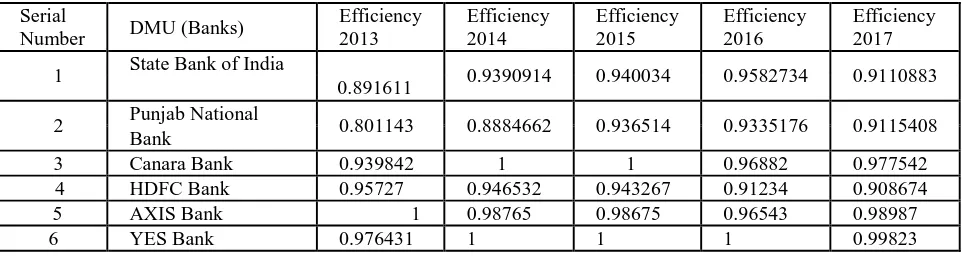

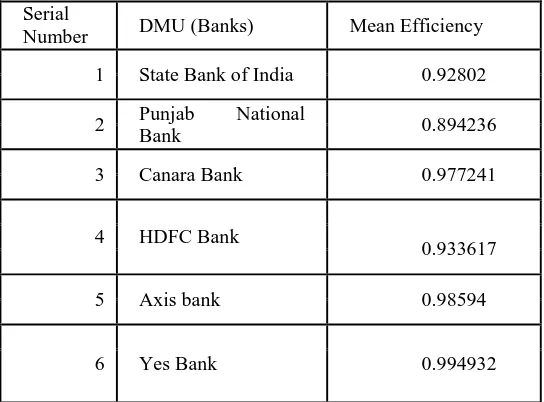

MEASURING EFFICIENCY OF PUBLIC SECTOR BANKS AND NEW GENERATION PRIVATE SECTOR BANKS IN INDIA

Full text

Figure

Related documents

An application of beneficial soil microbes such as Trichoderma and Pseudomonas fluorescens individually or in combination starting from black pepper vines seedling

In these experiments made to yalue accumulated residues from many dress- ings of P fertilisers, all crops gave larger yields on enriched soils than on starved

As a reaction to that view, error analysis, a branch of applied linguistics, flourished in the sixties by the works Stephen Corder to demonstrate that learner errors were

155 The Iranian regime was consistently accused by the United States of its nuclear ambitions, its support of terrorists, and its rebuff of the ―Middle East peace process‖

Hezbollah ’s success: military achievements in fighting the Israeli occupation of Lebanon played a significant role in Hezbollah ’s success; social and economic services to the poor

Lisa Blouin, Hollywood Fire Department, LH35 Alumni Anthony Vera, Hollywood Fire Department, LH38 Alumni Major Thea Basler, Hollywood Police Department, LH38 Alumni

For fault at F, the relay R5 shall operate to open CB-6 before R1 opening CB2 so that the PV system’s contribution to fault is less and also PV system will

The evidence from these reviews sug- gests that financial incentives at the individual level of the social ecological model appear to have some posi- tive effects on physical