Collaborating for high performance

in cloud-based services

How High Tech companies can realize the full benefits

of cloud computing, for themselves and their customers

By Philippe Roussiere and Robin Murdoch

Leading companies in the technology industries (sectors including software, networking, servers, storage, consumer electronics, PCs and semiconductors) are well aware of the significant benefits that cloud computing-based services can deliver to organizations of all sizes in every sector. The scale of these benefits means the opportunities for creating and selling such services are huge and growing exponentially. Yet to date these opportunities are largely untapped in many industries. Despite the current economic turbulence, and the blend of hype and confusion about the true capabilities of cloud services and technologies, the past two years have seen leading players from a wide spectrum of technology segments enter the cloud services marketplace. These entrants range from technology infrastructure providers, to independent software vendors (ISVs) and process outsourcers.

Cloud reaches critical mass

This influx of service offerings has seen the “cloud wars” escalate, as enterprises come to appreciate the real business benefits of cloud, and enthusiastically embrace the cloud concept. Cloud’s IT impacts can be used to support the business strategy, and the principal benefits it delivers are summarized in the accompanying information panel. The overall effect can be to deliver major cost and effectiveness gains across organizations, while promoting innovation.As a result, we believe that 2010 and 2011 will be pivotal years for the build-out and maturing of the cloud market, and for the emergence of "enterprise-grade" cloud services. In light of this, it is vital that every participant in the High Tech business-to-business (B2B) sector develops a strategy to accommodate cloud computing and its distinctive implications and opportunities in its business model.

Collaborating for high performance in

cloud-based services

Cloud: Flexible IT at lower cost

Most organizations buying cloud computing services neither know nor care where the processing power comes from, or how the computing capability is put together. What users do care about is the capacity of cloud computing to introduce significant new levels of scalability and flexibility, including:• Lower infrastructure, maintenance and energy costs

• Pay-per-use capacity as the business needs it, with the flexibility to scale the service and price up and down to handle unexpected load changes

• Accelerated speed to market, including faster pilots

• High-powered computing, including effectively “infinite” computing capacity on demand.

The evolving cloud computing

landscape

Before we examine these implications and opportunities, let’s take a look at the cloud landscape that is now emerging. Cloud computing allows companies to access IT-based services, including infrastructure, applications, platforms and business processes, via the internet. In general, a cloud-based model provides rapid acquisition, low to no capital investment, relatively low operating costs and variable pricing tied directly to use. Although the term “cloud computing” was coined relatively recently, many elements of the concept, such as timesharing and virtual machines, have been around for several decades.

What makes cloud computing a growing reality for today’s businesses is the pervasiveness of the Internet and Internet technologies, combined with advances in virtualization, hardware commoditization, standardization, and open source software. A key catalyst is the success of major

Internet companies such as Google, Amazon and Microsoft, coupled with the emergence of a group of highly credible pure-play firms, including Salesforce.com and Workday. Across all these offerings, cloud services tend to share several characteristics:

• Little or no requirement for capital

investment to enable use

• Variable pricing based on

consumption; buyers “pay per use”

• Rapid acquisition and deployment • Lower ongoing operating costs than

IT owned and managed in-house

• Programmable and adaptable in use.

Cloud: Growing fast

Cloud computing is real, it’s here now, and it’s growing fast. In 2009, cloud services made up 5 percent of worldwide IT spending and are expected to account for 10 percent by 2013, according to IDC.1 These

services are helping organizations reduce costs, enhance scalability, increase implementation speed and improve applications and business processes. But the real promise of cloud computing lies in developing new markets and services that give clients competitive advantage in rapidly changing markets.

A continuum of cloud options

Within these overall parameters, clouds can take two forms: private and public. Private clouds are built within a company’s data center and are designed to provision and distribute virtual application, infrastructure and communications services for internal business users. In contrast, public clouds extend the data center’s capabilities by enabling the provision of IT services from third-party providers over a network.Both types of cloud can operate in a continuum of segments or layers. For many companies looking to migrate to cloud services, the initial focus is cloud-based IT infrastructure, targeting benefits including financial flexibility, lower TCO, needs-based utilization, speed to market, and availability of information anywhere and anytime.

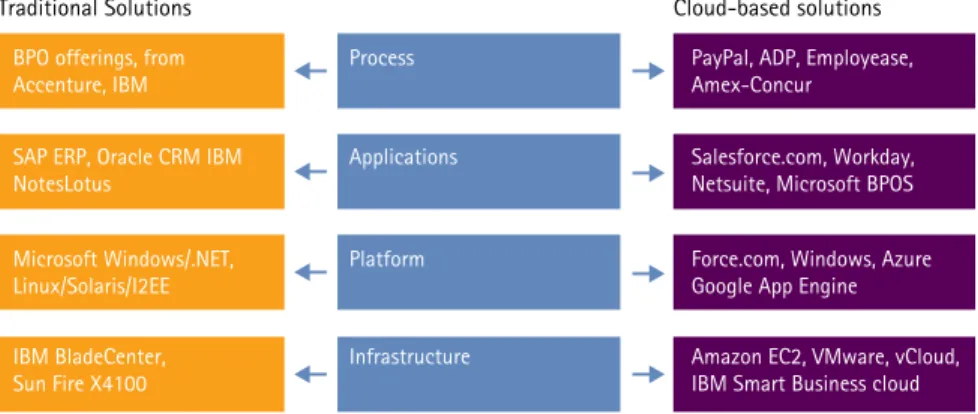

However, cloud is about much more than infrastructure, since it offers opportunities for providers and customers to expand similar benefits up the value continuum to platforms, applications and processes. The escalating hierarchy of cloud opportunities is shown in Figure 1, along with a selection of traditional and cloud-based solutions in each area.

Moving up the hierarchy

Companies have already begun to move up this hierarchy to realize the escalating benefits that each level can deliver. At the infrastructure level, companies have begun to source raw computing resources, processing power, network bandwidth and storage from the outside on an on-demand basis. In most cases, these resources, also known as infrastructure-as-a-service, or IaaS, are used to augment rather than replace existing in-house infrastructure, which itself is increasingly virtualized.At the platform level, cloud-based environments, also known as platform-as-a-service, or PaaS, provide

application developers with similar functionalities to those available in traditional desktops, including tools for development, testing, deployment,

runtime libraries, and hosting. The emergence of cloud-based platforms enables ISVs and IT staff to develop and deploy online applications quickly using the third-party infrastructure. At the application level, the first wave of cloud-based application-as-a-service offerings, also known as software-as-a-service or SaaS, has tended to fall broadly into the areas of office collaboration, software development tools and CRM. The second wave is set to focus on desktop productivity tools, including word processing, spreadsheets, e-mail and Web conferencing. Today, application clouds running on third-party infrastructure span all major enterprise solution areas, ranging from procurement to enterprise resource planning and content management. These services are available via standard browsers, supporting device independence and anywhere access. At the business process level, cloud-based solutions, also known as business process utility (BPU), offer an Internet-enabled, externally provisioned service for managing an entire business process. These services are often targeted at industry vertical markets. Unlike traditional BPO, which often requires the service provider to take over an existing software installation, the process cloud uses a common, one-to-many platform to automate highly standardized processes. It differs from application clouds in that it provides end-to-end process support, covering not just software but also people processes such as contact centers. Examples

include Accenture-owned Navitaire New Skies cloud-based offering for ticketing in the travel industry. Over time, we believe that industry-specific processes are the most likely to be the first to move to this model, since many core horizontal processes, finance and administration, for example are linked to large existing ERP systems.

A dual focus

Across all levels of the cloud hierarchy, High Tech companies have a dual focus on cloud computing. One dimension is a drive to realize the benefits of cloud in terms of flexibility and scalability within their own organizations. The second is to generate rising revenues and profits by delivering these same benefits externally to customers in all sectors, by selling them commercial cloud-based services.

Against this background, the

challenge facing High Tech companies in their markets is creating and operationalizing robust, commercially-viable services that are differentiated from their competitors. Given the flood of new entrants and intensifying competitive pressures, this challenge is growing all the time. We will now examine how players in the technology industries are rising to meet the challenge of cloud, and seizing the opportunities it presents to them and to their customers in all sectors.

Traditional Solutions

BPO offerings, from Accenture, IBM SAP ERP, Oracle CRM IBM NotesLotus Microsoft Windows/.NET, Linux/Solaris/I2EE IBM BladeCenter, Sun Fire X4100 Process Applications Platform Infrastructure

PayPal, ADP, Employease, Amex-Concur

Salesforce.com, Workday, Netsuite, Microsoft BPOS Force.com, Windows, Azure Google App Engine

Amazon EC2, VMware, vCloud, IBM Smart Business cloud

Cloud-based solutions

With High Tech companies currently heavily engaged in rolling out cloud services, and enterprise-grade cloud services gaining momentum, several areas of opportunity are emerging. To exploit these, different players in the technology industries are pursuing a wide range of cloud strategies reflecting their contrasting market positions and the differing impacts of cloud on their core markets.

While some are rapidly extending their entire solutions ecosystem to the cloud, others are hanging back. The strategic direction of travel also varies, with some players evolving their SaaS portfolio and growing their hosting business; others pursuing infrastructure virtualization services to help build public, private or hybrid clouds; and still others taking a more measured approach, launching complementary offerings and waiting for a clearer business case to emerge. In our view, the market for SaaS (or Application-as-a-Service) delivery within the enterprise presents some

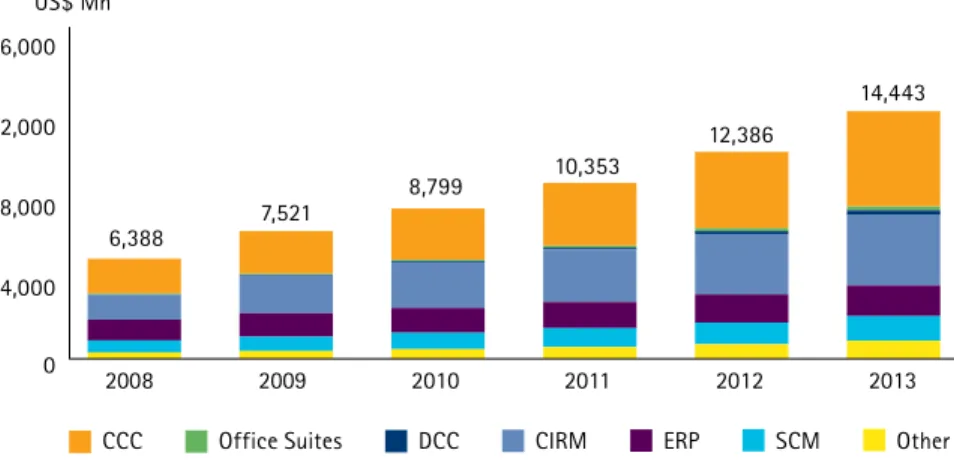

of the most significant revenue opportunities for technology vendors, followed by IaaS and PaaS. According to Gartner, enterprises will spend US$112 billion cumulatively over the course of the next five years on software as a service (SaaS), platform as a service (PaaS), and infrastructure as a service (IaaS) combined. SaaS will continue to account for the bulk of this overall marketplace (see Figure 2). This chart focuses on Iaas, PaaS and SaaS, and excludes cloud-based BPO services, which is a separate but growing segment.

Gartner has come to the view that the Platform-as a-service (PaaS) market is still small ($110 million in 2009) and while it will grow considerably to $650 million by the end of 2014, it adds that this projection is quite speculative. PaaS covers two distinct opportunities. Enabling formerly discrete systems to integrate via the cloud represents a larger but less widely-recognized market that is also maturing quickly. In addition, an embryonic market under which the cloud vendor builds, replatforms and/or develops and manages a portfolio of applications for the client, is now coming of age in commercial terms.

In the Infrastructure as-a-Service (IaaS) domain, services such as storage and backup are currently still in their infancy, setting the stage for rapid growth. From 2011 new outsourcing models and utility features will enable the adoption of hybrid cloud models, driving broader adoption.

Cloud services in the High Tech industry:

emerging opportunities

“As some companies turn to cloud computing providers that offer IT services over the Internet, others are building private clouds designed to grab some of the cost savings inherent in cloud computing while also maintaining control over their IT infrastructure.”3

SaaS drivers: collaboration,

Web 2.0 — and SMBs

Industry estimates indicate that rising use of SaaS offerings by enterprises will continue to focus primarily on two areas: firstly content, communication and collaboration (CCC) services, and secondly CRM (see Figure 3, again from Gartner). This suggests that key drivers behind the rising adoption of SaaS are the increasingly collaborative business environment, and the related roll-out of Web 2.0 initiatives. However, an alternative perspective is that SaaS adoption is strongest in the small and medium-sized business (SMB) segment, fueled by the desire of these companies to gain access to equivalent functionality as larger corporations, without the time and cost of implementing larger on-premises solutions from the major providers of enterprise platforms such as ERP systems. There are also indications that buyers are seeking to pay for what they use in a more granular fashion without incurring large up-front and periodic investment costs in implementation and refresh/upgrades. In response to these various

dynamics, many SaaS offerings to date have primarily focused on office collaboration, software development tools and CRM. At the same time, most large software vendors have chosen to follow a hybrid model in the ERP space, augmenting their existing on-premise solutions with cloud-based value-added services, and using SaaS to win market share in the SMB segment. The rising use of cloud-based CRM services provides a strong validation of the SaaS model, as adoption grows and competitors multiply. By 2013, cloud-based CRM is expected to exceed $4 billion in total software revenue, accounting for 30% of the overall CRM market. Meanwhile, adoption of SaaS within ERP and supply chain management (SCM) varies depending on the complexity of the specific processes. ERP SaaS is predicted to reach more than $1.9 billion by 2013.

Figure 2: Cloud services market (excluding BPO) 2009-2014 ($ Billion)5

2009 2010 2011 2012 2013 2008 0 4,000 8,000 12,000 16,000 US$ Mn 6,388 7,521 8,799 10,353 12,386 14,443 CCC

CCC = Content, communications, and collaboration DCC = Digital content creation

Office Suites DCC CIRM ERP SCM Other

Figure 3 : Total software revenue forecast for SaaS delivery within the enterprise application software markets, 2008-20136

“Oracle expects that through its acquisition of Sun Microsystems, it has a way to sell a full spectrum of hardware and software to business customers. For one, Oracle plans to keep putting support behind OpenOffice, a free open-source productivity suite that competes with Office from Microsoft, Oracle's longtime nemesis. Most notable, Oracle will introduce an online version called Oracle Cloud Office, said Edward Screven, the chief corporate architect at Oracle” 4

0 5 10 15 20 25 30 35 40 2009 2010 2011 2012 2013 2014

Application-as-a-Service Integration-as-a-Service PaaS

Partnerships and

alliances on the rise

A further unifying factor of the cloud ecosystem going forward is that cloud alliances and partnerships will support the industry’s growth and development. Strong cloud alliances are already starting to emerge. Notable examples include EMC, Cisco and VMware joining forces in Acadia (formerly known as the Virtual Computing Environment alliance - see information panel).

The growing use of partnerships targeted at specific opportunities reflects the varying depth and pace of cloud’s impact on different High Tech segments (see Table 1). Cloud’s largest effects are initially being felt in servers and storage followed by software and networking. In contrast, the Consumer Electronics industry has yet to feel much impact.

“Cisco Systems Inc., EMC Corp. and VMware Inc. unveiled a joint venture to help sell a new integrated data center product, part of a broader trend by technology companies to offer a wider range of products and services…The partnership between the three companies targets what they call the "private cloud," an offshoot of one of the biggest trends in technology, cloud computing.7

Industry

Cloud’s impact

Rationale

Servers Very High Companies turn to cloud computing to cut hardware capex and control opex.

New and existing servers need to be enabled to serve a cloud infrastructure.

Storage Very High Rapid scalability, on-demand capacity and more accessible services drive the

need for cloud storage.

Networking High Virtualization and grid computing are driving an explosive growth in demand for

bandwidth hungry networking equipment akin to the early public Internet days.

Software High Vendors are positioning SaaS offerings as right-sized, zero-CAPEX alternatives to

on-premise applications, especially to small businesses. Consumer

Electronics

Medium-High Consumer technology is steadily moving to embrace cloud computing, as new generations of devices — including handsets, Internet TVs and game consoles — are introduced with built-in web access to scaled consumer cloud services.

PCs Medium-High Traditional PCs are somewhat removed from the cloud. However, the uptake in

netbooks and tablet PCs could increase its impact.

Semiconductors Medium Despite shrinkage driven by virtualization and rationalization, increased demand for specialized chipsets for new servers and new markets (eg. Google, Amazon and Yahoo represent 25% of the world’s servers installed) will result in a net positive.

As we pointed out earlier in this paper, leading High Tech companies have a dual focus in the cloud computing space. One focus area is realizing the cost, flexibility and scalability benefits of cloud within their own organizations. The second is delivering these same benefits externally to customers. Accenture has proven capabilities in helping support leading players in the technology industries in both of these areas.

Delivering the benefits of cloud

— internally and externally

Accenture’s skills and capabilities mean we understand and can support all the critical cloud capabilities, both in realizing the internal benefits of cloud and offering differentiated cloud service externally. For internal cloud planning and adoption, we help High Tech clients to develop clear, fully-costed cloud strategies, and then proceed to rapid development and implementation, with go-live in a matter of a few months at as little as 25% of the traditionalimplementation costs. We also assist clients in implementing SaaS solutions and integrating them with existing applications rapidly and at low cost. And we can help with cloud-based infrastructure and application rationalization programs that reduce support costs by 40%.

We bring these same differentiated capabilities to bear in partnering with cloud providers to optimize their services offerings and revenues. As cloud solutions, including

process-as-a-service offerings, gain traction in vertical markets, our industry knowledge will provide clear competitive edge to High Tech companies working with us. Our pioneering work in cloud-enabled BPO services means we have the expertise and experience to help our clients in the technology industries take cloud services to the next level, driving the delivery of flexible, one-to-many process-as-a-service offerings with costs linked directly to consumption.

Six key capabilities to help High

Tech clients take cloud to the

next level

As the cloud ecosystem evolves, Accenture’s distinctive combination of hands-on experience in creating and running cloud-based services with our acknowledged global leadership in technology, technology independence, industry expertise and business process outsourcing (BPO) assets is proving its worth. This unique blend means Accenture is uniquely positioned and qualified to collaborate with High Tech companies in designing, building and delivering the right cloud offerings for the right customers at the right price. Furthermore, we can help our alliance companies to expand and improve their own customer base, by providing a valuable and highly credible channel to market.

Accenture’s unique positioning as a cloud

partner

Accenture’s experience to date suggests that successful creation and management of cloud offerings depends critically on six key capabilities. We are helping several High Tech clients address gaps in each of these capabilities through our consulting approach and our “solution accelerators” solutions that include the embedded management and monitoring that are critical to success. The six key capability areas are: 1. Pricing: Today, cloud pricing varies widely across the different segments of cloud, with different models being applied including per-user per-month, milestone payments, subscriptions, per cpu, per Gigabyte of memory, and per Gigabyte of bandwidth consumed. The key is to be able to offer flexibility in the pricing model, and thereby become responsive to customers’ specific requirements. While transactional pricing may sound good in theory, in reality customers tend to shy away from it because of concern over unbudgeted costs. This means SaaS pricing has become more an “entrepreneurial art” rather than an accounting-based science. In the longer term, fully accountable pricing for usage will be a vital element of business models going forward. 2. Billing and metering: Sophisticated billing and metering in hardware or software represent a key prerequisite for a successful move into SaaS/IaaS. EMC has a proven, leading practice in the storage industry, partly thanks to embedded management and monitoring at the product level, a key advantage in enabling effective billing. 3. Service-level agreements (SLAs): Service-level agreements are vitally important, since most software and hardware companies tend to have limited experience in providing a service and signing up for service penalties, credits, data loss clauses, and so on. As a result, we find that SLAs can be an especially contentious issue in discussions around contracting for cloud services from providers. The maturing cloud will bring "5-9"

SLAs, 99.999% availability, and bring significant implications for platform-as-a-Service and infrastructure-as-a-Service providers.

4. Channel management and partnering: Smart and carefully-targeted partnering helps High Tech companies to build new cloud-related competencies in software development and delivery, integration, collaboration, and community-building. For

ISVs, existing sales channels and partnerships are extremely important. So SaaS, a very direct sales model, must be clearly delineated from other models via architectural clarity, or there is a risk that channel relationships may be undermined. Issues around customer data privacy can also raise issues in partner agreements.

5. Salesforce training and enablement: The sales process is becoming more complicated and sophisticated, but also less emotional and more rational. These shifts mean completely new skill sets are required, including a higher level of business-oriented and industry-relevant sales skills, and a background in selling ongoing services (rather than product sales) for account holders. Furthermore, companies need to re-think their compensation model for their salesforce, because what used to be a large software sale at the end of the quarter is now spread out over several years. The compensation challenge also applies to the channel, since companies need to work out how to compensate channel partners who sell or embed their cloud services in what they do.

A further factor related to the salesforce is that the central IT function in many enterprises now accepts that SaaS is here to stay, and has reclaimed the purchasing decision from the end-user executives who tended to be the acquirers of the first wave of SaaS offerings. Going forward, the sell/buy process will become more complex as more stakeholders become involved and more is at risk.

SaaS providers need to be skilled at balancing a business message for end-user executives with a technology message for IT.

6. Customer care and support: The shift from a product-oriented to service-oriented model means enterprises have changing needs in terms of accountability and the single point of contact. The fact that end users will be able to deploy an integrated application stack at the click of a mouse drives dramatic changes in their wants and needs in term of support from their vendors. Remote support solutions and online customer care analytics will free up vendors to focus resources on higher-value support interactions, and to reach an affordable price point through robust channel management and diagnostic capabilities.

Supporting multiple types of

services

Leading players in the technology industries can realize value from the cloud in multiple ways: by entering the infrastructure space and/or the platform, applications and processes space, or possibly all of these at once. Accenture can support all cloud strategies, including investing jointly with clients to help create the next generation of cloud-enabled BPO offerings.

References

1 IDC, Cloud Computing 2010 - An IDC Update, Doc # TB 20090929, September 2009

2 Gartner, Forecast: Sizing the Cloud; Understanding the Opportunities in Cloud Services, March 18, 2009 Chart created by Accenture based on Gartner data

3 The Wall Street Journal, 4 November 2009

4 The New York Times, February 1, 2010 Move Source to end of Paper 5 Gartner, Forecast: Public Cloud Services, Worldwide and Regions, Industry Sectors, 2009-2014, June 2, 2010

Chart created by Accenture based on Gartner data

6 Gartner, Market Trends: Software as a Service, Worldwide, 2008-2013, November 4, 2009

Chart created by Accenture based on Gartner data

7 The Wall Street Journal, 4 November 2009

8 Accenture Proprietary Research, 2010

ACC10-1399

Copyright

©

2010 Accenture All rights reserved.Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

About Accenture

Accenture is a global management consulting, technology services and outsourcing company, with more than 190,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$21.58 billion for the fiscal year ended Aug. 31, 2009. Its home page is www.accenture.com.

Contact

To find out how Accenture can help your High Tech business capitalize on the opportunities presented by cloud, please contact:

Philippe Roussiere

[email protected] Philippe Roussiere leads Accenture’s global Communications & High Tech research team. To our clients he brings the insights gathered from Accenture’s Electronics and High Tech Industry program as well as market and competitive analyses in topics related to convergence of communications, content and technology. Philippe has 20-years of experience in research in Asia, the US and Europe.

Robin Murdoch

[email protected] Robin Murdoch, an executive out of the Seattle office, leads Accenture’s global portal industry segment within Accenture’s Media & Entertainment practice. He directs strategic programs with internet companies and interactive divisions of global media companies. Robin also leads Accenture’s Management Consulting Cloud Initiatives.