International Research Journal of Management and Commerce Vol. 4, Issue 2, February 2017 Impact Factor- 5.564 ISSN: (2348-9766)

© Associated Asia Research Foundation (AARF)

Website: www.aarf.asia Email : [email protected] , [email protected]DETERMINANTS OF REVERSE MORTGAGE USE INTENTION: A

THEORETICAL FRAMEWORK

Mohammed Ishaq Mohammed1, Noralfishah Sulaiman2

1,2

Department of Real Estate, Faculty of Technology Management and Business, UniversitiTun Hussein Onn Malaysia, Johor, Malaysia.

1

Department of Estate Management and Valuation, Faculty of Environmental Technology AbubakarTafawaBalewa University Bauchi, Nigeria.

ABSTRACT

Reverse mortgage is a relatively new financial product specially designed to enable the elderly

people convert the trapped equity in their homes into liquid cash in order to supplement their

existing income. This paper aims at proposing a model that can predicts potential consumers;

intention to use reverse mortgage as a source of supplementary income in old age by adopting

the original TPB and extending it with a view to identifying the behavioural factors likely to

influence reverse mortgage use. The methodology of the paper is based on review of relevant

literatures on reverse mortgage and behavioural change theories. The proposed model, Reverse

Mortgage Use Intention Model (ReMUIM), is expected to identify the underlying behavioural

factors that can influence potential reverse mortgage consumers’ willingness to use reverse

mortgage as a source of supplementary income in old age.

KEYWORDS: Ageing, Behaviour, Elderly, Financial insecurity, Intention, Reverse mortgage

1. Introduction

Ageing trend which started in developed countries has long surfaced in the developing

Globally, the population of the elderly people aged 60 years and above is expected to reach 2

billion by the year 2050[1]. Malaysia is not an exception to this demographic reality either. The

population of the elderly people in the age group 60 years and above is expected to reach 10%

of the country‘s total population in the year 2020[2]. This will enlist the country among the league of ageing nations based on the United Nations‘ benchmark.

One of the challenges facing the elderly people globally is lack of sufficient finances to

fund increased medical needs and other associated costs[3,4]. This problem is further

complicated given the fact that the sustainability of the social security systems such as pension

schemes and other welfare schemes that are meant to support the elderly after their active

working age is being doubted[5,6].The Malaysian elderly people are not exception to this

problem either because inadequacy of savings upon retirement has been identified as the main

challenge facing this group of individuals[7].Studies have shown that the elderly people in

Malaysia are facing challenges in terms of financial sustainability, adequacy of retirement

income and health care financing as a result of increasing life expectancy, changing family

structure and other socio-economic changes being witnessed in the country[8]. A report indicated

that retirees in Malaysia use up the average RM150, 000 ($ 37,000 approximately) of their

Employee Provident Fund (EPF) savings in the first three to five years of retirement[9]. This is

alarming because the EPF is the most popular retirement savings scheme in the country that

covers private sector employees and other public sector employees that are not eligible for the

public pension scheme.

Furthermore, an alternative means through which the elderly people could avoid the

effect of financial insecurity in later life is by savings during their youthful age. Lamentably,

however, Malaysians are not saving enough to enable them cushion the effect of income shocks

in later life[10]. This is further verified by recent report which indicated that 90% of the urban

households and 86% of the rural households in the country have zero savings[11]. Similarly,

while family traditionally serves as an important source for support to the elderly, recent

evidences point to the gradual decline of this long lasting Asian legacy among many as a result

of modernisation[12].

Even though the elderly are considered ―cash-poor‖, on the other hand, they are considered to be ―asset-rich‖ by virtue of the enormous housing wealth they own which, if turned

16]. In the case of Malaysia, for example, real estate has been established to constitute the largest

single asset for majority of household irrespective of financial status[17]. Malaysia‘s national

home ownership rate in 2012 is 74.5%, which surpasses the 66.9% national rate of the

US[18,19]. This scenario depicts the Malaysian elderly people to fall within the ―cash-poor‖ but

―asset-rich‖ classification.Thus, this paper propose a model that could be used to predict individual‘s willingness to use reverse mortgage as a source of supplementary income in old-age

with a view to identifying the behavioural factors that may likely affect reverse mortgage

demand in Malaysia.

2. Determinants of Reverse Mortgage Use

Reverse mortgage is one of the many financial products that enable consumption

smoothing over the life cycle. The general name for this product class is ―home equity release products‖. Home equity release products have generally been promoted as a means of tapping

the equity trapped in residential houses[20]. This is especially for retired elderly homeowners

whose debt-free properties form the major part of their net assets[21]. The continuous increase in

the cost of providing old age-related payments and services amidst persistent global economic

crisis is linked to the growing popularity of real estate asset as a potential source of income

capable of supplementing the dwindling pension fund and various social security funds in many

countries[22,23]. Being the most significant asset among majority of households, the primary

home is regarded as a store of wealth that can be used to augment the income needs of elderly

people after their retirement. This led to the emergence of a number of financial products that

make it possible for homeowners to access the illiquid wealth trapped in their residential real

estates. These financial products are generally termed ―home equity release products‖.

Home equity release products give home owners the flexibility of consuming their

accumulated housing wealth without necessarily moving out of the property. This can be done

through lease-back arrangement, where an owner sells his property to a buyer then rent the

property back and become a renter. It can also be in the form of physical subdivision of the

property to create two separate units which makes it possible for one of the units to be rented out

or even be sold. Similarly, other alternative products allow the homeowner to sell the property to

jurisdictions, banks and other financial institutions introduced some financial products that offer

homeowners access to housing equity while maintaining the ownership of their residential

properties, popular among which are equity withdrawal and reverse mortgage[24].

Reverse mortgage has been described as a form of annuity to the homeowner for the

length of time he/she remains in the home[20]. It is designed for elderly homeowners to enable

them access their accumulated home equity while continuing to live in their homes[19] . In

contrast to a conventional forward mortgage, where periodic payment is made to the lender, in

reverse mortgage contract, the payment is made by the lender to the homeowner. The loan

principal and the accumulated interest are repaid when the borrower sells the home, moves

permanently or dies[20,24]. The amount of money a borrower can access in reverse mortgage

contract is a function of borrower‘s age, value of the property and prevailing interest rate[25].

The product is designed to provide elderly people who are ―asset-rich‖ but ―cash-poor‖

and who require additional fund to finance their medical needs, children education, house

improvement, leisure, bills payments and other necessities that may arise during the remaining

years after their active working life. Unlike the conventional forward mortgage where the

borrower must surrender collateral to which recourse can be made upon default, a reverse

mortgage loan does not require any form of collateral to be surrendered by the borrower.

Repayment of the loan principal and the accumulated interest is made from the proceeds realized

from selling the home after the death of the borrower or when he/she decides to move out from

the home permanently to care facility. The loan can be accessed through receipt of regular

monthly payments, lump sum payment, or line of credit, or a combination of these options.

The growth and sustainability of reverse mortgage product market is linked to a set of

inter-related factors as evidenced in literature. Although no study specifically concentrated on

investigating the influence of behavioural factors on reverse mortgage use decision, some studies

hinted on the possible effect of behavioural factors on individual‘s decision to use or demand for

reverse mortgage. For instance, a study in Italy reported that risk/uncertainty-related elements

have significant correlation with people‘s interest in reverse mortgage[26]. This is buttressed by

another study where it was found that debt aversion, perception of home equity as savings for

high origination costs, and unexpected expenses as the reasons behind the slow growth of the

In a different study that analysed the demand factor of regional difference for reverse

mortgage in Beijing and Hangzhou, China, it was revealed that even though the respondents

owned their houses and have monthly income below the disposable income level they, however,

show weak interest in applying for reverse mortgage to supplement their monthly income[28].

The resultant weak demand willingness for reverse mortgage is attributed to the attitude of the

elderly towards the product where it is seen as a last resort means of finance only in emergency

situations. Respondents also show strong motive to leave houses to their children. It is further

found that in Beijing elderly people suffering from health problems are more likely to apply for

reverse mortgage than their healthy counterpart because of the increase in medical expenses.

Moreover, result of a simulation study on reverse mortgage choice shows that elderly people

who are mainly concerned with the impact of unavoidable expenditure shocks on their standard

of living, shows higher probability of using line of credit plan than either tenure or term plans.

The choice of the line of credit plan is based on the fact that it gives the borrower access to a

large sum of money, rather than adding an additional fixed component to an existing income[29].

Individuals‘ decision to consider applying for reverse mortgage has also been found to be influenced by the level of individual‘s financial awareness and involvement, which describes the

general financial behaviour of individuals. A recent study discovered that lack of product

knowledge significantly affect the demand for reverse mortgage[30]. They pointed that demand

for reverse mortgage product can reasonably be increased by reducing the inherent complexity in

the product design.

Similarly, in China, a research that explored the feasibility of using reverse mortgage as

alternative option for generating retirement income for asset-rich-cash-poor elderly revealed that,

possession of stock, bond or fund were positively related to willingness to apply for reverse

mortgage[31]. This finding indicates the role of financial awareness as a determinant for reverse

mortgage demand since the respondents that showed strong willingness indicated that they

possess one or more financial product in their possession thus indicative of financial market

awareness. However, a more recent study found no significant relationship between financial

literacy and interest in reverse mortgage product among their respondents[26].

On the socio-cultural perspective, a number of studies on reverse mortgage market

attachment, ethnicity and/or race, intergenerational transfer and expectation from family

members have been found to influence individual‘s interest in applying for reverse mortgage

loan. For example, evidence have shown that young people‘s high expectation for inheritance

was found to negatively affects their willingness to approve of their parents‘ application for

reverse mortgage[32]. Moreover, in a study that investigate the feasibility of implementing

reverse mortgage for house-rich-cash-poor older adults in Hong Kong, it was found that living

arrangement, desire to leave ones property to descendants and intergenerational transfers

received from children and grandchildren are barriers to interest in reverse mortgage[33].

In another study that explored the relationship between family and community ties and

demand for reverse mortgage in the USA, a fairly strong relationship between family and

community ties and interest in reverse mortgage was established. It was discovered that higher

incidence of out-migration tends to increase demand for reverse mortgage while

old-out-migration tends to reduce demand for reverse mortgage[34].Similarly, evidence was found that

homeowners who are less attached to their home and have no fear of liquidating it are more

likely to be interested in reverse mortgage[26].

Interest in reverse mortgage was also found to differ among ethnic and/or racial enclaves.

It was found that communities with higher percentage of Whites and individuals with higher

educational attainment are found to be more interested in reverse mortgage[34]. The result also

revealed that demand for reverse mortgage is also influenced by race, educational achievement

and the extent of market penetration.

In discussing the reasons for the small sized nature of the reverse mortgage product

market in some European countries, cultural suspicion arising from the perception that reverse

mortgage promotes personal consumption against intergenerational transfers has been identified

as one of the barriers preventing its wider acceptance among the elderly in the region[23].

Corroboratively,debt consolidation, altruistic motives and the attitude to offer financial

assistance to younger generations have also been identified as factors capable of influencing

demand for equity release products[35].

The aforementioned studies highlighted the role of behavioural factors such as attitude,

bequest motive, social influence, financial behaviour, and place attachment as possible

determinants of reverse mortgage use. However, in almost all the previous studies, these factors

worthwhile to combine these factors in a single model to determine their interaction effect on

individuals‘ intention to use reverse mortgage.

3. Overview on the Theory of Planned Behaviour (TPB)

The Theory of Planned Behaviour (TPB) (originally Theory of Reasoned Action, TRA) is

identified as one of the most widely referred and used behaviour theory[36]. The theory is based

on cognitive approach to explaining individual‘s attitudes and beliefs. The theory sets to predicts

and understand individual behaviour based on some antecedents. According to the theory,

individual‘s behaviour is predictable by intention. In turn, intention is predicted by attitude,

subjective norms, and perceived behavioural controls[37,38]. Attitude toward behaviour means

the positive or negative evaluation of a particular behaviour based on individual‘s beliefs.

Subjective norm is individual perceptions of whether significant referents approve or disapprove

of the behaviour. It is the social pressures exerted on an individual resulting to the perceptions of

what others think they should do and their inclination to comply with these[36]. Perceived

behavioural control described the perceived difficulty of performing the behaviour. It reflects

past experience as well as anticipated barriers and the perceived control over the opportunities,

resources, and skills necessary to perform a behaviour[39–41]. In essence, the more favourable

the attitude toward performing a behaviour, the greater the perceived social approval; the easier

the performance of the behaviour is perceived to be, the stronger the behavioural intention41. The

main idea behind TPB is to predict actual behaviour from behavioural intention by three

independent constructs: attitude, subjective norm and perceived behavioural control[43]. The

Figure 1: Theory of Planned Behaviour[37]

3.1The TPB constructs

The TPB is an improvement on a previous theory, Theory of Reasoned Action (TRA),

which was criticized for ignoring the effect of individual‘s control belief on behaviour. The

inclusion of perceived behavioural control as a construct in the TPB was to deal with conditions

in which individuals have incomplete volition control over behaviour[44]. TPB assumes that

human action is guided by three kinds of considerations: beliefs about the likely outcomes of the

behaviour and the evaluations of these outcomes (behavioural beliefs), beliefs about the

normative expectations of others and motivation to comply with these expectations (normative

beliefs), and beliefs about the presence of factors that may facilitate or impede performance of

the behaviour and the perceived power of these factors (control beliefs). In their respective

aggregates, behavioural beliefs produce a favourable or unfavourable ‗attitude toward the

behaviour‘; normative beliefs result in perceived social pressure or ‗subjective norm‘; and

control beliefs give rise to ‗perceived behavioural control‘. In combination, attitude toward the

behaviour, subjective norm, and perception of behavioural control lead to the formation of a

‗behavioural intention‘[37]. The main constructs in the TPB are explained in the following

3.1.1Intention

The central factor in the TPB is the individual‘s intention to perform a given behaviour.

Intention is described as indications of how hard people are willing to try and the amount of

effort they are planning to exert in order to perform a particular behaviour. In essence, intentions

are assumed to capture the motivational factors that influence behaviour[37]. Generally, the

stronger the intention to engage or perform behaviour, the more likely should be its

performance[37].

3.1.2Attitude (ATT)

Attitude has been defined as an individual's positive or negative feelings (evaluative

affect) about performing the target behaviour[45]. They posit that individuals form attitudes

toward behaviour by evaluating their beliefs through an expectancy-value model. For each

attitude toward behaviour, individuals multiply the belief strength by the outcome evaluation and

then sum the entire set of resulting weights to form the attitude.

3.1.3 Subjective norm (SN)

Subjective norm has been defined as the person‘s perception that most people who are

important to him think he should or should not perform the behaviour in question[45].

Individuals multiply the normative belief strength by the motivation to comply with that referent,

and sum the entire set of resulting weights to determine their behavioural intention.

3.1.4 Perceived behavioural control (PBC)

Individual‘s volitional control in the context of TPB was conceptualized as perceived

behavioural control[38]. Perceived behavioural control is the individual‘s belief of how easy or

difficult it is to perform the behaviour in question[46]. The extent of one‘s control to perform a

given behaviour is determined by presence or absence of requisite resources and opportunities.

The more resources and opportunities is possessed, and the fewer barriers is anticipated, the

greater the perceived behavioural control over the behaviour[47]. Moreover, individual‘s belief

about behavioural control is partially affected by past experience with the behaviour and by

and by other factors that increase or reduce the perceived difficulty of performing the behaviour

in question[47].

4. APPLICATION OF TPB IN INVESTMENT AND FINANCIAL DECISIONS

TPB is widely used in varied fields to study individuals‘ behavioural intention towards a

particular event, service, or product. Its application is found in the field of technology adoption

such as e-commerce, internet banking, credit card use, computer usage. It is also applied to study

customers‘ behaviour in the hospitality and tourism industry; health sector, and financial and

investment decision. In all these studies, the original TPB model or modified models were used

to investigate individuals‘ behavioural intention with regard to the specific subject of interest.

The current study falls within the general financial decision parlance. In order to appreciate the

extent of use of TPB to study individuals‘ financial decision, a review of some selected studies is

given. This is to help contextualized the present study in line with the previous studies in the

finance and investment fields that adopted the TPB as a theoretical model.

In a study that aimed at determining the acceptance of diminishing partnership home

financing in Malaysia, attitude and subjective norm were discovered to be the main determinants

of intention[48]. In another study that explored the individual factors that are likely to influence

the investment decisions of potential investors in Barbados, attitude, subjective norm, perceived

behavioural control, and risk propensity were identified as the most significant predictors of

investment decision[49].

Similarly, a research conducted in Malaysia that aimed at investigating the effect of

attitude, social influence, religious obligation, government support and pricing on the intention to

use Islamic personal financing revealed that attitude, social influence and pricing significantly

predict intention[50]. Subsequently, the TPB model was adopted to investigate whether

religiosity influence customers‘ intention to undertake Islamic home financing in Malaysia. The

findings shows that attitude, perceived behavioural control and religiosity explains 50.5%

variance in the intention to undertake Islamic home financing among the respondents[51].

Similarly, attitude and knowledge were found to have positive and significant influence on

intention while social influence was reported as insignificant factor in determining Muslim

Furthermore, a study in the United States that examined the link between TPB and

financial literacy by developing a predictive model for credit card debt among college students, it

was found that attitude, subjective norm and perceived behavioural control predicts

intention[53]. However, financial literacy was found to be statistically insignificant predictor of

intention to use credit card while positive correlation was established between attitude and

amount of credit card debt.

In a study that investigates the effects of subjective norm, relative advantage, simplicity,

compatibility and perceived behavioural control on Islamic home financing adoption, it was

discovered that subjective norm, relative advantage and simplicity are significant determinants of

attitude to adopting Islamic home financing. In addition, it was found that attitude, subjective

norm, relative advantage, simplicity, compatibility and perceived behavioural control are

statistically significant predictors of Islamic home finance adoption[54]. A different study by the

same authors that explored the willingness of bank customers in Malaysia to participate as

partner in MusharakahMutanaqisahrevealed that about 55% variation in intention was explained

by attitude, subjective norm and perceived behavioural control. The relationship between attitude

and subjective norm was also found to be statistically significant[55].On the other hand, a study

in the Islamic insurance sector test the effect of attitude, subjective norm and quality of

information about Islamic insurance on demand using Theory of Reasoned Action (TRA). The

result shows that attitude and quality of information positively affect the demand for Islamic

insurance while subjective norm affects it negatively[56]. Similarly, another study that

investigates the determinants of customers‘ intention to use Islamic personal finance confirmed

that attitude, social influence and religious obligation significantly influence intention to use

Islamic personal finance[57]. Moreover, religiosity and product knowledge were found to

significantly influence customers‘ attitude toward halal credit card service while attitude has

significant influence on customers‘ intention to accept halal financial credit card services[58].In

the annuity market, attitude, and subjective norm were also found to significantly determine

longevity annuity purchase intention among Italian younger adults. similarly, gender, household

annual income and educational attainment are significant moderators to intention[59].

The foregoing literatures indicate the applicability of TPB in determining the behavioural

next section discusses the justification for adopting TPB to investigate the intention to use

reverse mortgage among Malaysians.

4.1Rationale for Adopting TPB in the study

Decision to use reverse mortgage falls within the general financial decision making

process. Economic based theories such as utility theory have been used by previous researchers

to evaluate the behaviour of individuals when making financial decisions. Similarly, other

behavioural theories such as Prospect Theory, Image Theory, and Mental Accounting have

emerged to deal with the phenomena. However, the theory of planned behaviour only received

limited attention in this area[60].

The TPB is adjudged the most widely used intention model. The strength of the model in

predicting behaviour and intention were confirmed in a meta-analysis of a data base of 185

independent studies where TPB was found to account for 27% and 39% of variance in behaviour

and intention respectively[61]. Therefore the universality of TPB and the corresponding recorded

success of its use in predicting behavioural intention in different aspect of human

undertakings[62,63] explain one of the justifications for its adoption in the present study.

Previous studies on reverse mortgage give hints on the role of some behavioural factors

that are capable of influencing the use of reverse mortgage. However, little or no effort has been

made to investigate the interaction of these factors holistically. For instance, evidence have

shown that reverse mortgage is attractive to some individuals because it gives them more

perceived control on their spending decisions[64]. The influence of psychological and

behavioural factors on willingness to use reverse mortgage have been documented[13,65–67].

Similarly, several other studies pointed to cultural and social factors as potential factors likely to

influence the willingness to use or the actual use of reverse mortgage[28,31,32,68]. Other likely

factors are bequest motive and sense of community/place attachment[23,32–35,69,70]. Some of

these factors reflect the main constructs of the TPB. It is therefore anticipated that applying TPB

to investigate the influence of these factors on the willingness to use reverse mortgage would

help in predicting reverse mortgage use in Malaysia. Similarly, the adoption of TPB in the study

would provide a framework that can best explain the interaction of the determining factors of

willingness for reverse mortgage use in the context of the TPB, thereby extending the application

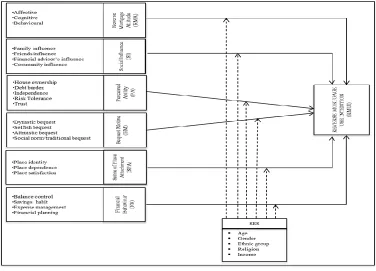

4.2 The proposed reverse mortgage use intention model (ReMUIM)

The intention of individuals to take up reverse mortgage is expected to be determined by

many psychological and behavioural factors such as attitude, societal expectation, self-control,

bequest motive, sense of place/neighbourhood attachment and financial behaviour. The proposed

reverse mortgage use model (ReMUIM) is meant to predict the use of reverse mortgage by

adopting the original TPB constructs and additional three constructs that are deemed necessary in

predicting the use of reverse mortgage. The justification for including the three new constructs is

based on the facts that the TPB is open to the inclusion of additional predictors if it is evident

that such predictors have significant contribution in predicting intention[63]. The proposed

model constitutes of eight (8) constructs. Four of the constructs, Perceived Ability (PA); Social

Influence (SI); Reverse Mortgage Attitude (RMA) and Reverse Mortgage Use Intention (RMUI)

convey the same meaning applied to the original TPB constructs. On the other hand, the

remaining four constructs, Bequest Motive (BM), Sense of Place Attachment (SPA), Financial

Behaviour (FB) and Socio-Economic Status (SES) are additional constructs identified in the

literature as potential predictors of willingness for reverse mortgage use.

In the next section, a detailed explanation of the constructs and their relationships as

depicted in the proposed model (Figure 2) is presented. The purpose of the explanation is to offer

a much clearer view on the proposed model by contextualizing the constructs in line with the

peculiarity of the current study and develop working hypotheses for further empirical

Figure 2: Reverse Mortgage Use Intention Model (ReMUIM)

Source: Authors (2017)

4.2.1 Reverse mortgage use intention (RMUI)

Although there is not a perfect relationship between behavioural intention and actual

behaviour, intention can be used as a proxy measure of behaviour. Behavioural intention is a

good predictor of actual usage of an application or system[71]. It may be a natural conclusion

then, that any factors influencing behaviour can indirectly influence intention[72]. In this study,

the degree of willingness to use reverse mortgage is examined in association with the other

constructs. It is expected that higher willingness will translate to higher actual use and lower

willingness will result to low or non-use.

4.2.2 Reverse mortgage attitude (RMA)

The attitude-behavioural intention relationship implies that people form intentions to

perform behaviour toward which they have positive effect. Perceived usefulness is the

consumer‘s perceptions regarding the outcome of an experience[73]. Therefore, it is expected

for money etc they are more likely to accept its use. On the other hand, if they perceived that

reverse mortgage is not useful, risky, complex, etc there could be higher likelihood of not

accepting or using the product. Therefore, the inter-relationship between perceived usefulness

and the intentions to use reverse mortgage are important to examine. In view of the

aforementioned, it is hypothesized that:

H1: Attitude significantly predict reverse mortgage use intention

4.2.3 Perceived Ability (PA)

Perceived ability reflects the perceived belief of performing the behaviour in question. In

the context of this research, the likelihood of individuals applying for reverse mortgage in the

future depends on their belief about the opportunities (availability of reverse mortgage products,

desire to age-in-place), resources (home ownership, information and knowledge), and barriers

(risk averseness, debt averseness), associated with their action. Similarly, as mentioned earlier

that individual perceived control is partially affected by past experience and second hand

information about the behaviour. It is assume that previous experience on financial and

investment decision such as buying annuity product, taking up mortgage, investing in shares will

influence the willingness to use reverse mortgage. Evidence in the reverse mortgage literature

indicate that low income, attachment to home, house ownership, previous investment decision,

risk averseness, and counselling influences interest in reverse mortgage. Therefore, it is

hypothesized that:

H2: Perceived ability significantly predict reverse mortgage use intention

4.2.4 Social Influence (SI)

Social influence is used in this context to convey the socio-cultural expectations that

could affect individual‘s willingness to use reverse mortgage. According to the TPB other people‘s expectations about individual‘s performance of an action influence intentions both

positively and negatively. Previous studies on reverse mortgage indicate that the decision to

apply or use reverse mortgage could probably be influenced by family members, community and

financial advisers[32]. It is anticipated that when family members support individual‘s decision

system such as bequest and intergenerational practices could influence one‘s willingness to use

reverse mortgage. Expectations to adhere to certain led down rules in administering one‘s

property could affect the intention to use reverse mortgage. Community and family expectations

to bequeath one‘s property to his offspring in line with the concept of reciprocity[74,75] could

influence decision to use reverse mortgage. Based on the aforesaid, this study hypothesized that:

H3: Social influence significantly predicts reverse mortgage use intention

4.2.5 Bequest motive (BM)

Bequest motive is an additional construct introduced in the original TPB. Its inclusion as

a construct in this study is based on the expectation that it will influence individual‘s willingness

on using reverse mortgage product. Literature on reverse mortgage demand indicated that

individual‘s desire to leave behind assets to heirs on the occasion of death might influence peoples‘ willingness to apply for reverse mortgage products[65,76,77]. Studies on bequest and

inheritance in Malaysia revealed that people hold different bequest motives with regards to the

sharing of their assets. Studies have revealed evidences of selfish life-cycle, altruistic, dynastic,

social norm and traditional bequest motives among Malaysians[11,78,79]. It is therefore

worthwhile to include bequest motive as additional construct in the TPB in order to investigate

its influence on the willingness of Malaysians to use reverse mortgage product. It is therefore

hypothesized that:

H4: Bequest motive significantly predict reverse mortgage use intention

4.2.6 Sense of place attachment (SPA)

One of the conditions in reverse mortgage contract is that the borrower ought to leave in

the house permanently until death. Findings from reverse mortgage studies implied that those

individuals who are highly attached to their environment are the most attracted to reverse

mortgage while those who anticipated moving out showed less interest in reverse mortgage[32].

In consideration of the aforementioned, addition of a construct that measures the degree of place

attachment to the original TPB is important because it is expected that individuals‘ willingness to

use reverse mortgage will be affected by the degree to which he plan to remain in the house or

community. Thus, it is hypothesized that:

4.2.7 Financial behaviour (FB)

In the financial behaviour literature, four major domains of financial behaviourwere

identified to include managing money, planning ahead, choosing products and staying

informed[80]. Effective engagement in these behaviours to improve one‘s financial well-being

leads to positive or desirable financial behaviour while their ineffective use translates to negative

or undesirable financial behaviour[81]. Thus it is expected that individual‘s financial behaviour

will influence decision to apply for reverse mortgage. It is expected that those individuals who

interact with other forms of financial products will be more likely to enter into reverse mortgage

transaction than those who do not involve in such, as such it is hypothesized that:

H6: Financial behaviour significantly predicts reverse mortgage use intention

4.2.8 Socio-Economic Status

Generally, socio-economic statuss have been established to influence people‘s decision in

many aspects of human activities[82–84]. Previous studies on reverse mortgage product market

highlighted the role of age, race, income level, gender, marital status, health status and place of

residence in determining the level of reverse mortgage usage among individuals[24,28,32,84]. It

is therefore suitable to include socio-economic characteristics as a possible predictor of reverse

mortgage use intention. Similarly, this study considered socio-economic characteristics as a

moderating variable between the identified six constructs and reverse mortgage use intention.

Therefore, the following hypotheses are formulated:

H7a: Socio-economic status moderates the relationship between reverse mortgage attitude and

reverse mortgage use intention

H7b: Socio-economic status moderates the relationship between perceived ability and reverse

mortgage use intention

H7c: Socio-economic status moderates the relationship between social influence and reverse

mortgage use intention

H7d: Socio-economic status moderates the relationship between place attachment and reverse

H7e: Socio-economic status moderates the relationship between bequest motive and reverse

mortgage use intention

H7f: Socio-economic status moderates the relationship between financial behaviour and reverse

mortgage use intention

5 CONCLUSION

The reverse mortgage product is a relatively new financial product specifically designed

to enable the elderly people avoid the risk of financial insecurity in old-age. Evidence has shown

that elderly people in Malaysia are facing the risk of financial insecurity in old-age. On the other

hand, they are considered to possess substantial illiquid wealth in the form of accumulated home

equity which is trapped in their homes. One of the cardinal points of the Malaysia‘s New

Economic Model (NEM) as a roadmap to the actualisation of the country‘s vision of becoming a

high income country is to ensure inclusiveness in all aspect of human activities in the country.

Institutions in the country are encouraged to ensure inclusiveness in their service and product

delivery as well. Therefore, by understanding the extent of potential customers‘ willingness to

use reverse mortgage and the respective factors that predict such behaviour, the financial

institutions will have clue on the future acceptability and marketability of reverse mortgage

product in the country, thus helping the financial institutions contribute to the government‘s

inclusiveness agenda as enshrined in the 10th Malaysia Plan.

REFERENCES

[1] United Nations Department of Economic and Social Affairs Population Division. World

Population Ageing 2013. New York: 2013. doi:ST/ESA/SER.A/348.

[2] Department of Statistics Malaysia. Population Projections in Malaysia 2010 - 2040. Kuala

Lumpur: 2012.

[3] Kumar PM, Divakaruni RK, Sri Venkata M. Reverse Mortgages - Features & Risks.

Mumbai: Institute of Actuaries of India; 2008.

[4] Hoe NK. The prospects for old-age income security in Hong Kong and Singapore. London

[5] Cocco JF, Lopes P. Reverse Mortgage Design. 2015.

[6] Zin RHM, Lee HA, Abdul-Rahman S. Social Protection in Malaysia. In: Adam E, Hauff

M von, John M, editors. Soc. Prot. Southeast East Asia, Singapore: Friedrich Ebert

Stiftung; 2002, p. 119–69.

[7] Abd Samad S, Awang H, Mansor N. Population ageing and social protection in malaysia.

Malaysian J Econ Stud 2013;50:139–56.

[8] Help Age International, UNFPA. Ageing in the Twenty-First Century: A Celebration and

a Challenge. Fundo Popul Das Nações Unidas 2012:12. doi:978-0-89714-981-5.

[9] Employee Provident Fund. EPF savings and your retirement 2015:6–7.

[10] Loke YJ. Household‘s Preparedness for Income Shock. Singapore Econ. Rev. Conf. 2013,

2013, p. 1–25.

[11] Alavi K. Intergenerational Relationships Between Aging Parents and Their Adult Children

in Malaysia. 20th Assoc Asian Soc Sci Res Counc Bienn Gen Conf 2013:1–19.

[12] Hanewald K, Post T, Sherris M. Portfolio Choice in Retirement What Is the Optimal

Home Equity Release Product ? 2014.

[13] Shan H. Reversing the trend: The recent expansion of the reverse mortgage market. Real

Estate Econ 2011;39:743–68. doi:10.1111/j.1540-6229.2011.00310.x.

[14] Ong R. Unlocking Housing Equity Through Reverse Mortgages: The Case of Elderly

Homeowners in Australia. Eur J Hous Policy 2008;8:61–79.

doi:10.1080/14616710701817166.

[15] Rasmussen DW, Megbolugbe IF, Morgan BA. Using the 1990 Public Use Microdata

Sample to Estimate Potential Demand for Reverse Mortgage Products. J Hous Res

1995;6:1–23.

Malaysia 2011:77. doi:10.1007/s13398-014-0173-7.2.

[18] Wang P. Feasibility Study of Reverse Mortgages for Pension —— A Case of Hangzhou ,

China 2011.

[19] Reed R, Gibler K. The case for reverse mortgages in Australia–Applying the USA

experience. Real Estate Soc Conf Brisbane, Aust 2003:19–22.

[20] Kumar M. Reverse mortgage as a retirement planning tool: an evaluation. punjabi

University, 2013.

[21] Ong R, Haffner M, Wood G, Jefferson T, Austen S. Assets, debt and the drawdown of

housing equity by an ageing population. vol. 153. 2013.

[22] Haffner MEA, Ong R, Wood GA. Mortgage equity withdrawal in Australia: Recent

trends, institutional settings and perspectives. Delft, The Netherlands: 2015.

[23] Doling J. Releasing Housing Equity. Socio-Economic Sci 2010:1–5.

[24] Mayer CJ, Simons K V. Reverse mortgages and the liquidity of housing wealth. Real

Estate Econ 1994;22:235–55. doi:10.1111/1540-6229.00634.

[25] Redfoot DL, Scholen K, Brown SK. Reverse mortgages: Niche product or mainstream

solution? Washington D.C.: 2007.

[26] Fornero E, Rossi MC, Brancati MCU. Explaining why, right or wrong,(Italian) households

do not like reverse mortgages. J Pension 2011:1–23. doi:10.1017/S1474747215000013.

[27] Lee C-C, Chen K-S, So-De Shyu D. Credit , Equity Conversion , and Housing

Endowment : Analysis of Reverse Mortgage Markets 2015;5:63–80.

[28] Zhou H. Analysis on demand factor of regional difference for reverse mortgage-based on

survey data in Beijing & Hangzhou. J Chem Pharm Res 2014;6:232–8.

[29] Fratantoni M. Reverse mortgage choices: A theoretical and empirical analysis of the

[30] Davidoff T, Gerhard P, Post T. Reverse Mortgages: What Homeowners (Don‘ t) Know

and How it Matters. JpwiwiRwth-AachenDe 2014:1–34.

[31] Chou KL, Chow NWS, Chi I. Willingness to consider applying for reverse mortgage in

Hong Kong Chinese middle-aged homeowners. Habitat Int 2006;30:716–27.

doi:10.1016/j.habitatint.2005.04.008.

[32] Yoo I, Koo I. Do Children Support Their Parents ‘ Application for the Reverse

Mortgage ?: A Korean Case. Seoul: 2008.

[33] Sau Po Centre on Ageing. Report on A Study on Reverse Mortgage Commissioned by the

The Hong Kong Mortgage Corporation Limited. Hong Kong: 2010.

[34] Knapp K. The Influence of Family and Community Ties on the Demand for Reverse

Mortgages. New York: 2001.

[35] Luiz JM, Stobie G. The market for equity release products : lessons from the international

experience. South African Bus Rev 2010;14:24–45.

[36] Morris J, Marzano M, Dandy N, O‘Brien L. Theories and models of behaviour and

behaviour change. For Sustain Behav Behav Chang Theor 2012:1–27.

[37] Ajzen I. Perceived Behavioral Control, Self-Efficacy, Locus of Control, and the Theory of

Planned Behavior1. J Appl Soc Psychol 1985;80:11–39.

doi:10.1111/j.1559-1816.2002.tb00236.x.

[38] Ajzen I, Fishbein M. Understanding attitudes and predicting social behavior. vol. 278.

1980. doi:Z.

[39] Ozmete E, Hira T. Conceptual Analysis of Behavioral Theories / Models : Application to

Financial Behavior. Eur J Soc Sci 2011;18:386–404.

[40] Rutherford LG, Devaney SA. Utilizing the Theory of Planned Behavior to Understand

Convenience Use of Credit Cards. J Financ Couns Plan Educ 2009;20:48–63.

college students. Soc Indic Res 2009;92:53–68. doi:10.1007/s11205-008-9288-6.

[42] Xiao J, Wu J. Applying the theory of planned behavior to retain credit counseling clients.

Arizona: 2006.

[43] Barua P. The Moderating Role of Perceived Behavioral Control : The Literature Criticism.

Int J Bus Soc Sci 2013;4:57–9.

[44] Aubele T. Investigation of consumer over- indebtedness within the German mail ‐ order

industry using the Theory of Planned Behaviour ‖. University of Gloucestershire, 2014.

[45] Fishbein M, Ajzen I. Belief, Attitude, Intention, and Behavior, An Introduction to Theory

and Research. 1975. doi:10.1016/B978-0-12-375000-6.00041-0.

[46] Ajzen I, Madden TJ. Prediction of goal-directed behavior: Attitudes, intentions, and

perceived behavioral control. J Exp Soc Psychol 1986;22:453–74.

doi:10.1016/0022-1031(86)90045-4.

[47] Taib FM, Ramayah T, Razak DA. Factors influencing intention to use diminishing

partnership home financing. Int J Islam Middle East Financ Manag 2008;1:235–48.

doi:10.1108/17538390810901168.

[48] Alleyne P, Broome T. An exploratory study of factors influencing investment decisions of

potential investors. Barbados: 2010.

[49] Hanudin A, Abdul Rahim AR, Stephen LSJ, Ang Magdalene CH, Amin H, Rahman ARA,

et al. Determinants of customers‘ intention to use Islamic personal financing: The case of

Malaysian Islamic banks. J Islam Account Bus Res 2011;2:22–42.

doi:10.1108/17590811111129490.

[50] Alam SS, Janor H, Aniza C, Wel C. Is Religiosity an Important Factor in Influencing the

Intention to Undertake Islamic Home Financing in Klang Valley ? 2012;19:1030–41.

doi:10.5829/idosi.wasj.2012.19.07.392.

[51] Wahyuni S. Moslem Community Behavior in The Conduct of Islamic Bank: The

doi:10.1016/j.sbspro.2012.09.1188.

[52] Kennedy BP. The Theory of Planned Behavior and Financial Literacy: A Predictive

Model for Credit Card Debt? Marshall University, 2013. doi:Paper 480.

[53] Amin H, Rahman ARA, Jr SLS, Hwa AMC. Determinants of customers‘ intention to use

Islamic personal financing: The case of Malaysian Islamic banks. J Islam Account Bus

Res 2011;2:22–42. doi:10.1108/17590811111129490.

[54] Amin H, Abdul Rahman AR, Abdul Razak D. Willingness to be a partner in musharakah

mutanaqisah home financing: Empirical investigation of psychological factors. J Pengur

2014;40:69–81.

[55] Gouider JJ, Gafsi N. Islamic insurance in Tunisia: fiction or reality? J Soc Sci Res

2014:639–48.

[56] Ahmad NHB. Determinants of Customers‘ Intention to Use Islamic Personal Finance.

University Utara Malaysia, 2014.

[57] Putit L, Johan ZJ. C onsumers‘ Acceptance of ―Halal‖ Credit Card Services : An

Empirical Analysis. J Emerg Econ Islam Res 2015;3:1–9.

[58] Nosi C, D‘Agostino A, Maria Pagliuca M, Alberto Pratesi C. Saving for old age:

Longevity annuity buying intention of Italian young adults. J Behav Exp Econ

2014;51:85–98. doi:10.1016/j.socec.2014.05.001.

[59] Southey G. The Theories of Reasoned Action and Planned Behaviour Applied to Business

Decisions : A Selective Annotated Bibliography. J New Bus Ideas Trends 2011;9:43–50.

[60] Cruz JN. Is white-collar crime a form of entrepreneurship? 2013.

[61] Armitage CJ, Conner M. Efficacy of the Theory of Planned Behaviour: a meta-analytic

review. Br J Soc Psychol 2001;40:471–99. doi:10.1348/014466601164939.

[62] Ajzen I. The theory of planned behavior. Orgnizational Behav Hum Decis Process

[63] Williams FL, Kao YE. Value of Home Equity Used in Reverse Mortgages as a Potential

Source of Income for Elderly Americans. Financ Couns Plan 1997;8:57–64.

[64] Leviton R. Reverse Mortgage Decision-Making. J Aging Soc Policy 2002;13:1–16.

doi:10.1300/J031v13n04_01.

[65] Dillingh R, Prast H, Rossi M, Brancati C. The psychology and economics of reverse

mortgage attitudes: evidence from the Netherlands. 2013.

[66] Andersson KC, Sandstrom J. Investigating a Psychological Perspective of Reverse

Mortgage - How is Reverse Mortgage Perceived by Potential Borrowers in Sweden?

Umeå University, 2013.

[67] Chen A, Jensen HH. Home Equity Use and the Life Cycle Hypothesis. J Consum Aff

1985;19:37–56. doi:10.1300/J081V04N01.

[68] Nakajima M, Telyukova IA. Reverse Mortgage Loans : A Quantitative Analysis. 2014.

[69] Chinloy P, Megbolugbe IF. Reverse Mortgages - Contracting and Crossover Risk. J Am

Real Estate Urban Econ Assoc 1994;22:367–86. doi:10.1111/1540-6229.00638.

[70] Venkatesh V, Davis FD. A Theoretical Extension of the Technology Acceptance Model:

Four Longitudinal Field Studies. Manage Sci 2000;46:186–204.

[71] Slatten LAD. An Application and Extension of the Technology Acceptance Model to

Nonprofit Certification. J NONPROFIT Manag 2010;14:47–55.

[72] Davis FD, Bagozzi RP, Warshaw PR. Extrinsic and intrinsic motivation to use computers

in the workplace. J Appl Soc Psychol 1992;22:1111–32.

doi:10.1111/j.1559-1816.1992.tb00945.x.

[73] Nicińska A. WHY DO PEOPLE BEQUEATH? ARGUMENTA OECONOMICA

2013;2:75–95.

[74] Kolm SC. Introduction to the Economics of Giving, Altruism and Reciprocity. In:

North-Holland: 2006, p. 1–122. doi:10.1016/S1574-0714(06)01001-3.

[75] Gotman A. Towards the end of bequest ? The life cycle hypothesis sold to seniors: Critical

reflections on the reverse mortgage financial fashion. Civ - J Soc Sci 2011;11:93–114.

[76] Caplin A. The Reverse Mortgage Market: Problems and Prospects. In: Mitchell OS, Bodie

Z, Hammond B, Zeldes S, editors. Innov. Retire. Financ., Pension Research Council;

2001.

[77] Chuan CS, Seong LC, Chau WH. Financial Satisfaction , Resource Transfers and Bequest

Motives A mong Malaysia ‘ s Urban Older Adults. Proc. B. ICETSR, Handb. Emerg.

Trends Sci. Res., vol. 8, PAK Publishing Group; 2014, p. 106–29.

[78] Alma‘amun S. Searching for bequest motives and attitudes to leaving a bequest among

Malaysian muslims. J Ekon Malaysia 2012;46:73–84.

[79] Kempson E, Collard S, Moore N. Measuring financial capability: an exploratory study.

London: 2005.

[80] Xiao JJ, Sorhaindo B, Garman ET. Financial behaviours of consumers in credit

counselling. Int J Consum Stud 2006;30:108–21. doi:10.1111/j.1470-6431.2005.00455.x.

[81] Dunlop S, Coyte PC, McIsaac W. Socio-economic status and the utilisation of physicians‘

services: results from the Canadian National Population Health Survey. Soc Sci Med

2000;51:123–33. doi:10.1016/S0277-9536(99)00424-4.

[82] Clark GL, Strauss K. Individual pension-related risk propensities: the effects of

socio-demographic characteristics and a spousal pension entitlement on risk attitudes. Ageing

Soc 2008;28:847–74. doi:10.1017/S0144686X08007083.

[83] Morgan BA, Megbolugbe IF, Rasmussen DW. Reverse Mortgages and the Economic

Status of Elderly Women 1 1990;36:400–5.

[84] Hancock R. Can Housing Wealth Alleviate Poverty among Britain‘s Older Population?

[85] Willis RM, Stewart RA, Giurco DP, Talebpour MR, Mousavinejad A. End use water

consumption in households: Impact of socio-demographic factors and efficient devices. J

![Figure 1: Theory of Planned Behaviour[37]](https://thumb-us.123doks.com/thumbv2/123dok_us/54247.1009037/8.612.155.457.49.254/figure-theory-of-planned-behaviour.webp)