JBE

Code of Ethics and Rules on Corporate Behaviour.

Some Insights from the Italian Context.

Katia Furlotti

Researcher in Business Economics

Faculty of Economics – University of Parma Via J.F. Kennedy, 6 – 43100 Parma, Italy Tel. 0039 0521 03 2503

E-mail: [email protected]

Pier Luigi Marchini

Researcher in Business Economics

Faculty of Economics – University of Parma Via J.F. Kennedy, 6 – 43100 Parma, Italy Tel. 0039 0521 03 2389

E-mail: [email protected]

Veronica Tibiletti

Researcher in Business Economics

Faculty of Economics – University of Parma Via J.F. Kennedy, 6 – 43100 Parma, Italy Tel. 0039 0521 03 2441

Abstract

Corporate code of ethics is an important tool for corporate governance. Reading the code, it’s possible to know the rules that inspire enterprise’s activity, and in particular its culture.

The role of corporate codes of ethics as modes of formal organizational discussion is confirmed by several studies that have examined codes in order to increase understanding of their terms, content, purpose, function, and effects.

Regarding Italian listed companies’ choices in issuing code of ethics, an important influence was made by the Decree Law 231/2001, that introduced in Italy the possibility of prosecuting and punishing legal entities when in the case of a finding of commission of crimes committed in the interest or benefit of the entity by parties who, in itself, are placed in top positions.

The new rules have an impact on the argument of ethical codes because article 6 states the exemption from penal responsibility for which enterprises that demonstrate to have set and adopted, before the commission of the crime, efficient organizational and management models, able to prevent the illegal facts described above. This possibility has produced – in particular in Italian listed companies - a large diffusion of statements, generally called code of ethics, that describes admitted and forbidden behaviours according to what stated in Decree Law 231/2001.

The present research studies the codes of ethics realized and adopted by the Italian listed companies with the aim to investigate if that codes could be an expression of the behaviours in terms of “values” that guide the firm or if, rather, those codes are tightly connected and are due to the rules introduced by the Decree Law 231/2001.

KEY WORDS: Business Ethics, Code of Ethics, Italian Listed Companies, Rules of Corporate Behaviour.

Introduction

Corporate code of ethics is an important tool for corporate governance that permits both to know the rules that inspire enterprise’s activity and its culture, both to introduce in enterprises specific organizational mechanisms that consider business ethic as a fundamental element of development strategies of enterprises (Brooks, 1989; Schwartz, 2004; Rodriguez-Dominguez et al., 2009; Van Zolingen and Honders, 2010). The code offers a synthetic view of the set of moral and philosophical reflections applicable to economic issues, first of all regarding stakeholders’ awareness of the need to rethink, redefining and point out ethic values that influence business attitude, in order to individuate the behaviour to have in business and to specify an explicit, well known and shared definition of ethic and social responsibilities of the people that is engaged in enterprise’s actions.

The role of corporate codes of ethics as modes of formal organizational discussion is confirmed by several studies that have examined codes in order to increase understanding of their terms, content, purpose, function, and effects (Canary and Jennings, 2008; see e.g., Adams et al., 2001; Carasco and Singh, 2003; Cassell et al., 1997; Farrell and Farrell, 1998; Gaumnitz and Lere, 2004; Lere and Gaumnitz, 2003; Schwartz, 2001; Stevens et al., 2005; Valentine and Barnett, 2002).

The purpose of corporate code of ethics is to be an instrument that regulates business choices, and to outline how employees ought to act in certain situations and how to manage the relationships between external stakeholders and enterprise itself (Kaptein and Schwartz 2008).

The fair representation of the principles that move the economic choices allow to obstruct illegal behaviour committed by who works in the firm using the name of the company.

Regarding Italian listed companies’ choices in issuing code of ethics, an important influence was made by the Decree Law 231/2001 (Decree Law of June, 8th, 2001, n. 231, Disciplina della responsabilità amministrativa delle persone giuridiche, delle società e delle associazioni anche prive di personalità giuridica, a norma dell’articolo 11 della legge 29 settembre 2000, n. 300) that introduced in Italy the

possibility of prosecuting and punishing legal entities when in the case of a finding of commission of crimes committed in the interest or benefit of the entity by parties who, in itself, are placed in top positions (Cimini, 2003; Conforti, 2003 Garegnani, 2008).

The new rules have an impact on the argument of ethical codes because article 6 states the exemption from penal responsibility for which enterprises that demonstrate to have set and adopted, before the commission of the crime, efficient organizational and management models, able to prevent the illegal facts described above. This possibility has produced – in particular in Italian listed companies - a large diffusion of statements, generally called code of ethics, that describes admitted and forbidden behaviours according to what stated in Decree Law 231/20011.

For the Italian listed companies, therefore, the choice to adopt a code of ethics that prescribes precise behaviours of the enterprises in terms of “values” are balanced between the voluntary decision to define ethical principles that guide the action of the firm and that answer to the necessity to define behaviours and actions for the respect of which is stated by the Decree Law 231/2001, with the aim to refuse from the responsibilities scheduled for the crimes committed in the interest of the firm. Some Authors have studied similar circumstances in other countries, like the influence of a US law issued in 2002 (the so called Sarbanes-Oxley Act - SOX) on the formulation of the code of ethics in the enterprises (Canary and Jennings, 2008).

The present paper studies the codes of ethics realized and adopted by a sample of Italian listed companies with the aim to investigate if that codes could be an expression of the behaviours in terms of “values” that guide the firm or if, rather, those codes are tightly connected and are due to the rules introduced by the Decree Law 231/2001.

The possibility for the companies to draft a code of ethics in accordance to the Decree Law 231/2001, in fact, couldn’t simply allow to think that in those firms is not present even an unconditional ethical orientation that could stimulate the voluntary adoption of a corporate code of ethics. For example, the consolidated experience in those matters, in particular if it is issued before the introduction of the Decree Law 231/2001, allows to think that the sensibility about ethic and behaviours principles are independent, even if coordinated, of the indications of the decree. In those cases, it is important to understand if and in what way the new rules introduced by law have influenced ethical considerations and thought that already existed. It is possible that in some situations the provision expressed in the code of ethics have been modified or in other cases they have been introduced side by side with the existing code new ad hoc tools to answer to the rules of the Decree Law 231/01.

Concerning the research method, the study first examines aspects related to code of ethics (characteristic, role and contents) and the rules introduced by the Decree Law 231/2001, with particular attention to the articles related to the exemption of responsibility for the companies that define and act fair model of organizational and management structure. The analysis of the normative rules has the aim to find the more remarkable consequences in terms of definition of the structure and contents of the codes adopted by the enterprises in consequence of the Decree Law.

Then, the study analyses empirically a sample of Italian listed companies with the aim to find:

1) the presence of a corporate code of ethics or a corporate code of behaviour or of another instrument concerning ethical action in the enterprises;

2) an explicit reference in the code of ethics about the Decree Law 231/2001; 3) the year of introduction of the code of ethics and of the possible modifications;

4) the possibility to know the link exisisting in term of adoption between Code of Etics and Decree Law 231/2001.

The work ends with some conclusive considerations and an illustration of the future developments of the research.

1 See the research “Governance e responsabilità sociale. Analisi sull’applicazione dei Codici Etici d’impresa in Italia” published in “I Quaderni di Unipolis”, 01, by Fondazione Unipolis.

Theoretical foundation about Code of ethics

In general, for a company, the code of ethics is an important governance tool through which to specify and report, outside and inside the organization, the rules that guide corporate conduct, by making clear the foundation of the culture that inspires its definition. At the same time, it allows the introduction into the company of precise organisational mechanisms aimed at considering business ethics an essential element of corporate development strategies (Caselli, 2004, p. 41 and following; see e.g. Brooks, 1989; Schwartz, 2004; Rodriguez-Dominguez et al., 2009; Van Zolingen and Honders, 2010. As regards the Italian context, see, among others: Bertolini, Castoldi, Lago, 1996; Dalle Donne, Battaglioli, 2005; Ferraris Franceschi, 2002; Gabrovec Mei, 1995; Gabrovec Mei, 1990; Riolo, 1995; Rusconi, 1997; Rusconi, 2002; Sacconi, 1991; Sacconi, 1997; Sacconi, 2005).

The document offers a synthesized expression of the body of moral and philosophical reflections that can be applied to economic issues, which can be dealt with at various levels: from the more general ones concerning State, institutions and market, to the intermediate levels ascribable to businesses and various organisations, and to the more particular and specific level relating to individual decisions (Sacconi, 2005, p. 611 and following). In relation to the different levels of analysis, a different connotation of code of ethics may emerge (Wood, Rimmel, 2003):

– at institutional level, the tool is useful if it proposes to regulate behaviour, by expressing clearly a set of fixed and mandatory rules and precepts that the persons it is aimed at are called on to follow;

– when inserted in an organisation, it assumes the features of a standard clarifying the principles and norms that the various participants of the organisation must be guided by, being aware that the said tool is, at the same time, a set of standards of behaviour to comply with and a reference to aspire to;

– from the viewpoint of the individual, it is intended to be an illustration of principles that must be acknowledged, introjected, discussed and shared by the individual operator to then lead him/her to independently choose his/her actions on this basis.

The approaches mentioned start from the awareness, perceived by various company operators, of the need to rethink, redefine and clarify the ethical values that drive behaviour in the economic field, so as to identify the behaviour and conduct to follow in relation to the various spheres of activity, and also offer a clear and explicit definition of the ethical and social responsibilities of all those who, in various capacities, are involved in the company.

The code of ethics therefore proposes itself as a tool that aims to govern the choices of the various operators, with specific reference to economic decisions, by establishing behavioural standards for regulating employees' attitudes in their internal relations and relations with the company, and the relations between the company and external stakeholders. According to this analysis perspective, it can be considered as the “Constitutional Charter” of a company, that is, the set of principles that specify the moral rights and duties of each participant in the organisation and identify the conduct to follow with reference to both the various critical areas of activity and the various categories of stakeholder. The clear identification and representation of principles and rules of conduct enables the prevention of irresponsible or illicit behaviour by anyone who acts in the name or on behalf of the company.

Furthermore, the external dissemination and disclosure of the document explains the company's ethical vision to readers and identifies the privileged interlocutors. By reporting the culture and policies followed, even to persons that are most remote from the corporate situation, expectations are created about what the organisation's conduct might be on the occasion of unforeseen events or in contexts where actual behaviour is not easy to see.

Code of ethics: opportunities and consequences

The opportunities and consequences arising from the definition and implementation of a code of ethics are significant for the company from various analysis perspectives.

In the first place, by setting out in a clear and formalised manner the fiduciary duties that the company assumes towards its stakeholders, the tool performs an important moral legitimation function.

Together with advantages in terms of legitimation and approval, benefits of a more strictly economic nature may result from the definition and setting up of a code of ethics, connected, for example, with improvement in relations with employees in terms of loyalty and dedication of personnel to the company and of general improvement in work climate. The clear definition of roles, functions and responsibilities, in fact, contributes to the development of employees' sense of belonging to the organisation, by promoting the sharing of corporate objectives and motivating employees to show personal commitment. In this sense, the possible resulting advantages for the company connected, for example, with reduction in staff turnover, greater dedication of workers and therefore with greater productivity or a reduction in trade union disputes, are evident. Furthermore, a better work environment can also encourage the development of personal initiatives and favour increased general performance.

Even on the level of relations with customers and suppliers, the improvement in relations, linked to the clear definition of the rules for carrying out negotiations and, in general, the relations described in the code of ethics, can bring about a reduction in costs for legal expenses due to disputes or costs for the definition of contracts and so on. In that regard, possible progress in relations with administrative authorities and society are also significant, with consequent positive repercussions in terms of image, simplification of inspection activities (with consequent reduction in the costs connected with them, such as fines, penalties or possible judicial consequences) and also an obvious improvement in communicative quality. With reference to this aspect, it also brings out the positive relationship with communication media, which boosts the legitimising effect of the code of ethics.

A further element to consider regards the effects that the code of ethics can have in the formulation of strategies and in the management of the company: by identifying the duties assumed towards stakeholders and binding the company's top management first of all to comply with fixed guidelines, the document makes clear the company's ultimate aims (the corporate mission) and also the methods with which the company intends to pursue the said aims.

The expository clarity and precise definition of the shared values and of the consequent behaviour rules bind the entire body of operators, in all orders of activity, from the strategic decisions made by top management to the daily operational choices made at all organisational levels.

Even before, it is the same process of formulation and definition of the principles and norms described in the code that, by giving rise to a formalised and fixed procedure of considering and sharing the said principles and norms, represents an important planning and design stage of corporate action considered in all of the aspects that characterise it, in the diversity and complementarity of the persons involved and in the complexity of the corporate aims.

In many cases, this procedure enables the values and rules that are in fact already in operation to be expressed clearly and systematised, by condensing provisions scattered in various documents or ways of being and operating, forming part of the operators' culture and the corporate history that in the code of ethics find openly defined form and expression.

From the internal relations viewpoint, finally, it identifies and clarifies the limits to the exercising of authority: by indicating the expectations and the claims that can be put forward by each participant in corporate activity, it increases the sense of belonging to the organisation with obvious repercussions in terms of loyalty, commitment and dedication. At the same time, the document performs an important deterrent action for illicit behaviour and, through training and participation activities, facilitates the sharing and consolidation of principles and values between collaborators.

Code of ethics: content

With regard to content, as previously mentioned, the code of ethics takes care of defining principles and values that are shared within the company and that guide the choices and behaviour undertaken. These principles are declined in a set of rules or norms that regulate the behaviour of persons in relation to the various areas of activity into which the corporate situation is divided. In its most complete formulation, the code therefore consists of a part in which general principles and values are presented, which are expressive of corporate culture and history, and a part, regarding the regulations, in which the principles are translated into a set of standards of conduct that must guide the behaviour of the corporate operators in such a way that this is always in line with the stated principles. This last section is frequently called code of conduct.

It is clear that the two parts are closely connected and interdependent, because principles and values find sense and implementation only if actually applied in operational situations, therefore requiring translation into precise behaviour rules, while at the same time, the standards of conduct need general principles and values that will clarify and justify their meaning and aims (Sacconi, 2005, p. 613 and following).

As concerns, in particular, the first part, it is necessary for each company to consider and assess which principles and values distinguish the corporate situation, and concentrate on clarifying the mission and on the historically implemented procedures or the procedures it plans to implement, to accomplish it in the most correct way. Obviously, the values to adopt must be expressive of the company's situation and shared by the whole organisation, and be distinguished from a sterile listing of principles that are ethically exemplary but extraneous to the individuals who work in the company. A preset list that is not shared by the whole organisation is not only unable to correctly represent the corporate situation by showing its real characteristics and peculiarities to the outside, but it also makes it impossible for operators, irrespective of the level held (management or operational), to identify with the proposed model and therefore to comply with it.

The criticality of the transition in question is characterised by the need to choose values that are able to express the corporate situation and interpret the entirety and complexity of the organisation and of all the individuals involved in it, and also for the need to be the result of a well-organised process of sharing these values at all levels. In fact, it is only in this way that the highlighted values can be successfully and spontaneously followed by the various operators, and perform the guide role given to them2.

Whereas, with reference to the definition of the second part (code of conduct or rules of behaviour), it is first of all necessary to identify the areas of activity and the contexts in which the previously defined principles and values must be applied. In that regard, it is necessary to identify the main reference stakeholders for the company, specify for each one the most critical relation aspects and define the ethical standards to be used for regulating and managing these in the best way.

Although the particularity and uniqueness that distinguishes the various corporate situations may lead to defining each individual code of ethics in a different or differently organised way, it is important to mention some elements that are usually significant for the majority of companies:

– shareholders with reference to whom it is important to define the principles that guide the corporate governance structures and the methods of communication to the market and transparency, and also to define some specific themes such as insider trading or the use of price sensitive information;

– employees as concerns a long series of contents regarding the work relationship: personnel selection and management, discrimination, career, development and training, remuneration and working hours, personal integrity and protection, health and safety, conflicts of interest, privacy, freedom of association and representation, information and communication, and obviously also what is relevant to the duties of collaborators;

– customers and suppliers with reference to selection criteria, marked by impartiality, integrity and independence in relations, conditions and methods of defining the contracts, timing and correctness of supplier information flows, quality of communications, guarantee of product quality, especially for customers, and also, with reference to suppliers, the need to disseminate ethical principles in the supply chain;

– institutions, Public Administration, Public Entities, with which it is necessary to engage with a perspective of effective collaboration for the common good and the good of the territory in which the company is inserted, and define relations based on respect and cooperation in relation to the forms of communication and to the commitments undertaken;

2The general principles that are often considered and chosen by companies regard, for example, impartiality, honesty,

correctness in the management of relations within the company (particularly in the event of conflicts of interest), correct management of relations with shareholders and financial backers, development of human resources, respect for the integrity of the person, impartiality of authority, transparency and completeness of information, diligence and accuracy in the performance of functions and contracts, and also correctness and equity in the management and renegotiation of contracts, the quality of the services and products offered, fairness in competition, responsibility towards the community and the surrounding environment.

– the community and the environment, with reference to environmental policies and strategies and to relations with political parties, organisations and associations and, finally, to the quality of external communication and information management, to be understood in terms of the processing of data and information and also of administrative and accounting management.

With reference to the described content, it is advisable to point out that the code of ethics is a voluntary choice of the companies that decide to formalise a combination of behavioural principles and standards that are considered inescapable for ethically qualifying their situation and come from a precise ethical vision of it. Therefore, it must differ from simple compliance with provisions imposed by virtue of rules of law or regulations, by distinguishing itself through additional aspects to those provided for by the existing standards or through consideration of aspects that are not regulated from the normative viewpoint. The previously outlined content can and must therefore be covered in the code of ethics, only to the extent that it proposes new or additional elements to the normative provisions. By way of example, aspects regarding employees can be covered in a code of ethics if the procedures defined by the company for the management of relations with its collaborators complement, with voluntary commitments arising from the company's free choice, what has been agreed by it in compliance with the contractual commitments undertaken.

It is nevertheless advisable to specify that the declaration of compliance with the commitments undertaken by virtue of rules of law and a description of their nature can also be inserted in the document if these elements are significant, in order to notify, in a single document, the set of responsibilities assumed by the company towards all the various interlocutors it considers fundamental to its situation, so promoting the knowledge and full awareness of it by all those involved. It is in fact possible that some categories of reader, albeit informed about what is due to them, are insufficiently informed about the attitude assumed by the company towards other categories of interlocutor. The summary of the information in hand in a single, easy to obtain document that is simple to read and understand (because it is not directed at specific and professional users), can improve knowledge about the company, highlight its qualities and merits or bring out shortcomings and fields of improvement.

Code of ethics: the process of defining and drawing up the document

Starting from the previously introduced content and in awareness of the fact that the code cannot be rigidly defined and imposed from outside, the procedure of defining, drawing up, disseminating and sharing the document is an essential aspect for the validity of the code itself. In fact, although the previously mentioned content and form are shareable and adaptable to many situations, the inalienable element that qualifies the code of ethics is its ability to represent the company's characteristics and particularities, being declined differently according to the company's peculiarities, its organisation, the type of activity, and also in relation to the criticalities of the market or sector it belongs to, as it requires sharing and acceptance by the entire organisation.

Although the various approaches adopted and the different choices that the company can implement may lead to the definition of profoundly different tools, some periods that represent essential points in the code of ethics constructionprocedure can be identified (Arena, Fazio, 2006. See also: OECD,2001; Sacconi, 2005):

1. definition of the general ethical principles that define the corporate mission and guide behaviour for its realisation;

2. identification of the stakeholders and analysis of the critical relation areas between them and the company, organised in relation to the type of interlocutor or to the specificity of the activity carried on; 3. definition of the standards of conduct that regulate the behaviour of the organisation's members in

relations with stakeholders;

4. definition of the field of application of the implementation tools and procedures, that is, of the combination of activities and initiatives started for disseminating knowledge of the code, promoting the sharing of its values, and also monitoring its level of application and actual implementation in order to ensure its effectiveness, possibly with the introduction of the necessary sanctions.

As a side note, it is necessary to clarify that, even though it cannot strictly be termed the drawing up of the code of ethics, in the context of the activities in question it is advisable to include some periods of verification and revision of corporate policies in the light of the principles identified in the code, in

particular by verifying the consistency of the implemented policies with the clearly expressed principles, and also the possible appropriateness of developing new policies relating to aspects or themes not dealt with before, or dealt with in an insufficiently effective way.

The development of the stages just mentioned firstly requires the definition and setting up of a special work group to which to give the precise job of overseeing the entire code construction procedure and also the subsequent stages of its implementation and realisation. The said group must be representative of the various corporate areas and functions and oversee the various stages of the drawing up process by continuously reporting to all the members of the organisation with whom each step of the process must be shared.

In order to correctly apply and manage the tool and allow its profitable development, after it has been drawn up, it is necessary to formulate suitable implementation and optimisation mechanisms supported by a different and functional organisational expression; it is in fact of overriding importance to plan and organise training periods focused on facilitating understanding of the work carried out, in order to promote the sharing of corporate values and vision. This training aims to reinforce and disseminate the organisation's culture and also allows possible obscure or problematic aspects requiring greater attention and a further effort of in-depth analysis to be brought out, in order to ensure full acceptance and sharing of all the aspects covered.

In parallel, it is advisable to implement internal ethical auditing and reporting processes, in order to periodically communicate the social, economic and environmental impact of the activity carried on, with assessment of the effectiveness of the results achieved with respect to the commitments undertaken on the basis of the code of ethics with its stakeholders.

At an organisational level, it is essential to set up an Ethical Committee to which to give supervision duties as regards the use and implementation of the code, specific powers of verification and control, for example as regards compliance of corporate processes and procedures and individual behaviour with the dictates of the code, and also decision making powers in terms of sanctions and measures in the event of defection. It is also important to appoint an Ethics Officer, that is, a person in charge of the programmes and initiatives relating to ethics within the company who will be a reference for everyone who, in relation to the theme in question, expresses doubts, problems, complaints, proposals or suggestions.

Finally, it is advisable to point out again that, at each stage of preparation, it is necessary to give priority attention to the participation and sharing of the tool. It is, in fact, essential that each aspect covered in the code – from general values and principles to standards of conduct declined for each stakeholder – is correctly understood, shared and approved by all members of the organisation, whatever the type of resulting document, irrespective of its level of completeness or complexity or of its degree of expression and formalisation. In that regard, at the preparation stage and afterwards when the code has to be disseminated and put into practice, it is essential that the persons in charge of defining the document or promoting and disclosing it are particularly careful to involve, through suitable forms of participation, all the persons belonging to the corporate situation, and also to consider their observations and implement and realise them.

Decree Law 231/2001

Italian Legislative Decree D. Lgs. no. 231 of 8 June 2001, which came into force on 4 July 2001 (hereinafter “the Decree”), was issued to implement Art. 11 of Law no. 300 of 29 September 2000, for ratification and execution of some international conventions on combating bribery of foreign public officials in international business transactions, of officials of the member states of the European Union and on protecting Community finances3. The Decree introduced rules and regulations applicable to the administrative responsibility of legal entities (in particular companies); in accordance with these provisions, companies can be punished under criminal law if it is ascertained that crimes have been committed by directors or by employees in the interests or to the advantage of the corporation they belong to. This provision in fact provides for the attribution of

3

Brussels Convention of 26 July 1995 on protection of the financial interests of the European Community (EC) and its First Protocol (Dublin, 27 September 1996); Brussels Convention of 26 May 1997 on combating bribery of public officials of the EC and of the member states; OECD Paris Convention of 17 December 1997 on combating bribery of foreign public officials in international business transactions; Convention and Protocols of the United Nations against transnational organised crime adopted by the General Assembly on 15 November 2000 and on 31 May 2001, ratified with law no. 146/2006.

some types of crime no longer only to the physical persons who have committed the criminal act, but also, and above all, to legal persons.

The Decree applies to a broad category of persons, typically carrying on a business activity, such as companies, or bodies of another kind, which may or may not have legal status4.

Article 2 of the decree, of criminal law origin, provides for the application of the rules and regulations governing the responsibility of legal persons only for the crimes to which the law, which came into force before the fact was committed, has expressly linked that responsibility. The crimes in question, which over time have been added to with respect to those provided for in the first version of the Decree, can so far be summarised as follows:

Offences against Public Authorities

Offences against public faith

Corporate offences

Crimes against the personality of the State

Crimes against the individual

Market abuses

Offences to do with safety at work

Offences to do with money laundering and handling stolen goods

Computer crime offences

Offences committed abroad

Article 5 of D. Lgs. 231 outlines the objective criteria on the basis of which responsibility for the offences that have occurred within the company can be attributed to the corporation. The first and fundamental requirement that must characterise the specific criminal act is that it has been committed «in the interests of the corporation» or «to its advantage». The first paragraph identifies the physical persons to whose criminal conduct the corporation's responsibility can be linked, and divides them into two categories: persons in top positions; persons under the direction of others5.

Interests exist when the action has been carried out with the objective of realising a future benefit for the corporation: the subjective element of the author prior to carrying out the notified conduct must be considered.

Advantage is considered as the actual and real economic benefit that the corporation has profited from as a consequence of the punished conduct. The assessment is objective and is carried out ex post.

According to the prevailing interpretation, it is sufficient for just one of the two elements to be present. Therefore the company should be answerable both when those who committed the offence acted to favour the corporation, even if it has not derived any advantage from the criminal conduct, and when the corporation has drawn advantage from commission of the offence.

Articles 6 and 7 of the decree regulate the criterion of subjective allocation of responsibility to corporations. The standard does not define the responsibility attribution criteria, but is constructed in terms of reversal of the burden of proof laid upon the corporation, which can overcome the presumption of responsibility by giving evidence of the existence of the four concurrent conditions required and specified in paragraph 1, letters a), b), c) and d).

4 Cf. Art. 1 of the Decree. In short, the following are subjected to the rules and regulations: private legal persons; all

companies (corporations, partnerships, cooperatives); non-chartered associations; public institutions of an industrial and commercial nature.

5

Directors, general managers, legal representatives, persons in charge of branch offices and managers of divisions having financial and functional autonomy come into the first category. As regards persons who in actual fact perform the management and control functions of the corporation, those who exert strong control over it are definitely to be considered top managers. All those who work in the corporation in a subordinate position are “persons under the direction of others”, provided they are under the direction or supervision of the top managers. But the corporation's responsibility is excluded, in accordance with paragraph 2, when the authors of the offence «have acted in their sole interests or those of third parties».

In particular, the corporation must prove that:

a) before commission of the fact, it adopted and implemented organisational and management models suitable for preventing offences similar to those that have occurred;

b) it has given a body of the corporation, with autonomous powers of initiative and control, the job of supervising the operation of these models and carrying out the updating of them (the Supervisory Committee, called in Italian “Organismo di Vigilanza”);

c) with respect to the offence, fraudulent evasion of the organisational models has been discovered; d) there has not been lack of, or insufficient, supervision by the control body.

The corporation can be considered blameless only if all four of the aforesaid conditions are met.

From the foregoing, it plainly emerges that the crucial point for preventing the offences provided for by the Decree and the formation of an exempting from responsibility mechanism for the company is the adoption and implementation of an organisational and management model suitable for preventing the commission of the said offences.

In that regard, the Decree (Art. 6, 2nd paragraph) sets out the guidelines that the organisation and management models must meet for the purpose of their effectiveness. In particular, these models must contain:

the identification of activities exposed to the risk of commission of offences;

provision for «specific protocols» for programming the formation and implementation of the corporation's decisions as a function of crime risk prevention;

the identification of procedures for the management of financial resources suitable for preventing the commission of offences;

provision for information obligations towards the control body on the operation of, and compliance with, the models;

the introduction of a suitable disciplinary system to punish failure to comply with the measures indicated in the model.

The company can be relieved of responsibility (Art. 6) if it provides proof that, before commission of the fact, it had effectively adopted organisation and management models suitable for preventing offences of the kind that has occurred, that it supervises compliance with these models and that the offence was carried out by a person who has fraudulently evaded the organisation and control models.

The advantages that come from the introduction of an organisation and management model can be numerous, such as for example: avoiding the application of pecuniary or debarring sanctions, reducing the risk of criminal acts, reducing the possibility of exclusion from public contracts and sub-contracts, protecting the investment of partners and shareholders in relation to economic damage due to the carrying out of the above-mentioned offences, protecting the company's image and increasing the company's competitive advantage by basing the policy on principles of ethical integrity.

The organisational models must:

allow identification of the corporation's activities within which offences might be committed;

provide for specific protocols aimed at programming the formation and implementation of the corporation's decisions in relation to the offences to be prevented;

provide for procedures for the identification and management of the financial resources allocated to the activity within which offences might be committed;

provide for information obligations towards the body appointed to supervise the operation of, and compliance with, the models;

provide for a suitable disciplinary system to punish failure to comply with the measures indicated in the model.

Following the legislative provisions, the “construction” of an effective organisational model can be divided into large phases: mapping of the risks; design and implementation of a preventive control system; identification of the Supervisory Committee; identification of the sanctions that can be imposed.

The decision to adopt model 231 by the corporation, in the absence of a rule of law, has been ascribed to a mere option, whose choice is left to the directors' discretionary power also in relation to the risk activities initiated by the company.

The provision for an organisation, management and control model with discriminant effectiveness has been interpreted as a sort of rewarding consideration for those companies that perform a concrete crime prevention action from a self-regulation perspective.

However, over the years, we have seen a transformation of the optional nature of this model; the tendency has been for it to become compulsory.

After having formulated a system of behaviour values and principles common to the entire organisation, these need to be translated into operational mechanisms. Essentially, an organisational system or model must be created that will make the behaviour principles examined during the previous phase operational, so that these are effectively introduced into the life of the company.

To define an organisational crime prevention system that can have general validity is an operation of little practical use, because each company has its own organisational and operational peculiarities that a universally valid system could not allow for. Consequently, given below are only some guidelines and examples regarding a general system of controls and procedures that is effective in accordance with the requirements of D. Lgs. 231/2001.

To act as exempting mechanism for corporations, the Organisation Models must actually be effective, and therefore they must identify the crime risk prone activities and implement the preventive protocols relevant to each of them.

Of the preventive protocols, the Code of Ethics has an important role as the corporation's official document that contains a set of “corporate code of conduct” principles, that is, the whole set of rights, duties and responsibilities of the corporation towards “interest holders” (employees, suppliers, customers, Public Administration, shareholders, financial market, etc.). In other words, the Code of Ethics aims to recommend, promote or prohibit certain behaviours, beyond and irrespective of what is provided for by the regulations. It is clear that the corporation's adoption of ethical principles that are also relevant for the purposes of crime prevention pursuant to D. Lgs. 231/2001 is an essential element of the preventive control system. To this is added that, in general, the “theoretical” principles of the Code of Ethics are made effective through the adoption of the Organisation, Management and Control Model, and become integrated with it. The Code of Ethics, therefore, belongs to the basic elements of the organisational design, to those elements that are chosen so as to achieve internal harmony or consistency and also, at the same time, a basic consistency with the company's situation: the size, the age and the type of environment in which it works.

Bearing in mind the intimate connection that, following the coming into force of the Decree, exists between Organisational Model and Code of Ethics, some authors (Salvatore, 2009) have stressed the need for autonomy of the Code of Ethics from the so-called reference criminal rules, in the sense that the Code should impose conduct or also (and above all) prohibit conduct that is not punished under criminal law or even that is just merely irregular: so it could well be that a breach of the Code of Ethics does not give complete, sufficient grounds for prosecution (for example, carrying out false accounting that has not reached the so-called “punishability thresholds”), that is, it does not cause responsibilities to the corporation pursuant to D. Lgs. 231/2001 (for example, the issuing of invoices for non-existent transactions, a conduct that, at present, is not a source of administrative responsibility laid upon the corporation).

According to a doctrinal position (Santi, 2004), Organisational Models and Codes of Ethics are absolutely distinct entities, by nature, content and legal effect.

But there are those who (Arena, Cassano 2007) - although acknowledging that the Code of Ethics could well, and actually should, exist autonomously irrespective of the adoption of an Organisational Model - consider that the Code of conduct is the “hard core” of the Organisational Model and, in any case, the starting point for drawing it up.

In that regard, it is pointed out that – although Models and Codes of Ethics both come from United States compliance programs – the same letter of the Decree indicates not only a difference between the two

different schemes, but also a logical and chronological sequence, in the sense that the Code of Ethics should exist before the Organisational Model and place itself at a higher level than the model (in this sense, see also Salvatore, 2009). The different nature also affects the content of the Code of Ethics, since, while it limits itself to dictating the Guidelines for the drafting of the Model, this last is the corporation's internal law, which must be observed by top management, subordinates and, in general, by everyone who is, in any case, connected with the corporation.

Empirical research

Sample description and methodology

As mentioned in the introduction, the empirical search carried out is aimed at the examination of the characteristics and peculiarities of the codes of ethics produced by a sample of listed Italian companies with the objective of looking into whether they can be an expression of the value positions that guide and drive the company or whether, rather, they are closely linked and dependent on regulatory execution descending from Decree 231 of 2001.

The research took as its subject of observation a combination of companies, those listed on the Milan Stock Exchange in the Star segment on 22 May 2010, as listed on the Borsa Italiana site with exclusion of companies suspended from quotation on that date and of those listed on foreign markets. As a result of the described procedure, the considered companies numbered 73.

With reference to these companies, the observation of the data was carried out with the help of an analysis grid prepared in order to systemically identify information about the existence and the main characteristics of the codes of ethics produced by them.

The analysis regarded the presence and the characteristics of the code of ethics, and also the existence of the relevant Organisational Model pursuant to D. Lgs. 231/2001.

In particular, with reference to the code of ethics, the observed data regarded the following: – presence of the code of ethics;

– placing of it in the section of the Internet site regarding corporate governance; – name used to indicate the document;

– first publication date of the code of ethics (expressed clearly or can be found from other sources of information such as Internet, the company's site, other company documents);

– presence in the document of an explicit reference to decree 231/01; – presence in the document of an explicit reference to the corporate group.

As concerns the Organisational Model, the observation of the data considered the following research elements:

– presence and availability of the organisational model;

– first publication date of the organisational model and date of any updates;

– explicit reference within the organisational model to the existence of the code of ethics. Empirical results

In the context of the research method just described, the first observation carried out was aimed at verifying the presence of the Code of Ethics for the companies belonging to the sample of observed companies.

Table I

Existence of Code of Ethics

Number %

Yes 68 93.15%

The collection of data produced the findings as shown in the table above, which indicate that over 93% of the companies in the sample have drawn up a Code of Ethics. This fact confirms the importance of the phenomenon and the vast dissemination of the tool that is the subject of observation.

For the 5 companies for which the lack of a Code of Ethics emerged, further research was carried out in order to verify whether this circumstance was ascribable to specific characteristics, or fortuitous conditions of these companies.

In that regard, while for one of them (BB Biotech AG) the absence of the code of ethics could be justified in terms of the fact that it is a joint-stock company with head office in Switzerland and listed on the Swiss Stock Exchange, in Germany (Prime Standard), as well as in the Star Segment in Italy, for the other four companies no particular conditions were seen to justify failure to draw up the document.

An important aspect that must be mentioned at the time of consulting a Code of Ethics is to be linked to the fact that the principles envisaged within it are applicable to the entire group that the parent company that prepared it belongs to. From the observations carried out, 46 of the 68 companies for which it was possible to proceed with the study of the Code of Ethics explicitly mentioned a reference to the “group” in the application of the principles envisaged therein, so highlighting a real perception of this aspect.

Based on what was said earlier in terms of importance of the Code of Ethics as governance tool, it seemed useful to check whether this document could be found on the company's website, and also whether or not it was present in the “Corporate Governance” section.

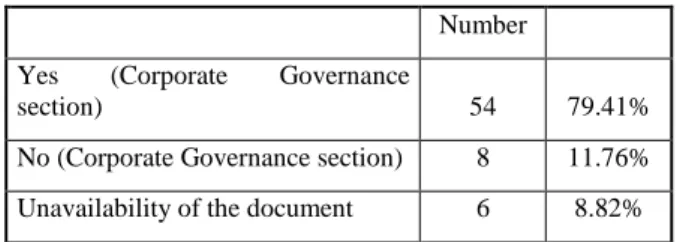

Table II

Availability of the Code of Ethics on the Internet site, CG section

Number

Yes (Corporate Governance

section) 54 79.41%

No (Corporate Governance section) 8 11.76%

Unavailability of the document 6 8.82%

As concerns the 68 companies for which the presence of a Code of Ethics was identified, for 6 of these it was not possible to download and view the document, because it was not present on the Internet site.

From the collected data, it can be deduced that almost 80% of the companies that have drawn up the Code of Ethics have inserted this document in the section of the site dedicated to Corporate Governance, so confirming the initial hypothesis, that is, that the Code of Ethics is considered a corporate governance tool by companies, together with other tools such as the Code of Conduct as regards Internal Dealing and the Report on Corporate Governance.

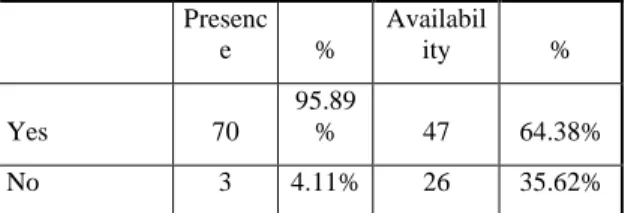

Subsequently, the research concentrated on the second aspect that was the subject of in-depth analysis, that is, on the adoption of the organisation, management and control Model pursuant to D. Lgs. 231/2001 (Organisational Model) by the companies of the sample. In addition to verifying that it had been drawn up, a search was made to see whether it was present on the company's Internet site.

Table III

Presence and availability of the Organisational Model

Presenc e % Availabil ity % Yes 70 95.89 % 47 64.38% No 3 4.11% 26 35.62%

The interesting fact that emerges from the observations made is that as many as 70 of the total 73 companies stated they had prepared and adopted an Organisational Model pursuant to D. Lgs. 231/2001, but only for 47 of those was it possible to find and consult the full version of the document. This last circumstance appears to be in net contrast with the function of the standard that the drawing up of this document should meet and, equally, in contrast with the spirit of transparency and sharing of the concepts contained therein that the companies that draw it up should adopt.

Moving on to a further aspect, the research planned to verify, with the observation of further data, whether the Code of Ethics had been adopted by the companies only as a consequence of the drawing up and application of the Model pursuant to 231/01, or whether this document came earlier, and was therefore originally independent of the application of regulations 231/01.

To that end, the following data were observed:

first publication date of the Code of Ethics and of the Organisational Model;

explicit mention, within the Code of Ethics, of its adoption based on the Organisational Model.

With reference to the research carried out regarding the identification of the first publication date of the Code of Ethics and of the Organisational Model, in the first instance, which of these documents contained this information was verified in numerical terms.

Table IV

Elucidation of first publication date

Code of Ethics Organisational Model

Yes 42 61.76% 48 70.59%

No 26 38.24% 22 32.35%

The observation carried out did not allow particularly comforting data to be seen, because only a little over 60% of the companies that have drawn up the Code of Ethics have given an indication of the first publication date directly in that document, while as regards the Organisational Model, the data are slightly better (about 70%). This indication would obviously be very useful in order to understand when the company started to undertake a procedure of explicit protection of the principles met by the drawing up of the two documents in question.

Considering the importance of this aspect, immediately afterwards, with reference to the Code of Ethics, the locating of the first publication date of that model, not only in the model but also in other documentary sources provided by the company (Internet site, Report on Corporate Governance and so on), was verified,

giving a more comforting finding than in the previous case, in terms of disclosure (58 out of 68 companies, equal to a percentage incidence of about 85%).

This observation was functional to performing another survey of particular interest, regarding the possibility of making a broader comparison between the first publication dates of the two documents, Code of Ethics and Organisational Model. The purpose of this research was to verify whether the drawing up of the Code of Ethics was pre-existent to the drawing up of the Organisational Model, in order to understand whether the drawing up of the Code of Ethics was carried out only in terms of meeting one of the dictates of the regulations pursuant to D. Lgs. 231/2001.

It was this observation that allowed an important criticality to be perceived in the relationship between Code of Ethics and Organisational Model.

Table V

Comparison between 1st publication date of Code of Ethics

and 1st publication date of Organisational Model

Companies for which it was possible to find both 1st publication dates at the same time Companies that drew up the Code of Ethics after drawing up the Organisational Model Companies that drew up the Code of Ethics in the same year as they drew up the Organisational Model Companies that drew up the Code of Ethics before drawing up the Organisation al Model 42 4 31 7

As shown in the table, in fact, for the 42 companies for which it was possible to make the comparison between the first publication dates, only 7 had drawn up the Code of Ethics before drawing up the Organisational Model, while as many as 31 companies had prepared the two documents at the same time (in the same year). Indeed, 4 companies had prepared the Code of Ethics, a fundamental element of the regulations pursuant to D. Lgs. 231/2001, in years subsequent to the drawing up of the Organisational Model.

The interesting conclusion arrived at following analysis of the observations made is that the great majority of companies for which it was possible to simultaneously identify the first publication dates of the documents in question do not appear to have adopted the codes of ethics through a real effort aimed at making explicit the moral and ethical reasons that guide the management and development of the business activity, so much as just because of the introduction of regulations pursuant to D. Lgs. 231/2001 that, indirectly, required them to be drawn up.

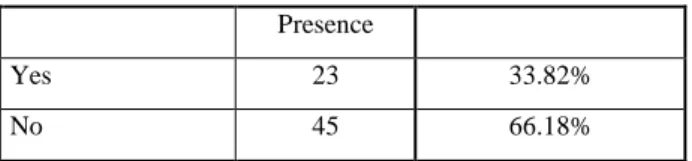

Evidence of this fact is also the observation carried out within the individual Codes of Ethics found, in relation to which, in as many as 23 cases, an explicit statement was seen according to which the preparation of that document as a consequence of the regulatory provisions imposed by D. Lgs. 231/2001 was acknowledged, as is expressed clearly in the following table.

Table VI

CE made expressly in observance of the regulations pursuant to D. Lgs. 231/2001

Presence

Yes 23 33.82%

No 45 66.18%

Moreover, this strong link is also borne out by the frequent reference, in the Code of Ethics, to the regulations pursuant to D. Lgs. 231 of 2001, since as many as 52 companies out of 68 have inserted an explicit reference to regulations 231/2001 in the Code of Ethics.

A last interesting observation in that regard can be made if the Code of Ethics preparation dates are considered. Table VII Year drawn up Only CE Code of Ethics and OM 2002 3 5.17% 0 0.00% 2003 4 6.90% 2 4.17% 2004 7 12.07% 4 8.33% 2005 4 6.90% 4 8.33% 2006 8 13.79% 8 16.67% 2007 6 10.34% 6 12.50% 2008 19 32.76% 17 35.42% 2009 6 10.34% 7 14.58% 2010 1 1.72% 0 0.00%

As clearly emerges from analysis of the table shown above, of the 58 codes of ethics in which the publication date was made clear, it is interesting to verify that the greatest drawing up frequency occurred between 2006 and 2009, with a particular note for the year 2008 in which about a third of the codes of ethics considered were prepared for the first time. The same observations are made, in parallel, in confirmation of what was mentioned earlier, if a similar line of reasoning is extended to the observed Organisational Models.

Conclusions

From the observations carried out, a wide dissemination of Codes of Ethics is found in the analysed sample of companies.

The great majority of companies that have drawn up the Code of Ethics have inserted that document in the section of the site dedicated to Corporate Governance, so confirming the initial hypothesis, that is, that the Code of Ethics is considered a corporate governance tool by companies.

As to the Organisational Model pursuant to D. Lgs. 231/2001, it has emerged that as many as 70 of the total 73 companies have stated they had prepared and adopted it, but only for 47 of those was it was possible to

find and consult the full version of the document. This last circumstance appears to be in net contrast with the function of the standard that the drawing up of this document should meet.

From a cross-reading of the data regarding the Code of Ethics and the Organisational Model, bearing in mind the close interrelations existing between the two and highlighted in the treatment, it has emerged that for the 42 companies for which it was possible to make the comparison between the first publication dates, only 7 had drawn up the Code of Ethics before drawing up the Organisational Model, while as many as 31 companies had prepared the two documents at the same time (in the same year). Indeed, 4 companies had prepared the Code of Ethics in years subsequent to the drawing up of the Organisational Model.

It follows that the great majority of companies for which it was possible to simultaneously identify the first publication dates of the documents in question do not appear to have adopted the codes of ethics through a real effort aimed at making explicit the moral and ethical reasons that guide the management and development of the business activity, so much as just because of the introduction of regulations pursuant to D. Lgs. 231/2001 that, indirectly, required them to be drawn up.

Moreover, this strong link is also borne out by the frequent reference, in the Code of Ethics, to the regulations pursuant to D. Lgs. 231 of 2001.

References

ARENA M.–CASSANO G.,La responsabilità da reato degli enti collettivi,Milano 2007, pp. 236 ss..

ARENA – FAZIO, Il contributo dei codici etici nello sviluppo della responsabilità sociale delle imprese, -Non Profit,

anno 2006, volume 12, fascicolo 2;

BERTOLINI S.-CASTOLDI R.-LAGO U., I codici etici nella gestione aziendale, Il Sole 24 Ore, Milano, 1996;

DALLE DONNE A.-BATTAGLIOLI M., La responsabilità sociale d’impresa. Codice etico, bilancio sociale e standard,

Amministrazione e Finanza - I corsi, fasc. 4, vol. 11, 2005;

FERRARIS FRANCESCHI R., Etica e economicità, Rirea, 2002;

GABROVEC MEI O., Etica e ricerca economica, Centro Universitario Etica e Scienza Vittorio Longo, Quaderno n. 14,

Trieste, 1995;

GABROVEC MEI O., Business ethics e codici etici, Rivista dei Dottori Commercialisti, 1990;

OECD, Codes of Corporate Conduct: Expanded Review of their Contents, Working Paper on International Investment, n. 2001/6, May 2001;

RUSCONI G., Impresa, accountability e bilancio sociale, in HINNA L. (a cura di), Il Bilancio sociale, Il sole 24 ore,

Milano, 2002;

RIOLO M., Etica degli affari e codici etici aziendali, Edibank, IGEB, Milano, 1995;

RUSCONI G., Etica e impresa. Un’analisi economico-aziendale, Clueb, Bologna, 1997;

RUSCONI G., L’etica dell’informazione aziendale agli stakeholder nella società attuale: bilancio d’esercizio, bilancio

sociale e codici etici, relazione presentata al 25° Convegno AIDEA, Novara, 4-5 ottobre 2002;

SACCONI L., Etica degli affari, Il Saggiatore, Milano, 1991;

SACCONI L., Economia etica ed organizzazione, Laterza, Roma-Bari, 1997;

SACCONI L. (a cura di), Guida critica alla responsabilità sociale e al governo d’impresa, Bancaria Editrice, Roma,

2005;

SANTIF., La responsabilità delle società e degli enti. Modelli di esonero delle imprese: d.lgs. 8.6.2001, n.

231 - d.m. 26.6.2003, n. 201, Giuffrè, Milano 2004.

SALVATORE A., Il "Codice Etico": rapporti con il Modello Organizzativo nell'ottica della responsabilità

sociale dell'impresa, La responsabilità amministrativa delle società e degli enti, 4/2008, Torino, Plenum. SAPELLI G., in CASELLI L. (a cura di), Le parole dell’impresa, Angeli, Milano,1995.

Reference for improve

ANNOVAZZI S., Il ruolo del Codice Etico e i principi della Corporate Social Responsibility nell’ambito dei protocolli preventivi, La responsabilità amministrativa delle società e degli enti, 4/2009, Torino, Plenum.

BENSON G.C.S.,Codes of Ethics,Journal of Business Ethics, n. 8, 1989.

BERTOLINI S.-CASTOLDI R.-LAGO U., I codici etici nella gestione aziendale, Il Sole 24 Ore, Milano, 1996.

CRESSEY D.R.-MOORE C.A., Managerial Values and Corporate Codes of Ethics, California Management

Review, Summer 1983.

DALLE DONNE A.-BATTAGLIOLI M., La responsabilità sociale d’impresa. Codice etico, bilancio sociale e

standard, Amministrazione e Finanza - I cocsr, fasc. 4, vol. 11, 2005.

FAZIO V.-ARENA P., Il contributo dei codici etici nello sviluppo della responsabilità sociale delle imprese,

Non profit, volume 12, fasc. 2, 2006.

FELICI G. (a cura di), Dall’etica ai codici etici, Franco Angeli, Milano, 2005.

FREDERICK W.C., The Moral Authority of Transnational Corporate Codes, Journal of Business Ethics, n. 10,

1991.

GABROVEC MEI O., Business ethics e codici etici, Rivista dei Dottori Commercialisti, fasc. 5, 1990.

GABROVEC MEI O., Etica e ricerca economica, Centro Univecsrtario Etica e Scienza Vittorio Longo,

Quaderno n. 14, Trieste, 1995.

KJONSTAD B.-WILLMOTT H., Business Ethics: Restrictive or Empowering ?, Journal of Business Ethics, n.

14, 1995.

LONZANO J.F., Proposal for a Model for the Elaboration of Ethical Codes Based on Discourse Ethics,

Business Ethics: A European Review, n. 2, April 2001.

MALONI M.-BROWN M.E., Corporate Social Responsibility in the Supply Chain: An Application in the Food

Industry, Journal of Business Ethics, n. 68, 2006.

MURPHY P.E., Corporate Ethics Statement: Current Status and Future Prospects, Journal of Business

Ethics, n. 14, 1995.

RIOLO F., Etica degli affari e codici etici aziendali, Edibank, IGEB, Milano, 1995.

RUSCONI G., “L’accountability globale dell’impresa” in RUSCONI G.-DORIGATTI M. (a cura di), La

responsabilità sociale di impresa, Franco Angeli, Milano, 2004.

RUSCONI G., Etica e impresa. Un’analisi economico-aziendale, Clueb, Bologna, 1997.

RUSCONI G.-DORIGATTI M. (a cura di), Etica d’impresa, Franco Angeli, Milano, 2005.

SACCONI L., Economia etica ed organizzazione, Laterza, Roma-Bari, 1997.

SACCONI L., Etica degli affari, Il Saggiatore, Milano, 1991.

SETHI S.P., Imperfect Markets: Business Ethics as an Easy Virtue, Journal of Business Ethics, 1994.

SACCONI L.-DE COLLE S., “Il codice etico come strumento di gestione delle relazioni con gli stakeholder”, in

SACCONI L. (a cura di), Guida critica alla responsabilità sociale e al governo d’impresa, Bancaria Editrice,

Roma, 2005.

SCHAWARTZ S.M., A Codes of Ethics for Corporate Code of Ethics, Journal of Business Ethics, n. 41, 2002.

SCHAWARTZ S.M., Effective Corporate Codes of Ethics: Perception of Codes Users, Journal of Business

Ethics, n. 55, 2004.

SERRA R. I codici etici, De Qualitate, fasc. 6, 1998.

STEVENS B., An Analysis of Corporate Ethical Code Studies: “Where Do We Go From Here”, Journal of

WOOD G.-RIMMER M., Code of Ethics: What Are They Really and What Should They Be?, International Journal of Value-Based Management, n. 16, 2003.

GALGANO C.,Responsabilità sociale d’impresa: è possibile per le piccole e medie imprese?, PMI, fasc. 11,

vol. 10, 2004.

MOORE G.-SPENCE L., Editorial: Responsibility and Small Business, Journal of Business Ethics, n. 67, 2006.

PERRINI F., SMEs and CSR Theory: Evidence and Implication from an Italian Perspective, Journal of