In the second paper in our Banking Series 2015, we explore product innovation in retail banking. We assess whether current products are relevant today, and recommend how the market can offer customers what they are really looking for from their banks.

Banking Series 2015:

Product development

Are today’s retail banking products fit for the

modern world?

Retail banking products

as we see them

There is competitive advantage to be gained and commercial value to be realised through innovating to develop new solutions – satisfied customers are loyal, and it is far less expensive to retain an existing customer, than acquire a new one.

The absence of any innovation in the retail banking market means customers are just not switching providers. Government initiatives such as the Current Account Switch Service have not been successful in significantly increasing switching volumes – switching only increased to 1.2m customers in 2014, up from 1m in 2013 (Source: Payments Council).

However, Santander has proved that customers will switch providers if offered a new and different type of product. After launching the 123 account, they experienced net gains of current account customers of 60,000, 12%, in Q2 2014 - the highest of any UK bank. Based upon Payments Council data, it appears that the net winners in the switching market are those who offer customers something for free. But with these products only offering customers an incentive to switch and no real innovation in product, does this go far enough? The current account proposition hasn’t really changed since the offset mortgage in 1994. In fact, any innovation happening inside the retail banking market is driven almost exclusively by new entrants. Most of these new entrants have a laser focus on enabling their proposition through seamless digital channels, rather than offering any truly new banking products – so there remains a massive opportunity for product innovation.

We believe that there are three key issues with the retail banking product set as it stands today:

1. Where is the innovation? No notable development in the retail banking product set since 1994. Product development in retail banking has been woefully poor to date.

2. Products fit for today’s world? Are we trying to shoehorn products designed to work inside a physical branch-based environment, into an online and real-time world?

3. Products fit for today’s life stages? We are fast becoming a cashless society and we are living longer, so our needs are changing. Do current retail banking products actually reflect what we need?

Innovation, innovation,

innovation

After an assessment of today’s retail banking products, a set of questions are clear:

Do customers want products as they are currently packaged? i.e. is there a need to have a current account, a savings account, credit cards and a loan? It appears that there isn’t any real benefit to the customer of segregating these products and by doing this, banks are actually creating more complexity for customers.

Do customers want different repayment vehicles for all their lines of credit, or would one mechanism make it easier for all?

Consider the benefit of offering higher net worth customers one line of credit that they could use for whatever they want.

Do customers want to be treated fairly? i.e. I can’t pay my card this month, but I have a revolving loan at a lower rate and my bank automatically pays off my card using the loan. I am about to go overdrawn so my Bank switch up to £1k of savings to my current account and let me know this had been completed.

If we look at what we as customers actually want from our banks, it’s very simple:

1. I want somewhere to safely deposit my income, no matter where it comes from. Somewhere that earns me interest when I am in credit.

2. I want to be able to easily make the different types of payment that I need to make, in the cheapest way possible. I want my bank to protect me from the complexity of the payment mechanisms in the market.

3. I want to be able to borrow money at competitive rates, I want flexible debit and credit limits and I want my bank to help me access my funds immediately in an emergency.

4. I want to understand how much money I have

available, whenever and wherever I am.

5. I want to be able to access my money and my bank’s services from my mobile devices

– having to go into the branch or use internet banking from a computer just doesn’t cut it any more.

And if I have more complex financial affairs:

1. I want to know what money is available to me

and what it will cost me to access that money.

2. I want help with financial forecasting and planning to help me better understand and take control of my financial position.

3. I want to be able to keep different types of transactions separate. I want a separate place for work expenses and my income from letting my property.

Fulfilling these core customer product needs is critical to a Banks success and must be considered a high priority within the organisations.

“If we look at what we as

customers want from our

banks, it’s very simple.”

Looking at the youth market today, we see a new type of customer. Online and mobile technologies are central to everyday life and technology is transforming the way individuals and organisations interact. The Office for National Statistics (ONS) found in 2014 that almost every single 16-24 year-old in the UK (96%) had used a mobile phone or portable device to get online while on the move. Generation Y, the millennials, were born into a world where the internet, smartphones and social networking are embedded into their everyday lives and everything from socialising and using maps to decide what and where to buy is achievable online and mobile.

The everyday banking needs of Generation Y:

I want access to my accounts online, in real time, and when I am on the move, so that I can:

- see my latest balances

- check payments and receipts have been made as planned

- make payments in a way that suits me

I want to purchase the right products, online and in real-time to help me maximise my money and spending power, so that I can:

- see my balances immediately updated

- receive offers that are actually relevant to me, rather than being pushed irrelevant products

I want my bank to help me optimise my finances by:

- looking after my personal data, and not allowing anyone else to access it without my permission.

Government scheme Midata, for example, safely and securely stores customer data in a personal data service that has the same level of security as bank systems. Data is individually and uniquely encrypted, which means customers are in complete control and can delete it all at any time.

- letting me easily see my forecasted position at the end of the month, year, and in the medium-term.

Investment management service Nutmeg does this and will build and manage

Products

fit for today’s world?

a portfolio for the customer based on information about their goals, risk tolerance and investment horizon. It allows customers real-time access to view their portfolio’s performance.

- playing me back useful insights.

Online personal finance management service Mint.com creates personalised budgets for their customers, providing custom tips on saving money and alerts customers to any unusual account charges. Mint provides its customers with an aggregated view of all of their accounts, loans and credit cards on one single slick dashboard.

- enabling me to easily compare deals. There are many price comparison websites, such as moneysupermarket.com and moneysavingexpert.com. They provide an impartial comparison of financial products and services from a range of providers in one place, making it easy for customers to find the best deal.

- sending me deals and offers that are relevant to me

Banks should be using their wealth of customer data to provide relevant offers. Think like Amazon: they use advanced algorithms to provide relevant recommendations based on past purchases.

- using scale to get me a better deal.

Daily deals website Groupon sells vouchers for products or services on behalf of

merchants. By generating a large number of takers on behalf of the merchant, they can dramatically undercut the margin taken by alternative channels to market.

I want to be protected from fraud:

- I don’t want my bank to call me and ask for my personal details while I am in a public place and can be overheard

- I need secure access to my accounts with only one set of login details to remember

- I need to know that if something does go wrong, I am fully protected

Digital products

for older generations

There are significant differences in the ways different generations typically use technology. Millions of older people are keen users of online banking and mobile banking applications. Nearly 2.3 million people in the UK over the age of 70 now use online banking (British Banking Association, 01/15). This is likely to increase, given the rapid growth of daily internet use by this age group, which has more than tripled between 2006 and 2014 (ONS 2014).

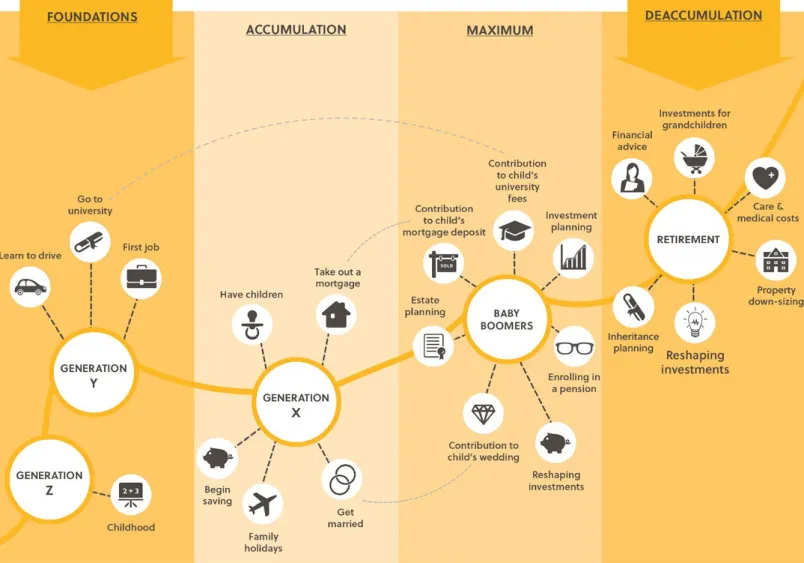

Over the last 20 years, considerable societal change has impacted the stages of life we all go through and the financial decisions that come with them. From the rising rate of divorce, more single person households, greater physical and job mobility, to longer life expectancy, these changing factors have a big impact on our financial needs.

What products

should banks consider?

THE GOLDEN OPPORTUNITY: RETIREES

It is evident from Figure 1 that customers at pre- and post-retirement stages have a number of underserved trigger points. This presents great opportunity for banks to design new propositions to take to market. What are the main drivers and what products do this generation need?

In the UK, a shortage of affordable housing coupled with elderly relatives needing care for longer is driving more families to move three generations in under one roof. According to research conducted for The Telegraph by Barclays, two thirds of us believe the solution to an ageing population would be to move towards a multi-generational household. But, only 1% of us said our current house would be suitable. Banks have historically been reluctant to lend to people past retirement age, but this is something that must be reassessed. In addition, the tax implications of estate planning will become increasingly complex given these new trends, an area where banks should be providing their expertise and guidance. In the private sector, pensions have moved away from final salary towards defined contribution pensions over the last 15 years. Combined with job mobility, many people now have multiple pension pots across various providers. With pension changes implemented in April allowing cash drawdowns for over 55s, how will these be used to secure a better long-term investment? Banks must consider the impact that the pension changes will have on the banking products required by people post retirement. From April 2015, those over 55 have been given the option of taking a number of small lump sums, with 25% of each sum tax-free.

Every milestone in our lives is a crucial opportunity for banks to trigger us out of apathy and encourage us to think about adopting a new product or service, or to switch providers entirely. Different types of product are required at each of our life stages. Using what we know about generation Z, Y, X and the baby boomers, banks can map out customer journeys and develop deeper understanding of customer needs to inform both new product development, and product marketing strategies.

There are a number of reasons why banks should focus on serving customers in relatively ‘new’ stages of life better:

Customers will acquire more complex products as they transition through key life stages. This is profitable for the customer and the bank. Residential care may well now be the biggest financial decision of an individual’s life. With an increasing need and substantial costs of this care, specialist banking products are required. New pension freedoms will give investors more control and they will be able to effectively use their pensions as a bank account, as the money they have saved will sit in a pension pot that they can access whenever they want.

Multi-generational living is starting to look like an increasingly attractive option to reduce outgoings while maximising a combined standard of living. Banks have a fantastic product development opportunity provide ‘family’ accounts that combine assets and liabilities.

So what does

the future look like?

There are some common characteristics starting to develop around the world, inching retail banking closer towards alignment with what their customers need:

CUSTOMER-CENTRIC: US bank Simple has been built around the customer. For example, they enable their customers to set limits online to help them make their buying decisions. A customer may ask: Can I afford to buy this suit, and still pay all of my regular bills? The ‘Safe-to Spend’ feature gives an accurate picture of what a customer can safely spend by taking their balance and subtracting upcoming bill payments, pending transactions and any set goals they may be saving for.

DIGITAL: Atom Bank will bring the first fully digital bank to the UK and Starling, a new UK challenger bank, is also promising a digital proposition. Starling challenges previous process norms, offering the only current account made for the smartphone generation, and product innovation we can only hope will be high on their agenda.

KEENLY-PRICED: In a bid to attract new customers, TSB has launched a current account that gives customers 5% interest on credit balances. However, these types of products are loss leaders in the marketplace and not sustainable in the medium term.

RELEVANT: Santander 1|2|3 rewards customers with cashback and loyalty offers relevant to their lifestyle.

PERSONALISED: Crédit Agricole opens core architecture and exposes APIs, allowing developers to create applications for customers, and increases the perception of innovation in the banking market by tapping into expertise outside it.

TARGETED: American Express provides ‘Offers Targeted to you’ based on customer data (e.g. transaction history, demographics) with a focus on relevance and value.

These common characteristics can be grouped into a number of core customer requirements, which banks must deliver.

Specifically designed for online Valuable Proactively informative Digitally optimised Simple to interact with Empowering

So what does

the future look like?

In order to innovate in product, retail banks should be looking at a person’s overall financial needs:

Area Description Example

Valuable

Generates value for customers, either through credit interest, or allowing them to purchase the goods and services they desire.

If you have money in your facility at the end of the month, we will pay you interest on it, and will tell you how much money you have made.

We will tell you simply how to grow your money over time and advise when the time is right to lock your money away in a longer-term, higher paying account.

Proactively informative

Work with key partners to get customers a better deal on everyday items at the point of purchase.

We will provide you with a tiered level of credit. In real time, we will let you know if you are going to use that credit and how much it will cost you.

If you are a property investor, we will tell you about up and coming areas you might want to consider, or recommended tradespeople in the areas local to your properties, and relationships we have with letting agents that mean we can help you negotiate a lower price.

Digitally optimised

Able to transact across multiple channels, and then pick up where the customer left off.

There is no need to have multiple accounts across multiple payments providers (ApplePay, Paypal etc) - we will deal with that on your behalf and present you with a consolidated view.

Specifically designed for online

Not just shoehorning a branch-based product into something which ‘fits’ online and mobile channels.

We will design our products so that we can manage data intelligently and gain deep customer insight, keeping our products fresh and relevant to your needs.

Simple to interact with

Make it very easy for the customer to do whatever they need to on the channel they want to do it on.

We will give you a facility you can use to easily manage your everyday banking.

You can make national and international payments at the cheapest possible rate, guaranteed.

Empowering

Put power back into the hands of the customer. Give them a choice about their money and how they can best use it to meet their needs and achieve their life goals.

We will provide you with a single line of credit which you can use to buy whatever your heart desires.

We will give you the choice of how to invest the credit we give you. So long as you can make the monthly repayments, we don’t mind if you buy one big property or a number of smaller properties.

We will regularly tell you if and how your property values have changed, and we will automatically let you know if the changes to your property values mean your line of credit could be extended (or contracted).

Winning with

product innovation

Product innovation within the Banking industry is far behind other, more innovative industries. Products are arguably not fit for today’s world or the ‘new’ customer life stages we are observing. Action is required to offer customers a better deal, and banks must innovate in order to stay in the market and retain existing customers.

CREATING INNOVATIVE PRODUCTS FOR CUSTOMERS IS KEY FOR BANKS IN ORDER TO:

Create loyalty and therefore retain existing customers, reducing churn which is expensive Increase customer advocacy, meaning that they tell their friends about the great products they have.

WHAT WILL IT TAKE TO REACH THE HALCYON DAYS OF RETAIL PRODUCT INNOVATION?

Focus on simple products which actually meet customer’s needs, breaking down previously constrained designs

Assess the broader market, challenging previous assumptions about suitability of products for key life stages.

Challenge all of the norms – just because it has always been like that, doesn’t mean it always should be…or that it is the optimal way

Use data and analytics to deliver ‘knowledge’ to customers, allowing them to make empowered decisions

MOVING INTO A MODERN, PRODUCT-LED WORLD WON’T BE A SIMPLE JOURNEY:

Use innovative approaches to drive product design – agile design can quickly take product design from initial thoughts to prototype Build robust business cases for these new products to ‘sell’ the concept to the board in order to gain adequate investment to deliver the innovative design

Don’t forget the marketing, and how you will differentiate within the marketplace. Complete market analysis must be carried out to ensure that new products design aren’t just “me too”. Make switching to your products as simple as possible – lean process engineering will make the process much slicker for new clients and become a welcome first customer experience. Product systems are often difficult to configure and hence the reason why we haven’t seen much innovation – this will require robust delivery management in order to manage the disparate elements of the platform which will need to be configured

Investment in data and analytics in order to return knowledge to a customer will be costly and need to be carefully articulated.

How Elixirr

can help

What do banks need to do in order to embrace product innovation?

We work with financial services institutions, helping them in the following areas to transform their business:

INNOVATIVE PRODUCT DESIGN:

definition of new product design, including the business case

to support these new product to ensure that they are commercially viable.

PROGRAMME DELIVERY:

managing major change programmes globally to effectively deliver

the expected results. We have many very experienced complex programme leaders who

are used to managing multiple workstreams, vendor arrangements and projects in the

retail banking industry and beyond. We also provide robust, and proactive PMO services,

not just a reactive capability that tells you what happened after the crisis.

BUSINESS CASE DEVELOPMENT:

we have experts in business cases development, for

new market launches, or new product launches who can help expedite business case

production and assist with the story-telling at board level.

TARGET OPERATING MODEL:

defining both the ‘As-is’ and the ‘To-be’ operating models,

understanding what differentiates the ‘To-be’ in the broader marketplace, and what it

takes to deliver those operating models in a practical way.

CUSTOMER JOURNEY MAPPING:

our experts are able to stand in a customers shoes and

design processes which are straightforward from their point of view.

SOURCING:

we are experts in supporting numerous sourcing processes for clients, ensuring

that the right partners, or solutions are chosen. We can run the vendor selection process

end-to-end, from initial RFI/market testing through to contracting, transition and

ultimately vendor management through your Commercial Office.

INNOVATION AGENDA:

Elixirr are on the ground in the startup ecosystems of London and

Silicon Valley. We are working with VC’s and startups in both locations to understand

emerging trends and disruptive technologies and companies. We then help our clients

connect to relevant startups to deliver new technology into their organisation.

Banking Series 2015:

future publications

PRODUCT DEVELOPMENT: BANKING PRODUCTS FIT FOR THE MODERN WORLD?

Starting with a blank sheet of paper, how would you design banking products for the modern, but regulated world?

UTILITY BANKING: OPTIMISING OPERATING MODELS THROUGH INDUSTRY PARTNERSHIPS.

Which banking capabilities are non-differentiating and don’t provide strategic advantage? Are industry-wide utilities a cost effective answer?

RESILIENCE: CORE BANKING SYSTEMS INFRASTRUCTURE – CHALLENGES AND OPPORTUNITIES.

How do you optimise resilience across core banking platforms while addressing the challenges and opportunities presented by today’s environment?

WORKFORCE 2020: DESIGNING MODERN ORGANISATIONS

How do banks create a service-led organisation committed to innovation that best serves their customers?

REGULATION: ANALYSING THE WHOLE

How do banks optimise the regulatory change required, taking implementation timelines, competing priorities and potential overlaps into account?

KY WHO? – THE COST OF GETTING IT WRONG

The potential for abuse of the banking system by criminals is shining a new regulatory interest on Know Your Customer (KYC) obligations. How do banks put the necessary controls in place to better understand their customers, but avoid a negative impact on the customer experience?

OPTIMISING AML

The key to Anti-Money Laundering (AML) is data. Banks must consolidate discrete data points in order to identify abuse within their systems. How do they define a clear AML strategy to enable them to do this?

BANK DIGITECH

The only route for a retail banks’ success is to fully embrace digital. It is not enough to digitise existing processes, banks must redesign their core processes to operate efficiently in the digital age. How can banks make this happen?

RETAIL BANK’ATION: SOLVING THE IDENTITY CRISIS IN BANKING

With a plethora of new entrants, and other providers nibbling away at the traditional core of banks, now is the time to decide what is a bank and what purpose do they serve in the market.