The Russian Offshore

Software Development

Table of contents

PREFACE...5

DISCLAIMER... 6

OFFSHORE SOFTWARE OUTSOURCING IN RUSSIA: AN EXECUTIVE SUMMARY. 7

THE RUSSIAN OFFSHORE SOFTWARE DEVELOPMENT INDUSTRY SURVEY ... 10

INTRODUCTION... 10

1. ORGANIZATIONAL STATUS OF COMPANIES... 10

2. COMPANIES’ FIELDS OF ACTIVITIES... 10

3. SIZE OF COMPANIES... 11

4. AVERAGE ANNUAL REVENUE OF COMPANIES... 11

5. AVERAGE SALARY, GROWTH ESTIMATION AND MARKET’S SIZE ESTIMATION. «GRAY» TEAMS. ... 13

6. AREAS OF SPECIALIZATION... 13

7. REPRESENTATIVE OFFICES: LOCATION AND STATUS... 16

8. CLIENTS’ BUSINESS... 19

9. GEOGRAPHICAL MARKETS... 19

10. RUSSIAN VENDORS: INDEX OF CITATION... 22

11. KEY TRENDS OF THE RUSSIAN OFFSHORE DEVELOPMENT MARKET... 22

12. MAIN PRIORITIES IN THE DEVELOPMENT OF COMPANIES... 22

13. SOFTWARE DEVELOPMENT PROCESS CERTIFICATION... 22

14. IT-ASSOCIATIONS... 23

OUTSOURCING TO RUSSIA: HOW TO... 24

CAPABILITY AND MATURITY: MORE THAN JUST DEVELOPMENT ISSUES... 24

SHAPING YOUR AGREEMENT: TEN STEPS TO HELP YOU STEER CLEAR OF TRAPS AND TROUBLE... 26

RISK MANAGEMENT IN PROJECTS: 17 STEPS TO SUCCESS... 28

OVERVIEW LEGAL FRAMEWORK FOR ACTIVITIES IN THE SPHERE OF INFORMATION TECHNOLOGIES IN THE RUSSIAN FEDERATION... 31

SOFTWARE PROTECTION IN RUSSIA... 36

BUSINESS DIRECTORY... 40

APLANA SOFTWARE... 40 ARCADIA, INC. ... 42 ARTEZIO, INC. ... 45 ATAPY SOFTWARE... 46 AURIGA, INC... 47DAROUT SERVICE CORP. LTD. ... 49

ECTACO-RUSSIA, LTD... 51 EPAM SYSTEMS... 52 EVELOPERS CORPORATION... 53 FORS... 54 HITSOFT... 56 JENSEN TECHNOLOGIES... 57 JS RCOM ... 58 “J-SOFT” JSC ... 59 KANAR SOFTWARE... 60

TERRALINK... 82

V6 TECHNOLOGIES... 83

VESTED DEVELOPMENT, INC. ... 85

CONTRIBUTORS AND SPONSORS ... 86

OUTSOURCING-RUSSIA.COM... 86

BEITEN BURKHARDT GOERDELER RECHTSANWALTSGESELLSCHAFT MBH ... 86

BROOKE NICOLE CONSULTANCY, INC. ... 86

INFORUS ... 87

Preface

Dear reader,

Thank you for your interest in the Russian offshore software development industry.

We’ve done our best to present this unique, three-in-one report containing the most up-to-date information regarding Russian capabilities in offshore outsourcing. We also believe that the included guidelines will be valuable in your search for an outsourcing vendor, as well as a useful Business Directory of major Russian providers. This report was especially intended to help small and midsize companies, with no prior experience in outsourcing, to find a suitable software development partner in Russia and to avoid the most common problems.

We at Outsourcing-Russia.com are devoted to helping the young, but quickly developing outsourcing industry in Russia to realize its great potential. I want to personally thank all those who share our vision and who contributed to this report. We also want to thank all the respondents who took part in the survey. Please feel free to contact Outsourcing-Russia.com in case you need further in-depth knowledge of the Russian software development industry or assistance in finding a reliable partner in Russia.

Best regards Alexey Filimonov

Editor, Outsourcing-Russia.com [email protected]

Disclaimer

Please be informed, that all of the information contained in this survey (except the Directory) is owned by Outsourcing-Russia.com and its Contributors and is protected by Russian and international copyright laws. Any reproduction or republication of all or part of this survey has to remain intact and include a notice on the copyright of Outsourcing-Russia.com or the Contributors, as applicable.

While the information of this survey has been presented with all due care, Outsourcing-Russia.com does not warrant the accuracy, completeness, usefulness and truth of survey’s information, links and logos derived from third parties. Outsourcing-Russia.com is not liable for any loss or damage occurring from the use of survey.

Offshore Software Outsourcing in Russia: An Executive Summary

The offshore software outsourcing industry in Russia has recently enjoyed a surge in interest and activity. There are more than 10,000 professional programmers in the industry in Russia, and recent estimations (particularly from Market Visio/EDC) put annual revenue at $150-200 million per year, with 50% annual growth.

At least a dozen major international companies have established offshore development centres in Russia. These include Motorola, Intel, Sun, Boeing, LG, Lucent and Nortel.

Russia has more personnel working in R&D than any other country in the world and ranks 3rd in the number of scientists and engineers per capita. Other advantages are competitive labour costs, proximity to Western Europe and good transportation links to the USA, a shared European culture and history that facilitates cross-cultural understanding (Source: “A Whitepaper on Offshore Software Development in Russia” from the American Chamber of Commerce in Russia).

The Russian offshore software outsourcing industry comes of age

The Russian offshore software outsourcing industry is 10+ years old and three major centres have emerged: Moscow, St. Petersburg, and Novosibirsk. Moscow State University, St. Petersburg State University, and Novosibirsk State University are, respectively, the top sources of programmers for each centre. There are also a smaller number of software development providers in Nizhny Novgorod, Yekaterinburg, Sarov, and Perm.

Russia is a rapidly growing offshore source for software development. Currently, more than 150 Russia-based companies are active in offshore software development. Labour costs are moderate and vary from $10 to $40 per developer’s hour depending on required skills and project size. The major software development centres have adequate telecommunications infrastructures.

The leading Russia-based software companies have 150+ permanent staff, established quality systems and are building their presence in the USA and Western Europe by opening sales and marketing branches.

A number of U.S. companies have set up development centres in Russia, and have reported excellent results.

According to the Whitepaper on Offshore Software Development in Russia, these include:

Intel, which started in 1993 by contracting with 10 programmers, now has its own facilities and a team of approximately 200 software developers in N.Novgorod, with announced plans to expand to 500.

Motorola, which started in 1993 with a small group of programmers, now has 200+ software engineers working as part of its global software manufacturing facilities in St.-Petersburg. This Motorola centre has recently achieved CMM Level 5 status.

Sun Microsystems, which has been active in Russia since 1989, now has a “Sparc Technology” centre with approximately 300 programmers through a partnership. These programmers are involved in the development of new software and worldwide support of existing products.

Other well-known companies developing software in Russia include IBM, Boeing, LG, Lucent and Nortel, as well as hundreds of less famous but large software and technology companies.

The advantages of Russia as an outsourcing partner

Availability of resources. It is no secret that a unique set of factors enabled Russia to make remarkable technological achievements in the heyday of the Soviet Union, starting with Sputnik. The Cold War rivalries fed more than 40 years of massive government-sponsored scientific initiatives at the country’s already highly developed academic establishment. Innovation and determined problem solving were at a premium.

In the decade following the Soviet era, Russia has experienced a decline in its capacity to harness talent as it did in the past. With the opening of borders, emigration led to a short-lived brain drain and the weakened economy during transition to the market could not support R&D generally at former levels. However, Russia not only retains vast pools of untapped technical resources, but also continues to produce large numbers of highly skilled graduates educated in the proud academic tradition from Soviet times. With new economic expansion, Russia’s fledgling IT sector is now attracting meaningful public and private support.

The World Bank estimates that Russia has more than 1 million technically trained personnel, more than the U.S., China or Japan, and three times as many as India. The ratio of researchers to the number of total inhabitants in Russia is 3,801 per million, less than Japan (4,909) to be sure, but greater than the United States (3698), Europe (2476), China (454), and India (151). (Source: “Russia: Offshore Software Development “Diamond in the Rough”, PWI, Inc).

According to surveys by Microsoft Research, within the last seven years 1.3 million people graduated from Russian universities with the skills to work in the IT industry. But only 70,000 actually work in IT companies in Russia, and only 8,000-10,000 is working within the offshore software industry.

Outsourcing-Russia.com, a portal devoted to outsourcing of software development to Russia, estimates that the total number of IT-related specialists who graduate each year from Moscow universities alone is approximately 5,000-5,500 and that Moscow universities produce an additional 16,000-18,000 annual graduates in various engineering fields that are also available for employment as programmers.

Costs. Although it is recommended to look beyond the low cost of Russian IT resources to the additional arguments in their favour, cost factors are undeniably a key consideration in any company's decisions around outsourcing.

Pricing of software development depends on a set of factors: needed skills, project size, commercial renown of the provider, the geographical location and experience of a provider, the provider's order book, and various fixed overheads whether included in the base price or not, the specific type of contract under negotiation (development or maintenance), ratio of onsite to offsite work, guaranteed workload and other factors. Accordingly hourly rates may vary from as low as $10 (in rare cases) to $40 and even $50. Testers and quality assurance personnel typically cost 20-30% less, and project managers 50-100% and even 150% more. Key personnel, if the client insists on a certain candidate, can cost up to 2 times more.

Technical excellence. Russian programmers possess all the needed up-to-date technical skills, as well as those needed for legacy migration. Within Russia all the latest worldwide technical literature is available both in English and in localized versions. Over recent years Russian student and school programming teams have consistently beaten their competitors from all over the world in closely watched international competitions.

Local providers understand the meaning of keeping abreast of all developments in the field and take the requisite preparatory steps: they organize specialized technical libraries and invite leading specialist to give special lectures on the latest trends and technologies. In addition, there are a number of certification centres from Sun, Microsoft, and Novell as a well as independent authorities.

R&D focus. Russian companies have a strong advantage in R&D and in software development that requires creativity plus additional skills in scientific domains. Esther Dyson, the widely recognized authority on technology stated to the New York Times in 2001 that, “Many Russian programmers are not mere programmers; they are mathematicians and scientists who turned to software to make a living…they excel at (solving) complex, large-scale technical problems. They don't simply want to follow directions; they want to be creative. The idea is that they can be very creative at solving tough problems, so their customers can put those solutions to practical use.”

European culture. Whatever else one may say about Russia, geography and centuries long tradition place it firmly in Europe. Today's young and middle age managers and specialists who work in hi-tech companies have the same or higher level of education, English language skills and motivation as their European colleagues.

Location. Although Russia is a vast country, major development centres are situated in the European region - St.-Petersburg, Moscow, N.Novgorod. It takes 3 hours to fly from Paris or Berlin and 8 hours from the USA to reach Moscow or St.-Petersburg. Russian offshore software development companies normally compensate for the time difference with their European and even American clientele by adjusting their working schedules so as to have maximal overlapping hours for mutual contact.

Political & economic situation in Russia

Russia’s economic and political climate has stabilized and improved during President Vladimir Putin’s first term in office. Putin enjoys popular support in his domestic constituency as well as an increasing respect in the international community. Russia’s debt and credit ratings are improving. Standard & Poor's has recently revised the outlooks on the ratings on the Russian cities of Moscow and St. Petersburg to positive from stable and affirmed its BB long-term credit and debt ratings on the two cities. Major legislative, regulatory and legal reforms planned and/or underway as well as rapid adoption of international accounting standards suggest stronger prospects for continued improvement of Russia’s economy, international standing and general business climate.

Political and legislative changes are beginning to exert a positive influence on the Russian offshore software development industry. The Russian government is planning to introduce tax privileges for software developers and IT specialists. Other programs including incubators to train new entrepreneurs and cooperative research programs such as the Russian Ministry for Economic Development’s $2.6 billion Electronic Russia Program are taking shape. There is a growing understanding of the role the industry should play in a modern Russian economy. The authorities, media, industry and academic communities now agree that offshore software outsourcing is one of the markets where Russia must be competitive.

The Russian Offshore Software Development Industry Survey

Introduction

Thirty-one companies from Moscow, Saint-Petersburg, Nizhni Novgorod, Novosibirsk, Samara, Taganrog and Voronezh took part in this survey of the Russian offshore software development industry, including all the major market players.

1. Organizational Status of Companies

The status of the majority of the companies (80,6%) is as an independent Russian legal entity, while 19,4% of the respondents are development centers of international companies.

Diagram 1. Organizational Status of Companies, % of Companies

% 8 0 ,6 1 9 ,4 0 2 0 4 0 6 0 8 0 1 0 0 R u s s ia n c o m p a n y R u s s ia n d e v e lo p m e n t c e n te r o f in te rn a tio n a l c o m p a n y

2. Companies’ Fields of Activities

All the respondents are involved in software development and maintenance. Almost half of them are also engaged in the development of their own products. System integration is one of the fields of activity for 42% of respondents.

Diagram 2. Companies’ Fields of Activity, % of Companies 1 0 0 4 2 4 2 0 2 0 4 0 6 0 8 0 1 0 0 S o f t w a r e d e v e l o p m e n t a n d m a i n t e n a n c e P r o d u c t s d e v e l o p m e n t I T - c o n s u l t i n g a n d s y s t e m i n t e g r a t i o n %

3. Size of Companies

Diagram 3.1 Companies’ Average Size Diagram 3.2 Percent of Companies Depending on Age

Number of employees 31 96 202 0 50 100 150 200 250

under 3 years 4-6 years 7+ years

38,7 16,1 45,2 under 3 years 4-6 years 7+ years %

As one would expect there is a dependency between the age and size of companies. For example, the average size of 7+ year old companies is 202 persons, while for the majority of the young companies the average number of employees is 31 persons. The overall average size of all companies, that took part in survey, is 110 persons. Usually, the size of an offshore department composes 80% of the entire company. At the present time Russia’s capital, Moscow, has the largest “human” potential – more then 50% of the total number of employees work in the capital of Russia. Saint-Petersburg accounts for about 25% of the labor force.

4. Average Annual Revenue of Companies

27 (of 31) respondents have disclosed their annual revenue range. As it follows from the diagram 4.1, the annual revenue of 15% of these companies lies between $2m and $4m. 30% of providers have an annual revenue that is more then $4m. One should note that the most of these companies have been working within the global outsourcing market for more than 7 years. The annual revenue of the majority of the young companies does not exceed $2m.

Diagram 4.1 Average Annual Revenue, % of Companies

26% 29% 15% 30% under $0,5m $0,5m - $2m $2m - $4m $4m and more

Diagram 4.2 Annual Revenue and Geographical Location, % of Companies 7,7 16,7 62,5 30,7 50 12,5 15,4 33,3 46,2 25 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Moscow St. Petersburg Regions under $0,5m $0,5m - $2m $2m - $4m $4m and more n=8 n=6 n=13

Diagram 4.3 Geographical Distribution of Companies Depending on Annual Revenue, % of Companies

14,2 50 50 75 14,2 37,5 50 71,6 12,5 25 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% under $0,5m $0,5m - $2 m $2m - $4 m $4 m and more Moscow St. Petersburg Regions n=6 n=4 n=8 n=7

5. Average Salary, Growth Estimation and Market’s Size Estimation. «Gray»

Teams.

In this survey we have also studied average minimum and maximum monthly salary of employees. For specialists employed in programming it ranges from $380 to $1200, for managers, including project-managers, from $700 to $1900. In general, salaries are higher in Moscow in comparison with other cities. But due to the fact that the top companies are from Saint-Petersburg, Novosibirsk and Nizhni Novgorod this difference is not so significant.

Despite a world economic recession Russian providers look to the future quite optimistically and estimate their growth on average at 64% in two years. Taking into consideration the average estimation for offshore software development market, given by respondents at $187m, and average companies’ growth, by 2004 the market is expected to grow up to $306m. This result more or less corresponds with the one predicted in the recent Market-Visio/EDC’s research “IT SERVICES AND OUTSOURCING IN RUSSIA - 2002”. The companies have estimated average size of “gray” offshore outsourcing market in Russia at 40%. One should note that some respondents consider the decrease of “gray” teams’ share as one of the key trends of the market.

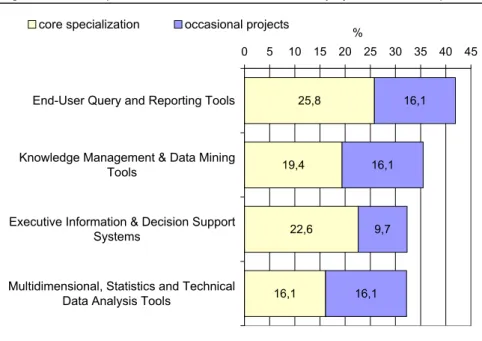

6. Areas of Specialization

Diagram 5.1. Core Specialization of Russian Providers

% of Com panies 51,6 45,2 38,7 35,5 29 25,8 0 15 30 45 60 Enterprise Resource Management Applications Electronic Com merce Content and Docum ent Management Applications Information and Data Management Software Information Access and Delivery Networking Software

As seen on the diagram 5.1, the majority of Russian providers have strong experience in development of various types of Enterprise Resource Management Applications,particularly 35,5% of vendors provide development of Services Industry Applications, including Banking/Finance Applications (25,8%) and Telecommunications/Utilities Applications (25,8%), Customer Relationship Management Systems (29%), Sales Applications (22,6%) and Project Management Applications (19,4%).

If you take into consideration those fields of expertise where vendors have had at least occasional projects, then the picture is as shown in the diagram 5.2. A detailed description of the main fields of specialization is shown on the diagrams 5.3-5.6.

Diagram 5.2. Fields of Expertise Where Vendors Have Had at Least Occasional Projects, % of Companies % 51,6 38,7 45,2 35,5 25,8 9,7 29 22,6 12,9 6,5 16,1 19,2 12,9 16,1 32,3 38,7 29 19,4 25,8 41,9 19,4 22,6 29 32,3 22,6 19,4 25,5 22,1 0 10 20 30 40 50 60 70 80 90

Enterprise Resource Management Applications Content and Document Management Applications Electronic Commerce Information and Data Management Software Networking Software Office Applications Information Access and Delivery Systems Middleware Collaborative & Messaging Applications Home Education/ Entertainment Software Speech and Natural Language Applications Application Design and Development Tools System Management Software Network Management Software

core specialization occasional projects

Diagram 5.3. Development of Enterprise Resource Management Applications, % of Companies

19,4 29 22,6 12,9 16,1 12,9 25,8 25,8 12,9 6,5 6,5 6,5 6,5 51,6 35,5 38,7 38,7 35,5 38,7 25,8 22,6 35,5 35,5 38,7 35,5 29 29 29 3,2 3,2 0 20 40 60 80

Project Management Applications Customer-Relationship Management Applications

Sales Applications Marketing Applications

Customer-Support and Contact-Center Software

Human Resource Management and Payroll Applications Banking/Finance Applications

Telecommunications/Utilities Applications Warehouse management systems Product Supply Chain Applications

Wholesale Distribution Applications

Logistics Applications Retail Applications

Accounting Applications Materials Management Applications

Diagram 5.4. Development of Software for Electronic Commerce, % of Companies 6,5 22,6 9,7 12,9 38,7 35,5 38,7 22,6 35,5 35,5 22,6 32,3 0 10 20 30 40 50 60 70

Retail/Point of Sale Applications Electronic Catalog Applications Electronic Marketplaces Software Online Community Software Web Content Management and

Publishing systems Websites (design and development)

% core specialization occasional projects

Diagram 5.5. Development of Information and Data Management Software, % of Companies

1 9 ,4 2 5 ,8 2 5 ,8 2 5 ,8 1 6 ,1 1 2 ,9 0 1 0 2 0 3 0 4 0 5 0 D a ta b a s e A d m in is tra tio n T o o ls a n d U tilitie s D a ta b a s e D a ta M o ve m e n t a n d R e p lic a tio n T o o ls D B M S s % c o re s p e c ia liz a tio n o c c a s io n a l p ro je c ts

Diagram 5.6. Development of Information Access and Delivery Systems, % of Companies

25,8 16,1

0 5 10 15 20 25 30 35 40 45

End-User Query and Reporting Tools

Knowledge Management & Data Mining

%

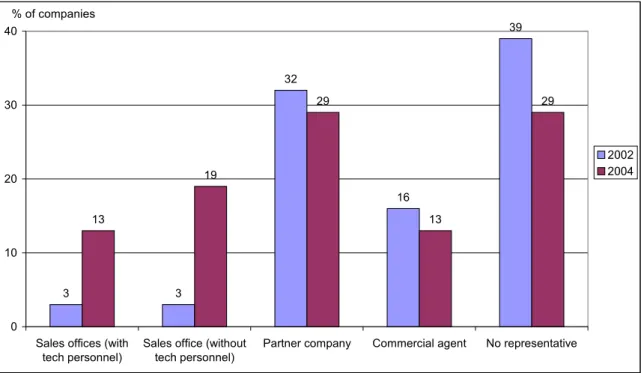

7. Representative Offices: Location and Status

An analysis of the diagrams 6.1-6.7 reveals certain trends in geography and status of the current and planned representative offices of Russian providers.

Diagram 6.1. Total Amount of Representative Offices

8 10 35 29 2 21 20 29 1 38 0 5 10 15 20 25 30 35 40

Sales office (with tech personnel)

Sales office (without tech personnel)

Partner company Commercial agent No representative

2002 2004

The diagram 6.1 shows the total amount of current and planned representative offices. As seen on the diagram, companies strive to become closer to their customers by opening sales and support offices in their target markets. This trend has also been noted as one of the key market tendencies by more than a third of the respondents.

Diagram 6.2. USA and Canada

19 13 35 19 26 39 10 39 26 7 0 5 10 15 20 25 30 35 40 45

Sales office (with tech personnel)

Sales office (without tech personnel)

Partner company Commercial agent No representative

2002 2004 % of companies

By 2004 the number of sales offices (with tech personnel) in USA and Canada is expected to increase by 90%. No wonder since the USA is the key market for a majority of Russian providers.

Diagram 6.3. Germany, Austria and Switzerland 3 3 32 16 39 13 19 29 13 29 0 10 20 30 40

Sales offices (with tech personnel)

Sales office (without tech personnel)

Partner company Commercial agent No representative

2002 2004 % of companies

A relatively high growth of the number of European sales offices and no substantial changes in the number of partner companies means that Russian providers plan to intensify direct sales to end-customers. Diagram 6.4. Scandinavia 0 0 13 13 65 3 13 23 19 35 0 10 20 30 40 50 60 70

Sales offices (with tech personnel)

Sales offices (without tech

Partner company Commercial agent No representative

2002 2004 % of companies

Diagram 6.5. Other Western European Countries 0 6 26 29 35 3 16 26 19 26 0 5 10 15 20 25 30 35 40

Sales office (with tech personnel)

Sales office (without tech personnel)

Partner company Commercial agent No representative

2002 2004 % of companies

Diagram 6.6. Southeast Asia

0 6 6 10 65 6 3 6 10 55 0 10 20 30 40 50 60 70

Sales office (with tech personnel)

Sales office (without tech personnel)

Partner company Commercial agent No representative

2002 2004 % of companies

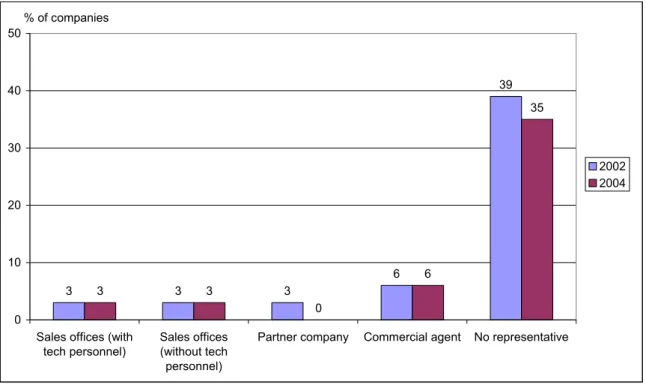

Few Russian companies keep in touch with countries from Southeast Asia, Israel and other regions. No remarkable changes are expected in these regions.

Diagram 6.7. Other Countries 3 3 3 6 39 3 3 0 6 35 0 10 20 30 40 50

Sales offices (with tech personnel)

Sales offices (without tech personnel)

Partner company Commercial agent No representative

2002 2004 % of companies

8. Clients’ Business

As it is shown in the diagram below, Russian vendors are used to work mostly with IT-related companies. Diagram 7. Clients’ Business

IT-consulting 15% Software development 50% Non IT 26% Other IT 9%

Diagram 8.1. USA and Canada 71 13 74 3 16 16 0 10 20 30 40 50 60 70 80

key market occasional projects no projects

2002 2004 % of companies

Diagram 8.2. Germany, Austria and Switzerland

16 52 23 29 10 48 0 10 20 30 40 50 60

key market occasional projects no projects

2002 2004 % of companies

The diagrams 8.2-8.4 show that in the near future more and more vendors will consider Europe as a key market. The number of vendors without clients in Europe may decrease to half.

Diagram 8.3. Scandinavia 6 26 52 13 42 19 0 10 20 30 40 50 60

key market occasional projects no projects

2002 2004 % of companies

Diagram 8.4. Other Western European Countries 13 42 32 23 52 6 0 10 20 30 40 50 60

key market occasional projects no projects

2002 2004 % of companies

The diagram 8.5 shows that the Southeast Asia market will not undergo any serious changes. Diagram 8.5. Southeast Asia

3 26 55 6 35 35 0 10 20 30 40 50 60

key market occasional projects no projects

2002 2004 % of companies

Diagram 8.6. Other Countries

35 26 25 30 35 40 2002 % of companies

10. Russian Vendors: Index of Citation

We have asked our respondents to name three leading Russian companies in the field software outsourcing. According to the number of citations, the undoubted leader among Russian software development vendors is LUXOFT. Runners-up are Novosoft, VDI, Reksoft and EPAM.

Please note, that the diagram below reflects the number of citations among the respondents, not the size or annual revenue of companies or any other characteristics. The rating shows recognition in Russia, which correlates with the vendors’ activity in the domestic market.

You may find an alternative rating in the recent “Buyer’s Guide to Offshore Outsourcing” from CIO Magazine (http://www.cio.com/offshoremap/russia.html), which gives a slightly different picture (with Fort-Ross consortium, Novosoft, Luxoft, and STAR Software mentioned in alphabetical order as major providers).

Diagram 9. Index of Citations

0 10 20 30 40 50 60

LUXOFT Novosoft VDI EPAM Reksoft

% of answers

11. Key Trends of the Russian Offshore Development Market

In this survey we have also questioned the major tendencies in the development of the Russian software outsourcing market. Almost 40% of vendors believe that more and more companies will certify their software development processes according to ISO 9000 and SEI CMM standards. Many predict market growth (20%) and expect an enlargement of market players (30%). Other tendencies are consolidation of software development companies under the umbrella of IT-associations (17%) and the decrease of “gray” teams’ share (9%).

12. Main Priorities in the Development of Companies

Software process certification has been noted as the critical success factor by more than 43% of companies. (That is one of the key trends in the development of the Russian software outsourcing market). Other priorities are client acquisition (39%) and development of “product” model (39%), establishment of representative offices in the USA and Canada (30%), and vertical specialization (9%).

13. Software Development Process Certification

As we have already mentioned, many vendors consider the software development process assessment as one of the main priorities in the company’s development and one of the key trends in the Russian software outsourcing industry. According to the survey’s results more than 35% of companies are certified according to ISO 9000 or SEI CMM standards. Diagram 13 shows SEI CMM is getting more and more recognition – 35,5% of companies plan on obtaining SEI CMM status in the nearest future. A third of the vendors are planning to get ISO 9000.

Diagram 10. Software Development Process Certification 26 9 32 35 10 0 10 20 30 40 50 60 ISO SEI CMM Not planning Planning Certified % of companies

14. IT-Associations

Consolidation of software development companies under the umbrella of IT-associations is one of the key trends in the Russian software development industry. As it follows from the diagram 11, the leading association is RUSSOFT.

Diagram 11. IT-Associations Membership, % of Companies

RUSSOFT 41,9% Inforus 12,9%

Fort-Ross 16,1%

Outsourcing to Russia: How To

Capability and Maturity: More Than Just Development Issues

Provided by Brooke Nicole Consultancy (http://www.brookenicole.com/)

As Russia and other countries chase down India for the leadership role in providing offshore development and services there has been a lot of attention and priority placed by these countries on achieving a certification level or appraisal for their software development and services capabilities or maturity. Although these are indeed worthy goals, there is much more a buyer and supplier must consider when working on the global market.

In a recent Gartner report, the independent research firm states, “In the past, U.S. enterprises have traditionally sourced work to external services providers by choosing some pre-selected criteria (e.g., strength in a particular vertical or horizontal process, geographic coverage, technical competency and quality certification) and then quickly creating a list of external services providers that might meet those criteria. However, with the shift to global sourcing, enterprises may not know most, if any, of the leading vendors in a particular country. They must also decide whether they even wish to do business in a particular country. Thus, they must consider a number of country-specific criteria that bear no relation to the standard, individual company selection factors."

This means that offshore companies that wish to remain viable long-term businesses must take the initiative to meet the customer’s need for independently developed information about both a country and company. Offshore vendors that do this proactively can expect to gain an edge over the competition. Truly the software development and service capabilities must be addressed, and yes, and independent appraisals, such as the CMM, ISO, and COPC hold the most credibility. But there is much more that ultimately can impact the offshore experience.

Brooke Nicole recommends both buyers and suppliers, regardless of what country they are from, ensure the following areas are communicated and understood during the business development life cycle:

Company history

Management team profiles Location

Country laws Government support Geopolitical risk Infrastructure

Labor pool characteristics Educational system English proficiency Cultural compatibility Labor cost advantage Technology capabilities Business / Market capabilities Reference account profiles

Software development life cycle analysis Quality assurance program analysis Change management process analysis Project management methodology analysis Strategic partnership analysis

Photographs of key personnel, facilities and infrastructure

Capability and maturity in the above areas are critical success factors that must be completely understood before engaging in an offshore B2B relationship. Doing so without this level of detail exposes the buyer to unnecessary risks.

As the offshore marketplace continues to grow, and competition expands beyond the traditional offshore hotbeds of Southern Asia and Eastern Europe, it will become more and more important for vendors to

differentiate themselves. One such manner will be by proactively meeting the informational needs of today’s savvy buyer. However, it is up to the buyer to challenge the supplier for the information. In the offshore development and services market, “trust us” simply doesn’t suffice.

In an effort to help both buyers and suppliers even further, Brooke Nicole is working with industry analysts (IDC, Yankee Group, and others) and independent media (CIO Magazine) to develop a set of criteria and a methodology for rating offshore companies. As an independent, unbiased consultancy Brooke Nicole will lead this project. The goal is to provide a scale, which buyers can use to determine the overall quality of an offshore company and the risks associated with doing business with it.

Much of the core data is already available in the Offshore Suppliers Directory (http://www.offshore-suppliers-directory.com/) and will be used throughout the project. Once the criteria are finalized Brooke Nicole foresees each area being measured independently and then all the criteria averaged up to provide a rating. However, one important factor in this effort will be the validation phase. Brooke Nicole is still determining how this validation will occur but foresees training “authorized” assessors in key geographies to deliver this most important, final phase. As such, an offshore company will receive a “preliminary” rating and those that have been verified by a authorized assessor will receive a “certified” rating.

As the offshore market continues to grow and mature it will become increasingly more important that an independent authority help oversee this market space. Brooke Nicole has positioned itself to do just that. ---

About The Author: Jeff Crump is President & CEO of Brooke Nicole Consultancy, Inc. Mr. Crump welcomes your feedback and comments. He can be reached via email ([email protected]). For more information about Brooke Nicole visit their Web site (www.brookenicole.com).

Shaping your Agreement: Ten Steps to help you steer clear of traps

and trouble

Provided by BEITEN BURKHARDT GOERDELER Rechtsanwaltsgesellschaft mbH(http://www.bblaw.de) Online version: http://www.outsourcing-russia.com/kb/docs/legal/l02101-03.html

Any IT Outsourcing Agreement requires both the company requiring services (Customer) and the company offering services (Supplier) to consider a number of issues that typically arise in international agreements. Keeping in mind the following points will minimize the risk of unforeseen problems and / or litigation. Of course, your agreement should serve your particular project and therefore the following points cannot be conclusive. They are, however, the basics that will get you started on the road to a sound agreement.

1. Parties

Verify the power to represent of the person who will sign the agreement on behalf of the other party. If your partner is a Russian company, the power to represent is determined by Russian law independently from the place where the agreement is signed or the law applicable to the agreement. For example, a Russian limited liability company (in Russian: Obshestvo s ogranichennoj otvetstvennostju) is represented by its general director. Any other person requires a power-of-attorney in order to validly represent the company.

2. Be specific

Be specific in determining the substantive scope of your agreement.

Software Development Agreement (see "How good is your Software Development Agreement" (http://www.outsourcing-russia.com/kb/docs/legal/l02101-04.html))

Service Level Agreement (see "How good is your Service Level Agreement" (http://www.outsourcing-russia.com/kb/docs/legal/l02101-05.html))

3. Subcontracting

When you have found your Russian partner, you may have a particular interest in having the agreement carried out by that partner. Therefore, address the issue of subcontracting. If subcontracting is prohibited, it should be explicitly stated in the contract.

There is also the possibility of regulating the terms of subcontracting. If the agreement allows subcontracting, agree on the liability of the Supplier in the event of the subcontractor's default.

4. Confidentiality

IT Outsourcing Agreements are often confidential in character. Confidentiality can be addressed in a clause within the agreement or can be the core of a separate non-disclosure agreement.

Any confidentiality clause or non-disclosure agreement should contain a precise definition of the information to be treated confidentially. The definition should refer to the subject matter of the information, the form of the information (for example, information given to the other party in writing and clearly identified as confidential information) and the recipients of the information (for example, the specific employee of the other party i.e. the project manager). It should specify the conditions under which the disclosure of information is allowed or that exclude liability of the other party.

5. Non-competition

Address the issue as to whether and to what extent the Supplier may enter into agreements with the Customer's competitors. However, please note that non-competition clauses are not permitted in every country. Russian competition law prohibits an agreement concluded between a Customer and a Supplier in which the Supplier holds a dominant position, and such an agreement may be held void by a Russian court if it leads or may lead to a restriction of competition in Russia.

6. Limitation of liability

Limitation of liability issues can be dealt with by agreeing upon a "cap" or maximum amount of liability arising from all breaches of the agreement and, in each single case, a "basket" or minimum amount of

damages necessary to resolve a claim. Furthermore, you may want to agree on a limitation period for claims.

7. Taxes

Check the applicability of Russian VAT (currently, July 2001, 20%). Whether Russian VAT applies depends on the structure of the agreement and, among other things, the activities of the Customer in the Russian Federation. For example, Russian VAT does not apply to agreements whereby the Supplier grants a license for the use of software to the Customer if the Customer has no presence or activity in the Russian Federation. If the Customer acquires software through a sale and purchase agreement, a 0% VAT rate will apply if the software is exported in conformity with the customs regulations for the export of goods. In order to achieve a more advantageous and cost efficient structure for both parties, the tax implications of any agreement should be reviewed on a case by case basis and at an early stage.

8. Applicable law

In an international agreement, you should always determine in advance which law governs the agreement. You are free to choose the law that will determine the legal relationship between you and the other party and, therefore, you may choose the law with which you are most familiar. However, any IT Outsourcing Agreement implemented in Russia has to take into consideration Russian law. In particular, copyright law, legal provisions on the protection of software, legal provisions on export control, customs law, currency law and tax law will have an impact on the implementation of the agreement.

It is therefore important at an early stage to seek professional advice on the impact of Russian law on your agreement.

9. Competent court

Practice shows that the authority of a contract stems from its enforceability. Therefore, even if litigation is not what you have in mind, you have to make sure possible claims can be enforced in Russia. Not every court judgment is enforceable in Russia. If there is no bilateral treaty on the enforcement of judgments of state courts between your country (or the country of another intended place of jurisdiction) and Russia, two options remain: Russian commercial courts (in Russian: arbitrazhnye sudy) or commercial arbitration (in Russian: tretejskie sudy). Russia is a member of the New York Convention on the recognition and enforcement of foreign arbitral awards. If you submit your agreement to arbitration outside Russia and the place of arbitration is located in a member country of the New York Convention, the arbitral award can be enforced in Russia. However, practice shows that the enforcement of foreign arbitral awards in Russia can be difficult, time consuming and expensive. The choice of the competent court should be decided case by case depending on your interest and needs.

10. Language

The parties to an international agreement are usually more at ease with the terms of the agreement if it is drafted in their respective languages. Agree on the preemptive status of one language in bilingual contracts. As a rule, the prevailing language should be an official language of the competent court.

Risk Management in Projects: 17 Steps to Success

Provided by Brooke Nicole Consultancy (http://www.brookenicole.com/)

Online version: http://www.outsourcing-russia.com/kb/docs/outsourcing/o04062-01.html

Theoretically, every decision on a project should be subjected to some form of risk analysis. However, to repeat a formal assessment is impractical for all but significant project events and changes. In other circumstances it is sufficient for the project manager to have a “risk awareness” of any changes taking place. The effective management of risk includes both this informal awareness and a structured approach. Within a project, there are 17 steps that can be taken to help manage risk. These steps can be grouped into four major categories:

Planning: Identifying the type of response appropriate for each risk; developing a detailed plan of action; confirming its desirability and objectives; and obtaining management approval

Resourcing: Identifying and assigning the people and other resources (e.g. money and equipment) necessary to do the work; also confirming that the plan is feasible

Controlling: Making sure that events on the plan are really happening

Monitoring: Making sure that execution of the plan is having the desired effect on the risks identified. Also ensuring that the management of risk processes is applied effectively

The extent to which these activities need to be addressed depends upon the size and nature of the particular project under review. Also, these activities are not necessarily carried out sequentially.

This paper will walk clients through the 17 steps and actions involved in risk management on a project basis.

Planning

The basis of risk management is in the “action plan”, which is developed in steps 1 – 7. It’s important to note that inadequate attention to some of the early steps may waste time and effort later.

Step 1: Determine risk indicators and pass information to risk evaluation. The level of acceptability of a risk or group of risks needs to be decided as part of the planning process prior to its use in the evaluation activity of risk analysis.

Step 2: Using the ordered set of risks, assess each against its indicators. When risk estimation is finished during the risk analysis phase, all the identified risks are placed into an order of importance based on their likelihood and potential consequences. It is now necessary to superimpose upon this list the risk indicators that have been defined.

Step 3: Select the most appropriate means of reducing each risk. No further action, other than monitoring, is required for risks that are below their risk indicator. Actions on risks, which are above their defined level of acceptability, may also be deemed undesirable. If the cost of such action is not justified then either the risk indicator needs to be adjusted or the project must be halted.

Step 4: If the risk is to be accepted without trying to avert it, go to Step 6. If risk is to be eliminated, its likelihood or consequences reduced, or its consequences mitigated, then design an appropriate course of action. If a risk is to be accepted without any reduction measures taken, then it need only be monitored. It is important, however, that the approach to monitoring is planned. If the elimination of risks, or reduction of their likelihood or consequence is selected, some proactive action is implied.

Step 5: Ensure that the course of action selected does not produce any unintended consequences. Part of the planning process is to ensure that whatever means are selected to deal with the risks identified, these new actions themselves will not make things worse.

Step 6: Create a preliminary risk management plan and define the initial monitoring requirements. A detailed risk management plan is created as a result of the planning process, to implement the risk reduction measures decided upon. The risk management plan summarizes the risk analysis conducted, as well as recommends courses of management based upon the level and types of risk present.

Step 7: Present plan to management for authority to proceed. Execution of the risk management plan must not begin until senior management has formally approved the plan. This step is undertaken to ensure that staff or cost commitments are fully appreciated, and that the approach being proposed for risk management is in line with the overall strategy of the organization.

Resourcing

To undertake the identified tasks, resources must be allocated to each task and final adjustments to plans made. These plans must reflect skills, experience and availability of the identified resources.

Step 8: Allocate resources to risk management plan. The allocation of resources to risk reduction is one of the critical activities of the risk management phase, and can proceed in parallel with Step 6 of the planning activity. The risk planning process must concentrate on ensuring that the highest priority risks are attended to first.

Step 9: Assign responsibility for the activities identified in the risk management plan. As part of the resourcing activity, authority for risk management activities is delegated and responsibility assigned throughout the organization to individuals and groups.

Step 10: Ensure the risk management plan is feasible, and perform re-analysis of risks if necessary. Having allocated resources to the plan it is necessary to make a final judgment concerning feasibility of the plan. Aspects to consider at this stage primarily concern appropriateness of resource allocation and whether this allocation has implications for planned cost and time.

Step 11: Finalize the risk management plan and begin its execution. Although the elimination of risks is the aim of management of risk, generally this is not plausible or practical due to the scarcity of resources available for risk reduction, the unacceptably high cost of any action, which would be effective, or the nature of the risk. Thus, a combination of acceptance, elimination, reduction and mitigation measures must be put into place.

Controlling

Once the risk management plan has been finalized and execution begins, then the activities defined within the plan must be undertaken with suitable control being exercised.

Step 12: Ensure progress against the risk management plan is within resource limits. Control activities concentrate on ensuring that the risk management activities specified in the project plan are being properly executed.

Step 13: Coordinate the execution of the risk management plan with existing organizational activities. Communication makes up a large part of the control activities. All risk reduction activities have to be coordinated with each other and with other activities, notably those concerned with the development of the project itself. Specific action may be necessary to harmonize the implementation of both risk reduction and project work.

Step 14: Resolve any conflicts over resource allocation. Resource conflicts must be addressed before they compromise the implementation of the risk management plan or the project development activities. There must be no hesitation in using the escalation procedure if the problem cannot be resolved at the project manager level.

Monitoring

Having planned and then controlled the activities on the project, it is necessary to monitor progress against the plan and assess whether everything is proceeding healthily. Project progress is specifically assessed at the control points, such as end-stage and mid-stage assessments.

Residual risks are acceptable, or are subject o continuing action on the plan; in this event the monitoring must continue

No other risks have materialized over time

Step 17: Discover the reason(s) for change in the risk status. If minor corrective action is required, return to Step 14. It is, of course, possible that the risk reduction measures are not working as well as had been expected, and thus that corrective action is required. If the corrective action required is significant in terms of cost and time, especially if it involves several risks (a highly likely situation), a new risk analysis may be required.

In summary, helping to identify the possible options is central to risk analysis; choosing between such options is central to risk management. The effort expended on analyzing and managing risk depends upon several factors, including:

Project size, length

Criticality of project to the business Experience of the project team

The effort expended on managing risk should be reasonable enough to keep risk exposure to acceptable levels within the overall constraints of the project.

For More Information: Please contact Brooke Nicole via telephone (Toll Free +1.877.788.0404) / (Direct +1.931.788.0404) or email ([email protected]). We welcome you to visit us on the Web at: www.BrookeNicole.com.

Overview Legal Framework for Activities in the Sphere of Information

Technologies in the Russian Federation

Provided by BEITEN BURKHARDT GOERDELER Rechtsanwaltsgesellschaft mbH (http://www.bblaw.de) Online version: http://www.outsourcing-russia.com/kb/docs/legal/l16092-01.html

1. Protection of Software and Databases

In Russia, copyright is available for software and databases. The two principle acts governing the copyright protection of software and databases in the Russian Federation are the Law of the Russian Federation "On Copyright and Adjacent Rights" No. 5351-I of 9 July 1993 (hereinafter - the "Law on Copyright") and the Law of the Russian Federation "On Legal Protection of Computer Programs and Databases" No. 3523-I of 23 September 1992 (hereinafter - the "Law on Computer Programs").

General

Software products are protected as literary works and databases as compilations. Copyright protection is offered for software and databases either originally published in Russia or remaining unpublished but existing in some objective form in Russia. The copyright on software and databases is automatic upon their creation, with no formalities required, although the author may elect to register them at any time during the period of copyright protection in order to ensure the confirmation of his/her copyright. The copyright may be registered in the Russian Patent Office (ROSPATENT). The copyright protection is offered during the lifetime of the author and for 50 years after his/her death.

Moral Rights and Economic Rights

The author is an individual whose creative efforts brought the software or the database into existence. Regardless of any economic rights, the author is guaranteed the following moral rights:

right of recognition as the creator of the product right to integrity

right to use the work under the author's name or a fictitious name right to make public

The author is granted the following economic rights: publishing right

reproduction right distribution right

modification right, including translation other economic rights

Unlike the moral rights, which are personal to the author and non-transferable, the economic rights may be licensed or assigned.

Licensing and Assignment

At the parties' discretion the licensing agreement may be registered with ROSPATENT. The license agreement must be in writing and must specify rights of use, term, territory, license fees, and other terms that the parties consider essential. Unless the term is specified the licensor may withdraw the license in five years with a six-month written notice. Sales of the software to end-users may be in the form of 'shrink-wrap' licenses.

The assignment of registered software or database is subject to mandatory registration with ROSPATENT.

damages, including lost profits

compensation from approximately USD 16,000 to USD 160,000 as may be determined by the court, in lieu of damages

2. Chip Design

GeneralProtection of computer chip design in the Russian Federation is regulated by the Law of the Russian Federation "On Legal Protection of Chip Design" No. 3526-I of 23 September 1992. The chip design is protected, provided that it is original, i.e. it was created independently by the author and not copied. The originality of the chip design is presumed. The author of the chip design is an individual whose creative efforts led to creation of the chip. The proprietor may use 'T' on the chip for notification of his/her proprietary rights.

Rights in Chip Design

The author is guaranteed the right to be recognized as the author of the chip. This right is personal to the author and inalienable. The author is also guaranteed the right to use the chip design by manufacturing and distributing the same. The right to use the chip design may be assigned, licensed, and bequeathed.

Term of Protection

The rights in the chip design are protectable for 10 years after the earlier of: (i) the first use of the chip; or (ii) the registration of the chip design with ROSPATENT.

Registration

Registration with ROSPATENT is optional and may be effected within two years after the chip was first used. Assignments of registered chip designs are subject to mandatory registration.

Liability For Infringement

In the event of infringement the following remedies are available to the aggrieved party in court: recognition of rights

restitution and termination of infringement (or acts which may lead to infringement) damages, in accordance with the Russian civil laws

3. Internet

There is no specific legislative act in the Russian Federation governing the relations connected with the use of the Internet. The information and data placed on the Internet are therefore regulated on the basis of existing Russian civil laws and legislation on copyright, trademarks, trade names, mass media, telecommunications, and unfair competition.

Providers of Internet services in the Russian Federation are considered providers of communication services and must act under licenses and certificates of compliance issued by the Ministry for Communications and Information.

Until recently domains of the second level of zone .ru have been administered by the Russian Scientific Research Institute for Development of Public Networks (RosNIIROS). Under the Resolution of the Government of the Russian Federation No. 533 of 17 July 2002 "On Amending and Supplementing the Regulations of the Ministry of the Russian Federation for Communications and Informatization", the powers of administration of domains of the second level within the .ru zone have been transferred to the Ministry for Communications and Informatization.

Case law on Internet

During the last three years there have been several court cases connected with the infringement of rights in the Internet. However, decisions by the Russian courts of different levels and different regions do not always demonstrate clear understanding of the problems. Russian courts are prepared to give protection against 'cybersquatting' if the disputed domains contain the claimant's trade name (Mosfilm v RosNIIROS, Decision of the Moscow Arbitration Court No. A-40-22492/99-15-232 of 7 July 1999; Eastman Kodak Co. v Grundul, Decision of the Federal Arbitration Court of the Moscow District No. KA-A40/6520-00 of 25 January 2001). Also, several recent cases show that the registration of domains may also be challenged on the basis of trademark infringement (Baxter International v Unitair, Decision of the Moscow Arbitration Court No. A-40-12817/02-110-138 of 14 May 2002; Miele&C GmbH v Sters, Decision of the Moscow Arbitration Court No. A-4042141/01-26-19 of 10 January 2002). In all the above cases the claimant succeeded in obtaining a court order for re-registration of the disputed domains in his name. It is also important to note that documents placed on Internet are under protection of the Russian copyright laws

(Media-Lingua v Rambler Internet Holding, Decision of the Moscow Arbitration Court No. A40 of 12 January 2001).

4. Electronic Commerce

There is no specific legislative act in the Russian Federation governing e-commerce. Such relationships are governed by the general provisions on sale of goods in the Civil Code; Federal Law "On Electronic Digital Signature" No. 1-FZ of 10 January 2002; Federal Law "On Information, Informatization and Protection of Information" No. 24-FZ of 20 February 1995. Powers for development and implementation of trade policy in the area of e-commerce are vested with the Ministry of Economic Development and Trade of the Russian Federation (Regulations on the Ministry of Economic Development and Trade, approved by Resolution of the Government of the Russian Federation No. 990 of 21 December 2000). The first reading of a draft law on e-commerce is currently being considered by the State Duma of the Russian Federation. The draft law is based on the approach of the UNCITRAL Model Law on Electronic Commerce.

5. Electronic Signatures

The Federal Law of the Russian Federation "On Electronic Digital Signature" No. 1-FZ was enacted on 10 January 2002 (hereinafter - the "Law on Electronic Signature"). The electronic signature is deemed legally equal to the handwritten signature on a paper document when the standards and conditions set out in the Law on Electronic Signature are met. The electronic signature keys must only be created using certified electronic signature devices. The electronic signature key consists of a private key (confidential and restricted to its holder) and an open key (required for confirmation of the electronic signature, available to all users of the system and corresponding to the closed key). The keys are created and issued by authorization centers licensed by the Federal Agency for Governmental Communications (FAPSI). Authorization centers also maintain registers of holders of electronic keys. The open key is issued to its holder in the form of signature key certificate, indicating among other things the software used for electronic signature. Electronic keys are valid for a period set out in a contract between their holders and the authorization center. The Law on Electronic Signature allows for individual and corporate systems of electronic signatures. Foreign signature key certificates are recognized in the Russian Federation if legalized or apostilled.

6. Licensing and Certification

Activities which are only permitted to be carried out on the basis of a license are set out in the Federal Law "On Licensing of Certain Activities" No. 128-FZ of 8 August 2001 (hereinafter - the "Law on Licensing"). In accordance with the Law on Licensing, among others, the following activities must be licensed:

development, manufacturing, and sale of encryption software and other software and hardware for the protection of confidential information- licensed by the State Technical Commission of the President of the Russian Federation;

development, manufacturing, maintenance, distribution of, and services in the area of cryptographic devices - licensed by the Federal Agency for Governmental Communications (FAPSI);

issuance of electronic signature key certificates, registration of holders of electronic signatures, services related to the use of electronic signatures, authentication of electronic signatures - licensed by FAPSI;

development, manufacturing, distribution and acquisition of surveillance and interception devices - licensed by Federal Security Service (FSB);

7. Computer Crimes

Chapter 28 of the Russian Criminal Code is specifically devoted to computer crime and contains three prohibited criminal offences:

Article 272 "Unlawful Access to Computer Information" prohibits unlawful access to computer information if it caused deletion, blocking, modification or copying of any information, interference with the operation of an individual computer, computer system or computer network. The maximum penalty is five years imprisonment.

Article 273 "Creation, Use and Distribution of Harmful Computer Programs" makes it an offence to create software or modify existing software so that it knowingly results in deletion, blocking, modification or copying of any information or interference with the operation of an individual computer, computer system or computer network, and to use or distribute such programs or any material media with such programs. The maximum penalty is seven years imprisonment.

Under Article 274 "Violation of Rules of Operation of Computers, Computer Systems or Computer Networks" such violations constitute an offence if they lead to deletion, modification, or copying of confidential information protected by law and caused substantial harm. The maximum penalty is four years imprisonment.

There are also a number of other activities prohibited by the Russian Criminal Code, which may be applicable to computer crimes, such as: Article 137 "Infringement on Privacy", Article 138 "Infringement on Privacy of Mail, Telephone Communication, Postal, Telegraph and Other Communications", Article 183 "Unlawful Obtaining and Distribution of Information Which Constitute Commercial, Tax or Bank Secrets", and Article 146 "Infringement on Copyright and Adjourning Rights".

The Russian courts have considered quite a number of criminal cases on computer crime to date. The Russian Supreme Court, however, has not issued any comments or guidance on how such cases should be uniformly adjudicated. Responsibilities for investigation of computer crimes are vested with the specialized 'R-Department' of the Ministry of Internal Affairs of the Russian Federation.

8. Electronic Russia 2002 - 2010

The Government of the Russian Federation has approved the federal program Electronic Russia 2002 - 2010 (Resolution of the Government of the Russian Federation No. 65 of 28 January 2002). The purpose of the Program is broad implementation of information and communication technologies, free distribution, transmission and receipt of information, and training of IT specialists and users. The following goals must be attained to ensure successful implementation of the Program: formation of efficient IT legislation; increased interaction among governmental authorities based on IT; efficient and broad use of IT in social and economic spheres; IT-based training; further development of telecommunications network; formation of the unified information and telecommunication network for interaction among governmental authorities; and creation of conditions for development of e-commerce.

The legislative developments in the area of IT must be based on the following principles: unified information field;

integration of Russia into the international system of information exchange; rights of individuals to receive information from public sources;

publicity and openness in drafting legislation;

publicity and openness in considering applications for licenses and certifications; equal business conditions and elimination of monopoly in the area of IT;

formation of legal framework for the use of electronic documents in the state management and civil law relations;

legal resolution of problems related to investigation of crimes in computer networks; simplified export of IT products;

development of a unified complex of Russian IT legislation and bringing the Russian legislation into compliance with the international laws.

An Interdepartmental Committee has been created for the implementation of the Program. The chairman of the Committee is Mr. German Gref, the Minister of Economic Development and Trade, and the deputy chairman is Mr. Reiman, Minister for Communications and Informatization.

The Program envisages three consecutive stages.

First Stage 2002. The first stage includes a plan for the creation of a monitoring system for the following matters: global tendencies in IT development and its use in the social and economic spheres; the degree of IT development in Russia, the efficiency of application of state funds in IT; the efficiency of IT use by the

efficiency of the existing IT legislation. The first stage also envisages the drafting of a number of bills in the areas of electronic documents, e-commerce, and bringing the Russian IT legislation in line with the international laws. Further, this stage of the Programme provides for implementation of pilot projects for transition to electronic documentation and development of telecommunications network by the governmental authorities and state-owned institutions, development of e-commerce, and training of IT specialists and users. Preparatory steps must be taken and pilot projects initiated to connect governmental authorities and state-owned institutions to computer networks. During the first stage the program for training government personnel, the unemployed and the socially unprivileged must be developed and initiated.

Second Stage 2003-2004. The second stage has as its purpose the implementation of projects associated with the interaction between the governmental authorities and businesses in the area of tax, customs, company registration and liquidation, licensing and certification, and other statutory filings. Pilot projects for implementation of unified IT systems in the defence enterprises are envisioned. A unified information and communication network must be created for the governmental authorities. Resources must be allocated for training IT specialists in the leading schools and increasing the number of IT graduates.

Third Stage 2005 - 2010. The third stage of the Program will create the basis necessary for massive IT access in all economic spheres on the basis of the single information and telecommunication network and the e-commerce system. A complex e-commerce system shall be implemented for the needs of governmental procurement. A standard system of electronic documentation and a system of security of information must be developed for these purposes. The unified system of information and communication of the governmental authorities and state-owned enterprises must be completed at the third stage.