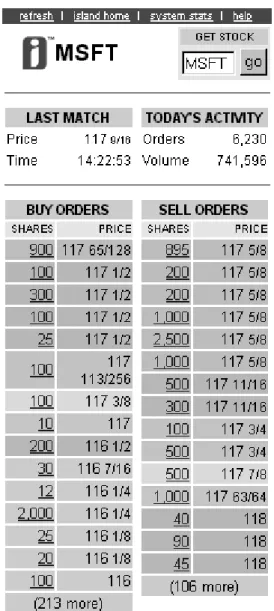

Chapter. The Playing Fields: Nasdaq and the NYSE

Full text

Figure

Related documents

The Inca Onset series of printers are full-width print array machines that offer very high quality prints and exceptional speed?. With the Onset machines, UV curing is immediate

HCC is developing in 85% in cirrhosis hepatis Chronic liver damage Hepatocita regeneration Cirrhosis Genetic changes

Water splitting on the rutile surface is instead largely dictated by oxy- gen vacancies in the rows of bridging oxygen atoms and is often dependent on the nature and density of

The encryption operation for PBES2 consists of the following steps, which encrypt a message M under a password P to produce a ciphertext C, applying a

(2010) Effect of Fly Ash Content on Friction and Dry Sliding Wear Behaviour of Glass Fibre Reinforced Polymer Composites - A Taguchi Approach. P HKTRSR and

(Also it says to not be afraid to tell sad stories or things of the like as it allows the girl to see you as more than a one dimensional guy) *Put emotion into it, don’t be crying

innovation in payment systems, in particular the infrastructure used to operate payment systems, in the interests of service-users 3.. to ensure that payment systems