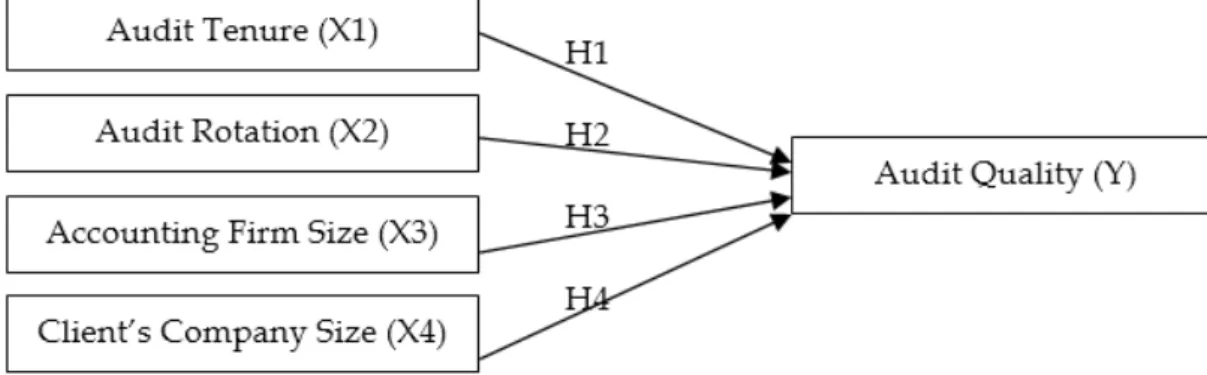

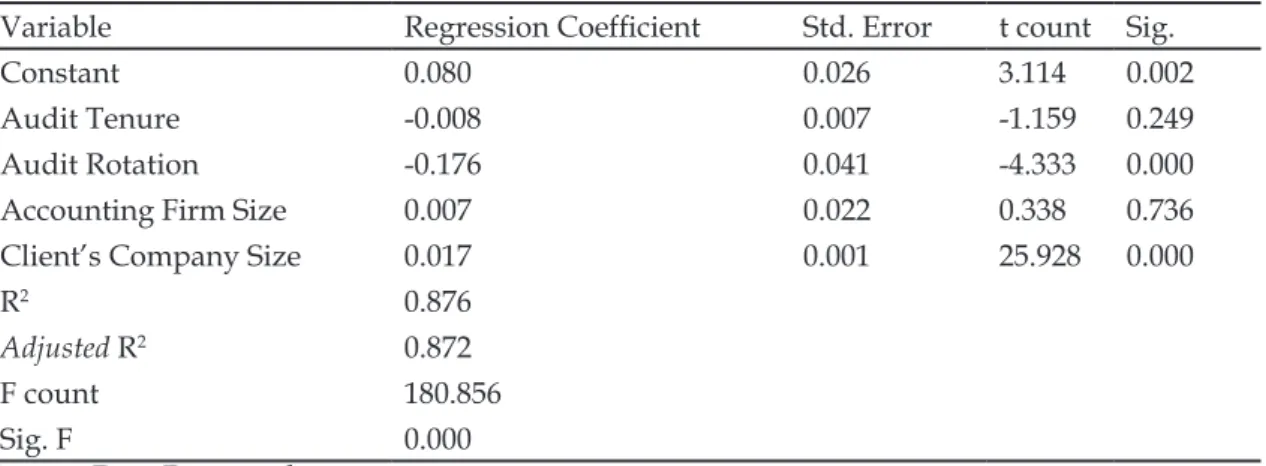

The effect of audit tenure, audit rotation, accounting firm size, and client’s company size on audit quality

Full text

Figure

Related documents

Such companies as RealEducation (eCollege), Collegis and Sylvan Learning Systems are marketing turnkey distance education systems to companies, universities and

As defined before, functional based training is a correctly designed program where the repetitive performance of movement patterns improves an individual's performance of job

By the systematic measurement of many javelin throws made by athletes of varying ability levels at different times of the year and over a period of several years, it has been

In our opinion, the Annual Report gives a true and fair view of the Group’s and the Parent Company’s assets, liabilities and financial position at 30 June 2005 and of the results

Psychology Research & Services Center, University of Houston September 2007 – August 2008 Supervisors: Amie Grills-Taquechel, Ph.D., Jack Fletcher, Ph.D.. Graduate

When a neuropsychologist attempts to establish an etiology for a neurocognitive outcome in a particular individual, he first considers, based upon available information, what factor

Career prospects: The agricultural productions of intensive farming that address the social and production needs in our society increases the demand for professionals with

DESIGNING SEARCH INTERFACES © 2001,2002 Whitney Quesenbery 23 Image browsing Q Image searches allow results to be browsed visually Q Display includes file name, size and