R

ETAIL

M

ARKET

A

NALYSIS

B

EACH

S

TREET

S

HOPPING

D

ISTRICT

D

AYTONA

B

EACH

, F

LORIDA

Prepared For:

C

ITY OFD

AYTONAB

EACHCRA

301 South Ridgewood Avenue Daytona Beach, Florida 32114

Prepared By:

G

IBBSP

LANNINGG

ROUP,Inc.

201 W. Mitchell Street, #150Petoskey, Michigan 49770

1 October, 2010

Daytona Beach, Florida Retail Report 1

I

NTRODUCTIONFigure 1: Daytona Beach’s Old Downtown, looking west. The historic shopping district fronts a waterfront park and has excellent access from the surrounding neighborhoods and highways. (Photo source: Bing Maps)

Executive Summary

The greater Daytona Beach market appeals to a broad and diverse population that includes a stable 260,000 residential base, 23,000 college students and 66,000 day time workers. The region is also a world class tourist destination with 7.75 million visitors enjoying its pristine beaches, the famous Daytona 500 Speedway and several special events. In 2010, the Daytona trade area (as defined in this study below) generated an estimated $2.6 billion in annual retail sales, including $811 million from tourism and $136 million worker spending. By 2015, the trade area‟s total spending is estimated to grow to $3.4 billion. A recent proposal from a major national restaurant to open a flagship unit on the waterfront underscores the region‟s economic vitality.

The Beach Street shopping district commercial area is located on the east side of the mainland and near the tourist district, enabling it the ability to appeal to all the various components of the area. The existing retail and restaurant base is largely locally owned and operated, and in most cases unique to the market. The shopping district is anchored by numerous restaurants, jewelry stores, a candy factory and specialty destination businesses. The northern periphery of the study district, with the southern boundary is anchored by municipal uses (5th District Court and a firehouse). The primary shopping district is found between Orange Avenue and Bay Avenue along Beach Street.

Daytona Beach, Florida Retail Report 2

Figure 2: One mile radius of Daytona Beach study area includes most of the historic central business district along Beach Street.

Daytona‟s trade area population includes a wide range of desirable population segments including active seniors, empty nesters and young families. The market is divided into specific subcategories and includes 16,000 “Senior Sun Seekers” whom are generally health-conscious watch cable television, read boating magazines and eat at family restaurants and steak houses. Approximately 23,000 or 20 percent of Daytona‟s trade area‟s population is classified as “Silver and Golds”. These seniors are well educated and financially prosperous. They drink imported wines, tend to own common stock, shop at Publix grocery stores order from the L.L. Bean, Eddie Bauer, and Land‟s End catalogs. They purchase golf clothing, go to the beach and dine out at least once a week. They go sailing, power boating, fishing and golfing and have taken an overseas cruise vacation.

Daytona‟s trade area is also made up of 9,500 “Old and New Comers”, who are either starting their careers or retiring. Their income is derived from wages, dividends, rental properties, retirement income; almost one-fourth of Old and Newcomers receive Social Security benefits. They purchase children‟s books, drink domestic table wines, buy home office furniture andgo to the movies about once a month. They listen to classic hits, classical and Hispanic radio and watch The Golf Channel and MTV2 on television. They also shop at Pier 1, Harris-Teeter and their favorite restaurants include Tony Roma‟s, Steak „n Shake, and Red Robin.

The “Mid Life Junction” demographic lifestyle group represents 10 percent of the trade area and includes 12,000 persons. Mid Lifers are phasing out of the child-rearing years and approaching retirement. Most Midlife Junction residents are still working and live quiet, settled lives. They spend their money carefully and don‟t succumb to fads. Favorite family restaurants include Krystal‟s, Ruby Tuesdays and Captain D‟s. They

Daytona Beach, Florida Retail Report 3

search for bargains in the J.C. Penney catalog and at Belk, Lowe‟s and Wal-Mart. They also order from the Eddie Bauer and Land‟s End catalogs.

This study finds that the greater Daytona Beach region is significantly under serving the commercial desires and needs of its local and visitor community as well as not fully taking advantage of its powerful international brand. Many of Daytona‟s visitors lodge outside of the region, or limit their stay and spending. The defined Daytona Beach Street district is attracting neither enough of the trade area residential base, nor the tourism spending, to maximize its potential.

Daytona‟s Beach Street has the potential to expand its existing commercial area by an additional 86,000 square feet of new retail, restaurant and entertainment venues by 2015. This expansion can be achievable by capturing existing retail and restaurant spending that is presently leaking outside of Daytona Beach by its residents,

employment base and visitors. If implemented, this expanded retail could generate up to $38.5 million in additional annual sales by 2015.

While the commercial area is an attractive historic destination, it simply lacks the popular regional and national brands that are preferred by many of its residents, workers and visitors. As a result, over $34.6 million of annual spending presently occurs elsewhere, or not at all. The existing businesses would likely experience significant increased traffic and sales with the addition of new entertainment, dining and retailers, such as Dave & Buster‟s, Lucky Strike, Starbucks and large themed restaurants.

This study finds that the following amounts of retail and restaurants are supportable in the defined Beach Street study area in addition to the existing businesses:

30,000 square feet of entertainment such as Dave & Buster‟s or Lucky Strike

26,000 square feet of restaurants, such as Famous Dave‟s or Chima and/or Rio‟s Brazilian Steakhouse

12,000 square feet of apparel and shoes

18,000 square feet of gifts and misc. retailers

In addition, GPG recommends that a year round, full time public market should also be considered for the Beach Street area. These markets operate seven days per week and include full range of locally grown fresh food, produce and quick service foods. GPG recommends that a 20,000 square foot market be studied in more detail. The North Market, in Columbus, Ohio and London, Ontario‟s Covent Garden Market could serve as a model for Daytona.

Daytona Beach, Florida Retail Report 4

.

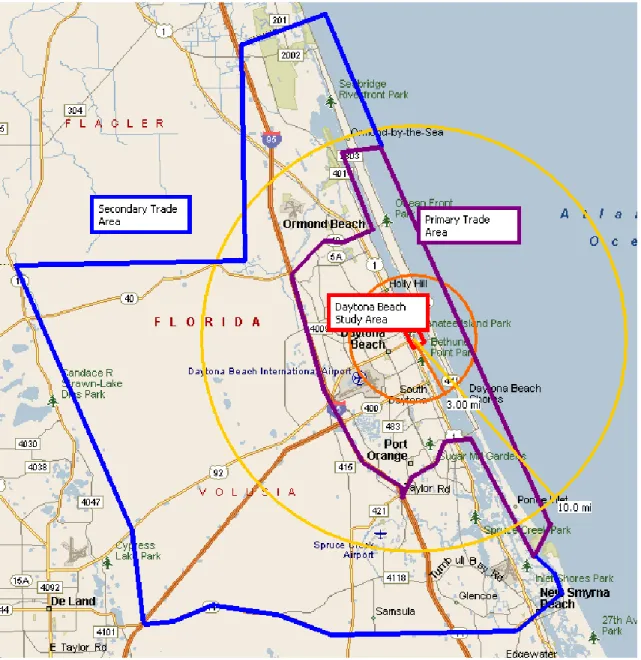

Figure 3: Daytona Beach is located on the Atlantic coast of Florida just 50 miles northeast of Orlando and is a popular vacation destination for both the region and the U.S. Eastern Seaboard.

This study has defined primary and secondary trade areas with a current population base of nearly 137,000 persons and 254,000 persons, respectively. This region is projected to increase to over 138,800 persons and 266,000 persons by 2015. The base reflects an older consumer (median age of 45.7 and 48.4 for the primary and total trade areas) with small household sizes (2.11 and 2.20, respectively). The home-ownership base is good (61% and 71%) with a strong seasonal household base found along the Atlantic Ocean in the community of Daytona Beach Shores (44%).

The region‟s large amount of retired population contributes to moderate household incomes of $37,285 in the primary trade area. However, 23 percent of the total trade area residents aged 25 and older has a college or higher degree. Nearly 60 percent of the total trade area‟s residents are employed in white collar positions.

In addition to the trade area‟s residential base, the Beach Street shopping district is well positioned to serve a strong employment base of over 66,000 daytime workers located within 10 miles. More than a third is employed in high paying executive and professional positions. The district is also located near a strong student population base of over 23,000 students attending Bethune-Cookman University and Daytona State College. These workers and students would likely shop and dine more frequently in the North Beach Street commercial area if it were better marketed and offered a broader selection of restaurants and retailers.

Daytona Beach, Florida Retail Report 5

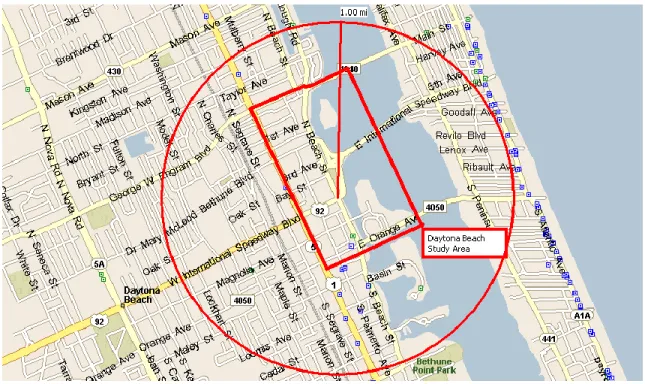

Figure 4: Daytona Beach Street shopping district study area is located on the main land, and within 1 mile of the beaches.

Finally, Dayton‟s Beach Street area is well situated to capture additional sales from the area‟s strong tourism base due to both the location as well as the other traffic generators located near the shopping district, including the ball park, Halifax Museum, City Library and the Daytona State College-News Journal Center. The Daytona Beach market is a strong tourist destination with an especially large potential to attract more day and overnight visitors from the Orlando markets.

Background

Gibbs Planning Group, Inc. (GPG) has been retained by the City of Daytona Beach CRA to access the viability of retail for the Beach Street shopping district (also called

Riverfront Marketplace) in Daytona Beach, Florida. The study area is located between Fairview Avenue and Orange Avenues (north to south) and Ridgewood Avenue (US Highway 1) and the Intercoastal Waterway (west to east).

Issues

The following issues were addressed in this analysis:

What is the existing and planned retail market in the greater Daytona Beach, Florida market?

Daytona Beach, Florida Retail Report 6

What are the current and projected trade area population and demographic characteristics? What are the trade area psychographics (lifestyles)?

What is the current and projected growth for retail expenditures for 2010 to 2015?

What additional components (i.e. tourism and college students) are available to help support retail in the district?

What type of retail is supportable and should be attracted to the Daytona Beach site? What are their anticipated sales volumes?

Methodology

To address the above issues, a detailed evaluation of the retail in Daytona Beach Heights, as well as all major existing and planned shopping centers and retail

concentrations in and surrounding the defined trade area, were conducted during the week of August 30, 2010. During this evaluation, GPG thoroughly drove the market and evaluated the major existing and planned retail concentrations in the area. The area was visited during the daytime, as well as the evening, to gain a qualitative understanding of the retail gravitational and traffic patterns throughout the study area.

GPG then defined a primary and secondary trade area for the Daytona Beach location based on the field evaluation. Population, demographic and lifestyle characteristics of trade area residents were collected by Census Tract from national sources, and updated based on information gathered from various local sources.

Additionally, GPG identified the other sources of sales for the district, including college students and tourism that would not be included in the Census data. Current and projected estimates of retail expenditure potential were computed using out proprietary models of expenditure potential, the US Census of Retail Trade, sales tax information, and trade area population levels. Using average sales per square foot (sf) for the identified retail categories, a retail void analysis of the market was conducted. Finally, based on the population and demographic characteristics of the trade area, existing and known planned retail competition, the results of the retail void analysis, and traffic and retail gravitational patterns, GPG developed this assessment of the Daytona Beach Heights site and forecast sales for the supportable retail.

Assumptions

Any study such as this analysis needs to make certain assumptions that may change over time. For the purposes of this analysis, the following assumptions have been made:

1) The economic conditions of the greater Daytona Beach, Volusia County market will remain stable and grow as projected through 2015. Further, the housing and time-share market will continue to stabilize. Given the current economic

conditions in eastern Florida, this is a conservative assumption.

2) The district will be developed to maintain the existing building structures and the non-retail uses in the area (Halifax Museum, City Library, Daytona Beach Cubs minor league baseball team, and News Journal Center (Daytona State College of the Arts) will continue to be utilized. Further, it is assumed that the new

Daytona Beach, Florida Retail Report 7

recommended retail, restaurant and entertainment venues will be opened by 2012.

3) The retail will have adequate visibility, ingress/egress and parking for the proposed uses. Additionally, they will be marketed as a single shopping destination in the area’s tourist guides.

4) The district will continue to be managed as a walkable district, to the best practices of The American Planning Association, The Congress for the New Urbanism, The International Council of Shopping Centers and The Urban Land Institute.

5) Parking for the area is assumed adequate for the proposed uses, with easy access to the retailers in the development. An overall parking ratio that meets industry standards or higher, is anticipated for this area. Additionally, the parking is assumed to continue to be free for off-street lots and that meters will be

installed for prime on-street locations. Limits of Study

The findings of this study represent GPG‟s best estimates for the amounts and types of retail tenants that should be supportable at the subject site through 2015. Every

reasonable effort has been made to ensure that the data contained in this study reflect the most accurate and timely information possible and are believed to be reliable. This study is based on estimates, assumptions, and other information developed by GPG independent research effort, general knowledge of the industry, and consultations with the client and its representatives. No responsibility is assumed for inaccuracies in reporting by the client, its agent and representatives or in any other data source used in preparing or presenting this study. This report is based on information that was current as of August 31, 2010, and GPG has not undertaken any update of its research effort since such date.

This report may contain prospective financial information, estimates, or opinions that represent GPG‟s view of reasonable expectations at a particular time, but such information, estimates, or opinions are not offered as predictions or assurances that a particular level of income or profit will be achieved, that particular events will occur, or that a particular price will be offered or accepted. Actual results achieved during the period covered by our prospective financial analysis may vary from those described in our report, and the variations may be material. Therefore, no warranty or representation is made by GPG that any of the projected values or results contained in this study will be achieved.

This study should not be the sole basis for programming, planning, designing, financing or development of a commercial center. Further research and analysis is advised prior to implementing development or land use policy stragetyies.

The Trade Area

Based on GPG‟s field evaluation and the existing retail nodes in the greater Daytona Beach market, it was determined that future retail in the study area could have both a neighborhood/community, as well as a more regional appeal. As such, the primary trade

Daytona Beach, Florida Retail Report 8

area (that would be served by the neighborhood and community-oriented retail) is approximately delimited by the following boundaries:

North to State Highway 40 (Granada Boulevard) (Six miles).

East to the Atlantic Ocean (One Mile).

South to Dunlawton Avenue (State Highway 421) (Six Miles).

West to Interstate 95 (Five Miles).

Please refer to the following Figure 5 below for boundaries of the primary trade area:

Figure 5: The estimated primary trade area boundary estimated by this study is shown above inside of the purple lines.

Daytona Beach, Florida Retail Report 9

The secondary trade area extends further north to the Volusia County Line, south to State Highway 44 (Lytle Avenue) and west to State Highway 11 and Deland as shown in the following Figure 6.

Figure 6: The secondary trade area described in this study is shown above inside of the blue lines.

Demographic Characteristics

Using data from both ESRI and Claritas, GPG obtained the population and demographic characteristics for the defined trade area, as well as for Daytona Beach and surrounding communities and Volusia County.

The primary trade area has an estimated 2010 population of 136,850 persons, which is projected to grow to 138,807 persons by 2015, a 1.4 projected increase over the five-year period. The number of households in the primary trade area, currently estimated at 62,050, is also expected to grow to 63,219, or 1.9 percent by 2015. Currently there are

Daytona Beach, Florida Retail Report 10

an estimated 2.11 persons-per-household, most (61%) of the household base is owner-occupied and 17 percent of the household base is seasonal.

The highest projected growth in the defined primary trade area is found in Census Tracts 808.04 and 824.09 (13% and 7%, respectively) located in the northwest and south west periphery of the primary trade area.

The secondary trade area offers an additional 117,340 persons for a total trade area population base of 254,200 persons. The population base is projected to grow 8.6 percent in the secondary trade area by 2015, resulting in a total trade area population base of 266,183 persons, a 4.7 percent projected growth rate. The household base in the secondary trade area is approximately 50,000, producing a total trade area

household base of 112,028. This base is projected to grow to 117,060 households (or 4.5%) by 2015. The persons-per-household in the secondary trade area is 2.30 and 2.20 in the total trade area. The total trade area‟s household base is 71 percent

owner-occupied and only 12 percent seasonal.

Table 7 presents and compares the demographic characteristics found in the defined primary trade area to that of the City of Daytona Beach and Volusia County:

Figure 7: Demographic Characteristics Table

Characteristics Primary

Trade Area Total Trade Area

Daytona Beach Volusia County 2010 Population 136,848 254,187 66,207 515,563 2015 Population 138,807 266,183 66,651 545,523

Projected 5-Year Growth 1.4% 4.7% 0.7% 5.8%

2010 Households 62,043 112,028 29,591 213,973

2010 Median Household Income $37,258 $44,259 $32,238 $45,451

2010 Per Capita Income $24,021 $27,158 $21,600 $25,100

% Households with Incomes

$100,000 or higher 10% 13% 8% 13%

Persons Per Household 2.11 2.20 2.04 2.34

% HHolds Owner -Occupied 61% 71% 47% 75%

% Seasonal Households 17% 12% 9% 8%

Median Age 45.7 48.4 38.8 46.3

% White-Collar Employed 57% 59% 55% 58%

% College Educated 21% 23% 21% 20%

As shown in Figure 7, incomes in the defined trade areas are moderate, but stronger in the total trade area than that found in the primary trade area. Close-in to the site, incomes are strongest in the census tracts found along the Atlantic Ocean.

Daytona Beach, Florida Retail Report 11

The cost of living in the area, according to Kiplinger, is comparable to the US average as shown in Figure 8 below:

Figure 8: Daytona Metropolitan Area Cost of Living

Metropolitan Area Cost of

Living*

Median Income

Income Growth

Daytona Beach/Deltona/Ormond Beach, FL 100 $41,772 4.4%

Jacksonville FL 94 $51,269 4.0%

Orlando Kissimmee, FL 98 $49,789 4.3%

Miami/Ft Lauderdale FL 120 $47,527 3.7%

Tampa/St Petersburg/Clearwater, FL 99 $45,243 4.7%

*Where 100 is the US Average

The average age in the market is much older than the US average (45.7/48.4 versus 35.6), resulting in a lower persons per household (2.11/2.20). Additionally, the area is primarily White (73%/82%), although the City of Daytona Beach has a strong African American base as well (37%).

The housing base is primarily occupied (61%/71%), with the stronger owner-occupied base found on the periphery of the primary trade area and in the secondary trade area. The housing base along the Atlantic Ocean is more apt to be seasonal housing than in the other areas of the defined trade areas.

When compared on a mile ring basis, there are 10,850 persons within one-mile of the site, growing to 61,840 persons in three-miles and 120,800 persons in five-miles. This base is projected to be stable close-in, but grow 0.2 percent and 0.6 percent at three- and five-miles over the next five years. The persons-per-household in the one-, three- and five-mile radius is reported as 1.87, 2.14 and 2.13, respectively. Year 2010 incomes (median household income/per capita income) in these radii are reported as

$21,850/$15,727, $29,692/$18,578 and $34,043/$21,119. The median age is reported as 37.0, 37.3 and 41.1 at the same radii. Home ownership is reported as 30 percent, 47 percent and 59 percent at one-, three- and five miles.

Tapestry Lifestyles

As a part of the research for this study, ESRI demographic data was purchased by GPG. ESRI is an international research group that has developed Tapestry Lifestyles, which is an attempt to create 65 classifications, or lifestyle segments, that help determine

purchasing patterns. These segments are broken down to the U.S. Census block group level throughout the United States and are used by many national retailers to help determine future potential locations. Figure 9 details the top Tapestry Lifestyles found in the greater primary and total Daytona Beach trade areas.

Daytona Beach, Florida Retail Report 12

Figure 9: Tapestry Lifestyles

Lifestyle Primary Trade Area Total Trade Area Short Description Senior Sunseekers 8,476 14% 15,900 14%

Although the median age in this market is 51.8 years, well over half of the householders are aged 55 years or older. Most of these households are married couples without children and single persons. The segment is not very ethnically diverse; almost 90 percent of the population is white. Escaping from cold winter climates, many Senior Sun Seekers have permanently relocated to warmer areas; others are “snowbirds” who move South for the winter. Trash compactors are popular appliances with Senior Sun Seekers residents.

They belong to a car dealer‟s auto club, drink low- or no-alcohol beer and tomato juice, and buy books at a warehouse store or by mail order. Health-conscious Senior Sun Seekers purchase bifocals, visit their internists and take Centrum Silver vitamins. They watch cable television, read boating magazines and eat at family restaurants and steak houses.

Silver & Gold 7,896 13%

23,243 20%

With a median age of 57.6 years, more than 20 years above the national average, Silver and Gold households are made up primarily of older married couples without children. Silver and Gold

neighborhoods are not ethnically diverse; more than 90 percent of these residents are white. These seniors are well educated and financially prosperous. Silver and Gold residents drink imported wines, buy books at a warehouse store, would buy a PC directly from the manufacturer, and own a fax machine.

They tend to own common stock, bank by mail, use a stock rating service, and hold personal liability insurance policies. They shop at Publix grocery stores and take prescription medications for arthritis. Silver and Gold residents are prototypes of active seniors.

Silver and Gold residents order from the L.L. Bean, Eddie Bauer, and Land‟s End catalogs. They order cookware, kitchen

accessories and flowers by phone, mail and online.

They purchase golf clothing and women‟s swimsuits, own a hot tub or whirlpool spa, go to the beach and dine out at least once a week. They go sailing, power boating, fishing and golfing and have taken an overseas cruise vacation.

Old & New Comers

7,843 13%

9,568 8%

Old and Newcomers are neighborhoods in transition, populated by renters who are either starting their careers or retiring. The general population indexes higher than the U.S. for age groups 20-29 and over 75. Old and Newcomers’ median household income of $39,400 is derived from wages, dividends, rental properties, retirement income; almost one-fourth of Old and Newcomers

receive Social Security benefits. Purchases of children‟s books, osteoporosis medications and long-term-care insurance policies reflect the disparate ages of the residents in Old and Newcomers

neighborhoods.

They take their cars to chain stores for service, drink domestic table wines and buy home office furniture. Younger Old and Newcomers go to the movies about once a month, visit the zoo and gamble in Las Vegas. They listen to classic hits, classical, and Hispanic radio and watch The Golf Channel and MTV2 on

Daytona Beach, Florida Retail Report 13 Lifestyle Primary Trade Area Total Trade Area Short Description

They shop at Pier 1, Harris-Teeter and Walgreen‟s stores, order from priceline.com and own a pet cat. Although they don‟t dine out very often, when they do their favorite restaurants include Tony Roma‟s, Steak „n Shake, and Red Robin.

Midlife Junction 7,268 12% 11,872 10%

The segment name says it all: Midlife Junction residents are phasing out of the child-rearing years and approaching retirement. Most Midlife Junction residents are still working, earning a median household income of $41,800 derived from wages, dividends, rental properties, retirement income and Social Security benefits. As Midlife Junction residents pass from child rearing into

retirement, they live quiet, settled lives.

They spend their money carefully and don‟t succumb to fads. Fiscally conservative Midlife Junction residents belong to senior banking clubs, own savings certificates and consult financial planners. They hold boat owners‟, travel and homeowners insurance policies. Mindful of their health, Midlife Junction

residents take vitamin supplements, arthritis medication and shop for sugar-free foods.

Favorite family restaurants include Krystal‟s, Ruby Tuesdays and Captain D‟s. They search for bargains in the J.C. Penney catalog and at Belk, Lowe‟s and Wal-Mart. They also order from the Eddie Bauer and Land‟s End catalogs.

Daytime Employment

In addition to the residential base, Daytona Beach‟s Beach Street district has the opportunity to serve a sizeable daytime employment base. Within a five-minute drive time of the site, there are 28,000 employees, of which 32 percent are employed in executive and professional positions. This base grows to 66,140 employees in ten-minutes of which 34 percent are employed in executive and professional positions. Figure 10 details the near-by daytime employment base by employment type. Major employers in the Volusia County area include:

Halifax Health 4,230 employees

Florida Hospital 3,720 employees

Publix 2,415 employees

Wal-Mart 2,140 employees

Embry Riddle Aeronautical Univ. 1,200 employees Florida Health Care 870 employees Bright House Networks 660 employees

Bert Fish Memorial 640 employees

Daytona Beach, Florida Retail Report 14

Figure 10: Business Facts: Workplace Population 2009

Description 5 Minute(s) 10 Minute(s)

Count Percent Count Percent

Total Employment 28,004 66,136

Executive and Professional 9,091 32% 22,719 34%

Management 1,936 7% 4,624 7%

Sales and Marketing 2,549 9% 8,980 12%

Health-Legal-Social 2,470 9% 3,980 8%

Engineer-Science-Computer Professional 451 2% 929 1%

Educators 1,091 4% 2,796 4%

Journalists-Creative Professional 594 2% 1,411 2%

Administration and Support 7,521 27% 16,643 26%

Management Support 867 3% 1,733 3%

Admin-Clerical Support 5,293 19% 12,409 19%

Technical Support 1,361 5% 2,501 5%

Service Personnel 5,161 18% 11,448 18%

Health Care Personnel 732 3% 1,568 3%

Food and Beverage 2,842 10% 6,458 10%

Personal Services 858 3% 2,094 3%

Protective Services 728 3% 1,328 2%

Trade and Labor 6,231 22% 15,326 22%

Construction 960 3% 2,140 3%

Installation and Repair 2,444 9% 5,915 8%

Craft Production 255 1% 830 1% Machine Operators 373 1% 1,086 1% Assemblers 147 1% 543 1% Transportation 953 3% 2,011 3% Agriculture 356 1% 737 1% Laborers 743 3% 2,064 3%

© 2010 The Nielsen Company. All rights reserved.

Unemployment in the Daytona Beach area is reported as 11.9 percent for the second quarter of 2010.

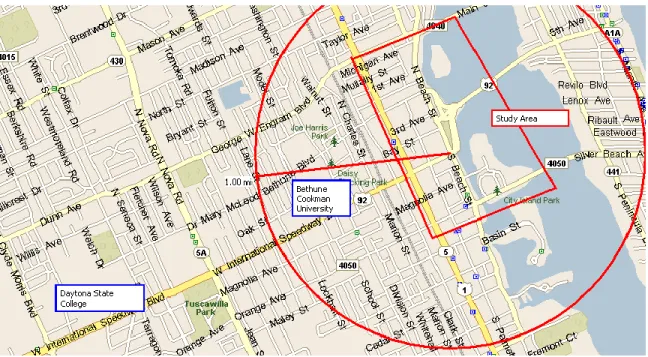

College Student Population Base

The site is well positioned to serve a strong and growing student population base. Both Bethune-Cookman University and Daytona State College are located within two miles of the study area, more than close enough to serve the retail and/or restaurants in the area. Bethune-Cookman University is affiliated with the United Methodist Church and offers

Daytona Beach, Florida Retail Report 15

degrees in 35 majors in seven academic schools.The University was founded in 1904, and boasts a diverse and international faculty and student body of more than 3,600 persons. The University is also one of three private historically Black colleges in the State of Florida.

The Daytona State College is located approximately two miles west of the study area and offers more than 100 certificate and associate degrees of science, as well as

bachelor degrees in applied sciences, supervision and management, and education. The school was established in 1957. The college student population of approximately 19,000 students is up from approximately 12,000 in 2004. In the past three years alone, the student base has risen 24 percent. Most of the increase is thought to be due to the current economic conditions and the re-training of personnel for new careers.

Figure 11: Location of Colleges to the Daytona Beach study area.

Tourist Component

Finally, Daytona Beach is a strong tourist destination, attracting 7.75 million visitors each year (2008 counts) that have an estimated $4.6 billion impact on the local economy. By expenditures, the Figure 12 details the added expenditure potential added to the Daytona Beach market.

Figure 12: Tourist Added Expenditure Potential

Tourist Expenditures Amount Percent Added Impact

Hotel Expense $763,310,000 48%

Other Expenditures $811,167,000 52%

Total $1,574,477,000

The major attraction to the area, other than the pristine beaches, is the Daytona 500, which alone attracts an estimated 185,000 persons per year. Aptly named, the Daytona

Daytona Beach, Florida Retail Report 16

500 is a 200 lap, 500 mile race that takes place in February. The Daytona International Raceway is also known as the “official attraction of NASCAR” offering 60,000 square feet of exhibit areas open year-round.

Hotel occupancy is highest in July, followed by March, February and June as shown in Figure 13 for the past two years:

Figure 13: Daytona Beach Hotel Occupancy for 2008-2009

By far, most visitors reach Daytona Beach via car (81-84%), with the Daytona Beach Airport reporting a total of 211,831 passengers arriving in 2009, down slightly from the 244,084 that utilized the airport in 2008.The average party size was reported as 2.5 and the average length of stay is 4.0 days.

Figure 14: Visitor Demographics

1st Qtr 2009 2nd Qtr 2009 3 rd Qtr 2009 4 th Qtr 2009 Annual 2009

% First Time Visitor 28.3 27.0 27.7 25.0 27.0

Average Party Size 2.4 2.6 2.7 2.4 2.5

% Traveled with no Kids 83.7 76.3 70.0 77.0 76.8

Average Length of Stay 5.2 3.5 3.7 3.7 4.0

Average Daily Expenditure* $117.33 $96.33 $99.00 $106.00 $104.67

Average Room Rate $119.81 $93.17 $92.58 $88.40 $98.49

Daytona Beach, Florida Retail Report 17

Major Museums and Performing Venues

Ocean Center. The newly expanded Ocean Center is a major attraction for conventions as well as an entertainment complex, offering 94,700 square feet of exhibition space, 25,400 square feet of meeting rooms, a 9,600 seat arena and a 12,000 square foot ballroom.

Halifax Historical Museum. The museum is housed in the former Merchant‟s Bank building located along Beach Street in the downtown historical district. It displays photographs from the late 1890‟s as well as historical data of the local Native Americans, the Spanish and British colonial eras, and early auto racing. It also has a theater with seating for 70.

Southeast Museum of Photography. This 10,000 square foot facility is one of the only Southeast museums to be devoted entirely to the art of photography. Daytona Beach Bandshell. Located in Oceanfront Park, the bandshell offers over 190,000 square feet of flexible space with seating for up to 9,000 persons. It plays host to a variety of performances including concerts, art exhibits and trade shows.

Daytona Beach, Florida Retail Report 18

Museum of Arts & Sciences. The area‟s largest museum sits on a 90 acre park preserve and is home to Chapman Root Hall (seating 260), the Root Family Museum, the Cuban Foundation Museum, the Williams Family Children‟s Museum and a planetarium. The museum is home to the largest Coca-Cola memorabilia collection in the State of Florida and offers a total of 98,000 square feet.

Peabody Auditorium. Situated across from the Ocean Center, the Peabody Auditorium is an historic 2,560-seat performing arts theater attracting renowned artists, symphony orchestras and ballet companies.

News Journal Center at Daytona State College. Situated on Beach Street, the venue is perfect for medium-sized musical and theatrical performances. The main theater seats 859 guests and the smaller studio theater seats 264. The Goddard Theater and Daytona State University Center. Located on Daytona State‟s main campus, theuniversity theater seats 490 people, while the Goddard Theater seats 150.

Mary McLeod Bethune Performing Arts Center. Located on the campus of Bethune-Cookman University, the center is a $23 million state-of-the-art facility that hosts a variety of performing events.

S

TUDYA

REAC

HARACTERISTICS LocationDaytona Beach, Florida Retail Report 19

The study area is located between Fairview and Orange Avenues (north to south) and Ridgewood Avenue (US Highway 1) and the Intercoastal Waterway (west to east) as shown in Figure 16. Beach Street offers the majority of the retail in the district with retail/restaurants facing east towards the waterway. The district is anchored on the northern periphery by the Daytona State College-News Journal Center and a collection of service businesses.

Figure 17: Old Town’s shopping district offers a collection of attractive historic buildings and unique restaurants and businesses. The district’s market has the potential to support an additional 86,000 square feet of new restaurants and retailers.

Figure 18: The News Journal Center, home of the Daytona State College of the Arts, is located on Beach Street between Bay Street and International Speedway Boulevard.

However, most of the shopping in the district is found between Bay Street and Orange Avenue, with International Speedway Boulevard the center point of the district. This portion of the area is easily walkable, with brick sidewalks and a landscaped center boulevard. The existing major destinations in the area include Coliseum Music Theater, News Journal Center (home of the Daytona State College of the Arts), Angell & Phelps Chocolate Factory and Café, Halifax Historical Museum and the Daytona Cubs Ball Park. The southern periphery of the study area is bounded by a Daytona Beach Firehouse and the 5th District Court of Appeals.

Daytona Beach, Florida Retail Report 20

Figure 19: The main shopping area along Beach Road (above) includes the Halifax Historical Building (bottom right).

A mixture of some retail can be found between Beach Street and Ridgewood Avenue (US Highway 1), but non-retail uses such as churches, government buildings (city and state services as well as a US Post Office and Justice Center) and residential housing (single family) are prevalent.

Figure 20: Non-retail uses such as the Daytona Beach Service Center (left), and the US Post Office (right) provide major employment centers and anchors for Daytona’s Old Town and are vital for its commercial sustainability.

Figure 21: Daytona Beach’s 1st

Baptist Church (left) and The Basilica of St Paul (right) are significant contributors to the downtown’s historic fabric as well as important anchors for its commerce.

Daytona Beach, Florida Retail Report 21

Figure 22: Significant buildings and destinations around the study area.

Figure 23: The Volusia County Early Learning Coalition (left) and the Daytona Beach City Center Building (right provide major employment centers for Old Town’s restaurants and retailers.

Daytona Beach, Florida Retail Report 22

Figure 24: Old Town is surrounded by numerous historic walkable neighborhoods that include a variety of good housing stock. The above homes are found between Beach Street and US Highway 1.

Access

Daytona is only 50 miles northeast of Orlando, and therefore benefits from quick access to major population centers. The Beach Street shopping district is less than five miles from I-95. Regional access is easily available via International Speedway Boulevard (US Highway 92), connecting Highway A1A along the Atlantic Coast to Interstate 95 (directly) and Interstate 4 (indirectly). Interstate 95 is the primary north/south interstate in eastern Florida. Interstate 4 connects the Daytona Beach area to Orlando and central Florida.

Local access to the site is also primarily provided by International Speedway Boulevard, with 4 lanes of traffic (35 miles per hour) at the site. Other east/west local access to the site is provided by Fairview and Orange Avenues, both of which offer additional access across the Intercoastal Waterway (Fairview turning into Main Street and Orange Avenue turning into Silver Beach Avenue). North/south local access to the area is provided by Ridgewood Avenue (US Highway 1). Both regional and local access could be easier with improved way-finding signage.

Figure 25 details the latest 24 hour average traffic counts as provided by the Volusia County Traffic Engineering Department.

Figure 25: Traffic Counts

Location Traffic Count Year of Count

Interstate 4 at Interstate 95 45,500 2009

Interstate 95 at International Speedway 119,000 2008

International Speedway at Beach Street 17,700 2009

Ridgewood (US Hwy 1) at Fairview Avenue 28,000 2009

Ridgewood (US Hwy 1) at Orange Avenue 29,000 2009

Daytona Beach, Florida Retail Report 23

Daytona Beach, Florida Retail Report 24

Visibility

Retail stores along Beach Street are challenged from their location between the heavily traveled beach roadways. In general, the commercial area has limited visibility due to the east/west traffic flow between the Atlantic Ocean and Interstate 95 and the retail‟s facing towards the east. Those staying along the ocean have no visibility of the district due to the buildings located between the hotels along the ocean and the waterway. Furthermore, those traveling along Ridgewood have no visibility of the retail located along Beach Street.

The introduction of new regional and national retail restaurant and retail anchors would provide needed pedestrian and shopper traffic for the existing independent retailers and improve their sustainability. Additional way-finding signage, marketing and

advertisement can also supplement Beach Street‟s visibility challenge.

Daytona Beach, Florida Retail Report 25

Parking

Parking for the retail/restaurant uses in the district is provided along Beach Street, (angled parking for south-bound traffic and parallel parking for north-bound traffic) as well as, lot parking provided behind the retail between Beach and Palmetto Streets. The downtown appears to have the necessary numbers of parking stalls for its size of

commercial. However, GPG noted that most of the Beach Street parking stalls was filled, even during the early morning, indicating that residents and employees likely park in front of the stores, rather in the rear surface lots. This is a common fact of urban commercial districts that can only be resolved with metered parking.

Today‟s urban shoppers consider time to be the new luxury, and prefer to park in front of the destination store or restaurant rather than in its back. Most of these shoppers will gladly pay a small fee for the convenience of close store front parking. Free remote parking should be provided for those more spend thrift shoppers. GPG has found that metered on-street parking stalls can generate up to $200,000 per stall in annual retail sales, or every two metered stalls can directly support one small business. The City has plans to widen Beach Streets sidewalks and add additional on-street parking. GPG recommends that all of the prime Beach Street parking stalls be metered with simple coin operated individual meters at a rate of $0.50 per hour 9:00 am to 8:00 pm Monday to Saturday.

Public Transportation

Almost all of the visitors to the Beach Street area will travel by cars or in a group tour bus. A considerable number of workers and residents live within a ten minute walk and make up a significant potential portion of the business districts commerce. There are several public bus stops provided along Beach Street as provided by Voltran, the area‟s public transportation service. The region is not served by light rail or high speed regional rail.

Figure 28: The Volusia Mall is the primary shopping destination in the City of Daytona Beach, featuring anchors including Dillard’s.

Other Shopping Areas

As part of GPG‟s field evaluation, most major shopping concentrations in and around the periphery of both the primary and secondary trade areas were visited. The primary shopping destination in the City of Daytona Beach is the Volusia Mall, located on US Highway 92/International Speedway Blvd. and Bill France Boulevard. The center offers 1.06 million square feet of retail space in a single level enclosed shopping experience. Anchors at the center include Dillard‟s, JC Penney, Macy‟s and Sears (56 percent of the

Daytona Beach, Florida Retail Report 26

total available space). The ancillary space at the center has only three vacancies and has a strong appeal to the area‟s moderate incomes.

The center anchors the eastern boundary of a strong core of big-box anchored retail along International Speedway Boulevard that extends to Interstate 95. In total, there are seven centers offering an additional 1.2 million GLA along the corridor, making the corridor the strongest shopping district in the area.

Figure 29: Shopping Centers along International Speedway Boulevard

Center Location Total GLA Anchors

Volusia Square 2455 International Speedway 373,383 Home Depot, Hobby Lobby, HHGregg, Toys‟R‟Us International

Speedway Square 2500 International Speedway 258,189

Bed Bath & Beyond, Dicks Sporting Goods, Stein Mart Volusia Marketplace 2400 International Speedway 145,000 Ashley Furniture, World Market Best Buy Plaza 1900 International Speedway 246,735 Best Buy, American Signature

Furniture, Barnes & Noble Speedway Village 2254-2296 International

Speedway 56,000 Vitamin Shoppe

Unnamed Center 2200 International Speedway 60,294 Haynes Bros. Furniture Volusia Plaza 1800 International Speedway 75,000 Marshall‟s

Figure 30: Volusia Square included major retail anchors.

Figure 31: International Speedway Square (left) and Best Buy Plaza (right) include some of the leading retailers such as Best Buy, Dick’s Sporting Goods and Old Navy.

Daytona Beach, Florida Retail Report 27

Figure 32: Map detailing the locations of shopping centers along International Speedway Boulevard.

The other regional-oriented retail center, located on the southern periphery of the

defined trade area is the Pavilion at Port Orange. The Pavilion is a new open-air lifestyle center anchored by Belk‟s and Hollywood Cinema, located at Williamson and Dunlawton just off Interstate 95. The center is still being developed and offers a mix of category-killer box retailers (Michaels, HomeGoods/Marshall‟s, Ulta and Petco) as well as smaller specialty/lifestyle retail such as Maurice‟s, David‟s Bridal, Rackroom Shoes, Rue 21, Malibu Beach Club and Kirkland‟s.

Finally, there is a blended-lifestyle center (Trails Shopping Center) located north of the site at Nova Road and Main Trail. The center is anchored by Publix, but also offers a core of specialty retailers such as Chico‟s, Ann Taylor Loft, Talbots, Coldwater Creek and Jos. A. Banks. The center also has a strong restaurant component, with a Panera Bread and Ormond Steakhouse.

Daytona Beach, Florida Retail Report 28

Figure 33: other regional-oriented retail centers, located on the far northern and southern periphery of the defined trade area.

Figure 34: The Pavilion at Port Orange (left) and the Trails Shopping Center (right).

Closer-in to the site, the most competitive retail to the study area is found east of the site along US Highway A1A (Atlantic Avenue). Atlantic Avenue is home to most of the area‟s

Daytona Beach, Florida Retail Report 29

resorts and timeshares, as such, offers a strong core of restaurant venues as well as the typical “beachwear” shops and convenience-oriented retail. Most of the core of the venues are located between International Speedway and Seabreeze Boulevard;

however, the only retail center is the Ocean Walk Village, located across from the Ocean Center and adjacent to the Hilton Hotel. The Ocean Walk Village is anchored by a 10 screen cinema and offers a mix of casual restaurants, but has a high vacancy rate (43 percent of the available shop space).

Figure 35: Ocean Walk Village is anchored by a 10 screen cinema and offers a mix of casual restaurants.

Additionally, Main Street offers the strongest core of bars and restaurants in the area, including Hog Heaven BBQ, Froggy‟s Saloon, the Pump Station, Full Moon Saloon, Boot Hill Saloon, Dirty Harry, and Cruzin Café. The retail in the Main Street district appeals primarily to the biker crowd.

On the mainland, close-in retail to the site is primarily located along Nova Road, and is neighborhood in orientation, as shown on the map in Figure 36.

Daytona Beach, Florida Retail Report 30

Figure 36:Close-in retail to the study area is primarily located along Nova Road, and is neighborhood in orientation.

S

UMMARY OFF

INDINGSAs a result of GPG‟s qualitative analysis, this study finds that the Beach Street shopping district area lacks enough retail and entertainment strength to attract its share of either the trade area‟s population base or the tourist potential. The primary retail attraction to the district is the Daytona State College-News Journal Center which anchors the northern end of the district.

This study also finds that while the existing restaurant base offers a diverse variety of independent operators, the base needs to be strengthened with several larger units having a wider appeal. As such, this analysis recommends several new restaurants for the district (both regional and national chains), as well as several smaller venues to further complement the existing base.

Daytona Beach, Florida Retail Report 31

Figure 37: The London, Ontario Covent Garden Market and the North Market, Columbus Ohio is successful mid-sized public markets that could serve as a model for a Daytona Beach public market.

A year round, full time public market should also be supportable in the Beach Street area. These markets operate seven days per week and include poultry, meat, cheeses, vegetables, fruits, flowers, prepared foods, and quick service foods. In general, the markets are more successful when there is two of each category (to promote competition). Such a market would provide needed goods and services for local residents, workers as well as the region and Daytona‟s many visitors. GPG

recommends that a 20,000 square foot market be studied in more detail. The North Market, in Columbus, Ohio could serve as a model for Daytona. The U.S. Department of Agriculture and other public and private agencies offer research and grants for markets. The district also needs to add more entertainment to attract the tourist component as well as the college students and local residents. As such, this study recommends either a Dave & Buster‟s or Lucky Strike (or similar entertainment venues).

Finally, with added entertainment and restaurant, the remainder of the district will be able to support additional small local shops (apparel, gifts and other retail).

Recommendations include shops from either the Daytona Beach area (some as

relocation) or from other Florida beach towns, to further complement the existing retail in the district. The added businesses will help to strengthen the retail base and increase exposure and sales of the existing base.

In total, this study finds that 86,000 square feet of additional retail, restaurants and entertainment venues is supportable in the defined Daytona Beach study area, as follows:

30,000 square feet of entertainment venues such as Dave & Buster’s or Lucky Strike Bowling center

18,000 square feet of casual restaurants serving liquor, such as Famous Dave’s, Chima or Rio’s Brazilian Steakhouse

8,000 square feet of casual restaurants and foods such as 5 and Diner, Cupcake Bakery or Heavenly Cheesecake, a local Burrito shop and/or a Vegan restaurant

12,000 square feet of casual and beach apparel and shoes

18,000 square feet of gifts and misc. retailers

Daytona Beach, Florida Retail Report 32

Please refer to the Appendix Tables for a complete recommended retail, restaurant and entertainment uses for the site.

Rationale

The rationale for recommending the above tenants is presented below:

Stable Trade Area Population Base The primary trade area, as defined, has a population base of 136,848 persons, growing 1.4 percent to 138,807 persons by 2015. The base grows to a total trade area total of 254,187 persons that is

projected to grow to 266,183 persons by 2015 (4.7%). The primary trade area will account for 50-65 percent of the retail/restaurant sales, depending on the

individual retailer or restaurant. The secondary trade area will account for an additional 10%-15% of the total sales.

Strong Tourist Potential. However, the site is well situated to capture

additional sales from the area‟s strong tourism base due to both the location as well as the other traffic generators located near the shopping district, including the ball park, Halifax Museum, City Library and the News Journal Center. The Daytona Beach market is a strong tourist destination, attracting 7.75 million visitors each year (2008 counts) that have an estimated $4.6 billion impact on the local economy. It is estimated that approximately $811 million is spent for

transportation, entertainment, and food and shopping by this tourist base annually. As such, we estimate that an additional 25-35% of the sales will be generated from the tourist population base.

Strong Daytime Population Base The site also has the potential to capture strong sales (10-15%) from the close-in daytime population base. Within a five-minute drive time of the site, there are 28,004 employees, of which 50 percent are employed in of which 32 percent are employed in executive and professional positions. Within ten minutes of the site this base grows to 66,136 employees, of which 34 percent are employed in executive and professional positions.

Strong Student Population Base The site is positioned near the Bethune-Cookman University which boasts a diverse and international faculty and student body of more than 3,600 persons. Additionally, Daytona State College is located approximately two miles west of the study area, and boasts a student population of approximately 19,000 students, up from approximately 12,000 in 2004.

Moderate Household Income Levels The primary trade area offers moderate household and per capita incomes levels reported as $37,258 and $24,021, respectively. The incomes levels are stronger in the secondary trade area resulting in higher, but still moderate, trade area incomes of $44,259 and $27,158.

Trade Area Demographics The total trade area base offers an older consumer (median age of 48.4) that has average education levels (23 percent of those aged 25 and older have a college degree) and primarily white collar employed (59%). Most of those employed are employed in sales (14%) or administrative

Daytona Beach, Florida Retail Report 33

support (12%) positions. Racially, the base is primarily white (82%), but has a stronger African American base close-in (37 percent in a three-mile radius).

Tapestry Lifestyles The trade area‟s Tapestry lifestyles depict an older

consumer with conservative purchasing habits. Many have relocated to the area and are either retired or semi-retired however maintain an active lifestyle. They typically dine at casual restaurants and shop for moderately priced apparel.

Site Characteristics The shopping district of the area is located on Beach Street, both north and south of International Speedway (US Highway 92). Visibility of the existing retail and restaurants is limited from International Speedway, with the exception of those few retailers located at the intersection. Parking in the area is ample for the uses, with spaces provided along Beach Street as well as behind the retail between Beach and Palmetto Streets. Beach Street is easily walkable and well maintained.

The district is currently anchored by Bruce Rossmeyer‟s Daytona

Harley-Davidson, the world‟s largest Harley-Davidson dealer, on the northern end of the district, with municipal uses to the south.

Shopping Center Competition Existing shopping center competition to the study area is found primarily three miles west between the Volusia Mall and Interstate 95. Competition close-in is neighborhood in orientation (west of the Intercoastal Waterway), or appeals to the area‟s tourist base along Atlantic Ocean (east of the waterway).

- END OF DOCUMENT -