1.

21.

57.

79.

103.

129.

Volume 11 Issue 1

June 2016

Volume 11 Issue 1

June 2016

The Role of Management Accountants in the Automotive

Supply Chain Management

Eley Suzana Kasim

Indra Devi Rajamanoharan

Normah Omar

Target Costing in a Stage-Gate Design System

Jan Alpenberg

Jeton Alku

Judita Rashiti

Paul Scarbrough

The Role of Strategic Planning, Accounting Information

and Advisors in the Growth of Small to Medium

Enterprises (SMEs)

M. Christopher Catto

Environmental Management Accounting: Identifying

Future Potentials

Amiruddin

Gagaring Pagalung

Organizational Learning Orientation and Sustainable

Competitive Advantage: Towards More Accountable

Government Linked Companies

Nur Nadiah Zulkarnain

Nik Herda Nik Abdullah

Jamaliah Said

Md. Mahmudul Alam

Chief Executive Officer (CEO) Shareholding and

Company Performance of Malaysian Public Listed

Companies

Soo Eng, Heng

Tze San, Ong

Boon Heng, Teh

Volume 1

APMAJ is indexed in Ebscohost, Cabell’s Directory of Publishing Opportunities in Management (www.cabells.com), Ulrichs (www.ulrichsweb.com) and the Journal Ranked List of Australia Research Council with ERA (Excellence in Research for Australia) and Australian Business Deans Council (ABDC). It is also indexed by UDLedge Social Science & Humanities Citation Index (SS&HCI) and Focus (Journals and Conference Proceedings). Since September 2015 APMAJ is indexed by the Emerging Sources Citation Index (ESCI) of Thomson Reuters.

ASIA-PACIFIC MANAGEMENT

ACCOUNTING JOURNAL

Prof Dr Akira Nishimura, Beppu University, Japan Prof Dr Amy H.Lau, University of Hong Kong, Hong Kong Prof Dr Malcolm Smith, University of South Australia, Australia Prof Dr Falconer Mitchell, University of Edinburgh, UK Prof Dr Foong Soon Yau, Universiti Putra Malaysia, Malaysia Prof Dr John Burns, University of Exeter, UK

Prof Dr Keith Maunders, University of South Pacific, Fiji Prof Dr Paul Scarborough, Brock University Canada Prof Dr Jan Alpenberg, Linnaeus University, Sweden Prof Dr Ralph Adler, University of Otago, New Zealand Prof Dr Takayuki Asada, Osaka University, Japan

Prof Dr Ibrahim Kamal Abd Rahman, Universiti of Kuala Lumpur, Malaysia

Prof Dr Yuanlue Fu, Xiamen University, China Prof Dr Sakhti Mahenthiran, Butler University, USA Prof Dr Nik Nazli Nik Ahmad, International Islamic University, Malaysia

Prof Dr Yang Tzong Tsay, National Taiwan University, Taiwan

Prof Dr Grahita Chandrarin, Merdeka Malang University, Indonesia

Prof Dr Mimba Ni Putu Sri Harta, University of Udayana, Indonesia

Prof Dr Mahmuda Akter, University of Dhaka, Bangladesh Prof Dr Yiming Hu, Shanghai Tiaotong University, China Prof Dr Thomas Ahrens, United Arab Emirates University, UAE Prof Dr Masaaki Aoki, Tohoku University, Japan

Prof Dr Taesik Ahn, Seoul National University, Korea Prof Dr Lin Zhijun, Hong Kong Baptist University, Hong Kong Prof Dr Chu Hsuan Lien, National Taipei University, Taiwan Prof Dr Robert P Greenwood, University of Gloucestershire, UK Prof Dr Chris Chapman, Imperial College Business School, UK Prof Dr Kannibhatti Nitirojntanad, University of Chullalongkorn, Thailand

Prof Mohammed Fawzy Omran, Qatar University

Assoc. Prof Dr Che Ruhana Isa, University of Malaya, Malaysia Assoc. Prof Dr Cheng Nam Sang, Singapore Management

University, Singapore CHIEF EDITORS

Prof Dr Normah Omar Universiti Teknologi MARA, Malaysia

EXECUTIVE EDITOR Prof Datin Dr Suzana Sulaiman Universiti Teknologi MARA, Malaysia

MANAGING EDITORS Dr Tuan Zainun Tuan Mat Universiti Teknologi MARA, Malaysia Assoc. Prof Sharifah Fadzlon Abd Hamid

Universiti Teknologi MARA, Malaysia

JOURNAL ADMINISTRATOR Ms Wan Mariati Wan Omar Universiti Teknologi MARA, Malaysia

EDITORIAL ADVISORY AND REVIEW BOARD Prof Dr Susumu Ueno

APMAA, Japan

Assoc. Prof Dr Jamaliah Said Universiti Teknologi MARA, Malaysia

Prof Dr Roger Willett University Tasmania, Australia

Dr Sharifah Norzehan Syed Yusuf Universiti Teknologi MARA, Malaysia

© UiTM Press, UiTM 2016

All rights reserved. No part of this publication may be reproduced, copied, stored in any retrieval system or transmitted in any form or by any means; electronic, mechanical, photocopying, recording or otherwise; without prior permission in writing from the Director of UiTM Press, Universiti Teknologi MARA, 40450 Shah Alam, Selangor Darul Ehsan, Malaysia.

E-mail: penerbit@salam.uitm.edu.my

ASIA-PACIFIC

MANAGEMENT

ACCOUNTING

JOURNAL

Volume 10 Issue 2 December 2015

C O N T E N T S

1. Role of Management Accountants in Automotive Supply Chain Management

Eley Suzana Kasim

Indra Devi Rajamanoharan Normah Omar

23 Target Costing in a Stage-Gate Design System Jan Alpenberg

Jeton Alku Judita Rashiti Paul Scarbrough

59 Role of Strategic Planning, Accounting Information and Advisors in the Growth of Small to Medium Enterprises

M. Christopher Catto

79 Environmental Management Accounting: Identifying Future Potentials

Amiruddin Gagaring Pagalung

95 Organizational Learning Orientation and Sustainable Competitive Advantage: Towards More Accountable Government-Linked Companies

Nur Nadiah Zulkarnain Nik Herda Nik Abdullah Jamaliah Said

Md. Mahmudul Alam

115 Chief Executive Officer Shareholding and Company Performance

of Malaysian Publicly Listed Companies Soo Eng, Heng

ABSTRACT

This study examines the role of management accountants in the supply chain management (SCM) of an automobile manufacturer. A case study was conducted on an automobile manufacturing firm operating in Malaysia. Drawing from SCM and management accounting literature and the Institute of Management Accountants’ statements on management accounting (SMAs), this study argues that despite recommendations from professional accounting bodies, the role of management accountants in SCM processes remains limited. However, management accountants are involved in the SCM of the case firm in one of four capacities: as a ‘planner’, ‘evaluator’, ‘controller’ and ‘verifier’. The results of this study provides additional insights into the contribution of management accountants to SCM as practiced within automotive manufacturing firms in Malaysia. Thus, this research adds to the body of knowledge on the integration of management accounting with SCM. Furthermore, it provides an opportunity to obtain increased understanding of how such an integration could be leveraged to enhance firm performance.

Keywords: supply chain management, role, management accountant, case study, Malaysia

R

ole of managementa

ccountantsina

utomotives

upplyc

hainm

anagementEley Suzana Kasim1,Indra Devi Rajamanoharan2, Normah Omar3

1Faculty of Accountancy,

Universiti Teknologi MARA Cawangan Negeri Sembilan, Malaysia. 2 Faculty of Accountancy,

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

INTRODUCTION

In the 21st century, firms, particularly in the automotive industry, constantly

respond to environmental changes to maintain their competitive advantage (Abdullah, Maharjan & Tatsuo, 2008). Local automotive firms at present face more challenges than before in maintaining their competitiveness as they strive to become serious competitors in global markets. The pursuit of competitiveness in the automotive industry relies largely on the ability of firms to achieve cost reduction, which in turn enables them to offer value-added products to consumers in terms of reduced prices without compromising quality. The Tenth Malaysia Plan of the Malaysian government recognises the importance of supply chain management (SCM) as a global competitive tool to achieve cost reduction. SCM focuses on increasing efficiency, reducing lead times, minimising inventory costs and maximising customer satisfaction, all of which aim to improve supply chain performance (Mentzer, DeWitt, Min, Nix, Smith & Zacharia, 2001; Ou, Liu, Hung & Yen, 2010; Stock, Boyer & Harmon, 2010).

A possible opportunity for the advancement of SCM as a global competitive weapon, but which remains largely neglected, is the potential contribution of management accounting (MA) in the implementation of SCM. SCM originated from the operations management and logistics discipline; however, recent development indicates an increasing amount of attention from MA researchers (Boute, Bruggeman & Vereecke, 2014; Pitingolo, 2012; Joyce, 2006; Cullen & Metcalf, 2006). Accordingly, management accountants are expected to offer significant contributions within the supply chain context (Chenhall, 2008). For example, Boute (2014) noted that management accountants are expected to provide managers relevant information regarding total supply chain activity costs which commonly include direct material, activity and driven overhead costs.

Nevertheless, despite concerns in the academia and the development of well-documented policies and standards that promote the active role of management accountants in SCM processes, the participation of management accountants in SCM processes remains low (see Alvarenga, 2014; Pitingolo, 2012; Chua & Mahama, 2007; Joyce, 2006; Ramos, 2004). In addition, empirical evidence on how the expertise of these management accountants is actually leveraged in practice is still limited. This gap implies that the nature of association between MA and SCM remains largely unexplored in literature. Hence, the need to examine further the potential roles of management accountants in facilitating SCM processes is evident. This research intends to close this gap by addressing the research question of how management accountants contribute to SCM processes, particularly within the Malaysian automobile manufacturing industry.

LITERATURE REVIEW

Supply Chain Management (SCM)

Globalisation causes organisations to operate in a more uncertain environment than that in the past. Efforts to mitigate uncertainties and enhance control over supply and distribution channels focus on SCM (Carter, Rogers & Choi, 2015; Borges, 2015; Boute, Bruggeman & Vereecke, 2014; Gunasekaran, Patel & McGaughey, 2004). Uncertainty factors, such as those related to product demand and supply, force organisations to collaborate with one another and result in the elaborate management of supply chains.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

to enhanced competitiveness of the supply chain and each member firm. This relationship ultimately improves the profitability of the supply chain and its members (Mentzer, DeWitt, Min, Nix, Smith & Zacharia, 2001).

Interface of Supply Chain Management (SCM) and Management Accounting (MA)

From a systemic point of view, Yasin, Bayes and Czuchry (2005) argued that the accounting sub-system within a firm should not be viewed in isolation from the other sub-systems, such as marketing and operations. A more open system view that integrates the accounting sub-system and others was proposed; the proposed view could result in a shift in the role of management accountants in firms. In particular, their study on quality orientation of firms suggests that the shift from transactional processing of accountants towards a strategic decision supportive role is warranted.

Role of Management Accountants in Supply Chain Management (SCM) Processes

The importance of the link between SCM and MA has been recognised by several professional bodies. For example, IMA in the US has issued a set of standards that delineate the roles and responsibilities of management accountants in supporting SCM processes. These standards comprise a series of SMAs to promote the organisation’s official professional standing in MA. Through the effort of its Management Accounting Practices (MAP) Committee, IMA successfully promulgated the statements as authoritative statements to guide MA practices in terms of concepts, policies and recommended practices. Through the publication of these SMAs, the potential contributions of management accountants in providing relevant data to operational managers on SCM issues are provided.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

Table 1: Roles of Management Accountants in SCM

Stages of

SCM Description of Roles

Design ● Creating or supporting the creation of an integrated supply chain management (ISCM) business case(s) as the need arises

● Supporting the design and development of effective, efficient integrated information systems

● Creating performance benchmarks, milestones and measures to support the development of the ISCM business case

● Supporting process redesign efforts focused on removing waste, reducing throughput time and increasing the flexibility and responsiveness of financial transactions across the supply chain

● Participating in the identification and implementation of new databases and information technology enablers for key supply chain transactions

● Creating management reporting and evaluation tools to ensure that the ISCM initiative meets its objectives and delivers the required performance improvements

Development ● Developing ‘virtual control’ systems to safeguard the

integrity of company and supply chain databases, transactions and flows

● Supporting the development of new forms of incentives and reward systems to encourage active participation and cooperation of individuals across the organisation in supply chain initiatives

● Developing new measurements, both financial and nonfinancial, to assess the degree of improvement of the supply chain

Stages of

SCM Description of Roles

Execution ● Providing economic and nonfinancial evaluation of

alternative improvement opportunities to facilitate the development of ISCM priorities

● Providing current estimates of supply chain costs and performance against defined customer expectations ● Providing management with timely reports that isolate

current performance shortfalls

● Participating in analysing proposed changes to ensure that economic factors are realistically portrayed

● Providing analytical support to ISCM teams, including identifying and estimating the costs and benefits of various decisions throughout design, conversion and execution efforts

● Participating in natural systems to improve team efforts ● Ensuring the integrity of supporting databases, internal

control procedures, key proprietary technologies, processes and physical and/or knowledge assets ● Examining existing transactional systems to identify ways

to reduce the costs or delays that reduce customer value, including instituting changes to the accounts payable effort within the order-to-payment system

● Collaborating with finance and operation professionals in partnering organisations to identify creative ways to solve logistics and support problems

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

From the local perspective, the Malaysian Institute of Accountants (MIA) in conjunction with the International Federation of Accountants (IFAC) has also developed a series of statements on International Management Accounting Practices (IMAPs) as an effort to enhance the quality of MA practices. However, unlike the standards issued by IMA, appropriate guidance has yet to be implemented on the SCM issued by MIA.

Despite the expected roles of management accountants in facilitating SCM processes, practical applications remain limited. This gap could be due to the limitation of traditional accounting practices that fail to fulfil their supporting role in inter-organisational decisions (Bastl, Grubic, Templar, Harrison & Fan, 2010). The present study seeks to examine the role played by management accountants in facilitating SCM processes in automotive firms. In particular, the nature of their contribution and the underlying factors that affect the degree of their contribution are investigated.

RESEARCH METHODOLOGY

The present study utilised the qualitative methodology to address the research question. Strauss and Corbin (1998) defined qualitative research as ‘any kind of research that produces findings not arrived at by means of statistical procedures or other means of quantification’. In particular, a case study was conducted as a method of investigation. Yin (2003) defined a case study as ‘an empirical inquiry that investigates a contemporary phenomenon within its real-life context, especially when the boundaries between phenomenon and context are not clearly evident’. Furthermore, he argued that this approach is appropriate when a ‘how’ or ‘why’ question is being asked about a contemporary set of events, over which the investigator has little or no control. Given that the nature of association between SCM and MA within the automotive industry is largely unexplored, the case study method is perceived as the most appropriate research strategy to be adopted.

data triangulation technique, several methods, such as face-to-face semi-structured interviews, observations and extensive use of archival data, were utilised to address the research question. The research issues were mainly addressed by using semi-structured face-to-face interviews with key informants within relevant departments in the case company. The informants were personnel employed at the senior management and managerial levels who are expected to be involved in the MA function that relates to SCM processes. The main respondents for addressing the current research question consist of accountants from the Finance and Accounts Department. Non-accountants within the case firm were also interviewed to obtain additional insights into the potential contribution of management accountants in SCM processes. The views of non-accountants, such as logisticians, procurement personnel and engineers, are crucial because they comprise the majority of the employees involved in SCM in the case firm. Interviews were conducted by setting prior appointment with the relevant interviewees. The interview meetings were on an ad hoc basis as and when deemed appropriate. Before conducting the interviews, the respondents were promised confidentiality to elicit candid responses.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

FINDINGS

Case Firm Profile – ACE

The case company, ACE, is an automobile manufacturer established in the 1990s. ACE is a manufacturing subsidiary of a holding company that was incorporated as a joint venture involving several local and foreign Japanese companies. The focus of ACE is on producing small and affordable vehicles. At the time of this study, the authorised and paid up capital of the holding company to which the case firm relates were RM500 million and RM140 million, respectively. The company has over 10,000 employees. The head office and its manufacturing plant share a common land area covering 200 acres. This land area uses 60% of the entire 340 acres of land area. The sales and services business of the group is handled by its own sales and service subsidiaries. To date, ACE has 41 sales branches and 139 sales dealers that cover sales activities nationwide. Throughout Malaysia, the holding company has 46 service branches and 124 service dealers that deal with after-sales services. Apart from catering to the domestic car market, ACE also manufactures automobiles for export to seven countries, namely, the United Kingdom, Singapore, Brunei, Fiji, Nepal, Mauritius and Sri Lanka.

The manufacturing plant of ACE covers an area of 64,000 square meters and has the capacity to produce 250,000 units per annum on a two-shift cycle. The plant is equipped with manufacturing facilities that consist of various shops, namely, press, body, paint and assembly. Other facilities include logistic, training centre, quality audit, pre-delivery inspection (PDI), stockyard and parts warehousing. Although the holding company is a local firm, ACE is effectively controlled by its Japanese parents. This scenario implies that the case firm follows instructions and reports regularly to its Japanese parent companies.

Findings on the Role of Management Accountants in Supply Chain Management (SCM)

The discussion in this section is based on the expected role of management accountants in SCM processes proposed by the IMA’s SMAs shown in Table 1. Case evidence from ACE was used to determine the extent to which management accountants fulfil these roles.

The case evidence revealed that the role of management accountants in ACE is broadly characterised into two functions, namely, financial and management accounting. As the custodian of financial accounting information, accountants are mainly concerned with the maintenance of accounting records, preparation of financial statements to fulfil statutory audit requirements, management of accounts receivable and accounts payable and management of the cash flow. From the MA perspective, accountants play an active role in management and decision making by providing relevant financial information to assist respective management levels.

For effective provision of accounting services within ACE, the Finance and Accounts Department is structured into the following four main sections.

1. General ledger section – preparation of all management accounts, including profit and loss accounts, and balance sheets

2. Accounts payable (and accounts receivable) section – preparation and processing of all payments

3. Product costing section

4. Treasury – management of the firm’s cash flows and foreign exchange exposure

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

Key Observations and Patterns of Involvement

The discussion on the role of management accountants in SCM processes at ACE is based on the four distinct categories of roles identified as follows:

1. Planner of strategic and operational SCM – ‘planner’ 2. Advisor/evaluator of SCM projects/initiatives – ‘evaluator’ 3. Controller of key internal operations – ‘controller’

4. Verifier of financial and non-financial accounting information – ‘verifier’

Management accountants are expected to participate actively in the design, development and execution stages of integrated SCM. Given this view, the case findings from ACE were used to discuss the involvement of management accountants in these stages. Table 2 summarises the key findings on the role of management accountants at ACE.

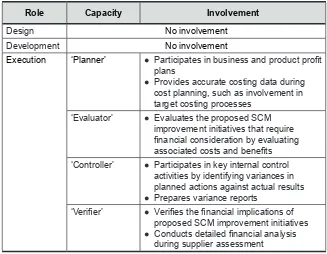

Table 2: Patterns of Management Accountants’ Involvement

Role Capacity Involvement

Design No involvement

Development No involvement

Execution ‘Planner’ ● Participates in business and product profit

plans

● Provides accurate costing data during cost planning, such as involvement in target costing processes

‘Evaluator’ ● Evaluates the proposed SCM

improvement initiatives that require financial consideration by evaluating associated costs and benefits

‘Controller’ ● Participates in key internal control

activities by identifying variances in planned actions against actual results ● Prepares variance reports

‘Verifier’ ● Verifies the financial implications of

proposed SCM improvement initiatives ● Conducts detailed financial analysis

As shown in Table 2, the management accountants at ACE have no direct involvement in the design and development stage of an integrated SCM because ACE employs the SCM framework that was adopted from the Toyota Production System (TPS). TPS serves as a main reference for most automotive firms not only in Japan but also in the entire world. As such, the framework of TPS is viewed as a universal SCM framework used by firms operating in the automotive industry, including ACE. Hence, very little contribution is expected from management accountants during the design and development phases of SCM within the case firm.

Involvement of Management Accountants at the Execution Stage of Supply Chain Management (SCM)

The case findings show that management accountants are involved in SCM processes at the execution level in their capacity as the ‘planner’, ‘evaluator’, ‘controller’ and ‘verifier’ of accounting information. The nature of their involvement under each capacity is presented in the following sections.

Management Accountants as ‘Planners’ of Supply Chain Management (SCM)

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

crucial stage of the new product development stage of ACE. Specifically, management accountants are involved in the application of target costing for new car models to be produced. According to a manager in the Finance and Accounts Department,

The main function of cost planning is to plan the cost before any model goes into mass production. Before we roll out a new model, they will perform a study project whereby they have a certain target cost to achieve. When the actual operation takes off, the costing department (product costing section) within my department will conduct actual cost computation for the purpose of reporting.

The target costing process requires accurate cost information because it is critical to determining the competitive pricing for the company’s products. Inaccurate cost planning could lead to inaccurate costing, which would adversely affect the profitability of the product. A manager of the cost planning section at ACE commented that

If the costing figures are incorrect, the new product costing will also be incorrect. Thus, the company cannot obtain profit. It is important for the figures to be correct, and these figures are collected by the [management] accountants.

Apart from the target costing techniques utilised in MA at ACE, management accountants are also involved in the other tools used for cost planning purposes, such as cost and value engineering.

Management Accountants as ‘Evaluator’ of Accounting Information

Any proposal that involves the supply chain, such as to fabricate a second link (mould) to overcome capacity problems, will be presented for approval in the monthly management committee meeting. If it is justified through the analysis of costs and benefits, the management will give its approval, and the project can proceed.

Therefore, the management accountants who are responsible for providing their evaluation of the costs and benefits act as an ‘evaluator’ of these decisions. These management accountants may challenge the financial figures presented by the proposer (the SC related personnel) on the justification of projected costs and revenue data.

Another example of the evaluative role of management accountants is evident in cost planning and cost management activities. While the cost planning process occurs at the research and development stage of a product, the cost management process involves cost control and cost improvement processes at the mass production stage. The cost control process involves the control of actual cost by comparing it with the standard costs derived at the cost planning stage. By contrast, cost improvement activities are concerned with the revision of existing standard costs followed by cost reduction activities based on the revised standard costs.

For effective cost management at ACE, each department within the case firm is required to improve continuously in terms of cost and expense reduction during the mass production stage. Each department is required to formulate specific action plans that are intended to reduce costs, particularly those at the operational level. These action plans are typically submitted by operational-level employees who basically have little background in accounting. Thus, most of the initiatives that they propose require evaluation from management accountants in terms of the projected financial implications of these cost reduction initiatives. An accounts manager commented that

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

Management Accountants as ‘Controller’ of Key Internal Control Activities

From the control perspective, management accountants actively participate in comparing the planned action against actual results by conducting variance analyses. These analyses, which are usually in aggregated forms, are presented at the monthly management committee meeting for further action. Apart from this, the control activities conducted by management accountants also concern cost reduction programs.

Cost control is a fundamental element in the cost planning process at ACE. This process is linked to the ‘plan-do-check-act’ (PDCA) cycle implemented in the cost planning process at ACE. The cost control process is combined with the PDCA cycle. Management accountants are mainly responsible for cost control through both the ‘do’ and ‘check’ processes within the PDCA cycle. As discussed previously, management accountants facilitate cost control by providing actual cost information which is allocated into separate cost centres. Based on this information, each department is able to assess their own spending and prepare a variance analysis for management control purposes. Consequently, at the ‘act’ stage of the PDCA cycle, cost improvement activities are carried out by establishing revised standard costs as a guideline. Based on these revised standard costs, each department identifies specific action plans to support the cost reduction activities.

Management Accountants as ‘Verifier’ of Accounting Information

At the end of the day when the lorry comes back, it is at a higher level efficiency, and the only person who can confirm the ringgit and sen (financial implication) is the staff from the accounts department.

In addition, management accountants are tasked with the detail audited of the cash flow position of the suppliers, which is performed during the selection of suppliers. They also deal with suppliers who are facing financial difficulties.

DISCUSSION OF FINDINGS

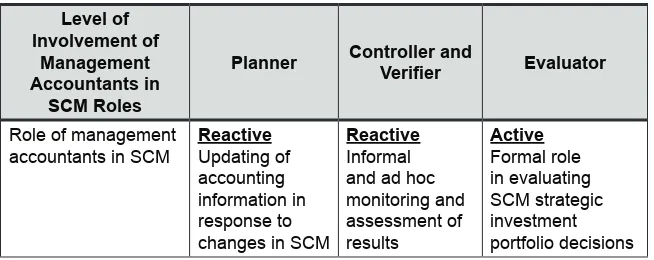

The section discusses the role of management accountants in facilitating SCM processes by comparing the framework suggested by the SMAs on integrated SCM with evidence from the case firm. In the SMAs discussed previously, management accountants are expected to be actively involved during the design, development and execution of SCM. However, contrary to the SMAs, the results showed that management accountants are not involved in the design and development stages. Nevertheless, management accountants are involved at the execution stage of SCM. Their involvement in SCM at this stage is in one of four capacities, namely, ‘planner’, ‘evaluator’, ‘controller’ and ‘verifier’. Contrary to Rajamanoharan (2007) who found that the role of management accountants in facilitating Six Sigma processes varies from being proactive to reactive, the results for both case firms showed that the level of involvement of management accountants in SCM varies from being active to reactive in each of the four capacities (Table 3).

Table 3: Level of the Involvement of Management Accountants

Level of Involvement of

Management Accountants in

SCM Roles

Planner Controller and Verifier Evaluator

Role of management

accountants in SCM Reactive Updating of

accounting information in response to changes in SCM

Reactive

Informal and ad hoc monitoring and assessment of results

Active

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

As indicated in Table 3, management accountants as ‘planners’ are mainly “reactive” by merely responding to the changes in environmental conditions and subsequently updating the plans. Meanwhile, as ‘controllers’ and ‘verifiers’, they are also “reactive” in their informal and ad-hoc monitoring of the results as well as in assessing the accuracies of accounting information proposed by the non-accountants on certain projects. By contrast, the more active role of management accountants as ‘evaluators’ is noted. As ‘evaluators’, they assume a more formal role, particularly when their input is highly regarded in approving strategic capital investment portfolio decisions for SCM purposes.

Although support was provided for the traditional bookkeeping and supportive roles of management accountants in SCM processes, the majority of the case participants raised the issue of the tasks being exclusively performed by management accountants. The views of one of the interviewees highlighted the usual practice of assigning accounting tasks to non-accountants.

The target costing technique that we used under cost planning is mostly done by the engineers.

Despite this concern, the contribution of management accountants to SCM is still valued. For instance, when asked to rate the importance of management accountants to SCM from 1 to 10 (1 being the least important and 10 being the most important), a manager at the Finance and Accounts Department replied: ‘If you talk in terms of numbers, such as “1” being not so important and “10”being very important, I would give a rating that is not less than 7’.

CONCLUSION

more active participation and contribution by management accountants are still required. Thus, this study concurs with previous research (see Rajamanoharan, 2007) that despite a plausible association and a strong call for the integration of MA and other management disciplines (including SCM), management accountants still play a limited role in SCM. Instead of demonstrating essential roles in facilitating SCM, management accountants merely play a supportive role. In particular, they are still viewed as traditional ‘number crunchers’ rather than business partners who can offer valuable accounting perspectives on facilitating SCM success. However, the absence of active involvement of management accountants in SCM did not affect the success of SCM in this study. The results show that non-accountants who have little background in MA are viewed as sufficiently competent in undertaking several of the MA roles in SCM. This finding is consistent with extant views on the limited role of management accountants in implementing MA practices (Rajamanoharan, 2007; Birkett & Poullaous, 2001; Abdul Rahman, 1993).

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

REFERENCES

Abdullah, R., Maharjan, K. L., & Tatsuo, K. (2008). Supplier development framework in the Malaysian automotive industry: Proton’s experience.

International Journal of Economics and Management, 2(1), 29-58.

Abdul Rahman, I. K. (1993). Privatisation in Malaysia with Special Reference to Changes in Accounting System. Unpublished doctoral thesis, University of Hull, England.

Alvarenga, C. A. (2014). The operations centered CFO: Reinventing the role of finance in supply chain management. Corporate Finance Review, January/ February 2014, 16-23.

Bastl, M, Grubic, T, Templar, S., Harrison, A. & Fan, I. (2010). Inter-organisational costing approaches: the inhibiting factors. The International Journal of Logistics Management, 21(1), 65-88.

Berry, T., Ahmed, A., Cullen, J. Dunlop, A., Seal, W., Johnston, S. & M. Holmes. (1997). The consequences of inter-firm supply chains for management accounting. Financial Management. 75(10), 74-75.

Birkett, W. & Poullaos, C. (2001). From accounting to management: A global perspective, In IFAC (Financial Management Accounting Committee) (ed) A Profession transforming: From Accounting to Management, New York, 1-20.

Borges, M. A. V. (2015). An evaluation of supply chain management in a Global perspective. Independent Journal of Management & Production, 6(1), 1-29.

Boute, R, Bruggeman, W & Vereecke, A. (2014). Cost management in the supply chain: An integrated approach – Part 1. Cost Management, November/ December 2014, 11-15.

Carter, C. R., Rogers, D. S. & Choi, T. Y. (2015). Toward the theory of the supply chain. Journal of Supply Chain Management, 51(2), 90-97.

Chenhall, R. H. (2008). Accounting for the horizontal organization: A review essay.

Accounting, Organizations and Society, 33(4/5), 517-550.

Cullen, J. (2009), Supply Chain Management Accounting. Management Accounting Guideline, Certified Management Accountants Canada / American Institute of Certified Public Accountants US / Chartered Institute of Management Accountants UK.

Cullen, J., Berry, A. J., Seal, W., Dunlop, A., Ahmed, M., & Marson, J. (1999). Interfirm supply chains: the contribution of management accounting.

Management Accounting, 77(6), 30-32.

Cullen, J., & Metcalf, D. (2006). Supply-chain accounting. Financial Management, 27.

Denzin, N. K., & Lincoln, Y. S. (2008). Strategies of Qualitative Inquiry (3rd ed.). Thousand Oaks, CA: Sage.

Gunasekaran, A., Patel, C., & McGaughey, R. E. (2004). A framework for supply chain performance measurement, International Journal of Production Economics, 87(3), 333-347.

Hiromoto, T. (1988). Another Hidden Edge: Japanese Management Accounting.

Harvard Business Review, 66(4), 22-25.

Institute of Management Accountants (IMA), (1999). Statement on Management Accounting: Implementing integrated supply chain management for competitive advantage. New Jersey.

Institute of Management Accountants (IMA), (1999). Statement on Management Accounting: Tools and techniques for implementing integrated supply chain management. New Jersey.

International Federation of Accountants (IFAC), (1998). International Management Accounting Practice Statement: Management accounting concepts. New York.

Institute of Management Accountants (IMA). (2008). Managing the total costs of global supply chains. Retrieved from http://www.imanet.org.

Joyce, W. B. (2006). Accounting, purchasing and supply chain management, Supply Chain Management: An International Journal, 11(3), 202–207.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

Maykut, P. S., & Morehouse, R. (1994). Beginning Qualitative Research: A Philosophic and Practical Guide. London: Falmer Press.

Mentzer, J. T., DeWitt, W., Min, S., Nix, N. W., Smith, C. D., & Zacharia, Z. (2001). Defining supply chain management. Journal of Business Logistics, 22(2), 1-26.

Miles, M. B., & Huberman, A. M. (1994). Qualitative Data Analysis: An Expanded Sourcebook (2nd ed.). Thousand Oaks, CA: SAGE Publications.

Ou, C. S., Liu, F. C., Hung, Y. C., & Yen, D. C. (2010). A structural model of supply chain management on firm performance. International Journal of Operations & Production Management, 30(5), 526-545.

Pitingolo, E. D. (2012). Management accounting and green supply chains: Identifying the problem. Journal on GSTF Business Review, 1(4), 25-30.

Rajamanoharan, I. D. (2007). The impact of the implementation of Six Sigma on performance measurement systems and the role of the accountant: case study evidence from firms based in Malaysia. (Unpublished doctoral dissertation). University of Exeter, UK.

Ramos, M. M. (2004). Interaction between management accounting and supply chain management. Supply Chain Management: An International Journal,

9(2), 134-138.

Simchi-Levi, D., Kaminsky, P. & Simchi-Levi, E. (2003). Designing and managing the supply chain: Concepts, strategies and case studies (2nd Ed.). New York:

Irwin/McGraw-Hill.

Sohal, A. S., Power, D. J., & Terziovski, M. (2002). Supply chain management in Australian manufacturing – two case studies. Computers & Industrial Engineering, 43(1-2), 97-109.

Strauss, A. & Corbin, J. (1998). Basics of qualitative research: techniques and procedures for developing grounded theory. London: Sage.

Yasin, M. M., Bayes, P. E. & Czuchry, A. J. (2005). The Changing Role of Accounting in Supporting the Quality and Customer Goals of Organizations: An Open System perspective. International Journal of Management, 22(3), 323-331.

ABSTRACT

The importance of new product development is observed in recent research on dynamic capabilities and target costing (TC). With established concepts from literature on dynamic capabilities and TC, we examine possible path-dependent conflicts in introducing TC to an organization using a traditional western product design approach. This study describes the attempt to add TC to a traditional stage-gate (SG) product development process. Implementing TC as a separate tool in an SG model raises the possibility that the sequential and rigorously “gated” design process would be in conflict with the iterative and multifunctional nature of TC. We find that conflict exists between the SG method and TC. This finding is consistent with criticisms on SG raised in literature. These criticisms include limitations on learning because of the truncation of sub-projects without iterations in TC. Moreover, we support the finding of a previous study that extremely rigorous gate evaluations reduce flexibility in the development system. We connect this previous study’s observations with the concept of dynamic capabilities to make our analysis highly granular and to highlight the aspects of TC that are in conflict with SG-type design processes.

Keywords:cost reduction, target costing, product development, process development, dynamic capability

t

aRgetc

osting in as

tage-g

ateD

esigns

ystemJan Alpenberg1, Jeton Alku1, Judita Rashiti1, Paul Scarbrough2

1School of Business and Economics Linnaeus University, Sweden 2Goodman School of Business

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

INTRODUCTION

Increased competition has increased the interest in product design. Several studies (i.e. Dannels, 2002; Marsh & Stock, 2003; Verona & Ravasi, 2003; Prieto, Revilla & Rodriguez-Prado 2009) have explored dynamic capabilities in product development and design. The authors argued that product development is an essential function by which a company can ‘create, integrate, recombine and shed resources and capabilities’ (Prieto, Revilla & Rodriguez-Prado, 2009). Dynamic capabilities comprise a set of variables that shape product development competencies.

A design method that has been gaining increased attention because of increased competition is target costing (TC) (Clifton, Bird, Albano & Townsend, 2004). Given that the performance, quality and costs of a product are believed by many to be determined at the design phase (Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997; Dekker & Smidt, 2003; Olhager, 2013), TC development is perceived as a strategic activity that is critical to a company’s survival.

The bulk of our understanding of TC originates from Toyota in Japan, where a method for strategic cost management emerged as a means to control costs during the early part of the product development phase (Kee, 2010; Afonso, Nunes, Paisana & Braga, 2008; Swenson, Ansari, Bell & Kim, 2003; Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997; Ellram, 2000; Kato, 1993; Kato, Böer & Chee, 1995). Most variations of TC integrate cost control in the product development process by aligning costs with customer requirements and the cost structure requirements of the company (Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997; Ibusuki & Kaminski, 2007). The aim is to control costs constantly during product development, starting from a concept to the finished product, by involving large portions of the value chain in a nonlinear manner (Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997; Nicolini, Tomkins, Holti, Oldman & Smalley, 2000; Zengin & Ada, 2010).

SG divides the new product development process into stages and meters progress from stage to stage by imposing decision gates. The stages are linear and sequential and based on mid-20th century views of the design

process derived from the Taylorist vision of the division between ‘thinking’ and ‘doing’, which was transferred to the product development arena as ‘design versus production’. In this view of product development, design is separated from supplier and production involvement in a series of silos.

Thus, two contrasting approaches to product development exist. These two approaches are recursive and multifunctional TC and linear and siloed SG. The dynamic capabilities required in these two approaches appear to be different and possibly mutually exclusive.

This study describes how TC is utilised in the SG product development process in a company called CEHaul to reveal the role of dynamic capabilities in the two contrasting approaches.

LITERATURE REVIEW

Previous studies have revealed the importance of adapting to rapid social change through dynamic capabilities, that is, to integrate, build and reconfigure internal and external skills (Tecce, Pisano & Shuen, 1997). The need to develop the ‘dynamic’ aspect of interactions with the environment has dominated recent research (i.e. Wang & Ahmed, 2007; Prieto, Revilla & Rodriguez-Prado, 2009). Alpenberg and Scarbrough (2013) revealed the significant effect of dynamic capabilities on the performance results of TC implementation and established the validity of the underlying concept that dynamic capabilities are potentially important in understanding TC. In the following sections, we draw upon previous research and present the conceptual pillars that frame this field research.

Product Development Process

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

product development (Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997). According to Ibusuki and Kaminski (2007), the product development process also consists of three steps, namely, concept, product and process development, in which each step consists of various measures. This description was supported by Cooper and Kleinschmidt (1987 & 1988) and Cooper, Edgett and Kleinschmidt (2002). These descriptions are derived from the mid-20th century Western

understanding of the product design process and contain path-dependent knowledge. Meanwhile, TC is developed with a different understanding of the product development process and embodies a different set of beliefs about the process.

Stage-gate (SG) Approach

The dominant approach for product development in the west is SG (Cooper & Kleinschmidt, 1987, 1988; Cooper, Edgett & Kleinschmidt,, 2002; Cooper, 1990). Companies that use rigorous SG evaluations enhance their product development efforts by improving performance, reducing new product cycle time, enhancing efficiency and introducing discipline. The SG process is a method of exerting control on product development (Cooper, 1994, 2001; Cooper, Edgett & Kleinschmidt, 2002).

Target Costing (TC) Process

Versions of the TC process have been documented by only a few authors, who have described TC in several ways (i.e. Ax, Greve & Nilsson, 2008; Burrows & Chenhall, 2012; Yazdifar & Askarany, 2012). Our primary in-depth understanding of the process is based on Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross and Zampino (1997) and Cooper and Slagmulder (1999). Other authors, such as Ellram (2006), Everaert, Loosveld, Van Acker, Schollier and Sarens (2006), Ibusuki and Kaminski (2007), Loosveld (2003), Hamood, Omar and Sulaiman (2013) and Kobayashi (2014), subsequently focused on several TC characteristics.

An aspect of TC indicates that the cost structure is determined during product development. The total cost in the entire life cycle is considered before the product is manufactured (Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997). This consideration is important because approximately 85% of the total life cycle cost is determined by market research, product design and product development (Atkinson, Kaplan, Matsumura & Young, 2012; Cooper & Chew, 1996).

To achieve the ‘target cost’, engineers, marketers and product developers analyse the factors that affect product cost to establish means to reduce cost without reducing product function and quality (Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997). This main method is referred to as value engineering (VE). TC and VE complement each other. TC identifies the target cost, and VE with quality function deployment (QFD) identifies opportunities for cost reduction (Akau & Mazur, 2003; Afonso, Nunes, Paisana & Braga, 2008; Akhbari, Alpenberg, Scarbrough & Wennberg, 2012; Ansari, Bell, Cypher, Dears, Dutton, Ferguson, Hallin, Marx, Ross & Zampino, 1997; Zengin & Ada, 2010).

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

component-level TC, describes the involvement of suppliers and the transfer of certain cost claims to them. Usually, the steps and tasks are repeated several times before the desired result is achieved, which means that the process is highly effective when several activities in the three steps are executed in parallel.

Dynamic Capabilities in Target Costing (TC)

We draw from the idea of Tecce, Pisano and Shuen (1997) that dynamic capabilities are the ultimate source of competitive advantage and are elements to enhance the existing resource configuration in a demanding environment (i.e. Tecce, Pisano & Shuen, 1997; Eisenhardt & Martin, 2000; Knight and Collier, 2009). The essence of dynamic capabilities is that they reside in the potential to change resources, routines and competences (Prieto, Revilla & Rodriguez-Prado, 2009). They are defined as ‘the organizational and strategic routines by which firms achieve new resource configurations as markets emerge, collide, split, evolve and die’ (Tecce, 2007; Eisenhardt & Martin, 2000; Tecce, Pisano & Shuen, 1997). Simplified, dynamic capabilities are a set of specific and identifiable processes, such as product development and strategic decision making (see Eisenhardt & Martin, 2000).

Dynamic capabilities in the product development process can be divided into three parts, namely, knowledge creation, knowledge integration

and knowledge re-configuration (Tecce, Pisano & Shuen, 1997, Tecce, 2007; Prieto, Revilla & Rodriguez-Prado, 2009). Knowledge generation (KG)

refers to developing specific activities to identify and solve problems and knowledge for the development and launch of new products. Knowledge integration (KI) refers to combining the knowledge and skills of individuals from various departments to design and develop a specific product; knowledge is revealed and shared as part of the product development process. Knowledge re-configuration (KR) is the ability to feel the need for reorganization and combination of knowledge or patterns that are embedded in products and activities by establishing flexible relationships and teams.

that managers play a key role because they bring external knowledge about resources and transfer such knowledge to new internal procedures to develop new and sustainable dynamic performances. Easterby-Smith and Prieto (2008) claimed that dynamic capabilities and the firm’s abilities for knowledge management are connected. In a later study, Akhbari, Alpenberg, Scarbrough and Wennberg (2012) and Alpenberg and Scarbrough, (2013) found that the adoption of TC by Swedish listed companies is influenced by dynamic capabilities. The authors also found a partially positive correlation between dynamic capabilities and performance results when TC is used.

RESEARCH PROCESS

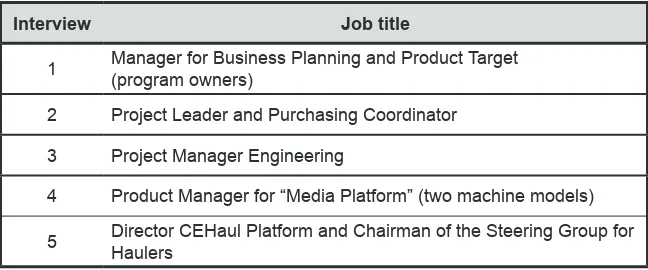

In this study, we adopted an individual case study research design, which is desirable when studying social sub-systems, such as institutions and organizations (Scapens, 1990). Case studies should be characterized by a few observation units and many variables to be able to describe, understand and explain what occurs within an organization (Yin, 2007). Interviews were the primary source of information in this study because this method creates the opportunity to follow up with additional questions for clarification (Yin, 2007; Bryman & Bell, 2005). Direct observations of daily activities and project meetings held by the project manager and sub-project leader were also conducted. During these meetings, we observed a large number of the participants in their work setting. Furthermore, we reviewed corporate documents to confirm the issues that emerged during the interviews (Patel & Davidson, 2003; Yin, 2007). We were given access to documents, such as TC training workshop materials, organizational chart, company brochures and the ‘Global Development Process’ (GDP) guide of the parent company.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

Table 1: Individual Interviewees at CEHaul

Interview Job title

1 Manager for Business Planning and Product Target (program owners)

2 Project Leader and Purchasing Coordinator

3 Project Manager Engineering

4 Product Manager for “Media Platform” (two machine models)

5 Director CEHaul Platform and Chairman of the Steering Group for Haulers

We used unstructured and semi-structured interviews. Unstructured interviews were used with the contact person to obtain a thorough understanding of the situation at CEHaul. Semi-structured interviews were used for the rest of the interviewees to obtain deep and detailed information. The interview guide addressed various questions, including each employee’s role in the TC process and the importance of skills and knowledge. All interviews were recorded and transcribed. Between interviews, we conducted direct observation of formal meetings held by two of the project managers. These meetings are usually held every two weeks and handle small sub-projects for cost savings. Each meeting is attended by about six individuals from various departments.

CASE DESCRIPTION: CEHAUL

The market for articulated haulers is mature, and products across competitors have become increasingly alike. CEHaul is one of the main players in the global market. It faces tough competition from Caterpillar and Komatsu. CEHaul manufactures all parts of its articulated haulers and performs the final assembly. Additional activities include product development and support for after-sales service, IT, personnel, finance, procurement and communications and global marketing.

For a long time, the competitive strategy of CEHaul has been to have the best product in the market. In the current and much more mature market, this goal is becoming extremely difficult because all competitive products are similar, and the expertise obtained from extensive experience is widely distributed among competitors. This situation results in extreme demands for quality and functionality when pursuing cost reduction. In addition, regulatory requirements change rapidly. This change entails additional costs for changes in products because of safety or environmental regulations. Product development at CEHaul is significantly influenced by regulatory requirements for emissions. New components are required to meet these requirements, which have influenced the company’s competitive strategy. Given the cost effect of these regulatory requirements, the company’s market price has increased without any added customer value. Meanwhile, customers demonstrate increased price sensitivity while demanding for additional functions and improved quality.

CEHaul attempted to implement TC twice. We report mainly on the second attempt. The first attempt of CEHaul to introduce TC to their already established product development process took place in 2011. The initiative came from CEGroup’s CEO, who challenged the entire organization to improve the profit for each product through cost reduction without reducing quality and functionality.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

According to CEHaul’s Improvement Project Chairman, the first attempt was failed. This failure was partly attributed to the complexity of the TC process. Despite some technical progress in emission reduction, the first TC attempt was a clear failure according to both the project manager and project leaders. The organization never managed to incorporate the new TC routines and informal responsibilities into the pre-existing SG product development process. This inability led to a feeling of lack of responsibility among participants and a feeling that the management control system was unable to support the TC initiative. This sense of confusion ultimately resulted in a situation in which the target cost was not achieved. The project manager and the project leaders at CEHaul realized that a clear process and project model for TC that everyone understands and can follow to create ‘order’ are necessary. The leaders of different subprojects in the cost reduction program at CEHaul highlighted the problems in implementing ideas when they described the situation as follows:

There is no lack of ideas. We have almost too many of them. The problem is how to execute these ideas.

All participants in the second attempt participated in the first failed attempt. The second attempt to introduce TC began in the fall of 2013. Even during the second attempt, a ‘workshop’ was the starting point. The TC process was implemented only once (during the TC workshop) and was directed by the consultants. In the TC workshop, employees from different departments were gathered to put forward improvement and cost reduction ideas. External consultants were hired, and they spent 15 weeks onsite at CEHaul together with the sub-project leaders. During this process, an articulated hauler was disassembled and studied to identify the areas for improvement. The work was performed in cross-functional teams, and several new ideas were obtained.

All ideas were subjected to a strict validation process and eventually resulted in the following four specific project categories.

1. Category 1: Large design changes and system upgrades

3. Category 3: Large improvements of all manufacturing processes throughout the plant

4. Category 4: Renegotiate conditions with suppliers and possibly identify supplier

The project leader expressed his thoughts about the validation process as follows:

The validation process aimed to “wash” all the ideas that had come in. We had two technical experts and the product manager with us during the meetings. For three weeks, we worked extremely hard in the validation process to determine if the ideas would reduce cost and can be implemented.

These projects led to new activities, including altered responsibility for daily routines, in the product development process. The project manager and the project leader summarized the work as follows:

However, the most significant challenge was to improve the product while cutting the cost before it is produced (project manager and project leader).

Product Development Process at CEHaul

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016 develop to indic Each p ‘gates’, prepara model a presente At CEH decision Validat include conform chairma the prod Global

In the f vieweda quality, changes

pment, final cate a particu

hase ends the project ationfor the

assumes a l ed below.

Haul, two im ns are to be tion ensures s subjective m to the req an explains duct right’.

Developm

first phase, as a feasib , lead time s, considera

l developme ular empha

Figure 1

with a ‘gat manageme next ‘gate’ linear,

non-mportant co e made rega s that the p e aspects. V quirements

that valida

ent Proces

pre-study, bility study.

s for produ ableemphas

ent, industr sis on proje

1: Product

te’. Certain ent assures ’and update

recursive p

oncepts in t arding prod products m Verification of the spec ation is to ‘b

ss (GDP): P

work with . This phas uct develop sis is placed

ialization an ect work.

Developm

n stages als that the cr es the proje process. A d

the product ducts; these meet the cus n ensures th cification. T build the rig

Pre-study P

business re se includes pment and don the ear

nd follow-u

ent Phases

so include riteria for t ct’s forecas detailed des t developm two concep stomers’ ne hat products To distingu ght product Phase equirements product p reduction rly phases.

up phases. E

s at CEHau

‘gates’ wit the current st of final d scription of

ent process pts arevalid eeds in thei s, subsystem uish these c

t’,whereas v

s and oppo planning to

of business The most p

Each phase

ul

thin a phas phase are delivery and the differen

s arise when dation and v

ir actual si ms, function

oncepts int verification

ortunities isd improve th s risks. To promising p

9 is intended

e. At these fulfilled in d risks. The nt phases is

n important verification

tuation and ns, or parts ternally, the is to ‘build

done and is he product avoid late projects are 9 d e n e s t . d s e d s , e e Figure 1: Product Development Phases at CEHaul

Each phase ends with a ‘gate’. Certain stages also include ‘gates’ within a phase. At these ‘gates’, the project management assures that the criteria for the current phase are fulfilled in preparation for the next ‘gate’ and updates the project’s forecast of final delivery and risks. The model assumes a linear, non-recursive process.

At CEHaul, two important concepts in the product development process arise when important decisions are to be made regarding products; these two concepts are validation and verification. Validation ensures that the products meet the customers’ needs in their actual situation and includes subjective aspects. Verification ensures that products, subsystems, functions, or parts conform to the requirements of the specification. To distinguish these concepts internally, the chairman explains that validation is to ‘build the right product’, whereas verification is to ‘build the product right’. A detailed description of the different phases is presented below.

Global Development Process (GDP): Pre-study Phase

projects are selected and prepared for the next phase, and the others are either rejected or worked on. The product manager pointed out that

During this phase, we start with the requirements or definitions, which include what we want, what the allowable cost level is, how much it is going to weigh and how profitable it has to be.

This phase is the main entry point for TC or for any goal. Notably, goals must be externally specified. In the past, the main set of goals was the engineering impetus to improve functionality based on the long-standing CEGroup strategy of having the ‘best product’. TC injects customer demands for both functionality and cost at this stage. Introducing these aspects created friction when the TC initiative was implemented because the company had never been considered at this stage previously.

The pre-study phase is one of the main phases to determine the target cost. A corporate decision by top management forced all the units in CEHaul to cut costs by a specified percentage. This percentage goal was mandated as the goal for the TC process at CEHaul. This step differs greatly from the normal TC view, in which the starting point is the market and its needs. Thus, one issue is that participant dedication may not be as great with externally imposed goals based on group needs that do not appear to be connected with the CEHaul employees’ understanding of their market.

Thus, CEHaul uses a hybrid model in which market research is performed to understand and measure customer requirements while the company follows a cost reduction target assigned by the upper management of the CEGroup. The target for cost reduction is broken down by assigning each reduction to a different department that deals with various aspects of the product life cycle. At CEHaul, this strategy is implemented at the pre-study phase. This step affects the structure of CEHaul’s TC process and is significantly different from traditional TC thinking.

AsiA - PAcific MAnAgeMent Accounting JournAl (APMAJ) Vol. 11 no. 1 June 2016

and quality when they reduce cost. However, CEHaul does not seem to use VE for these purposes.

The articulated hauler project leader describes market development by referring to existing products and analysis of trends on the basis of profitability. This definition coincides with ‘physical-attributes-based adjustment’, which is used for products with a functionality that is changing gradually and where physical attributes are based on customer requirements. This situation sets a market price that the company thinks is appropriate based on contact with customers.

At this stage, we observe knowledge generation occurring as the project team looks outward to develop new functions or improve existing functions. Although several teams are cross functional in a limited sense, knowledge generation is fairly narrow in scope. Very little or no knowledge integration or knowledge reconfiguration exists indicated in this phase, which is different from the early stages of TC where all three stages indicate development.

Global Development Process (GDP): Concept Phase

The primary task in this phase is to generate the concept that has the potential to satisfy the requirements of customers. The difficulty in this part of the process is illustrated with the following excerpt from the interview with the product manager.

We might have developed a smart concept but if it doesn’t ‘hit’ the product cost the right way, it does not take off. We need the product to be profitable when it is delivered to the customers. The first phase in which we set the requirements is straightforward, but to balance the different concepts along the requirements is where it gets tricky.

suppliers and manufacturing activities are planned, and the timetable is updated. However, no actual contact with suppliers exists at this point, which is a violation of TC.

To reach the target for cost reduction, CEHaul applies a small measure of VE in the concept phase for components and items. Each component and item are assigned their own target cost, and together, they lead to the cost reduction target. In this step, cost engineers contribute with special tools, such as cost tables. These tables involve detailed cost information on raw materials, purchased components and processes. However, the bulk of the information needed is unavailable but is indicated in later stages because suppliers are not part of this analysis. This limitation exerts negative effects on the CEHaul development process because the company must ‘simulate’ the possible cost reduction by suppliers instead of obtaining help from actual suppliers.

According to the product manager, the process in the concept phase is unpredictable and produces negative effects. The entire TC process was only executed once during the TC workshop with consultants when the cost reduction program began. This is another reason for the weak support in the organization, processes and structure of CEHaul. These deficiencies lead to each task taking longer than necessary, which, according to the project leader, is wasteful and adversely affects the company in the long term when it comes to time-to-market. The tight integration of Japanese

keiretsu members as suppliers and customers is part of the TC process in Japan. However, this condition is usually unnoticed by western observers. The use of TC by CEHaul appears to suffer from the lack of participation of all suppliers.