Interplay among credit, insurance and savings for farmers in

developing countries

Francesca de Nicola Ruth Vargas Hill Miguel Robles

International Food Policy Research Institute

March 30, 2012

Preliminary and incomplete

Abstract

Agricultural income in low income countries is subject to many risks, such as weather un-certainty, pests and disease. Much of this risk remains uninsured by existing risk management tools and this uninsured risk constraints investment. In this paper we examine the potential benefits of three financial products-weather index insurance, savings accounts, and insured agri-cultural loans-that could improve a household’s ability to manage agriagri-cultural risks to answer the question of what financial instruments do farmers really need? We develop and estimate a dynamic stochastic model that quantifies the impact of these three products on consumption, investment and welfare. The parameters of the model are calibrated with data from farmers in Ethiopia All three instruments offer welfare gains to farmers. The gains from index insurance and insured credit are particularly high, but basis risk mutes these gains. When basis risk is high the investment response to index insurance is weaker which results in lower consumption gains. Combined with higher consumption volatility, this results in lower welfare. However, we find that improved access to savings limits the negative effects of basis risk, suggesting that an approach that develops multiple financial instruments for farmers may be better than an approach focused on one instrument alone.

1

Introduction

In all countries, agricultural income is subject to many risks, such as weather uncertainty, pests and disease. The intensity of these risks is often higher in developing countries where many households derive a large share of their income from agricultural enterprises. Although farmers use assets, networks and informal credit to manage as much of this risk as they can, much of this risk remains uninsured. Without formal insurance, farmers have a number of strategies that help them manage risk. They run down assets or borrow in bad years and save or pay loans back in good years. They ask for help from a network of friends and family members in bad years, and help out those in their network in good years. However, these strategies are limited in their effectiveness in managing certain types of agricultural risk. A large shock, a shock that affects many farmers in one area (a covariate shock), or a series of repeated shocks in quick succession prove particularly difficult for households to insure. In these cases farmers reduce food consumption, take children out of school, sell-off productive assets and engage in risky income-earning activities. These have immediate and long-run welfare costs. These have deleterious long-run effects on welfare (Dercon(2004);Alderman, Hoddinott and Kinsey (2006);Burke, Gong and Jones (2011)). The cost of this uninsured risk on the welfare of farmers suggests that, were the right financial instruments available, farmers would be better off.

Additionally, uninsured risk discourages innovation and risk taking. Absent the special case of output risk that is positively correlated with consumption prices, theoretical work has shown that increases in risk reduce the scale of risky crop production (Sandmo(1971),Fafchamps(1992), Fafchamps and Kurosaki(2002)) as households limit their exposure to risk that they cannot insure against. Empirical studies have confirmed the predictions of these models: households with less insurance devote less land to high-yielding but volatile rice varieties and castor in India (Morduch (1990)); more land to low-risk and low-return potatoes in Tanzania (Dercon(1996)); and less labor to price-volatile coffee in Uganda (Hill (2009)). Walker and Ryan (1990) found that in semiarid areas of India, households may sacrifice up to 25% of their average incomes to reduce exposures to shocks.

The threat of shocks can also make households reluctant to access credit markets because they fear the consequences of an inability to repay (Carter, Cheng and Sarris(2011)). This in turn limits

a household’s ability to use costly inputs. In Ethiopia, households that are less able to manage income risk are less likely to apply fertilizer available on credit (Dercon and Christiaensen(2011)). This work suggests that reductions in risk, such as those that would result from an insurance contract or other financial products that allow households to manage agricultural risk, will increase investments that are susceptible to weather risk and result in welfare benefits. Evaluations of the impact of index insurance suggest this may be the case (Karlan et al. (2011), and Cole, Gin´e and Vickery (2011)) although the analysis of impacts has been hindered by limited take-up. In this paper we examine the question of what types of financial products will enable farmers to better insure yield risk, and yield higher returns as a result. We consider three commonly proposed financial products, and examine how they perform under standard assumptions. We also consider what happens when a combination of these products are available.

The three products we consider are weather index-insurance contracts, savings accounts, and lending by a bank that reinsures its agricultural loan portfolio to cover weather risk. There is a convincing rationale as to why each product could help farmers manage risk; and equally each product is also limited in the degree to which it is able to insure farmers.

Innovations in weather index insurance contracts have provided new insurance possibilities not provided by traditional indemnity insurance contracts. Under index insurance contracts payouts are based on an independently observable and verifiable index (such as weather at a local weather station) rather than an on-field assessment of farmer losses. As such, problems of adverse selection, moral hazard and costly loss assessment that have made indemnity insurance contracts prohibitively expensive for smallholder farmers (to the extent that these markets do not exist) are overcome, allowing insurance contracts insuring small plots of land to be sold (Skees, Hazell and Miranda (1999)). However, because the payout is based on the index and not on loss-assessment estimates, the farmer takes on basis risk in these contracts and may experience losses that are not indemnified. For this, and other reasons (such as high insurance premiums, liquidity constraints, lack of trust and poor understanding) take-up has been low. We also expect that the basis associated with these contracts will limit the gains resulting from them, although this has only been modeled inde Nicola (2010).

Index insurance can also be used by rural banks to help them manage the risk they hold by making agricultural loans. Higher rates of default are likely when production losses are realized

which makes lending to agriculture inherently risky. However, banks can purchase index insurance to insure this risk and guarantee to farmers that they will not ask for repayment when index insur-ance pays out. This type of scheme has been examined byMiranda and Gonzalez-Vega(2011) and an example is a weather index insurance policy that will be sold to rural microfinance institutions in Peru to help offset loan defaults and liquidity problems caused by El Ni˜no-induced excess rainfall (Skees and Collier (2010)). Evidence has suggested that in many contexts lending to agriculture currently includes excusable state-contingent default (see for example,Udry(1994),Gin´e and Yang (2009)) which is effectively priced into the cost of the loan contract. However in Ethiopia state-contingent default has not been widely practiced with default punished quite severely (Dercon and Christiaensen (2011)). This has resulted in a reluctance to take credit for the use of agricultural inputs. Offering a loan with excusable state-contingent default may thus be a means by which ac-cess to agricultural finance is increased for smallholder farmers. However, these schemes also have their challenges. Banks are also subject to basis risk and will have to engage in discussions with farmers to explain to them when debt is forgiven and when it is not. Banks may be concerned that conditional debt forgiveness will undermine a repayment culture. Although farmers will increase their access to credit and insure lending as a result of this scheme they will not be able to insure their livelihoods.

Savings may also allow an individual to better insure against risk, by allowing an individual to accumulate savings in good years and use these savings to cover uninsured losses. In fact, we may expect insurance and savings to be substitutes (Dionne and Eeckhoudt,1984). Savings and index-insurance, however, have somewhat different strengths and disadvantages in this context. Unlike index-insurance, savings can be used to insure farmers against covariate and idiosyncratic shocks. However, although savings may have a beneficial role, it is not clear how much given they are very expensive form of insurance against large shocks and are an ineffective means of insuring against shocks that occur in quick succession (Deaton and Paxson(1994)).

We set-up a dynamic stochastic optimization problem within the context of an agricultural household model in which these three risk management instruments are each made available in turn. A key feature of this model is that investments in agriculture are subject to multiple sources of risk, both idiosyncratic and covariate in nature, and that a large part of this uncertainty is covariate. This allows us to correctly model the basis risk inherent in some of the financial

innova-tions available. We numerically solve the optimization problem using calibrated parameters from Ethiopian household survey data to show the impact of each of these instruments on consumption, investment and welfare. We also consider what happens when more than one of these instruments is made available, and examine whether there are synergies among them (e.g. insurance and insured credit) or substitution (e.g. saving and insurance) and their combined effect on farmers’ choice.

We find that weather insurance increases investment in agricultural production and increases household consumption. As a result of both increased consumption and reduced consumption volatility, welfare gains to the household are positive. However, higher levels of basis risk mute the welfare gains from index insurance. Increased basis risk reduces the amount that households are willing to invest in agricultural production, and increases the resources that a household chooses to keep in risk-free assets instead. As a result consumption improvements are lower and welfare gains in short and long run are more muted for households at all wealth levels, but particularly for the poorest.

Improved access to savings is also welfare increasing, however under this scenario welfare gains come largely from increased consumption, rather than substantial reductions in consumption volatil-ity. When availed with a high return savings instrument, farmers reduce their investment in agri-cultural production switching resources into the higher return savings account instead. We also find that, when offered with index insurance, savings enables households to increase their welfare gains in the presence of substantial basis risk. This is because savings can be used to help farmers manage the basis risk associated with the index insurance product. Finally, we show that insured credit for agricultural production can also be used as a form of insurance by avoiding repayment in case of negative shocks.

The paper proceeds as follows, in the following section we set-out the model used, in Section 3 we present the Ethiopian data set used in calibrating the model. In Section 4 we present and discuss the results and in Section5 we conclude.

2

Model

We construct a dynamic model of farmers in developing countries facing aggregate weather risks and idiosyncratic shocks, in order to characterize their consumption and investment decisions and

the relative welfare levels.

2.1 Baseline scenario

We first present a “baseline” model that captures the living conditions of Ethiopian farmers, in the absence of financial markets. In each period a farming household decides how much of their resources to consume,ci,t, how much to keep in assets,ai,t, and how much to invest in agricultural inputs, ki,t from which farm income in the following period,wi,t+1, is derived.

The household is assumed to have limited asset options available to them; as such the resources invested in assets have zero return. However, we assume that these assets are riskless. We could think of these assets as being grain kept in store, or cash kept under the bed (in both cases assuming minimal crop losses and inflation rates respectively).

The household earns farm income according to a production function with decreasing marginal returns. There are two inputs to this production function, agricultural inputs, ki,t and labor li,t. Furthermore there are two multiplicative shocks to the production function: a covariate shock

ηt+1 whose realization is unknown to farmers at the time the investment decision is made, and

an idiosyncratic shock to farmers’ productivity, i,t+1, also unknown to farmers at the time the

investment decision is made. We can think of the covariate shock as a weather shock whose realization is unknown at the time of investment in seeds and fertilizer; and the idiosyncratic shock as a health shock.

The presence of multiple uninsured risks is an important feature of many rural settings, where informal insurance markets, although better at insuring idiosyncratic rather than covariate shocks, do not perfectly insure idiosyncratic risk. These multiple sources of uninsured risks influence in-vestment decisions and lower welfare. This feature of the environment will have an effect on the utility of the instruments considered. It is also important that we think of these shocks as multi-plicative. Shocks that affect agricultural profits are highly unlikely to enter as additive independent terms. This is because if a household loses its crop from drought, it cannot lose it again due to labor constraints resulting from ill-health. It is also not reasonable to assume that you can lose your entire crop only if every shock occurs to its maximum possible extent. As such it is more appropriate to model agricultural losses as multiplicative (Clarke et al.(2012)).

The household’s income in period t+ 1,wi,t+1 is going to be given as follows:

wi,t+1=Aii,t+1ki,tαl1

−α

i,t ηt+1+ai,t

whereAi is an individual-specific time-invariant productivity coefficient.

The idiosyncratic terms, Ai and i,t+1, are both log-normally distributed with mean 1 and

variance, respectively, of σA2, and σ2. The distribution of the weather shock, ηt+1, is empirically

calibrated from the data as discussed in Section3.

The household maximizes the expected present discounted value of consumptionEtP∞j=0βju(ci,t+j) where u(ci,t) =

c1i,t−ρ

1−ρ is a constant relative risk-aversion (CRRA) utility function with a coefficient of relative risk aversion ρ.

The household’s optimization problem can thus be written as:

V(wi,t) = max ki,t≥0

[u(ci,t) +βEtV(wi,t+1)]

wi,t = ci,t+ai,t+ki,t (1)

wi,t+1 = Aii,t+1ki,tαl1

−α

i,t ηt+1+ai,t

The first-order conditions are computed by equating the marginal utility of consumption today to the expected discounted marginal utility of consumption tomorrow:

u0(ci,t) = βEt[u0(ci,t+1)αAii,t+1ki,tα−1ηt+1]

u0(ci,t) = βSEt[u0(ci,t+1)]

(2)

Solving for Equation 2 allows us to derive the finite target level of wealth towards which the household will converge, it corresponds to the level of wealth in the tth period that corresponds to the expected amount in the following period tth+ 1. It plays an important role in the analysis, since the calculation of the welfare gains from the different interventions are based on it.

The scope of the paper is to investigate the qualitative impact of the provision of index insurance, improved savings and insured credit on consumption, investment and welfare for farmers. We thus

incorporate these financial instruments in our theoretical framework. For clarity, we introduce one element at the time

2.2 A market for weather insurance

Now, we assume that a well-functioning market for weather insurance has been established. This market for weather insurance allows the household to insure against the covariate shock ηt+1 that

affects their production income. However, as discussed in the introduction, it is unlikely that the weather insurance product will insure households perfectly against ηt+1. These design limitations

will lead to a source of basis risk, which means that not all of the covariate shock will be covered. Two recent theoretical papers -Clarke (2011) and de Nicola (2010)- have furthered our under-standing of the nature of demand for index insurance. Each paper models basis risk differently, but importantly they both treat it as quite different from the additive background risk that is present in models of demand for indemnity insurance in which the uninsured losses are entirely independent of the insured event. We use the framework set-up by de Nicola(2010) because de Nicola’s model highlights an important insight for the context we are considering. For an agricultural household, all non-insured shocks to agricultural production-even health shocks to the labor a household can allocate to crop production-are multiplicative and as such if farmers can purchase only weather insurance, even if it insured perfectly against the covariate source of risk, they would not fully insure.

This framework allows us to consider both the design issues associated with the contract and the fact that, however well designed, a contract designed to insure covariate sources of yield risk will not insure farmers against idiosyncratic shocks such as health shocks that constrain the supply of labor to agricultural production in a given season. The take-up and welfare impact of insurance is limited by design imperfections, but also by these other uninsured sources of non-covariate risk. We denote basis risk as ξt+1 and assume that it is lognormally distributed with mean one and

standard deviation, σξ. The idiosyncratic source of risk, i,t+1, is left entirely uninsured by this

insurance product, and this will be another source of basis risk to the household, as ultimately they would like to insure the risk to their crop production income.

A household can buy multiple units of weather insurance. The actuarially fair price of each unit is given as Pt =R1

multiple,θ≥1, above its actuarially fair price, in order to cover the costs of marketing the product, and of transferring some risk to international markets.

The decision problem for the household thus becomes:

V(wi,t) = max kit,ιi,t≥0

[u(ci,t) +βEtV(wi,t+1)]

wi,t = ci,t+ai,t+ki,t (3)

wi,t+1 = Aii,t+1ki,tαηt+1+ai,t+ιi,t((1−ηt+1)ξt+1− Pt(1 +θ))

whereιi,t are the number of units of weather insurance the household decides to purchase.

If θand σξ are zero, and farmers can observe the realization of their idiosyncratic productivity before deciding how much insurance to purchase, i.e. if the insurance contract is actuarially fair priced and abstracts from basis risks, farmers are fully insured and optimally setιi,t =Aii,t+1ki,tα.1 However, it is no longer optimal to be fully insured as soon as one of these three conditions fails to hold, and numerical solutions need to be found to determine the optimal amount of weather insurance that a farmer will purchase, ιi,t.

2.3 Better savings instruments

Currently, households have access to risk-less assets that allow them to save income in one period and transfer it to future periods. However, these assets have zero return. Our second financial intervention is improved access for farmers to savings accounts that allow them to save money in one period for positive return in future periods should improve their welfare. Incentivizing saving may also allow the household to better smooth income shocks from one period to another. However, as discussed in the introduction, savings will always be limited in this regard.

We formally model the introduction of improved savings instruments, by introducing a positive return, S, on resources held as assets, ai,t:

V(wi,t) = max ki,t,ai,t≥0

[u(ci,t) +βEtV(wi,t+1)]

wi,t = ci,t+ki,t+ai,t (4)

1

Seede Nicola(2010) for a detailed analysis of the impact on consumption, investment and welfare of actuarially-fair basis-risk-free weather insurance. The qualitative results apply also to the current context, even though the analysis inde Nicola(2010) is based on data from Malawi.

wi,t+1 = Aii,t+1ki,tαl1i,t−αηt+1+Sai,t

When deciding the optimal allocation of capital, farmers will balance two contrasting effects. On the one hand, the marginal productivity of capital of agricultural production is inversely pro-portional to the amount of resources invested, thus at low level of capital farmers may invest more in agricultural production and less in the safe asset that yields a lower return. On the other hand, farmers wants to invest in the safer asset that guarantees a constant return in order to protect their future consumption from the higher income volatility that would derive from investing all their resources in more productive but riskier technology.

2.4 Lending for agricultural investment

Finally, we consider the effects of providing access to formal credit for financing capital investments in production. Typically banks are reluctant to lend to agricultural investments, given the high level of risk they are perceived to hold as a result of production shocks. We therefore assume that access to lending for agricultural investment is undertaken by the bank only when the bank is able to insure their loan portfolio against production shocks experienced by the farmer. The loan that the farmer receives is one in which default is allowed when a shock is experienced. This default risk is priced into the loan offered by the bank through the interest rate, and is insured by the bank purchasing insurance for the portfolio of agricultural lending products it offers. We assume, for now, that the bank is able to observe both the covariate and idiosyncratic shock. However, in future work we will want to revise this assumption so that the bank only has access to the same covariate index and insurance as the farmer (but at a lower unit price given the larger scale of contract it purchases).

Farmers borrow di,t to finance capital expenditure. We allow farmers to default on their credit when hit by a severe shock, that is:

wi,t+1=

Aii,t+1ki,tαηt+1−Rbdi,t, ifi,t+1 >˜i,t and ηt+1 >η˜t+1; Aii,t+1ki,tαηt+1, otherwise.

where ˜ηt+1 is the extreme weather event and ˜i,t+1 is the extreme idiosyncratic event that triggers

to default, that isRb =R(1−d), whered corresponds to the probability of default.

3

Data and Calibration

We need to pin down the parameters of the model in order to numerically solve the model and show the impact of insurance, credit and savings on farmers’ allocation of resources between consumption and investment and ultimately quantify the impact on welfare of these financial assets. In particular, the value of β,ρ,α, andS, and the parameters of the distribution of andη are required to solve the “baseline” framework, and the value ofRand the parameters of the distribution ofξ, in order to solve the other frameworks.

Table 1: Calibrated Parameters

Parameters Value Parameters Value

CRRA coefficient, ρ 3.9 Interest rate on savings, S 0 (3)%

Discount factor, β 0.96 Capital share, α 0.39

Interest rate on debt, R 30% SD of idiosyncratic shock,σ 80%ση

Loading factor, θ 0.5 Design effect 70%ση

Distribution of weather shock Empirical distribution from LEAP

The selected values are summarized in Table 1 and are based on household survey data to pin the main parameters of the model and meteorological and agroecological data to estimate the weather shock. In particular, we use the Ethiopian Rural Household Survey (ERHS), a multipurpose panel survey of approximately 1,400 households located in 15 Ethiopian villages that have been interviewed seven times since 1994. While these data are not nationally representative, the survey included the main agroclimatic zones of the country. Each round collected data on demographic characteristics, assets, occupation, cropping patterns, nonagricultural income, consumption, and experiences with shocks.

The 2009 survey round included specialized modules on risk and time preferences that allow us to compute the coefficient of relative risk aversion and the discount factor. The former, ρ, is computed from the choices of farmers among a series of lotteries with real (monetary) payouts `a

equating the expected utility from the different gambles, we calculate the upper and lower bounds for the true value ofρ, and then take the average of the median value for each interval. The point estimate is 3.9 indicating that farmers are risk averse. Time preferences were elicited by asking individuals to consider a situation in which they were about to receive a gift. They could choose to receive the gift of ETB 100 today or could instead choose to receive a gift of ETB 100 +X

one month from now, where X was increased by ETB 25 up to the point at which the household chose to wait. The discount rate,β, is calculated using the information on how much an individual requires to be paid to choose to wait. Specificallyβ is computed as 1

1+100+100X−100 = 100

100+X and is on average 0.6, consistent with estimates from other developing country (Duflo, Kremer and Robinson (2011)). Such low level of discount rate suggests that farmers tend to be present biased which may lead to underestimate the benefits of future policy interventions.

The production function parameter, α, is set at 0.39 which is the coefficient from regressing the agricultural output (in logs) on the value of agricultural inputs (also in logs). The interest rate on savings, S, is is given as 3%. This assumption is potentially generous in that real interest rates could actually be negative because of the double-digits inflation rate that Ethiopia experienced in the past. The Commercial Bank of Ethiopia offers savings account accruing 5.5% interest rates on deposits. However, according the World Bank estimates, the inflation rate is more than 20% in 2011 increasing from the 8% level in 2009 and 2010. Thus assuming a 3% interest rate, if anything, could overestimates the value of savings.

The interest rate on debt, R, is calculated as the average value farmers pay on loans from a formal source such as the Commercial Bank of Ethiopia, a private bank, or microfinance institution. The distribution of the weather shock, η, is approximated using the LEAP (Livelihoods, Early Assessment and Protection) software estimating the sensitivity of crop production across Ethiopia to changes in rainfall.2 These calculations are based on (i) the rainfall data, i.e. the 10-day

Africa estimates from 1995 onwards obtained from the US Climate Prediction Center, and (ii) the agroecological information of Ethiopia’s main staple crops simulating the growth and crop water requirements during the growing season. The calculation are based on the methodology developed by the FAO and provide estimates of yield changes due to moisture stress. We match the meteorological data with the location of the ERHS farmers and the agroecological data with

2

the crops typically grown. From the ERHS, we see that the principal crops varied by location. The idiosyncratic shock is assumed to be lognormally distributed with mean one and standard deviation σ. If σ is zero, then farm income is exposed only to weather shocks. However, house-holds report suffering also from other shocks. Beyond droughts househouse-holds cite pest infestations, death, and illness as serious shocks experienced in the past years.3 We therefore account also for idiosyncratic shocks and assume a non-zero σ. We fix it at a lower level than ση (σ = 0.8ση) to reflect the fact that these shocks are less frequently reported.

Figure 1 plots the distribution of the two shocks. The weather shock is normalized to be distributed between zero and one, where zero corresponds to the most disruptive event, either a drought or a flood. The idiosyncratic shock has positive support, taking values between 0.5 and 1.5.

Finally, in the theory section we allowed for the fact that the index contract may not be designed to perfectly insure the covariate shock. In the simulations that follow we look at the impact of index insurance under two scenarios regarding this design problem. Under one scenario we assume that there is no design problem and that the covariate shock is perfectly insured by the index. In this scenario the only source of basis risk results from the presence of the idiosyncratic shock to production. In the second scenario we assume that the design problem results in σξ = 0.7ση which results in a correlation between losses and payout of 0.8. This correlation between losses and payouts reflects analysis conducted in an ongoing IFPRI pilot study on the degree to which insurance contracts designed in the pilot study were able to insure droughts reported by farmers over the last 25 years.

4

Results

Under the benchmark calibration (Table 1), we solve the optimization problem (1) and compute the optimal consumption and investment decisions in the absence of functioning financial markets. Extremely poor farmers invest all their resources in the risky farm investment, kt, because the higher returns to capital compensate the larger volatility that farmers expose themselves to. As households become richer, they substantially increase the amount of resources to the risk-free asset,

3In the questionnaire, the shock is referred to as “an event that led to a serious reduction in your asset holdings,

at.

In this context, we introduce one financial instrument at a time and evaluate its impact on average wealth, consumption, farm-investment and investment in the risk-free asset over time. Finally, we examine the welfare gains that farmers may achieve depending on their level of wealth and on the time the policy change was introduced.

First, we study the effect of providing weather index insurance. In developed markets index insurance is priced at a low multiple above the actuarially fair price. For example the multiple of unsubsidized index insurance in the US is about 1.11 (Deng et al 2007). However in markets where index insurance is newer, such as India, the multiple can range from 1.8 to 4.5 (Cole et al 2009). A more subtle concern regards the presence of basis risk whereby the insurance payout is not perfectly correlated with the farmers’ losses, both as a result of the idiosyncratic shock and as a result of a design effect which causes the index to imperfectly predict covariate weather shocks.

We incorporate both these aspects in our analysis and in Figure2we plot the impulse response functions from the introduction at time t∗ of weather insurance. We show the impact of insurance on the amount of capital invested in farm production (kt), the level of risk-free assets held (at), the consumption of the household (ct) and the income earned by the household (wt). The simulations are initialized at the target level of wealth derived under the “baseline” scenario, and setting idiosyncratic and weather shocks to their mean values in order to better capture the effect of the policy intervention.4 The squares indicate the impact of providing households with the opportunity to buy a weather insurance that is perfectly correlated with the covariate shock, and the circles indicate the impact of providing households with the opportunity to buy weather index insurance that has a correlation of 0.8 with losses from the covariate shock. Both contracts are priced at 1.5 times the actuarially fair price.

The impact on consumption and investment, both in risky and risk-free assets, are qualitatively similar, irrespective of the level of basis risk. The availability of insurance allows farmers to more effectively shield themselves against the covariant shock and therefore weakens the precautionary motives that led to over investment in the safe asset. This is well captured by the initial fall in at, and the increased investment inkt. The fall in at is larger among richer farmers that were overinvesting a larger amount of resources in order to protect themselves against weather variations.

4

Investing in the more productive technology, farmers earn higher income and are able to sustain a higher level of consumption over time and across all level of wealth.

When basis risk is increased due to a fall in the correlation between losses and payouts from 1 to 0.8, the change in at and ktis muted: the fall in at is reduced and the increase in kt is smaller. Because this weather insurance contract is less effective it produces a smaller contraction of the precautionary motives that lead farmers to accumulate unproductive assets.

This is reflected in the welfare gains that are defined as the permanent increase in consumption that would make farmers without weather insurance equally well off as farmers with weather

insur-ance. Formally, they correspond to theχtsuch thatEtP∞j=0βju(c“baseline”t+j (1 +χt)) =EtP∞j=0βju(c“insurance”t+j ).5 As expected, welfare gains are higher when basis risk is lower. They are also larger at low levels of

wealth since poorer households benefit the most from improving the risk-coping mechanism used against covariant shocks.

The dynamic structure of the model allows us to look at how the welfare gains change across time. We find that the welfare gains from the introduction of weather insurance are increasing over time. This is because the more efficient allocation of resources brought about by weather insurance allows farmers to enjoy higher and less volatile consumption over time.

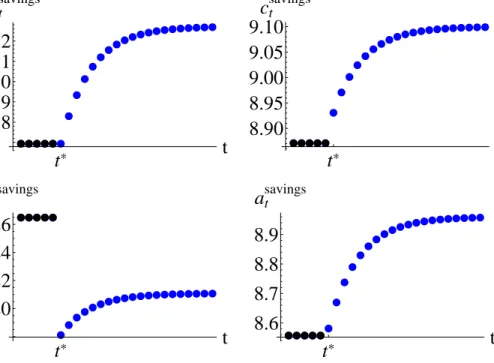

Farmers can alternatively shield their consumption from negative shocks by putting money in a savings account earning a positive constant rate of return, S. Such a fund can be used to insure against both covariant and idiosyncratic shocks.

In Figure3, we plot the impulse response functions from the sudden and unexpected provision of saving accounts. Farmers increase the investment in the risk-free asset at that now earns a 3% return. The initial increase in at is financed by reducing the investment in farm inputs, kt. After the initial contraction, the investment in risky assets gradually increases and levels off at a level lower than the initial steady state. The fall in farm income is more than compensated by the increase in off-farm income that allows farmers to enjoy higher consumption.

In contrast to the case of weather insurance, the welfare gains are an increasing function of wealth. Richer farmers are able to invest more in at and are therefore also extracting larger benefits. Similarly to the case of weather insurance, we find that welfare gains are increasing over

5Given the properties of the CRRA utility function, this expression can be solved by taking the ratio of the respective

time.

When weather insurance is combined with the provision of savings accounts, we observe that the impulse response functions mimic those from the provision of weather insurance alone (Figure

??), thus farmers react by initially cutting at despite its higher return. However, we also find that the provision of savings accounts improves farmers’ ability to cope with the basis risk associated with these contracts. As such the impact of increased basis risk on lowering investments in farm inputs is less pronounced when savings are present. In turn this results in consumption levels being less affected by basis risk which increases welfare gains. Poorer farmers benefit the most from the joint provision of weather insurance and savings.

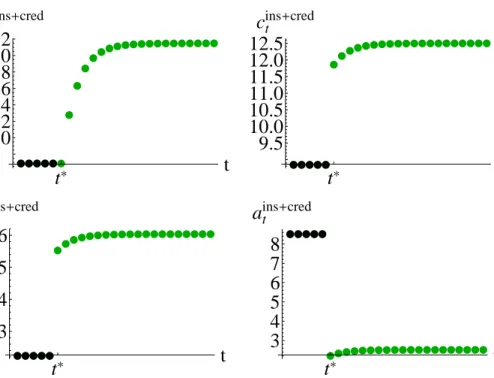

Finally, in Figure5we plot the impulse response functions from the supply of weather insurance, savings and insured credit. As mentioned in Section 2, insured credit allows farmers to take a loan and receive debt forgiveness for their loan if they are hit by the worst idiosyncratic or covariant shock. Such a generous credit contract allows farmers to substantially cut savings, at and redirect their investment to farm inputs. At the same time, farmers are able to increase their level of consumption which remains at a stable higher level over time. The combination of weather insurance, insured credit and savings accounts translates into high welfare gains, especially at low levels of wealth where farmers not only benefit from the insurance but also from the additional resources available to finance agricultural investment and grow faster.

5

Conclusions

Farmers in low income countries are cultivating under high levels of uninsured risk. As a result much work over the last decade has looked at the question of how to develop financial products that farmers can use to insure some of this risk. Innovations in weather index insurance, insured credit and savings accounts for smallholder farmers, offer considerable promise. However, much of the analysis has looked at these products in isolation, making it difficult to answer the question of which financial product may prove more useful to farmers under which settings, and also what the complementarity and substitution between products might look like. In this paper we have exam-ined the potential benefits of three financial products-weather index insurance, savings accounts, and insured agricultural loans-to explore these questions. We developed and estimated a dynamic

stochastic model that quantifies the impact of these three products on consumption, investment and welfare. We calibrated the model with data from farmers in Ethiopia. Under the assumptions of our model all three instruments offer welfare gains to farmers. The gains from index insurance and insured credit are particularly high.

We also find that basis risk mutes the gains from index insurance. As such the degree to which index insurance is a useful tool for smallholder farmers depends on the level of basis risk that is present. Basis risk results both from the inadequacy of the index to insure the covariate shock and the fact that farmers face multiple sources of uninsured risk, some of which is idiosyncratic in nature and cannot be insured by an indexed insurance instrument.

However, we find that improved access to savings limits the negative effects of basis risk, sug-gesting that an approach that develops multiple financial instruments for farmers may be better than an approach focused on one instrument alone.

A

Figures

0 2 4 6 8 Density 0 .5 1 1.5 Weather shock Idiosyncratic shockèèèèèè è èè èèè èèèèèèèèèèèèè ä ä ä ä ä ä ä ää ää ä ä ä ä ä ää ä ä ä ä ä ä ä èèèèè t* t 20 22 24 26 28 wtinsurance èèèèèè è èè èèèèè èèèèèèèèèèè ä ä ä ä ä ä ä ää ä ää ä ä ä ä ä ä ä ä ä ä ä ä ä èèèèè t* t 9.5 10.0 10.5 11.0 11.5 12.0 ctinsurance èèèèè è èè èèè èèèèèèèèèèèèèè ä ä ä ä ä ä ää ää ä ä ä ä ää ä ä ä ä ä ä ä ä ä èèèèè t* t 2.5 3.0 3.5 ktinsurance èèèèè èè èèèèè èèèèèèèèèèèèè ä ä ä ä ä ää ä ää ä ä ä ä ä ä ä ä ä ä ä ä ä ä ä èèèèè t* t 4 6 8 10 12 atinsurance

Figure 2: Impulse response functions of wealth, consumption and investment to the introduction of weather insurance. Squares indicates that weather insurance abstracts from basis risk, circles indicates it does not

èèèèèè

è

è

è

èè

èèè

èèèèèèèèèèè

èèèèè

t

*t

19.8

19.9

20.0

20.1

20.2

w

t savingsèèèèè

è

è

è

èè

èèè

èèèèèèèèèèèè

èèèèè

t

*t

8.90

8.95

9.00

9.05

9.10

c

t savingsèèèèè

èè

èèè

èèèèèèèèèèèèèèè

èèèèè

t

*t

2.20

2.22

2.24

2.26

k

tsavingsèèèèèè

è

è

è

èè

èèè

èèèèèèèèèèè

èèèèè

t

*t

8.6

8.7

8.8

8.9

a

tsavingsFigure 3: Impulse response functions of wealth, consumption and investment to the introduction of savings

èèèèèè

è

è

è

èè

èèèè

èèèèèèèèèè

ääääää

ä

ä

ä

ää

ääää

ääääääääää

èèèèè

t

*t

20

22

24

26

28

w

t insurance+savingsèèèèè

è

è

è

èè

èèè

èèèèèèèèèèèè

äääää

ä

ä

ä

ä

ää

ääää

ääääääääää

èèèèè

t

*t

9.5

10.0

10.5

11.0

11.5

12.0

c

t insurance+savingsèèèèè

è

è

è

èè

èèèèèè

èèèèèèèèè

äääää

ä

ä

ä

ää

äää

ääääääääääää

èèèèè

t

*t

2.4

2.6

2.8

3.0

3.2

3.4

k

tinsurance+savingsèèèèè

è

è

è

è

èè

èèè

èèèèèèèèèèè

äääää

ä

ä

ä

ä

ää

ääää

ääääääääää

èèèèè

t

*t

9

10

11

12

13

a

tinsuranceFigure 4: Impulse response functions of wealth, consumption and investment to the introduction of savings and weather insurance. Squares indicates that weather insurance abstracts from basis risk, circles indicates it does not

èèèèèè

è

è

èè

èèèèèèèèèèèèèèè

èèèèè

t

*t

20.0

20.2

20.4

20.6

20.8

21.0

21.2

w

t ins+credèèèèè

èè

èèèèèèèèèèèèèèèèèè

èèèèè

t

*t

9.5

10.0

10.5

11.0

11.5

12.0

12.5

c

tins+credèèèèè

èèè

èèèèèèèèèèèèèèèèè

èèèèè

t

*t

3

4

5

6

k

tins+credèèèèè

èèèèèèèèèèèèèèèèèèèè

èèèèè

t

*t

3

4

5

6

7

8

a

tins+credFigure 5: Impulse response functions of wealth, consumption and investment to the introduction of insured credit, weather insurance and savings

References

Alderman, H., J. Hoddinott, and B. Kinsey. 2006. “Long term consequences of early

child-hood malnutrition.” Oxford Economic Papers, 58(3): 450–474.

Binswanger, H.P. 1981. “Attitudes toward risk: Theoretical implications of an experiment in

rural India.”The Economic Journal, 91(364): 867–890.

Burke, M., E. Gong, and K. Jones. 2011. “Income Shocks and HIV in Sub-Saharan Africa.”

IFPRI discussion papers.

Carter, M.R., L. Cheng, and A. Sarris. 2011. “The Impact of Inter-linked Index Insurance

and Credit Contracts on Financial Market Deepening and Small Farm Productivity.”

Clarke, D.J. 2011. “A Theory of Rational Demand for Index Insurance.” Insurance Design for

Developing Countries, D. Phil. Thesis, University of Oxford.

Clarke, D.J., N. Das, F. de Nicola, R.V. Hill, N. Kumar, and P. Mehta. 2012. “The

value of (customized) insurance for farmers in rural Bangladesh.”

Cole, S., X. Gin´e, and J. Vickery. 2011. “How Does Risk Management Influence Production

Decisions? Evidence from a Field Experiment.” mimeo.

Deaton, A., and C. Paxson.1994. “Intertemporal Choice and Inequality.” Journal of Political

Economy, 437–467.

de Nicola, F.2010. “The impact of weather insurance on consumption, investment, and welfare.”

Dercon, S. 1996. “Risk, Crop Choice, and Savings: Evidence from Tanzania.” Economic

Devel-opment and Cultural Change, 44(3): 485–513.

Dercon, S. 2004. “Growth and shocks: evidence from rural Ethiopia.” Journal of Development

Economics, 74(2): 309–329.

Dercon, S., and L. Christiaensen.2011. “Consumption risk, technology adoption and poverty

Dionne, G., and L. Eeckhoudt.1984. “Insurance and saving: some further results.”Insurance: Mathematics and Economics, 3(2): 101–110.

Duflo, E., M. Kremer, and J. Robinson. 2011. “Nudging Farmers to Use Fertilizer: Theory

and Experimental Evidence from Kenya.”The American Economic Review, 101(6): 2350–2390.

Fafchamps, M. 1992. “Cash crop production, food price volatility, and rural market integration

in the third world.”American Journal of Agricultural Economics, 74(1): 90–99.

Fafchamps, M., and T. Kurosaki. 2002. “Insurance Market Efficiency and Crop Choices in

Pakistan.” Journal of Development Economics, 67(2): 419–453.

Gin´e, X., and D. Yang.2009. “Insurance, Credit, and Technology Adoption: Field experimental

Evidence from Malawi.” Journal of Development Economics, 89(1): 1–11.

Hill, R.V. 2009. “Using stated preferences and beliefs to identify the impact of risk on poor

households.” The Journal of Development Studies, 45(2): 151–171.

Karlan, D., I. Osei-Akoto, R. Osei, and C. Udry. 2011. “Examining underinvestment in

agriculture: Measuring returns to capital and insurance.” Mimeo, Yale University.

Miranda, M.J., and C. Gonzalez-Vega. 2011. “Systemic risk, index insurance, and optimal

management of agricultural loan portfolios in developing countries.” American Journal of Agri-cultural Economics, 93(2): 399–406.

Morduch, J.1990. “Risk, Production and Saving: Theory and Evidence from Indian Households.”

Harvard University, Manuscript.

Sandmo, A.1971. “On the theory of the competitive firm under price uncertainty.”The American

Economic Review, 61(1): 65–73.

Skees, J., P.B.R. Hazell, and M. Miranda.1999. “New approaches to crop yield insurance in

developing countries.” EPTD discussion papers.

Skees, J.R., and B. Collier. 2010. “New approaches for index insurance.”2020 Vision Briefs.

Udry, C.1994. “Risk and insurance in a rural credit market: An empirical investigation in northern Nigeria.” The Review of Economic Studies, 61(3): 495–526.

Walker, T.S., and J.G. Ryan. 1990. “Village and Household Economies in India’s Semi-Arid Tropics.”