The recent financial crisis has challenged

Full text

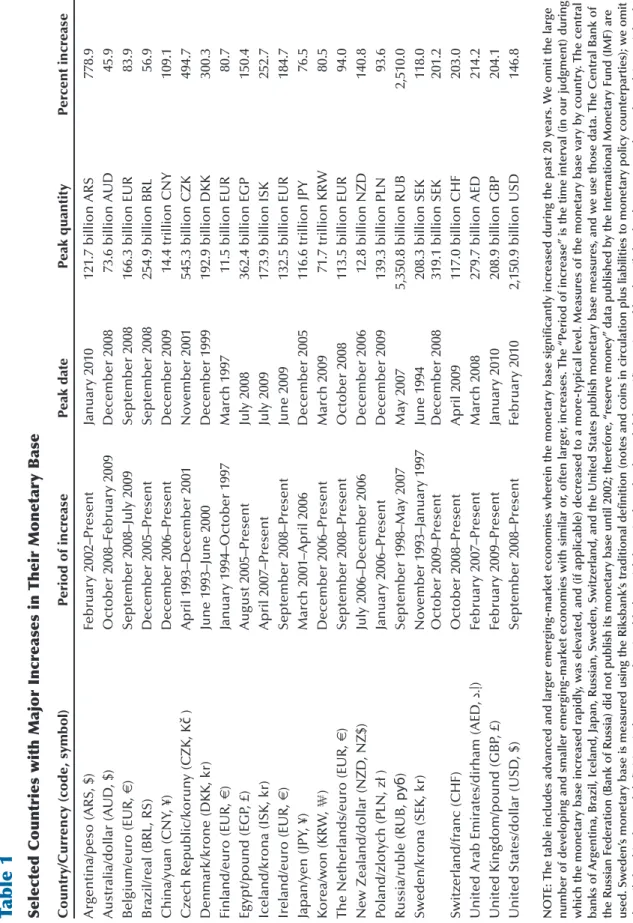

Figure

Related documents

There is a trade off with increasing daily minimum temperature post silking: increased minimum temperatures force a shorter grain fill period by accelerating phenology, but on

Extend the life of your critical industrial, commercial, and military systems with our superior service and support!. We

To have a more detailed and in-depth insight into the learning style preferences of Iranian English as a foreign language (EFL) university students, the researchers

Nations Peacekeeping Mission to Eritrea and Ethiopia (UNMEE) in December 2000, at the request of the two parties, to oversee the ceasefire and demilitarization of the border area,

• Averaging weak learners, over many training sets, gives estimates with low bias and low variance. • Replicate training sets are rarely available, but consider the next set

Department of Computer Science, Kulliyyah of Information and Communication Technology, International Islamic University Malaysia, P.O.. Box 10, Kuala

The novel snapshot based system level simulation methodology and the analytical eval- uation methodology are used to evaluated the impact of data traffic and user scheduling on

With few exceptions, the national statistics of work and production continue to ignore the unpaid labor and economic output contributed by women (and men) through household