To: Members of the Passenger Transport Pension Fund Committee

Appropriate Officers

NOTICE OF COMMITTEE MEETING

You are hereby summoned to a meeting of the South Yorkshire Passenger Transport Pension Fund Committee to be held at the offices of South Yorkshire Pensions Authority, Regent Street, Barnsley, S70 2HG at 12.00 pm on Monday 19 June 2017 for the purpose of transacting the business set out in the agenda.

D Terris

Clerk to the Combined Authority

This matter is being dealt with by: Gill Richards Tel: 01226 772806 Email: [email protected]

Distribution

Councillors I Auckland, D Leech (Chair), D Lelliott, G Lindars-Hammond and B Mordue.

Terms of Reference of the South Yorkshire Passenger Transport Pension Fund Committee

The functions of the Authority as an administering body under the Local Government Pensions Regulations.

Contact Details

For further information please contact: Gill Richards

Joint Authorities Governance Unit 18 Regent Street, Barnsley, South Yorkshire S70 2HG Tel: 01226 772806 [email protected] Andrew Shirt

Joint Authorities Governance Unit 18 Regent Street, Barnsley, South Yorkshire S70 2HG Tel: 01226 772207 [email protected]

SOUTH YORKSHIRE PASSENGER TRANSPORT PENSION FUND COMMITTEE MONDAY 19 JUNE 2017

TIME AND VENUE:- 12.00 PM AT THE OFFICES OF SOUTH YORKSHIRE PENSIONS AUTHORITY, REGENT STREET, BARNSLEY, S70 2HG

Agenda: Reports attached unless stated otherwise

Item Page

1 Apologies.

2 Announcements.

3 Urgent items.

To determine whether there are any additional items of business which by reason of special circumstances the Chair is of the opinion should be considered at the meeting; the reason(s) for such urgency to be stated.

4 Items to be Considered in the Absence of the Public and Press.

To identify items where resolutions may be moved to exclude the public and press. (For items marked * the public and press may be excluded from the meeting).

5 Declarations of interest by individual Members in relation to any item of business on the agenda.

6 Minutes of the meeting held on 27 March 2017 1 - 8

7 Minutes of the Joint Local Pension Board held on 16 March 2017 9 - 16

8 Update on matters arising since the last meeting Verbal Report

9 Work Programme 17 - 20

10 Local Authority Pension Fund Forum - January 2017 Meeting 21 - 22

11 Barnett Waddingham Review of Bond Benchmark and De-Risking Mechanism

Item Page

12 6 Monthly Administration Review of the South Yorkshire Passenger Transport Pension Fund for the period 1st October 2016 to 31st March 2017

35 - 38

13 Governance Compliance Statement 39 - 54

14 Investment Pooling: Update

Verbal Report

SHEFFIELD CITY REGION COMBINED AUTHORITY

SOUTH YORKSHIRE PASSENGER TRANSPORT PENSION FUND COMMITTEE 27 MARCH 2017

PRESENT: Councillor D Leech (Chair)

Councillors: I Auckland, D Lelliott, G Lindars-Hammond and B Mordue I Baker (Pensions Manager SYPA), S Barrett (Interim Fund Director), F Bourne (Administration Officer SYPA), M McCarthy (Deputy Clerk), S Smith (Head of Investments SYPA) and C Tyler (Principal Policy and Communications Officer)

E Lambert (Advisor)

Apologies for absence were received from G Chapman, A Frosdick and M McCoole

1 APOLOGIES.

Apologies for absence were noted as above.

2 ANNOUNCEMENTS.

None.

3 URGENT ITEMS.

None.

4 ITEMS TO BE CONSIDERED IN THE ABSENCE OF THE PUBLIC AND PRESS.

None.

5 DECLARATIONS OF INTEREST BY INDIVIDUAL MEMBERS IN RELATION TO

ANY ITEM OF BUSINESS ON THE AGENDA. None.

6 MINUTES OF THE MEETING HELD ON 13 FEBRUARY 2017

At item 14 – Quarterly Report to 31st December 2016, it was noted the benchmark

is quoted in respect of the fiscal year, not calendar.

RESOLVED, that the minutes of the meeting of the Committee held on 13th

February be agreed and signed by the Chair as a correct record.

7 UPDATE ON MATTERS ARISING SINCE THE LAST MEETING

Page 1

SYPTPFC 27/03/17

None.

8 WORK PROGRAMME

The Committee was presented with the Work Programme for note and consideration.

9 LOCAL PENSION BOARD

Members were advised the Local Pension Board (LPB) is now well established and meeting regularly.

The LPB benefits from having a former First Group employee as a sitting member (a move made by First Group nationally).

It was further noted the LPB has a full Terms of Reference, good levels of member attendance bot at meetings and on training courses and is positioned to provide a good level of challenge to officers.

10 DE-RISKING TRIGGER MECHANISM

S Barrett provided the Committee with an explanation of the de-risking trigger mechanism noting that essentially, if a fund achieves a certain level of over-performance, this facilitates the capability to transfer assets from equities to bonds. It was noted this action has never been taken but is something the Committee needs to remain mindful of.

11 ACTUARIAL VALUATION

A report was received to provide Members with the final outcomes of the 2016 triennial actuarial valuation of the South Yorkshire Passenger Transport Pension Fund.

Members were reminded that at the November 2016 meeting, a presentation from the actuary was received which provided the provisional results for the 2016 valuation exercise, including the assessment of a revealed notional deficit of £24.88M representing a funding level of 89% (an improvement of 3% from the last valuation) and an average employer’s future accrual contribution rate of 30.5% (an average increase of 7.4% from the last valuation).

It was further noted that following discussions with the actuary, Members agreed the actuarial assumptions to be used and were made aware that provisional results had been issued to the employer, and Members also agreed that the current deficit plan would be maintained, with an additional payment of £1.15m on 31st March 2024.

It was confirmed that this year’s deficit payment of £3m has been received. The report noted the actuary has now completed his calculations and Members were provided with the valuation report (attached at Appendix A to the covering report).

SYPTPFC 27/03/17

The report also noted that following consultation with the employer, the overall final result is unchanged from that previously notified although the contribution payment requirements have been stepped over the three years instead of a single rate throughout. However the average rate remains as previously notified.

E Lambert suggested the report presents ‘good news’ and evidence of good progress towards the target of achieving a 100% level of funding.

RESOLVED, that the Committee Members approve the valuation results and note the contents of the valuation report.

12 FUNDING STRATEGY STATEMENT

Members were provided with the revised Funding Strategy Statement.

The report noted that the Pension Regulations require the Authority to prepare, maintain and publish a written statement setting out their funding strategy and in doing so, regard must be had to the guidance published by CIPFA and its own Investment Strategy Statement (ISS), must be revised in accordance with any change in policy on the matters set out in the statement and any material change to the ISS and, in particular, must be revised so that the actuary can take account of it when preparing his report on the triennial valuation.

It was noted consultation has taken place with First Yorkshire and there have been no material changes to the initial valuation results or funding plan. The employer has also been consulted on the funding strategy statement and requested no amendments.

The updated version of the Statement was attached to this report. It was noted this has been revised to incorporate references to the current valuation and has been reviewed by the Actuary.

The report directed members’ attention to the principles contained in the statement and in particular the objectives to achieving the funding target (described in

section 5 of the report).

The report noted that following final approval, the Statement will be published via the Pensions Authority’s website and be included in the formal Annual Report. RESOLVED, that the Committee Members approve the revised Funding Strategy Statement.

13 INVESTMENT POOLING: UPDATE

Members were provided with an update in respect of the intention of First group to merge their 3 pension schemes (South Yorkshire, West Yorkshire and Greater Manchester) into 1 scheme (to be held by Greater Manchester).

SYPTPFC 27/03/17

It was noted DCLG civil servants have indicated they supportive of the principles under consideration and confirmed there would be consultation with all affected parties prior to any transfer or asset and liabilities.

It was again noted that as the pooling would likely take place prior to the

instauration of the Border to Coast Pension Partnership and therefore not be part of the Partnership transfers.

It was recognised the pooling is for the administrative convenience of the

employer and not reflective of the excellent management of the fund by the South Yorkshire Pensions Authority.

It was noted that S Smith and G Chapman sit on the transition project

management team (Project Magpie) and the transfer would be formally reported to Members once complete.

Cllr Lindars-Hammond questioned whether breaking the close relationship

between local pensions and a localised service would be to their detriment. It was acknowledged there would be implications for scheme members due to the loss of localisation. It was noted there are currently 4 satellite officers across South

Yorkshire that members drop in at for meetings or to receive face to face assistance, but this will be largely replaced by telephone and online interaction. Cllr Lindars-Hammond asked if there would be any impact on the main fund. It was suggested the relatives sizes of the fund (£7bn rising to £40bn as part of the BCPP versus £300m) means this won’t be an issue.

E Lambert suggested the transfer should be a relatively simple process and won’t be beset by the complications that would arise if the fund was already an intrinsic part of the main fund. It was also noted the Probation Service had recently made moves to ‘pool’ its funds, suggesting this demonstrates general moves nationally towards achieving administrative efficiencies.

The Chair suggested the work officers have done for the Fund to date has been brilliant and noted a hope that the transfer goes smoothly.

14 INVESTMENT STRATEGY STATEMENT

A report was received seeking Members’ approval of the Investment Strategy Statement (ISS) (attached to the report). It was noted this is an updated version of the strategy previously outlined in the Statement of Investment Principles (SIP) which was subject to regular review.

It was noted that administering authorities are required to publish the new

Statements by 1 April 2017 in accordance with the provisions of regulation 7 of the Local Government Pension Scheme (Management and Investment of Funds) Regulations 2016.

It was confirmed the pooling of investments has given rise to new regulations which require an ISS. Members’ attention was therefore drawn to section 4 of the ISS – Approach to Asset Pooling.

SYPTPFC 27/03/17

Acknowledging the risk of BCPP pooling intentions not coming to fruition, consideration was given to whether a review of the ISS should be imminent. However, it was suggested the existing Strategy is progressive enough to provide assurance of its robustness. It was also noted the de-risking trigger mechanism exists as a further safeguard.

It was noted the Statement must also set out the maximum percentage of the total value of all investments of fund money that it will invest in particular investments or classes of investment and be kept under review and revised from time to time and at least every three years. This information was provided at section 2.7 of the ISS and highlights planned reductions in UK and Overseas Equities and increases in Bonds.

The report noted the ISS references the Authority’s compliance with both the ‘Myners’ corporate governance principles and the Financial Reporting Council’s (FRC’s) UK Stewardship Code. The ISS has also been subject to consultation with the Fund’s actuary, the Fund’s independent external advisor and the Local

Pension Board.

RESOLVED, that the Investment Strategy Statement (ISS) be approved and reviewed at least every three years.

15 THE PRINCIPLES OF INVESTMENT GOVERNANCE IN THE LGPS

A report was received to remind Members of the process regarding compliance with the Principles for Investment Governance in the Local Government Pension Scheme.

It was noted Members have adopted a system of self-assessment which will enable the Fund to comply with the requirements of the Principles for Investment Governance in the Local Government Pension Scheme (attached at Appendix A to the report).

It was noted the self-assessment process will consist of three separate forms (assessment of the Committee, assessment of the Chair and assessment of the Investment Advisor). In order to facilitate benchmarking, forms will be personalised where possible to show the scores given in the previous year by individual

Members.

Th report noted individual copies of the self-assessment template will be posted to Members immediately after the meeting. Members are requested to return them, duly completed, to the offices of the Combined Authority by 30 April 2017. Any development needs that arise from the self-assessment will be addressed as part of the Member learning and development schedule.

E Lambert noted South Yorkshire is one of the few areas to have adopted a proactive assessment and evaluation process.

RESOLVED, that the Committee Members:

SYPTPFC 27/03/17

1. Note the report.

2. Confirm their commitment to the self-assessment process. 3. Agree to any development needs arising from the results.

16 MEETINGS OF THE PASSENGER TRANSPORT PENSION FUND COMMITTEE

IN 2017/18

A report was received providing the proposed Committee meeting dates to September 2017.

It was noted this are timed to accord with meetings of the Combined Authority’s

Transport Committee, for which future meeting dates are as follows: 8th May 2017,

19th June 2017, 31 July 2017 and 25th September 2017.

However, it was suggested that due to the nature of the business to be transacted, the May and July meetings may not be required. Members were asked to hold all dates in the interim and assured that any deferrals will be confirmed as early as possible.

The report reminded Members that in deciding the optimum meeting cycle, business will be conducted in a timely manner and stand-alone meetings can be arranged where necessary. Members were therefore asked to note that the Committee’s meeting cycle might need to be varied in due course to

accommodate matters arising out of the Investment Pooling timetable.

RESOLVED, that the Committee Members note the current cycle of meeting dates.

17 VOTING GUIDELINES

A report was received seeking Members’ consent to the retention of the current voting guidelines.

It was noted the Fund’s UK voting guidelines, as one of the Pensions Authority’s suite of corporate documents, is reviewed annually and were last amended in April 2016. Officers have now had the opportunity to review them in conjunction with the Authority’s corporate governance advisor, PIRC, and in the light of best practice there are no further revisions to be made.

The report reminded Members that officers’ review individual resolutions at company meetings and that the voting guidelines are overridden if necessary. The current UK voting guidelines were attached for reference.

Regarding risk implications, the report noted the Committee is the formal decision-making body for issues relating to the Passenger Transport Pension Fund and as such is responsible for its responsible investment strategy. As responsible

investment is an investment objective of the Authority there may be an

SYPTPFC 27/03/17

unquantifiable risk if the Authority’s voting guidelines are not reviewed regularly in order to reflect legislative changes. There is also a reputational risk associated with non-compliance with agreed objectives.

RESOLVED, that the Committee Members note the report.

18 RESPONSIBLE INVESTMENT: ENGAGEMENT REPORT

Members were presented with a report on Responsible Investment engagement activities.

It was noted the Pensions Authority is fully committed to responsible investment and the good stewardship of its investments and recognises that investment in a company not only brings rights but also responsibilities and, as the Authority therefore believes that good governance in the companies in which it invests is best achieved by ensuring that directors are held accountable for their stewardship of the company, it also regards its voting rights as an asset and uses them

carefully, exercising them in accordance with company law for all UK listed companies in which there is a holding.

It was noted that although the Authority will engage directly where appropriate, all of the activity over the current financial year has been directed via the Local Authority Pension Fund Forum (LAPFF).

The report provided information regarding where the Forum has been engaged with a number of companies on various issues and at which, South Yorkshire has been a ‘scene setter’ for championing responsible investments.

RESOLVED, that the Committee Members note the contents of the report.

CHAIR

SHEFFIELD CITY REGION COMBINED AUTHORITY/SOUTH YORKSHIRE PENSIONS AUTHORITY

JOINT LOCAL PENSION BOARD 16 MARCH 2017

PRESENT: G Boyington (Unison) (Chair)

G Berrett (Employer, SYP), S Carnell (Scheme Member), N Doolan-Hamer (Unison), A Hurst (Sheffield CC), K Morgan (UCATT), S Ross (Scheme Member), J Thompson (Employer, Action Housing) and G Warwick (GMB)

Officers: S Barrett (Interim Fund Director), G Chapman (Head of Pensions Administration), M McCarthy (Deputy Clerk), G Richards (Democratic Services Officer) and S Bradley (Audit Manager, BMBC)

Apologies for absence were received from Councillor T Corden

1 WELCOME AND APOLOGIES

The Chair welcomed everyone to the meeting noting that it was the first meeting for Councillor A Hurst, representing Sheffield CC as an employer.

Apologies were noted as above.

2 DECLARATIONS OF INTEREST

None.

3 MINUTES OF THE MEETING HELD ON 6 OCTOBER 2016

With regard to the vacancy for an Academy representative on the Board, M

McCarthy informed members that after advertising the position again recently, there had been seven requests for information and two completed application forms returned. The closing date was Friday 17 March. He would be in touch with the Chair and Vice-Chair with regard to the interview process.

There had been no material changes to the Risk Register, therefore it had not been included on the agenda. It would be on the agenda for the July meeting.

With regard to an employer representative for the Passenger Transport Pension Fund, in view of the likelihood of the Fund being transferred to Greater Manchester Pension Fund in the future, it was decided to seek an alternative employer

representative. It was agreed that if there were suitable applicants to appoint two Academy representatives.

Page 9

SCRCA/SYPA JOINT LOCAL PENSION BOARD 16/03/17

It was agreed to remove item 5.1 – Monitor the validity of any discretions made by the employers/Administering Authority from the Terms of Reference as it wasn’t relevant to the Board.

With regard to the need for indemnity insurance for the Board, although the risk was remote, officers were looking into including cover for the Board in the new insurance policy which was due for renewal if the cost was not prohibitive.

M McCarthy informed the Board that the website had recently been updated so the Local Pension Board section was on the front-facing page; further information would be added in the near future.

RESOLVED – That the minutes of the meeting of the Board on 6 October 2016 be agreed as a true record.

4 WORK PROGRAMME

The Board considered its Work Programme.

G Berrett questioned whether the Administration Strategy would be reviewed annually.

G Chapman replied that it would be looked at in April and any revisions taken to the October meeting of the Authority.

The Chair requested that the Board review this at their July meeting for input before the Authority meeting in October.

G Chapman agreed that if there were to be any revisions a report would be brought to the Board.

With regard to the Board’s input into the Authority’s Annual Report, this would have to be done by email due to the timings of the Board’s meetings.

G Berrett questioned when the Board was going to review Internal Audit recommendations. It was noted that this was already done by the Corporate Planning and Governance Board but the Board received electronic links to all agendas and therefore could access all reports.

It was agreed that an email would be sent to members to flag any reports that were relevant to the LPB and invite comments.

With regard to the appointment of external auditors, the Authority had decided to opt in to a sector led procurement scheme where an Appointed Person appointed the external auditor on the Authority’s behalf.

SCRCA/SYPA JOINT LOCAL PENSION BOARD 16/03/17

5 THE ROLE OF INTERNAL AUDIT

Audit Manager, Sharon Bradley informed the Board that Barnsley MBC delivered the Internal Audit Service for the Pensions Authority (this is a statutory function), their other clients were:

South Yorkshire Fire & Rescue

South Yorkshire Police & Crime Commissioner and Chief Constable

Sheffield City Region Combined Authority

South Yorkshire Passenger Transport Executive

Berneslai Homes; and

Barnsley MBC

Sharon explained the Institute of Internal Auditors definition of Internal Audit – the most recent developments being around the consultancy approach for Internal Audit, to enable Internal Audit to work with Clients (not “do to”) and therefore provide an added value service.

The Internal Audit Team was governed by the Public Sector Audit Standards and there are several principles within these. The Internal Audit service were required to undertake a comprehensive self-assessment annually and also commission an external assessment every five years. The external assessment was undertaken last year and the Service were found to be fully compliant. The assessments form part of the effectiveness of Internal Audit reports that were presented annually/six-monthly to the CP&GB.

Each year an Internal Audit Charter and Strategy was presented to the Authority (CP&GB). This details the purpose, objectives and approach adopted by Internal Audit. Additionally, the Head of Internal Audit prepared an Annual Audit for the CP&GB, to provide for an overall assurance opinion of the effectiveness on the Risk, Governance and Control Framework, based on the broad coverage of Internal Audit work undertaken during the year.

A risk-based Annual Internal Audit Plan was also prepared, in consultation with the Corporate Planning & Governance Board members, the Statutory Officers and the Authority’s Senior Management Team. The Plan details the number of days

allocated annually to the Authority and the title and scope of the audits. This year 245 days had been assigned to the Authority, which was slightly less than the previous year. The Plan was designed to be flexible and to prioritise resources. Quarterly updates were provided to the CP&GB. Sharon also had regular plan update meetings with a member of the SMT.

The Chair thanked S Bradley for attending the meeting.

6 LGPS POOLING UPDATE

G Boyington referred the Board to a string of emails between the Chairs of Local Pension Boards regarding scheme member representation at pool level.

SCRCA/SYPA JOINT LOCAL PENSION BOARD 16/03/17

The first email had been received from the Chair of Tyne and Wear Local Pension Board the day before the Extraordinary meeting of SYPA to discuss their

membership of the Border to Coast Pension Partnership.

At that meeting the decision was deferred and the Chair was asked to contact the other Chairs of the proposed pool members to ascertain their opinions on scheme representation at pool level.

As with the Chairs of the Local Pension Boards, the Authority Chairs’ opinion was split, but with the majority being in favour of non-voting scheme member

representation.

The Authority had approved an amended report at their meeting earlier in the day that supported scheme member representation.

The Board also commented on the current staff of SYPA and the need to ensure that they were not adversely affected, whether they were transferring to the pool or remaining with the Authority.

S Barrett informed the Board that discussions were in the early stages but every effort would be made to ensure that all staff were happy with the arrangements.

7 THE PENSIONS REGULATOR SELF-ASSESSMENT TOOL

The Pensions Regulator had issued a self-assessment tool for those involved in running a public service pension scheme to help identify issues and actions to take to improve governance and administration of the scheme.

G Chapman informed the Board that he had taken the assessment informally and, although there was some room for improvement, the results were generally good. The restructure would strengthen the technical team and this would help further with achieving compliance.

The self-assessment results would go to the Authority at the October meeting to reassure the Authority regarding compliance and the plan in place to address any issues.

An interim report would be submitted to the July meeting of the Local Pension Board to enable the Board to comment on the position.

8 INVESTMENT STRATEGY STATEMENT

The Board considered the Investment Strategy Statements (ISS) for South Yorkshire Pensions Authority and the South Yorkshire Passenger Transport

Pension Fund. These were updated versions of the strategies previously outlined in the Statement of Investment Principles. Pooling of investments had given rise to new regulations including a change of name to Investment Strategy Statement..

SCRCA/SYPA JOINT LOCAL PENSION BOARD 16/03/17

The Investment Board had approved SYPA’s ISS on 9 March 2017 and the SYPTPF ISS would be submitted to the meeting on 27 March 2017.

9 FUNDING STRATEGY STATEMENT

The Board were informed that the Authority had approved a revised Funding Strategy Statement at its meeting earlier in the day; a revised Funding Strategy Statement would be submitted to the Passenger Transport Pension Fund

Committee on 27th March 2017.

The Funding Strategy Statements had been amended to align with the Investment Strategy Statement.

SYPA funding level had risen to 85% and the ISS proposed a shift in investment classes to build on the long term strengths of the fund.

The Passenger Transport Pension Fund was in a different position as it was a closed fund with approximately 150 members and was 92% funded. There had been no shift in core investment strategy.

10 ANNUAL FUND MEETING SURVEY

The Board considered a report to inform of the results of a survey carried out among Scheme members who had attended the Annual Fund meeting.

The meeting had been attended by 62 delegates, 41 of whom returned a completed survey.

Members preferred the amended format where Q & A sessions were held after every presentation rather than at the end of the meeting with 95.12% of delegates agreeing this was better.

Overall the delegates were satisfied with most elements of the meeting, the main concern being the length of the bus journey from Sheffield. Officers had agreed to look at this before the next meeting.

11 FEEDBACK FROM CIPFA LPB SPRING SEMINAR

Several members of the Board had attended the CIPFA/Barnett Waddingham Local Pension Board Spring Seminar in Leeds on 1 March 2017.

Members had found it useful to varying degrees; it was thought that the section on record keeping had not been relevant.

S Ross felt that it had been useful to meet other Board members and learn what their Boards were doing.

Members were disappointed there had not been a more involved discussion on the subject of member-nominated representatives’ involvement in pensions pooling

SCRCA/SYPA JOINT LOCAL PENSION BOARD 16/03/17

arrangement, despite the lack of guidance from the government or the Scheme Advisory Board.

Members were unsure overall if the event had been a worthwhile use of expenditure.

12 COMMUNICATIONS BETWEEN THE SY JOINT LOCAL PENSION BOARD,

SCHEME MEMBERS AND EMPLOYERS

The Board discussed their ability to communicate with Scheme members. It was felt that this was an area that could be progressed; active Trade Union

representatives already had the ability to communicate with their members whereas it was more difficult for other members of the Board.

G Chapman informed the Board that all the Authority’s channels of communication was at their disposal, including social media, the website, employer systems and space in the newsletter. Surveys could also be conducted if the Board required feedback.

The Chair commented that it was important for Scheme members to know who the Board were, what they did and how to get in touch with the Board.

G Warwick thought that communications could be used to advise Scheme members in certain areas e.g. capping final payments, although it would be

important to make clear that any views expressed were those of the Board and not the Authority.

The Chair requested the Board be informed when the next newsletter was in production so the Board could consider if they wanted to have something included. M McCarthy suggested including a Communications Strategy in the Annual Report; this was agreed.

13 LPB BUDGET

The Board noted its budget, the majority of which had been spent on training and travel costs.

It was agreed the budget would remain at £10,000 for the next financial year; there may need to be some provision for indemnity insurance.

14 MEETING CYCLE REPORT

The Board considered the meeting cycle for 2017/18.

Meetings were scheduled after meetings of the Authority or Corporate Planning and Governance Board; it was felt that Investment Board meetings were too long to schedule a further meeting afterwards. Members were always welcome to attend an Investment Board meeting if they so wished.

SCRCA/SYPA JOINT LOCAL PENSION BOARD 16/03/17

Meeting dates were confirmed as: 20 July 2017

5 October 2017 18 January 2018 15 March 2018

15 LPB TRAINING EVENTS

The Board considered training events attended by members during the year. Further events would be offered as they became available and the Board would continue to be invited to all Authority training sessions.

16 ANY OTHER BUSINESS

None. CHAIR

Updated 8.6.17

SHEFFIELD CITY REGION COMBINED AUTHORITY

South Yorkshire Passenger Transport Pension Fund Committee

Work Programme

Page 17

Updated 8.6.17

7 November 2016 13 February 2017 27 March 2017 19 June 2017 25 September 2017

Minutes Minutes Minutes Minutes Minutes

Local Pension Board Local Pension Board Local Pension Board Local Pension Board Local Pension Board Verbal update on

matters arising since last meeting

Verbal update on matters arising since last meeting

Verbal update on matters arising since last meeting

Verbal update on matters arising since last meeting

Verbal update on matters arising since last meeting

External Training Events External Training Events External Training Events External Training Events External Training Events LAPFF Minutes

LAPFF Conference

LAPFF Minutes LAPFF Conference

LAPFF Minutes LAPFF Minutes

De-risking Trigger Mechanism De-risking Trigger Mechanism De-risking Trigger Mechanism Review of Bond Benchmark and de-risking Mechanism Actuarial Valuation Initial Results Actuarial Valuation (verbal update) Actuarial Valuation Report 6 Monthly Administration Review Government Actuary Department Report Funding Strategy Statement Governance Compliance Statement

Pooling: Verbal Update Pooling Report Pooling: Verbal Update Pooling: Verbal Update Pooling: Verbal Update 6 Monthly

Administration Review FoIA Annual Report Investment Strategy Statement SYPTPF Quarterly Report SYPTPF Quarterly Report SYPTPF Quarterly

Report SYPTPF Quarterly Report Members/Advisor Self-Assessment Annual Report

Annual Report and Accounts

IMA Level 1 Disclosure Notice

Meeting Cycle Dates Shareholder

Engagement Statement IMA Level 2 Disclosure Notice Voting Guidelines

Updated 8.6.17

7 November 2016 13 February 2017 27 March 2017 19 June 2017 25 September 2017

Statement of Investment

Principles Responsible Investment Engagement Report

Corporate Class Actions EU Member State Tax Rules Potential Tax Refunds

Summary

To inform Members that the minutes of the January 2017 business meeting have been issued.

1. Issue

To notify Members that the minutes of the January meeting have been approved and issued.

2. Recommendations

It is recommended that the Committee Members: 2.1 Note the report.

3. LAPFF Business Meeting

3.1 The last business meeting of the Forum was held on 11 April 2017 in London. At this meeting the January 2017 minutes were approved and these will be handed to Members at this meeting.

3.2 The items discussed at the April meeting included the regular reports from the officers of the Forum and the minutes of the last Executive meeting. It was noted that Durham Pension Fund had decided to join taking membership to 73 funds.

3.3 Verbal updates were given on Pooling, the work of the Scheme Advisory Board and the All Party Parliamentary Group. Reports put to the meeting included a paper on cyber risk, an increasing problem for investors and companies. It was agreed that a focused, direct engagement programme be undertaken with a small number of companies where the risk is seen to be the greatest. A presentation was given on the subject by a representative of the PRI (Principles for Responsible Investment). A paper on climate change and investment policy was also put to the meeting; as a result of this a workshop is to be held in June for funds. A member fund previously requested the Forum undertake engagement with Motorola Solutions in relation to activities in Israel; this led to a paper being put to the meeting on Investment in Israel and occupied Palestinian territories. The decision was taken to engage with Motorola and two other companies on human rights policy.

SOUTH YORKSHIRE PASSENGER TRANSPORT PENSION FUND COMMITTEE 19 June 2017

JOINT REPORT OF THE CLERK AND THE DIRECTOR OF FINANCE LOCAL AUTHORITY PENSION FUND FORUM – JANUARY 2017 MEETING

Page 21

3.4 The quarterly engagement report for January to March included comments on holdings based engagement. A follow up collaborative engagement meeting was held with the Rio Tinto Chair to see how the company is making progress complying with elements of the strategic resilience shareholder resolution. LAPFF continues to engage with Sports Direct over employment standards but is still awaiting a meeting with a member of the board. The report also included LAPFF responses to a number of reviews including the Parker Review on ethnic diversity, the recommendations of the Task Force on Climate-related Financial Disclosure, and the Government green paper on corporate governance. 3.5 The next LAPFF Business meeting is scheduled for 27th June in London.

4. Implications

4.1 Financial

There are no financial implications. 4.2 Legal

LAPFF is a collaboration of Local Government Pension Scheme administering authorities. It exists to promote the investment interests of local authority pension funds, and to maximise their influence as shareholders to promote corporate social responsibility and high standards of corporate governance amongst the companies in which they invest, commensurate with statutory regulations.

The Authority has a general discretionary power under Section 111 of the Local Government Act 1972, subject to any other enactment, to do anything which is calculated to facilitate, or is conducive or incidental to, the discharge of any of its functions.

Attendance at LAPFF meetings and conferences and expenditure arising there from is considered to fall within the discretionary powers conferred by Section 111. There are no other legal implications.

4.3 Diversity

There are no diversity implications. 4.4 Risk

This Committee is the formal decision-making body for issues relating to the Fund and as such is responsible for its responsible investment strategy. Responsible investment is an investment objective of the Authority. The employment of an independent advisor to assist the Committee strengthens the governance of decision-making.

Diana Terris/Eugene Walker Clerk/Director of Finance

Officer responsible: Steve Barrett

Interim Fund Director SYPA Tel 01226 772887

Documents used in the preparation of this report are available for examination at the offices of the South Yorkshire Pensions Authority.

Summary

Review of the design of the Bond portfolio Benchmark and de-risking mechanism to consider whether any updates are required to reflect the updated data, assumptions and calculations used for the 2016 Triennial Valuation exercise.

1. Issue

To bring to Members’ attention a report from Barnett Waddingham following on from the 2016 Triennial Valuation.

2. Recommendations

It is recommended that the Committee Members endorse the changes to the bond portfolio benchmark and to the Liability Proxy suggested by Barnett Waddingham. 3. Background information

3.1 The fundamental objective of the Fund is to have sufficient assets to meet liabilities for benefit payments to members as they fall due. Following the actuarial valuation in 2010, the Committee put in place a strategy to reduce the level of the funding level risk by a gradual switch of assets from equities in to bonds in line with the change in the proportion of liabilities in respect of non-pensioners. At the same time the protection portfolio benchmark was adjusted to more closely match the shape and nature of the liabilities. The Fund also has a de-risking mechanism in

SOUTH YORKSHIRE PASSENGER TRANSPORT PENSION

FUND COMMITTEE

19 June 2017JOINT REPORT OF THE CLERK AND THE DIRECTOR OF FINANCE

BARNETT WADDINGHAM REVIEW OF BOND BENCHMARK AND DE-RISKING MECHANISM

Page 23

place such that if the funding position improved faster than expected then this would trigger a quicker move from equities into bonds. This is monitored by measuring a proxy portfolio of index-linked gilts that were chosen so that the total value of the proxy portfolio will move broadly in line with the values of the Fund’s liabilities as market yields change.

3.2 This strategy was reviewed after the March 2013 valuation and the analysis then suggested that the strategy was still appropriate for the Fund. The duration of the liabilities and the bond benchmark remained broadly in line and it was not felt necessary to change the benchmark at that time.

3.3 Following the completion of the March 2016 valuation the Fund’s bond portfolio benchmark and de-risking mechanism was again reviewed by Barnett Waddingham. They used the updated membership data, assumptions and calculations used for the 2016 valuation and checked the validity of the current bond portfolio benchmark and de-risking mechanism.

3.4 Although they say that the current bond portfolio remains reasonable relative to that of the liabilities, they are recommending a change to the bond portfolio benchmark to create a better match for the Fund’s liabilities in terms of duration and rate sensitivity. If this is agreed any changes in the underlying portfolio would be incorporated in the next switch from equities to bonds which occurs at the end of September. They are also recommending a change to the Liability Proxy portfolio which is used by us to monitor the change in liabilities of the Fund under the de-risking mechanism. This does not impact the underlying portfolio.

4. Implications 4.1 Financial

There are no implications. 4.2 Legal

There are no legal implications. 4.3 Diversity

There are no diversity implications. 4.4 Risk

There are no risk implications connected to this report. Diana Terris/Eugene Walker

Clerk/Director of Finance

Officer responsible: Sharon Smith

Head of Investments Tel 01226 772886

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 1 of 10

South Yorkshire Passenger Transport Pension Fund

Review of Bond Benchmark and de-risking mechanism

1.

Introduction

The Committee of the South Yorkshire Passenger Transport Pension Fund (the Fund) previously commissioned Barnett Waddingham to carry out a strategy review in conjunction with the 2013 actuarial valuation. The ‘Investment Strategy Review’ paper dated 20 October 2014 set out our recommendations following this review which included a recommended structure for the Bond Portfolio Benchmark and a dynamic de-risking mechanism.

Barnett Waddingham has now reviewed the design of the Bond Portfolio Benchmark and de-risking mechanism to confirm whether any updates are required to reflect the updated data, assumptions and calculations used for the 2016 valuation exercise (as summarised in the valuation report dated 17 March 2017). The scope of this review has been restricted solely to these matters and therefore does not consider alternative strategy options or de-risking approaches.

This note set out the results of our review and in particular confirms that we suggest updating the current Bond Portfolio Benchmark and Liability Proxy used for the Fund’s de-risking mechanism.

2.

Summary of Fund liability profile

(31 March 2016 valuation)

The table and chart below set out the key characteristics of the Fund’s liability profile that we have identified using the data, assumptions and calculations for the 31 March 2016 valuation exercise, rolled forward to 31 December 2016.

Table 1: Fund Liability profile characteristics Value at 31 December 2016 Present value of liabilities on gilts flat basis £278.9m

Duration of liabilities 15.2 years

Interest rate sensitivity (PV01)* £423,000

Inflation rate sensitivity (IE01)* £382,000

* PV01 = Expected change in value of liabilities (on yield curve basis) due to a 0.01% increase in nominal gilt yields

IE01 = Expected change in value of liabilities (on yield curve basis) due to a 0.01% increase in inflation expectations

Expected benefit cashflow payments (31 Dec 16)

The chart to the left illustrates how the undiscounted expected benefit cashflows from the Fund are expected to evolve over time.

We have run analysis using various inflation sensitivities (allowing for the interaction of inflation caps on benefits) which indicates that the majority of the Fund’s benefits are inflation linked. *Inflated with market implied inflation as published by the Bank of England.

Page 25

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 2 of 10

3.

Review of Bond Portfolio Benchmark

Scope of review To consider whether the current basket of bonds used as the benchmark for the Fund’s Bond Portfolio (set out in table 2 below) remains reasonable for the Fund’s liability profile.

Table 2: Current Bond Benchmark Current Benchmark weighting iBoxx All Stocks Sterling Non Gilts Index 30%

2.5% Index-Linked Gilt 2020 25%

1.25% Index-Linked Gilt 2027 17.5%

1.125% Index-Linked Gilt 2037 15%

0.75% Index-Linked Gilt 2047 7.5%

1.25% Index-Linked Gilt 2055 5%

Analysis carried out Our analysis involved the following steps:

Obtain liability cashflow data (run on a range of inflation scenarios) from the Barnett Waddingham Actuarial Team;

Use these cashflows to determine how the split of fixed and inflation linked cashflows evolves over time;

Calculate the expected cashflows from the current Bond Portfolio Benchmark;

Consider whether the profile, duration, interest rate sensitivity and inflation sensitivity of the Bond Portfolio Benchmark cashflows remain a reasonable representation for the Fund’s liability profile characteristics.

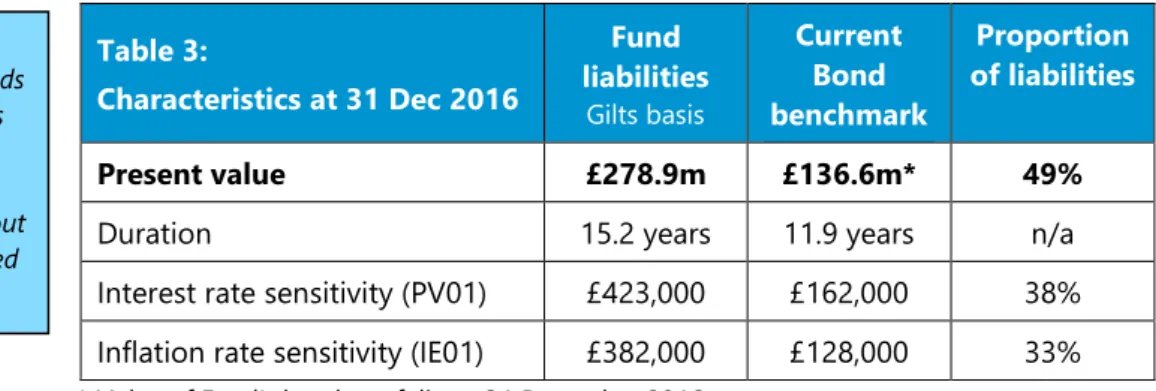

Results of analysis The table below compares the characteristics of the current bond portfolio to the Fund’s liability profile:

Table 3: Characteristics at 31 Dec 2016 Fund liabilities Gilts basis Current Bond benchmark Proportion of liabilities Present value £278.9m £136.6m* 49%

Duration 15.2 years 11.9 years n/a

Interest rate sensitivity (PV01) £423,000 £162,000 38% Inflation rate sensitivity (IE01) £382,000 £128,000 33% * Value of Fund’s bond portfolio at 31 December 2016.

The characteristics of the current Bond Portfolio Benchmark remain reasonable relative to that of the liabilities, although the Bond Portfolio Benchmark is slightly more mature than the term of the liabilities.

It is possible to amend the Bond Portfolio Benchmark weightings slightly in order to more closely match the Fund’s liability profile. We have set out in the section below these proposed benchmark weightings which we suggest the Committee considers replacing the current Bond Portfolio Benchmark with.

As the Fund is not fully invested in bonds nor fully funded, it is not possible to fully match the liability characteristics without considering leveraged LDI strategies.

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 3 of 10

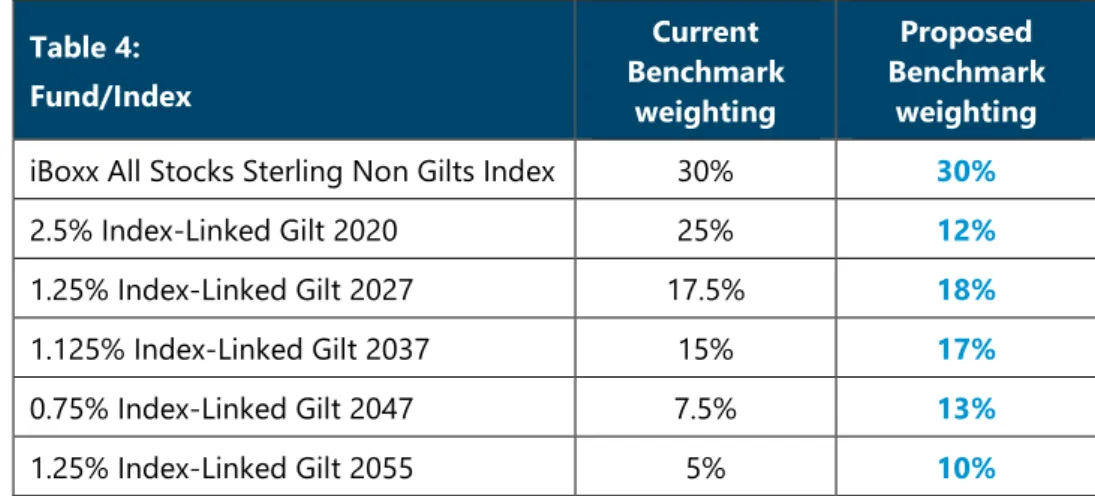

Confirmation of Bond Benchmark

Table 4 below shows how the proposed Bond Portfolio Benchmark compares to the current benchmark in force.

Table 4: Fund/Index Current Benchmark weighting Proposed Benchmark weighting

iBoxx All Stocks Sterling Non Gilts Index 30% 30%

2.5% Index-Linked Gilt 2020 25% 12%

1.25% Index-Linked Gilt 2027 17.5% 18%

1.125% Index-Linked Gilt 2037 15% 17%

0.75% Index-Linked Gilt 2047 7.5% 13%

1.25% Index-Linked Gilt 2055 5% 10%

Table 5 illustrates that this proposed Bond Portfolio Benchmark is a better match for the Fund’s liabilities, in terms of duration and rate sensitivity:

Table 5: Characteristics at 31 Dec 2016 Fund liabilities Gilts basis Proposed Bond benchmark Proportion of liabilities Present value £278.9m £136.6m* 49%

Duration 15.2 years 15.2 years n/a

Interest rate sensitivity (PV01) £423,000 £207,000 49%

Inflation rate sensitivity (IE01) £382,000 £172,000 45%

We recommend that the Committee considers updating the Bond Portfolio Benchmark in line with the proposed allocation set out in table 4. We also suggest that this benchmark is reviewed again as part of the next valuation exercise in 2019. In any case, the benchmark will need to be reviewed prior to the redemption of the 2020 Index Linked Gilt in April 2020.

From discussions in 2014, we understand that the Committee does not currently wish to consider leveraged LDI approaches.

With this in mind, we have assumed that the Fund is targeting a bond benchmark with a similar maturity to the liability profile and PV01and IE01 broadly in line with the proportion of liabilities backed by bonds (i.e. 50% as at 31 December 2016).

The Fund’s post retirement discount rate assumption includes a margin above the return on gilts. Therefore, we have proposed maintaining the same overall allocation to corporate bonds so as not to disrupt this assumption.

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 4 of 10

4.

Review of de-risking mechanism: Liability Proxy and Triggers

Scope of review The current de-risking mechanism was put in place following the 2010 valuation and recalibrated following the 2013 valuation. The mechanism was designed to identify opportunities to accelerate the Fund’s programme of fixed annual switches from growth assets to protection assets.

The scope of this review is to consider whether the basket of government bonds (designed to act as a proxy for the Fund’s liability movements) and the magnitude of the trigger need to be recalibrated to reflect the updated data and calculations carried out for the 2016 valuation.

Analysis carried out Our analysis involved the following steps:

Calculate the expected cashflows from the current Liability Proxy;

Consider whether the profile, duration, interest rate sensitivity and inflation sensitivity of the Liability Proxy cashflows remain a reasonable representation for the Fund liability profile characteristics;

Calculate the expected funding levels at each future monitoring date, which were projected from the 2016 valuation (based on the ongoing funding assumptions);

Based on the above information, calculate appropriate funding position triggers.

Recap of current de-risking mechanism approach:

SYPA fund managers have been issued with a simplified Liability Proxy for the Fund’s liabilities (the “Liability Proxy portfolio”). The Liability Proxy is a basket of 6 single index-linked government bonds whose value is expected to move broadly in line with changes in the Fund’s liabilities over time as market yields change;

Barnett Waddingham LLP also provided the SYPA managers with the expected funding levels at each future monitoring date, which were projected from the 2013 valuation and based on the gilts funding assumptions;

The SYPA managers compare the Liability Proxy portfolio to the value of the Fund’s assets on a quarterly basis to monitor the Fund’s approximate funding position against the expected funding level at that date;

The projections of the funding level act as the trigger for any further de-risking. Trigger levels were set at a level such that the Fund’s assets needed to outperform by more than the additional value that would be placed on the liabilities if the valuation assumptions took account of the post de-risking switch asset allocation.

When a trigger point is achieved (i.e. the actual funding position is higher than the projected funding level), the SYPA managers would switch assets from equities to bonds to attain an overall (pre-set) higher proportion of protection assets;

SYPA fund managers contact Barnett Waddingham LLP if they think a trigger has been hit so that a more accurate funding level calculation can be carried out to verify if an additional de-risking switch should be implemented and confirm the new benchmark.

It should be noted that the calculations carried out by Barnett Waddingham LLP were more accurate than the Liability Liability Proxy used by the SYPA managers but not as precise as the detailed valuations used for a formal actuarial valuation because this simply would not be practical or cost effective. Liability Proxy at 31 Dec 2016: 24% of 2020 IL Gilt 24% of 2027 IL Gilt 21% of 2032 IL Gilt 17% of 2037 IL Gilt 10% of 2047 IL Gilt 4% of 2055 IL Gilt The Liability Proxy allocations drift over time as the bonds in the above basket mature.

This is intended to reflect how the Fund’s liabilities are expected to mature.

A corporate bond allocation is not required in this basket as the de-risking analysis is carried out on a gilts only basis.

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 5 of 10

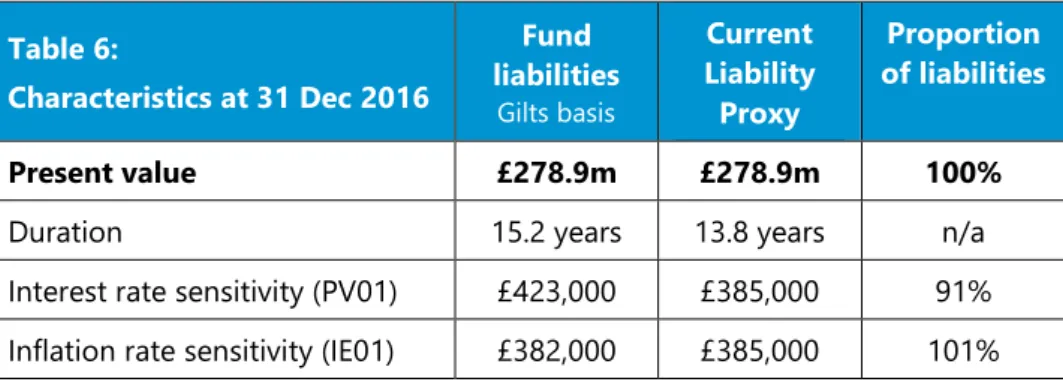

Results of analysis The table below compares the characteristics of the current Liability Proxy to the Fund’s liability profile:

Table 6: Characteristics at 31 Dec 2016 Fund liabilities Gilts basis Current Liability Proxy Proportion of liabilities Present value £278.9m £278.9m 100%

Duration 15.2 years 13.8 years n/a

Interest rate sensitivity (PV01) £423,000 £385,000 91% Inflation rate sensitivity (IE01) £382,000 £385,000 101% * Value of Fund’s bond portfolio at 31 December 2016.

The characteristics of the current Liability Proxy remain reasonable relative to that of the liabilities, although the Liability Proxy is slightly more mature than the term of the liabilities.

It is possible to amend the Liability Proxy weightings slightly in order to more closely match the Fund’s liability profile. We have set out in the section below this proposed proxy portfolio of bonds which we suggest the Committee considers replacing the current Liability Proxy with.

Confirmation of Liability Proxy

Table 7 below shows how the proposed Liability Proxy compares to the current Liability Proxy in force.

Table 7: At 31 Dec 2016 Current Liability Proxy weighting Proposed Liability Proxy weightings 2.5% Index-Linked Gilt 2020 24% - 2.5% Index-Linked Gilt 2024 - 28% 1.25% Index-Linked Gilt 2027 24% - 4.125% Index-Linked Gilt 2030 - 33% 1.25% Index-Linked Gilt 2032 21% - 1.125% Index-Linked Gilt 2037 17% 21% 0.75% Index-Linked Gilt 2047 10% 9% 0.5% Index-Linked Gilt 2050 - 7% 1.25% Index-Linked Gilt 2055 4% - 0.125% Index-Linked Gilt 2058 - 2%

Table 8 compares the characteristics of the proposed Liability Proxy to that of the Fund’s liabilities, in terms of duration and rate sensitivity:

Note: The Liability Proxy allocations drift over time as the bonds in the basket mature (i.e. there is no rebalancing).

This reflects that the Fund’s liability is also expected to mature over time.

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017 RESTRICTED Version 1.0 6 of 10 Table 8: Characteristics at 31 Dec 2016 Fund liabilities Gilts basis Proposed Liability Proxy Proportion of liabilities Present value £278.9m £278.9m 100%

Duration 15.2 years 15.5 years n/a

Interest rate sensitivity (PV01) £423,000 £432,000 102%

Inflation rate sensitivity (IE01) £382,000 £432,000 113%

Although the Fund’s benefits are primarily linked to the change in the Consumer Prices Index, there are some caps on the level of increases applied to Guaranteed Minimum Pensions which results in a small proportion of the Fund’s liabilities having little to no sensitivity to changes in inflation.

This means that in order to create a Liability Proxy that more accurately replicates movements in the Fund’s liability value, we would need to add fixed interest gilts (with a range of maturity dates) to the current Liability Proxy portfolio. However, doubling the number of gilts in the Liability Proxy would significantly increase the administrative complexity for the SYPA investment managers to carry out their quarterly de-risking monitoring check. Therefore, we propose that the benefit of making the Liability Proxy a more accurate match for the nature of the Fund’s liabilities is outweighed by the burden of increased administrative complexity. Instead we have suggested an updated portfolio of 6 index-linked gilts that is expected to have broadly the same interest rate sensitivity but slightly higher inflation sensitivity compared to that of the Fund’s liabilities. This means that the Liability Proxy will be more likely to suggest a trigger has been hit due to movements in expected inflation than would be identified by the more accurate calculations that Barnett Waddingham would carry out. Under the de-risking monitoring process, the SYPA managers will contact Barnett Waddingham if they believe a trigger has been hit. These more accurate calculations would then detect the instances where the Liability Proxy is incorrectly suggesting a trigger has been hit and no de-risking switch would be made.

We believe this approach is preferable to retaining the current Liability Proxy which is expected to be less sensitive to interest rate movements than the Fund’s liabilities and therefore there is the potential that a trigger that would have been identified via Barnett Waddingham’s more accurate calculations is not detected by the Liability Proxy. In this scenario, Barnett Waddingham would not be asked to undertake their more accurate checks and no de-risking switch would be made even though the Fund could be ahead of the expected funding position.

We recommend that the Committee reviews the Liability Proxy again as part of the next valuation exercise in 2019. In any case, this will need to be reviewed prior to the redemption of the 2024 Index Linked Gilt in July 2024.

Note: If the SYPA investment managers believe a trigger has been hit then Barnett Waddingham carry out more accurate

calculations to confirm this.

We have retained the same number of gilts in the Liability proxy basket to maintain the same level of

administrative complexity for the monitoring process. This is done at the expense of adding small allocations to fixed interest gilts across the curve which would match the small proportion of the Fund’s non-inflation linked liabilities.

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 7 of 10

Confirmation of expected development of funding position

As part of our analysis, we projected forward the funding position (on a gilts basis) on a quarterly basis that would be expected if the 2016 valuation assumptions are borne out in practice. The expected deficit at each quarter end is confirmed in Appendix 1.

Confirmation of Triggers

The following table sets out our updates to the estimates of the amounts by which the Fund’s actual funding position would need to be ahead of the expected funding position in order to trigger the respective changes in benchmark (previous trigger levels shown for comparison).

Table 9: Triggers for specified percentage change in benchmark

5% 10% 15%

Approximate amount ahead of expected funding position –

based on 2013 valuation £1.9m £4.9m £7.5m

Approximate amount ahead of expected funding position – based on 2016 valuation

£3.0m £6.0m £9.5m

For example, the Fund’s deficit would need to be at least £3m smaller than the deficit expected at that date based on the 2016 valuation projections in order to trigger a 5% switch from growth assets to bond assets.

Reminder of process Appendix 1 sets out how the de-risking mechanism process operates and confirms our proposals based on the updated analysis.

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 8 of 10

5.

Summary and next steps

We have reviewed the design of the Fund’s bond portfolio benchmark and de-risking mechanism to confirm whether any updates are required to reflect the updated data, assumptions and calculations used for the 2016 valuation exercise.

A summary of the results of the analysis is as follows:

The current Bond Portfolio Benchmark remains broadly reasonable however we suggest the Committee considers making the updates set out in Table 4 to improve the match with the Fund’s liabilities;

The current Liability Proxyremains broadly reasonable however we suggest the Committee considers making the updates set out in Table 7 to improve the match with the Fund’s liabilities;

We have calculated the expected deficit (on a gilts basis) at future quarter end dates based on projections from the 2016 valuation exercise. These are set out in Appendix 1;

We have proposed updated trigger levelsin Table 9.

We would be happy to discuss this paper with the Committee and/or the Investment Managers at the Authority.

Jemma Arfield Chris Binns

Barnett Waddingham LLP Barnett Waddingham LLP

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 9 of 10

Appendix 1

De-risking mechanism process

1. Estimated value of liabilities using Liability Proxy at the quarter end date. Value of liabilities at 31 December 2016 (on a gilts curve basis) = £278.9 million

Basket of gilts at 31 December 2016 to use as a broad measure for changes in the value of the Fund’s Liabilities:

Gilt Proportion at 31 Dec 16

2.5% Index-Linked Gilt 2024 28% 4.125% Index-Linked Gilt 2030 33% 1.125% Index-Linked Gilt 2037 21% 0.75% Index-Linked Gilt 2047 9% 0.5% Index-Linked Gilt 2050 7% 0.125% Index-Linked Gilt 2058 2%

Allocation in this basket of gilts assumed to drift over time (i.e. not rebalanced to above allocation at each quarter end).

Expected cashflows from liabilities:

Period Expected cashflows during period

31 December 2016 – 31 March 2017 £2.6m 31 March 2017 – 30 June 2017 £2.6m 30 June 2017 – 30 September 2017 £2.6m 30 September 2017 – 31 December 2017 £2.6m 31 December 2017 – 31 March 2018 £2.6m 31 March 2018 – 30 June 2018 £2.7m 30 June 2018 – 30 September 2018 £2.7m 30 September 2018 – 31 December 2018 £2.7m 31 December 2018 – 31 March 2019 £2.7m 31 March 2019 – 30 June 2019 £2.7m 30 June 2019 – 30 September 2019 £2.7m 30 September 2019 – 31 December 2019 £2.7m

Page 33

www.barnett-waddingham.co.uk South Yorkshire Passenger Transport Pension Fund – Review of Bond Benchmark and de-risking mechanism – 17 May 2017

RESTRICTED Version 1.0 10 of 10

Approximate liability figure at end of period = liability figure at previous period end date * (1+ return on gilt basket over period) – cashflow during period

2. Compare the value of this Liability Proxy to the value of the Fund’s assets (less the cumulative value of any Employer contributions in respect of new service) at the quarter end date to produce an approximate deficit figure.

3. Compare this approximate deficit figure to the expected deficit at the respective quarter end date.

Quarter end date Expected deficit

(on a gilts curve basis)

31/03/17 -£42.0m 30/06/17 -£40.7m 30/09/17 -£39.4m 31/12/17 -£38.1m 31/03/18 -£33.6m 30/06/18 -£32.6m 30/09/18 -£31.6m 31/12/18 -£30.6m 31/03/19 -£26.1m 30/06/19 -£25.3m 30/09/19 -£24.6m 31/12/19 -£23.8m

4. If approximate deficit figure is lower than expected deficit figure by £3m or more then contact Barnett Waddingham so that more accurate calculations can be carried out to confirm if a trigger has been hit. Otherwise, mechanism has indicated that trigger has not been hit.

5. If trigger is assessed as having been hit, Barnett Waddingham LLP will confirm the switch from growth assets to protection assets required and the de-risking switch should be implemented within 6 weeks of the quarter end. Barnett Waddingham LLP will also confirm the new benchmark allocation which will become effective as at the next quarter end date.

Summary

A report on the administration of the South Yorkshire Passenger Transport Pension Fund for the period 1st October 2016 to 31st March

2017

1. Recommendations

It is recommended that the Committee Members:

Note the contents of the report with a view to commenting on the performance reported

2. Background information

2.1 South Yorkshire Pensions Authority administers the South Yorkshire Passenger Transport Pension Fund on an agency basis on behalf of the Sheffield City Region Combined Authority.

2.2 It keeps Members updated on its administrative performance and other related issues pertaining to the Fund through the provision of 6 monthly reports, of which this is the latest in the series.

PASSENGER TRANSPORT PENSION FUND COMMITTEE

19 June 2017REPORT OF THE CLERK

Page 35

3. Introduction

3.1 The last report was presented against a background of declining performance alongside a promise of plans, actions and strategies for improvement.

3.2 I am pleased to be able to say that this report is presented against a background of improvement in performance and a sense of optimism of further improvements to come. 3.3 The Authority accepts that it is not yet back to where is wishes to be in terms of casework

performance but hopes Members can see that the actions taken to date have brought about the start of the upward climb towards the historical standards that the Authority was used to reporting prior to the introduction of UPM.

4. Routine Casework Performance

4.1 The tables below show the performance for the latest reporting period. Also shown are the previous reporting period figures for comparison purposes.

1 October 2016 – 31 March 2017

Category Cases Target Achieved

Priority 77 100% 71.43% Other 111 96% 76.58% Overall 188 97% 74.47% 1 April 2016 – 30 September 2016

Category Cases Target Achieved

Priority 81 100% 59.26% Other 111 96% 55.86% Overall 192 97% 57.29%

4.1 Following the poor performance reported to the last meeting for the 6 month reporting period April to September 2016 I am pleased to report that performance levels increased over the last 6 months.

4.2 Casework numbers remained at around the same level as for the previous reporting period but priority performance increased by just over 12%, non-priority by just over 20% and overall performance by just over 17%.

4.3 As promised new procedures and alert reports were developed and introduced during the reporting period and that has seen an immediate improvement in performance levels. It is