International Journal Advances in Social Science and Humanities

Available Online at: www.ijassh.com

RESEARCH ARTICLE

The Relationship between Corporate Social Responsibility (CSR)

and Financial Performance of Textiles Sector in Bangladesh

Especially in Barisal Division

Abdullah Al Masud*, Sariful Islam

Department of Management Studies, Faculty of Business Studies, University of Barisal, Barisal-8200, Bangladesh.

*Corresponding Author: E-mail: [email protected]

Abstract

The main purpose of this research is to find out the relationship between corporate social

responsibility (CSR) and financial performances of textiles sector in Bangladesh especially in Barisal division. A structured questionnaire with 5 point likert scale has been designed to collect the data by conducting survey. A sample of 100 respondents has been selected conveniently from Barisal division in Bangladesh. In this research, different statistical techniques like descriptive statistics, correlation and multiple regressions analysis have been conducted through using SPSS software (16.0 versions) to find the objectives of this research. The study found that CSR dimensions have significant effect on financial performance together. The result of the analysis also revealed that environment and occupational health & safety CSR dimensions have positive & significant impact or relationship on financial performance as well as fair pay and labor rights CSR dimensions have no significant impact or relationship on financial performance.

Keywords: Corporate Social Responsibility (CSR), Occupational Health & Safety, Environment, Financial Performance.

Introduction

Corporate social responsibility is become a crucial part of how companies do business in this planet. Corporate social responsibility (CSR) has become increasingly important for businesses, particularly in the context of the global spread of unethical practices among businesses in both developed and developing countries, as it helps businesses retain their reputation and be more competitive, sustainable [1-2].

In context of Bangladesh, corporate social responsibility (CSR) has become increasingly important for maximizing profit in textiles sector. The realities of globalization and tougher competitive conditions, as well as the increase in the power of corporations, put pressure on businesses to examine their social responsibilities and to integrate responsible practices with their business operations [3-4-5]. CSR concepts encourages certain social activities whereby such activities are not related to business directly but to social responsibilities which positively

impact on the business indirectly [6]. A. Carroll [7] identified corporate social responsibility (CSR) has having four aspects to it, economic, ethical, legal and discretionary. Corporate social responsibility (CSR) defined as business activities to ensure sustainable development and corporate behavior that not only ensure shareholders profit, products and services to customers and wage to employees but also they must respond to societal and environmental concerns and value.

Bangladesh, it is essential to ensure a lot of researches in this field. But there are a few studies conducted in this field. So this study is conducted to investigate the relationship between corporate social responsibility (CSR) and financial performance of textiles sector in Bangladesh especially in Barisal division. To find out objectives of this study, the first section reviews the existing literatures. The second section discusses research framework, research hypothesis and research methodology. The third section discusses data analysis and research findings. The final section gives conclusion and recommendations.

Research Objectives

The general or main objective of this research is to find out the relationship between corporate social responsibility (CSR) and financial performance of textiles sector in Bangladesh especially in Barisal division.

The Specific Objectives Included is as Follow

To identify the financial performance level for each CSR dimension.

To explore the relationship between CSR dimensions and financial performance.

To examine the dimensions of CSR toward the financial performance.

To identify which of the dimension of CSR causes the most significant effect towards financial performance.

Literature Review

Today the corporate world is facing the concept of corporate social responsibility (CSR) wherever we see. The RMG industry especially textiles sector is important in Bangladesh for multiple reasons. First, the RMG industry (textiles) has played an instrumental role in the growth of developing countries, particularly those in Asia [9].

With low fixed costs and emphasis on labor-intensive manufacturing, RMG has been a springboard for national development, and is the typical starter industry for countries engaged in export-oriented industrialization [10]. Second, the World Trade Organization’s (WTO) phase-out of the Multi-Fiber Arrangement (MFA) between 1995 and 2005 had significant implications for developing countries in Asia in accessing the apparel markets of developed countries [11].

While China has been the big winner, other developing countries such as Bangladesh, India, Vietnam and Indonesia have also benefitted [11] and the changes in management attitudes and ethics that have arisen are worth examining. Last, as an industry dealing with large multinational corporations (MNCs) with a buyer-driven value chain, the RMG (textiles) offers the opportunity to analyze the gap between the rhetoric and reality of CSR. In both the corporate and the academic world there is uncertainty as to how CSR should be defined. Many other researchers during the 60s have tried to validate and to narrate the more accurate definition of CSR [12]. Davis [13] States CSR as “Actions and decision made by business persons partially beyond the Organization’s direct economic and technical interest”. Since the 1970s, different scholars have paid more attention toward the Corporate Social Performance (CSP) as well as CSR [7].

Rahman Belal [14] says lot of CSR studies have been conducted very well in the context of developed countries such as the USA, Western Europe and Australia. Very few studies are obtainable on the CSR practices in the developing countries. Basically in the context of Bangladesh, we can see the practice of CSR has not been found widely in this country [14]. Alafi & Al Sufy [15] conduct the research on CSR and Firm performance and they find the positive relationship between CSR and Firm performance. Several previous researches show there is positive correlation between CSR and corporate financial performance. Jo & Harjoto [16] find there is strongly positive impact for firms that engage in CSR on firm value.

market-based measures of financial performance and accounting based measures of financial performance approaches, these approaches has been identified by previous researches when they measured financial performance of different variables [20].

Market-based financial performance measures changes rates or ratios such as stock performance, market return and share price which reflects company’s market value in the perspective capital market. Accounting based measures calculate return on asset

(ROA), return on equity (ROE), and net profit

and so on for measuring financial performance. There are different dimensions of CSR which are used in RMG industry specially textiles sector of Bangladesh like Occupational health and safety, Fair pay,

Environment, Labor rights, Social welfare and so on. From the discussion of different authors, we used Occupational health and safety, Fair pay, Environment and Labor rights as dimensions of CSR which are responsible to create impact on financial performance of textiles sector in Bangladesh especially in Barisal division.

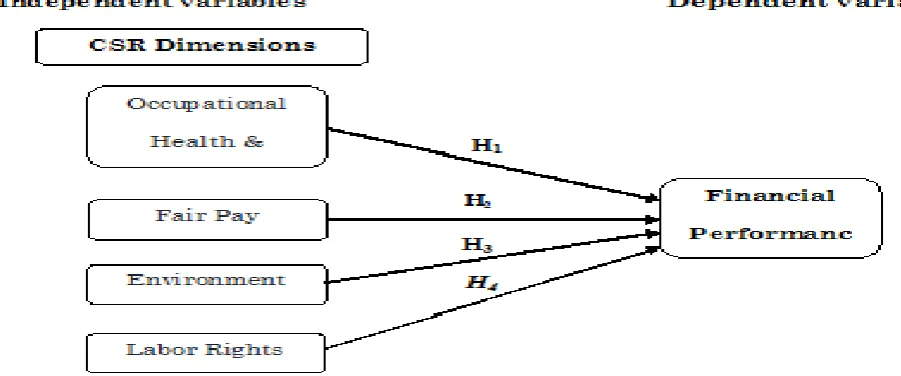

Research Framework

A research framework was constructed and formulated. In the research framework, independent variables are CSR dimensions like occupational health & safety, fair pay, environment & labor rights and the dependent variable is financial performance. The framework shows the relationship between the dimensions of CSR and financial performance which is given here.

Figure 1: Conceptual Framework

Research Hypothesis

This Research is Conducted to Address the Following Hypothesis

H1:-Occupational health & safety has a positive and significant impact on financial performance.

H2:-Fair pay has a positive and significant impact on financial performance.

H3:-Environment has a positive and significant impact on financial performance.

H4:-Labor rights have a positive and

significant impact on financial performance.

Research Methodology

For the purpose of this research, a survey was conducted to collect primary data from textiles firms in Bangladesh especially in Barisal division. Sample size of the

employees was hundred (100) in numbers. All the respondents were employees from textiles firms. The convenient sampling method was used for collecting the data and identifying the respondents. A structured questionnaire was designed to collect the data. All questions in the questionnaire are closed-ended because all possible answers were given to the respondents.

tried to analyze these questions through using SPSS software (16.0 versions). The statistical techniques like reliability analysis, factors analysis, descriptive statistics analysis, correlation analysis and multiple regressions analysis have been conducted to find the findings of the objectives of this research.

Data Analysis and Research Findings Demographic Profile Analysis

The demographic profile analysis of the research included: gender, age and education which were given to the following Table.

Table 1: Demographic Profile of Respondents

Profile Frequency Percentage (%)

Gender

Male 60 60

Female 40 40

Total 100 100

Age

20-30 years 32 32

31-40 years 45 45

41-50 years 18 18

Above 50 years 5 5

Total 100 100

Education

SSC 4 4

HSC 13 13

Graduation 78 78

Post-Graduation 5 5

Total 100 100

Table 01 has shown the frequency and percentage of respondents based on gender, age and education. There were 100 respondents in the survey. In gender portion from this table, it has found that 60% or 60 respondents are male respondents and 40% or 40 respondents are female respondents. In age portion from this table, it has found that majority of respondents fall on age group between 31-40 years old which amounted to 45% (45 respondents).

The second highest is age group between 20-30 years old which amounted to 32% (32 respondents). The third highest is age group between 41-50 years old which amounted to 18% (18respondents). The lowest percentage is age group above 50 years old which amounted to 5% (5 respondents).In education portion from this table, it has found that the

highest percentage of respondents are graduates which amounted to 78% (78 respondents).The second rank is about 13% or 13respondents who are completed their HSC. The frequency of 5 and 5% out of 100 respondents are post graduates which are third highest percentage among all. The last rank is about 4% or 4 respondents who are completed their SSC exam.

Reliability Analysis

In this research, reliability is measure by using Cranach’s Alpha. Cranach’s Alpha measures internal consistency or how the items are closely related with each other. Cranach’s Alpha of 0.7 and above is considered acceptable, where scale between 0 (no internal reliability) and 1 (greatest internal reliability is present) according to Bryman & Bell [21] .

Table 2: Reliability Statistics

Cronbach’s Alpha No of Items

0.760 28

Cronbach’s alpha (0.760) for 28 items (dependent and independent variables) has shown in this table which are greater than benchmark of 0.7, which indicates good and acceptable according to the rules of thumb, therefore the questionnaire formed is reliable.

Factors Analysis that affect the Financial Performance

Occupational Health & Safety

Table 3: Occupational Health & Safety

Statements No. of Respondents Ranking

(Based on percentage of Strongly Agree)

1 2 3 4 5

The firm maintains health care of its

workers.

0

(0%) (2%) 2 (31%) 31 (57%) 57 (10%) 10 1 The firm handles the fire related incidents effectively. The firm maintains

safety in the workplace. (2%) 2 (2%) 2 (40%) 40 (43%) 43 (13%) 13 2 The firm have adequate fire safety measures or first aid. The firm have good

working conditions. (2%) 2 (6%) 6 (34%) 34 (44%) 44 (14%) 14 3 Main gates of factory unit are not locked during working hours. The firm have adequate

fire safety measures or first aid.

2

(2%) (2%) 2 (28%) 28 (46%) 46 (22%) 22 4 strong enough and highly Buildings of the firm are ventilated. Buildings of the firm are

strong enough and highly ventilated.

0

(0%) (2%) 2 (28%) 28 (50%) 50 (20%) 20 5 The firm have good working conditions.

Main gates of factory unit are not locked during working hours.

0

(0%) (0%) 0 (28%) 28 (51%) 51 (21%) 21 6 The firm maintains safety in the workplace.

The firm handles the fire related incidents

effectively.

0

(0%) (2%) 2 (19%) 19 (51%) 51 (28%) 28 7 The firm maintains health care of its workers.

From this Table, it has shown that the statement (The firm handles the fire related incidents effectively) is ranked as first position for attaining highest percentage of strongly agree (5) which is 28% (28 respondents).The statement (The firm have adequate fire safety measures or first aid) is ranked as second position for attaining percentage of strongly agree (5) which is 22% (22 respondents).The statement (Main gates of factory unit are not locked during working hours) is ranked as third position for attaining percentage of strongly agree (5) which is 21% (21 respondents).The statement (Buildings of the firm are strong enough and highly ventilated) is ranked as fourth

position for attaining percentage of strongly agree (5) which is 20% (20 respondents). The statement (The firm have good working conditions) is ranked as fifth position for attaining percentage of strongly agree (5) which is 14% (14 respondents).The statement (The firm maintains safety in the workplace) is ranked as sixth position for attaining percentage of strongly agree (5) which is 13% (13 respondents).The statement (The firm maintains health care of its workers) is ranked as last position for attaining percentage of strongly agree (5) which is 10% (10 respondents).

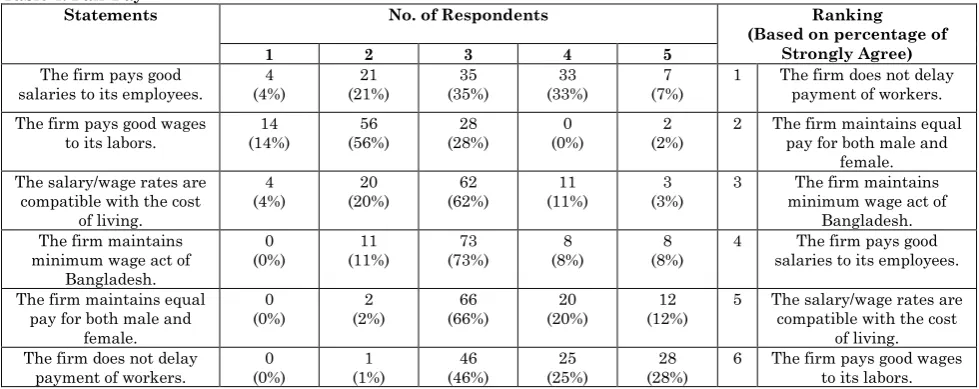

Fair Pay

Table 4: Fair Pay

Statements No. of Respondents Ranking

(Based on percentage of Strongly Agree)

1 2 3 4 5

The firm pays good

salaries to its employees. (4%) 4 (21%) 21 (35%) 35 (33%) 33 (7%) 7 1 The firm does not delay payment of workers. The firm pays good wages

to its labors.

14 (14%) 56 (56%) 28 (28%) 0 (0%) 2 (2%)

2 The firm maintains equal pay for both male and

female. The salary/wage rates are

compatible with the cost of living. 4 (4%) 20 (20%) 62 (62%) 11 (11%) 3 (3%)

3 The firm maintains minimum wage act of

Bangladesh. The firm maintains

minimum wage act of Bangladesh. 0 (0%) 11 (11%) 73 (73%) 8 (8%) 8 (8%)

4 The firm pays good salaries to its employees.

The firm maintains equal pay for both male and

female. 0 (0%) 2 (2%) 66 (66%) 20 (20%) 12 (12%)

5 The salary/wage rates are compatible with the cost

of living. The firm does not delay

payment of workers.

0 (0%) 1 (1%) 46 (46%) 25 (25%) 28 (28%)

6 The firm pays good wages to its labors.

From this Table, it has shown that the statement (The firm does not delay payment of workers) is ranked as first position for

both male and female) is ranked as second position for attaining percentage of strongly agree (5) which is 12% (12 respondents). The statement (The firm maintains minimum wage act of Bangladesh) is ranked as third position for attaining percentage of strongly agree (5) which is 8% (8 respondents). The statement (The firm pays good salaries to its employees) is ranked as fourth position for attaining percentage of strongly agree (5)

which is 7% (7 respondents). The statement (The salary/wage rates are compatible with the cost of living) is ranked as fifth position for attaining percentage of strongly agree (5) which is 3% (3 respondent). The statement (The firm pays good wages to its labors) is ranked as last position for attaining percentage of strongly agree (5) which is 2% (2 respondent).

Environment

Table 5: Environment

Statements No. of Respondents Ranking

(Based on percentage of Strongly Agree)

1 2 3 4 5

The firm located in non-industrial zones. 0 (0%) 0 (0%) 17 (17%) 49 (49%) 34 (34%)

1 The firm does not create air pollution and noise. The firm follows building

and safety codes or appropriate industrial standards which favorable

to environment. 2 (2%) 2 (2%) 9 (9%) 51 (51%) 36 (36%)

2 The firm does not increased fire hazard

due to the highly flammable nature of raw

materials and products. The firm does

not increased fire hazard due to the highly flammable nature of raw

materials and products.

0 (0%) 0 (0%) 30 (30%) 32 (32%) 38 (38%)

3 The firm does not create domestic power shortages

caused by the huge consumption of electricity.

The firm does not create domestic power shortages

caused by the huge consumption of electricity.

0

(0%) (2%) 2 (27%) 27 (34%) 34 (37%) 37 4 The firm follows building and safety codes or appropriate industrial standards which favorable

to environment. The firm does not create

air pollution and noise. (2%) 2 (2%) 2 (17%) 17 (38%) 38 (41%) 41 5 The firm located in non-industrial zones.

From This Table, it has shown that the statement (The firm does not create air pollution and noise) is ranked as first position for attaining highest percentage of strongly agree (5) which is 41% (41 respondents).The statement (The firm does not increased fire hazard due to the highly

flammable nature of raw materials and

products) is ranked as second position for attaining percentage of strongly agree (5) which is 38% (38 respondents).The statement (The firm does not create domestic power shortages caused by the huge consumption of

electricity) is ranked as third position for attaining percentage of strongly agree (5) which is 37% (37 respondents).The statement (The firm follows building and safety codes or appropriate industrial standards which favorable to environment) is ranked as fourth position for attaining percentage of strongly agree (5) which is 36% (36 respondents). The statement (The firm located in non-industrial zones) is ranked as last position for attaining percentage of strongly agrees (5) which are 34% (34 respondents).

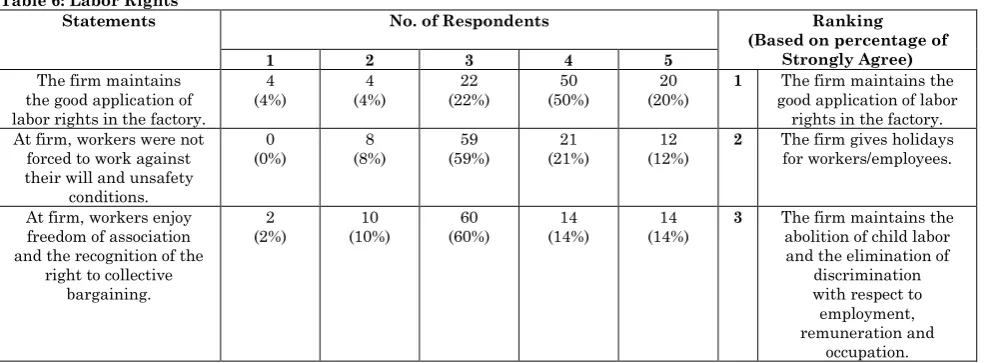

Labor Rights

Table 6: Labor Rights

Statements No. of Respondents Ranking

(Based on percentage of Strongly Agree)

1 2 3 4 5

The firm maintains the good application of labor rights in the factory.

4 (4%) 4 (4%) 22 (22%) 50 (50%) 20 (20%)

1 The firm maintains the good application of labor

rights in the factory. At firm, workers were not

forced to work against their will and unsafety

conditions.

0

(0%) (8%) 8 (59%) 59 (21%) 21 (12%) 12 2 The firm gives holidays for workers/employees.

At firm, workers enjoy freedom of association and the recognition of the

right to collective bargaining.

2

(2%) (10%) 10 (60%) 60 (14%) 14 (14%) 14 3 The firm maintains the abolition of child labor and the elimination of

discrimination with respect to employment, remuneration and

There are strong trade union movements which are not politicized in the

firm.

0

(0%) (5%) 5 (51%) 51 (33%) 33 (11%) 11 4 At firm, workers enjoy freedom of association and the recognition of the

right to collective bargaining. The firm maintains the

abolition of child labor and the elimination of

discrimination with respect to employment, remuneration

and occupation.

4

(4%) (24%) 24 (25%) 25 (31%) 31 (16%) 16 5 At firm, workers were not forced to work against their will and unsafety

conditions.

The firm gives holidays for workers/employees.

0 (0%)

3 (3%)

20 (20%)

58 (58%)

19 (19%)

6 There are strong trade union movements which are not politicized in the

firm.

From this Table, it has shown that the statement (The firm maintains the good application of labor rights in the factory) is ranked as first position for attaining highest percentage of strongly agree (5) which is 20% (20 respondents).The statement (The firm gives holidays for workers/employees.) is ranked as second position for attaining percentage of strongly agree (5) which is 19% (19 respondents).

The statement (The firm maintains the abolition of child labor and the elimination of discrimination with respect to employment, remuneration and occupation) is ranked as third position for attaining percentage of strongly agree (5) which is 16% (16

respondents).The statement (At firm,

workers enjoy freedom of association and the

recognition of the right to collective bargaining) is ranked as fourth position for attaining percentage of strongly agree (5) which is 14% (14 respondents). The statement (At firm, workers were not forced to work against their will and unsafely conditions) is ranked as fifth position for attaining percentage of strongly agree (5) which is 12% (12 respondents).The statement (There are strong trade union movements which are not politicized in the firm) is ranked as last position for attaining percentage of strongly agree (5) which is 11% (11 respondents).

Descriptive Statistics Analysis

Here we represent Mean, Standard Deviation of occupational health & safety, fair pay, environment, labor rights and financial performance by following Table.

Table 7: Descriptive Statistics

Groups N Mean (M) Std. Deviation (SD)

Occupational Health & Safety 100 3.8143 0.36913

Fair Pay 100 3.1033 0.40464

Environment 100 4.1240 0.42524

Labor Rights 100 3.5283 0.48203

Financial Performance 100 4.0875 0.58859

Table 07 has shown that the statistical description of CSR dimensions with financial performance. From this table, it has found that employees of textiles organizations perceived Environment (with the highest mean score, i.e. M = 4.1240, SD = 0.42524) to be the most dominant CSR dimension as well as it have the highest financial performance level towards CSR dimensions and evident to a considerable extent, followed by Occupational Health & Safety

(M = 3.8143, SD = 0.36913) and Labor

Rights (M = 3.5283, SD = 0.48203) which

were rated as moderate CSR dimensions as well as they have moderate financial performance level toward CSR dimensions of textiles organizations. Fair Pay (with the

lowest mean score, i.e. M = 3.1033, SD =

0.40464) to be the least CSR dimension as well as it have the lowest financial performance level towards CSR dimensions in textiles organizations. The average mean value of Financial Performance is 4.0875 and standard deviation is 0.58859. The standard deviations were quite high, indicating the dispersion in a widely-spread distribution. This means that the effects of Corporate Social Responsibility (CSR) on Financial Performance are an approximation to a normal distribution. This also indicates that respondents were in favor of financial performance.

Correlation Analysis

In correlation table, the quantity r is the linear correlation coefficient which measures the strength and the direction of a linear relationship between two variables.

Relationship of Occupational Health & Safety with Financial Performance

Table 8: Relationship of Occupational Health & Safety with Financial Performance

Financial Performance

Occupational Health & Safety

Pearson Correlation .374**

Sig. (2-tailed) .000

N 100

**. Correlation is significant at the 0.01 level (2-tailed).

The result of this Table revealed that a significant positive relationship between occupational health & safety and financial performance (r = 0.374, p<0.01).

So occupational health & safety (CSR dimension) influenced financial performance of textiles organizations.

Relationship of Fair Play with Financial Performance

Table 9: Relationship of Fair Play with Financial Performance

Financial Performance

Fair Pay

Pearson Correlation .190

Sig. (2-tailed) .059

N 100

The result of this Table revealed that a least significant relationship between fair pay and financial performance (r = 0.190, p>0.05). So

fair pay is a least influencing variable of CSR

which weakly influenced financial

performance of textiles organizations.

Relationship of Environment with Financial Performance

Table 10: Relationship of Environment with Financial Performance

Financial Performance

Environment

Pearson Correlation .378**

Sig. (2-tailed) .000

N 100

**. Correlation is significant at the 0.01 level (2-tailed).

The result of this Table revealed that a significant positive relationship between environment and financial performance (r =

0.378, p<0.01). So environment (CSR dimension) highly influenced financial performance of textiles organizations.

Relationship of Labor Rights with Financial Performance

Table 11: Relationship of Labor Rights with Financial Performance

Financial Performance

Labor Rights

Pearson Correlation .211*

Sig. (2-tailed) .035

N 100

*. Correlation is significant at the 0.05 level (2-tailed).

The result of this Table revealed that a significant positive relationship between labor rights and financial performance (r = 0.211, p<0.05). So labor rights (CSR dimension) influenced financial performance of textiles organizations.

Multiple Regression Analysis

In this part of the analysis includes a regression model to test the hypothesis. Four extracted CSR dimensions were taken as independent variables against financial

performance as dependent variable in a multiple regression model. Here we used 95% confidence interval to test hypothesis. Through the Multiple Linear Regression analysis, the Multiple Linear Regression equation is formed as following, this equation

examines the relationship between

independent variables and dependent

variable.

Where,

Y= Financial Performance.

X1= Occupational Health & Safety. X2= Fair Pay.

X3= Environment. X4= Labor Rights. e = Error term.

Table 12: Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

(1) .451 .203 .170 .53626

Predictors

(Constant), Occupational Health & Safety, Fair Pay, Environment and Labor Rights. From Table-12, it has been seen that R value is 0.451. Therefore, R value (0.451) for the overall CSR dimensions suggested that there is a strong effect of these four independent variables (Occupational Health & Safety,

Fair Pay, Environment and Labor Rights) on financial performance. It can also observed that the coefficient of determination i.e. the R-square (R2) value is 0.203, which

representing that 20.3% variation of the dependent variable (Financial Performance) is due to the independent variables (CSR dimensions), which in fact, is a strong explanatory power of regression.

Table 13: ANOVA

Model Sum of Squares df Mean Square F Sig.

(1)

Regression 6.977 4 1.744 6.065 .000

Residual 27.320 95 .288

Total 34.297 99

Predictors

(Constant), Occupational Health & Safety, Fair Pay, Environment and Labor Rights.

Dependent Variable

Financial Performance.

From Table-13, it is identified that the value of F-stat is 6.065 and is significant as the level of significance is less than 5% (p< 0.05). This indicates that the overall model was fit and there was a statistically significant association between CSR dimensions and financial performance.

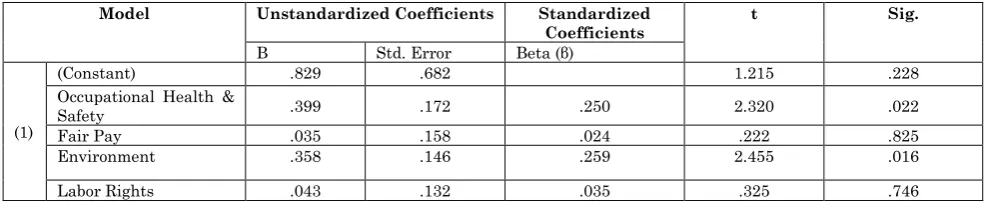

Table 14: Coefficients

Model Unstandardized Coefficients Standardized

Coefficients

t Sig.

B Std. Error Beta (β)

(1)

(Constant) .829 .682 1.215 .228

Occupational Health &

Safety .399 .172 .250 2.320 .022

Fair Pay .035 .158 .024 .222 .825

Environment .358 .146 .259 2.455 .016

Labor Rights .043 .132 .035 .325 .746

Dependent Variable

Financial Performance

In Table-14, unstandardized coefficients indicated how much the dependent variable varies with an independent variable, when all other independent variables are held constant. The beta coefficients indicated that how and to what extent CSR dimensions such as occupational health & safety, fair pay, environment and labor rights influence financial performance of the organization. It has been found that, Environment (β= .259, t= 2.455, p<0.05) and Occupational Health & Safety (β= .250, t= 2.320, p<0.05) have the highest influence or significant impact on financial performance of textiles

organizations in Bangladesh especially in Barisal division because of t value of the coefficient of beta of Environment and Occupational Health & Safety is more than +1.96 and p-value is lower than 0.05.

financial performance of textiles organizations in Bangladesh especially in Barisal division because of t value of the coefficient of beta of Labor Rights and Fair Pay is lower than +1.96 and p-value is more than 0.05. Therefore, the hypothesis H4 is rejected that states labor rights has a positive and significant impact on financial performance as well as the hypothesis H2 is

rejected that states air pay has a positive and significant impact on financial performance in this research.

Here the study found that Environment (β = .259, t = 2.455, p<0.05) is the most significant dimension of CSR that causes the effect towards financial performance of textiles organizations.

Then the Fitted Regression Model is

Financial Performance (Y) = 0.829 + 0.250 (Occupational Health & Safety) + 0.024 (Fair Pay) + 0.259 (Environment) + 0.035 (Labor Rights).

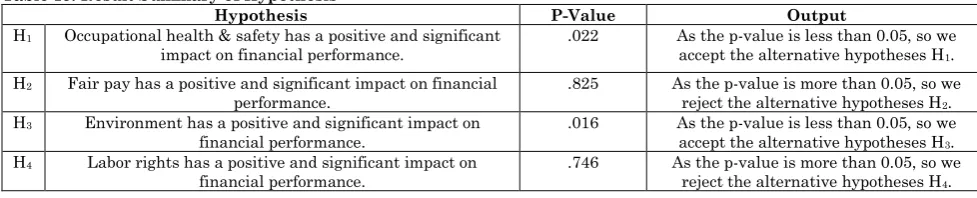

Table 15: Result Summary of Hypothesis

Hypothesis P-Value Output

H1 Occupational health & safety has a positive and significant

impact on financial performance. .022 As the p-value is less than 0.05, so we accept the alternative hypotheses H1.

H2 Fair pay has a positive and significant impact on financial

performance. .825 As the p-value is more than 0.05, so we reject the alternative hypotheses H2.

H3 Environment has a positive and significant impact on

financial performance.

.016 As the p-value is less than 0.05, so we accept the alternative hypotheses H3.

H4 Labor rights has a positive and significant impact on

financial performance. .746 As the p-value is more than 0.05, so we reject the alternative hypotheses H4.

Conclusion and Recommendations

Corporate Social Responsibility (CSR) is a critical business requirement. CSR investment is an asset to the organization.

This study investigates corporate social responsibility (CSR) and financial performance relationship of textiles sector in Bangladesh especially in Barisal division in terms of four CSR dimensions such as occupational health & safety, fair pay, environment and labor rights and financial performance dimension. The study reveals that the combination of occupational health & safety, fair pay, environment and labor rights dimensions together have significant effect on financial performance. Among these CSR dimensions, environment and occupational health & safety dimensions have positive & significant impact or relationship on financial performance as well as fair pay and labor rights dimensions

have no significant impact or relationship on financial performance. According to the findings, environment is the key CSR dimension to increase financial performance of textiles firms. We suggest the following recommendations for increasing financial performance in case of CSR practices of textiles firms in Bangladesh especially in Barisal division.

Proper pay structure should be established for the employees.

Employee friendly CSR policy should be established & implemented in the organization.

Labor standards& rights, health & safety measurements, women empowerment, social compliance and sustainable business practices should be ensured for the employees.

Labor complaints should be solved quickly in the organization.

References

1. Carroll AB, Shabana KMM (2010) The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. International Journal of Management Reviews, 12(1): 85-105.

2. Lee MDP (2008) A review of the theories of corporate social responsibility: Its

evolutionary path and the road ahead. International Journal of Management Reviews, 10(1):53-73.

4. Burke L, Logsdon JM (1996) ow corporate social responsibility pays off. Long Range Planning, 29(4):495-502.

5. UNCTAD (2011) World Investment Report 2011: Non-Equity Modes of International Production and Development. United

Nations Publication.

https://doi.org/10.1016/j.asieco.2007.02.015

6. Fischer J (2004) Social responsibility and ethics: Clarifying the concepts. Journal of Business Ethics, 52(4):381-390.

7. Carroll A (1979) A three-dimensional conceptual model of corporate performance. Academy of Management Review, 4:497– 505.

8. Dalton, Daily, Johnson, Ellstrand (1999) Number of Directors and Financial Performance: A Meta Analysis. Academy of Management Journal, 42(6):674-686.

9. Gereffi G, Memedovic O (2003) The Global Apparel Value Chain: What Prospectrs for Upgrading by Developing Countries. United Nations Industrial Development Organization.https://doi.org/10.2139/ssrn.42 4560

10. Gereffi G (1999) International trade and industrial upgrading in the apparel commodity chain. Journal of International Economics,48(1):37-70.

11. Gereffi G, Frederick S (2010) The global apparel value chain, trade and the crisis. Vhallenges and opportunities for developing countries. World Bank Policy Research Working 5281. https://doi.org/Book_Doi 10.1596/978-0-8213-8499-2

12. Iqbal N, Ahmad N, Kanwal M (2013) Impact of Corporate Social Responsibility on Profitability of Islamic and Conventional Financial Institutions. Applied Mathematics in Engineering, 1(2):26-37.

13. Davis K (1960) Can Business Afford to Ignore Corpo- rate Social Responsibilities? California Management Review, 2:70-76.

14. Rahman Belal A (2001) A study of corporate social disclosures in Bangladesh. Managerial Auditing Journal. https://doi.org/10.1108/02686900110392922

15. Alafi K, Al Sufy FJH (2012) Corporate Social Responsibility Associated With Customer Satisfaction and Financial Performance a Case Study with Housing Banks in Jordan. International Journal of Humanities and Social Science, 2(15):102– 115.

16. Jo H, Harjoto MA (2011) Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility. Journal of Business Ethics, 103(3). https://doi.org/10.1007/s10551-011-0869-y

17. Choi JS, Kwak YM, Choe C (2010) Corporate social responsibility and corporate financial performance: Evidence from Korea. Australian Journal of Management, 35(3):291-311.

18. Lindgreen A, Swaen V, Johnston W (2009) The supporting function of marketing in corporate social responsibility. Corporate Reputation Review, 12(2):120-139.

19. Hillman AJ, Keim GDGD (2001) Shareholder value, stakeholder management, and social issues: what’s the bottom line? Strategic Management Journal, 22(2):125-139.

20. Orlitzky, Marc, Frank L, Schmidt SLR (2003) Corporate social and financial performance: A meta-analysis. Organization Studies, 24(3):403-441.