International Journal Advances in Social Science and Humanities

Available online at: www.ijassh.com

RESEARCH ARTICLE

Economic Advantages of Utilizing Natural Gas for Indonesian Domestic

Fuels in Lieu of Fossil Liquids and Coals

Tjendrasa, Kinsenary (Kin)*

DMB - Universitas Padjajaran, Bandung, Indonesia.

*Corresponding Author:Email:[email protected]

Abstract

This paper explores the economic advantages of utilizing natural gas and incentives to switch in different forms such as pipe gas or CNG (Compressed Natural gas) for domestic consumptions in Indonesia to replace diesel, kerosene, gasoline and coal. The 2011 data indicates that the domestic demand on energy was circa 3 MMBOEPD (million barrels oil equivalent) with refined crude oil supplying half of the demand. More than half of 950 MBOPD crude oil was imported as Indonesian government entitlement from PSC production is circa 60% of production at under Production Sharing Contract (PSC). With 6% annual national growth rate, the demand will be 4 MMBOEPD by 2015. Indonesia has much small to medium size gas reserves scatter around major Indonesian islands that can be commercialized if the financial reward is right. Among the constraints are the economic returns that investors of which the consumers and Government of Indonesia can benefit from, the assurance of continuous supply and acceptance of long term benefit on conversion to gas in economics and environmental protection. The key success factors are energy pricing policy, incentive to use clean energy and firm enabling regulation for quick monetization and assurance on investment. Indonesia has proved and probable (2P) gas reserves of 237 TCF can be tapped for commercialization. Indonesia also has 21 billion tons of coal reserves that can be exported to earn foreign reserves. Lacking of gas infrastructure increases the complication of gas utilizations. The investors need to get the risked economic return on their investments; they may have invested to where they get higher rewards in other countries as money has no ”border”. The missing link is the competitive commercial prices, supporting infrastructures, consumers’ willingness and incentive to shift using natural gas.

Keywords: Natural gas, Domestic consumptions, Energy pricing policy, Enabling regulations, Risked economic return.

Introduction

Indonesia’s oil and gas industry has been initiated since 1885, and is recognized as the third oldest in the world after the United States and Russia. The first discovery of oil in commercial quantities occurred in 1885 in North Sumatra; the main oil producing fields in Central Sumatra were not discovered until the 1930s and 1940s. Following its independence in 1945, Indonesia sought to realize the potential that the oil and gas industry possessed for providing the funds necessary for the development of the country and its

infrastructure. The application of PSC

(Production Sharing Contract) resulted many significant oil discoveries above 100 million barrels of oil in 1968/1972 from Offshore North West Java’s Ardjuna field and South East

Sumatra’s Cinta field. In late 1971, a major gas discovery was made in the Arun field in northern Sumatra by Mobil Oil Indonesia Inc., followed by Huffco Indonesia in the Badak field in East Kalimantan in early 1972. These two independent discoveries established Indonesia as a major exporter of LNG (liquefied Natural Gas) with the shipment of its first LNG cargo taking place in August 1977 to Japan. Since then, Indonesia has become the largest exporter of LNG in the world according to the Indonesian US Embassy’s Petroleum Indonesia Report.

Fig. 1: Map of Indonesia with Gas Infrastructures

(Source of map: BPH Migas)

Indonesia, officially the Republic of Indonesia, is the largest archipelago country located in Southeast Asia along the equator line that covers 1,811,569 km2 land comprising over 17,500 islands over 5200KM from Sabang to Merauke. It has 33 provinces with over 238 million people,

and is the world's fourth most populous country. The population is mostly concentrated in western part of Indonesia, mainly Java, Bali and Sumatra. Indonesia shares land borders with Papua New Guinea, East Timor, and Malaysia. Other neighboring countries are Singapore, Philippines, Australia, and the Indian territory of the Andaman and Nicobar Islands. Figure 1 is the map of Indonesia, also indicates the location of major natural gas facilities and its infrastructure.

Currently, over 200 contracts are in place with independent operators, including over 130 PSCs, for the exploration, development and production of oil and gas reserves. In 2005, Indonesia struggled to maintain oil self-sufficiency and the Government is continuously seeking to incentivize investment in the oil and gas industry. Having been a mainstay of the economy for many decades since the first discovery of oil in 1885, Indonesia’s oil and gas sector is perceived as in a state of decline. Having become a net importer of oil in 2004 and relinquishing OPEC (Organization of Petroleum Exporting Countries) membership in 2008, oil production figures have continued to decrease from their high above 1.6 MMBOPD (Million Barrel Oil per Day) in 1997.

Since the Asian Crisis of 1998, investment in exploration of new fields has dwindled and the sector shrank by 3.61% in 2010 according to the Central Statistics Agency. Per 2011 data, the country has 4.0 BBO (Billion Barrel of Oil) and

188 TCF (Trillion Cubic Feet) of oil and gas Proved reserves according to BP’s 2012 World Energy Statistical Data, respectively, but substantial investment is required to access them and fund the necessary exploratory infrastructure. In addition, Indonesia also has 3.5 BBO and 49 TCF of Probable oil and gas reserves, respectively (Source: Directorate General of Oil and Gas). It is important to recognize that many technically discovered reserves were not booked due to its lack of commercial values, especially marginal gas discovery. In addition, Indonesia has 21.1 Billion tons of Coal reserves with total coal resources of 105 billion ton. In 2011, Indonesia produced 290,000 ton of coals, exported 209,000 tons and domestic use of 65,000 ton (source of data: Direktorat Jendral Mineral dan Batubara).

Structure of Oil and gas Management in

Indonesia

Above chart describes how the Indonesian government managed oil and gas under existing law no. 22/2001. Law No. 22/2001 which governs the activities of the oil and gas sector in Indonesia states that BP Migas is formed to be the regulatory body for upstream activities in oil and gas such as exploration and exploitation through PSC between BP Migas and the company involved in PSC which may be state owned, branch of a foreign company or private local company. The body has emphasized more on controlling rather than managing the growth of Indonesian oil and gas businesses.

BPH Migas (Badan Pengatur Hilir Minyak dan Gas Bumi) BPH Migas covers the downstream sector such as processing, transport and storage. Foreign companies with a representative office in the country may engage in both upstream or downstream but cannot be involved in both areas in one single legal entity. The law also states the preference for use of local manpower and expertise in execution of projects as well as environmental standards that must be met by companies.

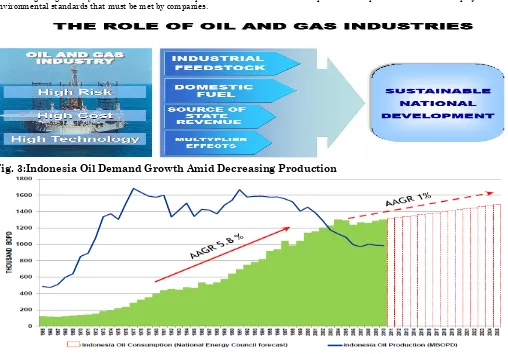

Fig. 3:Indonesia Oil Demand Growth Amid Decreasing Production

Fig. 4: Sources: IPA Convention, May 2012

The oil and gas sector has played important roles in Indonesia's economy, accounting for 7% of Indonesia's GDP, directly over 25% of state revenues and US$16 Billion of direct investment annually. In addition, she added that declining oil production from 1.6 MMBPD in 1996 to about 942 MBPD (Thousand of Barrel Oil per Day) in 2011 reflects the maturity of existing fields and the lack of new developments, emphasizing that Indonesia needs to unlock new resources and realize the potential of gas reserves, together with further development of sustainable renewable energy resources.

In current Indonesian government income, the revenue from oil and gas play a very important role contributing 22% to state expenditure in 2012 estimate. In 2011, oil and gas contributed 35 billion US $ to Government of Indonesia. On oil production, Indonesian oil production in 2011 was 942 MBOPD while the consumption was 1430 MBOPD. Indonesia has been net oil importer since 2004.

Overview of Indonesian Natural Gas

Sector

Indonesia with proved gas reserves of

approximately 188 tcf is the twelfth largest holder of gas reserves in the world. Indonesia ranks

Fig. 5: Indonesian natural gas production & domestic consumptions

Source: BP Migas presentation in May 2012 IPA convention

Several fields are expected to come on stream in 2013 and will boost production. Indonesia exports gas to Malaysia and Singapore via pipeline. Indonesia is also the world’s third largest LNG exporter with LNG plants at Arun, Bontang and Papua’s Tangguh.

The GoI (Government of Indonesia) requires gas producers with a PSC signed after 23 November 2001 to supply 25 per cent of their gas production to the domestic market. However, this domestic obligation has failed to keep pace with growing domestic demand for gas from both the power and fertilizer industries, left alone for motor vehicles which consume most of the gasoline and diesel Indonesia partially imports to fulfill domestic demand. As a result the GoI introduced a policy to redirect gas intended for export to domestic projects. To this end, gas has been diverted from the Bontang and Arun LNG projects. Recently the GoI has stated that producers will be allowed to export gas provided there are no domestic buyers. The Ministry of Energy & Mineral Resources (MEMR) claims domestic customers will be given the first opportunity to negotiate the purchase of gas.

The opportunity of CBM (Coal bed methane) which starts in 2007, offers huge potential to Indonesia given that it holds the world’s second largest reserves, estimated to be 453 tcf. As yet there is no commercial production of CBM in Indonesia. The first CBM cooperation contracts were awarded in 2008 and a further four are expected to be auctioned in mid 2010.

As demonstrated in the graph (figure 4) above, in 2011, Indonesia’s gas consumption was about ½ of the 7.3 BSCFD (Billion Standard Cubic Feet per Day) productions. The fertilizer, petrochemical and power generation are the principal domestic consumers of natural gas in Indonesia. However, Indonesia’s limited natural gas transmission and distribution network remains an obstacle to further domestic consumption. Historically, natural gas transmission and distribution activities are carried out by the State-owned utility PGN (P.T. Perusahaan gas Negara,

(Persero), Tbk), subsequently, PGN has

transformed into a public listed company. The Government announced a “Master plan” in 2006 for the development of a natural gas transmission and distribution network and subsequently, following a public tender process, the downstream regulator, BPH Migas, awarded concessions (“Special Rights”) to construct and operate a Trans Java and a Kalimantan to Java pipeline to

non-PGN consortia. The implementation of the master plan is very slow, if not idle.

At international (regional) connections, Indonesia began exporting natural gas via pipeline in 2001, with the opening of the 400-mile, 325-million standard cubic feet per day (MMscf/d) subsea pipeline from West Natuna to Singapore. In August 2002, Indonesia began delivering 250 MMscf/d of piped natural gas to Malaysia’s Duyong platform. And in August 2003, a second natural gas connection to Singapore was opened when the South Sumatra-Singapore pipeline was completed. This line reached 350-MMscf/d maximum capacity during 2006 and will deliver natural gas to Singapore over a 20-year contract. Indonesia has played a leading role in discussions of the proposed “Trans-ASEAN Gas Pipeline” (TAGP), which envisions the establishment of a transnational pipeline network linking the major natural gas producers and consumers in Southeast Asia. The TAGP concept was initially proposed in 1997 as part of ASEAN’s “Vision 2020” initiative. In July 2002, energy ministers from the ASEAN countries signed a memorandum of understanding to study the viability of the project, although much work remains to be completed to fully realize the project’s goals (for more information, see ASEAN’s Plan of Action for Energy Cooperation, 2004-2009).

Indonesia is a leading LNG (Liquefied Natural Gas) exporter. Indonesia was the world’s largest exporter of LNG in 2005, although some reports suggest that the country was surpassed by Qatar sometime in 2006. During 2005, Indonesia exported 23 million tons (MMt, or 1,123 Bcf) of LNG, or about 16 percent of the world total. Indonesia produces LNG from three terminals: the Bontang facility in Badak, East Kalimantan, the Arun plant in North Sumatra and the Tangguh LNG plant in West Papua.

Domestic

Gas

Distributions

and

Utilization

PGN are jointly financing the project. So far, the planned interconnection is partially complete, and is scheduled to be fully operational in 2010 with a capacity to transport 2.2 Bcf/d of natural gas. In addition, Pertamina (PT Pertamina (Persero) has some pipeline network in West and East Java and East Kalimantan for Industrial estates.

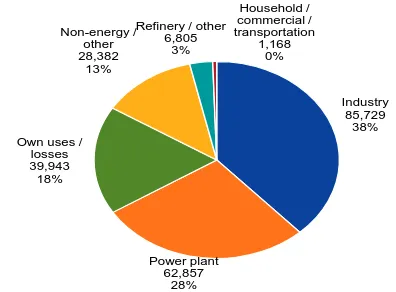

Industry 85,729 38% Power plant 62,857 28% Own uses /

losses 39,943 18% Non-energy / other 28,382 13%

Refinery / other 6,805 3% Household / commercial / transportation 1,168 0%

Fig. 6a: Use of natural gas in Indonesia – 2010 (MMBOE)

Transportation 227,203 57% Power plant 63,611 16% Industry 57,602 15% Non-energy / other 28,743 7% Household / commercial 21,466 5%

Own uses / losses

628 0%

Fig. 6b: Use of fuel in Indonesia – 2010 (MMBOE)

Source: 2011 Handbook of Energy & Economic Statistics of Indonesia

The gas industry in Indonesia may look rosy, however, Indonesia is lacking of domestic and regional gas transmission to enable quick transportation of gas to consumer area. Observing the data, the gas utilization for domestic land transportation such as motor vehicles is at most, 1 % of the production (Figure 6a). This phenomena is an interesting anomaly and good research topic, we need to find out the hidden reasons behind. Natural gas is deemed environmental friendly; relatively lower price compared to crude oil or coal liquid; many countries import natural gas for their motor

vehicles, power generation uses; many

government give incentive for converting liquid fuel to gas, and Indonesia has not done so, or at most, at the pilot phase for many years and moving nowhere.

On the other hand, the domestic liquid fuel consumptions with heavy subsidy are continuous and can hardly see any good effort to reduce and ultimately, eliminate this subsidy and use the

money for better people development to build a prosperous society where people can make enough income to support their living and more. Even recently, the utilization of natural gas for PLN (Perushaan Listrik Negara, the national

electricity (power) company) increases

substantially, much need to be done to ship the gas to remote area in lieu of using diesel or coal.

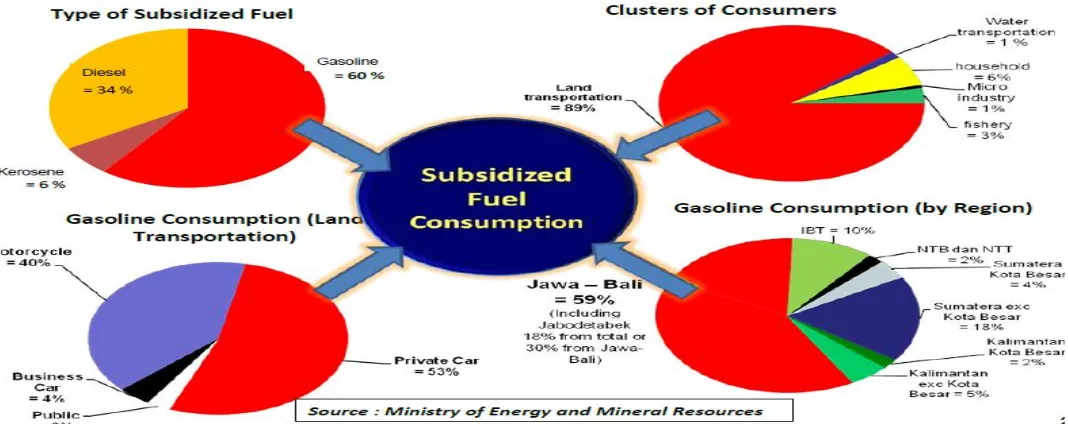

Motor Vehicle Fuel Subsidy and CNG

From Indonesian Ministry of Finance report,in 2012 fiscal budget, Indonesian government has targeted a 208.9 trillion rupiah, or at IDR of 9,500/ US$, is approximatrely US$.22 billion. In deed, the budget was insufficient, and revised budget for additional subsidy was recently granted . That is the results of using 40 million kilo liter of fuel at subsidized price, comprised of 24.4 million kilo liter for Primium gasoline 13.9 million kilo lter of diesel and 1.7 million kilo liter of kerosine. The low consumption in Kerosine for home cooking was the result of conversion to LPG (Liquefied Petroleum gas) in 2008. The consumptions of Kerosine in 2007 was 9.9 million kilo liter. The conversion to LPG due to its clean and easy to transport in nature has reduced as much as 9 million kilo liter of Kerosine consumption.Composition

of

Subsidized

Fuel

Consumptions

There is one opportunity in which government of Indonesia can intensify the conversion, which is using CNG for motor vehicle to replace Premium gasoline. In August 2012, Premium gasoline consumption in Jakarta topped 1.41 million kiloliters, 37.4 percent more than the government's allocation of 1.03 million kiloliters for the month, according to state energy firm PT Pertamina. The subsidised Premium gasoline is sold at 4,500/l at pmp. IN the $100 /BBL crude oil FOB (free on board) price , Pertamina has reckoned that the full cost breakeven price is circa 8,000 / liter, or Indonesia government is subsiding 56% of fuel cost. Imagined for 1.41 kilo liter at IDR 3,500/leter, that was a sudidy of IDR 4.9 tillion or US$519 million. If governemnt can use natural gas through an intensive development program with higher incentive to oil and gas players, the subsidy can be elimated. The way is to convert the Premium gasoline users (four wheel car to start with) to use CNG, compressed natural gas.

Fig. 7: Fiscal policy office, ministry of finance

Source: IPA May 2012 Convention

have not been established, or at most, is at “pilot” phase. On the other hand, There are many small sub economic natural gas scattereed among the PSC area in Indonesia. The main reason for subeconomic is that, theere is has no defined market mechanism for natural gas on domestic market, the selling price is negotiated as economic price, making each gas sale through a lengthly negotiation between customers, government and producer. If government can encourage domestic gas sale as in crude oil, using x percentage of crude oil price parity as in Bontang LNG formula, this can shorten the commercialization of natural gas in much shorter time. The other main reason for subeconomic is due to tough fiscal term as compared to US or UK tax system or royalty and tax system. In deed, the calculation in table 1 below demonstrated that the government does not have to alter current PSC terms, but lower the government split from 70/30 to 50/50 profit share, and enable the quicker development and provide one off subsidy to consumers in term of Premium gasoline to CNG conversion kit,say free of charge. The kit can easily be financed from the government take from the sale of natural gas in the form of CNG.

Gas Economics for Marginal Field

In exploration activities in Sumatra, Kalimantan, as well as in Java, there are many technically proved gas discovered in smaller accumulation at 0.5 – 3 BCF (billion cubic feet) of which they were deemed non economics with current market prices (3-6$/MCF) and fiscal terms. If the gas price can be liberated to equal to 90% of crude price (assumed current market of $90/BBL) in similar heating value using Bontang LNG price formula, we can expect that PSC contractor can make

money and willing to invest by taking higher exploration risk, provided that the government can also shorten the development approval timing to enable commercial sales in 24 months from exploration success to first gas. To do this, there will need major de-bureaucratize on current approval and tendering procedures, including regional government complicated permit and fee. The economic evaluation demonstrated that, even with a natural gas discovery, as low as 1 BCF, can be economics and to be used as CNG in the area where the gas discovered (within 200 km radius) if the road infrastructure is available. Calculation below has not considered other elements as time value money (NPV, Net Present Value), IRR (internal rate of return) or WACC, (Weighted Average Cost of Capital).

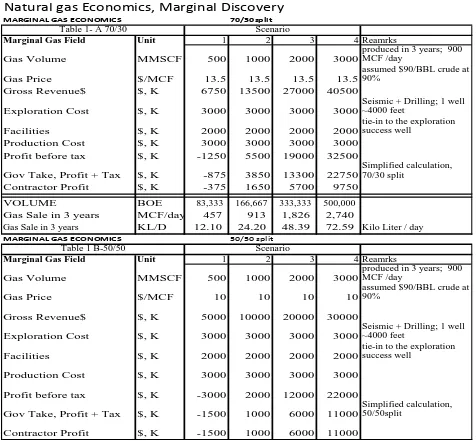

Table1: Natural gas economics,marginal discovery

Natural gas Economics, Marginal Discovery

MARGINAL GAS ECONOMICS 70/30split

Marginal Gas Field Unit 1 2 3 4 Reamrks

Gas Volume MMSCF 500 1000 2000 3000

produced in 3 years; 900 MCF /day

Gas Price $/MCF 13.5 13.5 13.5 13.5

assumed $90/BBL crude at 90%

Gross Revenue$ $, K 6750 13500 27000 40500 90

Exploration Cost $, K 3000 3000 3000 3000

Seismic + Drilling; 1 well ~4000 feet

Facilities $, K 2000 2000 2000 2000

tie-in to the exploration success well

Production Cost $, K 3000 3000 3000 3000

Profit before tax $, K -1250 5500 19000 32500

Gov Take, Profit + Tax $, K -875 3850 13300 22750

Simplified calculation, 70/30 split

Contractor Profit $, K -375 1650 5700 9750

VOLUME BOE 83,333 166,667 333,333 500,000

Gas Sale in 3 years MCF/day 457 913 1,826 2,740

Gas Sale in 3 years KL/D 12.10 24.20 48.39 72.59 Kilo Liter / day

MARGINAL GAS ECONOMICS 50/50 split

Marginal Gas Field Unit 1 2 3 4 Reamrks

Gas Volume MMSCF 500 1000 2000 3000

produced in 3 years; 900 MCF /day

Gas Price $/MCF 10 10 10 10

assumed $90/BBL crude at 90%

Gross Revenue$ $, K 5000 10000 20000 30000 90

Exploration Cost $, K 3000 3000 3000 3000

Seismic + Drilling; 1 well ~4000 feet

Facilities $, K 2000 2000 2000 2000

tie-in to the exploration success well

Production Cost $, K 3000 3000 3000 3000

Profit before tax $, K -3000 2000 12000 22000

Gov Take, Profit + Tax $, K -1500 1000 6000 11000

Simplified calculation, 50/50split

Contractor Profit $, K -1500 1000 6000 11000

Scenario Table 1- A 70/30

Table 1 B-50/50 Scenario

It has not been a secret in oil and gas industry in Indonesia, a discovery of oil may take at least 36 months to 60 months to put on first commercial and the gas discovery can be as long as 5 to 10 years. BP Tangguh gas was discovered in 1994 and put on production in 2008. Inpex Masela gas field was discovered in 2004 and current plan is to have fisrt commercial gas by 2018. Both are LNG project as the gas is in West paupua offshore and Arafura sea of Maluku. This kind od major discovery will need strong capital back up to spend the money without income for 10 plus years.

CNG in Lieu of Premium Gasoline and

Coal

Indonesia has very limited use of natural gas for motor vehicles. And home cooking. Observing that Indonesia has almost no CNG car, except for a few taxi in Jakarta. CNG is natural gas compressed for the purpose of simplified transport

and storage. Bulk CNG transport technology is not new, it is well-proven -CNG has been

successfully transported on land by road-trailer (trucking) for over thirty years. The up-scaled application of proven CNG technology to a marine (shipping) transport system is new. A bulk CNG road delivery system is considered best suited for short range projects, normally under 200km one-way, with continuous end unloading supply and low storage requirements. A CNG project system is normally designed around the main criteria of annual and daily volume of NG required and route distance.

length and can be made of steel or lighter-weight composite materials – one technology uses coiled small diameter pipe for marine transportation.

The natural gas in small volume , up to 800 MSCF can be tranposted easily thorugh a CNG carrier.

They are widely used in industrial gas storing, natural gas vehicle (NGV) station, transportation, power generating plant, hotel, restaurant etc. High pressure semi-trailer is widely applied in the storage and transportation of natural gas, hydrogen, helium, purified gas, etc.

This technoly enables gas transportation to remote area just similar to diesel transport. The

module can be custom made to meet the local infrastructure in remote area in term of using as motor vehicle fuels or small scale power generation. Similar economic apply in term of utilizing coal versus CNG for smaller scale power plants. Economic advantage in term of investment to burn clean “coal” versus natural gas will be elaborated in the next papaer.

Table 2: CNG Economics

3 I II III IV

Crude Price $/BBL 90 80 100

Well head gas price: $/MMBTU* 13.50 12.00 15.00 10.00 90% of crude price, compressed to 2500 PSI

Toll Fee to depot or CNG truck $/MMBTU 0.68 0.60 0.75 0.50 5% of well head price

gate price $/MMBTU 14.18 12.60 15.75 10.50

pump/ distribution margin, 3% 0.43 0.38 0.47 0.32 3% of CNG price

pump price 14.60 12.98 16.22 10.82

VAT 10% 1.46 1.30 1.62 1.08

Pump Price post VAT $ 16.06 14.28 17.84 11.90

Price /liter IDR 5,759 5,119 6,398 4,266

IDR/USD IDR/$ 9,500 9,500 9,500 9,500

Calculation in table 2 coupled with gas economics in table 1 demonstrated that a liter equivalent of natural gas can be sold around IDR 5,000 – 6,000 per liter equivalent. If the government can improve the contractor take to 50/50, rather than 70/30, the well head natural gas price can be reduced to $10/MMBTU and the pump CNG price can be reduced to as low as IDR 4,266/liter equivalent.

What GoI can do to increase Indonesian

Gas production for Domestic

useWe know the GoI wants to increase oil and gas production and to maximize the use of natural gas for its domestic market. The effort should focus on how to monetize oil and gas resources efficiently and quickly. The GoI should maximize exploiting the oil and gas to build the country while protecting the environment from irresponsible development. This will need to revisit the execution of national energy policy.

There are opportunities and challenges for the Indonesian Oil and Gas Industry, and the GoI and Investors can work together to resolve them on the exploration and development front. In the exploration area, the opportunity comes as industry growth moves from acquisitions to

exploration since the oil price increases starting in early 2004. In a high crude price environment, the industry is cash long and opportunity short. Indonesia has good prospects, the attractive incentives for will surely attract more interest if other negative factors impairing or lengthening the time of exploration success to first commercial production can be reduced.

The challenges remain high as the international oil and gas companies retain tight capital discipline, whilst Indonesia is competing for capital with more countries than ever before. Indonesia’s high service cost environment and lack of availability of equipment & services are obstacles that GoI needs to speed up in resolving. Also complicating the investment picture is the uncertainty in law, regulation and taxes with highly bureaucratic procurement process.

Conclusion and Recomendation

We are also aware that business decisions are sensitive to the time-value of money. NPV, IRR and Investment Efficiency are used to measure the robustness of an investment decision. Longer procurement and development time reduces NPV. Longer cash return circle reduces NPV. Obviously, the GoI imposed bureaucracy has negative impact on NPV and hence lower the investors expected return.

The GoI needs to be aware of the effect of WACC, which is not “cost- recoverable”. A 20% IRR project will be rejected by the investor if its WACC is in the typical 15% to 25% range (depends on the reputation and the risk profile of the company). Most of Indonesia’s recent oil discoveries are marginal with reserves less than 100 MBO, whereas investors are looking for 30% to 40% IRR projects. GoI approval and procurement bureaucracy are the major negative contributors to NPV, not to mention the reputation damage due to delay of retendering and obtaining permits.

The challenges are:

Lower PSC bottom line take of GoI from 70% to circa 50%

Apply IFRS accounting concept, where cost of fund is part of operating expenses

Minimize local entry barrier,s make one window permit to get all required permits for project execution

Expedite the exploration success to production cycle through debureaucratic current tendering and controlling procedures

Simplify the system where applicable

1. Create an incentive program for car user to use CNG, such as:

Lower motor vehicle ROAD TAX due to using environmental friendly-clean fuel

Provide free Conversion kit from gasoline to CNG to motor vehicle users.

Encourage car producer to sell CNG car by giving higher tax credit incentives

A fair market driven energy prcing policy that will create efficient gas market supporting the calculated risked return of petroleum economic.

The government needs to respond to the challenges quickly, the longer the government waits, the more budget will go to subsidy of fuel which is non productive, the fund can be diverted to educate and build a better Indonesia. The moment is now as Indonesia has received favorable rating of Baa3 with stable outlook for investment from Moody’s; BB+ from S&P and BBB- from Fitch. These represent the positive encouragement to the political stability in Indonesia with sustainable strong GDP growth above 6% p.a.

Epilog

Due to time constraint, the writer has limited his research and discussion to economic expectaion from private investors and national interest in utilising utilising natural gas to replace liquid fuel. The willingness and ability to utilise CNG in lieu of gasoline to reduce subsidy, reduce oil import and utilize otherwise uptapped or other wise wasted clean and environmental friendly energy named natural gas. This paper has not covered in details on the switching of natural gas to coal for its economic benefit and envrornmental friendly character. The idea can further be elaborated with more research and acation from both government and investors. The paper is jsut a start to further elaborate mechanism to work out the implemenation plan, It takes two to tango!

Reference

1. Law No.22, Year 2001.

2. PWC report on Indonesia Oil and Gas: Exploring the Black Gold* Investor Survey of the Indonesian oil and gas industry-2008 & 2005.

3. PWC 2012 Oil and Gas in Indonesia: Investment and Taxation Guides, 5th edition, May 2012.

4. Tjendrasa, Kinsenary, Exploring the Hidden reason of Low Investment in Indonesian Upstream Oil and Gas Exploration and Development. The 29th Pan

Pacific Conference in Haikou, Hainan Island, Chine May 24-27,2012 .

5. Tjandranegra, Abdul Qoyum: GAS BUMI SEBAGAI

SUBSTITUSI BAHAN BAKAR MINYAK:

OPTIMASI INVESTASI INFRASTRUKTUR DAN

ANALISIS DAMPAKNYA TERHADAP

PEREKONOMIAN NASIONAL, a desertation to

defense his Doctorate degree from University of Indonesia; July 2012.

6. Natural Gas Use in the Transportation Sector – Center for Climate and Energy Solution, May 2012. 7. Indonesian Law no.22/2001 on Oil and Gas.

8. Wood MacKenzie July 2012: Price Increases boost Indonesia gas developments.

9. Ministry of Energy and Mineral Resources report: 2011 Hand book of Energy & Economic Statistics of Indonesia.

10. BP 2012 Statistics on Oil and Gas.

Chris Newton, Revisiting The Challenge, 1.3 MMStb/day in 2009; Continuing and Sustaining investment effort to enhance energy sector activities

Priyono, R. OIL & GAS IN THE PRIMARY ENERGY MIX: Bridging Fuel for Economic Growth Sustainability; 23-25 May 2012, the 36th IPA

convention

Brodjonegoro, Bambang S: Fiscal Policies for Oil and Gas Industry in Indonesia – 23-25 May 2012, the 36th IPA convention

Santoso, Hendi Prio, Meeting Indonesian Energy Needs; 23-25 May 2012, the 36th IPA convention