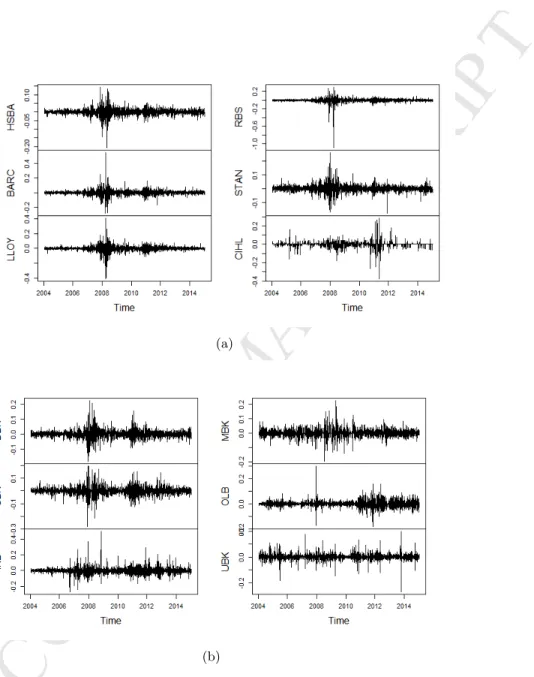

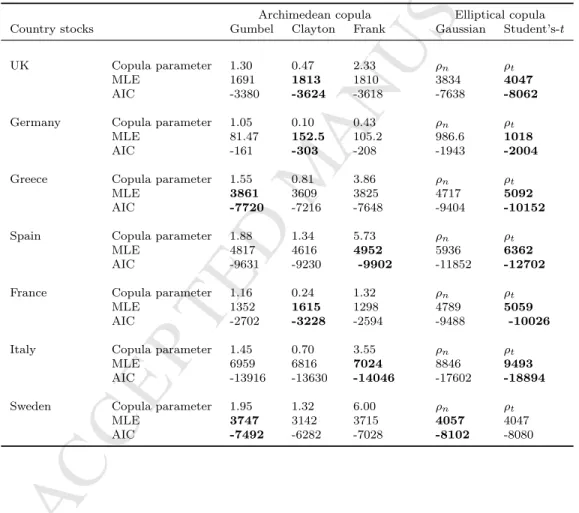

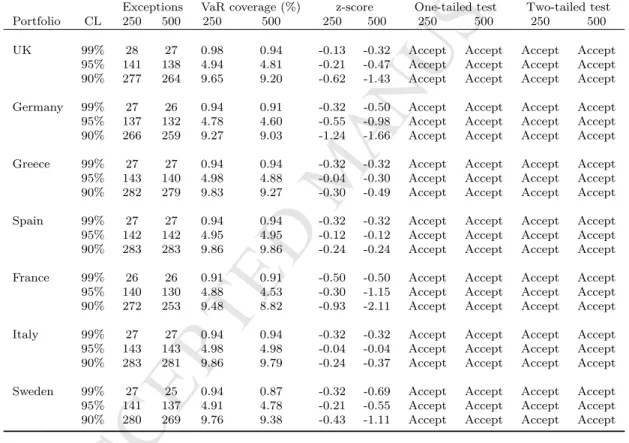

Estimating value-at-risk using a multivariate copula-based volatility model: Evidence from European banks

Full text

Figure

Related documents

Pendant arm mount with power supply box for a AutoDome Series cameras, no transformer, white. Order number

In the southeastern margin of the Iberian Massif, the westernmost exposure of the European Variscan Orogen, there are two big units corresponding to the Alpine

Hence, the answer to the question of why creditors might be willing to voluntarily accept a 50 percent haircut is: “Because in a situation of high uncertainty and continued

The reason is that it includes college specific SAI data on key momentum points such as the percent of students making no momentum after one year, college level points per

(2011) “Ranking economists and economic institutions using RePEc: some remarks”, Ifo Working Paper Series , No.96, University of Munich. (2013a) “Quantile kernel regression

In this chapter, the influence of fibre distribution / orientation on the tensile performance of steel fibre reinforced self-compacting concrete (SFRSCC) was characterized by

This study has shown, for the first time, that the addition of an ICS to a LABA results in a significantly greater proportion of patients with COPD having a clinically

In this paper, I set up a proper model for data for method comparison studies which in the case of constant difference between methods leads to the classical LoA, and in the case