the respondents that prepare budget agree or strongly agree with the statement that “the budget assumptions are explicit and arise from an agreed strategy”. The result is incongruent with the neely et al. (2001) which states that budgets are “rarely strategically focused and based on implicit but invalid assumptions”. The difference in these two results may arise as the respondents are from different countries and time period.

About 75% of the respondents that prepare budget agree or strongly agree with the statement that “Budget preparers and reviewers share the same understanding of the budget assumptions”. The high percentage is indicative of a well-functioning budgeting process in Singapore.

The litmus test whether budgets should continue to exist depends on whether their benefits exceed budgeting costs. About 75% of the respondents that prepare budget agree or strongly agree with the statement that “the benefits outweigh the costs (time and resource spent) of the budgeting process”. The results show that budgeting would continue to exist in Singapore on its own merits and not due to the lack of viable alternatives or tools.

DISCUSSION AND CONCLUSION

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

to higher value-adding activities such as analysing variance, educating managers on using variance for decision making, supporting analysis such as breakeven, costing, tracking strategy implementation and performance. Our motivation for this study is to better understand this lever and identify where accountants can help.

We found that about 7% of Singapore firms do not prepare budgets, and nearly 30% incorporate business strategy assumptions in budgets to a large extent. About a quarter of the firms with annual revenue below $1m do not prepare budgets, which is much higher than the overall average of 7%. Expectedly, incremental budgeting is more popular than zero based budgeting because it demands less resource.

About 40% of Singapore firms prepare budgets without any business plan compared with 14% in the US. These firms are likely to benefit from discussing about the business strategy and programs before preparing budgets when sequencing the business planning process. Accountants who are involved in the planning stage can better help managers to assess the financial impacts of their plans. The rewards for the accountants come later when the basis of the budget is more easily understood and the managers will be more cooperative in meeting the deadlines for submitting budget drafts.

Multinational companies are more likely to prepare budgets than local companies; diversified firms are more likely to prepare budgets than non-diversified firms. These results allude to more extensive use of budget for strategic control as firms operate in more locations and have more significant business units. The prevalence of the top down approach to bottom up approach to budgeting is approximately 60:40. Top down approach is especially common in small firms while the bottom up approach is more common in GLC.

101

Analysing the average time allocated to budgeting activities reveals that about 70% of the time is spend on developing the budget and about 30% on using it. Disaggregated analysis shows that as managers spend more time on budgeting, a higher proportion of the time is spend on activities for using the budget, which is where the real benefits lie.

Our findings show that for firms that prepare budgets with business plans, managers generally consider budget a useful management tool where pros outweigh the cons. About 40% of the respondents recognize the problems that slow budgeting can make budget obsolete and budget can constrain response to business changes. However, an overwhelming 88%-98% of the respondents recognize the value of budget to allocate resource, coordinate and track strategy, and coordinate cross functional effort via budget variance. The Singapore results, therefore, show that when budgets are prepared with business plans, the prescription of the Beyond Budgeting initiative may be too radical. Instead, improvement of budgeting practice through training and adoption of best practices would be a more pragmatic approach.

Our findings suggest that the use of budgeting in strategic planning appears to be divided into two groups. For very small firms with annual revenue below $1m, the primary objective appears to be maintaining liquidity where there is a strong focus on forecasting cash flows, guiding and coordinating business activities, and low importance associated with variance analysis. In the other group, there appears to be a greater focus on using budget for strategic planning as firm size increases. We observe that as size increases for this group, there is less use of budget for forecasting cash flows, more use for guiding business activities, more management by variance, and more budget revision in response to external changes. Therefore, the budgeting needs in the two groups are different, and designing training programs for budgeting needs to consider the differences.

Asia-Pacific Management Accounting Journal, Volume 12 Issue 1

generally increase with firm size. For example, a quarter of the firms with annual revenue below $1m compensate by budget performance, while half of the firms with revenue above $100m do so. not compensating by budget performance can mean firms are not paying for performance at all, or are using other measures to pay for performance. Other measures to pay for performance include using market indicators like share price, subjective ratings or rankings, peer or subordinate ratings and combinations of indicators.

Our results on challenges in budgeting appear to be less disheartening than suggested by extant literature. Responses agreeing or strongly agreeing to the problems of low buy-ins of budget, target distortions due to politics, budget hindering strategic response and budget ratcheting range from 50% to 76%, but responses agreeing or strongly agreeing to positive aspects like well-trained preparers and reviewers, common assumptions in budgeting, budgets are adapted to external changes, and assumptions are based on strategy range from 71% to 88%. The litmus test that budget benefits exceed costs elicits agreement or strong agreement from 75% of the respondents. The finding means that accountants may be receptive to receive training in how to be more effective in the budgeting process.

REFERENCES

Bazerman, M. H. & neale, M. A. (1993). Negotiating Rationally. new York: Simon and Schuster.

Hope, J. & Fraser, R. (2003). new ways of setting rewards: The beyond budgeting model. Californian Management Review, 45(4), 104-119.

Horngren, C. T., Bhimani, A., Srikant M. & Datar, F.G. (2002). Management and Cost Accounting. Harlow: Financial Times/Prentice Hall.

Jensen, M. (2003). Paying People to Lie: the Truth about the Budgeting Process. European Financial Management, 9(3), 379-406.

103

neely, A., Sutcliff, M. & Heyns, H. (2001). Driving Value through Strategic Planning and Budgeting. new York: Accenture

Rumelt, R. P. (1974) Strategy, Structure and Economic Performance. Boston: Harvard Business School.