ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 758

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

The Impact of Information and Communication Technologies

on the Competitiveness: Evidence of Manufacturing SMEs in

Aguascalientes, Mexico

LUIS AGUILERA ENRÍQUEZ

Faculty of Management and Economic Science, Autonomous University of Aguascalientes, Mexico

Email: [email protected]

HÉCTOR CUEVAS-VARGAS

Faculty of Management and Economic Science, Autonomous University of Aguascalientes, Mexico

Email: [email protected]

MARTHA GONZÁLEZ ADAME

Faculty of Management and Economic Science, Autonomous University of Aguascalientes, Mexico

Email: [email protected]

Abstract

The adoption of Information and Communication Technologies (ICTs) plays a key role in developing business strategies that enable businesses, especially small and medium enterprises (SMEs), improving their competitiveness in a globalized, changing and competitive market, as the one they face today. That is why this empirical research of explanatory type was aim to analyze the impact of ICT on the competitiveness of manufacturing SMEs of the state of Aguascalientes, México. Firstly, the scales to measure the use of ICTs and competitiveness were identified, then they were subjected to a Confirmatory Factor Analysis (CFA) through the method of maximum likelihood, which have both reliability and validity. Information obtained from 200 manufacturing SMEs was treated statistically through the Structural Equation Modeling (SEM), and the tested hypotheses results allow us to infer that ICTs impact positively and significantly on the financial performance, the costs reduction, the use of technology and on the competitiveness of these kinds of businesses.

Key Words: ICTs, Financial Performance, Costs Reduction, Technology Use, Competitiveness, SEM.

Introduction

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 759

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

According to Stern (2002), ICTs have become a catalyst for organizational processes, becoming support tools for business management, leveraging at building strategies aimed at competitiveness and innovation, and generating sustainability of companies over time. In such situation, if SMEs claim to have acceptable levels of competitiveness and growth, they require their production processes to be controlled, administered and enforced by appropriate ICTs strategies, otherwise, their customers will likely switch suppliers (Aguilera, Colin & Hernandez, 2013).

To Ashrafi & Murtaza (2008), ICTs refer to a wide range of computerized information communication technology; which include products and services such as desktop computers, laptops, mobile devices, wired or wireless intranet, business productivity software, such as text editor, spreadsheet, business software, data storage and network security, among others. According to Buckley, Pass & Prescott (1988), a firm is competitive if it has the ability to manufacture and deliver products and services of superior quality and low cost compared to its national and international competitors. Therefore, competitiveness can be understood as a synonym of performance, express in terms of profitability in the long term and in terms of ability of the firm to compensate employees and provide superior returns to owners of the company. In this sense, some studies that address the implications of ICTs on competitiveness began in the mid-eighties, in which several case studies described how companies were able to improve their market share and profits by using innovative ICTs (Ives & Learmonth 1984; McFarlan, 1984; Porter & Millar, 1985; Rackoff, Wiseman & Ullrich, 1985), so within these case studies it is suggested that ICTs could be used to create entry barriers, increase switching costs, change the basis of competition, reduce the bargaining power of suppliers, and create new products or businesses.

Currently, ICTs are universally recognized as an essential tool in improving the competitiveness of the economy in a country, and also have significant effects on the productivity of companies (Olviera & Martins, 2011). Therefore, it is essential to promote business management in organizations, the use of new

ICTs, particularly in SMEs, as this strategy will enable them to achieve competitive success (Donrrosoro et

al., 2001; Llopis, 2000). Similarly, it is important to note that while it is true that studies illustrate instances where the adoption of ICTs by enterprises have been successful, there are others that evidence barriers and obstacles which make implementation difficult (Arendt, 2008; Modimogale & Kroeze, 2009), which occurs in the case of MSMEs, for this reason it is of great value to provide empirical evidence of this research for both decision-makers and for public policy designers. Moreover, it is noteworthy that most of the empirical studies presented in the current literature on the use of ICTs and their impact on competitiveness have focused on large companies in highly developed countries, and few studies of SMEs in developing countries as is the case of Mexico. Therefore, an additional contribution of this study is the application of a methodology that consists in completely testing the theoretical model by checking their hypotheses through Structural Equation Modeling of first and second order.

That is why this study was aimed to analyze the impact of ICTs on the competitiveness of manufacturing SMEs in Aguascalientes, Mexico. In this sense, the study was done in the state of Aguascalientes with a sample of 200 SMEs during the period from September to November 2014. The results will provide empirical evidence in the context of the Mexican manufacturing industry, provided that SMEs shows the need to establish technologies to activate their business, and thus improve their competitiveness in the market. Therefore, the development of the research model of the present study describes the relationship of ICTs with each of the dimensions that competitiveness was measured, these being, financial performance, cost reduction and the use of technology, as well as the overall competitiveness of SMEs.

Literature Review

ICTs Relationship with Financial Performance

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 760

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

in information technology and digital platforms are critical enablers of organizational competence and the performance of the company. Similar research has shown that investments in information technology and skills through ICTs are associated with higher productivity, customer satisfaction, organizational capacity and the performance of companies (Bhatt & Grover, 2005; Brynjolfsson & Hitt, 1996; Mithas, Ramasubbu, Krishnan & Sambamurthy, 2005).

As for the empirical evidence, it has been found that ICTs positively impact in the financial performance of companies, as shown by Menéndez, López, Rodriguez & Francesco (2007), in their study carried out with Spanish companies, who found that process innovations linked to the use of new technology, particularly of ICTs in relationship with customers and suppliers, positively affect the performance of companies. In this sense, according to Esselaar, Stork, Ndiwalana & Deen-Swarray (2008) organizations currently implementing ICTs in their production processes can be benefited with a better level of productivity and, therefore, it can be assumed that their level of profitability will be acceptable, because they have substantial improvements in the management of information technology. Thus, under these perspectives the first hypothesis arose:

H1: The greater the use of ICT, the greater the level of financial performance of SMEs.

ICTs Relationship with Costs Reduction

There is theoretical evidence showing that ICTs are a strategic resource that helps companies find new opportunities in the market, with low cost and a high probability of success (Shin, 2007). In this sense, empirical evidence of the relationship of ICTs on reducing costs has been found, as evidenced by Cachon & Fisher (2000) in their study, indicating that use ICTs in logistics leads to reducing costs and improving the flow of goods through the supply chain.

For Peirano & Suarez (2006) by ICTs enabling better coordination tasks between agents, reducing dead time and other costs associated with business relationships and its environment, can help improve business efficiency and the economic system general. Similarly, in a qualitative study conducted with MSMEs of Guanajuato, Rios, Toledo, Campos & Alejos (2009) found that the use of ICTs can help them reduce costs, by improving operational efficiency, replacing manual processes and improving management information of customers and suppliers, enabling them to generate additional income using the Internet to sell their products and services, and thereby reach new customers and cover or increase their coverage in the current market and new markets. Thus, under these perspectives the second hypothesis is proposed:

H2: The greater use of ICT, the greater the level of cost reduction by SMEs.

ICTs Relationship with the Use of Technology

Customization of ICTs applications and infrastructure related to the specific production processes of the plant, such as the manufacture and assembly of the final product, is a complex process and often inimitable by competition (Bardhan, Whitaker & Mithas, 2006). For this reason, it is essential that SMEs succeed in developing these types of benefits from technology products, processes and / or equipment.

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 761

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

As for the empirical evidence it has been found that there is a positive relationship of ICTs with the use of technology, such as Black & Lynch (2001), in their research by studying the relationship between productivity and the use of computers in production facilities, found that the greater the use of computers by non-management workers, the greater productivity obtained at the worksite. Meanwhile, López (2004) in his research indicates that the investment and use of ICTs, the level of implementation and the increased use of these technologies will lead to sustainable improvements in productivity, to a greater extent in SMEs and in sectors with low levels of implementation. In this regard and under the above arguments, the third hypothesis is stated:

H3: The greater the use of ICT, the higher the level of technology use by SMEs.

ICTs Relationship with Competitiveness

Similarly, it has been found that the adoption and use of ICTs represent the fundamentals of competitiveness and economic growth for companies and countries that are able to exploit them (Higon, 2011; Ollo-López & Aramendia-Muneta, 2012; Steinfield, LaRose, Chew & Tong, 2012; Vehovar & Lesjak, 2007).

Therefore, it is essential that SMEs have an adequate strategic plan defining the objective of ICTs, as stated by Bhatt & Grover (2005), despite being the basic technological infrastructure for the organization, it is not triggered at a competitive advantage if it is not supported by a strategic plan defining the objective of ICTs. Thus, the use of ICTs is considered a strategy that allows companies to improve competitiveness in their particular interest to regenerate their work systems (Bardhan et al., 2006; Diaz-Chao & Torrent-Sellens, 2010).

Empirical evidence demonstrating the positive relationship that ICTs have on the competitiveness of enterprises has also been found, as in the case of a study conducted with 400 MSMEs in Aguascalientes,

Mexico, Maldonado et al. (2010) found that MSMEs with greater use of ICTs gain greater performance, so

it can be confirmed that ICTs represent a great opportunity for companies, especially SMEs, to improve their competitiveness level. In the same order of ideas, Aguilera et al. (2013) in their study of SMEs in Aguascalientes found that ICTs have a positive impact on the competitiveness of SMEs, since such companies give importance on the effectiveness of their administrative and financial control, and therefore the adoption of appropriate technological tools allow them to count on systems to precisely control finances, as well as any costs generated in operations.

On the other hand, Cuevas-Vargas, Aguilera, González & Servin (2015) in their study with Mexican SMEs found that that ICTs have a positive and highly significant relationship with the competitiveness of these types of businesses, finding no evidence that the size or age of these kind of organizations influence over the impact on the competitiveness using ICTs, and that the use of ICTs for document exchange with the firms’ suppliers have enable them to streamline their processes and have higher attentiveness and a better relationship with their customers, largely achieving satisfaction to these requirements, delivering products and/or services of higher quality, as long as the use of ICTs is accompanied by an appropriate implementation strategy that defines the objective of ICTs (Bhatt & Grover, 2005), and by educating and creating a society possessing knowledge helping correctly the use of ICTs which will allow the firms to improve their competitiveness. Thus, under these arguments the fourth hypothesis arises:

H4: The greater the use of ICT, the higher the level of competitiveness of SMEs.

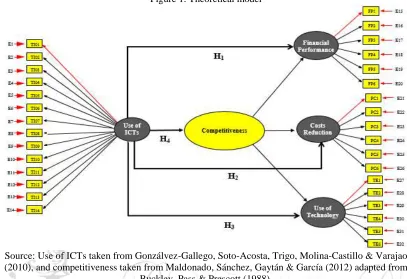

Theoretical Model

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 762

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

Figure 1. Theoretical model

Source: Use of ICTs taken from Gonzálvez-Gallego, Soto-Acosta, Trigo, Molina-Castillo & Varajao (2010), and competitiveness taken from Maldonado, Sánchez, Gaytán & García (2012) adapted from

Buckley, Pass & Prescott (1988).

Methodology

Sample Design and Data Collection

Empirical research was performed using an explanatory cross sectional quantitative approach through SEM. The use of ICTs and their impact on the competitiveness of manufacturing SMEs were analyzed. The base instrument of this research consists of 32 items measured on a 5 point Likert scale, which ranks from 1=total disagreement to 5=total agreement in the case of competitiveness and 5=low importance to 5=high importance for the case of the ICTs Variable, which was applied to managers of manufacturing SMEs in the state of Aguascalientes, Mexico.

Table 1. Research Design

Characteristics Research

Population 435 Small and medium-sized enterprises

Geographical area The state of Aguascalientes, México

Object of study Manufacturing SMEs from 11 to 250 employees

Data collection method Personal interviews with Managers

Sampling method Simple random sampling

Sample size 205 SMEs

Sample Error ±5% error, reliability level of 95% (p=q=0.5)

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 763

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

The database provided by the National Statistical Directory of Economic Units INEGI (2015) was taken as reference, where a total of 4,996 manufacturing companies appear to be registered in the state of Aguascalientes until February 5th, 2015, of which 435 of them are SMEs ranging from 11-250 workers. That is why the survey was designed based on the theoretical model, to be answered by managers or owners of SMEs in the manufacturing sector of Aguascalientes, and was randomly applied, yielding a response rate of 97.5% and an error margin of 5%, summing up a total of 200 valid questionnaires, as shown in Table 1, which refers to the research design.

For the preparation of the measuring instrument, two blocks were used, the ICTs block and competitiveness

block. To measure the use of ICTs, the factor adapted by Gonzálvez-Gallego et al. (2010) was considered

and was measured with a scale of 14 items; regarding the measuring of competitiveness, the three factors proposed by Buckley et al. (1988) were taken into account and adapted by Maldonado et al. (2012) and tested in other studies by Aguilera, Cuevas & Hernández (2014) and Cuevas-Vargas, Aguilera & Hernández (2014), of these financial performance was measured with a 6-item scale, purchasing cost reduction was measured with a 6-item scale, and the use of technology was also measured with a 6-item scale.

Reliability and Validity

To evaluate the reliability and validity of the scales, a Confirmatory Factor Analysis (CFA) using the maximum likelihood method through the use of EQS 6.1 statistical software was performed, working the four constructs as first order factors (Bentler, 2005; Brown, 2006; Byrne, 2006). Also, the reliability of the

four proposed measurement scales was evaluated from the Cronbach's Alpha coefficients and the

Composite Reliability Index (CRI) (Bagozzi & Yi, 1988). From the results, all values of the scale exceeded

the recommended level of 0.7 for Cronbach's Alpha which provides evidence of reliability and justifies the

internal reliability of the scales (Hair, Anderson, Tatham & Black, 1999; Nunnally & Bernstein, 1994), as shown in Table 2. Also robust statistical testing was used (Satorra & Bentler, 1988) in order to provide better evidence of statistical adjustments.

Model Adjustment

The adjustments that were used in the model under study were the normed fit index (NFI), the non-normed fit index (NNFI), the comparative fit index (CFI) and the Root Mean Square Error of Approximation (RMSEA) (Bentler & Bonnet, 1980; Hair et al., 1999). It is noteworthy that NFI NNFI and IFC values between 0.80 and 0.89 represent a reasonable adjustment (Segars & Grover, 1993) and an equal value to or greater than 0.90 are good evidence of a good fit (Byrne, 1989; Jöreskog & Sörbom, 1986; Papke-Shields, Malhotra & Grover, 2002). Likewise, RMSEA values below 0.080 are acceptable (Hair et al., 1999; Jöreskog & Sörbom, 1986). Another Index proposed by Bagozzi & Yi (1988) and Hair et al. (1999) is the

S-B X²/df lower than 2.0 which shows a good evidence of the model adjustment. In Table 2 the obtained

results are shown having applied the first order CFA for the ICTs variable, and second order for the competitiveness variable.

Therefore, in applying the CFA of first and second order, it was found that the original model did not present problems of adjustment, since the model has a very good fit to the data with reference to the robust statistics (S-B X² = 803.7067; df= 459; p = 0.000; S-B X² / df= 1.75; NFI = 0.906; NNFI = 0.954; CFI = 0.957; and RMSEA = 0.061), since the values of NFI, NNFI and CFI are above 0.90, S-B X²/df is lower

than 2.0, and the RMSEA is less than 0.08, meaning they are acceptable (Bagozzi & Yi, 1988; Hair et al.,

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 764

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

Table 2.Internal consistence and convergent validity of the theoretical model

Variable Indicator

Standardized Factor Loading Robust t-value Average Factor Loading Cronbach’s

Alpha CRI AVE

Use of ICTs

ICT1 0.935*** 1.000ᵅ

0.962 0.994 0.994 0.927 ICT2 0.914*** 52.895

ICT3 0.951*** 53.956 ICT4 0.959*** 42.465 ICT5 0.973*** 60.776 ICT6 0.951*** 45.093 ICT7 0.956*** 40.582 ICT8 0.977*** 47.417 ICT9 0.960*** 37.947 ICT10 0.983*** 46.758 ICT11 0.984*** 47.430 ICT12 0.982*** 45.263 ICT13 0.975*** 42.472 ICT14 0.975*** 49.582

Financial Performance

(F1)

FP1 0.931*** 1.000ᵅ

0.955 0.984 0.984 0.914 FP2 0.956*** 25.928

FP3 0.975*** 22.032 FP4 0.975*** 22.323 FP5 0.964*** 18.482 FP6 0.933*** 20.455

Costs Reduction (F2)

CR1 0.785*** 1.000ᵅ

0.907 0.967 0.966 0.828 CR2 0.882*** 14.754

CR3 0.922*** 14.021 CR4 0.953*** 13.450 CR5 0.933*** 15.181 CR6 0.971*** 14.302

Use of Technology (F3)

UT1 0.909*** 1.000ᵅ

0.962 0.987 0.987 0.927 UT2 0.954*** 40.186

UT3 0.985*** 34.007 UT4 0.987*** 32.878 UT5 0.975*** 28.669 UT6 0.964*** 29.807

Competitiveness

F1 0.606*** 5.023

0.707 0.743 0.752 0.505

F2 0.729*** 4.728

F3 0.786*** 5.301

S-B X²= 803.7067; df= 459; (S-B X²/df)= 1.75; P= 0.000; RMSEA= 0.061 NFI= 0.906; NNFI= 0.954; CFI= 0.957

ᵅ = Parameters constrained to this value in the identification process CRI= Composite Reliability Index; AVE= Average Variance Extracted Index

Significance level= *** = p < 0.001; ** = p < 0.05

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 765

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

(1994). The composite reliability represents the extracted variance between the group of observed variables and the fundamental construct (Fornell & Larcker, 1981). Generally, a Composite Reliability Index (CRI) greater than 0.60 is considered desirable (Bagozzi & Yi, 1988), in our research, this value is greatly exceeded. The Average Variance Extracted index (AVE) was calculated in the same way for each of the constructs, resulting in an IVE greater than 0.50 (Fornell & Larcker, 1981) in each and every one of the factors.

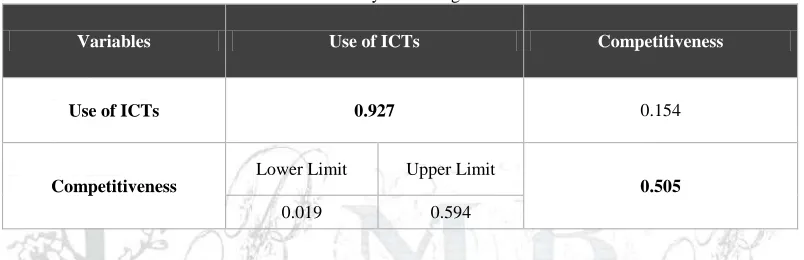

With regard to the evidence of discriminant validity, the results obtained are presented in Table 3, where the measurement is provided in two ways: the first one, the confidence interval test proposed by Anderson & Gerbing (1988), which stablishes that with a 95% reliability interval, none of the latent factorial individual elements of the correlation matrix has the value 1.0. The second one, the extracted variance test proposed by Fornell & Larcker (1981) between the pair of constructs is greater than its corresponding AVE. Therefore, based on these criteria, it can be concluded that the various measurements performed in this investigation demonstrate enough evidence of reliability and convergent discriminant validity of the adjusted theoretical model.

Table 3. Discriminant validity measuring of the theoretical model

Variables Use of ICTs Competitiveness

Use of ICTs 0.927 0.154

Competitiveness

Lower Limit Upper Limit

0.505

0.019 0.594

As it can be seen, The diagonal numbers (in bold) represent the Average Variance Extracted (AVE), whereas below the diagonal, it is shown the correlation estimation of the factors with a confidence interval of 95%; and above the diagonal, the results for the Extracted Variance Test are shown through the correlation square between each of the factors.

Results

For the statistical results of the research hypotheses, SEM was performed, it is understood as multivariate techniques combining aspects of multiple regression (examining dependence relationships) and factor analysis (representing immeasurable concepts with multiple variables) to estimate a series of interrelated dependence relationships simultaneously (Hair et al., 1999), using the statistical software EQS 6.1, from the first and second order application of CFA (Bentler, 2005; Byrne, 2006; Brown, 2006), with the same variables to check the model structure and get the results that allow to verify the raised hypothesis presented in Table 4.

With regard to the first hypothesis H1, the results presented in Table 4 (β = 0.392, p <0.001), indicate that

ICTs have positive and significant effects on financial performance, therefore, the H1 is accepted; regarding

the second hypothesis H2, the results obtained (β = 0.463, p <0.001), indicate that ICTs have positive and

significant effects in reducing purchasing costs, therefore, the H2 is accepted; as for the third hypothesis H3

the results obtained (β = 0.515, p <0.001), indicate that ICTs have positive and significant effects on the use of technology, therefore, the H3 is accepted; Finally, regarding the last hypothesis H4, the results obtained

(β = 0.764, p <0.001), indicate that ICTs have positive and significant effects on the competitiveness of

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 766

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

Table 4. Structural Equation Modeling results from the theoretical model

Hypothesis Path Standardized

Path Coeficients Robust

t-value R Square

H1: Higher level of ICTs, higher level of financial performance

Use of ICTs → Financial

performance 0.392*** 5.859 0.154

H2: Higher level of ICTs, higher level of costs reduction

Use of ICTs → Costs

reduction 0.463*** 6.691 0.214

H3: Higher level of ICTs, higher level of use of technology

Use of ICTs → Use of

technology 0.515*** 8.068 0.265

H4: Higher level of ICTs, higher level of competitiveness

Use of ICTs →

Competitiveness 0.764*** 6.872 0.583

S-B X²= 795.9817; df= 458; (S-B X²/df)= 1.737; p= 0.000; RMSEA= 0.061 NFI= 0.907; NNFI= 0.955; CFI= 0.958

*** = p < 0.001; ** = p < 0.05

Discussion

Regarding the relationship of ICTs and financial performance, the results indicate that ICTs have a significant positive impact on the financial performance of the manufacturing SMEs, therefore, the results

obtained by Menendez et al. (2007) are corroborated, who found that the innovations in processes linked to

the use of new technologies, particularly of ICTs in relations with customers and suppliers, positively affect

the performance of companies and likewise coincide with the findings by Esselaar et al. (2008), since the

organizations currently implementing ICTs in their production processes may benefit with a better level of productivity, therefore it can be assumed that their level of profitability will be acceptable by presenting substantial improvements in management of information technology.

With regard to the relation of ICTs and cost reduction, the results indicate that ICTs have a positive and significant impact on reducing the cost of purchases made by SMEs, which are themselves consistent with the findings obtained by Cachon & Fisher (2000); Peirano & Suarez (2006); and Rios et al. (2009), who found that the use of ICTs can help SMEs and MSMEs reduce costs and improve the flow of goods through the supply chain. On the relation of ICTs with the use of technology, the results indicate that ICTs have a positive and significant impact on the use of technology by SMEs, therefore, corroborating the results obtained by Aguilera-Enriquez et al. (2011) given that SMEs need to modernize their management and production through the use of technology and the inclusion of systems to streamline their functions and to become more productive and competitive; reaffirming the findings of Black & Lynch (2001) stating that the greater the use of computers by non-management workers, the greater the productivity obtained; and agreeing with findings by López (2004), noting that probably the investment and the use of ICTs, the level of implementation and the increased use of these technologies will lead to sustainable improvements in the productivity of organizations.

And as for the relationship of ICTs and competitiveness, the results indicate that ICTs have a positive and significant impact on the competitiveness of manufacturing SMEs in Aguascalientes, thus confirming the results obtained by Maldonado et al. (2010), who found that MSMEs with a greater use of ICTs gain greater performance, so it can be confirmed that ICTs are a great opportunity for SMEs to improve their

competitiveness level; They are equally consistent with the results obtained by Aguilera et al. (2013), thus

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 767

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

Finally, the findings are consistent with the results obtained by Cuevas-Vargas et al. (2015) who found that

the use of ICTs have a positive and highly significant relationship with the competitiveness, due to the use of ICTs for document exchange with the firms’ suppliers have enable them to streamline their processes and have higher attentiveness and a better relationship with their customers, largely achieving satisfaction to these requirements, delivering products and/or services of higher quality, furthermore the age or the size of the company did no matter in order to achieve competitive success, as long as the use of ICTs is accompanied by an appropriate implementation strategy that defines the objective of ICTs (Bhatt & Grover, 2005), and by educating and creating a society possessing knowledge helping correctly the use of ICTs which will allow the firms to improve their competitiveness.

Conclusion

Regarding the objective of this research it is concluded that the use of ICTs have a positive and highly significant impact on the competitiveness of SMEs, since according to the interpretation of the 200 manufacturing businesses managers, the results obtained allow us to infer that companies with a higher level of ICTs use improve their competitiveness level by obtaining better financial performance, further reducing purchasing costs and improving the use of technology as compared to those companies that give less use or flat out do not use ICTs. That is why the use of ICTs within the business strategy of any organization, especially SMEs, offers sustainable advantages, thus the adoption and use of ICTs represent the fundamentals of competitiveness and economic growth for companies and countries that are able to exploit them (Higon, 2011; Ollo-López & Aramendia-Muneta, 2012;. Steinfield et al., 2012; Vehovar & Lesjak, 2007).

As for the implications, firstly, it has been found that SMEs that give more importance to the use of ICTs on the quality of customer service and the management of relationships with them, as well as to integrated information systems with suppliers to place orders, they have managed to obtain good financial results as well as very good profits in the past three years. Secondly, it was found that SMEs have given more importance to the impact of ICTs over the quality control of products with suppliers and have integrated information systems with suppliers to place orders, which have allowed the production cost of their business and the cost of product delivery with their suppliers to decrease.

Finally, the empirical evidence shows that the SMEs under study have given more importance to the use of ICTs in order to have integrated information systems to receive orders from their customers and of course to be in touch with the suppliers when ordering, giving importance to the use of ICTs for the management of their company, which has been reflected in project planning, development of production processes, improvement of machinery and equipment, and the development of information technology. That is why as stated by Esselaar et al. (2008), the organization that currently implements ICTs in their production processes may benefit with a better level of productivity and, therefore, its level of profitability will be acceptable, by presenting substantial improvements in the management of information technology, materials, or simply in the internal changes required to implement ICTs efficiently. The results obtained are of great value to managers and decision makers of Mexican SMEs, as well as for policy makers, therefore managers may realize how much of an impact the use of ICTs have in the competitiveness of SMEs, and thereby make the best decisions when investing.

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 768

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

References

Aguilera, E.L., Colín, S.M., and Hernández, C.O. (2013). La influencia de las Tecnologías de la Información en los procesos productivos para una mayor competitividad de la Pyme de

Aguascalientes: Un estudio empírico. Desarrollo Gerencial, 5(1), 40-68.

Aguilera, E.L., Cuevas, V.H., and Hernández, C.O. (2014). Impacto de la responsabilidad social y el capital

intelectual en la competitividad de las pymes manufactureras de Aguascalientes. Revista de Economía,

31(83), 129-162.

Aguilera-Enríquez, L., González-Adame, M., and Rodríguez-Camacho, R. (2011). Small business

competitiveness model for strategic sectors. Advances in Competitiveness Research, 19(3/4), 58-73.

Anderson, J., and Gerbing, D. (1988). Structural equation modeling in practice: a review and recommended

two-step approach. Psychological Bulletin, 103(3), 411-423.

Aragón, S.A., and Rubio, B.A. (2005). Factores explicativos del éxito competitivo: el caso de las PyMEs

del estado de Veracruz. Contaduría y Administración, Mayo-Agosto, 216, 35-69.

Arendt, L. (2008). Barriers to ICT adoption in SMEs: How to bridge the digital divide? Journal of Systems

and Information Technology, 10(2), 93-108.

Ashrafi, R., and Murtaza, M. (2008). Use and impact of ICT on SMEs in Oman. The Electronic

Information System Evaluations, 11(3), 125-138.

Bagozzi, R.P., and Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy

of Marketing Science, 16(1), 74-94.

Bardhan, I., Whitaker, J., and Mithas, S. (2006). Information Technology, Production Outsourcing, and

manufacturing plant performance. Journal of Management Information Systems, 23(2), 13-40.

Bentler, P.M. (2005). EQS 6 Structural Equations Program Manual. Encino, CA: Multivariate Software.

Bentler, P.M., and Bonnet, D. (1980). Significance tests and goodness of fit in analysis of covariance structures. Psychological Bulletin, 88(3), 588-606.

Bhatt, G.D., and Grover, V. (2005). Types of information technology capabilities and their role in

competitive advantage: An empirical study. Journal of Management Information Systems, 22(2),

253-277.

Black, S.E., and Linch, L.M. (2001). How to compete: the impact of workplace practices and information

technology on productivity. Review of Economics and Statistics, 83(3), 434-445.

Brown, T. (2006). Confirmatory Factor Analysis for Applied Research, New York, NY: The Guilford

Press.

Brynjolfsson, E., and Hitt, L. (1996). Paradox lost? Firm level evidence on the returns to information

systems spending. Management Science, 42(4), 541-558.

Buckley, J.P., Pass, L.C., and Prescott, K. (1988). Measures of international competitiveness: A critical

survey. Journal of Marketing Management, 4(2), 175-200.

Byrne, B.M. (1989). A primer of LISREL: Basic applications and Programming for Confirmatory Factor

Analysis Analytic Models. New York, NY: Springer.

Byrne, B.M. (2006). Structural Equation Modeling with EQS, basic concepts, applications, and

programming, 2nd edition, London: LEA Publishers.

Cachon, G., and Fisher, M. (2000). Supply Chain Inventory Management and the Value of Shared

Information. Management Science, 46(8), 1032-1048.

Cuevas-Vargas, H., Aguilera, E.L., and Hernández, C.O. (2014). The influence of innovation activities and knowledge management on the production processes for a higher level of competitiveness of Mexican

SMEs. International Journal of Business and Social Science, 5(13), 53-63.

Cuevas-Vargas, H., Aguilera, E.L., González, A.M., and Servin, J.L. (2015). The use of ICTs and its

relation with the competitiveness of Mexican SMEs. European Scientific Journal, 11(13), 294-310.

Diaz-Chao, A., and Torrent-Sellens, J. (2010). ¿Pueden el uso de las TIC y los activos intangibles mejorar

la competitividad? Estudios de Economía Aplicada, 28(2), 1-24.

Donrrosoro, I., García, C., González, M., Lezámiz, M., Matey, J., Moso, M., and Unzuela, M. (2001). El

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 769

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

Esselaar, S., Stork, C., Ndiwalana, A., and Deen-Swarray, M. (2008). ICT usage and its impact on

profitability of SMEs in 13 African countries. Information Technologies and International

Development, 4(1), 87-100.

Fornell, C., and Larcker, D. (1981). Evaluating structural equation models with unobservable variables and

measurement error. Journal of Marketing Research, 18(1), 39-50.

Gonzálvez-Gallego, N., Soto-Acosta, P., Trigo, A., Molina-Castillo, F.J., and Varajao, J. (2010). El papel de las TICs en el rendimiento de las cadenas de suministro: el caso de las grandes empresas de España

y Portugal. Universia Business Review, Cuarto Trimestre,28, 102-115.

Hair, J.F., Anderson, R.E., Tatham, R.L., and Black, W.C. (1999). Análisis Multivariante (5th Ed.). Madrid: Prentice Hall Iberia.

Higon, D.A. (2011). The impact of ICT on innovation activities: evidence for UK SMEs. International Small Business Journal, 30(6), 684-699.

INEGI, 2015. Directorio Estadístico Nacional de Unidades Económicas. [On line]

Available at: http://www3.inegi.org.mx/sistemas/mapa/denue/Cuantificar.aspx

[Last access: Feb 10th, 2015].

Ives, B., and Learmonth, G.P. (1984). The information system as a competitive weapon, Communications

of the ACM, 27(112), 1193-1201.

Jöreskog, K.G., and Sörbom, D. (1986). LISREL VI: Analysis of Linear Structural Relationships by

Maximum Likelihood, Instrumental Variables and Square Methods, Moorsville, IN: Scientific Software.

Kumar, R.L. (2004). A framework for assessing the business value of information technology

infrastructures. Journal of Management Information Systems, 21(2), 11-32.

Llopis, J. (2000). Dirigiendo: 11 factores clave del éxito empresarial. Barcelona: Ediciones Gestión 2000.

López, S.J.I. (2004). ¿Pueden las tecnologías de la información mejorar la productividad? Universia Business Review, Primer Trimestre,1, 82-95.

Maldonado, G.G., Martínez, S.M.D.C., García, P.D.L.D., Aguilera, E.L., and González, A.M. (2010). La

influencia de las TICs en el rendimiento de la PyME de Aguscalientes. Investigación y Ciencia, Abril,

47, 57-65.

Maldonado, G.G., Sánchez, G.J., Gaytán, C.J., and García, R.R. (2012). Measuring the competitiveness level in furniture SMEs of Spain. International Journal of Economics and Management Sciences,

1(11), 9-19.

McFarlan, F.W. (1984). Information Technology changes the way you compete. Harvard Business Review,

62(3), 98-103.

Menéndez, J., López, J., Rodríguez, A., and Francesco, S. (2007). El impacto del uso efectivo de las TIC sobre la eficiencia técnica de las empresas españolas. Estudios Gerenciales, 23(103), 65-84.

Mithas, S., Ramasubbu, N., Krishnan, M.S., and Sambamurthy, V. (2005). Information technology infrastructure capability and firm performance: An empirical analysis. Working paper. Ross School of Business, university of Michigan, Ann Arbor.

Modimogale, L., and Kroeze, J. (2009). Using ICTs to become a competitive SME in South Africa. In Proceedings of the 13th International Business Information Management Association (IBIMA)

Marrakech, Morocco, (pp. 504-513).

Nunnally, J.C., and Bernstein, I.H. (1994). Psychometric Theory. 3ª Ed. New York: McGraw-Hill.

Ollo-López, A., and Aramendia-Muneta, M.E. (2012). ICT impact on competitiveness, innovation and

environment. Telematics and Informatics, 29(2), 204-210.

Olviera, T., and Martins, M.F. (2011). Literature Review of Information Technology Adoption Models at

Firm level. The Electronic Journal Information Systems Evaluation, 14(1), 110-121.

Ongori, H., and Migiro, S.O. (2010). Information and communication technologies adoption in SMEs:

Literature review. Journal of Chinese Entrepreneurship, 2(1), 93-104.

ISSN: 2306-9007 Aguilera, Cuevas-Vargas & González (2015) 770

I

www.irmbrjournal.com September 2015I

nternationalR

eview ofM

anagement andB

usinessR

esearchVol. 4 Issue.3

R

M

B

R

Peirano, F., and Suarez, D. (2006). TICS y empresas: Propuestas conceptuales para la generación de indicadores para la sociedad de la información. Journal of Information Systems and Technology Management, 3(2), 123-142.

Porter, M.E., and Millar, V.E. (1985). How information gives you competitive advantage. Harvard

Business Review, 63(4), 149-160.

Rackoff, N., Wiseman, C., and Ullrich, W.A. (1985). Information systems for competitive advantage:

implementation of a planning process. MIS Quarterly, 9(4), 285-294.

Ríos, M.M., Toledo, R.J., Campos, O.O., and Alejos, G.A.A. (2009). Nivel de integración de las TICs en

las MiPymes, un análisis cualitativo. Panorama Administrativo, 3(6), 157-179.

Sambamurthy, V. Bharadwaj, A., and Grover, V. (2003). Shaping agility through digital options: Reconceptualizing the role of information technology in contemporary firms. MIS Quarterly, 27(2), 237-263.

Santhanam, R., and Hartono, E. (2003). Issues in linking information technology capability to firm

performance. MIS Quarterly, 27(1), 125-153.

Satorra, A., and Bentler, P.M. (1988). Scaling corrections for chi square statistics in covariance structure analysis. American Statistics Association 1988 Proceedings of the Business and Economic Sections, 36, 308-313.

Segars, A.H., and Grover, V. (1993). Re-examining perceived ease of use and usefulness: a confirmatory factor analysis. MIS Quarterly, 17(4), 517-525.

Shin, N. (2007). Information technology and diversification: how their relationship affects firm

performance. In System Sciences. Proceedings of the 40th Hawaii International Conference on System

Science on. IEEE: Hawaii, USA.

Steinfield, C., LaRose, R., Chew, H.E., and Tong, S.T. (2012). Small and medium-sized enterprises in rural business clusters: the relation between ICT adoption and benefits derived from cluster membership.

The Information Society, 28(2), 110-120.

Stern, C. (2002). A strategy for development. Washington, D.C.: The World Bank.