Preventive Action Plan Belgium

After regulation No 994/2010 of the European Parliament and of the Council

of 20 October 2010 concerning measures to safeguard security of gas supply

December 2014

FPS Economy, S.M.E.s, Self-Employed and Energy North Gate III, Koning Albert II-laan 16

Table of contents

EXECUTIVE SUMMARY ... 3

1. INTRODUCTION ... 4

2. CONTEXT REGULATION 994/2010... 5

3. SUMMARY OF THE MAIN RESULTS OF THE RISK ASSESSMENT ... 6

3.1. RISK & SCENARIO ANALYSIS ... 6

3.2. RISK EVALUATION ... 8

3.3. RISK TREATMENT ... 9

3.4. DIVERSIFICATION ANALYSIS ... 12

4. INFRASTRUCTURE & SUPPLY STANDARD ... 13

4.1. INFRASTRUCTURE STANDARD (N-1) ... 13

4.2. SUPPLY STANDARD ... 15

4.3. INTERRUPTIBLE & PROTECTED CUSTOMERS ... 20

4.3.1. End-users on the distribution network ... 20

4.3.2. End-users on the transport network ... 23

4.4. STRESS TEST ... 25

4.4.1. N-x analyses ... 25

4.4.2. Scenario analysis ... 25

4.4.3. Commodities analysis ... 25

5. OBLIGATIONS IMPOSED ON NATURAL GAS UNDERTAKINGS AND OTHER RELEVANT BODIES, INCLUDING FOR THE SAFE OPERATION OF THE GAS SYSTEM ... 27

5.1. PUBLIC SERVICE OBLIGATIONS (PSO’S) ... 27

5.1.1. National legislation ... 27

5.1.2. Regional legislation (distribution network) ... 28

5.2. QUALITY & LEVEL OF MAINTENANCE OF THE NETWORK ... 28

6. OVERVIEW PREVENTIVE MEASURES ... 29

6.1. SUPPLY SIDE & MARKET BASED MEASURES ... 30

6.1.1. Increased import flexibility (through long term and short term contracts) ... 30

6.1.2. Facilitating the integration of gas from renewable energy sources into the gas network infrastructure ... 30

6.1.3. Commercial gas storage – withdrawal capacity and volume of gas in storage ... 31

6.1.4. LNG terminal capacity and maximal send-out capacity ... 32

6.1.5. Diversification of gas supplies and gas routes ... 32

6.1.6. Reverse flows and investments in infrastructure ... 33

6.1.7. Coordinated dispatching by transmission system operators ... 33

6.2. DEMAND SIDE & MARKET BASED MEASURES ... 33

6.2.1. Use of interruptible contracts ... 33

6.2.2. Fuel switch possibilities including use of alternative back-up fuels in industrial and power generation plants ... 34

6.2.3. Voluntary firm load shedding ... 35

6.3.1. Use of strategic storage ... 35

6.3.2. Enforced use of electricity generated from sources other than gas ... 35

6.3.3. Enforced storage withdrawal ... 35

6.4. DEMAND-SIDE & NON MARKET BASED MEASURES ... 36

6.4.1. Enforced fuel switching ... 36

6.4.2. Enforced utilisation of interruptible contracts ... 36

6.4.3. Enforced firm load shedding ... 36

7. MECHANISMS FOR COOPERATION WITH OTHER MEMBER STATES ... 36

7.1. TRANSPARENCY ... 37

7.2. COHERENCE ... 37

7.3. COOPERATION... 38

7.4. COMMUNICATION ... 38

7.5. COMMON CRISIS EXERCISES ... 38

7.6. LEARNING FROM BEST PRACTICES... 39

8. INFORMATION ON EXISTING AND FUTURE INFRASTRUCTURE IN BELGIUM ... 39

8.1. EXISTING AND NEW INFRASTRUCTURE ... 39

8.2. REVERSE FLOW ANALYSIS ... 42

ANNEX 1: OVERVIEW TABLE OF THE MARKET BASED SUPPLY SIDE MEASURES ... 45

ANNEX 2: OVERVIEW OF THE MARKET BASED DEMAND SIDE MEASURES ... 48

ANNEX 3: CALCULATION DETAILS AND RESULTING ESTIMATIONS OF GAS DEMAND BELGIAN PROTECTED COSTUMERS ... 49

Executive Summary

The preventive action plan identifies all the measures the Belgian government and the stakeholders in the gas industry can take in order to reduce risks that can occur in the gas supply chain. A series of risks were already identified in the risk assessment drafted by the Energy administration in 2011 and was updated in 2014. From the risk analyses, we could conclude that the Belgian gas system never had any serious incidents threatening the gas supply to protected customers. However, if there is an accumulation of circumstances (for example a pipeline blow during very severe winter conditions), the gas supplies to protected customers1 could be endangered.

The preventive action plan picks up on the main points of the risk analyses, notably what we consider as main threats for the Belgian security of supply (mainly incidents upstream that cause a complete shut off of one source of gas), the results of the N-1 analyses and an analyses of the reverse flows and the degree of diversification. One important element in the preventive action plan is the supply standard. In Belgium, a main part of the responsibility to keep the gas system in balance lays with the shippers and suppliers. Therefore the suppliers will have to meet certain obligations if they are supplying the distribution network. At last, we will give an indication of which market and non-market based measures could be implemented in Belgium.

1

Protected customers are defined in Belgium as the consumers connected to the distribution grid (residential and non-residential), as described in the Ministerial Decree on 18 December 2013 establishing the federal emergency plan for the supply of natural gas.

1.

Introduction

The purpose of the preventive action plan is to

identify the possible measures the Belgian

government and the stakeholders in the gas industry can take in order to reduce risks that could occur in the gas supply chain. It gives an overview of the actions that already exist and makes an analysis of new actions that could be introduced. We already mention that a distinction will be made between risks that could have an impact on a local level, or

incidents that could endanger the entire gas systems and therefore have possible effects on neighbouring countries as well. Our primary focus will be on the risk for the entire gas system. Risks that only have a local impact are part of the emergency planning of the transmission system operator and/or the distribution system operator.

In the risk assessment a series of risks were identified. The risk assessment gives a first indication of the main risk for our gas security of supply. The actions to take to prevent and mitigate the risks are now taken up in the preventive action plan and in the emergency plan. Article 4 of the Regulation stipulates that the plans should be notified to the European Commission by December 3, 2014. In the first part of the preventive action plan, we will sum up the main elements from the risk analyses, notably what we consider as main threats for the Belgian security of supply (mainly incidents upstream that cause a complete shut off of one source of gas), the results of the N-1 calculation, an analyses of the reverse flows and the degree of diversification. Secondly, we will take a closer look at the supply standard and what will be done to enforce it. Thirdly, we will list up the generally accepted risks in the gas supply chain and what actions already exist in Belgium to mitigate them, and finally we will make an analysis of the market based and the non-market based measures that could be implemented in case of an emergency.

On this last point, we can already point out that in Belgium most of the focus during a supply disruption lies on actions at the supply side. Momentarily, there aren’t any possible actions that can be conducted on the demand side to reduce the impact of a supply disruption. However a study is being conducted to investigate possible actions that can be taken in the future.

The preventive action plan will make an evaluation of the actions to take. The next step will be to effectively implement those measures with an accurate legal framework and a regularly follow up of those measures.

2.

Context regulation 994/2010

The intention of the Regulation 994/2010 of the European Parliament and of the Council Concerning Measures to Safeguard Security of Gas Supply is to prevent the kind of gas crisis situations EU-27 experienced in January 2009. One of the means considered in the Regulation to achieve this target is performing a full risk assessment, a preventive action and emergency plan.

As for the preventive action plan, article 5 of the Regulation stipulates the following on the content of the Preventive Action Plan:

“The national and joint Preventive Action Plans shall contain:

(a) the results of the risk assessment as laid down in Article 9 ( CHAPTER 3);

(b) the measures, volumes, capacities and the timing needed to fulfil the infrastructure and supply standards, as laid down in Articles 6 and 8 (CHAPTER 4);

(c) obligations imposed on natural gas undertakings and other relevant bodies, including for the safe operation of the gas system (CHAPTER 5);

(d) the other preventive measures, such as those relating to the need to enhance interconnections between neighbouring Member States and the possibility to diversify gas routes and sources of supply, if appropriate, to address the risks identified in order to maintain gas supply to all customers as far as possible (CHAPTER 6);

(e) the mechanisms to be used for cooperation with other Member States for preparing and implementing joint Preventive Action Plans and joint Emergency Plans, as referred to in Article 4(3), where applicable (CHAPTER 7);

(f) information on existing and future interconnections, including those providing access to the gas network of the Union, cross-border flows, cross-border access to storage facilities and the physical capacity to transport gas in both directions (bi-directional capacity), in particular in the event of an emergency (CHAPTER 8);

(g) information on all public service obligations that relate to security of gas supply.

(CHAPTER 5)”

This report is fully structured in function of above bullets and will attempt to address the respective elements.

3.

Summary of the main results of the risk assessment

As mentioned, in 2011 the Belgian Energy Administration as competent authority performed a risk assessment, which was based on the International Standard on risk management ISO 31000 that suggested by the Joint Research Centre (JRC) of the European Commission. This risk assessment was updated in 2014.

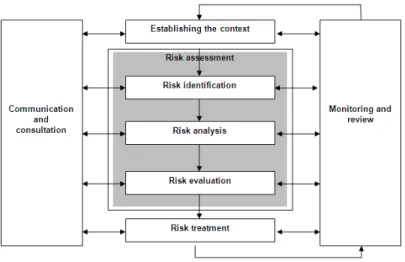

Figure 1: Methodology risk assessment

The methodology is structured in five steps:

• Step 1: Establishing the context of the Belgian gas sector • Step 2: Risk identification

• Step 3: Risk analysis • Step 4: Risk evaluation • Step 5: Risk treatment

This chapter will go deeper into some general results of the Belgian risk assessment, and more specifically results from the scenario analysis and risk evaluation (step 3 & 4). Risk treatment (step 5) is proposed for identified risks. Other, more specific results of the risk assessment (such as infrastructure & supply standards, diversification analysis, reverse flow analysis,…) will be discussed in separate chapters.

3.1.

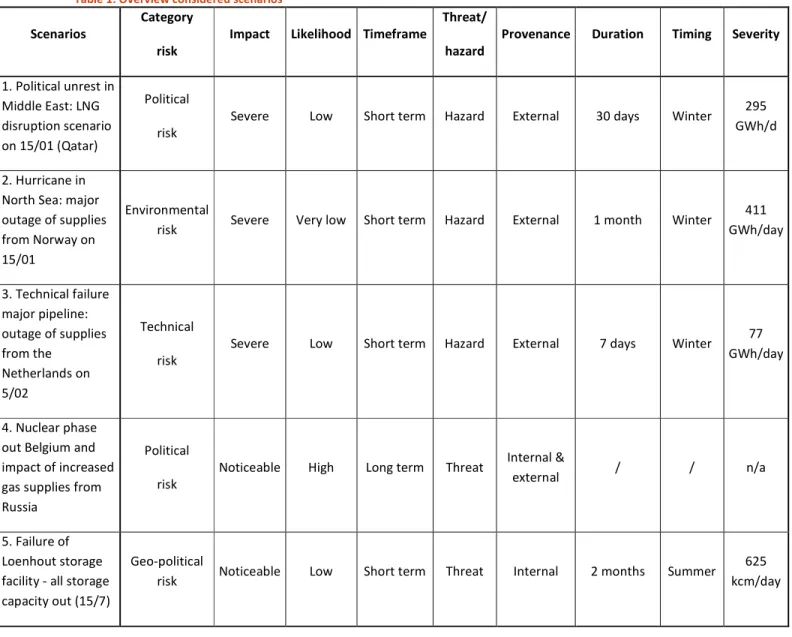

Risk & scenario analysis

Five risk scenarios were identified in the risk assessment of which three incidents upstream and two scenarios with incidents internally in the Belgian network. The three upstream scenarios concerned an LNG disruption from Qatar (ex. through the closure of the Strait of Hormuz), a technical incident

on Zeepipe (supplies from Norway) and an incident on one of the L-gas pipelines coming from the Netherlands. The two scenarios we envisaged inside the Belgian gas network are an incident with the storage facility and an increased gas demand due to the nuclear phase out. Outside of those scenarios identified, technical incidents (pipeline burst, leakage, ICT breakdown, accidents, loss of power supply, explosion...) can occur anywhere else in the network.

Table 1: Overview considered scenarios

Scenarios

Category risk

Impact Likelihood Timeframe

Threat/ hazard

Provenance Duration Timing Severity

1. Political unrest in Middle East: LNG disruption scenario on 15/01 (Qatar) Political risk

Severe Low Short term Hazard External 30 days Winter 295 GWh/d

2. Hurricane in North Sea: major outage of supplies from Norway on 15/01

Environmental

risk Severe Very low Short term Hazard External 1 month Winter

411 GWh/day 3. Technical failure major pipeline: outage of supplies from the Netherlands on 5/02 Technical risk

Severe Low Short term Hazard External 7 days Winter 77 GWh/day

4. Nuclear phase out Belgium and impact of increased gas supplies from Russia

Political risk

Noticeable High Long term Threat Internal &

external / / n/a

5. Failure of Loenhout storage facility - all storage capacity out (15/7)

Geo-political

risk Noticeable Low Short term Threat Internal 2 months Summer

625 kcm/day

As for any of the simulated scenarios, the impact on the gas flows in and to Belgium will be manageable for a certain period of time and the supplies to protected customers will not be impacted, we assume that this will be the case for either incident in the network.

Of course, the impact of a technical incident in the Belgian network will depend on several conditions (timing of the incident e.g. during winter peak demand or summer, disproportion in the demand zones or supply entries in the Belgian network, ...). For example, an incident on Zeepipe in the middle of winter will lead to the emergency phase in a couple of hours if the market is not able

to renominate the gas via other entry points within three hours. The impact of the closure of the Strait of Hormuz will be much harder to assess. First of all, in the risk analyses, we could see that the impact on the Belgian gas network would be manageable if supplies could be increased from other sources. However, as all of the Qatari gas would fall away due to a blockage in the strait of Hormuz, all European buyers of Qatar gas would draw on their additional supplies, which could come from the same sources as the Belgian supplies.

3.2.

Risk evaluation

In the risk evaluation, all risks (with its likelihoods and impacts) identified and analysed during the risk identification & risk analysis, are evaluated.

• Risk is acceptable => OK

• Risk is not acceptable => risk treatment/risk avoidance/risk transfer is needed.

As for the risk evaluation, it is not feasible to guarantee a total protection of the entire Belgian gas supply. A reasonable risk threshold, that determines a realistic protection level, has to be defined. The level of the threshold will depend on several matters, most of all on:

- the quantities of gas lost

- the probability of the risks considered - the duration to cover

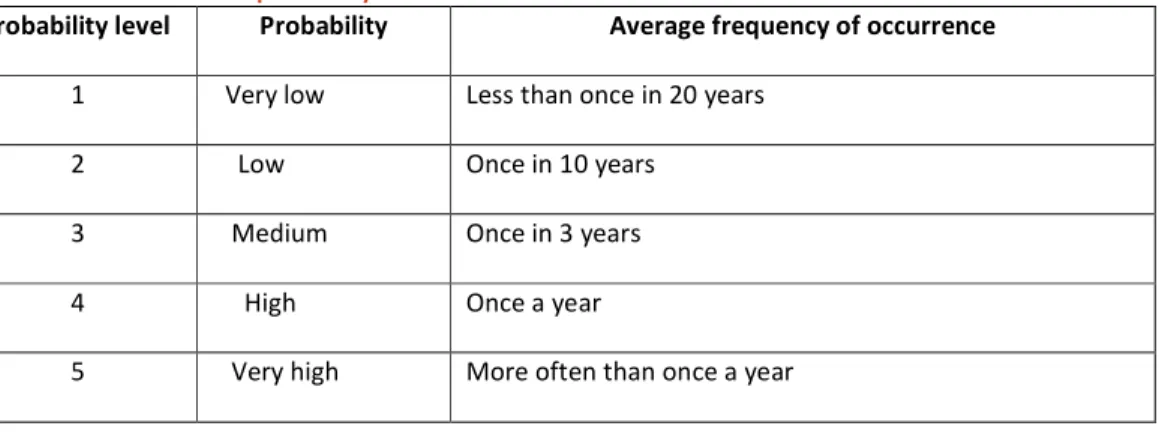

The guarantee of a secure gas supply in Belgium comes at a cost. The higher the risk that needs to be covered, the higher the price tag. We can try to classify the risks according to the probability levels and the impact. The classification only gives a broad indication of the risks, as the impact of the same risk may vary according to the timing and the location of the incident. We have tried to take into account the most likely outcome of the incidents based on historical experiences.

Table 2: Severity levels of consequences criteria

Impact Description

Minor Short-term disturbance of sector activity. No direct consequences to other sectors. Low Temporary disturbance of national gas supply. Consequences are eliminated by efforts of

Fluxys Belgium alone. Impact of consequences of disturbance of gas supply on other sectors (heat supply) are negligible.

Noticeable Gas supply disruption to the area and necessity of back-up systems or alternative measures. Severe The impact of the disruption of gas supply to other sectors is severe. (Load shedding) Very severe Long-term efforts required for restoration of gas supply. Impact on other sectors and

Table 3: Assessment of the probability accidents

Probability level Probability Average frequency of occurrence

1 Very low Less than once in 20 years 2 Low Once in 10 years

3 Medium Once in 3 years 4 High Once a year

5 Very high More often than once a year

The risk matrix below (table 4) gives an overview of the main scenarios (see table 1) as identified in the risk assessment:

Table 4: Risk – matrix

Probability

Impact Very low Low Medium High Very High Minor Low Noticeable Failure Loenhout Nuclear phase out Severe Loss supply Norway Closure strait Hormuz; L gas scenario Very Severe

Conclusion: From this risk assessment & analysis, we could conclude that the Belgian gas system has never had any serious incidents threatening the gas supply to protected customers. However, if there is an accumulation of circumstances (for example a pipeline blow during very severe winter conditions), the gas supplies to protected customer could be endangered.

3.3.

Risk treatment

Risk treatment (step 5) is not part of the risk assessment as such and is addressed in the preventive action plans and emergency plans. The main threats that we identified in the risk assessment are mostly of a technical nature. Indeed, most of the incidents in the gas network that occurred in Belgium were either pipeline blows (ex. Ghislenghien), or other short lived technical incidents on interconnection points, this on either side of the border. Fortunately, those incidents have always been handled without the system integrity being endangered and with no impact on the gas consumption of the protected customers.

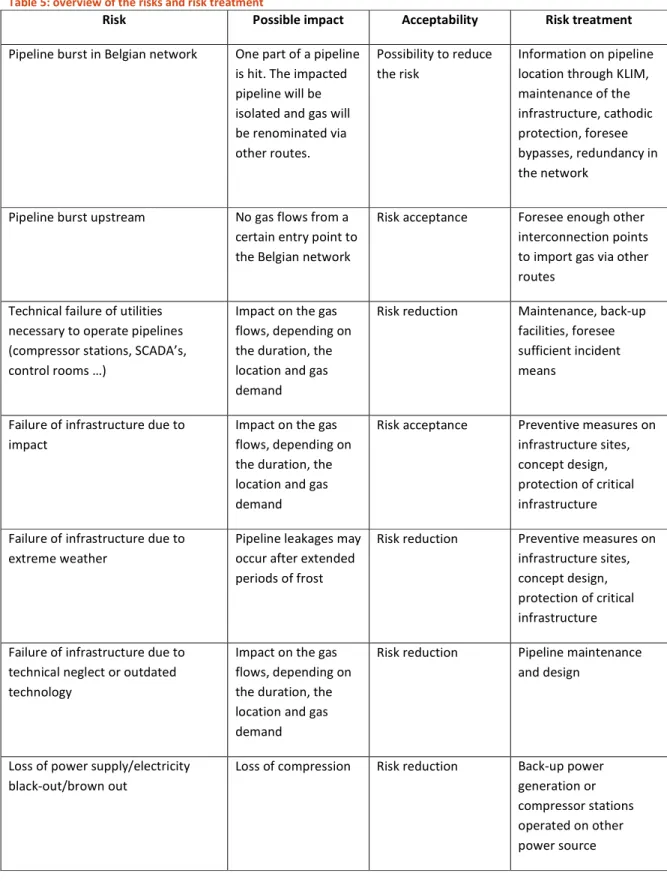

In table 5, for the considered risks, we give an overview of possible risk treatment. Possible market based and non-market based measures will be described in chapter 6.

Table 5: overview of the risks and risk treatment

Risk Possible impact Acceptability Risk treatment

Pipeline burst in Belgian network One part of a pipeline is hit. The impacted pipeline will be isolated and gas will be renominated via other routes.

Possibility to reduce the risk

Information on pipeline location through KLIM, maintenance of the infrastructure, cathodic protection, foresee bypasses, redundancy in the network

Pipeline burst upstream No gas flows from a certain entry point to the Belgian network

Risk acceptance Foresee enough other interconnection points to import gas via other routes

Technical failure of utilities necessary to operate pipelines (compressor stations, SCADA’s, control rooms …)

Impact on the gas flows, depending on the duration, the location and gas demand

Risk reduction Maintenance, back-up facilities, foresee sufficient incident means

Failure of infrastructure due to impact

Impact on the gas flows, depending on the duration, the location and gas demand

Risk acceptance Preventive measures on infrastructure sites, concept design, protection of critical infrastructure Failure of infrastructure due to

extreme weather

Pipeline leakages may occur after extended periods of frost

Risk reduction Preventive measures on infrastructure sites, concept design, protection of critical infrastructure Failure of infrastructure due to

technical neglect or outdated technology

Impact on the gas flows, depending on the duration, the location and gas demand

Risk reduction Pipeline maintenance and design

Loss of power supply/electricity black-out/brown out

Loss of compression Risk reduction Back-up power generation or compressor stations operated on other power source

Intentional sabotage Impact on the gas flows, depending on the incident, the duration, the location and gas demand

Risk reduction Protection of critical infrastructure

Virus/cyber attack Destabilisation of SCADA ‘Supervisory Control and Data Acquisition’

Risk reduction Computer Emergency Response Team (CERT)

Sudden gas peak demand (e.g. Due to cold wave)

Interruptions to end consumers

Risk reduction Introduction of supply standard Commercial disputes/supplier default Shortfall in gas supplies, interruptions to end consumers

Risk reduction Financial check through obtaining supply license

Strikes in gas sector Blockage of gas infrastructure, no staff for control room,…

Risk reduction Conclude minimum service agreements

Floods/landslides/earthquakes Damage to infrastructure

Risk reduction Preventive measures on infrastructure sites, concept design, protection of critical infrastructure

With respect to the risk of a loss of power supply/electricity black-out, a serie of preventive actions are taken by the Transmission System operator of Natural Gas, Fluxys Belgium, in collaboration with the Transmission System Operator of the Electricity Grid Elia, National Regulatory Authority CREG and the Belgian Energy Administration, in order to assess and minimise the impact of a loss of power supply/electricity:

• A black-start study has been conducted to assess the possibility and the conditions under which Fluxys Belgium can assist Elia in rebuilding the balance of the Electricity Transmission Grid by supplying a natural gas to black-start power plants.

• On the other hand, Fluxys Belgium provided a list of Installations to Elia together with priorities indicating their necessity for safeguarding the security of gas supply when load shedding is applied in the Electricity Transmission Grid

• Finally, Fluxys Belgium established an emergency plan specifically aimed at actions to be undertaken in case of an emergency situation in the Electricity Transmission Grid and invested in Back-up power generation.

Belgium has also participated during summer 2014 to the European study on the impact of a scarcity of natural gas coming from Russia and/or via the transit route through Ukraine during the winter 2014-2015 (the stress test scenario). The result of the stress test for Belgium indicates that the Fluxys Belgium TSO network is quite interconnected and supply sources quite are diversified.

3.4.

Diversification analysis

In above table, we mainly took into account the risks for gas supply on the Belgian national territory because we assume that upstream risks are out of our power to treat. The main remedy is to have well diversified supply routes.

Belgium has a well-diversified gas portfolio and supply network for H-gas that allows looking for alternative supplies in case of a supply disruption. We had already mentioned in the risk assessment that the suppliers no longer manage their portfolios according to the demand of the consumers in a specific country, but they keep rather EU-wide portfolios. On the one hand, this makes it very difficult to determine the supply portfolio destined for the Belgian market. On the other hand, it increases the flexibility of the suppliers to deal with an emergency somewhere in the European market. Mostly they have storage available in other countries and access to flexible contracts and more diversified supply routes. This means that renominations should also be easier to handle in case of an emergency.

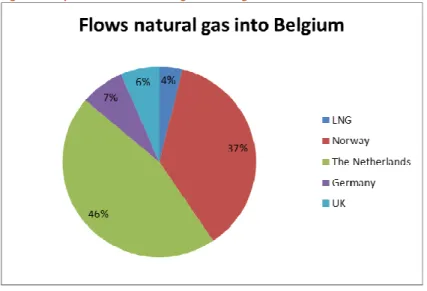

Figure 2: Physical flows of natural gas into Belgium in 2013

Source: FPS Economy

It is however necessary to keep in mind supplies can only be re-routed if the suppliers have access to upstream capacity to enter the gas in Belgium through another entry point or to make use of the secondary capacity market. The supplies of L-gas originate mainly from the Netherlands. The availability of L-gas on the market can normally be guaranteed because the Dutch system no longer makes a difference in the gas quality, the Dutch network transmission operator can convert H-gas into L-gas by ballasting it.

Natural gas can enter the country through a series of entry points on the natural gas transmission network. LNG supplies come mainly from Qatar by long-term contracts, via the Zeebrugge terminal and accounted for a share of 4% of the physical flows into Belgium in 2013 .

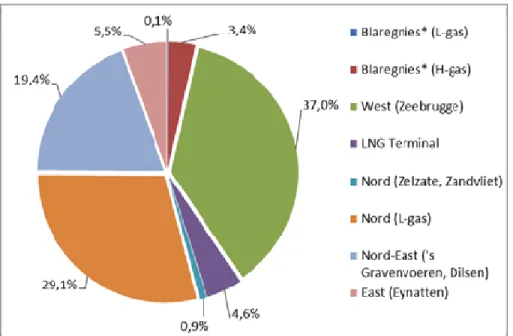

Natural gas customers who use L-gas are supplied directly from the Netherlands. Figure 3: Distribution of the entry volumes in 2013

Source: CREG; *The entry points of Blaregnies are opposite to the physical flows (reverse flows) by making use of the dominant transits on these points

In order to increase the flexibility of the system and to increase the security of supply, the TSO works with an Entry-Exit model. The main advantage for the security of supply (mainly for the H-gas network) of the Entry-Exit model is the increased flexibility that is introduced through:

• only one balancing point for H-gas (imbalances over the currently three H-gas balancing zones will automatically be re-distributed to create virtually one balancing zone) and one for L-gas on which intraday balancing will be applied;

• introduction of a virtual trading point for H-gas;

• free exchange of quantities of natural gas from any interconnection point within the Belgian system to any interconnection point or domestic exit point.

4.

Infrastructure & supply standard

4.1.

Infrastructure standard (N-1)

The N – 1 formula describes the ability of the technical capacity of the gas infrastructure to satisfy total gas demand in the calculated area in the event of disruption of the single largest gas infrastructure during a day of exceptionally high gas demand occurring with a statistical probability

of once in 20 years. Gas infrastructure includes the gas transmission network including interconnectors as well as production, LNG and storage facilities connected to the calculated area. The technical capacity of all remaining available gas infrastructure in the event of disruption of the single largest gas infrastructure should be at least equal to the sum of the total daily gas demand of the calculated area during a day of exceptionally high gas demand occurring with a statistical probability of once in 20 years.

In the risk assessment, we noted that transit flows to neighbouring countries are not taken into account for the calculation of the N-1 standard. Therefore, the N-1 calculation assumes that all the gas flows are destined for the Belgian domestic market. In practice, this is not the case. To take into account the gas flows for the neighbouring countries, it could be useful in the future to calculate the N-1 standard at regional level.

For Belgium, the N-1 calculation for the H-gas infrastructure gave a result of 172,34% in 2011 and 162,48% for 2015. This means that the full demand could be covered during a day of exceptionally high gas demand in the event of the disruption of the single largest gas infrastructure. The single largest gas infrastructure for Belgium is IZT, the interconnector between UK and BE. We refer to the risk assessment for the detailed calculation of the N-1 formula.

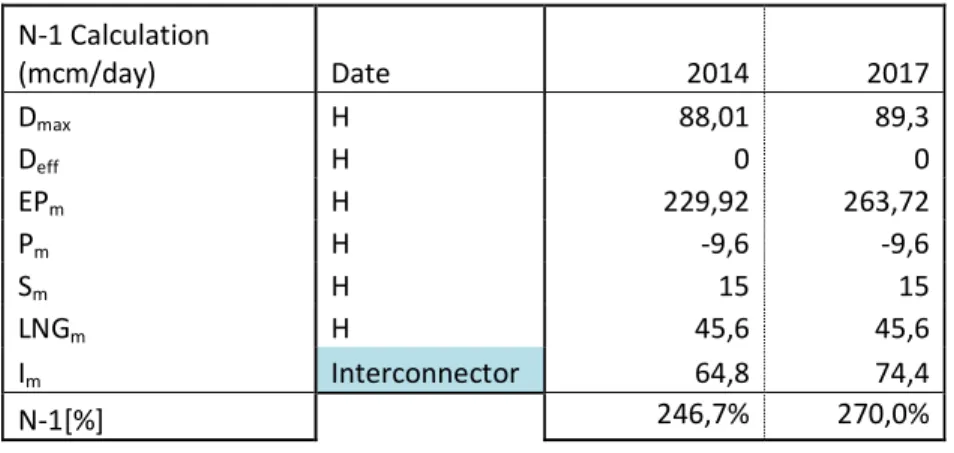

No demand side measures were taken into account for the calculation of the N-1. The table below gives an overview of the N-1 calculations up to 2020 bases on the capacity expansions in the investment plan of Fluxys Belgium (see also chapter 8). We took the most restrictive approach for this calculation, based on the minimum of the available capacity between the Fluxys Belgium network and the TSO network. We can state that even with the most restrictive approach, Belgium has sufficient capacity available to meet the N-1 criteria.

Table 6: Based on Fluxys capacity and loss of Interconnector pipeline

N-1 Calculation (mcm/day) Date 2014 2017 Dmax H 88,01 89,3 Deff H 0 0 EPm H 229,92 263,72 Pm H -9,6 -9,6 Sm H 15 15 LNGm H 45,6 45,6 Im Interconnector 64,8 74,4 N-1[%] 246,7% 270,0%

Table 7: Based on min(Fluxys, adjacent TSO) capacity and loss of Interconnector pipeline N-1 Calculation (mcm/day) Date 2014 2017 Dmax H 88,01 89,3 Deff H 0 0 Epm H 229,92 263,52 Pm H -8,64 -8,64 Sm H 15 15 LNGm H 45,6 45,6 Im Interconnector 63 63 N-1[%] 248,7% 282,7%

As from 2016, the new interconnection point at Alveringem will be added to our network (new pipeline from the LNG terminal in Dunkirk in France to Belgium).

4.2.

Supply standard

According to article 8 of the regulation, the gas undertakings have to be able to supply the protected customers of the Member State in the following cases:

- Extreme temperatures during a 7-day peak period occurring with a statistical probability of once in 20 years

- Any period of at least 30 days of exceptionally high gas demand, occurring with a statistical probability of once in 20 years

- For a period of at least 30 days in case of the disruption of the single largest gas infrastructure under average winter conditions

The gas undertakings that will need to live up to those standards are all gas undertakings that deliver gas to the distribution network.

In our risk analysis, we already tried to convert the above standards in more concrete criteria that can be applied and checked on a transparent basis. First of all we had to check what temperature profile corresponds to the 7 day peak period occurring with a statistical probability of once in 20 years. For this period we had identified the number of degree days and the equivalent temperature, based on historical data of the last 100 years. This way we can establish a profile that can be used to simulate gas demand.

Table 8: Degree days and equivalent temperature for the 7 day peak period occurring once in 20 years

begin end Degree Day/Equivalent temperatures Sum/mean 28/12/1996 3/01/1997 23,1 23,3 20,1 23,1 26,9 27,4 25,3 169,2 -6,6 -6,8 -3,6 -6,6 -10,4 -10,9 -8,8 -7,7 1/01/1979 7/01/1979 25,6 24,6 23,7 22,9 24,6 25,7 22,9 170,0 -9,1 -8,1 -7,2 -6,4 -8,1 -9,2 -6,4 -7,8 17/01/1963 23/01/1963 23,6 26,9 26,2 22,8 22,9 23,9 22,3 168,6 -7,1 -10,4 -9,7 -6,3 -6,4 -7,4 -5,8 -7,6 17/12/1946 23/12/1946 23,4 23,5 24 25,8 25,6 23,6 23,4 169,3 -6,9 -7 -7,5 -9,3 -9,1 -7,1 -6,9 -7,7 19/01/1940 25/01/1940 24,5 25,6 23,5 26,5 24,6 23,6 22,2 170,5 -8 -9,1 -7 -10 -8,1 -7,1 -5,7 -7,9 Average 24,0 24,8 23,5 24,2 24,9 24,8 23,2 169,5 -7,5 -8,3 -7,0 -7,7 -8,4 -8,3 -6,7 -7,7 Source: FPS Economy

For the 30 day period of peak demand, we obtained the following results for the degree days based on the historic data of the last 100 years:

Table 9: Average Degree Days (DD) per peak period and amount of DD with 5% risk

Consumption Slope 1 month 5 month

6

month 1 year due to 1 day 7 days 30 days

150 days 180 days 365 days Central

Heating (CH) Linear Varying

Average 100 years 21,2 133,0 466 1.734 1.913 2.325 in function of DD Peak 5% 100 years 26,8 169,6 594 2.037 2.325 2.650 Others than CH Constant 3,3 22,8 98 488 585 1.186 Total Average 100 years 24,5 155,8 564 2.222 2.498 3.511 Peak 5% 100 years 30,1 192,4 691 2.525 2.910 3.836 Source: FPS Economy

The volumes (energy in kWh) and the transport capacities (in m³(n)/h) corresponding to the supply standards are given in the following tables 10 and 11. The fact that in Belgium, two types of gas are distributed, leads to two values, one for the protected customers in the low calorific gas zone and one for the protected customers in the high calorific gas zone. These values were based on the gas year 2011-2012 and can be re-actualized with the last data available (transfer of costumers from the low calorific gas market to the high calorific gas market, growth on the distribution network,…). Due to the cold spell in gas year 2011-2012 these values however are quite representative for a winter colder than average.

For H and L gas we will apply respectively the conversion factor energy/volume of 11,3 KWh/m³ and 9,77 kWh/m³.

The following tables will included under chapter 4.2 (page 16) of the preventive action plan. Table 10: volumes (in TWh) corresponding to the supply standard

H (TWh) L (TWh)

7 days (5% climatic Risk) 2,95 2,83

30 days (5% climatic Risk) 10,87 10,30

30 days (50/50 climatic Risk) 9,14 8,56

Table 11: capacities (in m³(n)/h corresponding to the supply standard.

H (m³(n)/h) L (m³(n)/h)

7 days (5% climatic Risk) 1.866.921 2.067.237

30 days (5% climatic Risk) 1.602.603 1.757.885

30 days (50/50 climatic Risk) 1.347.949 1.459.843

To enforce the supply standard, the suppliers to the Belgian market will need to contract enough gas to meet those criteria for the 7 day peak demand, the 30 day peak demand and sufficient supplies through alternatives routes in case of a disruption of the largest gas infrastructure. As such a standard does no longer exist in Belgian national legislation, Belgium will introduce a new legal framework that obliges suppliers to foresee enough gas to supply the 7 day peak period.

In the past, the following criteria were applicable in the Belgian market:

1. A transport capacity covering the hourly peak demand of -11°Ceq (statistical risk of 1 in 20 years)

2. The gas volumes need to be able to cover the gas demand linked to the winter peak of 1962/1963, the coldest year in the century (statistical risk of 1 in 95 years)

3. A gas volume covering gas demand for a 5 day peak period between -10°Ceq and -11°Ceq (average temperature during the day measured at Uccle with a statistical risk of 1 in 95 years)

According to our calculations above, the peak winter peak value occurring once in 20 years is still -11°Ceq, we will opt to reintroduce these standards by law. The above criteria fall into two parts. The first part is the infrastructure obligations and the second part is the molecule obligation.

For the infrastructure calculations, the TSO still bases its calculations in the investment plan on the -11°Ceq hourly peak criterion. By introducing the same criteria for the shippers, both the molecule standards will be in line with our infrastructure standard. An improvement is already made through the introduction of the new entry-exit model. The TSO will calculate the needed capacity per aggregated receiving station (ARS) to cover the full demand distribution network behind that specific ARS at -11°Ceq. The shippers and suppliers will then be forced to book the capacity calculated by the TSO in order to cover the winter peak demand and to avoid free riding. This way, at least the capacity is already in place to cover the peak demand.

To solve the issue of the molecule obligation, the question remains how the government will monitor if the suppliers live up to the molecule standard. A possible option is to launch an annual winter information request on demand and supply portfolio of the suppliers. This information is

intended to assess the security of supply situation for the approaching winter. Requested information could amongst others include: the supplier‘s/ shipper‘s anticipated supply portfolio, including the source of contracted supply (e.g. National Balancing Point, Liquefied Natural Gas (LNG) imports and storage) demand information, including the volume of interruptible contracts and volume of demand that is not yet met by existing supply contracts.

Information on the supply-demand portfolio could be requested for various scenarios such as the 7 day peak demand, the 30 day exceptionally high demand and in case of the disruption of the single largest infrastructure. This way, suppliers could be asked to provide demand and supply information for the entire winter as a whole or for different periods in winter (e.g. September to November and December to February).

We would like to note that it is sometimes difficult to obtain data that can be aggregated consistently. Suppliers hold information in different formats and it has been difficult for some suppliers to provide the requested information in the required format. Given that contractual positions can change rapidly, there is also a question about the usefulness of such information. Furthermore, we will need to look at the consequences that can be imposed on shippers that cannot fulfil the supply standard, for example some sort of financial penalty.

A second option is to adjust the licence conditions. The licence condition could require suppliers to prove that they can meet demand under specified security of supply standards. If companies fail to prove compliance with these standards, then this would constitute a licence breach. This would be assessed ex-ante before an emergency occurs and would not affect company‘s behaviour in or immediately prior to an emergency. In general, a licence condition benefits from not favouring a particular source of demand or supply flexibility above others. However, supply solutions do implicitly deliver different types of flexibility in terms of response time and certainty of delivery. This might need to be taken into account when designing an ex-ante license condition. In this case, such an obligation may increase the number of long-term supply contracts, as a means of demonstrating compliance with the obligation, which could potentially dampen market innovation. There is a risk that relying on an ex-ante assessment could be somewhat ineffective since suppliers could rapidly change their contractual positions following compliance with the license condition.

An ex-post license condition could significantly reduce monitoring costs. In addition, given the potentially significant consequences associated with a license breach, we think that this requirement could be effective in ensuring suppliers take adequate measures to protect their firm customers. However, there are legal risks associated with this option as parties might disagree for example, on whether a supplier has used best endeavours to avoid a gas deficit.

In order to implement the above mentioned measures, a new legal framework to enforce the supply standard for identified consumers (based on the regulation 994/2010) has been drafted. The supply standard enforces suppliers to have enough natural gas in their portfolio to first of all cover the peak demand that will be set at an equivalent temperature of -11°Ceq of their identified customers connected to the distribution grid and this for a period of at least 7 days. Secondly, to cover a winter period of exceptional high natural gas demand and thirdly, to cover the natural gas demand of their

customers connected to the distribution network for a period of at least 30 days in case of a disruption of the single largest gas infrastructure.

The Administration will define a clear standard (e.g. the winter period could be defined by royal decree) for those thresholds and communicate them to the suppliers, but without being responsible if any natural gas disruption might still occur even if the suppliers all meet the standard.

Another option is to make the natural gas suppliers responsible if any shortage of natural gas (for identified consumers) occurs during a winter peak demand or if there is a disruption in single largest and only have an ex-post checks on the companies. This could however lead to serious discussions about which supplier is responsible afterwards.

A measure that is already in place to make sure suppliers deliver gas to Belgian end-users, is the daily market balancing regime. The Belgian TSO monitors the balance between entry and exit on a

cumulative basis for all hours of a given day and intervenes in order to keep the system balanced at all times.

Two kinds of interventions are possible: • Within day interventions

• End of day interventions

Within day interventions:

In case the market balancing position goes beyond the upper (or lower) market threshold, the Belgian TSO intervenes through a sale (or purchase) transaction on the commodity market.

• The considered volume is then settled in cash with the grid users (s) contributing to such imbalance in proportion of their individual contribution.

• Grid users are penalized by 10% of the Belgian TSO price for the settled volumes. End of day interventions:

At the end of the gas day, each grid user is returned to zero by a settlement in cash: • Grid users helping the system pay or paid the Belgian TSO price

• Imbalance causing grid users pay or paid the Belgian TSO price and pay an additional penalty of 10% price on their contribution to the market settlement exceeding the end of day market tolerance of +/- 2,5 GWh/d.

Conclusion

To conclude, there is no supply danger if a supplier doesn’t fulfill its contractual engagements related to its clients. In case of an imbalance of the market, the Belgian TSO will identify the supplier(s) that caused the imbalance and a penalty needs to be paid (depending on kind of intervention needed to balance system).

4.3.

Interruptible & protected customers

Energy end-users include residential and commercial customers as well as industrial firms and electric utilities. These customer groups have different energy requirements and thus quite different service needs. In the natural gas market, consumers can contract for either firm or interruptible service. Residential and small commercial customers such as households, schools, and hospitals use natural gas primarily for space and water heating and need reliable supply. Such customers require on demand service with no predetermined quantity restrictions, known as firm service. In contrast, larger commercial, industrial, and electric utility customers could have fuel switching or dual-fuel capabilities (which is rarely the case in Belgium) and could receive natural gas through a lower priority service known as interruptible service. In theory, energy supply reliability could be effectively handled at the customer level ability to switch quickly to an alternative fuel. Therefore, some countries distinguish between protected customers for whom most of the capacity offered is firm capacity. In Belgium, interruptible capacity is only offered if all the firm capacity is booked by the shippers.

4.3.1. End-users on the distribution network

The definition of protected customers in the regulation states that protected customers include all household customers connected to a gas distribution network and can also include small and medium sized enterprises and essential social services connected to the gas distribution network provided that these additional customers do not represent more than 20% of the final gas use. The regulation defines the protected customers as all household customers connected to a gas distribution network and may also include:

- small and medium-sized enterprises connected to the distribution network and essential social services connected to the gas distribution or transmission network if they do not represent more than 20% of the final gas use

- district heating installations to the extent that they deliver heating to household customers and to customers mentioned above provided that these installations are not able to switch to other fuels and that they are connected to the distribution or transmission network.

For Belgium the protected customers are defined as all customers connected to the distribution network. One of the reasons is that a selective shut off is not possible on the distribution network. Protected customers represent about 50% of the total gas demand. Most of this demand stems from household consumers. It might be useful to study (in consultation with the distribution network operators) if it could be possible for the tele-measured clients to reduce their consumption in case of an emergency.

Table 12 gives a detailed overview of the consumption profiles on the distribution network during the winter peak.

Table 12: Consumption profiles and their representation on the distribution network

2012-2013 S30 S31 S32 S41 S31+S32+S41

H 10,13% 12,63% 19,90% 57,34% 89,87%

L 13,34% 12,14% 19,62% 54,91% 86,67%

There are 4 consumption profiles on the distribution network: S30, S31, S32 and S41. The household customers are represented under category S41. Their consumption is heavily reliable on the outside temperature. The other three profiles dispose of a VAT number and correspond to the tertiary, commercial and industrial sector.

The profiles S31 and S32 are the non-telemeasured clients. S31 are the commercial clients that consume less than 150.000 KWh/year, S32 clients consume more than 150.000 KWh/year. The gas consumption of those clients is dependent on the outside temperature so they are close to household consumers. It is however not possible to get a more clearer explanation of the type of consumers under categories S31 and S32, under category S31 there are for example combined profiles with residential and business use, S32 consist mainly of a significant part of professional components that are influenced by a residential behavior for example hospitals, nursing homes,…

The profile S30 represents the telemeasured clients. Those are the larger clients with an hourly counting of the gas consumption (hospitals, administrative buildings, large supermarkets,…) connected to the distribution grid. We can see that the gas consumption of these consumers (except for the hospitals) is less dependent on the outside temperature. The consumption of those clients represents less than 20% of the total gas demand.

In category S30 and to a lesser extend in category S32 there are non-eligible consumers i.e. consumers which are not eligible in the definition contained in art. 2(1) of the Regulation.

First of all the impact is very limited due to the following reasons:

The Belgian transport network is a well-connected network and well-present in all the regions on the most strategic places. Because of this connectivity it is often possible to connect large industrial clients and power plants (about 250) directly to the transport network (transport pipeline is nearby the industrial plants). The costs to connect them to the transport network are not significantly greater than the total costs to connect them to the distribution grid. On other hands, it is economically more advantageous for an industrial customer to be connected to the transport network than the distributor network, as the costs for the first are far less important than those of the second, what still constitutes an incentive not to be connected to the distribution network. Only a very small part of the industrial clients is still connected to the distribution network.

• Added volume due to non-eligible customers on distribution network is also limited

When looking at the total gas consumption in Belgium, which is 183,2 TWh in 2013, protected customers (i.e. eligible in term of the definition contained in art. 2(1) of the Regulation 994/2010) on the distribution network will consume at least 79,23 TWh and the non-eligible customers less than 15,85 TWh. The total percentage of end-users on the distribution network that don’t comply with Article 2 of the Regulation is less than 8,65%.

Indeed, this 15,85 TWh has to be considered as an overestimated volume. This volume of energy contains the volume consumed by larger essential social services like hospitals and a small part of SMEs, which meets the definition of protected costumers. But due to the fact that there are referenced under category S30, there are considered as non-protected costumers in our calculation. We must also add that a small amount of industrial clients within the S32 and S30 categories have a contract that allows them to be interrupted in case of for example extreme cold weather2. This indicates that this percentage is definitely overestimated.

• The impossibility to fully dissociate on distribution network protected customer (cfr. art 8(1)) from non-eligible user (cfr. art 8(1)) due to technical reasons

S30 and the estimation of the remaining 1/4 of S32 (estimated number 2000 clients), connected to the distribution network, these clients should, based on our estimation, be considered as not compliant with the definition of protected costumers. The only relevant information available about the distribution today is related to the annual consumption of the customers on this network. In function of this information (annual consumption of the different categories), we have been able to estimate the volume and the number (but not identify) belonging in the different categories foreseen In the regulation (i.e. household customer, SME and others (Industries and large industries)). Due to the fact that those clients are not referenced in the database of the suppliers or the distribution network companies as SME’s or little, middle or large industrial clients, there can’t be individually identified as such (no bottom-up information (local or regional) but only through top-down information (federal)). Furthermore, usually, those non-eligible customers do not have their consumption monitored on an hourly basis. It can’t therefore be expected to control if they consume gas or not in case of curtailment situation. So for more than 80% of these customers, it isn’t possible

2

today to monitor the respect of the curtailment on the distribution network. Due to the above limitations, it is today not foreseen to curtail these categories of customers. Only 1000 of the remaining clients have today their consumption monitored hourly. As far as the monitoring is concerned, the situation could evolve in the future if the number of clients with tele-measured gas meter increases.

• No impact on compliant with art 8(2)

First of all, there is enough capacity available in Belgium on the transport network to permit the free flow of commodities. The transport capacity allows the gas undertakings to have an easy access to all neighboring trading places, to the LNG facilities in Zeebrugge and also direct access to producing counties (as NL and Norway). Even under extreme winter conditions3, the capacity needed to transport the gas will not be affected due to these increased volumes to some non-protected customers (cfr. art8(1)) on distribution network. The flow chart shows clearly that the transit from or to other EU countries through Belgium can be about 2-3 times higher than the correlated consumption of Belgian internal market.

Secondly, the probability that this extra volume allocated to non-protected users (cfr. art 8(1)) could have any impact one day is very very low.

Thirdly, even if this unlikely event would occur, a regional authority competent in Belgium for the distribution networks has foreseen a legal possibility to curtail (reduce) the consumption of some customers on the distribution network in case of absolute necessity or technical problems, and this, even if the technical instruments to control or monitor the respect of this kind of curtailment obligations are not always in place.

• Conclusion

Even if Belgium is not able to totally dissociate non eligible consumers relating to article 8(1) of the regulation on the distribution network, nevertheless, we are convinced that this increased supply of non-eligible customers does not have any relevant impact on the compliance with the regulation 994/2010.

4.3.2. End-users on the transport network

Contrary to the protected customers, the gas supply to industrial consumers connected to the Fluxys transport network could be interrupted. Historically, the infrastructure for transporting and delivering natural gas is designed and operated primarily to meet the need for firm service. Because the peak demand for natural gas tends to be seasonal, interruptible service contracts allow pipeline and distribution system operators to increase on of their fixed assets and better manage costs of service on average. These arrangements allow operators to maximize economic efficiency by meeting the needs of their committed firm service customers while providing delivery during off

3

peak periods to interruptible and seasonal customers. In the past, these arrangements provided opportunities for large-volume energy consumers such as industrial firms and electric generators to attain lower-cost energy supplies.

There are two kinds of interruptible contracts: 1. Supplier interruption:

Suppliers have the right to interrupt the customer, normally in return for a discount on price and with some notice in advance. The notice period will be specified in the energy contract. Most interruptible contracts specify that there will only be a few hours’ notice, unless it is specified otherwise in the contract. Customers with an interruptible contract have agreed to receive gas but are willing to have supply interrupted at some point, according to the reasons in the contract (mostly meteorological circumstances) and for a maximum amount of hours or days.

Interruptible contracts are more and more disappearing from the stage. This is due to the fact that the attributed discounts are no longer a sufficient incentive on the longer term. In the industrial sector, interruptible contracts account for less than 5% of the total contracted volumes between end users and suppliers. Interruptions are also limited to force majeure events. For the power plants, we also see a tendency towards more firm contracts (depends a lot on the supplier).

2. Transporter or border-to-border interruption:

The TSO has the right to interrupt supply (this is to interruptible contracted customers) in the network for operational reasons under normal circumstances. Again this will be covered in the transmission contract signed by the network user. Interruptible capacity is hardly booked by the shippers because Fluxys Belgium only offers interruptible capacity to the market if there is no firm capacity left. Even if Fluxys Belgium would offer interruptible capacity, the price difference between interruptible and firm capacity has become too small to be an incentive. Therefore we can say that interruptible capacity for the shippers is negligible in Belgium.

We have to be clear however that the above mentioned interruptions are separate to other interruption rights, which exist for use only in potential or actual emergency situations. In emergency situations, some companies can reduce demand considerably when prices are high or maintain production by switching to back-up fuels. However, they still need to maintain a certain level of gas to keep systems going and to let their plant safely shut down.

At any point an accident could damage a major part of the gas infrastructure and cut off supply. Some gas users have back-up systems and fuels to switch to in the event of an emergency or if commercial incentives make using an alternative fuel source preferable. Not every gas user has back up fuels (most of the end consumers in Belgium do not have back up fuels), so the gas system and the procedures that exist within it are designed to minimise the risk of gas being switched off from those who don’t expect it to be (those not on interruptible contracts). Appliances for commercial premises generally incorporate flame out safety devices. These allow for supplies to be quickly and safely reinstated following a cessation in gas supplies.

In the unlikely event of an emergency, the safe provision of gas to domestic users and other low volume users (all connected to the distribution network) is the top priority. Before firm customers are interrupted, emergency plans provide for the suspension of the normal market for gas. After the suspension, it will depend on how quickly gas supply and demand is balanced, before firm customers start to be interrupted. Before firm customers are interrupted, firm border-to-border transmission will be interrupted. Public appeals may take place asking the public to restrain gas usage but this would depend on the type of emergency.

4.4.

Stress test

As ask by the European Commission a stresstest was conducted to see if the Belgian gas network could cope with the 4 given scenarios:

• Disruption Ukrainian route for 1 month • Disruption Ukrainian route for 6 months

• Disruption of all Russian gas to Europe for 1 month • Disruption of all Russian gas to Europe during 5 months

4.4.1. N-x analyses

Different possible cases were calculated which could be possible on the Belgian network, also linked interruption scenarios were taken into account.

• Complete disruption of the Interconnector

• Complete disruption of the Eynatten 1 and 2 entry points • Complete disruption of the ‘s Gravenvoeren entry point

• Complete disruption of the Eynatten 1 and 2 entry points and the underground storage facility of Loenhout

• Complete disruption of the Eynatten 1 and 2 entry points and ‘s Gravenvoeren entry point • Complete disruption of the Eynatten 1 and 2 entry points and the Interconnector

• Complete disruption of the Eynatten 1 and 2 entry points, the Interconnector, the underground storage facility of Loenhout

Based on the N-x analyses it can be concluded that the entry capacity for the Belgian market is high enough to cover a complete disruption of Russian gas coming to Belgium.

4.4.2. Scenario analysis

In the scenario analysis which was made did not show an insurmountable problem on the Belgian gas supply during an average winter period. Based on the made assumptions there is always a solution to cover the Belgian gas supply. However the scenario left out the months of March and April which are (based on the climatic data of the last years), two cold months at the end of the winter period with a possible higher use of gas than the months of September and October.

4.4.3. Commodities analysis

The commodities analysis shows that 90% of the Belgian market is supplied by 6 players. The possibility exist that about 12% of the Belgian market is supplied by gas coming from Russia,

however because the supply contracts are not for one end-user market but also contract gas for other Member States, it is not possible to know what the real amount of Russian gas will be used to cover the needs of the Belgium customers. When the suppliers make use of a specific gas contract and for which market(s) is completely dependent on their decision on possible opportunities and needs.

In comparison of the last 3 years the underground storage facility of Loenhout was more filled and so more prepared for the winter period. The use of this storage facility is however completely market-based.

5.

Obligations imposed on natural gas undertakings and other relevant

bodies, including for the safe operation of the gas system

Next to the future supply standard, the PSO’s are the main imposed obligations in Belgium4. A second part of this chapter will focus on the safety policy of the TSO with regard to the quality and maintenance of the network.

5.1.

Public Service Obligations (PSO’s)

There is specific legislation related to public service obligations (PSOs). As required by the security of gas supply regulation, the legislation related to PSOs was communicated in February 2011 to the European Commission. Hereafter those PSOs are described.

5.1.1. National legislation

• Article 15/1 of the Gas Act (12/04/1965), modified by article 20 from the law of 01/06/2005: general obligation related to the responsibility of the exploitation and development of the gas installations

• Article 15/11,§1 of the Gas Act (12/04/1965), modified by article 109 (law of 22/12/2008) and article 5 (law of 27/02/2003) = PSO on the necessary investments (al.1°) and on both the regularity and quality of supplies (al. 2°)

• Royal Decree of 16/12/1999 giving a list of priority consumers in case of supply disruption

• Ministerial Decree of 23/10/2002 related to PSOs in the gas market = implementing decree

for already mentioned article 15/11, §1, al.1° (Gas Act of 12/04/1965) and indicating specific cases where supply disruption is authorized

• Article 1 of the Gas Act (12/04/1965), modified by article 2 from the law of 11/6/2011: Law to amend the Act of 12 April 1965 on the transport of gaseous and other products by pipeline

• Article 1,2 ,15/13 of the Gas Act (12/04/1965), respectively modified by article 55, 56, 86 from the law of 08/01/2012: Law to amend the Act of 29 April 1999 on the organization of the electricity market and the Act of 12 April 1965 on the transport of gaseous and other products by pipeline

• Ministerial Decree of 18/12/2013 establishing the federal emergency plan for natural gas supply

4

5.1.2. Regional legislation (distribution network)

• The Flemish « Energy Decree » on energy policy (08/05/2009) concerning i.e. the DSO’s responsibilities (art. 4.1.6) and Public Service Obligations imposed to DSO’s & suppliers (art. 4.1.16, 4.1.19, 4.1.20, 4.1.22, 6.1.1, 6.1.2., 7.5.1)

• The Flemish « Act » on energy policy (19/11/2010) concerning the organisation of the gas market including Public Service Obligations (several articles under Title III)

• The Flemish «Technical Regulation Gas Distribution» by Ministerial Decree (21/01/2010) concerning Planning Code (Chapter II)

• The Walloon « Decree » on gas market (19/12/2002) concerning i.e. the DSO’s

responsibilities (art. 12) and the Public Service Obligations imposed to DSO’s & suppliers (art. 32-33)

• The Walloon « Decree » on gas market (19/12/2002) concerning i.e. the DSO ‘s Investments

Plan called Adaptation Plan (art.16) aiming to ensure the continuity of supply, the safety, the development and the extension of the network

• The Brussels « Ordonnance » on gas market (01/04/2004, modified by Ord. 14-12-2006 and

by Ord. 20-07-2011) concerning i.e. the DSO’s responsibilities and tasks (art. 5) and the Public Service Obligations imposed to DSO’s & suppliers (art. 18)

• The Brussels « Ordonnance » on gas market (01/04/2004, modified by Ord. 14/12/2006 and

by Ord. 20-07-2011) concerning i.e. the DSO ‘s Investments Plan (art. 10) aiming to the continuity and the security of supply

5.2.

Quality & level of maintenance of the network

Fluxys Belgium, the TSO, is responsible for the quality and the maintenance of the network.

One of the main concerns is the quality and reliability of its network. A lot of the attention goes to the choice of materials. The high-pressure pipelines are made of the highest quality steel and meet all applicable European and international standards. The pipes undergo stringent quality-control procedures at the factory and these procedures are overseen by a recognised independent inspection body. The pipes also have a synthetic coating system and are fitted with a cathodic protection system to prevent external corrosion.

Also, a tracking system that monitors the quality and reliability of operation of its transportation network and transportation services has been developed. The report of this tracking system takes into account the situations in which subscribed transportation services were interrupted or reduced. During 2013 neither reductions nor interruptions of firm services were observed.

The maintenance periods are planned in consultation with adjacent TSO’s and customers connected to the transmission network. The work and intervention overview published on the Fluxys Belgium website lists the works and interventions planned for the current year that could affect the execution of the transmission contracts. The overview is updated each month for the current calendar year.

Internal Line Inspections (‘ILI’ also called I-pigging) have been performed for several years. The targeted frequency is an inspection of each line every 7 to 10 years. Pigging results, when validated, can lead to requests to further physically inspect the condition of the pipeline. These examination works are performed with a priority depending on the type of issue discovered during the I-pigging run.

All lines are not accessible Internal Line Inspections for various reasons (geometry of the line, gas flow, presence of pig traps,…): At the moment 75 % of the Belgian high pressure network is “piggable”. The Belgian TSO is conducting a program to improve this ratio, at the same time that research en development is running to develop other methodologies of inspection in order to cover 100% of the network. The maintenance of the network is supported by a centralized management system (SAP Plant Maintenance) and is based on Plants Orders generated by this system. Different tasks are performed to ensure the maintenance and the monitoring (preventive maintenance) of the network. Pipelines are scraped (pigging) systematically in a defined interval (cleaning of the pipe, scraping and rinsing, any repairs). Area lines are perpetually maintained (pruning, weeding) and the special points (air passages, pipelines in rivers) are subject to appropriate supervision (bridges, diving).

Patrols by helicopter flights are performed on the main sections on a regular basis (daily for mains pipelines to 2x a week or fortnight for the entire network). Moreover, this air surveillance is supplemented by patrols by car (1x per month for pipelines) and foot patrols throughout the network (1x per year).

Point measurements of predetermined gases are also conducted as part of these patrols: during the helicopter flights with the CHARM-system (unique system equipped by only one helicopter in Germany and leased by Fluxys Belgium) and during the pedestrian supervision.

Finally, monitoring of third-party works (work sites nearby high pressure pipelines) is performed during these different interventions and tends to be even sharper, thanks to new technologies in place or planned (detecting work by optical fiber and shock on a pipeline detection via the ThreatScan system).

One of the challenges is the replacement of the aging gas infrastructure where necessary. Fluxys Belgium is currently looking into some replacement investments between Poppel and Blaregnies where part of the pipelines will be replaced on the section after Weelde in 2014-2015.

6.

Overview preventive measures

In this chapter, we will make an evaluation of the possible measures (supply side & demand side) and attempt to assess the most efficient means that can be used to reduce the impact of an incident. We will discuss each measure separately. For each of the measures we will check if they are already applied in Belgium, what the potential impact is of the measure, what the potential costs are to apply it, if the measure could be carried out and supported by the gas sector and what actions would be necessary to execute the measure in Belgium. In Annex 1, we will provide a table with an overview of the most important comments per supply side market based measure. In Annex 2, the same is done for the demand side market based measures.