A generalized credit value adjustment

Mats Kjaer

Quantitative Analytics, Barclays Capital, 5 The North Colonnade,

Canary Wharf, London E14 4BB, UK; email: [email protected]

In this paper we prove three results about the valuation of over-the-counter deriva-tive portfolios under counterparty risk. First, we derive a generalized credit value adjustment (CVA) under the assumption that both parties can default. Second, we show how this CVA can be hedged in a simple bilateral credit model using single-name credit default swaps and vanilla options on the underlying portfolio. Third, we prove the conditions under which adding a CVA to the counterparty default risk-free mark-to-market value of a portfolio is equivalent to discounting the portfolio cashflows with the risky curve of the counterparty. The generalized CVA derived in this paper contains the standard bilateral CVA as well as non-standard CVAs such as the so-called extinguisher and set-off CVAs as special cases.

1 INTRODUCTION

The importance of correctly pricing and hedging counterparty risk in over-the-counter (OTC) transactions became very clear during the turbulent market events of the sum-mer and autumn of 2008. However, valuing securities under the assumption that the parties of the transaction could default has a longer history than that. Perhaps the first example is the pricing of corporate bonds, where the price discount compared with the equivalent government bond1can be seen as a compensation for credit risk.2 The introduction of OTC contracts like swaps and options in the 1970s triggered the development of derivative valuation techniques for the case when one of the parties may default. An early paper on the topic by Johnson and Stulz (1987) shows how

The author thanks Vladimir Piterbarg, Christoph Burgard and Tom Hulme of the Quantitative Analytics Group at Barclays Capital for proposing improvements to the manuscript and for fruitful discussions regarding the role of the funding curve in the context of counterparty risk. This paper represents the views of the author alone and not the views of Barclays Capital or Barclays Bank Plc. 1We assume that governments cannot default since they can print money in order to pay off their debts, which is the case at least for the US.

the valuation of vanilla options changes when the option writer may default. They refer to these options as vulnerable options, and use a Merton-type structural credit model. Jarrow and Turnbull (1995) extend this work by using reduced-form credit models and by considering vulnerable options on risky corporate zero-coupon bonds, where both the option writer and the zero-coupon bond issuer may default. Sorensen and Bollier (1994) discuss the valuation of vulnerable swaps, where both parties can default, and show how the credit risk can be hedged using swaptions and credit default swaps (CDSs).

An OTC derivative is a legally binding contract between the two parties and, in order to simplify the paperwork, the legal contract is usually derived from the 2002 International Swaps and Derivatives Association (ISDA) Master Agreement.3 This document stipulates that the main mechanism used to reduce counterparty risk is netting, that is, trades with positive value are offset against trades with negative value when determining the claim submitted to the bankruptcy administrators. In addition to netting, the ISDA Master Agreement offers two more optional mechanisms for reducing counterparty risk. The first one is a so-called credit support annex, which details the posting of collateral. The second mechanism is an additional termination event, which allows a party to terminate a portfolio if the credit rating of the other party falls below a predetermined threshold. This paper will not discuss credit support annexes or additional termination events.

As discussed in Redon (2006), the Basel II agreement requires financial institu-tions to monitor their exposure given default to their counterparties. Moreover, new fair-value accounting rules require that the reported mark-to-market values of OTC portfolios include a credit value adjustment (CVA) to reflect counterparty risk.

Because of the presence of netting in the 2002 ISDA Master Agreement, the results of Johnson and Stulz (1987) and Jarrow and Turnbull (1995) cited above are not applicable, since they only deal with single options (and hence extend to nonnetted portfolios). Papers, book chapters and books that develop methodologies for valuation of derivative portfolios under counterparty risk include, but are not limited to, Brigo and Mercurio (2007), Brigo and Chourdakis (2008), Li and Tang (2007), Gregory (2009), Alavianet al(2008), Redon (2006) and Pykhtin and Zhu (2007). The main result of the references cited above is a generic formula for an additive CVA that holds regardless of the model used for the asset price and credit. More specifically, the total value of a portfolio including counterparty risk is given by the portfolio value, calculated assuming all transaction parties are default free (referred to as the “counterparty risk-free value” in this paper), minus a CVA. This result has influenced the way that many financial institutions organize their trading and hedging. The nor-mal desks (fixed income, commodities, foreign exchange, etc) value and hedge the

counterparty-credit risk-free value, whereas pricing and hedging of the CVA part is performed by a separate CVA desk.

Until the start of the credit crisis in the summer of 2007, the credit spreads of most financial institutions were so small compared with those of the counterparties that most models that were used to calculate the CVA assumed that the financial institution could not default. The resulting CVA is referred to as the unilateral CVA. As the spreads widened, however, the need for a so-called bilateral CVA,4which takes into account the fact that both parties can default, arose. A derivation of the standard bilateral CVA formula can be found in many of the references cited above (see, for example Brigo and Capponi (2008)). Gregory (2009) also derives this model but criticizes it for implicitly assuming that the parties can short their own credit. In Section 5 we discuss this topic further and demonstrate how a party may short its own credit in practice as part of a hedging strategy. This result is very similar to the one derived in Burgard and Kjaer (2010), although that paper uses delta hedging and partial differential equation techniques, whereas this paper uses a semistatic replication. Burgard and Kjaer (2010) also derive a bilateral CVA formula in the presence of positive funding spreads.

Other recent papers on counterparty risk include Blanchett-Scalliet and Patras (2008), Brigo and Capponi (2008), Brigo and Chourdakis (2008), Brigo and Pallavicini (2007), Crépey et al (2009), Jarrow and Yu (2001), Leung and Kwok (2005) and Lipton and Sepp (2009). These papers primarily study counterparty risk for CDSs.

The derivations of the unilateral and bilateral CVA formulas both assume that the cashflows at default to be the ones specified in the ISDA Master Agreement. Sometimes, however, parties agree other terms, such as “extinguishers”, where the surviving party never has to pay the defaulting party, or “set-offs”, which allow the surviving party to pay any obligations with bonds issued by the defaulting party at face value. Extinguishers and set-off contracts may be unilateral or bilateral and result in different CVA formulas compared with the regular unilateral or bilateral CVAs implied by the ISDA Master Agreement.

In this paper we extend the results given in the papers and books cited above in three directions. First, we derive a generalized CVA formula, from which the unilateral and bilateral CVA, extinguisher CVA and set-off CVA follow as corollaries. The first benefit of this result is a clearer link between the contractual cashflows occurring given a default and the resulting CVA formula. The second benefit is that many different types of CVA can be computed with one formula. Second, we extend the work of Sorensen and Bollier (1994) and propose a discrete hedging strategy for the CVA in a simple credit model where the two default times are independent of each other and all

the asset prices. The replicating portfolio contains options on the portfolio as well as single-name CDSs on the two parties, and we prove that the hedge error goes to zero as the hedging frequency goes to infinity. As part of the hedging section, we show that the strategy always generates enough cash at the right times to allow a party to buy and sell protection on itself and the counterparty. We believe that this hedge strategy will be helpful when risk-managing counterparty risk in practice. The third result shows under what circumstances subtracting a CVA from the counterparty risk-free value is equivalent to replacing discounting the cashflows with the risky rate of the counterparty. An implication of this result is that it is easy to compute the CVA of highly exotic derivatives, as long as the cashflows are always nonnegative.

This paper is organized as follows. In Section 2 we review the existing CVA models from the papers cited above and set some notation. Section 3 presents the model assumptions behind the generalized CVA derived in Section 4. Having derived the generalized CVA, Section 5 shows how it can be hedged in a simple credit model. The equivalence between CVA and discounting with the risky rate of the counterparty is discussed in Section 6 before giving some numerical examples in Section 7. We conclude in Section 8. Lengthy proofs are found in Appendix A and Appendix B.

2 NOTATION AND EXISTING CVA MODELS

In this section we will introduce some notation and review the standard unilateral and bilateral CVA formulas derived in many of the papers, book chapters and books cited in Section 1: see, for example, Brigo and Capponi (2008) or Gregory (2009).

Let.˝;F; P;Ft/be a filtered probability space satisfying the usual conditions as defined in Protter (1990). HereFt D .Gt [Ht/, whereGt contains all market information (including credit spreads) up to timetandHt carries information about the default times. The probability measure P is the equivalent martingale pricing measure corresponding to the numeraire processN.t / > 0and expectations with respect to this measure are denoted byE.

The two parties are labeled B (“the issuer”) and C (“the counterparty”) and their default times are denoted byBandC, respectively, and their recovery rates byRB andRC, respectively. Moreover, we let the first default time be given by B^C and assume that the last cashflow of the OTC portfolio occurs at timeT >0. Finally, we letV .t / be the value of the portfolio to issuer B at timet > 0, assuming that

neither of the parties can default. Similarly,V .t /O is the value of the portfolio if the parties can default.

All the derivations of the standard bilateral CVA cited in Section 1 implicitly or explicitly make the following assumptions on the cashflows given default.

(2) The defaulting party pays the surviving party as much as it can if it owes money (ie,V . / > 0from the perspective of the surviving party). This is modeled as paying a known recovery rate times the money it owes.5

Under the assumptions above, and using the notationVC.t /max.V .t /; 0/and

VC.t / min.V .t /; 0/, many of the papers cited in Section 1 (see, for example,

Gregory (2009)) show thatV .t /andV .t /O are linked through the relation:

V .t /D OV .t /C .t / (2.1)

where the regular bilateral CVA .t /is given by:

.t /D.1RB/E

V. /1fDB;6Tg

N.t / N. / ˇ ˇ ˇ ˇFt

C.1RC/E

VC. /1fDC;6Tg

N.t / N. / ˇ ˇ ˇ ˇFt

(2.2)

By also assuming that party B cannot default in Equation (2.2), we obtain the regular unilateral CVA.t /as:

.t /D.1RC/E

VC. /1fC6Tg

N.t / N. / ˇ ˇ ˇ ˇFt

(2.3)

The CVAs in Equations (2.2) and (2.3) are entirely general in that they hold for any combination of credit and market models. In order to actually compute the CVA, however, we need to specify models for the distribution of B, C and V .t /. An important feature of a model is its capability to capture wrong-way and right-way risk, a concept discussed in detail in Loosely speaking, it means that the nature of the dependence between the portfolio value and the default time is such that default occurs when exposures are higher than expected (wrong-way risk) or lower than expected (right-way risk). The simplest and most common credit model, which we shall refer to hereafter as the fully independent CVA model, independent CVA model, assumes that the default timesBandCare the first jump times times of two independent time inhomogeneous Poisson processes with deterministic hazard ratesB and andC, respectively. These default times are also assumed to be independent of the portfolio valueV .t /, so it follows that this model cannot capture wrong-way and right-way risk. Under this assumption the bilateral CVA (2.2) becomes:

.t /D.1RB/

Z T

t

E.t; u/fB.t; u/GC.t; u/du

C.1RC/

Z T

t

E.t; u/fC.t; u/GB.t; u/du (2.4)

where:

E.t; u/DE

V.u/N.t / N.u/

ˇ ˇ ˇ ˇFt

is the negative expected exposure

E.t; u/DE

VC.u/N.t / N.u/

ˇ ˇ ˇ ˇFt

is the positive expected exposure

GB.t; u/Dexp

Z u

t

B.s/ds

is the conditional probability of party B

GC.t; u/Dexp

Z u

t

C.s/ds

is the conditional probability of party C

fB.t; u/DB.u/GB.t; u/ is the conditional density ofB

fC.t; u/DC.u/GC.t; u/ is the conditional density ofC

Similarly, the unilateral CVA (2.3) becomes:

.t /D.1RC/

Z T

t

E.t; u/fC.t; u/du (2.5)

In practice, we may only have the positive and negative expected exposures available at the discrete set of fixed6exposure datesfT

ngNnD0withT0 D0,TmDtandTN DT. If this is the case, the integrals (2.4) and (2.5) are often discretized as:

N.t /D.1RB/ N1

X

nDm

Em;npm;n;nC1qm;nC1

C.1RC/ NX1

nDm

Em;npm;n;nC1qm;nC1 (2.6)

N.t /D.1RC/ NX1

nDm

Em;npm;n;nC1 (2.7)

whereEi;nDE.Ti; Tn/,Ei;nDE.Ti; Tn/and:

pi;j;k DGB.Ti; Tj/GB.Ti; Tk/

pi;j;k DGC.Ti; Tj/GC.Ti; Tk/

qi;k DGB.Ti; Tk/

qi;k DGC.Ti; Tk/

TABLE 1 Cashflow scenarios at default.

Scenario V./ > 0 V./ < 0

DB, < T ˛V . / ˇV . / DC, < T V . / ıV . / DBDC, < T "V . / V . /

withTi 6 Tj 6 Tk. The advantage of this discretization of the integral (2.4) over some other scheme (eg, Simpson, Gauss–Legendere) is that the total probability mass is preserved for any number of exposure datesN, and not only whenN ! 1.

It is also possible to assume thatB andCare joined by a copula but are still of

V .t /. Alternatively, each default time could be modeled as the first jump of a Cox process whose hazard rate is correlated with the hazard rate of the other party as well as withV .t /, but the Poisson jumps are independent of each other andV .t /. If the portfolio contains CDSs, it may be desirable to create a stronger dependence between the default times and the portfolio value. Brigo and Chourdakis (2008) propose using stochastic hazard rates joined by a copula model in this case.

The remainder of the paper will deal with generalizing Equation (2.2) and we will not assume any particular credit model, except for in Sections 5 and 7, where we will use the fully independent CVA model described above.

3 ASSUMPTIONS ON CONTRACTUAL CASHFLOWS GIVEN DEFAULT

Having fixed the notation in Section 2 we now state the generalized default-time cashflow scenarios in Assumption 3.1 below.

Assumption3.1 (Cash flows given default) Let˛,ˇ,,ı,", andbe real numbers inŒ0; 1. Then we assume that the cashflows from counterpartyCto issuerBat the default time Dmin.B; C/are given by Table 1.

In Assumption 3.1 we allow for simultaneous defaults as in Gregory (2009). In practice, a simultaneous default reflects the fact that a bankruptcy may take months to settle, during which it is possible for the surviving party to default as well. The default of the first party may even contribute to the default of the second party, a phenomenon known as default contagion. When this happens, the party that defaulted first would receive less than the full amount if it was owed money.

[image:7.595.119.474.124.189.2]4 THE GENERALIZED CREDIT VALUE ADJUSTMENT FORMULA

We start this section by introducing some notation. The contracts of the portfolio are assumed to generate a sequence of random cashflowsf.tm; Ym/gMmD1 satisfying the following conditions:

(1) tmis anFtstopping time;

(2) Ym2FtmandYm2L

1.˝;F; P /;

(3) tmandYmdo not depend on any credit information about parties B and C.

The last condition is necessary for the standard resultV .t /O DV .t / .t /to hold, and excludes all Bermudan and American options as well as all physically settled European options. The intuition behind this is that an optimal exercise decision when maximizingV .t /O rather thanV .t /will depend on the credit of the two parties.

Next we define the random variableC.t; T /for06t6T as:

C.t; T /D M

X

mD1

Ym

N.tm/

1ft6tm<Tg (4.1)

which can be interpreted as the sum of numeraire-adjusted cashflows inŒt; T /. This random variable satisfiesC.t; t /D0and:

C.t; T1/DC.t; T0/CC.T0; T1/ (4.2)

for t 6 T0 6 T1, which ensures that there is no double counting of cashflows. Moreover, it follows thatC.t; T /2L1.˝;F; P /, so, by standard derivatives pricing theory, the counterparty-credit risk-free valueV .t /of the portfolio at some timet is given by:

V .t /DN.t /EŒC.t; T /jFt (4.3)

With the different default scenarios in Assumption 3.1 in mind, we define the four disjoint default scenariosSA,SB,SCandSDas:

SAD fB > Tg \ fC> Tg

SB D fB < Cg \ fB6Tg

SC D fC < Bg \ fC6Tg

SDD fC DBg \ fC6Tg

which implies that:

1D1SAC1SBC1SCC1SD (4.4)

Lemma4.1 LetC.t; T /denote the sum of numeraire-adjusted cashflows as defined in (4.1). Then, fork DB;C;D, it holds that:

EŒC.k; T /1SkN.t /jFtDE

V .k/1Sk

N.t / N.k/

ˇ ˇ ˇ ˇFt

whereDD.

Proof See Appendix A.

Proposition4.2 (Generalized CVA) Let the cashflows from the portfolio under the default scenariosSA–SD be the ones given in Assumption 3.1. Then the total

portfolio valueV .t /O at timet >0satisfies:

O

V .t /DV .t / .t /

where the generalized CVA .t /is given by:

.t /DE

f.1˛/1SBC.1 /1SCC.1"/1SDgV C

. /N.t / N. / ˇ ˇ ˇ ˇFt CE

f.1ˇ/1SBC.1ı/1SCC.1/1SDgV

. /N.t / N. / ˇ ˇ ˇ ˇFt

Proof See Appendix B.

If the probability of a simultaneous default is zero, then .t /simplifies to:

.t /DE

f.1˛/1SBC.1 /1SCgV C

. /N.t / N. / ˇ ˇ ˇ ˇFt CE

f.1ˇ/1SBC.1ı/1SCgV

. /N.t / N. / ˇ ˇ ˇ ˇFt (4.5)

If party B cannot default, we obtain the generalized unilateral CVA of Corollary 4.3 below.

Corollary4.3 (Generalized unilateral CVA) The generalized unilateral CVA.t /

is given by:

.t /DE

f.1 /VC. /C.1ı/V. /g1fC6Tg

Proof The assumption that party B cannot default is equivalent to1SBD ;,1SC D

1fC6Tgand1SD D ;. Inserting these identities into Proposition 4.2 then gives the

result.

We conclude this section by showing that some common variations of CVA, such as the standard bilateral CVA, are special cases of the CVA that was presented in Proposition 4.2.

LetRBswap,Rbond

B ,R

swap

C R

swap

C andRbondC denote the swap and bond recovery rates for B and C, respectively. Then the generalized CVA (4.5) can be used to construct the following:

The standard bilateral CVA. This CVA corresponds to setting˛ D 1, ˇ D RswapB ,

DRswapC andıD1in the CVA formula (4.5).

The set-off CVA. This CVA is obtained by setting˛D1,ˇDRBswap, DRCswapand

ıDRbond

C , which means that if party C defaults first and is owed money, then party B can pay with the defaulting party’s bonds (counted at par) instead of cash.

The one-sided extinguisher CVA. This CVA is obtained by setting˛D1,ˇDRswapB ,

DRswapC and D RCswap andı D 0, which means that if party C defaults first and is owed money,

The two-sided extinguisher CVA. This CVA is obtained by setting˛D0,ˇDRswapB ,

D RCswap ı D 0, which means that the surviving party does not have to pay anything if owing the defaulting party money.

From Proposition 4.2 it follows that if˛Dˇ, Dıand"D, then:

.t /DE

f.1˛/1SBC.1 /1SCC.1"/1SDgV . /

N.t / N. / ˇ ˇ ˇ ˇFt

We conclude this section by noting that, in the full independence model presented in Section 2, the generalized CVA in Proposition 4.2 becomes:

.t /D

Z T

t

f.1˛/E.t; u/C.1ˇ/E.t; u/gfB.t; u/GC.t; u/du

C

Z T

t

f.1 /E.t; u/C.1ı/E.t; u/gfC.t; u/GB.t; u/du (4.6)

The discretized version N of (2.4) is given by:

N.t /D NX1

nDm

f.1˛/Em;nC.1ˇ/Em;ngpm;n;nC1qm;nC1

C NX1

nDm

f.1 /Em;nC.1ı/Em;ngpm;n;nC1qm;nC1 (4.7)

where again we assumed thattDTm.

Comparing the generalized CVA (4.6) with the regular bilateral CVA (2.4) (or the corresponding formulas for N) shows that, in the full independence model, we can compute a generalized CVA with the same formula as the regular bilateral CVA (2.4), provided that we modify the positive and negative exposures and use zero recovery rates. This approach is practical since very little extra work is needed to implement the generalized CVA formula once the regular bilateral CVA is implemented.

5 HEDGING

In this section we show how we can hedge the generalized CVA (4.6) in the fully independent credit model described in Section 2 using single-name CDSs on parties B and C, together with call and put options on the underlying portfolio. If these options do not trade in the market, we assume that they can be synthetically replicated. The strategy requires some assumptions about hedging transactions that are considered admissible that may not hold in practice. These assumptions are not necessary to hedge the unilateral equivalent of (4.6).

To derive the hedging strategy we start by rearranging (4.7) as:

N.t /D N1

X

nDm

f.1˛/pm;n;nC1qm;nC1C.1 /pm;n;nC1qm;nC1gEm;n

C NX1

nDm

f.1ˇ/pm;n;nC1qm;nC1C.1ı/pm;n;nC1qm;nC1gEm;n

NX1

nDm

m;nEm;nC NX1

nDm

m;nEm;n (5.1)

This way of presenting the CVA N shows that it is equal to a portfolio of long calls and short puts on the underlying portfolio, which is a generalization of the work by Sorensen and Bollier (1994), who show that the CVA of a swap is a default probability weighted portfolio of swaptions.

A default of a party triggers one of the cashflow scenarios specified in Assump-tion 3.1 due to (partial) repayment of the underlying portfolio value. However, there is also a second cashflow coming from liquidating the remaining puts and calls of the CVA hedge, so in general, the CDS notional needed for full protection will not equal the exposure. Before defining our hedging strategy˘N.t /in Definition 5.1 below, we define the forward starting CVA N.t; TmC1/fort 2.Tm; TmC1as:

N.t; TmC1/D NX1

nDmC1

mC1;nE.t; Tn/C NX1

nDmC1

mC1;nE.t; Tn/ (5.2)

so, by definition N.Tm; Tm/ D N.Tm/. Next we define our hedging strategy in Definition 5.1.

Definition5.1 (The hedging strategy˘N) Let˘N.t /denote the value of a port-folio containing the following assets fort2.Tm; TmC1,06m < N:

(1) long calls onV with maturitiesfTngNnDm1C1 and notionalsfmC1;ngNnDm1C1;

(2) short puts onV with maturitiesfTngNnDm1C1and notionalsfmC1;ngNnDm1C1;

(3) short CDS protection on issuer B for the period.Tm; TmC1with notional:

.1˛/Em;mC.1ˇ/Em;m N.TmC; TmC1/

(4) long CDS protection on counterparty C for the period.Tm; TmC1with notional:

It is important to note that the assumption of deterministic hazard rates means that we only have to hedge the default risk and that there is no need to hedge credit-spread movements. By Definition 5.1, it follows that˘N.t / D N.t /only when

t2 fTngNnD01 and we do not know if˘N.t /is self-financing or not, so the question is whether˘N.t /is a good hedge of the CVA (4.6) or not. Proposition 5.2 gives an answer to this question.

Proposition5.2 The strategy˘N.t /introduced in Definition 5.1 satisfies:

lim

N!1˘N.t /D .t /

for allt6T. Moreover,˘N is asymptotically self-financing asN ! 1.

Proof The first claim follows easily by the fact that if the positive and negative expected exposuresE.t; u/andE.t; u/defined in Section 2 are reasonably regular functions ofu, then N.t / ! .t /asN ! 1. The claim now follows from the earlier observation that˘N.Tm/D N.Tm/for allfTmgNmD10.

To prove the asymptotic self-financing property, we first compute the revenue of the portfolio rebalancing transactions at timeTm. Negative revenues should be interpreted as costs and negative long CDS notionals should be interpreted as the notional on which protection has been sold.

(1) Exercise the call and put options expiring atTm. This generates a revenueI1.m/ given by:

I1.m/Dm;mEm;mCm;mEm;m

(2) Increase the remaining long-call-option notionals fromm;ntomC1;nand the remaining short put option notionals fromm;ntomC1;n. The notionals satisfy:

m;nDqm;mC1qm;mC1mC1;n and m;nDqm;mC1qm;mC1mC1;n

so the revenueI2.m/from this transaction is given by:

I2.m/D.qm;mC1qm;mC11/ N.TmC; TmC1/

(3) Buy CDS protection against the default of counterparty C with notional equal to the cashflow given default according to Assumption 3.1 minus the cashflow from liquidating the remaining calls and puts. This results in a revenueI3.m/ given by:

(4) Buy CDS protection against own default with notional equal to the cashflow given default according to Assumption 3.1 minus the cashflow from liquidating the remaining calls and puts. This results in a revenueI4.m/given by:

I4.m/D f.1˛/Em;mC.1ˇ/Em;m N.TmC; TmC1/gpm;m;mC1

Adding the cost and revenues above gives that the total profitI.m/ D I1.m/C

I2.m/I3.m/I4.m/is given by:

I.m/D pm;m;mC1pm;m;mC1f..1˛/C.1 //Em;m

C..1ˇ/C.1ı//Em;mg

Cpm;m;mC1pm;m;mC1 N.TmC; TmC1/

where we have used thatqm;mC1 D 1pm;m;mC1 and qm;mC1 D 1pm;m;mC1.

Before proceeding, we note that the hedging errorI.m/over the period.Tm; TmC1 equals the total cashflow triggered if both parties default in the period.Tm; TmC1 times the probability of this happening. The fact thatI.m/¤0means that the strategy is not self-financing, but we are going to show that the sum of the hedging errors converges to zero asN ! 1, since the probability of a joint default in.Tm; TmC1 is proportional tojTmC1Tmj2whenjTmC1Tmjis “small”.

The total hedging gain (or loss):

IN NX1

mD0

I.m/

is anFT-measurable random variable satisfying:

jINj6 max

06m<Npm;m;mC1 N1

X

mD0

pm;m;mC1j N.TmC; TmC1/j

C max

06m<Npm;m;mC1f.1˛/C.1 /g N1

X

mD0

pm;m;mC1Em;m

C max

06m<Npm;m;mC1f.1ˇ/C.1ı/g N1

X

mD0

pm;m;mC1jEm;mj

WhenN ! 1we have that:

max

06m<Npm;m;mC1!0 max

NX1

mD0

pm;m;mC1 N.TmC; TmC1/!

Z T

t

C.u/j .u/jdu

NX1

mD0

pm;m;mC1Em;m!

Z T

t

C.u/E.u; u/du

NX1

mD0

pm;m;mC1jEm;mj !

Z T

t

B.u/E.u; u/du

where we have used that pm;m;mC1 C.Tm/.TmC1 Tm/ when jTmC1 Tmj is “small”. This in turn implies thatjINj ! 0 almost surely, since the integrals above are finite almost surely because the underlying portfolio generates finitely

many integrable cashflows.

In the above strategy issuer B sells put options and may also sell CDS protection against the default of B and/or C. Any sold protection against the default of C does not require any collateral, since the third party A will only lose a payout if both issuer B and counterparty C default in the same time interval .Tm; TmC1. When

T D jTmC1 Tmj is small, then the probability of this event is proportional to

. T /2, so we could argue that this probability is so small that it can be ignored. Repeating the arguments of the proof of Proposition 5.2 shows that the total cost of this protection converges to zero asN ! 1.

The strategy˘N in Definition 5.1 requires issuer B to sell put options and CDS protection on itself to the risk-free party A. Both these transactions only make sense if issuer B posts collateral with party A to eliminate any losses for A if issuer B defaults. In order for the issuer to be able to cover these collateral requirements using the assets available within the hedging strategy˘N, we need to make the following assumptions:

The issuer B hedges the default-risk-free portfolio valueV and is allowed to post this hedge as collateral with party A at its mark-to-market valueV (eg, whenV < 0) when hedging the CVA. Moreover, the hedge ofV is funded at the risk-free rate.

All long call options can be posted as collateral with party A at their mark-to-market value.

The amountX to be posted as collateral is obtained by adding the value of the put options and the short CDS notional on B, so:

X D NX1

nDMC1

mC1;nEm;n.1˛/Em;m.1ˇ/Em;mC N.TmC; TmC1/

D NX1

nDMC1

mC1;nEm;n.1˛/Em;m.1ˇ/Em;m

LetY denote the value of the assets that issuer B has available to post as collateral. Above, we assume that the long call options can be used by issuer B as collateral at their mark-to-market value, so:

Y D NX1

nDMC1

mC1;nEm;n

which implies that:

Y X D.1˛/Em;mC.1ˇ/Em;m

and it follows that ifEm;m< 0, thenEm;m D0, which in turn implies that the call options alone will not provide sufficient collateral. However, we assume above that issuer B hedges the derivative portfolio and can post the hedge as collateral with party A. HereEm;m< 0means that the account holding the replicated option value contains the positive amountEm;m. Of this amount, a proportionˇof this can be used to pay counterparty C according to the cashflow Assumption 3.1, whereas the proportion.1ˇ/can be posted as collateral with the third party A. In reality,ˇoften represents a recovery rate, which is not known or specified in any ISDA agreement. Since issuer B has no contractual obligations to return any specified proportion of the portfolio value to C, he or she can post any proportion of the replicated portfolio that is required as collateral with the third party A. Note that issuer B only posts collateral with party A in order to be able to hedge the CVA, but does not post any collateral with counterparty C as part of a credit support annex.

the ability to raise funds by selling put options and protection on itself without having to pay any additional unilateral CVA charges to party A.

Of course, the assumptions above about collateral are rather idealistic, but since the bilateral CVA is commonly used, we believe that it is important to show the assump-tions that are needed to make it the initial cost of an admissible hedging strategy. If one believes that these assumptions are too idealistic, one might want to adjust the generalized CVA formula. For example, one could choose not to collateralize the sold put options, and instead pay an additional unilateral CVA to party A on these options. The proof of Proposition 5.2 used the fact thatBandCare assumed to be indepen-dent, which implies that the probability of a simultaneous default in a time interval of length T is proportional to. T /2. One fortunate consequence of this is that the hedging can be done using single-name CDS only. The Marshall–Olkin copula used in Gregory (2009), for example, has a probability of simultaneous default pro-portional to T, so any hedging strategy for this model would need one CDS that pays out if B defaults conditional on C being alive, and another that pays if C defaults conditional on B being alive. We leave it to future research to investigate the hedging of CVA in these more general dependence models. This work is important since there are currently strong systemic fears within the CDS market, making the independence assumption rather unrealistic.

6 CREDIT VALUE ADJUSTMENT AND DISCOUNTING WITH THE RISKY CURVE

The valueP .t; T /O at timetof a zero coupon bond issued by party C is given by:

O

P .t; T /DP .t; T /f1.1RC/P .C6T /g

which is equal toP .t; T /C.t /, where.t /is the regular unilateral CVA of Corol-lary 4.3. Alternatively, the risky zero coupon bond price can be seen as a unit cashflow discounted by the risky discounting curve of party C, also known as the funding curve of party C. This section will under what conditions discounting cashflows with the risky curve of the counterparty is equivalent to adding a CVA to the counterparty-risk-free value of the portfolio as described in Proposition 4.2. The answer is given in Proposition 6.1 below.

Proposition6.1 (Relation between CVA and discounting with the risky curve)

Let the following three conditions be satisfied:

(1) only party C can default;

(2) all cashflowsYmare nonnegative;

Then the credit risky valueV .tO 0/is given by:

O

V .t0/DP .t0; T /f1.1RC/P .t0 < 6T /gEŒC.t; T /jFt0

Proof By the nonnegativity of the cashflowsYmit is sufficient to prove the claim for a single random cashflowY occurring at timeT.

Corollary 4.3, the corollary to Theorem 18 in Chapter 1 of Protter (1990) and the nonnegativity of cashflows yield:

O

V .t0/DV .t0/.1 /N.t /EŒVC. /1f6Tg=N. /jFt0

DV .t0/.1 /N.t /EŒV . /1f6Tg=N. /jFt0

DV .t0/.1 /N.t /EŒN. /EŒY =N.T /jF1f6Tg=N. /jFt0

The independence ofandY yields thatEŒY =N.T /jFDEŒY =N.T /, so:

O

V .t0/DV .t0/.1 /N.t /EŒEŒY =N.T /1f6TgjFt0

DV .t0/.1 /N.t /EŒY =N.T /EŒ1f6TgjFt0

DV .t0/.1 /V .t0/P .t0 < 6T /

DV .t0/f1.1 /P .t0< 6T /g

DN.t0/f1.1 /P .t0 < 6T /gEŒY =N.T /jFt0

If we chooseN.t / DP .t; T /and D RC, this becomes equivalent to discounting

with the risky bond.

Negative cashflows should be discounted with the risk-free rate since they represent the exposure of party C to party B and party B is assumed default free. Burgard and Kjaer (2010) derive a CVA formula for the case when party B is not default free and consequently has to fund itself at a rate higher than the risk-free rate.

If the default time and the portfolio value are dependent, we have a situation referred to in Redon (2006) as wrong-way or right-way risk depending on the direction of the dependence. Wrongly applying Proposition 6.1 in this case and discounting with the funding curve would ignore right-way and wrong-way risk and would hence overestimate or underestimate the CVA.

7 EXAMPLES

In this section we calculate the generalized unilateral and bilateral CVA for some values on the parameters˛,ˇ,,ı,"and. For simplicity, we consider a portfolio containing the single commodity forward specified in Table 2 on the next page. To simplify matters further, we select a hybrid market and credit model with a constant and deterministic risk-free interest rater > 0so that the bank accountB.t /used as numeraire evolves as:

dB.t / B.t / Drdt

Moreover, we assume that the WTI forward priceF .t; T /follows the dynamics:

dF .t; T /

F .t; T / D.1e

.Tt /

C2/dW .t /

where1 > 0,2 > 0and > 0are deterministic constants andW .t /is a Wiener process under the equivalent martingale measure induced by choosingB.t /as the numeraire. Finally, we let the default times B and C be the first jump times of two independent Poisson processes with hazard ratesBandC, respectively. As in Section 2, we takeB andC to be independent of the WTI forward price process

F .t; T /.

The generalized CVA that we are going to compute is given in Equation (4.7), so we need to calculate the positive and negative expected exposures. For the commodity forward in Table 2 on the next page, it is easy to show thatE.t; u/is a call option on a forward contract expiring at timeu, which yields that:

E.t; u/Der.Tt /fF .t; T /˚.d1/K˚.d2/g

E.t; u/Der.Tt /fF .t; T /Kg E.t; u/

where:

d1 D

log.F .t; T /=K/C 12A2.t; u; T / A.t; u; T /

d2 D

log.F .t; T /=K/ 12A2.t; u; T /

A.t; u; T /

A2.t; u; T /D 2 1

2.e

2.Tu/

e2.Tt //

C22.ut /C212 .e

.Tu/

e.Tt //

TABLE 2 Term sheet for the commodity forward used in this section.

Commodity West Texas Intermediate (WTI) crude oil Amount 1 barrel

[image:20.595.121.476.245.357.2]MaturityT October 20, 2016 StrikeK US$85.00

TABLE 3 Market data parameters for the November 2016 WTI contract used in this section

(all parameters are annualized).

Valuation datet August 26, 2009

F .t; T / Varies per moneyness scenario

˛ 0.60

1 0.25

2 0.80

r 4%

B 2%

C 2%

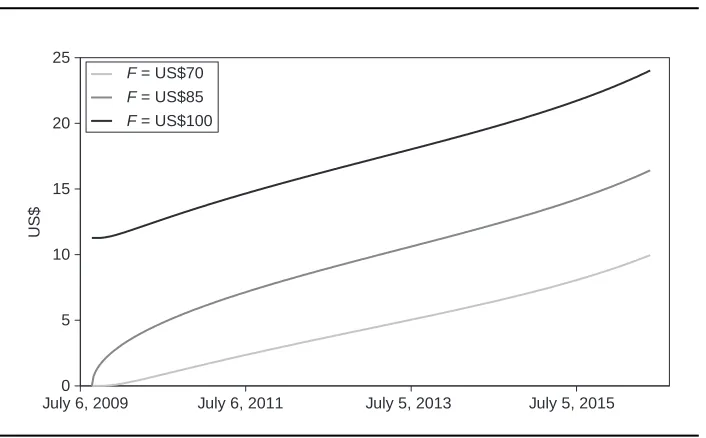

FIGURE 1 Positive expected exposures.

25

20

15

10

5

0

F = US$70 F = US$85 F = US$100

July 6, 2009 July 6, 2011 July 5, 2013 July 5, 2015

US$

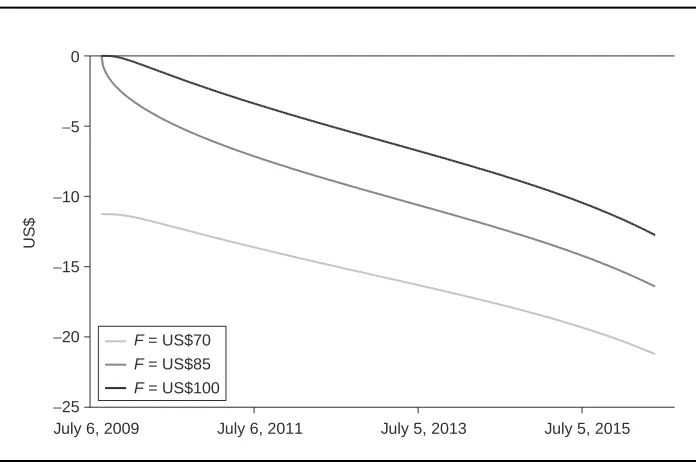

[image:20.595.124.477.398.617.2]FIGURE 2 Negative expected exposures.

F = US$70 F = US$85 F = US$100

US$

−25 −20 −15 −10 −5 0

July 6, 2009 July 6, 2011 July 5, 2013 July 5, 2015

Negative expected exposures for the commodity forward specified in Table 2 on the facing page with market data from Table 3 on the facing page and initial forward pricesF .t; T /DUS$70, US$85 and US$100.

Next, we compute the generalized CVA (4.7) for some different combinations of˛,

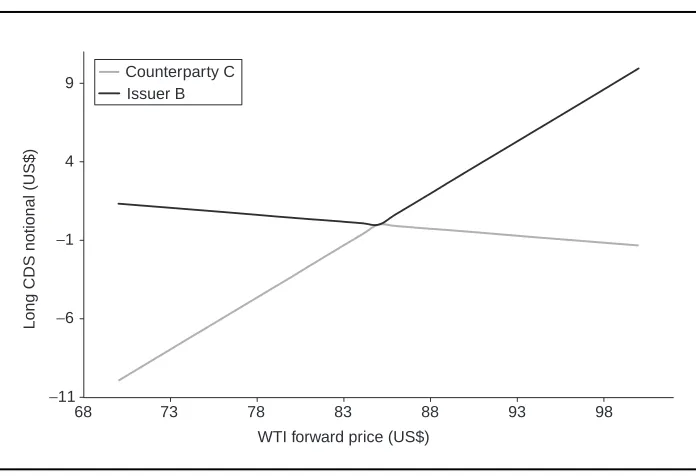

ˇ,andıand three initial values of the WTI forward contract and display the results in Table 4 on the next page. The results show that the CVA varies widely depending on the type of agreement that is in place between the two parties. In particular, the bilateral extinguisher A agreement is also highly sensitive to the initial forward price. Finally, we compute the hedging strategy discussed in Section 5 for the forward in Table 2 on the facing page as a function of the initial WTI forward price in the case of a regular bilateral CVA withRB DRCD0. The results are shown in Figure 3 on the next page.

[image:21.595.124.472.121.352.2]TABLE 4 Generalized CVAs for the forward in Table 2 under three different market

sce-narios.

CVA CVA CVA

CVA type ˛ ˇ ı OTM ATM ITM

Bilateral regular 1.00 0.40 0.40 1.00 0.80 0.00 0.80 Unilateral regular N/A N/A 0.40 1.00 0.33 0.72 1.30 Bilateral extinguisher A 0.00 0.00 0.00 0.00 2.67 0.00 2.67 Unilateral extinguisher A N/A N/A 0.00 0.00 1.42 0.00 1.42 Bilateral extinguisher B 1.00 0.40 0.00 0.00 2.43 0.66 0.93 Bilateral extinguisher C 1.00 0.40 0.00 0.40 1.70 0.22 1.20 Unilateral extinguisher C N/A N/A 0.00 0.40 0.63 0.48 1.72 Bilateral set-off 1.00 0.40 0.40 0.40 1.90 0.66 0.40 Unilateral set-off N/A N/A 0.40 0.40 0.85 0.00 0.85

Here the CVA N.t /given in (4.7) has been evaluated using weekly time steps. Abbreviations: OTM stands for

“on-the-money”, ATM stands for “at-the-money” and ITM stands for “in-the-money”. Here “unilateral” is equivalent to settingBD0. The OTM scenario corresponds toF .t; T /DUS$70, ATM toF .t; T /DUS$85 and ITM to

F .t; T /DUS$100.

FIGURE 3 Long CDS notional.

Counterparty C Issuer B

Long CDS notional (US$)

−11 −6 −1 4 9

68 73 78 83 88 93 98

WTI forward price (US$)

[image:22.595.123.475.142.294.2] [image:22.595.124.472.370.608.2]8 CONCLUSION

In this paper we first proved a generalized CVA formula from which we then derived some commonly used special cases such as the regular unilateral CVA, the regular bilateral CVA, the set-off CVA and the one-sided and two-sided extinguisher CVAs. This result allows for the unified calculation of different types of CVAs. In a numerical example we computed the CVA on an OTC WTI oil forward contract, and we saw that the CVA varies widely depending on the type of agreement that is in place between the two parties.

Next we proposed a hedging strategy of this generalized CVA in a model with deterministic credit spreads. The starting point was a discrete-time hedging strategy, which was shown to be exact and self-financing in the limit of continuous time hedg-ing. We also demonstrated how the strategy contains enough assets to use as collateral in order to enable the issuer to sell put options and CDSs against own default provided that we make some rather idealistic assumptions about the rules for collateral. We also computed the hedge for a bought commodity forward and saw how important it is to have CDS protection in place against counterparty default, even if there is no current exposure.

We continued by demonstrating that, under certain circumstances, counterparty risk may be accounted for simply by discounting with the risky curve of the counterparty. This makes it a lot easier to compute the CVA of portfolios of exotic trades provided that their cashflows are all nonnegative.

All the results so far have relied on the fact that the hedging of the counterparty risk-free valueV can be funded at the risk-free interest rate. Positive funding spreads and counterparty risk are just two sides of the same coin, so in practice, given that both parties B and C can default, it is more likely that this funding occurs at a funding rate higher than the risk-free rate. Given that the funding spreads of financial institutions are currently historically high, adding funding costs to the model would be a natural extension of this paper. Also, the addition of a collateral agreement between B and C would be another possible extension.

APPENDIX A: PROOF OF LEMMA 4.1

Without loss of generality, we prove Lemma 4.1 forkDB only. In the proof we will make extensive use of the corollary to Theorem 18 in Chapter 1 of Protter (1990). It states that ifY 2L1.˝;F; P /andS andT are stopping times, then:

EŒEŒY jFSjFTDEŒEŒY jFTjFS

withS ^T min.S; T /andFS,FT andFS^T being the corresponding stopping time-algebras.

Applying (A.1) withS DtandT D B^C, and recalling that almost surely, yields:

EŒN.t /C.B; T /1SB jFtDEŒN.t /C.B; T /1SBjFt^

DEŒEŒN.t /C.B; T /1SBjFjFt (A.2)

Again, using (A.1) in (A.2) withS DBandT DCgives:

EŒN.t /C.B; T /1SB jFtDEŒEŒN.t /C.B; T /1SB jFB^CjFt (A.3) DEŒEŒEŒN.t /C.B; T /1SB jFBjFCjFt (A.4)

DN.t /EŒEŒEŒC.B; T /jFB1SBjFCjFt (A.5)

because1SBis known conditional onBandC.

Next, we prove that the inner expectation of (A.5) satisfies:

EŒN.B/C.B; T /jFBDV .B/ (A.6)

To do this, we first rewrite (4.3) as:

V .t /=N.t /DEŒC.t; T /jFt

D M

X

mD1

EŒYm=N.tm/jFt1ft6tmg

D M

X

mD1

Vm.t /1ft6tmg (A.7)

Moreover, ifBmB^tm, then:

EŒC.B; T /jFtD M

X

mD1

EŒYm=N.tm/jFB1ft6tmg

D M

X

mD1

EŒYm=N.tm/jFm

B 1fB6tmg

D M

X

mD1

EŒVm.tm/jFm

B 1fB6tmg (A.8)

by (A.7) and the fact that1fB6tmgD0if

m

of Protter (1990) or Chapter 4 in Durrett (1995)) gives that:

EŒVm.tm/jFm

BDVm.

m

B/ (A.9)

so combining (A.9) and (A.8) allows us to write:

EŒC.B; T /jFtD M

X

mD1

Vm.Bm/1fB6tmg

D M

X

mD1

Vm.B/1fB6tmg

DV .B/=N.B/

Having proved (A.6), we continue by inserting it into (A.5), which yields:

EŒN.t /C.B; T /1SB jFt

DEŒN.t /EŒEŒV .B/=N.B/jFB1SBjFCjFt (A.10)

DEŒN.t /EŒEŒV .B/=N.B/1SB jFBjFCjFt (A.11)

DEŒN.t /EŒV .B/=N.B/1SB jFjFt (A.12)

DEŒN.t /V .B/=N.B/1SB jF^t (A.13)

DEŒN.t /V .B/=N.B/1SB jFt (A.14)

Here (A.12) and (A.13) follow by using (A.1) withS D B,T D C andS D ,

T Dt, respectively. Finally, (A.14) is a consequence of the fact that >t almost surely.

APPENDIX B: PROOF OF PROPOSITION 4.2

By standard arbitrage-free pricing theory, V .t /O is given by valuing the cashflows given the default scenariosSA,SB,SCandSD, so:

O

V .t /DEŒC.t; T /N.t /1SA jFt

CE

C.t; B/N.t /C˛VC.B/

N.t / N.B/

CˇV.B/

N.t / N.B/

1SB

ˇ ˇ ˇ ˇFt CE

C.t; C/N.t /CVC.C/

N.t / N.C/

CıV.C/

N.t / N.C/

1SC

ˇ ˇ ˇ ˇFt CE

C.t; /N.t /C"VC. /N.t / N. / CV

. /N.t / N. /

By (4.4) it follows that:

1SA D11SB1SC1SD

so after substituting this into (B.1) we obtain:

O

V .t /

DEŒC.t; T /N.t /jFt

CE

.C.t; B/C.t; T //N.t /C˛VC.B/

N.t / N.B/

CˇV.B/

N.t / N.B/

1SB

ˇ ˇ ˇ ˇFt CE

.C.t; C/C.t; T /N.t /CVC.C/

N.t / N.C/

CıV.C/

N.t / N.C/

1SC

ˇ ˇ ˇ ˇFt CE

C.t; /C.t; T /N.t /C"VC. /N.t / N. /CV

. /N.t / N. /

1SD ˇ ˇ ˇ ˇFt (B.2)

Invoking the relation:

C.t; T /DC.t; /CC.; T /

then yields:

O

V .t /DEŒC.t; T /N.t /jFt

E

C.B; T /N.t /˛VC.B/

N.t / N.B/

ˇV.B/

N.t / N.B/

1SB

ˇ ˇ ˇ ˇFt E

C.C; T /N.t /VC.C/

N.t / N.C/

ıV.C/

N.t / N.C/

1SC

ˇ ˇ ˇ ˇFt E

C.; T /N.t /"VC. /N.t / N. / V

. /N.t / N. /

1SD ˇ ˇ ˇ ˇFt (B.3)

Applying (4.3) to the first line of (B.3) and using Lemma 4.1 in the three last lines of (B.3) then results in the equality:

O

V .t /DV .t /E

fV .B/˛VC.B/ˇV.B/g

N.t / N.B/

1SB ˇ ˇ ˇ ˇFt E

fV .C/VC.C/ıV.C/g

N.t / N.C/

1SC ˇ ˇ ˇ ˇFt E

fVD"V C

. /V. /gN.t /

N. /1SD ˇ ˇ ˇ ˇFt (B.4)

SinceV .t / D V .t /CCV .t / andk D onSk fork D A;B;C;D, .t /may finally be rewritten as:

.t /DE

f.1˛/VC. /C.1ˇ/V. /gN.t /

N. /1SB ˇ ˇ ˇ ˇFt

CE

f.1 /VC. /C.1ı/V. /gN.t /

N. /1SC ˇ ˇ ˇ ˇFt

CE

f.1"/VC. /C.1/V. /gN.t /

N. /1SD ˇ ˇ ˇ ˇFt

(B.6)

from which the desired result follows by rearranging the terms.

REFERENCES

Alavian, S., Ding, J., Whitehead, P., and Laiddicina, L. (2008). Counterparty valuation adjustment (CVA). Working Paper.

Bingham, N., and Kiesel, R. (1998). Risk-Neutral Valuation. Springer.

Blanchett-Scalliet, C., and Patras, F. (2008). Counterparty risk valuation for CDS. Working Paper.

Brigo, D., and Mercurio, F. (2007). Interest Rate Models: Theory and Practice, 2nd edn Springer.

Brigo, D., and Pallavicini, D. (2007). Counterparty risk and contingent CDS valuation under correlation between interest-rates and default. Working Paper.

Brigo, D., and Capponi, A. (2008). Bilateral counterparty risk valuation with stochastic dynamical models and application to credit default swaps. Working Paper.

Brigo, D., and Chourdakis, K. (2008). Counterparty risk for credit default swaps: impact of spread volatility and default correlation. Working Paper.

Burgard, C., and Kjaer, M. (2010). PDE representations of options with bilateral counter-party risk and funding costs. Working Paper.

Canabarro, E., and Duffie, D. (2003). Measuring and marking counterparty risk. In Asset

Liability Management of Financial Institutions, Tilman, L. M. (ed). EuroMoney Books,

London.

Cesari, G., Aquilina, J., Charpillon, N., Filipovic, X., Lee, G., and Manda, L. (2009).

Mod-elling, Pricing and Hedging Counterparty Credit Exposure: A Technical Guide. Springer

Finance, New York.

Crépey, S., Jeanblanc, M., and Zagari, B. (2009). Counterparty risk on a CDS in a Markov chain copula model with joint defaults. Working Paper.

Durrett, R. (1995). Probability: Theory and Examples, 2nd edn. Duxbury Press, Belmont, CA.

Gregory, J. (2009). Being two-faced over counterparty credit risk. Risk 22(2), 86–90. Huge, B., and Lando, D. (1999). Swap pricing with two-sided default risk in a rating-based

model. European Finance Review 3(3), 239–268.

Jarrow, R., and Yu, F. (2001). Counterparty risk and the pricing of defaultable securities.

Journal of Finance, 56(1), 1765–1799.

Johnson, H., and Stulz, R. (1987).The pricing of options with default risk. Journal of Finance

42(2), 267–280.

Leung, S., and Kwok, Y. (2005). Credit default swap valuation with counterparty risk. Kyoto

Economic Review 74(1), 25–45.

Li, B., and Tang, Y. (2007). Quantitative Analysis, Derivatives Modeling, and Trading

Strate-gies in the Presence of Counterparty Credit Risk for the Fixed-Income Market. World

Scientific, Singapore.

Lipton, A., and Sepp, A. (2009). Credit value adjustment for credit default swaps via the structural default model. The Journal of Credit Risk 5(2), 123–146.

Protter, P. (1990). Stochastic Integration and Differential Equations: A New Approach. Springer.

Pykhtin, M., and Zhu, S. (2007). A guide to modelling counterparty credit risk. GARP Risk

Review July/August, 16–22.

Redon, C. (2006). Wrong-way risk modelling. Risk 4, 54–60.

Sorensen, E., and Bollier, T. (1994). Pricing swap default risk. Financial Analysts Journal