Acquisitions, Ownership Efficiency, and the Tax Shield of Debt

⇤Pehr-Johan Norbäck

Research Institute of Industrial Economics (IFN) Lars Persson

Research Institute of Industrial Economics (IFN) and CEPR Joacim Tåg

Research Institute of Industrial Economics (IFN) August 13, 2012

Abstract

We show how the tax shield of debt can distort ownership efficiency in the market for corporate control. Firms with higher optimal leverage, but who are less efficient owners, can outbid more efficient owners of assets with lower optimal leverage. If the acquisition price is fully deductible, however, tax shields play no role because competitive bidding for assets generate sufficient deductions from the acquisition price alone to ensure bidders pay no taxes in equilibrium. Policies to equalize the tax treatment of debt and equity (such as limits the tax shield of debt) can improve ownership efficiency and total welfare by weaken-ing the connection between leverage and outcomes in biddweaken-ing contests.

Keywords: Acquisitions, Capital Gains Tax, Corporate Tax, LBOs, M&As, Ownership Efficiency, Private Equity, Tax Shields.

JEL classification: D20, G32, G33, G34, H25, H32, L19, L22

⇤We thank Andreas Haufler, Roger Gordon, Luigi Guiso, Magnus Henrekson, Christian Keuschnigg, Mikko

Mustonen, Gordon Phillips, three anonymous reviewers, and participants at the FDPE Workshop in Helsinki, SIFR and IFN in Stockholm, 9th Journées Louis-André Gérard-Varet Conference in Public Economics in Mar-seille, and at Copenhagen University for great comments and suggestions. Financial support from Tom Hedelius’ and Jan Wallander’s Research Foundations and the NASDAQ OMX Nordic Foundation is gratefully acknowl-edged. This paper was written within the Research Program on Entrepreneurship at IFN. This paper replaces our earlier working paper entitled “Ownership Efficiency and Tax Advantages: The Case of Private Equity Buyouts”. E-mail: [email protected]

1 Introduction

The tax shield of debt created by the ability to deduct interest expenses have a substantial impact on firms in many countries. As a subsidy for debt financing, the economic implications are large. Kemsley and Nissim (2002) estimate the value of the tax shield of debt to equal roughly 10% of firm value. In the wake of the financial crisis, a debate is raging on the welfare consequences of the “debt bias” introduced by the tax shield of debt (de Mooij (2011)). The fundamental problem, critics argue, is that equity and debt financing face different tax treatment, which induces firms to take on too much leverage which can lead to distortions in social welfare.

An concrete example is the debate surrounding investments by private equity firms. During the period 1985 to 2006, private equity firms have bought corporate assets in the U.S. yearly at an average value of approximately 1% of the total U.S. stock market value, with a top value of 3% in 2006 (Kaplan and Strömberg (2009)).1 The rise of this ownership form has been

accompanied with a concern that some transactions take place simply because of tax reasons.2

In particular, commentators argue that high leverage gives private equity firms advantages over other bidders in the market for corporate since interest deductibility creates a tax shield of debt.3 Policy responses range from attempts to ensure tax neutrality and transparency, to

a more direct intervention in capital structure, competition policy, and corporate governance (Walker (2007); PSE (2007)). For example, several countries have already taken some steps to reduce the deductibility of interest payments and goodwill: Denmark has passed a law that limits deductions and Germany has enacted a law limiting the deductibility of net interest expenses to below 30% of EBITA, which is similar to laws adopted in Italy (Thomsen (2009)).

Despite policy relevance, little formal work exists on how tax policy affects ownership effi-ciency when some bidders in takeover contests benefit more from the tax shield of debt than others. In this paper, we develop a model to study this question. We show how tax shields of debt can distort ownership efficiency when bidders in acquisitions differ in optimal leverage and there is limited deductibility of the acquisition price. Firms with higher optimal leverage can outbid more efficient firms with lower optimal leverage. Policies aimed at equalizing the tax treatment of debt and equity, such restricting interest deductibility or allowing corporate equity deductions, can improve ownership efficiency by weakening the connection between leverage and outcomes in bidding contents.

Formally, we develop a model of endogenous ownership, taxation and leverage. The model combines an endogenous acquisition model along the lines of Norbäck et al. (2009) with a standard corporate finance trade-off theory model for capital structure choice (see e.g.Bradley et al. (1983)) . A firm called the target, t, has assets needed for production in a monopoly

1See Kaplan and Strömberg (2009).

2See, for instance, “Testing the Model: Private Equity Faces a More Hostile World” (Jul 9 2009, The

Economist), “Editorial, New Rules for Private Equity” (August 30 2009, New York Times) or “Private Equity Fights Tax Plan” (February 27 2009,Financial Times).

3Empirically, private equity backed firms have higher leverage than other firms (Axelson et al. (2010)).

More-over, Badertscher et al. (2009) empirically document that majority owned private equity backed firms face lower marginal tax rates as a result of the tax shield of debt and Kaplan (1989) show that interest deductibility benefits equal 21% of the premium paid in leveraged buyout transactions. A plausible reason for higher leverage in private equity backed firms is that private equity firms face lower real costs of bankruptcy. Hotchkiss et al. (2011) show that private equity backed firms tend to emerge from bankruptcy quicker than other types of firms.

industry. In stage one,t’s assets are up for sale through a first price perfect information auction.

The bidders in this auction are firms of typeiorpwho are not currently present in the industry.

In stage two, after the assets have been sold, the owner l decides on how to finance the firm’s

operations by settingD, which is a (fully deductible) debt repayment that must be made in stage

three. An important (non-standard) aspect of our model is that we view Das a decision of the

owner of the firm who cash out in terms of a debt repayment and/or an equity payout. Hence, conflicts of interest between debt-holders and equity holders (e.g. Jensen and Meckling (1976)) are not present in our framework. In stage three, profits are realized, debts are repaid, and tax payments are made. Tax payments consist of corporate (or profit) taxes net of deductions in case the firm owned by ldoes not default.

The model underscores two central insights:

1. The degree to which the (endogenous) acquisition price is deductible from corporate taxes is an important determinant of whether the tax shield of debt creates distortions in ownership efficiency. An example is the goodwill associated with the acquisition, which is deductible from corporate taxes in most jurisdictions.4 Under full acquisition price deductibility, tax

shields are irrelevant because competitive bidding for assets generate sufficient deductions from the acquisition price alone to ensure bidders pay no taxes in equilibrium.

2. With limited acquisition price deductibility, however, the tax shield of debt can lead to distortions in ownership efficiency and total welfare. Intuitively, companies that have higher optimal debt levels (because of, for example, facing lower real bankruptcy costs) can outbid more efficient owners of assets because their valuation of target firms is higher as a direct result of the tax shield of debt. The higher firm value created by the tax shield of debt offsets a potential lower productivity leading to distortions in ownership efficiency. More generally, from a total welfare perspective, the tax shield of debt leads to higher leverage which introduces two distortions: i) a distortion in ownership efficiency (reducing consumer surplus) ii) an increase in expected real bankruptcy costs.

Our model generates several policy implications. Under limited acquisition price deductibility and in the presence of tax shields of debt, a reallocation of surplus from consumers and the gov-ernment to the target firm take place because of the tax shield. The benefit to firms is reduced tax payments, but from a welfare perspective these are simply transfers whereas the increase in expected real bankruptcy costs are real welfare losses. Hence, policies such as full acquisi-tion price deductibility or equalizing the tax treatment of equity and debt disconnects leverage decisions from outcomes in the market for corporate control, leads to ownership efficiency, and maximizes total welfare. With this in mind, policies such as restricting the deductibility of net interest expenses as implemented in Germany and Italy makes sense.

We have organized the paper as follows. The next section discusses related literature. In section 3 we set up and solve the model to derive our results. In section 4, we then take a broader perspective and study the effects leverage differences and various policy interventions

4Goodwill is typically defined as the part of the acquisition price above the value of deductible assets in

the acquired firm.Dunne and Ndubizu (1995) report that acquisitions are associated with different international accounting and tax treatments for goodwill and that these have changed over time.

on ownership efficiency and total welfare. We discuss extensions in section 5 and give concluding remarks in section 6.

2 Related Literature

Our paper is related to four strands of literature. First, it relates to the emerging literature on international taxation and ownership efficiency, which has proposed the concept of Capital Ownership Neutrality (CON). In informal work, Desai and Hines (2004) argues that in a perfect competition framework with ownership asymmetries, tax rules should be set up such that assets end up with the buyer who has the highest reservation price in the absence of tax differences. Devereux (2008) extends the definition by proposing that global neutrality requires both that taxes should not distort the location of corporate activity and that taxes should not distort competition between any companies operating in the same market. Formalizing the notion of CON, Becker and Fuest (2010) combine an optimal tax model with a non-strategic acquisition model and study when international exemption is an appropriate policy choice. Becker and Fuest (2009) use a similar framework to analyze tax competition and tax coordination when both source and residence based taxation are available. Departing from the literature on international mergers and acquisitions, Norbäck et al. (2009) also implicitly study CON by using a more detailed acquisition model with double taxation and allowing for an imperfectly competitive product market. They show that reductions in foreign profit taxes tend to trigger inefficient foreign acquisitions, while reductions in foreign capital gains taxes could trigger efficient foreign acquisitions. In relation to Becker and Fuest (2010) and Becker and Fuest (2009), our model explicitly accounts for how potential buyers’ valuations of target firms and potential sellers’ reservation prices depend on the tax shield of debt and optimal leverage decisions by firms. By studying endogenous ownership, our approach explicitly allows for firms to be acquired through competitive auctions which is not the case in Becker and Fuest (2010) and Becker and Fuest (2009). In contrast to Norbäck et al. (2009) we allow for deductions related to both tax shields of debt and acquisition costs and we explicitly model optimal leverage using a trade-off theory model from the finance literature. We show how different owners may be differently positioned to benefit from leverage, which can lead to distortions ownership efficiency and a reduction in total welfare.

A second related literature is work on the welfare effects of leverage. Most papers, as we do, have underscored negative externalities connected with high leverage. For example, Kiyotaki and Moore (1997) show how credit constraints can cause temporary shocks in one sector to persist and spill over to other sectors and create credit cycles and Shleifer and Vishny (1992) emphasize how liquidation of assets can lead to fire sales thus have negative externalities on other firms in the industry. Two recent paper, however, emphasize that subsidizing firm leverage through, for example, a tax shield of debt can be optimal. He and Matvos (2012) show, relying on a conflict of interest between equity and debt-holders, how the tax shield of debt will increase the incentives of firms to exit the industry. Because exit is socially beneficial, but privately costly, a tax shield of debt can improve welfare through encouraging creative destruction. In similar vein, Almazan et al. (2012) embed leverage choices and tax shields in a macro labor search model

to study how monetary and tax policy affect labor markets and the creation and destruction of firms. A bankruptcy has negative externalities on the unemployed, who now are more that compete for the same number of new jobs, but positive externalities on new firms as hiring labor is cheaper. Depending on the business cycle, the equilibrium number of liquidations of firms may be socially too low or too high allowing policy to play a role. None of these papers, however, study the effects of leverage choices and tax shields of debt on the market for corporate control and on ownership efficiency.

Third, our paper relates to the literature in corporate finance that has studied how capital structure decisions interact with the optimal scope of the firm.5 One example is Leland (2007),

who points out that financial synergies from mergers, and thus motivations for acquisitions or divestitures, depend on tax rates, default costs, size considerations and the riskiness and correlation of cash flows. In contrast to our paper, this literature typically focuses only on total firm value and ignores effects on consumers or concepts of ownership efficiency relating to how efficient different types of owners are at running firms. It also abstracts from how differences in optimal leverage affect the allocation of ownership as a result of bidding competition for firms up for sale.

Finally, there is also a related literature on cross-border acquisitions and taxes that abstracts from the ownership efficiency asymmetries and tax shields of debt we focus on. Gordon and Bovenberg (1996) propose a model with asymmetric information between foreign and domestic owners to explain why capital is so immobile internationally. Becker and Fuest (2011) analyze tax competition in a model where mergers and greenfield investments are alternative modes of entry and show that mergers intensify tax competition. Haufler and Schulte (2007) considers tax incentives in a model where mergers can take place within and across borders showing that ownership patterns are highly important for the welfare implications of tax policy choices. A paper that empirically do consider the tax shield of debt is Egger et al. (2010), who show that different tax treatment of debt in various countries affect how multinational firms allocate leverage across countries.

3 The Model

3.1 Setup

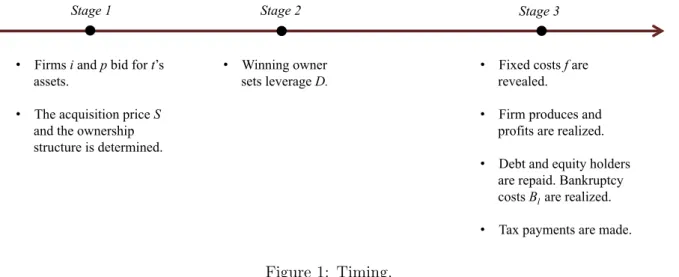

The timing of the game is described in Figure 1. A firm called the target, t, has assets needed

for production in a monopoly industry.

In stage one, t’s assets are up for sale through a first price perfect information auction. The

bidders in this auction are firms of type i or p who are not currently present in the industry.

Specifically, the set of bidders is J ={i1, i2, .., in, p1, p2, .., pm}, where the first n entries refer to the n number of i:s and the final m entries to the m number of p:s. The set of potential

owners of t’s assets are L= J, where l2 L is an element. The winner in the auction,l, pays

an acquisition price of S and obtains t’s assets (and can thus produce in stage three).

In stage two, leverage is determined. The owner l decides on how to finance the firm’s

operations by setting D, which is a (fully deductible) debt repayment that must be made in 5See Graham (2006) or Myers (2003) for a survey.

• Firms i and p bid for t’s assets.

• The acquisition price S and the ownership structure is determined.

• Winning owner sets leverage D.

• Fixed costs f are revealed.

• Firm produces and profits are realized.

• Debt and equity holders are repaid. Bankruptcy costs Bl are realized.

• Tax payments are made.

Stage 1 Stage 2 Stage 3

Figure 1: Timing.

stage three. In the first part of the analysis, we will for clarity suppose that D is exogenously

determined. Since we view D as a decision of the owner of the firm (who cash out in terms of

a debt repayment and/or an equity payout), we implicitly assume away any conflicts of interest between debt-holders and equity holders (e.g. Jensen and Meckling (1976)).

In stage three, profits are realized, debts are repaid, and tax payments are made. Let⇡(x, l) denote the product market profit given a product market action (x) and the ownership (l). The

optimal actionx⇤(l) is defined from ⇡(x⇤, l)>⇡(x, l)for all x, so we can define a reduced-form

product market profit for a firm of type l as ⇡(l) = ⇡(x⇤(l), l). Notice that because conflicts of interest between debt-holders and equity-holders are not present, the optimal leverage choice will not affect product market actions and profits (in contrast to Brander and Lewis (1986)). At this stage, firm also faces a (deductible) fixed cost of f withH(f) 2[0,f¯]and the probability density function h(f). Events unfold as follows in this stage. First, the fixed cost f is paid.

Second, debt repayments Dare made. If debt repayments exceed product market profits net of

fixed costs,⇡(l) f < D, the firm defaults and incurs a real fixed bankruptcy cost ofBl(suppose ¯

f ⇡(l) Bl such that the bankruptcy cost is not too large). Finally, tax payments are made. For simplicity, the target’s owners pay no taxes on the acquisition price and no capital gains or dividend taxes are paid by ownerl. The only tax payments made are thus corporate (or profit)

taxes net of deductions in case it does not default: (l) =

ˆ ⇡(l) D 0

(⌧[⇡(l) f D])h(f)df. (1)

To define ownership efficiency, let the parameter l > 0 correspond to how efficiently l can use t’s assets to produce output. Increased efficiency leads to higher profits, d⇡(l)/d l > 0, so we can then define ownership efficiency as:

Definition 1. Letle = arg maxl⇡(l) and let l⇤ denote the equilibrium ownership oft0sassets. Under ownership efficiencyl⇤ =le.

Under ownership efficiency, t’s assets will be possessed by the owner with the highest

effi-ciency parameter which is also the owner that makes the best productive use of the assets. Assuming simple monopoly pricing, maximizing ownership efficiency will also maximize the

sum of consumer surplus and product market profits since consumers will benefit from higher efficiency through lower prices.

To illustrate the importance of the endogenous deductions created by bidding competition for t’s assets, we will first (subsection 3.2) consider a simplified version of the model with i)

exogenous debt repayments (only stage one and three); ii) zero bankruptcy costs and fixed costs; and iii) the acquisition price is deductible from corporate taxes (full deductibility). This reflects a setting in which the acquisition itself generates tax deductions from corporate taxes because of asset write-ups or the creation of goodwill on the balance sheet. We show how in such a setting tax shields do not affect the allocation of t0s assets. We then show (subsection

3.3) how ownership efficiency in the simplified model can be distorted by tax shields when S is

not deductible from corporate taxes (limited deductibility). Finally, we solve the full model with endogenous leverage and the possibility of a default (subsection 3.4) to show that the results carry over to a setting with endogenous leverage but differences in real bankruptcy costs between owner types.

3.2 Full acquisition price deductibility

Suppose the acquisition price is deductible at the corporate level (full deductibility). Suppose also that debt repayments D are exogenously set (with D < ⇡(l)), but that owners differ in their choice of leverage: D =D(l). Finally, suppose that bankruptcy and fixed costs are zero (Bl=f = 0).

3.2.1 Stage three: product market profits, debt repayment and taxation. In stage three, the payoff to ownerl is

V(l) = [⇡(l) D(l)] max{0,⌧[⇡(l) D(l) S]} | {z } Equity value + D(l) |{z} Debt value (2) The first two terms captures the equity payout to ownerlnet of corporate taxes. The third term

is the debt repayment. Deductions cannot be larger than profits, so⌦(S) =⇡(l) D(l) S 0 must hold. Note that many cases, it may be possible for firms to make use of deductions either at a later point in time or to use them to make deductions from profits in other industries or countries. For simplicity, we here ignore this possibility but we will come back to it later in our analysis.

3.2.2 Stage one: the acquisition auction

Skipping stage two, in stage one the acquisition auction takes place. The acquisition process is depicted as an auction where owner typesiandpsimultaneously post bids. Everyone announces

a bid,bj, which is either accepted or rejected byt. Following the announcement of bids,t’s assets

are sold to the highest bidder (if pand iare tiedimakes the acquisition). To solve the auction

and determine bids, we need to determine the valuations of the bidders for obtaining the assets. To aid in this, we introduce the net gain function l(S)which defines the net gain for a bidder of typel if the acquisition price isS.

Table 1: The equilibrium ownership structure and the acquisition price.

Ineq: Definition: Equilibrium owner,l⇤: Acquisition price,S⇤:

I1 : vp > vi p vp

I2 : vi vp i vi

The net gain for l is thus

l(S) = 8 < : ⇡(l) ⌧[⇡(l) D(l) S] S for⌦(S)>0 ⇡(l) S for⌦(S)0 (3) The maximum willingness to pay for l is vl ⌘maxS, s.t l(S) 0. Solving the upper line in equation (3) gives˜vl=⇡(l) + [⌧c/(1 ⌧c)]D. However, iflwere to payS= ˜vl,it directly follows that ⌦(S) = (1 + [⌧/(1 ⌧)])D <0. Therefore, the maximum valuation forl must be given

solving the lower line in equation (3) to obtain

vl=⇡(l) (4)

and ⌦(vl) = 0.

Given the valuations vl we can now solve the auction for t’s assets and determine the equi-librium ownership structure and acquisition price.

Lemma 1. The equilibrium ownership structure l⇤ and the acquisition price S⇤ are described in Table 1.

Proof. Note that bj >maxvl for l={i,p} is a weakly dominated strategy, since no owner will post a bid above its maximum valuation of obtaining the assets andtwill accept a bid iffbj >0. Assume that a bidder indifferent between not posting a bid/posting a losing bid (gaining zero) and posting a bid equal to his or her maximum valuation (again gaining zero) always chooses to post the bid equal to his or her maximum valuation. Suppose also that ifiandp have equal

bids, an owner of type i will obtain t’s assets. Then, competition within owner groups means

that the equilibrium acquisition price must bevi andvp foriandprespectively (anyjdeviating to a bidvl ✏will post a losing bid and prefer to bid his or her maximum valuation instead). It then follows that an owner of typepacquires the assets at pricevp iffvp > vi and thatiacquires the assets at pricevi iff vi vp.

It is now apparent that leverage differences D(l) are irrelevant for ownership efficiency. Bidding competition ensures that all owner typesibidvi and all owner typesp bidvp. Lemma 1 then states that the assets end up with the owner that has the highest valuation, and that this owner pays his or her full valuation. Since all valuations are independent ofD, ownership

efficiency is also unaffected byD.

Proposition 1. If the acquisition price is fully deductible from corporate taxes, the tax shield of debt does not lead to distortions in ownership efficiency (l⇤ =loe) as the equilibrium ownership pattern l⇤ is independent ofD(l).

Intuitively, bidding competition drives up the acquisition price so high that deductions based on the acquisition price alone are enough to ensure that no tax payments are made in equilibrium. The proposition underscores the important point that tax rules governing the deductibility of acquisition prices (e.g. goodwill) from corporate taxes interact closely with the tax shield of debt

as long as the acquisition does not create tax credits for the firm that can be used in the future or in another market. A general lesson from this section is that, from an ownership efficiency perspective, there is less concern for distortions created by the tax shield of debt in countries that allow deductions of the acquisition price at the corporate level.

3.3 No acquisition price deductibility

Suppose now, however, that the acquisition priceS is not deductible from corporate taxes, but

otherwise the setup is as in the previous section (debt levels are exogenous, bankruptcy and fixed costs are zero).

3.3.1 Stage three: product market profits, debt repayment and taxation. In stage three, the payoff to ownerl is now

V(l) = [⇡(l) D(l)] ⌧[⇡(l) D(l)] | {z } Equity value + D(l) |{z} Debt value (5) The first two terms again capture the equity payout to owner l net of corporate taxes and the

third term is the debt repayment. Because D(l) <⇡(l), the tax shield of debt will always play a role when the deduction created by the acquisition priceS is not available.

3.3.2 Stage one: the acquisition auction In stage one, the net gain for lnow

l(S) =⇡(l) ⌧[⇡(l) D(l)] S (6) The maximum willingness to pay forl isvl ⌘maxS, s.t l(S) 0 which now gives

vl= (1 ⌧)⇡(l) +⌧D(l). (7)

Crucially, notice now that the valuation vl is now dependent on D(l). Hence, any difference in ownership efficiency (manifesting in differences in ⇡(l) between i and p) can be compensated

for by benefits from the tax shields of debt. Applying Lemma 1, we immediately see that if

D(p)> D(i)but i> p we can be in a situation in whichvp> vi and thus pacquirest’s assets despite not being able to make as good use of them as i.

Proposition 2. If the acquisition price is not deductible from corporate taxes, the tax shield of debt can lead to distortions in ownership efficiency (l⇤ =p6=lef f). The larger the tax⌧ and the

Notice that bidding competition between owner types no longer have any bite, because it does not lead to additional deductions from corporate taxes when the acquisition price is not deductible from corporate taxes. Note also that a result that directly follows from proposition 2 is also that tax revenues for the government will be reduced if ownership efficiency is distorted since i) profits are lower ii) higher deductions are possible.

3.4 Endogenous leverage

Let us now solve the full model with endogenous leverage and limited deductibility. Note that with full deductibility, all tax payments can be evaded using only deductions from the acquisition price S which implies that optimal leverage is zero. The model would collapse to the simple

model with D = 0 as the marginal benefit of leverage (lower total tax payments) is zero while the marginal cost (the increased risk of incurring bankruptcy costsB) is still positive.

3.4.1 Stage three: product market profits, debt repayment and taxation. In stage three, the payoff to ownerl is now

V(l, D) = ˆ ⇡(l) D 0 [⇡(l) f D]h(f)df ˆ ⇡(l) D 0 ⌧[⇡(l) f D]h(f)df | {z } Equity value + ˆ ⇡(l) D 0 Dh(f)df+ ˆ f¯ ⇡(l) D [⇡(l) f Bl]h(f)df | {z } Debt value (8)

The first two terms captures the equity payout to ownerlnet of corporate taxes in case the firm

does not default. The third and fourth term is the debt repayment, the third term corresponding to the debt repayment D which is made in case the firm does not default and the fourth term

corresponding to the debt repayment⇡(l) f Bl< Dthe firm defaults. 3.4.2 Stage two: optimal leverage

In stage two, the debt level of the firm D is set by owner l to maximize total firm value: D⇤l = argmaxDV(l, D). The first order condition (FOC) for this maximization problem can, using the Leibniz integral rule, be split into marginal benefits (MB) and marginal costs (MC) of debt.6 We obtain dV(l, D) dD = ˆ ⇡(l) D 0 (1 ⌧)h(f)df Dh(⇡(l) D) + ˆ ⇡(l) D 0 h(f)df+ [D Bl]h(⇡(l) D) = ⌧H(⇡(l) D) | {z } M B Blh(⇡(l) D) | {z } M C = 0 (9)

6The general Leibniz integral rule states d dx ´b(x) a(x)f(y, x)dy = db(x) dx f(b(x), x) da(x) dx f(a(x), x) + ´b(x) a(x) d dxf(y, x)dy.

This equation illustrates that the marginal benefit of debt is reduced corporate tax payments whereas the marginal cost is increase real bankruptcy costs. Assuming that the second order condition is satisfied, we can implicitly define optimal debt levelD⇤(l) from

⌧cH(⇡(l) D⇤(l)) =Blh(⇡(l) D⇤(l)) (10) The first order condition also tells us that reducing real bankruptcy costs increases leverage. Differentiating this first order condition with respect to Bl, we obtain

dD⇤(l)

dBl

= h(⇡(l) D⇤(l))

⌧cH0(⇡(l) D⇤(l)) +Blh0(⇡(l) D⇤(l))

<0 (11)

where the denominator is negative from the second order condition. Hence, an owner type with lower real bankruptcy costs will take on higher leverage to benefit from the tax shield of debt. 3.4.3 Stage 1: The acquisition auction

In stage one, the net gain for buyer typel is now simply

l(S) =V(D⇤(l), l) S. (12) The maximum willingness to pay is given byvl ⌘maxS, s.t l(S) 0. Solving for l(S) = 0 gives us maximum valuations of obtaining t:

vl=V(D⇤(l), l). (13)

Using these valuations, we can invoke Lemma 1 to state that forvi vpowner typeiwill obtain

tat priceSi =vi while forvi< vp owner typep will obtaintat priceSp =vp. Notice that vl is directly dependent onD⇤(l)and thus on the tax shield of debt. As in subsection 3.3, ownership efficiency can be distorted. We can now state the following proposition.

Proposition 3. Differences in optimal leverage (D⇤(p) > D⇤(p)) as a result of differences in real bankruptcy costs (Bp< Bi), can lead to distortions in ownership efficiency (l⇤ =p6=lef f).

We have already shown in equation (11) that differences in real bankruptcy costs translate into differences in optimal leverage. To see that leverage differences can induce distortions in ownership efficiency, note we can have a situation in which the valuation ofp is higher than for i (vp > vi) despite that i is more efficient than p ( i > p). Start with assuming that i > p and note that firm valueV(l) is decreasing in bankruptcy costs B: dV(l)/dB <0. We obtain

dV(l) dB = @V @D dD⇤ dB + @V @B = @V @B = ˆ f¯ z⇤Bh(f)df <0 (14)

since we know that@V /@D = 0 from the first order condition in equation (10). Reducing real bankruptcy costs increases the maximum willingness to pay to obtaint’s assets sinceV(l) =vl.

Since we we started from i> p, ifp has sufficiently low real bankruptcy costs in relation toi this could compensate for lower ownership efficiency and thus allow pto inefficiently acquiret.

Proposition 3 mirrors Proposition 2, but it accounts for endogenous differences in leverage arising from differences in real bankruptcy costs. It underscores that differences between owner types in terms of real bankruptcy costs translates into differences in leverage, which in turn through the a greater tax shield of debt could allow less efficient owners of assets to acquire assets in equilibrium. Note, however, that differences in leverage only distorts ownership efficiency if they are sufficiently large and it is the less efficient owner that has lower real bankruptcy costs. If the difference is small or it is the more efficient owner than also has lower real bankruptcy costs ownership efficiency is unaffected by leverage differences.

More generally, we have in this section argued that differences in optimal leverage for firms can through the tax shield of debt distort the ownership efficiency in the market for corporate control. Note, however, than it is still the owner with the highest valuation that obtains assets. Our notion of ownership efficiency captures only how productively ownerl can use the assets of t, ignoring potential real bankruptcy costs, while total firm value accounts for real bankruptcy

costs. Dealing with this discrepancy is the topic of the next section.

4 Welfare and policy

4.1 Surplus allocation with tax shields

The tax shield of debt in our setting introduces two types of distortions in social welfare that are important to separate.

1. The tax shield of debt reduces productive efficiency as less productive but more highly leveraged firms can outbid more productive firms with lower leverage.

2. The tax shield of debt leads to increased real bankruptcy costs by giving firms incentives to take on debt in the first place.

The problem is fundamentally that while the firm internalizes the increase in real bankruptcy costs when setting leverage, it does not internalize the externality on the government (reduced tax revenues) or the externality on consumers (reduced productive efficiency). Intuitively, the gain to the firm from increased leverage (and thus the incentive to outbid less leveraged but more productive rivals) is based ontransfer of wealth from the government while the increased bankruptcy cost is areal welfare loss.

From a first-best perspective, optimal leverage would thus entail zero leverage (independently of Bl). To see this formally, denote total welfare as

W(l) =CS(l) + (l) +A(l) +T(l) (15) whereCS(l)is consumer surplus, (l)is tax revenues andA(l)is the acquirers surplus, andT(l) is the target’s surplus. Consumer surplus is increasing in ownership efficiency as a more efficient owner will quote lower prices (@CS(l)/@ > 0). Tax revenues (D, l) are transfers from the firm to the government and thus the level of taxes does not affect overall welfare. The acquirers surplus A(D, l) will in equilibrium equal zero because bidding competition drives up prices to

the equilibrium acquisition price: T(D⇤, l⇤) =S⇤ =V(D⇤, l⇤). This means that any corporate tax gains that arise in equilibrium for the acquirer will through the acquisition price directly benefit the owners of the target firm instead (this is consistent with empirical evidence of tax planning in private equity buyouts mostly benefitting the sellers of target firms through higher acquisition prices, see e.g. Jenkinson and Stucke (2011)).

Proposition 4. In the presence of tax shields of debt, if leverage differences distorts ownership efficiency (l⇤=p6=lef f), then

(i) a reallocation of surplus from consumers and the government to the target firm take place; and

(ii) a decrease in total surplus occurs if the effect on consumer welfare through lower prices is stronger than the effect on firm value through lower bankruptcy costs.

To see the first part, note that from Lemma 1 the acquisitions price S will always equal the

valuationvl implying that the buyer lwill make zero profits in equilibrium and pay zero taxes. From Proposition 3, we know that ownership efficiency is weakly lower under lower bankruptcy costs since dV(D,l)

dB <0 and we can havep as the owner even though i > p if Bp < Bi. Since consumer surplus is increasing in , consumers are worse of at the expense of higher firm value

Vp. From equation (??) we see that higher leverage reduces tax revenues so the government is

worse off. To see the second part, note that taxes are transfers from the target and the acquirer to the government, so total welfare is unaffected by taxation and the acquisition price. Firm value increases because of lower (expected) bankruptcy costs(Vp > Vi), but ownership efficiency is reduced. Hence, the effect on total welfare involves a trade-off between bankruptcy costs and consumer surplus.

4.2 Policy interventions

As mentioned, first-best would involves a tax and deduction policy that ensures zero leverage in equilibrium and thereby zero expected real bankruptcy costs and no distortions in ownership efficiently. As the next proposition clarifies, full acquisition price deductibility and a removal of the tax shield of debt are two such policies.

Proposition 5. Full acquisition price deductibility or equalizing the tax treatment of equity and debt disconnects leverage decisions from outcomes in the market for corporate control, leads to ownership efficiency, and maximizes total welfare (implements first best).

The proposition underscores that increases in acquisition price deductibility and restrictions to the tax shield of debt are substitutes and both can be used to mitigate the distortative effect of leverage differences on the market for corporate control.

First, consider removing the tax shield. In our base line model with exogenous debt, it is the no longer the case that ownership efficiency can be distorted as it is always the owner l

with highest efficiency parameter that obtains the assets. With endogenous debt, firms will no longer face any incentives to take on leverage if the tax shield of debt is removed. Thus, the removal of the tax shield of debt will now have two effects: in addition to shutting down the possibility of misallocations of ownership efficiency, it also reduces real bankruptcy costs. Our

Table 2: The equilibrium ownership structure and the acquisition price.

Ineq: Definition: Equilibrium owner,l⇤: acquisition price,S⇤:

I1 : vp> vi p vi

I2 : vi vp i vp

model underscores that removing the tax shield of debt will always lead to weak improvements in consumer surplus (as l⇤=lef f) and in tax revenues. Total firm value will, however, decrease despite removing (deductible) real bankruptcy costs as transfers from the government will seize. Hence, removing the tax shield of debt weakens the connection between leverage and outcomes in the market for corporate control and can thereby improves ownership efficiency.

Second, if the government has no need for collecting tax revenues, then the following three policies all will implement first-best:

1. allowing both deductions for debt and equity. 2. implementing full acquisition price deductibility, 3. lowering taxes to zero.

Under full acquisition price deductibility, the acquisition price can be used to deduct all profits other deductions are irrelevant and ownership efficiency will not be distorted since leverage differences will not emerge. Hence, a substitute policy to implementing a deduction of both equity and debt would be to allow a larger share of the acquisition price to be deducted.

In standard tax theory, all investment costs should be deductible from taxes so investment decisions are not distorted by taxation. Our results are in line with this view as acquiring a firm is an investment as well. This motivates both tax shields of debt and tax shields of equity in addition to full acquisition price deductibility. The market for corporate control is then not affected by leverage decisions and all taxes are raised from the target firm’s owners.

5 Robustness and discussion

5.1 Limited bidding competition

Bidding competition plays a crucial role for Proposition 1. However, what is important for ownership efficiency under full acquisition price deductibility is not bidding competition within

owner types butacross. To see this, consider the simple model again with exogenous debt levels and zero fixed costs and bankruptcy costs. To introduce limited bidding competition, suppose that the is only one i and one p: J ={i, p}, where j2 J is an element. Bidding competition

within owner groups will then not take place. Given the valuations vi and vp, we can now solve the auction for the t’s assets and determine the equilibrium ownership structure and the

acquisition price.

Lemma 2. The equilibrium ownership structure and the acquisition price with limited bidding competition are described in Table 2.

Proof. First, bj >maxvl for l={i,p}is a weakly dominated strategy, since no owner will post a bid above its maximum valuation of obtaining the assets and t will accept a bid iff bj > 0. Assume that a bidder indifferent between not posting a bid/posting a losing bid (gaining zero) and posting a bid equal to his or her maximum valuation (again gaining zero) always chooses to post the bid equal to his or her maximum valuation. Then, for vp > vi owner type p will post a bid exactly equal to the second highest valuation (vi) and obtain the assets. For vi = vp, i will obtain the assets but be forced to pay vi =vp because of bidding competition from p. For

vi > vp, it is enough that ipays the second highest valuation (vp) to obtain the assets. This lemma allows us to state the following proposition.

Proposition 6. Under limited bidding competition, leverage differences does not distort owner-ship efficiency (l⇤=loe).

Lemma 2 shows that t’s assets will end up with the owner with the highest valuation but

the acquisition price will equal the second highest valuation. However, all valuations vl are still independent of D as the acquisition price can be used to deduct all profits. To illustrate,

suppose i > p such that vi > vp. Theni will obtain the assets and ownership efficiency will be attained. Leverage differenceD cannot helpp to outbidisince vp=⇡(p)< vi =⇡(i). Thus ownership efficiency is not distorted by leverage differences.

Tax revenues, however, could now be reduced as it may be that ⌦(l) =⇡(l) D S⇤ 0 since vp=⇡(p)>⇡(i) =S⇤. Whenp has a positive net profit⇡(p) D S⇤ 0, differences in leverage imply that tax revenues are reduced as some profits are left for pfrom whichD can be

deducted even with full acquisition price deductibility.

5.2 Stock versus asset purchases

Extending the model to account for differences in acquisition types or acquisition financing strategies among owner types would involve considering this heterogeneity instead of hetero-geneity in leverage. Indeed, in our baseline model the deduction D available to p type owners

could correspond to exogenous differences in financing strategies for the acquisition which in turn lead to different deductions being created. Our baseline results would thus remain unaffected. A number of insights then follow. With respect to asset versus stock acquisitions, in many juris-dictions stock acquisitions create less deductions than direct asset acquisitions. Reinterpreting the exogenousDin the baseline model as the additional deductions that asset acquisitions

gen-erate over stock acquisitions, it immediately follows that distortions in ownership efficiency are more likely to occur for stock acquisitions that do not trigger additional deductions. With re-gards to financing strategies, similar results can be drawn. If financing through raising debt for the acquisition creates additional deductions then this financing strategy has more potential for introducing distortions in ownership efficiency. More generally, ownership efficiency will be max-imized when various financing and acquisition strategies create equal deductions which would correspond toD= 0 in our baseline model. Naturally, endogenizing differences in financing or acquisition strategies is an excellent avenue for further research.

5.3 Tax credits

In our analysis of full acquisition price deductibility we have abstracted for inter-temporal effects of taxation and deductions, but these could be important as the acquisition may create tax-loss carry-forwards that are valuable to the firm or allow the firm to make use of deductions through profit transfers from other industries. In our setting, this would imply that deductions from the acquisition price are valuable even when they exceed product market profits (it no longer holds that ⌦(S) =⇡(p) S D 0). While bidding competition between owner types still ensures that any gains there deductions create are incorporated into the acquisition price, an owner with lower ownership efficiency could now acquire the assets because of the future tax credits that are created. Hence further research on the inter-temporal effects of taxation is motivated.

5.4 Heterogeneity in investor level taxation

We have made no distinction between capital gains and dividend taxation in our model. Capital gains taxes are usually paid by the target firm’s owners on the equilibrium acquisition price, whereas the acquirer may be forced to pay out profits as dividends carrying a higher tax rate. Accounting for this difference will in our setting affect equilibrium tax collection, but it will not affect our results on ownership efficiency as these results rely entirely on deductions available to various owners. In however, different owners vary in their equilibrium dividend policies and this gives rise to higher or lower tax payments at the corporate level for certain types of firms ownership efficiency could be effected.7 Again, we could reinterpret the exogenous D in

our simplified model as a difference in tax deductions which arises from various owners having different optimal dividend policies. A direct implication is then that ownership efficiency could be distorted by dividend policies if the acquisition price is not fully deductible from corporate taxes.

Going back to our motivating example of private equity firms, an aspect of the policy debate concern how income for the general partners in the private equity fund should be taxed. In several countries a debate rages on whether carried interest (at the investor level) should be taxed as labor income or capital income. To incorporate this into our framework, we could assume that the private equity firm consists of only a few general partners. Consider introducing the requirement that carried interest (a share of the returns to owner type p) is taxed at at a

higher (labor income) tax rate⌧L than the capital gains tax rate ⌧L >⌧g. From the equations determining maximum willingness to pay in our extension with capital gains taxation, we can note that capital gains taxes does not affect maximum valuations. Thus, such an intervention would not affect ownership efficiency. Intuitively, capital gains taxes are not important because bidding competition for ts assets ensures that no buyers makes a positive profit and thus as

long as the acquisition price is deductible from capital gains taxes the tax level does not play an important role.

7For example, Michaely and Roberts (2011) document that dividend policies of privately owned and publicly

6 Concluding remarks

Motivated by the debate surrounding the tax shield of debt and the tax treatment of private equity firms, we have developed a model for studying how acquisition price deductibility and the tax shield of debt affects ownership efficiency and tax revenues when bidders differ optimal leverage. We pointed out that equalizing the tax treatment of debt and equity and/or ensuring full acquisition price deductibility leads to improvements in ownership efficiency by weakening the connection between leverage and outcomes in the market for corporate control.

In deriving our results, we have made numerous omissions which are excellent avenues for further research. Our framework omits, but can be extended to include, differences in capital gains and divided taxation, inter-temporal effects of tax payments, tax loss carry forwards, internal transfer policies for incumbent firms, dividend policy decisions and differences between asset and share acquisitions. Additionally, it is well suited to incorporate limited product market competition among incumbent firms and can be extended to study effects of conflicts of interest between equity and debt holders. As such, our paper offers a convenient framework for future study of optimal capital structure, tax policy and issues related to mergers and acquisitions in the presence of taxation.

References

Almazan, A., A. de Motta, and S. Titman (2012). Debt, labor markets and the creation and destruction of firms. Mimeo.

Axelson, U., T. Jenkinson, P. Strömberg, and M. S. Weisbach (2010). Borrow cheap, buy high? The determinants of leverage and pricing in buyouts. NBER Working Papers 15952, National Bureau of Economic Research, Inc.

Badertscher, B., S. P. Katz, and S. Olhoft Rego (2009). The impact of private equity ownership on corporate tax avoidance. HBS Working Paper 10-004.

Becker, J. and C. Fuest (2009). Source versus residence based taxation with international mergers and acquisitions. CESIFO Working Paper No 2854.

Becker, J. and C. Fuest (2010). Taxing foreign profits with international mergers and acquisi-tions. International Economic Review 51, 171–186.

Becker, J. and C. Fuest (2011). Tax competition - greenfield investment versus mergers and acquisitions. Regional Science and Urban Economics 41, 476–486. CESifo Working Paper No 2247.

Bradley, M., G. A. Jarrell, and E. H. Kim (1983). On the existence of an optimal capital structure: Theory and evidence. The Journal of Finance 39, 857–878.

Brander, J. A. and T. R. Lewis (1986). Oligopoly and financial structure: The limited liability effect. American Economic Review 76, 956–970.

de Mooij, R. A. (2011). Tax biases to debt finance: Assessing the problem, finding solutions. IMF Staff Discussion Note.

Desai, M. A. and J. R. Hines (2004). Rules and new realities: Corporate tax policy in a global setting. National Tax Journal 57, 937.

Devereux, M. (2008). Taxation of outbound direct investment: Economic principles and tax policy considerations. Oxford University Centre for Business Taxation Working Paper 0824. Dunne, K. M. and G. A. Ndubizu (1995). International acquisition accounting method and

corporate multinationalism: Evidence from foreign acquisitions. Journal of International Business Studies 26, 361–377.

Egger, P., W. Eggert, C. Keuschnigg, and H. Winner (2010). Corporate taxation, debt financing and foreign-plant ownership. European Economi 54, 96–107.

Gordon, R. H. and A. L. Bovenberg (1996). Why is capital so immobile internationally? possible explanations and implications for capital income taxation. American Economic Review 86, 1057–1075.

Graham, J. R. (2006). A review of taxes and corporate finance. Foundations and Trends in Finance 1, 573–691.

Haufler, A. and C. Schulte (2007). Merger policy and tax competition. Discussion Papers in Economics 2074, University of Munich.

He, Z. and G. Matvos (2012). Debt and creative destruction: Why could subsidizing corporate debt be optimal? Mimeo.

Hotchkiss, E. S., D. C. Smith, and P. Strömberg (2011). Private equity and the resolution of financial distress. Available at SSRN: http://ssrn.com/abstract=1787446.

Jenkinson, T. and R. Stucke (2011). Who benefits from the leverage in LBOs? Available at SSRN: http://ssrn.com/abstract=1777266.

Jensen, M. C. and W. H. Meckling (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3, 305–360.

Kaplan, S. N. (1989). Management buyouts: evidence on taxes as a source of value. Journal of Finance 44, 611–632.

Kaplan, S. N. and P. Strömberg (2009). Leveraged buyouts and private equity. Journal of Economic Perspectives 23, 121–146.

Kemsley, D. and D. Nissim (2002). Valuation of the deb tax shield. The Journal of Finance 57, 2045–2074.

Kiyotaki, N. and J. Moore (1997). Credit cycles.The Journal of Political Economy 105, 211–248. Leland, H. E. (2007). Financial synergies and the optimal scope of the firm: Implications for

mergers, spinoffs, and structured finance. The Journal of Finance 62, 765–807.

Michaely, R. and M. R. Roberts (2011). Corporate dividend policies: Lessons from private firms. Available at SSRN: http://ssrn.com/abstract=927802.

Myers, S. (2003).Handbook of the Economics of Finance, Chapter 4: Financing of Corporations, pp. 215–253. Elsevier.

Norbäck, P.-J., L. Persson, and J. Vlachos (2009). Cross-border acquisitions and taxes: Efficiency and tax revenues. Canadian Journal of Economics 42, 1473–1500.

PSE (2007). Hedge funds and private equity: A critical analysis. Report of the PSE Group in European Parliament.

Shleifer, A. and R. W. Vishny (1992). Liquidation values and debt capacity: A market equilib-rium approach. The Journal of Finance 47, 1324–1366.

Thomsen, S. (2009). Should private equity be regulated? European Business Organization Law Review 10, 97–114.