Munich Personal RePEc Archive

Billionaires, millionaires, inequality, and

happiness

Popov, Vladimir

21 May 2019

1

Billionaires, millionaires, inequality, and happiness1

Vladimir Popov2 Abstract

The relationship between inequality and happiness is counterintuitive. This applies to both

inequality in income and wealth distribution overall and also inequality at the very top of the wealth

pyramid, as measured by billionaire intensity (the ratio of billionaire wealth to GDP). First,

billionaire intensity appears to be higher in countries with low, not high, levels of income

inequality. Second, happiness indices are higher in countries with high percentages of billionaire

and millionaire wealth as a proportion of GDP, but with low levels of income inequality.

This paper uses databases from the Forbes billionaires list, the Global Wealth Report (GWR), and

the World Happiness Report, as well as from the World Database on Happiness. Using these

datasets, I examine the relationship between income inequality and happiness for over 200

countries from 2000 to 2018.

It turns out that in relatively poor countries – below $20,000-$30,000 per capita income – inequality raises happiness rather than lowers it, but inequality has a negative impact on happiness

in rich countries. A certain degree of inequality of wealth and income distribution has a positive

impact on happiness feelings, especially in countries with low levels of income. Furthermore,

wealth inequalities, and especially the degree of concentration of wealth at the very top of the

wealth pyramid, raise happiness self-evaluations even when income inequalities lower it.

Keywords: inequality in income and wealth distribution, share of billionaires’ and millionaires’

wealth in GDP, happiness indices

JEL: D31, D63, I31

1This paper is the logical continuation of my two 2018 papers ‘Paradoxes of happiness. Why do people feel more

comfortable with high levels of inequality and high murder rates?’ DOC Expert Comment, 18 June 2018and ‘Why do some countries have more billionaires than others? Explaining variations in the billionaire-intensity of GDP’. DOC Expert Comment, 24 July 2018.

2 Dialogue of Civilizations Research Institute, Berlin, Germany. My thanks go to Tony Shorrocks who kindly

2

Billionaires, millionaires, inequality, and happiness3

Vladimir Popov4 Literature review, puzzles, and hypotheses

There are some important paradoxes in the dynamics of happiness indices and the relative levels

of these indices for various countries and different populations groups. One puzzle, the Easterlin

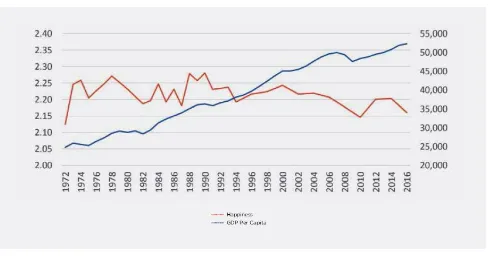

paradox, is the non-increasing level of happiness in the US in spite of constantly rising personal

[image:3.612.74.563.293.551.2]incomes (fig. 1).5

Figure 1: Average happiness score (left scale) and GDP per capita, dollars, (right scale) in the US in 1972- 2016

Source: Sachs (2018).

3This paper is the logical continuation of my two 2018 papers ‘Paradoxes of happiness. Why do people feel more

comfortable with high levels of inequality and high murder rates?’ DOC Expert Comment, 18 June 2018and ‘Why do some countries have more billionaires than others? Explaining variations in the billionaire-intensity of GDP’. DOC Expert Comment, 24 July 2018.

4 Dialogue of Civilizations Research Institute, Berlin, Germany. My thanks go to Tony Shorrocks who kindly

provided me with the excel table of the GWR database. I am also most grateful to Elena Sulimova for collecting the data and preparing the database for the analysis and to Jonathan Grayson for editing.

3

Sachs (2018) argues that America’s subjective wellbeing is being systematically undermined by three interrelated epidemics, notably obesity, substance abuse (especially opioid addiction), and

depression. But in other countries without as much obesity, drugs, and depression, there is also a

decline in happiness that goes hand in hand with rising real incomes.

In India, the happiness index score fell from 5 to 4 over the 2006-18 period despite strong growth of income in this period. In China, over the 1990–2000 decade, happiness plummeted despite massive improvements in material living standards. Brockmann, Delhey, Welzel, and Hao (2008)

explain this by growing income inequality within China, i.e., in relation to the average national

income, the financial position of most Chinese people deteriorated.

Similarly, in the US the recent increase in income inequalities could be responsible for the decline

in happiness: in 1980-2014, the post-tax incomes of the richest 10% rose by 113%; of the top 1%,

by 194%; and of the top 0.001%, by 617% (Piketty, Saez, Zucman, 2016), whereas the US

happiness index score over this period fell. However, the relationship between inequality and

happiness is also not straightforward and presents another puzzle.

Normally we assume that greater equality –‘inclusive development that leaves no one behind’ – is both morally just and desirable for the creation of happy societies. But there is evidence that

income and wealth inequalities are positively associated with happiness, as measured by the

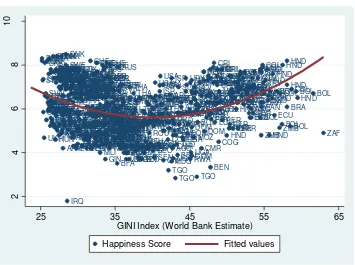

happiness index, at least for a group of countries. There are some poorer countries with high

income inequalities – Bolivia, Honduras, Colombia, Ecuador, Costa Rica and some other Latin American countries – and yet also with very high happiness index scores (fig. 2). It may well be that a certain degree of inequality is necessary to keep alive a kind of ‘American dream’: a future-oriented belief in getting rich and achieving success in life.

Alesina, Di Tella, and MacCulloch (2001) showed that there is a large, negative, and significant

4

mobility. People who believe that American society offers equal opportunities to all are more

averse to redistribution in the face of increased mobility.

On the other hand, those who see the social rat race as a biased process do not see social mobility

as an alternative to redistributive policies. Alesina and Giuliano (2009) presented evidence that

individuals who believe other people try to take advantage of them rather than being fair have a

strong desire for redistribution; similarly, believing that luck is more important than work as a

driver of success is strongly associated with a taste for redistribution.

Inequality at the very top does not seem to lead to pressure for redistribution. In Victorian England,

inequality within the elite was associated with more conditionality and less generous welfare

expenditure. Removing institutional advantages that benefited the elite did not appear to reduce

the effect of elite inequality, which suggests results cannot be explained by a classic median voter

model (Chapman, 2018).6 Therefore, an increase in inequality at the very top may be self-perpetuating; there is no pressure to redistribute and no mechanism to automatically ‘correct’ the inequality.

6This model predicts that in a majority-rule voting system, the outcome selected at the polls will be the one

5

Figure 2: Happiness index (Word Happiness Report and World Database on Happiness), 0-to-10 scale; and GINI coefficient of income inequality in percentage terms, 2000-18

Source: World Database on Happiness (2019); WDI.

There is also some evidence that happiness is positively correlated with murder rates, especially

when this goes hand in hand with inequalities (Popov, 2018a; 2018b). Inequalities lead to higher

murder rates, but this does not lead to a decline in happiness, at least up to a certain point.

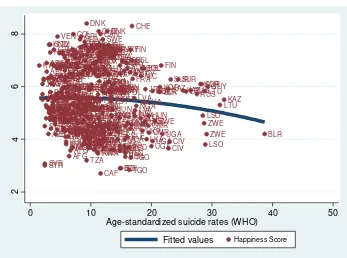

Furthermore, happiness scores also seem almost independent of suicide rates, which is often

considered an objective indicators of happiness, in contrast to happiness indices that measure

self-perception through surveys where people measure their own happiness on a 0-to-10 scale.

The relationship between self-reported happiness and objective indicators of frustration and

distress is somewhat counterintuitive. Murder rates are correlated positively with happiness index

scores (fig. 3), although this correlation is not statistically significant, whereas the correlation

between suicide rates and happiness is negative (fig. 4), as one would expect but very weak: in

regressions of happiness on murder rates, suicides rates, and per capita income, R2 is less than 2%

and the suicide rate is significant only in random effects specification – it is apparent with the

ALB DZA AGO ARG ARG ARG ARG ARG ARG ARG ARG ARG ARG ARG ARGARG ARM ARM ARM ARMARMARMARMARMARMARMARM

AUS AUSAUS

AUTAUT AUTAUTAUTAUTAUTAUTAUTAUT

AUT AUT AUT BGD BGD BLR BLRBLR BLRBLR BEL BEL BEL BELBEL BELBEL BEL BEL BELBELBELBEL

BEN BEN BTN BOL BOL BOL BOL BOL BOL BOL BOL BOL BOL BOL BOL BOL BIH BIH BIH BRA BRA BRA BRA BRA BRA BRABRA BRA BRA BGRBGR BGRBGRBGRBGRBGR BGR BGR BFA BDI BDI CMR CMR CAN CAN TCD CHL CHL CHL CHL CHL CHLCHL CHN CHN COL COL COL COL COLCOLCOLCOL

COL COL COL COL COM COD COG

CRI CRICRI CRI CRI

CRICRICRICRICRI CRI CRI CRI CRICRI CIV CIV HRV HRV HRV HRV HRV HRV HRV CYP

CYPCYPCYPCYPCYP CYP

CYPCYPCYPCYP

CYP CZE

CZE CZE CZECZECZE

CZE CZE CZECZE CZE CZE DNK DNKDNKDNK DNKDNKDNKDNKDNK

DNK DNK DNK DJI DOM DOM DOM DOM DOM DOM DOM DOM DOMDOM ECU ECUECU ECU ECU ECU ECU ECU ECU ECU ECU ECU ECU EGYEGY EGYEGY SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV EST EST ESTEST ESTEST

ESTESTESTEST EST EST EST ETH ETH FIN FIN FINFINFINFIN FIN FIN FIN FINFIN FINFIN FRA FRA FRA FRA FRA FRA FRA FRA FRA FRA FRA FRAFRA GAB GEOGEO GEO GEOGEO GEO GEO GEO GEO GEOGEO DEUDEUDEUDEUDEUDEU

DEU DEUDEU

GHA GRCGRCGRCGRCGRCGRC

GRC GRCGRC GRC GRC GRC GRC GTMGTM GIN GIN HND HND HND HND HND HND HND HND HND HND HND HND HND HUN HUN HUN HUN HUN HUNHUNHUNHUNHUN

HUN HUN ISL IND IDN IRNIRN IRN IRQ IRQ IRL IRLIRL IRL IRL IRL IRLIRL

IRLIRLIRL IRL IRL ISR ISR ISR ITA ITA ITA ITA ITA ITA ITAITAITA

ITA ITA ITA ITA JPN JOR JOR JOR JOR KAZ KAZ KAZ KAZ KAZ KAZKAZ KAZ KAZ KAZ KEN KORKOR KOR KOR KOS KOS KOS KOS KOS KOS KOS KOS KOS KGZ KGZ KGZ KGZKGZ KGZ KGZKGZ KGZ KGZ KGZ LAO LAO LVA LVA LVA LVALVA

LVA LVALVALVA LVA LVA LVA LBN LBR LBR LTU LTU LTULTULTULTU LTU LTU LTULTU

LTU LTU LUX

LUXLUX LUXLUXLUXLUX LUXLUX LUX LUX LUX LUX MKD MKD MKD MKD MKD MKD MDG MYS MYS MYS MYS MYS MLI MLI

MLTMLTMLTMLT MLTMLTMLT MLT MLTMLT MRT MRT MEX MEX MEX MEX MEX MEXMEX MEX MDA MDA MDA MDA MDA MNG MNG MNG MNGMNG MNEMNE MNE MNE

MNEMNEMNEMNE

MOZ MMR

NPL NLD NLDNLDNLDNLD NLD NLD NLD NLD NLD NLD NLD NIC NIC NIC NER NER NER NGA NOR NOR NORNOR PAK PAK PAK PAK PAK PAN PAN PAN PAN PAN PAN PAN PAN PANPAN PAN PRY PRY PRY PRY PRY PRY PRY PRY PRY PRY PRY PRYPER PER PER PERPER PER PER PER PER PER PER PER PERPER PRTPRT PRT PRT PRT PRT PRT PRTPRT PRT PRT PRT PRT ROU ROU ROU ROU ROUROUROU

ROU ROU ROU RUS RUS RUS RUS RUS RUS RWA SEN SLE SVKSVK SVK SVKSVKSVKSVKSVKSVKSVKSVK SVN

SVN SVN

SVN

ZAF ESPESPESPESPESPESPESP

ESP ESP ESP ESP ESPESP LKA LKA LKALKA SDN SWESWE

SWE SWESWESWESWESWESWESWE

SWE SWE SWE CHECHE CHE CHE CHE CHE CHE CHE TJK TJK TJK TZA TZA THA THA THA THA THA THA THA THA THA THA TGO TGO TGO TUN TUR TUR TURTUR TUR TUR TUR TUR TUR TURTUR TUR TUR TUR TUR UGA UGA UGA UGA UKR UKR GBR GBRGBRGBR GBR GBRGBR GBR GBR GBR GBR GBR USA USA USAUSAUSA

URY URY URY URY URY URY URY URY URY UZB VEN VEN VEN VEN VNM VNM VNM VNM VNM VNMVNM YEM ZMB ZMB ZWE 2 4 6 8 10

25 35 45 55 65

GINI Index (World Bank Estimate)

6

naked eye from a comparison of figure 4, which presents cross-section data for the single year of

2018, and figure 5, which presents panel data for the years 2000-18.7

The murder rate is clearly positively correlated with income inequality (fig. 6), but the suicide rate

is correlated negatively, if at all (fig. 7).

Figure 3: Happiness index (Word Happiness Report and World Database on Happiness), 0-to-10 scale; and murder rate per 100,000 inhabitants in 2000-18

Source:WHO; World Database on Happiness.

7

HappinessIndex = 5.8*** – 9.7e-07Ycap + 0.007MURDERrate*– 0.01SUICIDErate

N=323 (Panel data for 2000-18 for over 200 countries, some observations are missing), R2=0.014, robust estimates,

no control for fixed and random effects

HappinessIndex = 5.7*** + 0.005MURDERrate– 0.02SUICIDErate* Random effects regression, R2 (between) = 0.02, N=328.

HappinessIndex = 5.7*** – 1.4e-08Ycap + 0.005MURDERrate– 0.03SUICIDErate**

Random effects regression, R2 (between) = 0.02, N=323.

Here and later the following notations are used: *, **, *** – denotes significance at 10, 5 and 1% level respectively. AFG AFG AFGAFG ALB ALB ALB ALB ALB ALB ALB ALB ALB DZA DZA DZA DZA

DZADZADZA

DZA DZAAGO AGO ARG ARG ARM ARM ARM ARM ARMARMARMARMARMARMARM AUS AUS AUS AUS AUS AUS AUS AUS AUS AUS AUS AUT AUT AUT

AUTAUTAUTAUT

AUT AUT

AUTAUTAUTAUT

AUT AUT AUTAUT AZE AZE AZE AZE AZE AZE AZE AZE BHR BHR BHR BHR BHR BHR BGD BGD BGD BGD BGD BGD BGD

BGDBGDBGD

BGD BLR BLR BLR BELBEL BEL BEL BEL BEL BEL BEL BEL BEL BELBELBELBELBELBEL

BLZ BLZ BLZBLZ BEN BTN BTN BTNBOL BOL BOL BOL BOL BOL BOL BOL BOL BOL BIH BIHBIH BIH BIH BIH BIH BIH BIH BIH BWA BWA BWA BRA BRA BRA BRA BRA BRABRA

BRABRABRABRABRA

BGR BGR BGR BGR BGR BGR BGR BGR BGR BGR BGRBGR BGR BGR BGR BGR

BFABFABFA

BFA BFA

BFABFA

BFA

BFABDIBDIBDIBDI

BDI BDIBDI KHM KHM KHM KHM KHM KHMCMR CMR CMR CMR CMR CAN

CANCANCAN

CAF TCD TCD CHL CHL CHL CHL CHL CHL CHL CHL CHL CHLCHL CHN CHN CHN CHN CHN CHN CHN CHN CHN CHN CHN CHN CHN COL COL COL COL COL COL COL COL COL COL COL COL COL COL COM COM COD COG CRI CRI CRICRI CRI

CRICRICRICRICRI

CRI CRI

CRICRICRI

CIV HRV HRV HRVHRV HRV HRV HRV HRV HRV HRVCUB CYP CYP CYP CYP CYP CYP CYP CYPCYP CYP CYPCYP CYP CYP CYP CYP CZE CZE CZE CZE CZECZE CZE CZE CZE CZE CZE CZE CZE CZE CZE CZE DNK DNK DNKDNK DNKDNK

DNKDNKDNKDNKDNKDNKDNK DNK DNK DNK DNK DJI DJI DOM DOM DOM DOM DOM DOM DOM DOM DOM ECU ECU ECU ECUECU ECU ECU ECU ECU ECU ECU ECU ECU ECU ECU EGYEGY EGY EGY EGY EGY EGY SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV SLV

SLV SLV SLV

ESTESTEST

ESTEST ESTEST EST EST EST EST EST EST EST EST ETH ETH FIN FIN FIN FIN FIN FIN

FINFINFIN

FIN FIN FIN FIN FIN FIN FIN FIN FRA FRAFRA FRA FRA FRA FRAFRA FRA FRA FRA FRA FRA FRA

FRAFRAFRA

GAB GAB GEOGEO GEO GEO GEO GEO GEO DEU DEU DEU DEU DEU DEU DEU DEU DEU DEU DEU DEU DEU DEUDEU DEUDEU GHA GHA GHA GHA GHA GHA GRC GRCGRC GRCGRC GRC GRCGRC GRC GRCGRC GRC GRC GRC GRC GRC GTM GTM GTM GTM GTM GTM GTM GTM GTM GTM GTM GTM GTM GTM GIN GIN GUY GUY GUY HTI HTI HNDHND HND HND HND HND HND HND HND HND HND HND HND HND HND HKG HKGHKG HKG HKG

HKGHUNHUN

HUN HUN HUN HUN HUN HUN HUN HUN HUN HUNHUN HUN HUN HUN ISLISL ISL IND IND IND IND IND IND IND IND IND IND IND IND IDN IDN IDN IDN IDN IDN IDN IDN IDN

IRN IRQ IRQ

IRQ

IRQIRQ

IRLIRLIRL

IRL

IRLIRLIRL

IRL IRL IRL IRL IRLIRLIRLIRL

IRLIRLISRISR

ISR

ISRISRISR

ISR ISR ISR ITA ITA ITA ITA ITA ITAITA ITA ITA ITA ITA ITA ITA ITA ITA ITA

ITA JAMJAM JAM

JAM JAM JAM JPN JPN JPN JPN JPN JPN JPNJPN JPN JPN JPN JPN JPN JPN JPN JORJOR JOR JOR JOR

JORJORJOR

JORJOR JOR JOR KAZ KAZ KAZ KAZ KAZ KAZ KAZ KAZ KEN

KENKENKEN

KEN KENKEN KEN KEN KEN KOR KOR KOR KOR KOR KOR KOS KOS KOS KOS KOS KOS KOS KOS KOS KWTKWT

KWTKWTKWT

KWT KGZ KGZ KGZ KGZ KGZ KGZ KGZ KGZKGZKGZKGZLAOLVALVALVALVA

LVALVA LVA LVA LVA LVA LVA LVA LVA LVA LVA LBN LBN LBN LBN LBNLBN LBN LBN LBN LSO LSO LSO LBR LBR LBRLBR LBY LBY LTU

LTULTULTULTU

LTU LTULTU LTU LTU LTU LTU LTU LTULTU LTU

LUXLUXLUX

LUX LUXLUX LUX LUXLUX LUXLUX LUX LUX LUX LUX MKD MKD MKD MKD MKD MKD MKD MKD MDG MYSMYS MYS MYS MYS

MYSMYSMYS

MLI MLI MLT MLT MLT MLT MLT MLTMLTMLTMLTMLTMLT MLT MLT MLT MLT MRT MRT MUS MUS

MUSMUSMUS

MEX MEX MEX MEXMEX MEXMEX MEX MEX MEX MEX MEX MDA MDA MDA MNG MNGMNG MNG MNG MNGMNG MNG MNG MNE MNE MNE MNE MNE MNE

MNEMNEMNEMNE

MAR MAR MAR MAR MAR MARMAR MAR MAR MOZ MOZMOZ MOZ MMR MMR MMR MMR MMR MMR MMR NAM NPLNPL NPL NPL NPL NPL NPL NPL NPL NPL NLDNLD NLD NLD NLD NLD NLDNLDNLDNLDNLDNLDNLD NLD NLD NLD NLD NZL NZL NZL NZL NICNIC NIC NICNIC NIC NIC NIC NIC NIC NIC NIC NIC NIC NIC NER NER NGA NGA NORNOR NOR NOR NOR NOR NOR OMNOMN PAK PAK PAK PAK PAK PAK PAK PAK PAK PAK PAK PAK PAN PAN PAN PAN PANPAN PANPAN PAN PAN PAN PRY PRY PRY PRY PRY PRY PRY PRY PRY PRY PRY PRY

PERPERPERPER

PHL PHL PHL PHL PHL PHL

PHLPHLPHL

POL POL POL POL POLPOL POL POL POL POL POL POL POL PRT PRTPRT PRT PRT PRT PRTPRT PRT PRT PRT PRT PRT PRT PRT PRT PRT PRI QAT QAT QAT

QATQATQATQAT

ROU ROU ROU ROU ROU ROU ROU ROUROU ROUROU ROUROU ROU ROU ROU ROU RUS RUS RUSRUS RUS RWA RWA RWA RWARWA RWA SAU SAU SAU SEN SEN SRB SRB SRB SRBSRB SLESLE SLE SLE SLE SLE SGP SGP SGP SGP SGP SVK SVK SVK SVK SVK SVK SVKSVK SVK SVK SVK

SVKSVKSVK

SVKSVK SVNSVN SVNSVN SVN SVNSVN SVN

SVNSVNSVNSVN

SVN SVN SVN SVN SOM SOM ZAF ZAF ZAF ZAF ZAF ZAF ZAFZAF ESP ESP ESP ESP ESP ESP ESP ESP ESP ESP ESP ESP ESP

ESPESPESP

ESP LKA LKA LKA LKA LKA LKA LKA LKA LKA LKASDN SWE SWESWE SWESWE SWE SWESWE SWE SWE SWE SWE SWE SWE SWE SWE SWE CHE CHE CHE CHECHE CHE CHE CHE CHE CHE CHE CHE CHE CHE SYR SYR SYR TWN TWN TWN TWN TWN TWN TJK TJK TJK TJK TJK TJK TZA TZA TZA TZA TZA TZA THA THA THA THA THA THA THA THA THA THA THA TGO TTO TTO TUN TUNTUN TUN TUR

TURTURTURTUR

TUR TUR TUR TUR TUR UGA

UGAUGAUGA

UGA UGA UGA UGA UGA UKR UKR ARE ARE ARE GBR GBRGBR GBR GBR GBR GBR GBR GBR GBR GBR GBR GBR GBR GBR

GBRGBRUSAUSAUSA

USAUSA USA USA USA USA USA USA USA USA

USAUSAUSA

URY URY URY URY URYURY URYURY URY URY

URYURYURYURY

UZB

UZB UZB

VEN VEN

VEN

VEN VENVENVENVENVEN

VEN VEN VNM

VNMVNMVNMVNMVNM VNM

YEMYEMYEM

YEM YEMYEM ZMB ZMB ZMB ZMB ZMB ZMB ZMB ZWE ZWEZWE 2 4 6 8 10

0 20 40 60 80 100

Intentional homicide rate (Wikipedia)

7

Figure 4: Happiness index in 2018 and suicide rates in 2016

Figure 5: Happiness index and suicide rates in 2000-18

Source: WHO; World Happiness Database.

Afghanistan Albania Algeria Angola Argentina Armenia Australia Austria Azerbaijan Bahrain Bangladesh Belarus Belgium Belize Benin Bhutan Bolivia

Bosnia and Herzegovina

Botswana Brazil Bulgaria Burkina Faso Burundi Cambodia Cameroon Canada

Central African Republic Chad Chile China Colombia Congo (Brazzaville) Congo (Kinshasa) Costa Rica Croatia Cyprus Czech Republic Denmark Dominican Republic Ecuador Egypt El Salvador Estonia Ethiopia Finland France Gabon Georgia Germany Ghana Greece Guatemala Guinea Haiti HondurasHungary Iceland India Indonesia Iran Iraq Ireland Israel Italy Jamaica Japan Jordan Kazakhstan Kenya Kuwait Kyrgyzstan Laos Latvia Lebanon Lesotho Liberia Libya Lithuania Luxembourg Macedonia Madagascar Malawi Malaysia Mali Malta Mauritania Mauritius Mexico Moldova Mongolia Montenegro Morocco Mozambique Myanmar Namibia Nepal Netherlands New Zealand Nicaragua Niger Nigeria Norway Pakistan Panama Paraguay Peru Philippines Poland Portugal Qatar Romania Russia Rwanda Saudi Arabia Senegal Serbia Sierra Leone Singapore Slovakia Slovenia Somalia South Africa South Korea South Sudan Spain Sri Lanka Sudan Sweden Switzerland Syria Tajikistan Tanzania Thailand Togo Trinidad & Tobago

Tunisia

TurkeyTurkmenistan

Uganda Ukraine United Arab EmiratesUnited KingdomUnited States

Uruguay Uzbekistan Venezuela Vietnam Yemen Zambia Zimbabwe 3 4 5 6 7 8

0 10 20 30 40

Suicide rate per 100,000 inhabitants in 2016

Happiness score in 2018 Fitted values

AFG AFG AFG ALB ALB ALB DZA DZA DZA AGO AGO ARG ARGARGARG

ARMARMARM

AUS AUS AUT AUT AUT AUT AZE AZE AZE BHRBHR BHR BGD BGD BGD BLR BLRBLR BEL BEL BELBEL BLZ BLZ BEN BEN BTN BTN BOL BOL BOL BOL BIHBIH BIH BWA BWA BWA BRABRA BRA BGR BGR BGR BFA BFA BFA BDIBDI KHM KHM KHM CMR CMR CMR CAN CAN CAN CAF CAF CAF TCD TCD TCD CHL CHL CHL CHL CHN CHN CHN COL COL COL COL

COMCOMCOM COD COD COG COG CRI CRI CRI CRI CIVCIV HRV HRV HRV CYP CYP CYP CZE CZE CZE DNK DNK DNKDNK DJI DJI DOM DOM DOM ECU ECU ECU ECU EGY EGYEGY SLV SLV SLV SLV EST ESTEST ETH ETH ETH FIN FIN FINFIN FRA FRA FRA FRA GAB GAB GAB GEOGEOGEO

DEU DEU DEU DEU GHAGHA GHA GRC

GRCGRCGRC GTM GTM GTM GTM GIN GIN GIN GUY HTIHTI HTI HND HND

HNDHND HUN HUN

HUN ISLISL IND IND IND IDN IDN IDN IRN IRN IRQ IRQ IRQ IRL IRL IRLIRL ISR ISRISR ITA ITAITAITA JAM JAM JAM JPN JPN JPN JOR JOR JOR KAZ KAZ KAZ KEN KENKEN KOR KOR KOR KWT KWT KWT KGZ KGZKGZ LAO LAO LVA LVA LVA LBN LBN LBN LSO LSO LBR LBR LBR LBY LBYLBY LTU LTU LTU LUX LUX LUX LUX MKD MKD MKD MDG MDG MWI MWI MYS MYSMYS MLIMLI MLI MLT MLT MLT MRT MRT MRT MUS MUS MEX MEX MEX MDA MDA MDA MNG MNG MNG MNE MNEMNE MAR MAR MAR MOZ MMR MMRMMR NAM NAM NPL NPL NPL NLD NLD NLD NLDNZLNZL NIC NIC NIC NIC NER NER NER NGA NGA NGA NOR NOR OMN PAK PAK PAK PAN PANPAN PRY PRY PRY PRY PER PER PER PER PHL PHL POL POLPOL PRT PRT PRT PRT QAT QAT QAT ROU ROU ROU ROU RUS RUS RWA RWA SAU SAU SAU SEN SEN SEN SRBSRB SLE SLESLE SGPSGP SVK SVK SVK SVN SVN SVN SOM SOM SOM ZAF ZAF ESP

ESPESPESP

LKA LKA LKA SDN SDN SDN SUR SUR SUR SWE SWE SWE SWE CHE CHE CHE CHE SYR SYR SYR TJK TJK TJK TZA TZATZA THATHA THA TGO TGO TTOTTO TUN TUN TUN TUR TUR TURTKM TKM UGA UGA UGA UKR UKR ARE ARE GBR GBR GBR GBR

USAUSAUSA URY URY URY URY UZB UZB UZB VEN VEN VEN VEN VNM VNM VNM YEM YEM YEM ZMB ZMB ZWE ZWE ZWE 2 4 6 8

0 10 20 30 40 50

Age-standardized suicide rates (WHO)

[image:8.612.76.423.397.655.2]8

[image:9.612.74.418.113.360.2]Figure 6: Murder rate per 100,000 inhabitants and Gini coefficient of income distribution in percentage terms in 2000-18

Figure 7: Suicide rate per 100,000 inhabitants and GINI coefficient of income inequality in percentage terms in 2000-18

Source: WHO, WDI.

ALB ALB ALB ALB DZA ARGARG ARM ARM ARMARMARM ARMARM

ARM ARMARMARMARMARMARMARMARMAUSAUSAUSAUS

AUTAUT

AUTAUTAUTAUTAUTAUTAUTAUTAUTAUTAUT AZE AZEAZE

AZEAZE BGDBGDBGD BLR BLR BLR BLR BLRBLRBLRBLRBLRBLRBLRBLR

BLRBLRBLRBELBELBELBELBELBELBELBELBELBELBELBELBEL BEN BTN

BTNBTN BOLBOL

BOL BOL BOL BOLBOL BOLBOL BOL BOL BIHBIHBIHBIHBIH

BWA BWA BRA BRA BRA BRA BRA BRA BRA BRA BRA BRA BRABRA BRA BRA BGRBGR

BGRBGRBGRBFABGRBGRBGRBGRBDI CMR

CANCANCANCANCAN CHNCHN CPVCHLCHLCHLCHLCHLCHL

COL COL COL COL COL COL COL COLCOL COL COL COL COL COL COL COG CRICRICRICRICRICRICRICRICRICRICRICRICRICRICRICRICRI CIV HRV HRV HRVHRV HRVHRV HRV CYPCYPCYPCYPCYPCYPCYPCYPCYPCYP CYPCYP CZE

CZE CZE CZECZECZECZECZE CZECZE CZE CZE DNK DNKDNKDNKDNKDNKDNKDNKDNKDNKDNKDNKDNK

DOM DOM DOM DOM DOM DOM DOM DOM DOMDOM DOMDOM DOM DOM DOMDOM ECU ECUECU ECU ECUECU ECU ECUECU ECU ECUECU ECUECU ECU EGY EGYEGY EGY SLV SLV SLV SLV SLVSLV SLV SLV SLV SLV SLV SLV SLVSLV SLV SLV SLV EST EST ESTEST ESTESTESTESTESTESTESTESTEST

ETH ETH FJI FJI FINFIN

FINFINFINFIN FINFINFIN FINFIN

FINFINFRA FRAFRAFRAFRAFRAFRAFRAFRAFRAFRAFRAFRA

GABGMB GMB GEO GEO GEO GEO GEOGEOGEOGEOGEO

GEOGEO GEO GEO

DEUDEUDEUDEUDEUDEUDEUDEUDEUGRCGRCGRCGRCGRCGRCGRCGRCGRCGRCGRCGRCGRC GHA

GTM GTM GTM GNB HTI HNDHND HND HND HND HND HND HND HND HND HND HND HND HND HND HUN HUN HUN HUN HUN HUNHUNHUNHUNHUNHUNHUN ISLISLISLISLISL ISLISL ISLISLISL

ISL ISL INDIRNIRNIDNIRN IRQ

IRLIRLIRL IRL IRL

IRLIRLIRLIRLIRLIRLITAIRLIRLITAITAITAITAITAITAITAITAITAITAITAITA ISR ISRISRISRISR

JAM JAM

JPNJORJORJOR KAZ KAZ KAZ KAZ KAZ KAZ KAZ KAZKAZ KAZ KAZ

KAZ KEN KEN

KORKOS KOS KOSKOS KOSKOSKOSKOS

KGZ KGZKGZ

KGZKGZKGZKGZKGZKGZKGZ KGZ

KGZ KGZKGZ KGZKGZ

KGZ LBNLVALVALVALVALVALVALVALVALVALVALVALVA

LSO

LBR LTU LTU LTULTULTULTU LTU LTU LTULTULTULTU LUX

LUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXMKDMKDMKDMKDMKDMKD MDGMDG MWIMYSMDVMYSMWIMYSMYSMYS MDV

MLTMLTMLTMLTMLTMLTMLTMLTMLTMLT

MRT MUSMUS MEX MEX MEXMEX MEX MEX MEX MEX MEXMEX FSM MDAMDA MDA MDAMDAMDAMDA MDAMDA MDA MDA MDA MDA MDA MDA MCO MCO MNG MNGMNGMNG MNGMNG MNE MNEMNEMNEMNE

MNEMNEMNEMNEMNE MMR MOZMOZ

NAM

NPL NPL

NLD NLDNLDNLDNLD NLD NLD NLD NLDNLDNLDNLD

NIC NIC NIC

NIC NER

NORNORNOR NORNOR NOR NOR

NORNORNORNORNORPAKPAKPAKPAK PAKPAKPAK

PAK PANPAN PAN PAN PAN PAN PAN PAN PAN PAN PAN PANPAN PAN PAN PAN PAN

PRY PRYPRY PRY PRY PRY PRY PRY PRYPRY PRY PRYPRY PRY PRY PER PER PER PERPERPER PRTPRT PRT PRT PRT PRT PRTROUPRTPRTROUPRTROUROUROUPRTPRTPRTROUROUROUROUROU

RUS RUSRUSRUS RUS RUS RUSRUS RUS RUSRUS RUS RUS RWA RWA STP SEN SYC SLE SVKSVK SVK SVKSVNSVKSVKSVKSVKSVKSVKSVKSVK SVN SVN SVN

SVNSVNSVNSVNSVNSVNSVNSVN SLB

ZAF

ZAF ZAF

ZAF ZAF

ESPESPESPESPESPESPESPESPESPESPESPESPESP LKA LKALKA

LKA SWESWESWESWESWESWESWESWESWESWESWESWESWETJKCHECHETJKCHE SYRCHECHECHETJKCHETJKCHECHECHE

TZATHATHATHATHATHATHATHATHA THATHATHA THA THA

TLS TONTON TGO TUN TUNTURTURTURTURTURTURTURTURTURTUR

UGAUGA UGA UKR

UKRUKRUKRUKR UKR UKR UKR UKR UKR UKR GBR GBRGBRGBR GBRGBRGBR GBR

GBRGBRGBRGBR USAUSA USA USAUSAUSAURYURYURYURYURYURY URYURYURYURY URY UZB UZBUZBVUT VEN VEN VEN VENVEN VEN VNM VNM VNM VNM VNM

YEM ZMBZMB

0 20 40 60 80 1 0 0

20 30 40 50 60 70

GINI Index (World Bank Estimate)

Intentional homicide rate 95% CI Fitted values AGO ARG ARG ARG ARMARMARM AUS AUTAUT BGD BGDBGD BLR BLR BLRBLR BEL BEL BEN BOL BOL BOL BIH BRA BGR

CANCAN CHL

CHL

COL COL COL COL CRICRICRICRI CIV HRV HRV CYPCYP CZE CZE

DNKDNK DOMDOMDOM DOM ECU ECU ECU ECU EGYEGY SLV SLV SLV SLV EST EST ETH ETH FIN FIN FRA FRA GMB GMB GEO GEO GEOGEO DEU DEUDEU

GRCGRC GTM

GNB HND HND HUN HUN ISL IRL IRL ISR ITAITA JOR KAZ KAZ KEN KOR KGZ KGZ KGZ KGZ LVA LVA LSO LTU LTU LUX LUX MKD MDG MWI MYS MLTMLT MRT

MEX MEXMEX MDA MDA MDA MDA MNG MNG MNE MMR NAM NPL NLDNLD NORNOR PAK PAK PAN PAN PAN PAN PRY PRYPRY PER PER PERPER PRT PRT ROU ROU RUS RUS RUS RWA RWA STP STP SVK

SVNSVN ZAF

ZAF

ESPESP LKA SWESWECHECHE

TJK TZA THA THA THA TGO TUN TUN

TURTURTUR UGA UKR UKR UKR GBR GBR USA USAUSA URY URY URY UZB VUTVNM VNM ZMBZMB 0 10 20 30 40 50

20 30 40 50 60 70

GINI Index (World Bank Estimate)

9

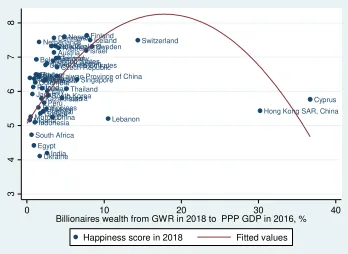

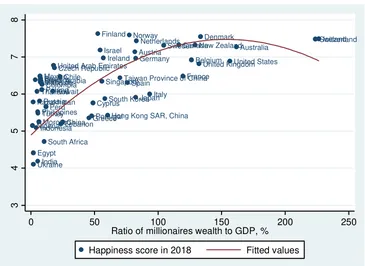

Wealth inequalities, especially inequalities at the very top of the wealth pyramid – the share of wealth belonging to billionaires and millionaires – are positively correlated with happiness indices (fig. 8-10).

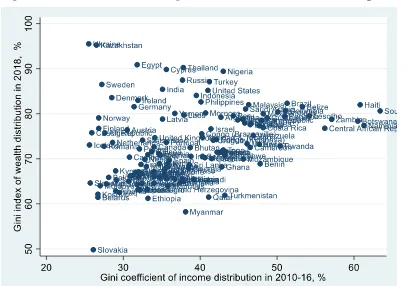

It is important to note that inequalities at the very top –billionaire and millionaire ‘intensity’, the ratio of billionaire/millionaire wealth to GDP – are not precisely correlated with general measures of inequalities like Gini coefficients. Whereas Gini coefficients for wealth and income distribution

are positively correlated with one another (fig. 12), and billionaire intensity is positively correlated

with Gini coefficients for wealth distribution (fig.13), the correlation of billionaire intensity with

general income-distribution Gini coefficients is negative, if present at all (fig. 14). That is to say,

there are countries with quite an even distribution of income, but levels of high billionaire intensity

in GDP; e.g., Scandinavian countries.

Figure 8: Happiness index (0-to-10 scale) and billionaire wealth from the Global Wealth Report as a percentage of PPP GDP in 2018

Argentina Australia Austria Belgium

Brazil Canada

Chile

China Colombia

Cyprus Czech Republic

Denmark

Egypt

Finland

France Germany

Greece Hong Kong SAR, China

Iceland

India Indonesia

Ireland Israel

Italy Japan

Kazakhstan Kuwait

Lebanon Malaysia

Mexico

Morocco Netherlands

New Zealand

Nigeria

Norway

Peru Philippines Poland

Portugal Russia Saudi Arabia Singapore

South Africa South Korea Spain

Sweden Switzerland

Taiwan Province of China

Thailand

Turkey

Ukraine

United Arab EmiratesUnited KingdomUnited States

3

4

5

6

7

8

0 10 20 30 40

Billionaires wealth from GWR in 2018 to PPP GDP in 2016, %

[image:10.612.80.428.407.661.2]10

[image:11.612.77.487.114.377.2]Figure 9: Happiness index (0-to-10 scale) and billionaire wealth from the Forbes list as a percentage of PPP GDP in 2018

Figure 10: Happiness index (on a scale of 0 to 10) and net worth of millionaires according to the Global Wealth Report as a percentage of PPP GDP

Argentina Australia

Austria Belgium

Brazil Canada

Chile

China Colombia

Cyprus Czech Republic

Denmark

Egypt Finland

France Germany

Greece Hong Kong SAR, China

Iceland

India Indonesia

Ireland Israel

Italy Japan

Kazakhstan Kuwait

Lebanon Malaysia

Mexico

Morocco Netherlands

New Zealand

Nigeria Northern Cyprus

Norway

Palestinian Territories Peru

Philippines Poland

Portugal Russia Saudi ArabiaSingapore

Somalia South Africa

South Korea

South Sudan Spain

Sweden Switzerland

Taiwan Province of China

Thailand

Turkey

Ukraine

United Arab EmiratesUnited KingdomUnited States

3

4

5

6

7

8

0 20 40 60

Net wealth of billionaires as a % of GDP in 2018

Happiness score in 2018 Fitted values

Argentina

Australia Austria

Belgium

Brazil

Canada

Chile

China Colombia

Cyprus Czech Republic

Denmark

Egypt

Finland

France Germany

GreeceHong Kong SAR, China

Iceland

India Indonesia

Ireland Israel

Italy Japan Kazakhstan

Kuwait

Lebanon Malaysia Mexico

Morocco

Netherlands New Zealand

Nigeria

Norway

Peru Philippines

Poland

Portugal Russia

Saudi Arabia Singapore

South Africa

South Korea Spain

Sweden Switzerland

Taiwan Province of China

Thailand

Turkey

Ukraine

United Arab Emirates United KingdomUnited States

3

4

5

6

7

8

0 50 100 150 200 250

Ratio of millionaires wealth to GDP, %

[image:11.612.77.442.445.711.2]11

Figure 11: Happiness index (on a scale of 0 to 10) and Gini coefficient of wealth distribution in 2018, percentage terms

Source: GWR; World Happiness Database; WDI; Forbes billionaires’ list.

Figure 12: Income and wealth inequalities, Gini coefficients in 2000-18, percentage terms Argentina

Australia

Austria Belgium

Brazil Canada

Chile

China

Colombia

Cyprus Czech Republic

Denmark

Egypt Finland

France

Germany

Greece Hong Kong SAR, China Iceland

India Indonesia Ireland Israel

Italy Japan

Kazakhstan Kuwait

Lebanon Malaysia

Mexico

Morocco Netherlands New Zealand

Nigeria Norway

Peru

Philippines Poland

Portugal

Russia Saudi Arabia Singapore

South Africa South Korea

Spain

Sweden Switzerland

Syria

Taiwan Province of China

Thailand

Turkey

Ukraine United Arab Emirates

United Kingdom United States

3

4

5

6

7

8

50 60 70 80 90 100

Gini index of wealth distribution in 2018, %

[image:12.612.71.482.416.702.2]12

Figure 13: Wealth of billionaires as a percentage of GDP and Gini index of wealth distribution, in percentage terms, in 2018

Figure 14: Gini coefficient of income distribution and ratio of billionaire wealth to PPP GDP, percentage terms

Source: WDI; GWR.

AFGAFGAFGAFGAFGAFG AFGAFGAFGAFGAFG AFG AFG AFGAFG AFG AFG ALBALB ALBALBALB ALBALB ALB

ALBALBALBALBALBALBALBALBALBALBALBAUSARMARMARMARMARMARMARMARMARMARMARMARMARMARMARMARMARMARMARMAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOAGOARGARGAGOARGDZAARGDZAARGDZAARGARGARGARGARGDZAARGARGARGARGDZAARGDZADZADZADZADZAARGDZAARGDZADZADZAARGDZADZADZAARGDZAATGDZAATGATGATGATGATGATGATGATGATGATGATGATGATGATGATGATGATGATG AUS

AUSAUSAUS AUS AUSAUS

AUS AUS

AUSAUSAUS AUS AUS AUS AUS AUS AUS AUTAUT AUT AUT AUT AUT AUT AUT AUT AUTAUTAUT AUT AUT AUT AUT AUT AUT AUT AZEAZE AZE AZE AZE AZEAZEAZE AZEAZEAZEAZEAZEAZE AZE AZEAZE AZE

AZEBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBGDBRBBRBBRBBRBBRBBRBBRBBRBBRBBRBBRBBRBBHRBHRBHRBRBBRBBRBBHRBRBBRBBHRBRBBHRBRBBHRBHRBHSBHRBHSBHSBHRBHRBHSBHSBHSBHRBHRBHRBHSBHSBHSBHSBHSBHRBHRBHSBHRBHRBHSBHRBHSBHSBHSBHSBHSBHS BLRBLR

BLR BLRBLR BLRBLRBLRBLRBLRBLRBLRBLRBLRBLRBLRBLRBLRBLRBELBELBELBELBEL

BEL BELBEL BELBELBELBEL BELBELBELBELBELBELBEL

BLZ BLZ BLZ BLZBLZBLZBLZBLZBLZ BLZBLZBLZBLZBLZBLZBLZBLZBLZBLZ BEN

BEN

BENBENBENBENBENBENBENBENBENBENBENBENBENBENBENBENBENBTNBTNBTNBTNBTNBTNBTNBTNBTNBOLBTNBTNBOLBTNBOLBOLBTNBOLBOLBOLBTNBOLBTNBOLBTNBOLBTNBOLBTNBTNBOLBOLBOLBOLBOLBOLBOLBOL BIH BIH BIH BIHBIH BIHBIH BIH

BIHBIHBIHBIHBIHBIHBIHBIHBIHBIHBIH BWABWABWABWABWABWABWABWABWABRABWABWABWABWABWABWABWABWABWABRABRABRABWABRA BRA BRA BRA BRA BRA BRA BRABRA BRA BRA BRA BRA BRA BRA

BRNBRNBRNBRNBRNBRNBRNBRNBRNBRNBRNBRNBRNBRN BRN BRNBRN BRN BRN BGRBGR BGR BGRBGR BGRBGRBGR

BGRBGRBGRBGRBGRBGRBGRBDIBDIBGR BFABGRBDIBDIBGRBDIBDIBDIBDIBDIBDIBDIBGRBDIBDIBDIBDIBDIBDIBDIBDIBFABFABFABFABFABFABFABFABFABFABFABFABFABFABFABFABFAKHMKHMKHMKHMBFACMRCMRCMRCMRCMRKHMKHMKHMKHMCMRCMRCMRCMRKHMKHMKHMCMRCMRCMRCMRCMRKHMKHMCMRKHMKHMCMRKHMCMRKHMKHMCMRKHMCMR CAN CAN CANCAN CAN CAN CAN CAN CAN CAN CAN CANCANCAN

CANCANCANCANCAN

CPV CPV

CPVCPVCPVTCDCPVTCDTCDTCDTCDTCDTCDTCDTCDTCDTCDCPVTCDCPVTCDTCDTCDCPVCPVTCDTCDCPVTCDCPVTCDCPVCAFCPVCAFCAFCAFCPVCAFCPVCAFCPV CPVCAFCAFCAFCAFCAFCAFCAFCPVCAFCAFCAFCAFCAFCAFCHLCHL CHL CHL CHL CHLCHL CHL CHL CHL CHL CHL CHL CHL CHL CHL CHL CHL CHL CHN CHN

CHNCHNCHNCHNCHNCHNCHN CHN CHN CHNCHNCHN CHNCHN CHN CHN CHN COLCOL COLCOL COLCOL COL COL COL COL COL COL COL COLCOLCOLCOL COL COL COM COM COMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOMCOM COD COD CODCODCODCODCODCODCOD CODCODCODCODCODCODCODCODCOD CODCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCOGCRICOGCOGCOG CRI CRI CRICIVCRICRICIVCRICIVCIVCIVCIVCIVCIVCIVCIVCRI CRICRI CRICIVCIVCRICIVCRICIVCIVCIVCRICRICIVCIVCIVCRICRICRICRI HRV HRV HRV HRVHRV HRVHRV HRV

HRVHRVHRVHRVHRVHRVHRVHRVHRVHRVHRV CYPCYPCYPCYPCYPCYP CYP CYP CYP CYP CYP CYP CYP CYP CYP CYP CZECZE CZECZECZE

CZE CZE

CZE

CZE

CZECZECZECZE CZECZECZE

CZE CZECZE DNK DNK DNK DNK DNK DNK DNK DNK DNK DNK DNKDNKDNK

DNK DNK DNK DNK DNK DNK DJI DJI

DJIDJIDJIDJIDJIDJIDJIDJI DJIDJIDJIDJIDJIDJIDJIDJIDJIECUECUECUECUDOMDOMECUECUDOMDOMECUDOMECUDOMECUECU ECUECUDOMDOMDOMECUEGYDOMDOMDOMDOMECUDOMECUDOMECUDOMEGYDOMDOMECUDOMEGYECUECUEGYDMADMADMADMADMADMADMADMADMADMADMADMADMADMADMADMADMADMADMA EGY EGYEGY

EGY

EGYEGYEGYEGYEGY EGYEGY EGY

EGY EGYEGY SLV

SLV SLV SLVSLV SLVSLV SLV SLV

SLVERISLVSLVSLV SLV GNQSLVSLVSLVSLVERISLVERIERIERIERIERIERIERIERIERIERIERIGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQGNQ ERIERI

ERI ERI ERI

ERIESTESTESTESTESTESTESTESTESTESTESTESTESTESTESTESTESTESTEST ETH

ETH ETHETHETHETHETHETHETH ETHETHETH ETHETHETH ETH ETH ETH

ETH FJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJIFJI FINFINFINFINFINFINFINFINFIN FIN FINFIN

FIN FINFIN FIN FIN FINFIN FRAFRA FRA FRA FRA FRA FRA FRAFRA FRAFRA FRAFRA

FRAFRAFRAFRA FRA FRA

GAB GAB

GABGEOGABGABGABGEOGEOGABGABGEOGABGABGABGABGABGEOGEOGABGEOGABGEOGABGABGEOGEOGEOGEOGEOGEOGABGABGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMBGMB GEO GEOGEO GEO GEO DEU DEU DEU DEUDEUDEU DEUDEU DEU DEU DEU DEU DEU DEU DEU DEUDEU DEU DEU GHA GHA GHAGHAGHAGHAGHAGHAGHA GHAGHAGHAGHAGHAGHAGHAGHA GHA GHA GRC GRCGRC GRC GRC GRC GRC GRC GRC GRC GRC GRCGRC GRCGRC GRC GRC GRC GRC GRD GRD GRDGRDGRDGRDGRD GRD GRD GRDGRDGRDGRDGRDGRDGRDGRDGRDGRD GTM GTM GTMGTMGTMGTMGTM GTM GTM GTMGTMGTMGTMGTMGTMGTMGTMGTMGTM GIN

GIN GINGINGINGINGINGIN GIN GINGINGINGINGINGINGINGINGINGIN GNB GNB

GNBGNBGNBGNBGNBGNBGUYGUY GUYGNBGNBGNBGUYGUYGNBGNBGNBGNBGNBGUYGUYGUYGNBGUYGUYGUYGUYGUYGNBGUYGUYGNBGUYGUYGUYGUYHNDHND HNDHNDHNDHNDHNDHNDHNDHNDHNDHNDHTI HTIHTIHTIHTIHNDHNDHTIHNDHTIHTIHTIHTIHTI HTIHTIHNDHTIHTIHTIHNDHTIHNDHNDHTIHTI HKG

HKG HKG

HKGHKGHKGHKG HKG HKG HKG HUN HUN HUN HUNHUN HUNHUN HUN HUNHUNHUNHUNHUNHUNHUNISLHUNHUNHUNISLISLHUNISL

ISL ISL ISL ISL ISL ISL ISL ISL ISL ISL ISL ISL ISL ISL ISL IND IND INDIND INDIND IND IND IND IND IND INDINDIND

IND INDINDINDIND

IDN IRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRN IRN IRNIRN IRN IRN IRQIRQIRQIRQIRQIRQIRQIRQIRQIRQIRQIRQIRQIRQ IRQ IRQIRQ IRQ IRQ IRLIRL IRL IRL IRLIRL IRL IRL IRL IRL IRL IRL IRL IRL IRL IRL IRL IRL IRL ISR ISR ISR ISRISR ISR ISR ISR ISR ISR ISR ISR ISR ISR ISR ISR ISR ISR ISR ITA ITA ITAITAITAITAITAITA ITAITAITAITA

ITA ITA ITAITA ITA ITA ITA JAM JAM JAM JAMJAMJAMJAM JAM JAM JAMJAMJAMJAMJAMJAMJAMJAMJAMJAM JPN JPN

JPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPN

JORJORJORJORJORJORJORJORJORJORJORJORJORJOR JORJORJORJORJOR

KAZKAZKAZKAZ KAZKAZ KAZ KAZ

KAZKAZKAZKAZ KAZKAZKAZ

KAZKAZKAZKAZ

KEN KEN KENKENKENKENKENKENKENKENKENKENKENKENKENKENKENKENKEN KIRKIRKIRKIRKIRKIRKIRKIRKIRKIRKIRKIRKIRKIR KIR KIRKIR KIR KIR KOR KORKORKOR KORKORKORKOR KOR

KORKORKOR KOR KORKOR KOR KOR

KOR KOR

KOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOSKOS

KWT KWT KWT

KWT KWT

KWTKWTKWTKWT KWT

KWT KWTKWTKWTKWTKWTKWTKWTKWT

KGZKGZKGZKGZKGZKGZKGZKGZKGZKGZKGZKGZKGZ KGZ KGZ KGZKGZ KGZ

KGZ LVALAOLAOLVALVALVALVALVALVALVALVALVALVALVALVALVALVALVALVALVALAOLAOLAOLAOLAOLVALAOLAOLAOLAOLAOLAOLAOLAOLAOLAOLAOLAO LBNLBNLBN LBN LBN LBN LBN LBN LBN LBN LBN LBNLBN LBN LBN LBN LBN LBNLBN LSO LSO LSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSOLSO LBR

LBR LBRLBRLBRLBRLBRLBRLBR

LBRLBRLBRLBRLBRLBRLBRLBRLBYLBRLBYLBRLBYLBYLBYLBYLBYLBYLBYLBYLBY LBY LBY LBYLBY LBY LBY LBY LBY LTU LTU LTU LTULTU LTULTULTU

LTULTULTULTUMKDMKDMKDMKDLTUMKDMKDLTULTUMKDMKDLTU LUXMKDMKDLTULTUMKDMKDMKDLTUMKDLUXMKDLUXLUXLUXLUXLUXLUXLUXLUXLUXMKDLUXMKDLUXMKDMKDLUXLUXLUXLUXLUXLUXMDGMDGMDGMDGMDGMDGMDGMDG MWIMDGMDGMDGMDGMDGMDGMDGMDGMDGMWIMDGMWIMWIMWIMWIMWIMWIMWIMWIMWIMDGMWIMWIMWIMWIMWIMWIMWIMWI MACMACMACMACMACMACMACMACMACMACMACMACMACMACMACMACMACMAC MYS MYS MYS MYS MYSMYS MYS MYS MYS MYS MYS MYS MYS MYS MYS MYSMYS MYSMYS MDVMDV MDV MDV MDVMDVMDVMDV MDVMDVMDVMDVMDVMDV MDV MDVMDV MDV MDV MLI MLI MLIMLIMLIMLIMLIMLIMLI MLIMLIMLIMLIMLIMLIMLIMLIMLIMLI MLT MLT MLT MLTMLT MLTMLT MLT

MLTMLTMLTMLTMLTMLTMLTMLTMUSMLTMLTMUSMUSMLTMUSMUSMUSMUSMUSMUSMUSMUSMUSMUSMUSMUSMUSMUSMUSMRTMRTMUSMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMRTMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHLMHL

MEX MEX MEXMEXMEXMEXMEXMEX MEX MEXMEXMEX

MEX MEX MEX MEXMEXMEXMEX FSMFSMFSMFSMFSMFSMFSMFSMFSMFSMFSMFSMFSMFSM FSM FSMFSM FSM FSM MDA MDA MDA MDAMDA MDAMDA MDA MDA MDA MDA

MDAMDAMDAMDAMNGMDAMDAMDAMNGMNGMNGMDAMNGMNGMNGMNGMNGMNGMNGMNGMNGMNGMNGMNGMNGMNGMNG MNE MNE MNE MNEMNE MNEMNE MNE

MNEMNEMNEMNEMNEMNEMNEMNEMNEMNEMNE MARMARMARMARMARMARMARMARMARMARMAR

MAR MARMARMAR MARMARMAR MAR MOZ

MOZ MOZMOZMOZMOZMOZMOZMOZ MOZMOZMOZMOZMOZMOZMOZMOZMOZ MOZ MMRMMRMMRMMRMMRMMRMMRMMRMMRMMRMMRMMRMMRMMR

MMR MMRMMR MMR

MMR NPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNPLNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNAMNLDNLDNLDNLDNAM NLD NLD NLD NLD NLD NLD

NLDNLDNLDNLDNLDNLDNLD NLD NLD NZL NZL NZL NZL NZL NZL NZL NZL NZL NZL NZL NZL NZLNZLNZLNZL NZL NZL NZL

NIC NIC NIC NICNIC NICNIC NIC NIC NICNICNIC NICNICNICNICNICNICNIC NER

NER NERNERNERNERNERNERNER NERNERNERNERNERNERNERNERNER

NER NGANGANGANGANGANGANGA NORNORNORNGANGANGANGANGANGANGANGANGANGANGANGA NORNOR NOR NOR NOR NOR NOR NORNOR NOR NOR NOR NOR NOR NOR NOR

OMNOMNOMNOMNOMNOMNOMNOMNOMNOMNOMNOMNOMNOMN OMN OMNOMN OMN OMN PAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAK

PAK PAKPAK PAK

PAK PERPERPERPERPER PERPLWPLWPLWPLWPRYPLWPERPERPERPRYPRYPANPRYPLWPNGPANPLWPRYPRYPRYPRYPLWPNGPNGPANPRYPLWPNGPRYPLWPLWPLWPANPRYPLWPLWPRYPRYPANPANPANPANPANPERPRYPRYPRYPLWPLWPANPLWPLWPANPLWPANPANPNGPANPNGPANPNGPNGPANPNGPRYPRYPNGPERPNGPNGPANPANPNGPNGPNGPNGPNGPNGPRYPNGPAN PER PER PER PER PER PERPER PER PHL PHL PHL PHL PHLPHLPHL PHL PHL PHLPHL PHL PHL PHL PHL PHL PHL PHL PHL POLPOL POL

POL POLPOL POL POL POL POL POLPOL POL

POL POL POL POLPOLPOL PRT PRTPRTPRT

PRT PRTPRT

PRT

PRT PRTPRTPRTPRTPRTPRTPRT

PRT PRT PRT

PRI PRI PRI PRIPRI PRIPRI PRI PRI PRIPRIPRI PRIPRIPRIPRIPRIPRIPRI QATQATQATQATQATQATQATQATQATQATQATQATQATQAT

QAT QATQAT QAT QAT ROUROU

ROUROUROUROU ROUROUROUROUROUROUROUROUROUROUROUROUROU RUSRUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RUS RWA RWA RWARWASMRRWARWASMRRWASMRSMRRWARWARWARWASMRSMRRWARWARWASMRSMRRWAWSMWSMWSMWSMRWARWAWSMRWAWSMWSMWSMWSMWSMWSMRWAWSMWSMWSMWSMWSMWSMWSMWSM SMRSMRSMRSMRSMRSMRSMRSMRSMRSMRSMR STP

STP STPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTPSTP

SAU SAU SAUSAU SAU SAU SAU SAU SAU SAU SAU SAU SAUSAUSAU SAUSAUSAUSAU SEN

SEN SENSENSENSENSENSENSENSENSENSENSENSENSENSENSENSENSEN SRB SRB SRB SRBSRB SRBSRB SRB

SRBSRBSRBSRBSRBSRBSRBSRBSRBSRBSRBSYCSYCSLESYCSYCSLESYCSLESLESLESLESLESYCSYCSYCSLESLESLESLESYCSLESLESYCSLESLESYCSYCSYCSYCSLESLESLESYCSLESYCSYCSYCSYC

SGP SGP SGP SGP SGPSGP SGP SGP SGP SGP SGP SGP SGP SGPSGP SGP SGP SGP SGP SVK SVK SVKSVKSVK SVKSVK SVK

SVKSVKSVKSVKSVKSVK SVKSVKSVKSVKSVK SVNSVNSVNSVNSVNSVNSVNSVNSVNSVNSVNSVNSVNSVN SVNSVNSVNSVNSVNSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLBSLB ZAFZAFZAFZAF ZAF ZAF ZAFZAF ZAFZAF ZAF ZAF ZAFZAF ZAF ZAF ZAF ZAF ZAF ESP ESP ESP ESP ESPESP ESP ESP ESPESP ESP ESPESP

ESP ESPESPESPESP

LKALKALKALKALKALKALKALKA LKALKALKALKALKALKA LKA LKALKA LKA

LKALCALCALCA LCALCALCALCALCALCA LCALCA LCALCALCALCALCALCALCALCA VCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCTVCT SDN

SDN

SDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDNSDN SWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSWZSURSURSURSURSURSURSURSURSURSURSURSURSURSURSURSURSURSURSUR SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE SWE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHECHE

SYRSYRSYRSYRSYRSYRSYRSYRSYRSYRSYR TWN TWN TWN TWN TWN TWN TWNTWN TWN TWN TWN TWNTWN TWNTWN TWN TWN TWN TWN

TJKTJKTJKTJKTJKTJKTJKTJKTJKTJKTJKTJK TJK TJK TJK TJKTJK TJK

TJKTZATZATZATZATZATZATZATZATZATZATZATZATZATZATZATZATZATZATZA THATHATHATHA THA THA THA THA THA THA THATHA THATHA

THA

THATHA THA THA

TLS TLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLSTLS TONTONTONTONTUNTUNTUNTUNTUNTUNTUNTUNTUNTONTUNTUNTUNTUNTUNTUNTONTONTONTUNTUNTONTONTONTUNTUNTONTONTONTTOTTOTTOTONTONTTO TTOTONTONTONTTOTTOTGOTGOTTO TTOTTOTTOTTOTGOTTOTGOTGOTGOTGOTGOTTOTGOTGOTGOTGOTGOTTOTGOTGOTTOTGOTGOTTOTGOTTOTTOTGOTURTURTUR TURTUR TUR TUR TUR TUR TUR TUR TUR TUR TUR TUR

TURTUR TURTUR

TKMTKMTKMTKMTKMTKMTKMTKMTKMTKMTKMTKMTKMTKM TKM TKMTKM TKM

TKMUKRUKRUKRUKR UGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGAUGA UKRUKR UKR UKR UKR UKR UKR UKR UKRUKR

UKR UKRUKRUKRUKR ARE

AREAREAREAREARE ARE ARE ARE AREAREAREARE

AREAREAREAREAREARE

GBRGBR GBRGBR

GBRGBR GBRGBRGBRGBRGBRGBRGBR

GBRGBRGBRGBRGBRGBR USA USA USA USAUSAUSA

USAUSA USAUSAUSAUSAUSAUSAUSAUSAUSAUSA

USA

URY URY URY URYURYURYURY URY URY URYURYURYURYURYURYURYURYURYURY UZBUZBUZBUZBUZBUZBUZBUZB UZBUZBUZBUZBUZBUZB UZB UZBUZB UZB

UZB VUTVUTVUTVUTVUTVUTVUTVUTVUTVUTVUTVENVUTVUTVUTVENZWEVENZWEVNMVNMVNMVENZWEVNMZWEVUTVUTZWEVUTVNMVUTZWEZWEVUTVENZWEZWEZWEZWEZWEZWEZWEVEN VENZWEZWEVENVENVNMZWEVENVENVENVENVENVENVNMVNMVNMVENVNMVNMVENVNMVNMZWEVNMVNMVNMZWEVNMVNMVNMVENVENZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBZMBYEMZMBYEMYEMYEMZMBYEMYEMZMBYEMYEMYEMYEMYEMYEMYEMYEMYEMYEMYEMYEMYEM

0

5

10

15

20

40 60 80 100

GINI Index (wealth distribution)

Wealth of billionares as a % of PPP GDP in 2018 Fitted values

ALB ALB ALB ALB

DZAARMARMARMARMARMARMARMARMARMARMARMARMAUSAUSARMARMARMARM ARGARGARGARGARGAGOARGARGARGARGARGARGARGARGARGARGAGOARG AUS AUS AUT AUT AUTAUT AUT AUTAUT AUTAUT AUT AUT AUT AUT AZE AZEAZE

AZEAZE BLRBLRBLRBLRBLRBLRBLRBLRBLRBLRBELBELBLRBLRBLRBLRBLRBLRBLRBGDBGDBGDBGD BEL BELBEL BELBEL BEL BEL BELBELBELBEL

BENBTNBEN BEN BTNBTN

BTN BOLBOLBOLBOLBOLBOLBOLBOL BOLBOL BOLBOLBOLBOLBOL BIHBIHBIHBIHBIH BRABRABRABRABWA BWA

BRA BRA BRA BRA BRA BRA BRA BRA BRA BRA BGRBGR BGRBGRBGRBFABGRBGRBGRBGR

BDI BDI CMRCMR CMR CANCAN CAN CANCAN CPV CPV CAF CAF

TCD TCD CHL

CHL CHLCHL CHL CHL CHL CHN CHN COL COL COL COLCOL COL COL COLCOL COL COL COL COL COL COL COM COM COD

COD COGCRICRICRICRICRICRICRICRICRICRICRICRICOGCRICRICRICRICRI CIVCIVCIV HRV HRV HRVHRV HRVHRV HRV CYPCYPCYP CYP CYP CYP CYP CYP CYP CYP CYP CYP CZE CZE CZE CZE CZE

CZECZECZE CZECZE CZE CZE DNK DNK DNK DNK DNK DNK DNKDNK

DNKDNKDNK DNK DNK

DJI DOMDJIDOMECUECUDJIDOMDOMECUECUECUDOMDOMECUDOMDOMECUDOMDOMECUECUDOMDOMDOMDOMDOMDOMDOMECUECUECUECUECUECU EGY EGYEGY EGYEGY SLV SLVSLV SLV SLVSLV SLV SLVSLVSLV SLV SLV SLVSLV SLV SLV SLV EST EST ESTEST ESTESTESTESTESTESTESTESTEST ETH ETH FJIFJI FJIETH FINFIN

FINFINFINFIN FINFINFIN FINFIN FINFIN FRA FRA FRA FRA

FRAFRAFRAFRAFRAFRA FRA FRA FRA

GAB GAB GMB GMB GMBGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEOGEO

DEU DEU DEU DEU DEU DEU DEUDEU DEU GHA GHA GRC GRC GRC GRC GRC GRC GRC GRC GRCGRC GRC GRCGRC GTMGTM GTM GIN GIN

GINGNB HTI HNDHNDHNDGNBHNDHNDHNDHNDHNDHNDHNDHNDHNDHNDHNDHND HUN HUN

HUN HUN HUN HUNHUNHUNHUNHUNHUNHUN ISL ISL ISL ISL ISL ISL ISL ISLISLISL ISL ISL IND IRNIRN IRN IRNIRN IRQIRQ IRL IRLIRL IRL IRL IRL IRL IRL IRL IRL IRL IRL IRL ISR ISR ISR ISR ISR ITA ITA ITA ITA ITAITAITAITAITA

ITA ITA ITAITA

JAM JAM JPNJORJORKAZKAZJORKAZJOR

KAZ KAZ KAZ KAZ KAZ KAZ KAZ KAZKAZ KAZ KAZ KAZ KEN KEN KIR KOR KOR KOR KOR

KOSKOSKOSKOSKOS KOSKOS

KOSKOSKOSKGZKGZKGZKOSKGZKGZKGZKGZKGZKGZKGZKGZKGZKGZLAO LAOKGZKGZLVAKGZLVALVALVALVALVALVALVALVALAOLVA LVALVAKGZ LBN

LSO LSO LBR

LBRLTULTULTULTULTULTULTU LTU LTULTULTULTU LUX

LUXLUXLUXLUXLUXLUX LUXLUXLUXLUXLUXLUX MKDMKDMKDMWIMDGMDGMKDMKDMDGMKDMWIMDG MYS MYS MYS MYS MYS MYS MDV MDVMLIMLI MLI

MLTMLTMLTMLTMLTMLTMLTMLTMLTMLTMRT MUSMRTMUSMRTMRT

MEX MEX MEXMEX MEX MEXMEX

MEXMEXMEX MEX FSM FSM MDAMDA MDA MDA MDAMDAMDA MDAMDA MDA MDA MDA MDA MDA MDAMDA

MDAMNEMNEMNEMNEMNEMNEMNEMNEMNGMNEMNGMNENPLMNGMNGMNGMNGMNG MMR NPLMOZMOZ MOZ NAMNAMNAM NLD

NLDNLDNLDNLD NLD NLD NLD NLDNLDNLDNLD

NIC NIC NIC NICNER NER

NER NER NGA NGA NORNORNOR

NOR NOR NOR NOR NOR NOR NOR NOR NOR

PAKPAKPAKPAK

PAKPAK PAKPAK PNG PERPERPRYPRYPRYPRY PRYPERPRYPERPERPERPERPANPERPERPANPRYPERPANPRYPRYPANPANPANPANPANPRYPRYPANPRYPRYPANPERPANPRY PRYPANPRYPANPANPANPANPAN PER PER PER PER PER PER PRTPRT PRT PRT PRT PRT PRTPRTPRTPRT PRT PRT PRT ROU ROU ROU ROU ROUROUROUROUROUROURUSRUS

RUSRUS RUSRUS RUS RUS RUS RUS RUS RUSRUS RUS RUS RUS RWA RWA RWA RWA WSM STP

STP SLE SENSLESENSEN SYC SVKSVK

SVK SVKSVNSVKSVKSVKSVKSVKSVKSVKSVK SVN SVN SVN

SVNSVNSVNSVNSVNSVNSVNSVN SLB SLB ZAF

ZAF ZAF

ZAF ZAF ESPESPESP

ESP ESP ESPESP ESP ESP ESPESP ESP ESP LKA LKA LKA LKALKA SDN SWESWE SWE SWE SWE SWE SWESWESWE

SWE SWE SWE SWE CHE CHE CHE CHE CHE CHE CHE CHE CHE CHE SYR TJKTJK TJK

TJK TJK TZA TZATZA THATHATHATHA THATHA THA THA THATHATHA THA

THA

TLS

TLSTLS TUNTON TUNTONTUN TURTGO TGOTGO TUR TUR TUR TUR TUR TUR TUR TUR TUR TUR TUR TURTUR TUR UGA UGAUGA UGAUGA UKR

UKRUKRUKR UKR UKR UKR UKR UKR UKR UKR UKR

UKRUKRUKR GBRGBRGBRGBRGBRGBRGBR GBR GBRGBRGBR

GBR

USAUSA USA USAUSAUSA

URYURY URYURY URY URY URYURYURYURY URY UZB

UZBUZBVUTYEMVNMVNMVNM VNMVNMVNMYEMVNMVNM ZMBZWE VENVENVENVENVENVEN ZMBZMBZMBZMB

0

5

10

15

20

20 30 40 50 60 70

GINI Index (World Bank Estimate)

13

There are at least two different types of income inequality, presented in the schema below: the

same Gini coefficients of income distribution can result from the concentration of inequalities at

the high end or the low end of the income pyramid. The graphical interpretation of the Gini

coefficient is the ratio of the area between the line of complete equality and the standard Lorenz

curve to the area of the shaded triangle.

In the first chart, the ABC triangle has about the same area as the ‘Lorenz curve–complete equality’ area – and the same Gini coefficient – but inequality in concentrated at the top end. So the 90% of the population at the poorer end of the income distribution are totally equal in their income among

themselves, but only account for 50% of total income, whereas the richest 10% have the other 50%

of total income; the per-capita income of the rich is exactly nine times higher than the per capita

income of the poor.8

In the second chart, the ABD triangle also has about the same area as the ‘Lorenz curve–complete equality’ area – and the same Gini coefficient – but inequality exists because the lower half of society has no income at all, and the other half has all the income.

The data seem to suggest that the first type of income distribution –‘90% poor and equal, 10% rich’ – is better for happiness than the second type.

14

Schema: Two types of inequality with the same Gini coefficient

0 10 20 30 40 50 60 70 80 90 100

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

S

h

ar

e

in

in

co

m

e

, %

Share of population, %

Complete equality among the poor, but high income of the few rich

Share in income - standard Lorenz curve

Complete equality

Share in income: 90% of poor have the same income

C B

0 10 20 30 40 50 60 70 80 90 100

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

S

h

ar

e

in

in

co

m

e

, %

Share of population, %

High inequalities between rich and poor

Share in income - standard Lorenz curve

Complete equality

Share in income: half rich-half poor

B

15

An explanation of the ‘inequality–happiness’ relationship in terms of statics (space – geography) and dynamics (time – history) could be the ‘big fish in a small pond’ effect. This is a model developed by Marsh and Parker (1984) to explain why good students prefer to stay in a class in

which they are above the average level, rather than be in a more challenging learning environment

where they are below the average level. This effect can be used to explain one of the paradoxes of

happiness: Strong growth is usually accompanied by growing income inequalities (Popov, 2018a,

fig. 10), so rapid growth is often associated with low happiness scores. A paper by Brockmann, Delhey, Welzel, and Hao (2008) refers to the concept of “frustrated achievers” and explains the decline in happiness scores in China through the deterioration of relative incomes for the majority

of the population due to rises in income inequality.

But there is a different relationship with regards to levels and change, stocks and flows, and space and time dimensions: with low levels of inequality people feel unhappy – the dream of the ‘big fish in a small pond’ is out of reach – but the transition to higher levels of inequality, when the relative position of the majority deteriorates in relation to the average, makes people even more

unhappy temporarily, during the transition. When transition to a higher level of inequality is over,

people – maybe new generations – start to feel happier.

The other explanation could be a different relationship between happiness and inequality in rich

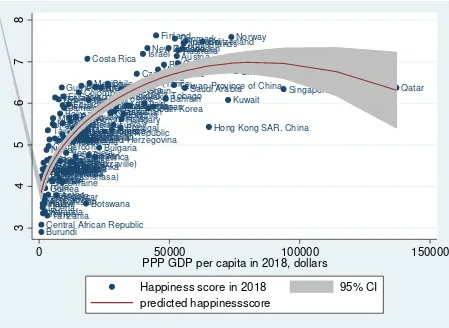

and poor countries. The dependence of happiness on income is characterised by a rising but

concave curve (fig. 14) that reaches its maximum at a level of income of about $75,000 (the level

of very rich Norway and Kuwait) and which increases only marginally after the income level of

about $30,000 (the level of the poorest OECD members – Greece, Chile, and Estonia). Whereas happiness index scores rise from 3 to 6 with a rise of PPP GDP per capita from less than $1,000 to

$30,000, they only increase from 6 to 7 when per-capita income rises from $30,000 to $75,000

16

Figure 15: Happiness index (Word Happiness Report and World Database on Happiness), 0-to-10 scale, and PPP GDP per capita in 2018, Dollars

Source: World Database on Happiness, 2019; WDI.

It may well be that in rich countries, the ‘money can’t buy happiness’ story is more true than in poor countries; i.e., a marginal increase in happiness due to a unit increase in income in rich

countries is lower than in poor countries.

First, for rich people, non-income determinants of happiness probably play a larger role, so the

negative effects of inequality are not counterweighted by higher incomes. Second, in rich countries, people derive pleasure from being better off than most of the world population – i.e., their ‘American dream’ has been achieved already – so inequality in their own country is less important and has only negative consequences.

Afghanistan Albania

Algeria

Angola

Argentina

Armenia

Australia Austria

Azerbaijan

Bahrain

Bangladesh Belarus

Belgium

Belize

Benin Bhutan Bolivia

Bosnia and Herzegovina

Botswana Brazil

Bulgaria Burkina Faso

Burundi Cambodia Cameroon

Canada

Central African Republic Chad

Chile

China Colombia

Congo (Brazzaville) Congo (Kinshasa)

Costa Rica

Croatia Cyprus

Czech Republic Denmark

Dominican Republic Ecuador

Egypt El Salvador

Estonia

Ethiopia

Finland

France

Gabon Georgia

Germany

Ghana

Greece Guatemala

Guinea Haiti

Honduras Hungary Hong Kong SAR, China Iceland

India Indonesia

Iran Iraq

Ireland Israel

Italy

Ivory Coast

Jamaica Japan

Jordan

Kazakhstan

Kenya Kosovo

Kuwait

Kyrgyzstan Laos

Latvia

Lebanon

Lesotho Liberia

Libya

Lithuania

Luxembourg

Macedonia

Madagascar Malawi

Malaysia

Mali

Malta

Mauritania

Mauritius Mexico

Moldova Mongolia

Montenegro Morocco

MozambiqueMyanmarNamibia Nepal

Netherlands New Zealand

Nicaragua

Niger Nigeria

Norway

Pakistan

Panama

Paraguay Peru Philippines

Poland

Portugal

Qatar Romania

Russia

Rwanda

Saudi Arabia

Senegal Serbia

Sierra Leone

Singapore Slovakia

Slovenia

South Africa

South Korea Spain

Sri Lanka Sudan

SwedenSwitzerland

Taiwan Province of China

Tajikistan

Tanzania

Thailand

Togo

Trinidad & Tobago

Tunisia

Turkey Turkmenistan

UgandaUkraine

United Arab Emirates United KingdomUnited States

Uruguay Uzbekistan

Venezuela Vietnam

Yemen Zambia

Zimbabwe

3

4

5

6

7

8

0 50000 100000 150000

PPP GDP per capita in 2018, dollars

Happiness score in 2018 95% CI

17

This paper uses the databases from the Forbes billionaires list and the Global Wealth Report

(GWR), as well as from the World Happiness Report and the World Database on Happiness. I use

the data to examine the relationship between income inequality, and happiness for nearly 20 years

(2000-18) for over 200 countries.

It turns out that inequality grows together with happiness in relatively poor countries, but harms happiness in rich countries. On the other hand, inequality of wealth distribution – wealth is a stock variable whereas income is a flow – is positively linked to happiness in all countries. Wealth distribution at the very top of the pyramid – billionaire and millionaire wealth as a proportion of GDP – is one of the most important determinants of happiness index scores in all countries.

The stylised fact is that there are two ‘typical’ statistical portraits of a happy country. One is of a country with relatively high income compared to the world average, a low level of income

inequality, but high wealth inequality and especially high wealth inequality at the very top – millionaire and billionaire intensity. This is very much the image of a Scandinavian country – high income compared to the rest of the world, low income inequality within the country, but pretty

high wealth inequality and billionaire intensity within the country. The other type of happy country

has lower levels of income, but high income and wealth inequalities, especially at the top of the

wealth pyramid. This is the Latin American and African model; e.g., Honduras, Bolivia, Ecuador,

Costa Rica, South Africa, and Zimbabwe.

Data

Income. Data on income are from the World Development Indicators database – purchasing power parity (PPP) GDP per capita.

Happiness. Data on happiness come from the World Happiness Report, as well as from the World Database on Happiness. This represents individuals’ self-perception of how happy they are. The scale is from 0 to 10, and the estimates are derived from the Gallup World Poll, the World Values

18

Income and wealth inequalities. Income inequalities data are from the World Development

Indicators database (WDI) and derived from national household surveys of income and

consumption in various countries. Wealth inequalities are computed through extrapolation: first,

regressions between the components of personal financial and non-financial wealth and its

determinants (real consumption; population density; market capitalisation rate; public pensions as

a percentage of GDP; domestic credits available to private sector; and Gini coefficient of income

distribution) are computed for about 40 countries for which these data are available, then an

extrapolation is made for countries that do not have estimates of these components of personal

wealth (Davies, Sandström, Shorrocks, and Wolff, 2007).

Wealth of high net worth individuals (HNWI) – billionaires and millionaires. Sample surveys

tend to omit HNWIs, so income and wealth distribution at the very top of the pyramid is very much

underestimated. That is why this paper uses the Forbes list of billionaires, which reports the wealth of all billionaires in the world since 1996 – see Popov (2018a) for details – and the Credit Suisse Global Wealth Report, which makes a number of adjustments to the Forbes data on billionaires

(GWD, 2018, pp. 110-113) and estimates the number and wealth of multi-millionaires,

millionaires, and other HNWIs.9

9This is how the estimation procedure is explained in the GWR: “We exploit the fact that the top tail of wealth distribution is usually well approximated by the Pareto distribution, which produces a straight-line graph when the logarithm of the number of persons above wealth level w is plotted against the logarithm of w. Our data yield a close fit to the Pareto distribution in the wealth range from USD 250,000 to USD 5 million. Above USD 5 million the relationship begins to break down, and the correspondence weakens further above USD 50 million, as expected given the limitations of the data sources. However, it still seems reasonable to use a fitted Pareto line to estimate the number of individuals in the highest echelons of the wealth distribution. To determine the precise features of the top wealth tail, we rely heavily on the rich list data provided by Forbes and other sources. We make particular use of the number of billionaires reported by Forbes, since the data are available for many years and are broadly comparable across countries. We recognize that rich list data have limitations. The valuations of individual wealth holdings are dominated by financial assets, especially equity holdings in public companies traded in international markets. For practical reasons, less attention is given to nonfinancial assets apart from major real estate holdings and trophy assets, such as expensive yachts. Even less is known – and hence recorded – about personal debts. Some people cooperate enthusiastically with those compiling the lists; others jealously guard their privacy. There are also different country listings for nationals and residents, which is especially evident for India, for instance. The true legal ownership within families – as opposed to nominal ownership or control – adds further complications. Assigning the wealth recorded for Bill Gates, for example, to all family members might well result in several billionaire holdings, so the number of billionaires would increase in this instance. In other cases, reassigning the family wealth would reduce all the individual holdings below the billionaire threshold. For all these reasons, rich list data should be treated with caution. At the same time, the broad patterns and trends are informative, and they

19

Forbes data show a higher ratio of billionaire wealth to GDP than the GWR data. For instance, for

Hong Kong, the comparison is 58% and 30% respectively. But overall, these two estimates are

[image:20.612.74.475.199.486.2]strongly correlated (fig. 16).

Figure 16: Billionaire intensity in percentage terms of PPP GDP according to the Forbes list and according to the Global Wealth Report

Afghanistan Albania Algeria

AngolaArgentina

Armenia

Australia Austria

Azerbaijan Bahrain Bangladesh

BelarusBelgium

Belize Benin Bhutan Bolivia

Bosnia and Herzegovina Botswana

Brazil

Bulgaria Burkina Faso Burundi Cambodia Cameroon

Canada

Central African Republic Chad

Chile

China Colombia Congo (Brazzaville) Congo (Kinshasa) Costa Rica Croatia

Cyprus

Czech Republic Denmark

Dominican Republic

EcuadorEgypt

El Salvador Estonia Ethiopia

Finland France

Gabon Georgia

Germany

GhanaGreece

Guatemala Guinea Haiti Honduras

Hong Kong SAR, China

Hungary

Iceland

India Indonesia Iran Iraq

Ireland Israel

Italy

Ivory Coast

JamaicaJapan

JordanKazakhstan

Kenya

KosovoKuwait

Kyrgyzstan Laos Latvia

Lebanon

Lesotho Liberia Libya Lithuania Luxembourg Macedonia Madagascar Malawi

Malaysia

Mali Malta Mauritania Mauritius

Mexico

Moldova Mongolia

MontenegroMorocco

Mozambique Myanmar Namibia

NepalNetherlands

New Zealand

Nicaragua Niger

Nigeria

Norway

Pakistan Panama

ParaguayPeru

Philippines

PolandPortugal

Qatar Romania

Russia

RwandaSaudi Arabia

Senegal Serbia Sierra Leone

Singapore

Slovakia Slovenia

South AfricaSouth Korea

Spain

Sri Lanka Sudan

Sweden

Switzerland

Taiwan Province of China

Tajikistan Tanzania

Thailand

Togo

Trinidad & Tobago Tunisia

Turkey Turkmenistan Uganda

UkraineUnited Arab Emirates

United Kingdom United States

Uruguay Uzbekistan Venezuela Vietnam Yemen Zambia Zimbabwe

0

20

40

60

0 10 20 30 40

20

Source: GWR; Forbes.

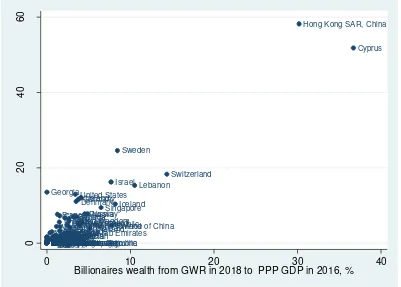

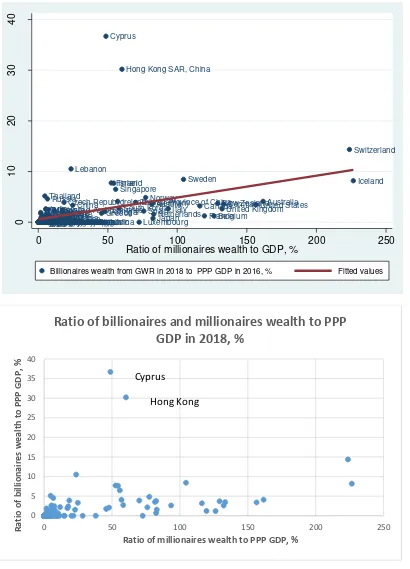

As figure 17 suggests, the ratio of millionaire wealth to GDP is correlated with the ratio of

billionaire wealth to GDP. However, data on the wealth of millionaires have the advantage of

including more countries. In 2018, there were only 24 countries, out of over 150, for which data

were available that did not have a single millionaire; in contrast the number of countries without

billionaires was nearly 100 out of over 150.

Suicide and murder rates. These data come from World Health Organization statistics on causes

of death.10 Murder rates statistics is also available from the UNODC (United Nations Office on

Drugs and Crime), which collects statistics mostly from WHO but from other sources as well.

10 External causes of death include murders, suicides, accidents, and ‘unidentified’. R² = 0.8933

0 10 20 30 40 50 60

0 5 10 15 20 25 30 35 40

B

il

li

o

n

ai

re

s

we

al

th

fr

o

m

Fo

rb

e

s

li

st

in

2018

to

PP

P

GDP

i

n

2016,

%

Billionaires wealth from GWR in 2018 to PPP GDP in 2016, %

Billionaires wealth as a % of PPP GDP according to Forbes list of billionaires and according to Global Wealth Report

Georgia

Hong Kong

21

Figure 17: Millionaire and billionaire intensity of PPP GDP according to the Global Wealth Report, percentage terms

Source: Global Wealth Report.

AfghanistanArmeniaAlgeriaAngolaArgentinaAlbania

Australia Austria

AzerbaijanBahrain

Bangladesh

BelarusBeninBhutanBotswanaBoliviaBosnia and HerzegovinaBelizeBulgariaBrazil Belgium

Burkina Faso

BurundiCameroonCambodia

Canada

Central African Republic

Chad Chile

China Colombia Congo (Brazzaville)

Congo (Kinshasa)CroatiaCosta Rica

Cyprus

Czech Republic Denmark

Dominican Republic Ecuador

Egypt

El SalvadorEstonia

Ethiopia

Finland

France

GabonGeorgia

Germany

Ghana

Greece Guatemala

GuineaHaitiHonduras

Hong Kong SAR, China

Hungary

Iceland

India Indonesia

IranIraq

Ireland Israel

Italy

Ivory CoastJordanJamaica Japan

Kazakhstan

KenyaKosovo

Kuwait

KyrgyzstanLaosLatvia

Lebanon

Lesotho

LiberiaMacedoniaLithuaniaLibya Luxembourg

Madagascar Malawi

Malaysia

Mali Malta

MauritaniaMongoliaMontenegroMoroccoMexicoMauritiusMoldova Mozambique

MyanmarNepalNamibia Netherlands

New Zealand

Nicaragua

NigerNigeria

Norway

PakistanParaguayPanama

Peru

PhilippinesPoland Portugal

Qatar Romania

Russia

RwandaSenegalSerbiaSaudi Arabia

Sierra Leone

Singapore

SlovakiaSouth AfricaSlovenia

South KoreaSpain

Sri Lanka Sudan

Sweden

Switzerland

Taiwan Province of China

Tajikistan Tanzania Thailand

TogoTrinidad & TobagoTunisia

Turkey Turkmenistan Uganda

UkraineUnited Arab Emirates United Kingdom

United States

Uruguay

UzbekistanVietnamYemenVenezuela

ZambiaZimbabwe

0

10

20

30

40

0 50 100 150 200 250

Ratio of millionaires wealth to GDP, %

Billionaires wealth from GWR in 2018 to PPP GDP in 2016, % Fitted values

0 5 10 15 20 25 30 35 40

0 50 100 150 200 250

R

atio

o

f b

il

li

o

n

ai

re

s

we

al

th

t

o

PPP

GDP

,

%

Ratio of millionaires wealth to PPP GDP, %

Ratio of billionaires and millionaires wealth to PPP

GDP in 2018, %

Cyprus