Wellgreen Platinum Ltd.

Amended and Restated Annual Information Form

for the Period Ended December 31, 2013

May 9, 2014

Suite 420, 1090 West Georgia Street Vancouver, BC, Canada V6E 3V7 Tel: (604) 569.3690 Fax: (604) 428.7528

Email:

Contents

Important information about this document ... 1

Reporting currency and financial information ... 1

Caution about forward-looking information ... 1

Examples of forward-looking information in this AIF ... 2

Material risks ... 2

Material assumptions ... 2

About Wellgreen Platinum ... 3

Vision and strategy ... 3

Employees ... 3

Principal products ... 3

Platinum market fundamentals and trends ... 4

Palladium market fundamentals and trends ... 8

Market and marketing ... 11

Economic dependence ... 11

Environmental conditions ... 12

Major developments ... 13

Recent developments... 15

How Wellgreen Platinum formed ... 15

Corporate organization chart ... 16

Our projects ... 18

Wellgreen ... 19

Shakespeare ... 38

Risks that can affect our business ... 42

Exploration, development, production and operational risks ... 42

Political risks ... 46 Regulatory risks ... 47 Financial risks ... 48 Environmental risks ... 51 Industry risks ... 52 Other risks ... 53 Legal proceedings... 55 Investor information ... 55 Share capital ... 55 Escrowed securities ... 57 Material contracts ... 57

Market for our securities ... 57

Trading activity ... 57

Governance ... 58

Directors ... 58

Officers ... 59

Important information about this document

This amended and restated annual information form (“AIF”) replaces and supersedes the annual information form of Wellgreen Platinum Ltd. filed on March 31, 2014, and provides important information about the Company. It describes, among other things, our history, our markets, our exploration and development projects, our mineral resources, sustainability, our regulatory environment, the risks we face in our business and the market for our shares. Information on our website is not part of this AIF, nor is it incorporated by reference herein. Our filings on SEDAR are also not part of this AIF, nor are they incorporated by reference herein.

Reporting currency and financial information

Unless we have specified otherwise, all dollar amounts are in Canadian dollars. Any references to US$ mean United States (US) dollars.

On August 1, 2011, we adopted International Financial Reporting Standards (“IFRS”), which have become the generally accepted accounting principles required to be used by most Canadian publicly accountable enterprises, and we have presented financial information in this AIF in accordance with IFRS.

Caution about forward-looking information

Our AIF includes statements and information about our expectations for the future. When we discuss our strategy, business prospects and opportunities, plans and future financial and operating performance, or other things that have not yet taken place, we are making statements considered to be forward-looking information or forward-looking statements under applicable securities laws. We refer to them in this AIF as forward-looking information.

Key things to understand about the forward-looking information in this AIF:

• It typically includes words and phrases about the future, such as believe, estimate, anticipate, expect, plan,

intend, predict, goal, target, forecast, project, scheduled, potential, strategy and proposed (see examples on page 2).

• It is based on a number of material assumptions, including those we have listed below, which may prove to be incorrect.

• Actual results and events may be significantly different from what we currently expect, because of the risks associated with our business. We list a number of these material risks below. We recommend you also review other parts of this AIF, including the section “Risks that can affect our business” starting on page 42, which discuss other material risks that could cause our actual results to differ from current expectations. Forward-looking information is designed to help you understand management’s current views of our near and longer term prospects. It may not be appropriate for other purposes. We will not update or revise this forward-looking information unless we are required to do so by applicable securities laws.

Throughout this document, the terms we, us, our, the Company and Wellgreen Platinum mean Wellgreen Platinum Ltd. and its subsidiaries.

Examples of forward-looking information in this AIF

• statements regarding the permitting, development and production of our Wellgreen property

• statements about completing an updated PEA (as defined below) on our Wellgreen property

• production estimates at our properties

• our expectations regarding our Wellgreen property

• forecasts relating to mining, development and other activities at our operations

• forecasts relating to market developments and trends in global supply and demand for PGM metals

• future royalty and tax payments and rates

• our mineral reserve and resource estimates

Material risks

• exploration, development and production risks

• recent global financial conditions

• commodity price fluctuations

• availability of capital and financing on acceptable terms

• our mineral reserve and resource estimates are not reliable, or we face unexpected or challenging geological, hydrological or mining conditions

• our Wellgreen property development, mining or production plans are delayed or do not succeed

• we cannot obtain or maintain necessary permits or approvals from government authorities

• we are affected by environmental, safety and regulatory risks, including increased regulatory burdens or delays

• there are defects in, or challenges to, title to our properties

• we are unable to enforce our legal rights under our existing agreements, permits or licences, or are subject to litigation or arbitration that has an adverse outcome

• accidents or equipment breakdowns

• cyclical nature of the mining industry

• there are changes to government regulations or policies, including tax and trade laws and policies

• we are adversely affected by changes in foreign currency exchange rates, interest rates or tax rates

• our estimates of production, purchases, costs, decommissioning or reclamation expenses, or our tax expense estimates, prove to be inaccurate

• we are affected by natural phenomena, including inclement weather, fire, flood and earthquakes

• our operations are disrupted due to problems with our own or our customers’ facilities, the unavailability of reagents or equipment,

equipment failure, lack of tailings capacity, labour shortages, ground movements, transportation disruptions or accidents or other exploration and development risks

Material assumptions

• the assumptions regarding market conditions upon which we have based our capital expenditure expectations

• the availability of additional financing on reasonable terms, or at all

• our mineral reserve and resource estimates and the assumptions upon which they are based are reliable

• our expected production levels and production costs

• the success of our Wellgreen property development, mining and production plans

• our expectations regarding spot prices and realized prices for platinum, nickel, copper and other base and precious metals

• production forecasts meeting expectations

• market developments and trends in global supply and demand for PGM metals meeting expectations

• our reclamation expenses

• the geological conditions at our properties

• our ability to comply with current and future environmental, safety and other regulatory requirements, and to obtain and maintain required regulatory approvals

• our operations are not significantly disrupted as a result of natural disasters, governmental or political actions, litigation or arbitration proceedings, the unavailability of reagents, equipment, operating parts and supplies critical to production, equipment failure, labour shortages, ground movements, transportation disruptions or accidents or other exploration and development risks

• our expectations regarding tax rates and payments, foreign currency exchange rates and interest rates

About Wellgreen Platinum

Headquartered in Vancouver, British Columbia, we are an exploration and development company led by an experienced management and technical team, and we are focused on projects with significant platinum group metals (“PGMs”) located in geopolitically stable regions.

We are publicly listed on the TSX Venture Exchange (“TSXV”) under the trading symbol “WG”, and in the U.S. on the OTC-QX under the trading symbol “WGPLF”.

Our management team has a track record of successful large scale project discovery, development, operations and financing,

Wellgreen Platinum Ltd.

(TSX-V: WG; OTC-QX: WGPLF)

Headoffice: Registered&Recordsoffice:

Wellgreen Platinum Ltd. Cassels Brock & Blackwell LLP 420-1090 West Georgia Street 2200 HSBC Building

Vancouver, BC V6E 3V7 885 West Georgia Street

Canada Vancouver, BC V6C 3E8

Telephone: 604.569.3690 Canada

combined with an entrepreneurial and collaborative approach to working with First Nations and communities.

Our flagship project is the Wellgreen PGM-Ni-Cu project located in the Yukon Territory, Canada, the highlights of which include the following:

• Large deposit – our 100% owned Wellgreen property is a significant undeveloped PGM deposit, and one of few outside of southern Africa or Russia.

• Open-pit – the project is amenable to open pit mining with bulk underground extraction potential. • Government support – the project has the support of the Yukon government and the First Nation

groups in the area.

• Accessible – located 30 kilometres from Burwash Landing and 317 kilometres from Whitehorse along the government-maintained paved Alaska Highway. Wellgreen can be reached by an all-weather, 15 kilometre gravel road off the highway. The project has access to all-season, deep sea ports located in Skagway and Haines, Alaska.

• Year-round mining – the project has an alpine climate tempered by west coast climate influences, with minimal rainfall compared to nearby regions, and this allows for year-round mining activity.

Vision and strategy

Our strategy is to advance our Wellgreen property towards production, while continually assessing future acquisitions of mineral properties that are aligned with our business plan and strategies, and that have significant geological and economic potential.

Employees

We employ 15 personnel and utilize consultants and contractors as needed to carry on many of our activities.

Principal products

We are currently in the exploration stage and do not produce, develop or sell mineral products at this time. Our principal focus is on PGMs, which are rare precious metals with unique physical characteristics that are used in

diverse industrial applications and in jewelry. The six PGMs are platinum, palladium, rhodium, ruthenium, iridium and osmium.

The unique characteristics of PGMs include:

• strong catalytic properties;

• excellent conductivity and ductility;

• high level of resistance to corrosion;

• strength and durability; and

• high melting points.

Platinum market fundamentals and trends

Platinum is used in catalytic converters, jewelry, electronics, chemical/petroleum refining and dental and medical applications. Because of low annual production levels and a lack of substitutes in many applications, platinum is a scarce, highly valuable metal. Market fundamentals are positive for platinum as demand for the metal continues to grow while production declines due to supply concentration from high geopolitical risk countries and systemic cost issues. The combination of rising demand and falling production caused the platinum market to fall into a deficit position of 605,000 ounces in 2013, based on estimates from Johnson Matthey PLC’s Platinum 2013 Interim Review.

Platinum supply

Only 179 tonnes (5,740,000 ounces) of platinum were produced in 2013, with approximately 92% of that production originating in South Africa, Russia and Zimbabwe. South African production, which accounted for approximately 72% of 2013 platinum production, has declined by 23% since 2006 due to labour unrest and rising operating costs, especially associated with wages and electricity prices. The CPM Group estimates that PGM cash costs in South Africa have risen at a compounded annual rate of 14.5% since 2000 and labour unions are demanding large wage increases this year. The majority of South African platinum operations are deep underground mines that involve labour-intensive thin-seam mining that cannot be mechanized; in addition, the CPM Group estimates that labour costs comprise approximately 50% of total costs. The potential for labour strikes and other work stoppages may negatively impact South African platinum production. Any shortfalls in South African production are unlikely to be offset by production from Russia or Zimbabwe. Russian platinum production has been declining since 2003 due to lower platinum grades being mined at Norilsk, while Zimbabwe is effectively nationalizing platinum mines by forcing companies to cede a 51% interest to the state empowerment fund.

Secondary supply of platinum from recycling contributed 2,075,000 ounces in 2013, up by approximately 1.7% from 2012 according to Johnson Matthey.

Source: CPM Group Platinum Group Metals Yearbook 2013

Johnson Matthey Platinum 2013 Interim Review estimates

Platinum demand

Platinum demand has risen at a compounded annual rate of approximately 4.1% since 1982, based on data from the CPM Group. Use in autocatalysts continues to be the largest demand source, accounting for approximately 37% of total demand in 2013. Autocatalyst manufacturers have been replacing platinum in catalytic converters with palladium due to its lower cost since 1995 and thrifting has reduced the platinum content per catalytic converter. The majority of catalytic converters for gasoline engines now use palladium, but platinum remains the dominant PGM in catalytic converters for diesel engines because it is less prone to sulphur poisoning and oxidation at low temperatures. However, the CPM Group estimates that palladium now accounts for about one-third of the PGMs loaded on a diesel catalyst, up from only approximately 5% in 2005. This substitution, combined with weak economic conditions in Europe, the largest market for diesel cars, has weighed on platinum demand over the past five years. Some of the demand weakness is expected to be offset by higher platinum demand for heavy duty vehicles,

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Pla

tin

um

(000

oz

)

Russian Pt Production

South African Pt Production

which faced stricter emission standards starting in January 2013. Platinum jewelry is also a source of demand growth due to increasing popularity in China and accounts for approximately 33% of total demand. Another increasingly important source of demand is investment demand, with platinum-backed electronic traded funds now holding 2.7 million ounces of platinum according to Thomson Reuters GFMS.

Johnson Matthey indicates platinum demand exceeded supply by 605koz (>10% of primary supply) in 2013.

Platinum Demand 2013 – Total 8.4Moz

Source: Johnson Matthey Platinum 2013 Interim Review estimates

Autocatalyst demand is expected to rise due to increasing global emission standards and strong auto demand from Brazil, Russia, India and China.

Source: CPM Group

Autocatalyst

37%

Jewellery 33%

Investment

9%

Chemical 6%

Other 5%

Medical &

Biomedicals

3%

Petroleum 2%

Glass 3%

Electrical 2%

Platinum trends

The negative impact of European auto sales on platinum demand is expected to be a temporary phenomenon and it is expected that platinum demand will increase as European economies recover and as substitution of palladium slows due to technological limitations and higher palladium prices.

Note: Supply includes recycling. Source: Johnson Matthey Market Data Table

• Primary platinum supply peaked in 2006 and has been declining at an average rate of

~2.6% per year since

• Platinum demand has been growing at an average rate of

~4.4% per year since 1982

• Substantial supply reduction due to labour strife and high production costs in South Africa moved the platinum market into a deficit equal to ~10% of

mining supply over the course of 2013

Note: Supply includes recycling. Source: Johnson Matthey Market Data Table

Platinum Global Gross Demand (Moz)

As demand grows, platinum markets could continue to face deficit positions as supply will likely continue to be constrained by labour stoppages and a lack of capital reinvestment; at the current price of platinum, approximately 70% of PGM production is failing to recover all-in cash costs according to Thomson Reuters GFMS cost data. New styles of platinum mines in South Africa that have thicker mineralized seams that are amenable to mechanized mining could boost production in the future, but the long-term issues that result from approximately 93% of supply originating from countries with high geopolitical risk will likely not be resolved unless new sources of supply in mining-friendly jurisdictions are developed.

Palladium market fundamentals and trends

Palladium is used in catalytic converters, electronics, chemical/petroleum refining, jewelry and dental and medical applications. Because of low annual production levels and a lack of substitutes in many applications, palladium is a scarce, highly valuable metal. Market fundamentals are positive for palladium as demand for the metal continues to grow while production declines due to supply concentration from high geopolitical risk countries and systemic cost issues. The combination of rising demand and falling production caused the palladium market to fall into a deficit position of 740,000 ounces in 2013, based on estimates from Johnson Matthey.

Palladium supply

Only 200 tonnes (6,430,000 ounces) of platinum were produced in 2013, with approximately 84% of that production originating from Russia, South Africa and Zimbabwe. Palladium supply from Russia, which accounted for approximately 42% of 2013 production according to Johnson Matthey, is comprised of mine production and sales from government stockpiles. Information on Russian government stockpiles is considered a state secret, but a number of palladium industry experts believe that stockpiles are close to being depleted. Russian mine production has also declined in the past decade as palladium grades have decreased at Norilsk. South African palladium production, which accounted for approximately 37% of total 2013 production, is as a by-product of platinum mining. As described earlier, South African platinum mines have faced rapidly rising costs and continue to face labour demands for higher wages. Therefore, palladium production from South Africa is unlikely to experience considerable growth in the near future.

Secondary palladium supply from recycling accounted for 2,460,000 ounces of palladium supply in 2013, up by approximately 7.4% from 2012 according to Johnson Matthey. The increase in recycling supply was attributed to higher palladium prices, indicating that recycling feedstock availability is price sensitive. The compounded annual growth rate in secondary supply since 2000 is approximately 3.1% and supply is expected to continue to increase due to the increasing use of palladium in autocatalysts in the previous decade. However, technological improvements and thrifting of palladium in autocatalysts over the past decade are expected to slow the rate of growth of palladium from recycling in coming years.

Palladium Supply by Region 2013 - Total 6.4Moz

Source: Johnson Matthey Platinum 2013 Interim Review estimates

Palladium demand

Palladium demand has risen at a compounded annual rate of approximately 3.9% since 1982, based on data from the CPM Group. Use in catalytic converters continues to be the largest demand source, accounting for approximately 72% of total demand in 2013. Palladium use in autocatalysts has been a major growth area as manufacturers have tried to substitute lower-priced palladium for platinum wherever possible. The majority of catalytic converters for gasoline engines now use palladium as the primary PGM and it now comprises about one-third the PGM content in a diesel catalytic converter. According to Johnson Matthey, Palladium demand from autocatalysts increased by approximately 3.9% in 2013. Demand growth was driven primarily by the Chinese auto market, due to auto market growth and the use of larger catalysts in anticipation of tightening emission standards. Passenger car sales were up by approximately 14% in 2013 and there is ample room to grow based on the low number of cars per household in China relative to GDP per capita. Emission standards are also being increased, which means that new vehicles will have higher PGM content. China implemented China 4 emission standards (similar to Euro 4 standards) on a nationwide basis in July 2013, while Beijing implemented China 5 emission standards in February 2013.

Johnson Matthey indicates palladium demand exceeded supply by 0.74Moz (approximately 12% of primary supply) in 2013.

Palladium Demand 2013 – Total 9.6Moz

Source: Johnson Matthey Platinum 2013 Interim Review estimates

South

Africa 37%

Russia

42%

Zimbabwe

5%

North

America

14%

Other 2%

Autocatalyst

72%

Electrical 11%

Chemical 6%

Dental 5%

Jewellery 4%

Investment

1%

Other 1%

Autocatalyst demand is expected to rise due to increasing global environmental standards & strong auto demand from Brazil, Russia, India and China (see chart on page 7 of this AIF).

Palladium trends

Strong demand for palladium in autocatalysts is expected to continue as global vehicle sales rise and emission standards become stricter, while supply growth will be negatively impacted by the systemic issues faced by South African platinum mines and declining Russian supply.

Source:Johnson Matthey Market Data Table *Source CPM Platinum Group Metals Yearbook 2012

• Palladium demand has been growing at an average rate of

~5% per year since 1982; up ~16% in 2012

• Primary palladium supply peaked in 2006 and has been declining at an avg. rate of

~3.3% per year since

• Primary palladium supply declined in 2013 by ~2% to the

lowest level in 11 years • ~61% decline in Russia

stockpile sales, along with its primary supply drop, drove global palladium market into a deficit equal to ~12% of mining

supply over the course of 2013

Palladium Global Gross Demand (Moz)

These fundamental trends have caused palladium prices to rise at a faster pace than platinum prices. Currently, the price of palladium is equal to approximately 56% of the price of platinum, which is substantially above the long-term (1968 to 2012) average of approximately 30%. Like platinum, it appears likely that palladium markets are likely to be in deficit until new sources of supply are developed. Given the inelastic nature of autocatalyst demand, new significant sources of supply located in geopolitically safe, mining-friendly jurisdictions should be of greater value to both investors and producers.

Specialized skills and knowledge

All aspects of our business require specialized skills and knowledge. Such skills and knowledge include the areas of geology, drilling, logistical planning and implementation of exploration programs and regulatory, finance and accounting. We rely upon our management, employees and various consultants for such expertise.

Market and marketing

There is a worldwide PGM and base metals market into which we could sell, if and when we reach production, and, as a result, we would not be dependent on a particular purchaser with regard to the sale of any PGMs or base metals that we produce.

Competitive conditions

The mineral exploration and mining industry is very competitive in all phases of exploration, development and production. We compete with other mining companies, some of which have greater financial resources and technical facilities, for the acquisition of mineral tenements, claims, leases and other mineral interests for exploration and development projects. We also compete with other mining companies for investment capital with which to fund such projects and for the recruitment and retention of qualified employees.

Cycles

The mining business is subject to mineral price cycles. The marketability of minerals and mineral concentrates is also affected by worldwide economic cycles. Platinum and palladium markets are affected by demands of the automobile and jewellery industry, and base metals, which typically occur with PGMs, such as nickel and copper, are affected by global economic conditions. Fluctuations in supply and demand in various regions throughout the world are common.

As we do not currently carry on production activities, our ability to fund ongoing exploration is affected by the availability of financing which, in turn, is affected by the strength of the economy and other general economic factors.

Economic dependence

Our business is dependent on the acquisition, exploration, development and operation of mineral properties. We are not dependent on any contract to sell the major part of our products or services or to purchase the major part of our requirements for goods, services or raw materials, or on any franchise or licence or other agreement to use a patent, formula, trade secret, process or trade name upon which our business depends.

Bankruptcy and similar procedures

There are no bankruptcies, receivership or similar proceedings against us, nor are we aware of any such pending or threatened proceedings. We have not commenced any bankruptcy, receivership or similar proceedings during our history.

Foreign operations

We currently hold an interest in certain non-core exploration stage mineral resource properties located in Uruguay. Such properties are exposed to various degrees of political, economic and other risks and uncertainties. See “Risks affecting our business”.

Reorganization

We have not completed any reorganizations, other than the acquisition of Ursa Major Minerals Incorporated (“Ursa”) in July 2012 and the acquisition of 0905144 B.C. Ltd. and the Wellgreen and Lynn Lake properties from Prophecy Coal Corp. (“Prophecy Coal”) in June 2011, as described below in the section “Major Developments”.

Environmental conditions

All aspects of our field operations are subject to national and local environmental regulations and generally require approval by appropriate regulatory authorities prior to commencement. These regulations pertain to construction and operating standards for the sites and include closure plan commitments regarding restoration requirements. Our Wellgreen property has not created significant disturbance and therefore is not considered to be a financial risk to the Company.

The Wellgreen property is currently not permitted for mine construction and will therefore require assessment by the Yukon Environmental and Socio-Economic Assessment Board (“YESAB”) and the Water Use License Board as well as appropriate engagement with the First Nations. These parallel processes could create delays to advancement of the project, as well as potentially create financial burdens; however, an Exploration Cooperation and Benefit Agreement is in place with one of the First Nations groups, the First Nations have provided excellent support for the project, the site is not located on any fish bearing rivers, and the Yukon (where the government licensing and permitting boards have been highly supportive of the Wellgreen property) was ranked 8th in the world based on “Investment Attractiveness” by the Fraser Institute in 2013.

Social or environmental policies

Our executive management team has implemented policies and procedures that provide a safe working environment for all of our employees, consultants, contractors and stakeholders. We recognize that safety and environmental due diligence are significant components that enable long-term sustainability of our operations and support our objective of projects being completed in a cost effective and timely manner with excellent quality control. We have not had any fatal or long-term disability accidents nor significant environmental incidents at any of our projects, and we have only had one lost time accident at our Wellgreen property.

Major developments

2013 ...

2013...

March

• We entered into a contract with JDS Energy & Mining Inc. to manage the Wellgreen Environmental Baseline, Assessment, and Mitigation reviews as well as the Socio Economic component associated with completion of a Project Description that we expect to submit to YESAB Ex Com late 2014.

June

• We completed a private placement raising gross aggregate proceeds of approximately $5.9 million (the “June 2013 Financing”) through the sale of 8,386,264 units, at a price of $0.70 per unit, with each unit comprised of one “flow-through” common share and one common share purchase warrant.

• In connection with the June 2013 Financing, in order to assist our management to build direct equity ownership in the Company and further align the interests of shareholders and management, we advanced short-term loans (the “Loans”) in the aggregate amount of $892,500 to members of our senior management team, as follows: Greg Johnson - $280,000; Jeffrey Mason - $227,500; John Sagman - $227,500; Rob Bruggeman - $70,000; and Samir Patel - $52,500. The Loans were advanced in order to allow the recipients to participate in the June 2013 Financing. The Loans were advanced under amended and restated unit purchase loan agreements, each dated June 20, 2013 (copies of which are available under our SEDAR profile at www.sedar.com). The full amount of each Loan was used by each recipient to subscribe for units under the June 2013 Financing on the same premium to market terms as other investors. The Loans bear interest at the rate prescribed by the Canada Revenue Agency from time to time for corporate taxpayers’ overpaid remittances on Harmonized Sales Tax, and were initially repayable in full (together with any accrued interest) on March 31, 2014 (the “Maturity Date”). Each recipient may prepay his Loan, in whole or in part, at any time prior to the Maturity Date. As general and continuing security for the payment and performance of the obligations owed by each recipient under his Loan Agreement, each has granted a securities pledge agreement in favour of Wellgreen Platinum constituting a first priority encumbrance over all units which the recipient purchased under the June 2013 Financing. The Maturity Date was subsequently extended to December 31, 2014. See “Recent Developments”.

July

• We announced the commencement of our 2013 field program at our Wellgreen property and the comprehensive re-logging and re-sampling of up to 12,000 metres of historic drill cores from across the main Wellgreen deposit, approximately 75% of which had never been previously analyzed.

November

• We announced a significant change to the majority shareholder base of our Company that resulted from the private sale by Prophecy Coal Corp. (“Prophecy Coal”) of a 24% equity interest in Wellgreen Platinum to three separate and independent, long-term financial investors (one of whom was Mr. Ernesto Echavarria, who more than doubled his existing position in Wellgreen Platinum to 17.6%). Following this private transaction, Prophecy Coal reported that its ownership in Wellgreen Platinum had decreased to 4.3% (excluding a lesser number of “held in trust shares” that Prophecy Coal holds in reserve for former option and warrant holders of Prophecy Resource Corp.). See “Investor Information – Escrowed Securities”.

• We announced that Mr. Greg Hall had resigned as a director of Wellgreen Platinum, effective November 17, 2013, and that the Company’s Chief Financial Officer, Mr. Jeffrey R. Mason, had been appointed to the Board of Directors of the Company (the “Board”) as of November 18, 2013 in place of Mr. Greg Hall.

• We announced that the management information circular and related meeting materials had been mailed to our shareholders for the Company’s annual general and special meeting of shareholders to be held on December 17, 2013 (the “2013 AGM”), and that at the 2013 AGM, shareholders would be asked to elect the following five nominated individuals to the Board for the ensuing year: Wesley J. Hall; Greg Johnson, Myron G. Manternach, Jeffrey R. Mason and Mike Sylvestre.

December

• We announced the voting results of Wellgreen Platinum’s 2013 AGM. The five directors of the Company elected at the 2013 AGM were: Wesley J, Hall; Greg Johnson; Myron Manternach; Jeffrey R. Mason; and Mike Sylvestre. Messers John Lee and Harald Batista ceased to be directors of Wellgreen Platinum immediately after the conclusion of the 2013 AGM. Shareholder participation at the 2013 AGM was very strong, with approximately 65% of our outstanding common shares having been voted at the meeting. The business items of setting the size of the Board at five, voting for each of the management-nominated directors and the appointment of the Company’s auditor were all approved by over 99% of votes cast, while the share-based compensation plan was approved by approximately 80% of votes cast by disinterested shareholders. Following the 2013 AGM, the Board appointed Mike Sylvestre as Chairman of the Board.

• We announced that the Company had changed its name from “Prophecy Platinum Corp.” to “Wellgreen Platinum Ltd.”, and that it had changed its trading symbols to “WG” on the TSXV and “WGPLF” on the US OTC-QX market, with all changes effective as of December 19, 2013.

• We announced that Wellgreen Platinum had changed its financial year end from March 31 to December 31 to allow the Company to provide continuous disclosure information on a comparable basis with its industry peer group, and that the Company had filed a Notice of Change in Year End under its SEDAR profile at www.sedar.com.

• We completed a private placement raising gross aggregate proceeds of approximately $1.93 million (the “December 2013 Financing”) through the sale of 3,521,339 units, at a price of $0.55 per unit, with each unit comprised of one common share and one common share purchase warrant.

Major developments (continued)

2012 ...

2012...

January

• During the 12 months of production ending January 31, 2012, the Shakespeare property delivered 151,910 (2011: 166,913) tonnes of ore to the Strathcona Mill for processing. Contained metals in the delivered ore totaled

approximately 1,052,000 pounds of nickel (2011: 1,314,000), 1,234,000 pounds of copper (2011: 1,499,000), 64,700 pounds of cobalt (2011: 92,204) and 1,650 ounces of platinum (2011: 1,900), 1,840 ounces of palladium (2011: 2,100), 960 ounces of gold (2011: 1,100) and 10,260 ounces of silver (2011: 12,100). The recovered and contained metals are subject to smelter recoveries and to further smelter deductions. For the 12 production months ended January 31, 2012, the ore averaged 0.314% nickel (2011: 0.357%), 0.368% copper (2011: 0.0407%), 0.019% cobalt (2011: 0.025%), and 0.941 gram/tonne precious metals (2011: 0.989). This is approximately 84% of the average budgeted grade for 2011 that is based on the previous mined grades 0.373% nickel, 0.419% copper, 0.027% cobalt and 1.069 grams/tonne precious metals.

February

• Operations at the Shakespeare property were suspended due to low metal prices.

March

• We acquired 16,666,667 common shares of Ursa at a price of $0.06 per share for aggregate gross proceeds of $1,000,000.

• We changed our year end from July 31 to March 31.

June

• On June 18th, we announced the results of an NI 43-101 compliant preliminary

economic assessment (the “2012 Wellgreen PEA”), prepared by Tetra Tech WEI Inc. (“Tetra Tech”) for the Wellgreen property.

July

• Pursuant to an arrangement agreement dated April 13, 2012 (a copy of which is available under our SEDAR profile at www.sedar.com), we acquired all of the issued and outstanding securities of Ursa under a court-approved statutory plan of arrangement. As a result, Ursa became a wholly-owned subsidiary of Wellgreen Platinum. We filed a business acquisition report dated July 24, 2012 in connection with this acquisition, and it is available under our SEDAR profile at www.sedar.com).

• We completed a private placement raising gross aggregate proceeds of $7,251,749.35 through the sale of 807,655 flow through common shares at a price of $1.45 per flow through common share and 5,067,208 units at a price of $1.20 per unit.

• We reported additional information including base cash metals pricing assumptions in connection with the 2012 Wellgreen PEA.

August

• We concluded our cooperation and benefits agreement with the Kluane First Nation to support our exploration program and environmental studies for the development of the Wellgreen property.

• We filed the 2012 Wellgreen PEA and announced the results of ongoing metallurgical testing for the Wellgreen property.

• We announced the appointment of Mr. Rob Bruggeman as Vice President Corporate Development.

• We completed a private placement of 2,500,000 million units at a price of $1.20 per unit for total gross proceeds of $3 million.

September

• We issued 83,333 common shares to Kluane First Nation at an ascribed value equal to the market price of $1.55 per share.

• We announced an updated mineral resource estimate report for the Shakespeare PGM-Ni-Cu deposit that we acquired through our acquisition of Ursa.

October

• We entered into a contract with EBA Engineering Consultants Ltd. (“EBA”), a Tetra Tech company, to initiate environmental baseline studies on the Wellgreen property.

November

• We appointed the following individuals to our management team: Greg Johnson (President and Chief Executive Officer), Jeffrey Mason (Chief Financial Officer), John Sagman (Senior Vice President and Chief Operating Officer) and Samir Patel (Corporate Counsel and Corporate Secretary).

• We terminated our option agreement with Marifil Mines Ltd. on the Las Aguilas Property in Argentina and wrote off our investment of $460,844.

December

• We completed a private placement raising gross aggregate proceeds of approximately $1.24 million through the sale of 1,135,635 flow through common shares at a price of $1.10 per flow through common share.

2011...

January

• We completed a private placement raising gross aggregate proceeds of $1,050,000 through the sale of 15,000,000 pre-consolidation units at a price of $0.07 per unit.

June

• Pursuant to an arrangement agreement dated March 30, 2011 (a copy of which is available under our SEDAR profile at

www.sedar.com), we completed the acquisition from Prophecy Coal of all of the issued and outstanding shares of 0905144 B.C. Ltd, which held $2,000,000 in cash, the Wellgreen Property and the Lynn Lake property, in consideration of the issuance of 45,000,000 post consolidation common shares. Prophecy Coal retained 22,500,000 post consolidation common shares and distributed the balance to its securityholders pursuant to a plan of arrangement. Immediately thereafter, we completed a consolidation of our share capital on a 10 old for 1 new basis.

August

• On August 30, 2011, we entered into a formal purchase agreement with Strategic Metals Ltd., dated August 4, 2011 concerning the transaction and completed the purchase of the Burwash property in exchange for the payment of $1,000,000 in cash.

November

• We completed a private placement raising aggregate gross proceeds of $10,015,620 through the sale of 3,709,489 common shares.

Recent developments

Subsequent to the end of our most recently completed financial year, on January 9, 2014, we completed a second tranche private placement under the same terms as our December 2013 Financing for total proceeds from the two tranches of approximately $2.6 million. The second tranche of this financing raised aggregate gross proceeds of approximately $660,000 (the “January 2014 Financing”) through the sale of 1,199,700 units, at a price of $0.55 per unit, with each unit comprised of one common share and one common share purchase warrant. Each warrant is exercisable for one common share of Wellgreen Platinum for a period of 36 months following the closing of the January 2014 Financing, at a price of $0.80, subject to the Company’s right to accelerate the expiry date of the warrants to a period of 30 days if, at any time after May 10, 2014, the closing price of Wellgreen Platinum’s common shares on the TSXV equals or exceeds $1.20 for a period of 10 consecutive trading days. In connection with the January 2014 Financing, the Company paid cash finder’s fees to certain finders in an aggregate amount of approximately $12,000.

On February 19, 2014, Victory Nickel provided the Company with a termination notice in connection with the option agreement concerning the Lynn Lake property, and as the Company had determined that the Lynn Lake property did not align with its strategic objectives, the Lynn Lake property was returned to Victory Nickel.

On February 24, 2014, we announced the completion of a detailed review of historical options that were granted to various persons on June 17, 2011 (the “June 2011 Options”) at an exercise price of $0.90. The review was conducted in keeping with our on-going commitment to strong corporate governance, and as a result of this review, we amended the price of 4,529,285 of the June 2011 Options to $0.91 (with the amendment to 2,309,285 of these options being subject to regulatory approval). Most of these options will expire by May 26, 2014. The review also resulted in the cancellation of 670,715 of the June 2011 Options (subject to regulatory approval).

In the first few weeks of March 2014, certain holders exercised some or all of their warrants (at exercise prices of $0.80 or $0.90, respectively), which resulted in approximately $1 million coming in to the Company through warrant exercise proceeds.

On March 28, 2014, the Company extended the Maturity Date of the Loans to December 31, 2014, with all other terms of the Loans remaining unchanged. On March 28, 2014, the Company also applied to the TSXV to amend the expiry date of an aggregate of 3,783,604 warrants. Subject to approval of the TSXV, the terms of the warrants will be extended to September 29, 2016, with all other terms of the warrants remaining unchanged.

In April 2014, we determined that the January 2006 feasibility study (“2006 Feasibility Study”) in respect of the Shakespeare property, and the information contained therein with respect to mineral reserve estimates, is no longer valid, because the operating and capital expenditures estimated in the 2006 Feasibility Study are outdated and no longer reliable. Accordingly, we have retracted the 2006 Feasibility Study and confirm that the Shakespeare property does not currently contain any mineral reserves, as such term is defined for the purposes of NI 43-101.

How Wellgreen Platinum formed

Our Company was incorporated under the Business Corporations Act (British Columbia) (the “BCBCA”) on April 5, 2006 under the name “Fargo Capital Corp.”, which changed its name to “Pacific Coast Nickel Corp.” on July 10, 2007. Following the June 2011 spin-out transaction involving Prophecy Coal Corp. and Pacific Coast Nickel Corp. (details of which are available under our SEDAR profile at www.sedar.com), the latter changed its name to Prophecy Platinum Corp. on June 13, 2011. The Company’s name was changed to Wellgreen Platinum Ltd. effective December 19, 2013.

We are a reporting issuer in the provinces of British Columbia (principal reporting jurisdiction), Alberta, Manitoba and Ontario, and we currently have the following five wholly-owned subsidiaries:

• 0905144 B.C. Ltd., a company incorporated under the BCBCA

• PCNC Holdings Inc., a company incorporated under the BCBCA

• Ursa Major Minerals Incorporated, a company incorporated under the Business Corporations Act

(Ontario)

• Pacific Coast Nickel Group, USA, a company incorporated under the laws of the State of Nevada

• Pacific Nickel Sudamerica S.A., a company incorporated in Uruguay

As of December 31, 2013, Wellgreen Platinum’s only material subsidiary is 0905144 B.C. Ltd.

Corporate organization chart

The following diagram shows our corporate structure:

We hold our mineral properties either directly or through the following subsidiaries:

• Wellgreen Platinum Ltd. - 100% interest in the Burwash nickel project located in the Yukon Territory, Canada

(the “Burwash property”).

• 0905144 B.C. Ltd. - 100% interest in the Wellgreen PGM-Ni-Cu project located in the Yukon Territory

(the “Wellgreen property”).

- interests in certain other exploration properties in British Columbia, Canada.

Prophec Platinum Corp. (1)

(British Columbia) Wellgreen Platinum Ltd.

(British Columbia) (100%) (100%) (100%) (100%) (100%) Ursa Major Minerals Incorporated. (Ontario) Pacific Coast Nickel Group, USA. (Nevada) Pacific Nickel Sudamerica S.A.(Uruguay) PCNC Holdings Inc. (British Columbia) 0905144 B.C. Ltd. (British Columbia) For more information

You can find more information about Wellgreen Platinum on SEDAR (sedar.com), and on our website (www.wellgreenplatinum.com).

See our most recent management proxy circular dated November 18, 2013 for additional information, including how our directors and officers are compensated and any loans to them, principal holders of our securities, and securities authorized for issuance under our equity compensation plans.

See our audited consolidated financial statements and

management’s discussion and analysis for the financial year ended December 31, 2013 for additional financial information.

• Ursa Major Minerals Incorporated

- 100% interest in the Shakespeare PGM-Ni-Cu project located in Ontario, Canada

(the “Shakespeare property”), which is subject to a 1.5% net smelter royalty. - 100% interest in the Shining Tree Ni-Cu exploration property located in

Ontario

(the “Shining Tree property”), which is subject to a 1% net smelter royalty, as well as interests in certain other exploration properties in Ontario.

Our projects

We have interests in mineral properties located in Canada and Uruguay. As at December 31, 2013, these properties were carried on our balance sheet as assets with a book value of approximately $40 million. The book value consists of acquisition costs plus cumulative expenditures on properties for which the Company has future exploration plans. The current book value is not necessarily the same as the total expenditures on each property by the Company, as part of the expenditures on some properties have been written down. The book value is also not necessarily the fair market value of the properties.

Our projects are set out below. Management of the Company considers the Wellgreen property to be our only material property for the purposes of National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and other applicable securities laws.

Wellgreen (Yukon)……….19 Shakespeare (Ontario)………..…….38 Other properties in the district

Shining Tree………40 Fox Mountain……….………..………41

Wellgreen

Our main project is our 100%-owned Wellgreen PGM-Ni-Cu project located in the Yukon Territory, Canada.

The Wellgreen property is a significant undeveloped PGM deposit, and one of few outside of southern Africa or Russia. It has an exploration and production history dating back to its discovery in 1952. The project is located 30 kilometres from Burwash Landing and approximately 317 kilometres northwest of Whitehorse in southwestern Yukon, and can be accessed from the paved Alaska Highway by a 15 kilometre gravel road.

In 2012, we retained Tetra Tech to prepare a preliminary economic assessment on the Wellgreen property entitled “Wellgreen Project Preliminary Economic Assessment, Yukon, Canada” and dated August 1, 2012 (defined above as the “2012 Wellgreen PEA”). This project description is based on the 2012 Wellgreen PEA except for some updates that reflect certain developments since that report was published. The 2012 Wellgreen PEA was prepared for us in accordance with NI

43-101, by or under the supervision of the following four qualified persons within the meaning of NI 43-101:

• Andrew Carter, Eur. Ing., C.Eng., MIMMM, MSAIMM, SME (Director of Metallurgy, Tetra Tech)

• Todd McCracken, P.Geo. (Principal Geologist, Tetra Tech)

• Pacifico Corpuz, P.Eng. (Senior Mining Engineer, Tetra Tech)

• Philip Bridson, P.Eng. (Senior Mining Engineer, Tetra Tech)

The conclusions, projections and estimates included in this description are subject to the qualifications, assumptions and exclusions set out in the 2012 Wellgreen PEA, except as such qualifications, assumptions and exclusions may be modified in this AIF. We recommend you read the 2012 Wellgreen PEA in its entirety to fully understand the Wellgreen property. You can obtain a copy of the report under our SEDAR profile at www.sedar.com. Readers should note that the 2012 Wellgreen PEA is preliminary in nature, in that it includes inferred mineral resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the estimates contained in the 2012 Wellgreen PEA will be realized. A mineral reserve has not been estimated for the project as part of the 2012 Wellgreen PEA. A mineral reserve is the economically mineable part of a measured or indicated mineral resource demonstrated by at least a pre-feasibility study. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

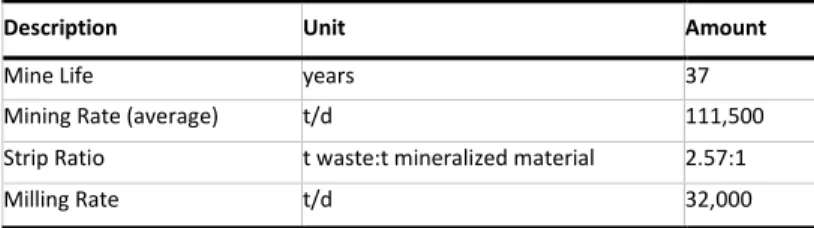

General project information

Location Approximately 317 kilometres northwest of Whitehorse in the Yukon Territory, Canada

Ownership 100%-owned by our wholly-owned subsidiary, 0905144 B.C. Ltd.

End product platinum group metals, nickel and copper concentrates

Mine type open pit and amenable to selective underground

Estimated mineral resources

(measured + indicated) 14.4 Mt

Estimated mineral resources (inferred) 446.6 Mt

Estimated mine life 37 years

Initial Capital US$863.1 million

Pre-tax NPV (8%)*

US$1.268 billion

Based on base case – 20% scenario from the 2012 Wellgreen PEA at US$1,270.38/oz Pt; US$465.02/oz Pd; US$1,102.30/oz Au; US$7.58/lb Ni; US$2.85/lb Cu; and US$12.98/lb Co

Taxation

The 2012 Wellgreen PEA did not include an after-tax analysis. Generally speaking, applicable taxes for mining in the Yukon Territory currently include a 15% federal income tax rate and a 15% territorial income tax rate. Under the Quartz Mining Act, a royalty of up to 12% of profits from mining may also be payable to the Yukon government. Generally speaking, income taxes are applicable to pre-tax cash flow from operations less royalties, capital cost allowance, interest expenses, non-capital carry forward losses and Canadian exploration expenses and Canadian development expenses. Generally speaking, royalties are based on profits minus a number of deductions, including development allowance, depreciation allowance, community and economic development expense allowance, plus other incentives for mining exploration activity.

* Readers should note that the 2012 Wellgreen PEA is preliminary in nature, in that it includes inferred mineral resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the estimates contained in the 2012 Wellgreen PEA will be realized. A mineral reserve has not been estimated for the project as part of the 2012 Wellgreen PEA. A mineral reserve is the economically mineable part of a measured or indicated mineral resource demonstrated by at least a pre-feasibility study. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

About the Wellgreen property

Property descriptionThe Wellgreen property is located approximately 317 km northwest of Whitehorse in southwestern Yukon, at approximate latitude 61°28’N, longitude 139°32’W onNational Topography System map sheet 115G/05 and 115G/06.

Mineral claims, leases and Quartz Mining Leases

In the Yukon, all hard rock mining claims (excluding coal) are administered through the Quartz Mining Act (“QMA”). A mining claim gives the holder of the claims the right to perform exploration work. It provides exclusive rights to the holder of the claim for the mines and minerals located within the area of that claim. The QMA also issues a Quartz Mining License (Class 1 to Class 5) that confirms that a claim holder has the following rights in relation to the minerals contained within the claim: the right to enter on and use and occupy the surface for the efficient and miner-like operation of mines and minerals; and the right to commercially produce a mineral and benefit from the sale of the mineral. Claims must be renewed on an annual basis by filing approved assessment work to a value of Cdn$100 per claim. A Quartz Mining Lease provides the leaseholder with the ability to hold claims for 21 years and can be renewed for an additional 21 year term, provided that during the original term of the lease, all conditions of the lease and provisions of the legislation have been adhered to. Annual rental fees are required to keep a Quartz Mining Lease in good standing. As at the date hereof, we hold 260 mineral claims, totaling 5,434 hectares, and 91 Quartz Mining Leases totaling 1,902 hectares, surrounding the Wellgreen deposit. We have title to all of these claims and leases ranging from 2015 to 2032.

Our interest in the Wellgreen property also includes one surface lease issued by the Government of Canada and administered by the Yukon Government (lease 115G05-001). The lease covers a 69.754 hectare parcel of land located at approximately Mile 1111 of the Alaska Highway (the “Mine Site”). Various operators have conducted historical exploration activities on this parcel of land since the 1950s, and exploration activities were carried out by Northern Platinum from approximately the early 1990s until October 31, 2011. Prior to expiration, Prophecy Coal took an assignment from Northern Platinum of the Mine Site, and the lease was subsequently assigned to us, and we then applied for renewal of the lease. Subsequent to the date of the 2012 Wellgreen PEA, the renewal of the lease was approved; the lease expires on May 31, 2034.

In addition, we also occupy a 62.56 hectare parcel of land located approximately 1 kilometre from the Mine Site and adjacent to the Alaska Highway (the “Mill Site”) under lease 115G11-003. Northern Platinum Ltd. (“Northern Platinum”) held a leasehold interest in this parcel from approximately the late 1990s until October 31, 2011. Prior to expiration, Prophecy Coal took an assignment from Northern Platinum, and it was subsequently transferred to us. As at the date of the 2012 Wellgreen PEA, Wellgreen Platinum was working with the Government of Yukon toward concluding a lease agreement by which it would obtain a leasehold interest in a portion of the Mill Site, excluding the Historical Liabilities (defined in the section “Environmental Liabilities” below), which relate to a historical tailings impoundment. Subsequent to the date of the 2012 Wellgreen PEA, a new lease agreement relating to 115G11-003 was reviewed with the Yukon Government and approved on November 1, 2012; the lease expires on November 1, 2022. This lease refers to a portion of the Mill Site, which excludes the tailings impoundment area containing the Historic Liabilities.

All permits and licenses to conduct exploration work on the Wellgreen property are in place. Accessibility

The Wellgreen property can be reached from the Alaska Highway (a paved all-weather highway maintained by the Government of Yukon) by gravel road which runs south-west beside Quill Creek for a distance of 14 kilometres. There is an all-weather airstrip which can support large aircraft maintained by NAV CANADA located 30 kilometres southeast of the property at Burwash Landing. There are two all-season, deep sea ports that are accessible by paved highway located in Skagway, Alaska and Haines, Alaska, approximately 400 kilometres to the southeast of the Wellgreen property.

Climate

The climate is alpine but tempered by west coast climate influences. Despite lengthy winter seasons, temperatures are less extreme than areas further east. The daily average temperature at the Burwash Landing station is -22°C in January and 12.8°C in July. Average annual precipitation for the Burwash Landing station is 279.7 millimetres, of which 192 millimetres falls as rain with 106.4 centimetres as snow.

Infrastructure

The Wellgreen open pit area is located approximately 14 kilometres from the paved Alaska Highway and is accessible by a gravel road. A process plant location has been proposed along the access road, with the Wellgreen deposit open pit further up the same access road.

A water supply, adequate for drilling operations, can be pumped from local creeks. Non-potable water was supplied for the camp from Nickel Creek, which flows past the portal to the underground workings. All local creeks freeze solid during the winter months. In order to maintain a year round camp or mining operation, drilling of water wells will be required.

In the 2012 Wellgreen PEA, the processing plant, primary crusher, ancillary buildings, power plant and permanent camp are located within the process plant area. A combined heat & power plant with low speed engine generator sets (6x10 MW) operating at 13.8 kV, 60 Hz output voltage, has been considered by us to meet the project’s power demands. The 2012 Wellgreen PEA assumed that the fuel supply would be diesel, delivered by truck to the power plant.

The tailings pond proposed in the 2012 Wellgreen PEA would be constructed of compacted rock fill using the downstream method with a geomembrane liner on the upstream face. The tailings impoundment footprint as proposed would be lined with a low density polyethylene liner over a layer of broadly graded silty sand and gravel, acting as low permeability bedding material and providing secondary containment. Figure 1.2 illustrates the overall site plan for the Wellgreen property, as outlined in the 2012 Wellgreen PEA.

Power on the Wellgreen property is currently supplied by generators installed for the exploration programs. Skilled labour and equipment is available in the city of Whitehorse and the small village of Haines Junction. The villages of Burwash Landing and Destruction Bay, located 15 and 30 kilometres southeast from the Wellgreen turn-off, respectively, from the Wellgreen property, can provide labour, basic food, fuel and lodgings if necessary.

Topography, elevation and vegetation

The Wellgreen property is located in the Kluane Ranges, which are a continuous chain of foothills situated along the eastern flank of the Saint Elias Mountains. The topography across the Wellgreen property has typical slopes in the 250 to 300 m range, and the highest peaks are at an approximate elevation of 1,800 m.

Vegetation consists of typical alpine grasses and wildflowers on the hill sides, along with a mixture of pine, spruce and poplar trees located in the lower elevations and creek beds.

History

As depicted on the table below, numerous operators have worked on the Wellgreen property since its initial discovery in 1952. Completed work includes 183 diamond surface drill holes, underground development and 519 underground diamond drill holes, together with mapping, trenching and geophysics. The majority of historical work at the Wellgreen property focused on the property’s East Zone, which has underground development on six levels.

1952 • Wellington Green, C. Aird and C. Hankins discover surface showings

• Property optioned from prospectors by Hudson Bay Exploration & Development (“HBE&D”), a subsidiary of Hudson Bay Mining & Smelting Co (“HBM&S”)

• Ownership transferred from HBE&D to another subsidiary of HBM&S, Yukon Mining Company (“YukonMining”)

• Yukon Mining completes 45,500 metres of surface drilling

1953-1954 • Yukon Mining completes 118,100 metres of surface drilling

1955 • Ownership transferred from Yukon Mining to another subsidiary of HBM&S, Hudson Yukon Mining Company (“Hudson Yukon Mining”)

• Hudson Yukon Mining completes 32,400 metres of surface drilling

1953-1956 • Yukon Mining/Hudson Yukon Mining completes 4,267 metres of underground development on 7 levels and 2 internal shafts

• Yukon Mining/Hudson Yukon Mining completes metallurgical test work, including a pilot plant

• Yukon Mining/Hudson Yukon Mining completes historical mineralized material reserves estimate of 500,000 t @ 1.34% copper and 2.14% nickel

1956-1967 • Idle

1968 • Hudson Yukon Mining carries out ground geophysics work (magnetics and electromagnetics) and a soil survey

• Hudson Yukon Mining completes 762 metres of surface drilling

1966-1970 • Hudson Yukon Mining completes metallurgical work at Lakefield Research Ltd., HBM&S, Lurgi-Frankfurt and Sumitomo

1969 • Hudson Yukon Mining completes feasibility study with historical “Proven Reserves” estimated at 669,150 t @2.04% Cu, 1.42% Ni, 0.073% Co, 1.30 g/t Pt, 0.93 g/t Pd and 0.17 g/t Au

1970 • Hudson Yukon Mining places property into production, with concentrate to be shipped to Sumitomo in Japan

• Development consists of slashing out exploration drifts, development of sub-levels, construction of mine dry, powerhouse, and compressor facility

• Mill with 600 t/d concentrator and town site established 11.5 kilometres from mine, adjacent to the Alaska Highway

1972 • On site milling commences

1973 • Hudson Yukon Mining suspends milling due to falling metal prices, excessive dilution and unexpected distribution of massive sulphide lenses

and 200 ppb Re

• Hudson Yukon Mining dismantles mine and mill and ships all equipment to Snow Lake, Manitoba

1981 • Foothills Pipelines leases mill site and town site

1986 • International All-North Resources Ltd (“All-North”)/Chevron granted an option to earn 50% of the Wellgreen property from Hudson Yukon Mining

1987 • Galactic Resources purchases 100% interest in Hudson Yukon Mining from HBM&S

• Galactic Resources acquires All-North as a wholly-owned subsidiary

• Transfer of title of the Hudson Yukon Wellgreen to All-North. Resulting Wellgreen ownership consists of: All-North 75%/Chevron 25%

• All-North and Galactic Resources conduct 1:2,500 geological mapping 50 m x 100 m spaced, soil sampling 100 m x 20 m spaced, very low frequency (VLF)-electromagnetic and magnetic survey, 10,000 cubic metres of bulldozer trenching and 45 diamond drill holes totalling 4,932 metres

• Joint venture formed between All-North, Chevron Minerals, Pak-Man Resources and Rockridge Mining (“Kluane JV”) to explore on the Arch Joint Venture Claims. Operated by Archer Cathro

• Kluane JV completes 1:10,000 geological mapping and sampling, VLF and magnetic survey, 50 h bulldozer trenching

1988 • Kluane JV carries out bulldozer trenching, and completes three diamond drill holes totaling 173.5 metres

• All-North /Chevron complete 5,500 metres of diamond drilling in 34 holes underground

• 4250 level is rehabilitated

• 6,073 metres of surface diamond drilling in 37 holes completed

• Klohn Leonoff carried out preliminary engineering surveys to evaluate mill and tailings disposal sites

• Norecol carried out preliminary environmental survey including water quality and wildlife study

1989 • All-North acquires Chevron’s interest in the Arch Joint Venture and the Wellgreen property

• Watts Griffis & McOuot (“WGM”)completes a historical reserve estimate for both the East and West Zones

• Metallurgical studies conducted at SGS Lakefield, Inco Tech, and CANMET

• Pre-feasibility completed by WGM

1993 • Galactic Resources files for bankruptcy in Canada

1994 • Northern Platinum signs option agreement with All-North to earn 80% interest in the Wellgreen property, with a 50% back-in right to J. Patrick Sheridan

1996 • Northern Platinum drills 57 4.5’’ rotary percussion drill holes totaling 3,900 metres

1999 • Northern Platinum agrees to purchase the remaining interest (20%) of the Wellgreen property from All-North

2001 • Northern Platinum surface drill program discovers the North Shear Zone, located 500 metres north of the Wellgreen deposit

2005 • Coronation Minerals Inc. (“Coronation Minerals”) entered option agreement with Northern Platinum to earn 100% of the Wellgreen property for $25 million

2006 • Coronation Minerals drills 11 diamond drill holes totaling 2,016 metres

2007 • Coronation Minerals drills three underground diamond drill holes totaling 577 metres

2008 • Coronation Minerals drills 13 diamond drill holes totaling 4,654 metres, and completes 854 line kilometres of helicopter-borne aeromagnetic survey

• NI 43-101 report completed by WGM

• Coronation Minerals drops option, returns Wellgreen property to Northern Platinum

2009 • Northern Platinum drills 10 diamond drill holes totaling 2,058 metres

2010 • Northern Platinum drills six diamond drill holes totaling 2,138 metres

• Prophecy Resources Corp. acquires Northern Platinum and completes one diamond drill hole totaling 117 metres

Historical estimates shown in the table above are considered relevant but not reliable. A qualified person (as defined under NI 43-101) has not done sufficient work to classify the historical estimate as a current mineral resource or mineral reserve. We are not treating the historical estimates as current mineral resources or mineral reserves and the historical estimates should not be relied upon.