THE EXCEPTIONS TO THE PRINCIPLE OF AUTONOMY OF DOCUMENTARY CREDITS

By

CHUMAH AMAEFULE

A thesis submitted to the

University of Birmingham

for the degree of

DOCTOR OF PHILOSOPHY

School of Law University of Birmingham August 2011

University of Birmingham Research Archive

e-theses repository

This unpublished thesis/dissertation is copyright of the author and/or third parties. The intellectual property rights of the author or third parties in respect of this work are as defined by The Copyright Designs and Patents Act 1988 or as modified by any successor legislation.

Any use made of information contained in this thesis/dissertation must be in accordance with that legislation and must be properly acknowledged. Further distribution or reproduction in any format is prohibited without the permission of the copyright holder.

i

Abstract

This thesis critically appraises the exceptions to the principle of autonomy in documentary credits. In appraising the exceptions, the central theme pursued is to address the question whether the application of the exceptions to the principle of autonomy is satisfactory. In addressing this general question, the study pays special attention to English law on documentary credits. However, the thesis also looks at the comparable position in other common law jurisdictions, such as United States, Canada, Australia, Singapore, and Malaysia.

Recently, in the different jurisdictions, opinion has not been consistent on what constitutes exceptions to the principle of autonomy in letters of credit. Apart from the traditional exception of fraud, recent English decisions to some extent have recognised illegality and express contractual restrictions on a beneficiary’s right to draw on a credit as compelling grounds on which the autonomy doctrine would be ignored. In other jurisdictions, other exceptions such as nullity and unconscionability have emerged. This dissertation assesses all these exceptions to the principle of autonomy with the aim of answering the question whether these exceptions facilitate documentary credits’ practice or as argued in some quarters, undermine the assurance of payment promised the seller/beneficiary.

ii

Acknowledgement

This thesis would not have been possible without the goodwill and assistance of a number of people and organisation.

My greatest debt is owed to my supervisor, Professor Nelson Enonchong. Special thanks must go to Mr Keith Uff for the painstaking and insightful corrections on this thesis. To Dr Djakhongir Saidov, I must say thank you for your support. I also would like to thank Professor Sarah Dromgoole for her encouragement.

So many offered support over the years that I cannot thank you all. But I have had the good fortune to work with some good friends whose careful thinking undoubtedly influenced my thinking in the course of this research. In this respect, my gratitude goes to Uche Chigbu who since meeting him in the summer of 2006 has remained very helpful both in my personal life and professional development. To Kris, your wife, I say thank you. Ebenezer Adodo has put up with more than most friends would in going through some of the ideas in this thesis and offering helpful comments. For your effort, I must also say thank you.

To the University of Birmingham, the part funding provided towards this research is fully appreciated. Lastly, to all members of my family especially my parents, Chima and Chinyere Amaefule for their financial support, love and encouragement throughout my life and more particularly during the period of this PhD.

iii

Table of Contents

Abstract ... i

Acknowledgement………..ii

List of Cases ... ix

List of Statutes ... xvii

Table of Figure ... xviii

Chapter One ... 1

1.0 General Introduction... 1

1.1 Overview of research ... 3

1.2 Methodology of research ... 5

1.3 The thesis outline ... 7

Chapter Two ... 11

2.0 Nature of Documentary Credit and Principle of Autonomy ... 11

2.1 Introduction ... 11

2.2 The Concept of documentary credits ... 12

2.3 Parties to documentary credit ... 14

2.3.1 The underlying contract of sale ... 16

2.3.2 The contract between the buyer and the issuing bank ... 19

2.3.3 The contract between the issuing bank and the advising bank ... 21

2.3.4 The contract between the issuing bank and the seller ... 23

2.3.5 The contract between the advising bank and the seller ... 25

2.4 The principle of autonomy ... 25

2.4.1 Common law position ... 27

2.4.2 The UCP 600 ... 30

2.4.3 Uniform commercial code (USA) ... 31

2.5 Does autonomy doctrine operate without the exceptions? ... 32

iv

Chapter Three ... 36

3.0 The Fraud Rule ... 36

3.1 Introduction ... 36

3.2 Rationale ... 38

3.3 The Scope of the fraud exception in English law ... 41

3.3.1 Fraud rule and tort of deceit ... 41

3.3.2 Ambit of fraud-fraud in the transaction ... 47

3.3.3 Ambit-fraud in differed payment obligation ... 49

3.4 Standard of proof ... 54

3.4.1 Injunctive relief ... 54

3.4.2 Summary Judgement Application………...59

3.4.3 Full Trial………..61

3.5 Fraud rule in some common law jurisdictions ... 63

3.5.1 Canadian approach to fraud rule ... 63

3.5.2 Singapore ... 69 3.5.3 Malaysia ... 77 3.6 Conclusion ... 83 Chapter Four ... 87 4.0 Nullity ... 87 4.1 Introduction ... 87

4.2 Nature of nullity exception ... 90

4.2.1 Nullity in general law ... 91

4.2.2 Nullity in documentary credit ... 92

4.2.3 Different jurisdictions- issues and legal positions ... 98

4.2.3.1 English position ... 98

4.2.3.2 The position in Singapore ... 100

4.2.3.3 United States of America ... 104

4.3 The nullity arguments ... 104

4.3.1 Arguments against the nullity exception ... 105

4.3.1.1 Want of certainty ... 105

4.3.1.2 That the principle of autonomy should generally prevail ... 110

4.3.1.3 Absence of the logic of ex turpi causa doctrine in nullity exception ... 112

v

4.3.1.5 Unfortunate consequences to the right of third parties ... 116

4.3.1.6 Matching banks duty to the applicant with that of seller/beneficiary .... 118

4.3.1.7 Lack of authority for the nullity exception ... 120

4.3.2 Pro-nullity argument ... 121

4.3.2.1 Bank deal in documents and not in goods ... 122

4.3.2.2 Duty to tender conforming documents ... 122

4.3.2.3 Discouraging forgery ... 126

4.3.2.4 Documents as bank’s security ... 127

4.3.2.5 Bank’s agreed mandate to the applicant ... 129

4.3.2.6 Prejudice to beneficiaries/sellers in a Chain ... 130

4.3.2.7 Understanding the letter of credit contract ... 132

4.4 The scope of the nullity exception ... 134

4.4.1 Formulating nullity in documentary credit ... 134

4.4.2 Standard of proof ... 139

4.4.2.1 Summary judgement ... 139

4.4.2.2 Resisting Bank’s Entitlement to Reimbursement ... 140

4.4.2.3 Injunction against payment ... 141

4.4.2.4 Injunction- other legal considerations ... 143

4.5 Conclusion ... 144

Chapter Five ... 147

5.0 Recklessness of the Beneficiary ... 147

5.1 Introduction ... 147

5.2 Possible Nature of the exception ... 149

5.2.1 Recklessness in general law ... 149

5.2.2 Beneficiary’s recklessness in documentary credit ... 151

5.3 Applying beneficiary’s recklessness: legal considerations ... 153

5.3.1 Does the beneficiary owe a duty to be careful? ... 153

5.3.2 Question relating to beneficiary’s recklessness ... 157

5.3.3 Objections to beneficiary’s recklessness ... 157

5.3.4 Arguments for beneficiary recklessness ... 158

5.4 Conclusion ... 160

vi

6.0 Unconscionability ... 163

6.1 Introduction ... 163

6.2 Nature of unconscionability ... 167

6.3 Unconscionability in selected common law jurisdictions ... 170

6.3.1 English law ... 170

6.3.2 Singapore ... 178

6.3.3 Position in Malaysia ... 180

6.3.4 Australia ... 182

6.4 Scope of the unconscionability exception ... 188

6.4.1 Standard of Proof ... 188

6.4.1.1 Singapore ... 189

6.4.1.2 Australia ... 190

6.4.2 Proving unconscionability- legal ingredients ... 193

6.4.2.1 Reprehensible Conduct of such a manner that a court of conscience will deprive the party involved or refuse to assist him/her ... 194

6.4.2.2 Insistence on strict application of legal rights, in cases where to do so is regarded, on the facts of the particular case, to be harsh or oppressive ... 195

6.5 Should English law recognize unconscionability? ... 196

6.5.1 Argument for ... 196

6.5.1.1 Long entrenched in English legal history ... 196

6.5.1.2 Complements the fraud rule ... 199

6.5.1.3 Flexible nature of unconscionability ... 200

6.5.1.4 Has support from common law ... 201

6.5.1.5 Progress of the unconscionability exception in other jurisdictions ... 202

6.5.2 Arguments against ... 202

6.5.2.1 Too vague and uncertain ... 203

6.5.2.2 Unconscionability would lead to easy grant of injunctions, thereby destroying the purpose of the autonomy principle ... 206

6.5.2.3 Involvement with dispute in the underlying contract ... 207

6.6 Conclusion ... 207

Chapter Seven ... 210

7.0 Illegality... 210

vii

7.2 Illegality defence in general ... 211

7.3 Illegality in documentary credit ... 212

7.3.1 Where the letter of credit is in itself illegal ... 214

7.3.2 Illegality affecting the credit and underlying transaction ... 215

7.3.3 Illegality in the underlying transaction ... 218

7.4 The rationale for the exception ... 220

7.5 The current state of authorities on illegality exception ... 225

7.5.1 United States of America ... 225

7.5.2 Position in Singapore ... 233

7.5.3 English law ... 234

7.6 Legal considerations for the application of illegality defence ... 238

7.6.1 Evidentiary requirement of illegality defence ... 238

7.6.2 Timing ... 240

7.6.3 The reliance doctrine and proof of illegality ... 243

7.7 Illegality: defining its boundaries ... 246

7.7.1 Seriousness of illegality ... 247

7.7.2 The knowledge and intention of the claimant/ beneficiary ... 249

7.7.3 A close connection ... 251

7.7.4 Whether denying relief will further the purpose of the rule which renders the contract illegal ... 255

7.7.5 Deterrent effect of illegality ... 256

7.8 Conclusion ... 257

Chapter Eight ... 260

8.0 Contractual Restrictions on Beneficiary's Right to draw on a credit ... 260

8.1 Introduction ... 260

8.2 Nature of the exception ... 263

8.3 Rationale for the exception ... 265

8.4. Current state of authorities ... 268

8.4.1 Jurisdictional approaches ... 269

8.4.1.1 Australia ... 269

8.4.1.2 Malaysia ... 273

8.4.1.3 England ... 274

viii

8.5.1 Argument in support of the exception ... 277

8.5.1.1 Novelty and variant of the more typical case ... 277

8.5.1.2 Legitimate expectation of the parties ... 280

8.5.1.3 Contractual Restriction as an express negative covenant ... 280

8.5.1.4 Lack of authority specifically against the exception ... 281

8.5.2 Arguments against the exception ... 282

8.5.2.1 Contrary to the independence principle ... 282

8.5.2.2 Want of certainty ... 283

8.6 The working principles of the exception ... 285

8.6.1 What kind of contractual restriction is required? ... 285

8.6.2 Beneficiary’s unconditional assent to express contractual stipulation ... 287

8.6.3 Standard of proof of the Express restriction on the beneficiary right to draw on the credit ... 288

8.7 Conclusion ... 291

Chapter Nine ... 294

9.0 General Conclusion ... 294

ix

List of Cases

United Kingdom

Akerhielm v De Mare [1959] AC 789. Alexander v Rayson [1936] 1 KB 169.

American Cyanamid Co v Ethicon Ltd [1975] AC396.

Antaios Compania Naviera SA v Salen Rederierna AB [1985] AC 191. Ayerst v Jenkins (1873) LR 16 Eq 275.

Baily v Merrell (1615)3 Bulst 95.

Banco Santander SA v Banque Paribas [2000] CLC 906. Baynes Clarke v Corless [2010] EWCA Civ 338.

Benyon v Nettlefold (1849) 60 ER 1047.

Beresford v Royal Insurance Co Ltd [1937] 2KB 197.

Bhoja Trader The Intraco v Notis Shipping Corp of Liberia [1981] 2 Lloyd’s Rep 256. Bolivinter Oil SA v Chase Manhattan Bank [1984] 1 Lloyd’s Rep 251.

Bowmakers, Limited v Barnet Instruments, Limited. [1945] KB 65. Briess v Woolley [1954] AC 333.

Bristol & West Building Society v Mothew [1998] Ch 1.

Canadian Imperial Bank of Commerce v Drutz (1996) ACWS (3d) 258. Carl Zeiss Stiftung v Herbert Smith [1969] 2 Ch 276.

Centri-Force Engineering Ltd v Bank of Scotland [1993] SLT 190. Chai Sau Yin v Liew Kwee Sam [1962] AC 304.

Chartered Electronics Industries Pte Ltd v Development Bank of Singapore [1999] 4 SLR 655.

Consolidated Oil Ltd v American Express Bank Ltd (unreported, 21 January 2000, CA).

Consolidated Oil Ltd v American Express Bank Ltd [2002] CLC 488. Continental Bank Leasing Corporation v Canada [1998] 2 SCR 298.

Czarnikow- Rionda Sugar trading Inc v Standard Bank of London Ltd [1999] 2 Lloyd’s Rep 187.

x DCD Factors plc and another v Ramada Trading Ltd and others [2007] EWHC 2820. De Beéche and Others v The South American Stores (Gath and Chaves) Limited [1935] AC 148.

Derry v Peek (1889) LR 14 App CAS 337.

Deutsche Ruckversicherung Aktiengeslleschaft v Walbrook Insurance Co ltd [1995] IWLR 1017, [1995] 1 Lloyd's Rep 153.

Diamond Cutting Works Federation v Triefus & Co Ltd [1956] 1 Lloyd’s Rep 216. Discount Record Ltd v Barclays Bank Ltd [1975] 1WLR 315.

Dong Jin Metal Co Ltd v Raymet Ltd, July 13, 1993, Lexis. Doyle v Olby (Ironmongers) Ltd [1969] 2 QB 158.

Edward Owen Engineering Ltd v Barclays Bank International Ltd [1978] QB 159. Elian & Rabbath v Matsas [1966] 2 Lloyd's Rep 495.

Esal (Commodities) v Oriental Credit [1985] 2 Lloyd’s Rep 546. Esso Petroleum Co v Mardon [1976] QB 801.

Euro-Diam Ltd v Bathurst [1990] QB 1. Foster v Driscoll and Others [1929] 1 KB 470.

Geismar v Sun Alliance and London Insurance Ltd [1978] QB 383. Gian Singh and Co Ltd v Banque de l'Indochine [1974] 1 WLR 1234.

Group Josi Re v Walbrook Insurance Co Ltd [1995] CLC 1532, [1996] 1 WLR 1152. Hamzeh Malas & Sons v British Imex Industries [1958] 2 QB 127.

Hedley Byrne & Co Ltd v Heller & Partners Ltd [1964] AC 465.

Henderson v Merrett Syndicates Ltd [1994] CLC 918, [1995] 2 AC 145. Hornal v Neuberger Products Ltd [1956] 3 All ER 970,[1957] 1 QB 247. Howe Richardson Scale Co. Ltd v Polimpex-Cekop [1978] 1 Lloyd's Rep 161.

Ibrahim Shanker Co. and Others v Distos Compania Naviera SA (“Siskina”) [1978] 1 Lloyd's Rep 1.

IE Contractors v Lloyds Bank plc [1989] 2 Lloyd’s Rep 205.

International Dairy Queen Inc v Bank of Wadley (1976) 407 F Supp 1270 (MD Ala). Intraco Ltd v Notis Shipping Corporation [1981] 2 Lloyd's Rep 256.

Itek Corp v First National Bank of Boston (1981) 511 F Supp 1341. Janson v Driefontein Consolidated Mines Ltd [1902] AC 484. KBC Bank v Industrial Steels (UK) Ltd [2001] 1All ER (Comm) 409. Komercni Banka AS v Stone and Rolls Ltd [2003] 1 Lloyd's Rep 383. Kono Insurance v Tins Industrial Co [1987] 3 HKC 71, [1988] 2 HKLR 36.

xi Laurence v Lexcourt Holdings Ltd. [1978] I WLR 1128.

Lepre v Caputo 131 NJ Super 118, 328 A.2nd 650 652. Louth v Diprose (1992) 175 CLR 621.

Lowson v Coombe The Times 2 December 1998. MacDonald v Myerson and another [2001] EGCS 15.

Mahonia Limited v JP Morgan Chase Bank, West LB AG (No 2) [2004] EWHC 1938 (Comm), 2004 WL 1808816.

Mahonia Ltd v JP Morgan Chase Bank and West LB (No. 1) [2003] EWHC 1927 (Comm) [2003] 2 Lloyd's Rep 911.

Man (E D and F) Ltd v Nigerian Sweets and Confectionery Co Ltd [1977] 2 Lloyd's Rep 50

Marconi Communications International Ltd v PT Pan Indonesia Bank Ltd TBK [2004] EWHC 129 (Comm) [2004] 1 Lloyd's Rep 594.

Marconi Communications International Ltd v PT Pan Indonesia Bank Ltd TBK [2005] EWCA Civ 422, [2007] 2 Lloyd's Rep 72.

Marles v Philip Trant & Son Ltd [1954] 1 QB 29. Moffat v Moffat [1984] 1NZLR 600 604-605.

Montrod Ltd v Grundkötter Fleischvertriebs GmbH [2001] CLC 466.

Niru Battery Manufacturing Company v Milestone Trading Ltd [2002] 2All ER (Comm) 705.

Noble v Owens [2011] EWHC 534 (QB) 2011 WL 722313. Österreichische Länderbank v S'Elite Ltd[1981] QB 565.

Owen (Edward) Engineering Ltd v Barclays Bank International Ltd [1978] QB 159. Pasley v Freeman (1789) 3 Term Reports 51.

Pearce v Brooks (1866) LR 1 Ex 213.

Phipps v Boardman [1965] Ch 992 (CA) [1967] AC 46 (HL). Pitts v Hunt [1991] 1 QB 24.

Potton Homes v Coleman Contractors [1984] 28 Build LR 19.

Printing and Numerical Registering Co v Sampson (1875) LR 19 Eq 462, 465. R v Metropolitan Police Commissioner [1975] AC 819 at 834

Rafsanjan Pistachio Producer’s Cooperative v Bank Leumi UK Plc [1992] I Lloyd’s Rep 513

Ralli Brothers v Compañia Naviera Sota Aznar [1920] 2 KB 287. RD Harbottle (Mercantile) v National Westminster Bank [1978] QB 146.

xii Re Ambrose Lake Tin and Copper Mining Co, ex p. Taylor, ex p.Moses (1880) ChD 390, 396-397.

Re H (Minors) [1996] AC 563.

Re Mahmoud and Ispahani [1921] 2KB 717. Regazzoni v KC Sethia (194) Ltd [1958] AC 301.

Royal Bank of Scotland v Homes [1999] Scot Law Times 563. Ruddick v Ormston [2005] EWHC 2547.

Safa Ltd v Banque du Caire [2000] CLC 1556.

Safeway Stores Limited v Twigger [2010] EWHC 11 (Comm) 2010 WL 19891. Saunders v Edwards [1987] 1 WLR 1116.

Shinhan Bank Ltd v Sea Containers Ltd and Another [2000] 2 Lloyd's Rep 406. Silverwood v Silverwood (1997) 74 P&CR 453.

Smith New Court Securities Ltd v Citibank NA [1997] AC 254. Smith v Chadwick (1883–84) LR 9 App Cas 187.

Solo Industries v Canara Bank [2001] 2 Lloyd's Rep 578. St John Shipping Corp v Joseph Rank Ltd [1957]1 QB 267.

Standard Chartered Bank v Pakistan National Shipping Corporation and Others [1998] 1 Lloyd's Rep 684, 687.

State Trading Corp of India v ED & F Man (Sugar) [1981] Com LR 235.

Stone & Rolls Ltd (in liquidation) v Moore Stephens [2008] EWCA Civ 644 [2009] 1 AC 1391 HL.

Strongman (1945) Ltd v Sincock [1955] 2 QB 525, Taylor v Bhail [1996] CLC 377. Thackwell v Barclays Bank Ltd [1986] 1 All ER 676.

The Federal Republic of Nigeria v Santolina Investment Corporation. [2007] EWHC 437 (Ch) [2007] WL 631676.

The Royal Bank of Scotland plc v Holmes [1999] SLT 563. Themehelp Ltd v West and Others [1996] QB 84.

Tinsley v Milligan [1994] AC 340.

Toprise Fashions Ltd v Nik Nak Clothing Co Ltd [2009] EWHC 1333 (Comm). Turkiye Is Bankasi AS v Bank of China [1996] 2 Ll Rep 611, [1998] CLC 182 (CA). Twycross v Grant (1877) 2 CPD 469.

United City merchants (Investment) Ltd v Royal Bank of Canada [1983] 1 AC 168. United Trading Corp v Allied Arab Bank [1985] 2 Lloyd’s Rep 554.

xiii West acre Investments Inc v Jugoimport-SDPR Holding Co [1999] QB 740.

Australia

Ampol Petroleum Limited v Mutton (1952) 53 SR1.

Anaconda Operations Pty ltd v Flour Daniels Pty Ltd (1999 Unreported). Bachmann Pty Ltd v BHP Power New Zealand Ltd [1999] 1 VR 420.

Barclay Mowlem Construction Ltd v Simon Engineering (Australia) Pty Ltd (1991) 23 NSWLR 451.

Boral Formwork & Scaffolding Pty Ltd v Action makers Ltd [2003] NSWSC 713. Clough Engineering limited v Oil and Gas Corporation Limited [2008] FCAFC 136. Hortico (Australia) Pty Ltd v Energy Equipment Co (Australia) Pty Ltd (1985) 1 NSWLR 545.

J H Evans Industries (NT) Pty Ltd v Diano Nominees Pty Ltd (unreported NT Supreme Court, 30 January 1989).

Mitsui Kensetsu Corporation Australia Pty Ltd v State of South Australia (unreported, Qld. Supreme Court, 9 August 1990).

Olex Focas Pty Ltd v Skoda export Co Ltd [1998] 3 VR 380.

Orrcon Operation Pty Ltd v Capital Steel & Pipe Pty Limited [2007] FCA 1319. Pearson Bridge Pty Ltd v State Rail Authority of New South Wales (1982) 1 Aust. Construction LR 81.

Selvas Pty Ltd v Hansen & Yuncken (S.A.) Pty Ltd (1987) 6 ACLR 36. Williamson Limited v Lukey and Mulholland (1931) 45 CLR 282, 299. Wood Hall Ltd v Pipeline Authority (1979) 141 CLR 443.

xiv Woodson (Sales) Pty v Woodson (Australia) Pty Ltd, Unreported Supreme Court of New South Wales 12 July 1996.

Canada

Angelica Whitewear in Cineplex Odeon Corp v 100 Bloor West General Partner Inc[1993] OJ No. 112.

Aspen Planners Ltd v Commerce Masonry and Farming Ltd [1979] 7 BLR 102. Bank of Nova Scotia v Angelica- Whitewear [1987] CarswellQue 24.

Bombardier Inc v Hermes Aero LLC 2004 CarswellQue 2865. Bosse v Mastercraft (1995) 123 DLR (4th) 161 (Ont CA).

Bruchet v Canadian Imperial Bank of Commerce (1982) 40 BCLR 318. Canadian Imperial Bank of Commerce v Drutz (1996) ACWS (3d) 258.

CDN Research and Development Ltd v Bank of Nova Scotia [1981] 32 OR (2d) 578 Henderson v Canadian Imperial Bank of Commerce (1982) 40 BCLR 318.

Lumcorp Ltd v Canadian Imperial Bank of Commerce (1977) CarswellQue 77. Morguard Bank of Canada v Reigate Resources Canada Ltd (1985) 40 Alta Lr (2d) 77.

Rossen v Pullen (1981) 16 BCLR 28.

Malaysia

Bains Harding (Malaysia) Sdn Bhd v Arab Malaysian Merchant Bank Bhd [1996] 1MLJ 425.

xv Daewoo Engineering & Construction Co Ltd v Titular Roman Catholic Archbishop of Kuala Lumpur [2004] 7 MLJ 136.

Esso Petroleum Malaysia Inc v Kago Petroleum Sdn Bhd [1995] I MLJ 149.

Kejurutteraan Awam Cang Ceng SDn Bhd v Standard Chartered Bank [1991] 3CLJ 2502.

Kirames Sdn Bhd V Federal Land Development Authority [1991] 2 MLJ 198. LEC Contractors Sdn Bhd v Castle Inn Sdn Bhd [2000] 3MLJ 339.

Lotterworld Engineering & Construction Sdn Bhd v Castle Inn Sdn Bhd & Anor [1998] 7 MLJ 105.

Malaysia Overseas Investment Corporation Sdn Bhd v Sri Segambut Supermarket Sdn Bhd [1986] 2 MLJ 382.

Nafas Abadi Holdings Sdn Bhd V Putrajaya Holdings Sdn Bhd &Anor [2004] MLJU 148.

Patel Holdings Sdn Bhd v Estet Pekebun Kecil & Anor [1989] 1 MLJ 190.

Perumahan Pegawal Kerajaan Sdn Bhd v Bank Bumiputra Malaysia Bhd [1991]2 MLJ565.

PDE Consulting Services Bhd v Chuan Cement Industries Sdn Bhd [2002] 681 MLJU 1.

Suharta Development Sdn Bhd v United Overseas Bank Bhd & Anor [2005] 2MLJ 762.

Transfield Projects Sdn Bhd & Anor v Malaysian Airline System Bhd [1999]428 MLJU 1.

Transfield Projects Sdn Bhd & Anor v Malaysian Airline System Bhd [2001] 2 MLJ 403.

The Radio and General Trading Co Sdn Bhd v Wayss & Freytag [1998] 1 MLJ 346. Royal Design Studio Pte Ltd v Chang Development Ltd [1991] 2 MLJ 229 (HC).

xvi

Singapore

Andoll Ltd v Korea Industry Co Ltd [1987] SLR 274.

Beam Technology (Mfg) Pte Ltd v Standard Chartered [2003] 1 SLR 597. Bocotra Construction Pte Ltd v Attorney general [1995] 2SLR 733.

Brody, White & Co Inc v Chemet Handel Trading (S) Pte Ltd [1993] 1 SLR.

Chartered Electronics Industries Pte Ltd v Development Bank of Singapore [1992] SLR 655.

Dauphin Offshore Engineering v The Private Office of HRH Sheikh Sultan Bin Khalifa [2000] 1 SLR 657.

DBS Bank Ltd v. Carrier Singapore Ltd [2008] 3 SLR 261.

Eltraco International Pte Ltd v CGH Development Pte Ltd [2000] 4 SLR 290. GHL Pte V Unitrack Construction Ltd [1999]4 SLR 604.

Hiap Tian Soon Construction Pte Ltd and another v Hola Development Pte Ltd [2003] 1 SLR 667.

Korea Industry Co Ltd v Andoll Ltd [1989] SLR 134.

Kvaerner Singapore Plc Ltd v UDL Shipbuilding (Singapore) Ltd [1993] 3 SLR 350. Lambias (Importers & Exporters) Co Pte Ltd v Hongkong & Shanghai Banking Corpn [1993] 2 SLR 751.

McConnell Dowell Construction Pty Ltd v Sembcorp Engineers and Constructors Pte Ltd [2002] 1 SLR 199.

Mees Pierson NV v Bay Pacific (s) Pte Ltd & Others [2000] 4 SLR 393. Min Thai Holdings Pte Ltd v Sunlabel Pte Ltd [1999] 2 SLR 368. Panatron Pte Ltd v Lee Cheow Lee [2001] 3 SLR 405.

Raiffeisen Zentralbank Osterreich AG v Archer Daniels Midland Co[2007] 1 SLR 196.

Raymond Construction v Low Yang Tong, Unreported July 1996.

Samwoh Ashphalt Premix Pte Ltd v Sum Cheong Piling Pte Ltd [2002] 1 SLR 1. Standard Chartered bank v Beam Technology (Mfg) Pte Ltd [2003] 1 SLR 597. Vita Health Laboratories Pte Ltd v Pang Seng Meng [2004] 4 SLR 16.

xvii

United States

Dynamics Corporation of America v The Citizens and Southern National Bank 356 F Supp 991 (1973).

International Dairy Queen Inc v Bank of Wadley 407 F Supp 1270. Intraword Industries Inc v Girard Trust Bank 461 Pa 343 (1975). Itek Corporation v First National Bank of Boston 730 F 2d 19 (1984). J Zeevi and Sons, Ltd v Grindlays Bank (Uganda) Ltd 333 NE 2d 168 (NY 1975).

KMN International v Chase Manhattan Bank NA 606 F 2d 10 (1979).

McConnell v Common Wealth Pictures Corporation 7 NY 2d 465, 166 NE 2d 494, 199 NYS 2d 483 (1960).

Mid-America Tire Inc v PTZ Trading Ltd. 95 Ohio St 3d 367, 768 N.E.2d 619 (2002). Old Colony Trust Co v Lawyers Title & Trust Co 297 F152.

Paris Savings &Loan Association v Walden 730 SW 2d 355 (1987). Ross Bicycle Inc v Citibank NA 178 AD 2d 388, 577 NYS 2d 826 (1991). Semetex Corporation v UBAF Arab American Bank [1995] 2Bank LR 73. Sztejn v Henry Schroder banking Corporation 31 NYS 2d 631 (1941). Tranarg CA v Banca Commerciale Italiana 90 Misc 2d 829 (1977).

Table of Statutes

Bretton Woods Agreement Order in Council 1946 Civil Procedure Rules 1998

Contracts (Right of Third Parties) Act 1999 Factors Act 1889

Financial Services Act 1986 Sale of Goods Act 1979

xviii Finance Act 1933

Sales of Reversion Act 1867 Unfair Contract Terms Act 1977

Unfair Terms in Consumer Contracts Regulations 1999

Table of Figure

1

Chapter One

1.0. General Introduction

The documentary credit1-characterized sometimes as ‘the life blood of commerce’2- retains its role as an instrument for financing international trade. Its development as a financing tool in international trade is a creation of modern commerce that involves parties trading long distances with at times neither previous commercial relationship nor being properly aware of parties’ financial position. In this kind of situation where parties sometimes are unaware of the other parties’ financial position, what the seller/beneficiary needs when dealing with a buyer/applicant with whom no previous commercial relationship exists is an assurance that before he makes shipping arrangements or parts with the goods that he will be paid after shipping the goods. These concerns of the seller/beneficiary3 with respect to his right to payment upon shipment of the goods remain a primary concern which documentary credits4 are designed to satisfy in international sales.

1 A payment instrument that ought to be differentiated from “open” or “travellers” letter of credit which is a letter furnished by a banker or by a merchant of reputation to a person travelling overseas, addressed to the issuers’ correspondents, who were promised with reimbursement for amounts advanced to the beneficiary. It has to be noted that the popularity of travellers’ letters of credit diminished after the development of travellers cheques in 1909 by American Express Co. and has gradually become obsolete. See Peter Ellinger and Dora Neo, The Law and Practice of Documentary

Letters of Credit (Hart Publishing 2009); Michael Bridge (ed), Benjamin’s Sale of Goods (8th edn, Sweet and Maxwell 2010) para 23-001. For detailed discussion on the origin of Documentary credits, see FR Sanborn, Origin of the Early English Maritime and Commercial Law (New York Press 1930) 347.

2 RD Harbottle (Mercantile) Ltd v National Westminster Bank Ltd [1978] QB 146, 155 (Kerr LJ); Power Curber International Ltd v National Bank of Kuwait SAK [1981] 2 Lloyd’s Rep 394,400

(Griffiths LJ); Intraco Ltd v Notis Shipping Corporation of Liberia; The Bhoja Trader [1981] 2 Lloyd’s Rep 256, 257 (Donaldson LJ); Hong Kong and Shanghai Banking Corporation v Kloecker &Co AG [1989] 2 Lloyd’s Rep 323, 330 (Hirst J).

3

Note also that there is equally a concern for the buyer/applicant who for the purposes of hedging his own position does not want to pay the price for the goods until the goods are no longer at the disposal of the seller.

4 It has to be noted that documentary credits are also used to cover payment obligations which do not arise from the shipment or supply of goods and hence does not require the presentation of shipping documents.

2 The documentary credit contract, despite being a creature of the seller’s and the buyer’s interest in the underlying transaction5 that gave rise to it, once issued has the fundamental characteristics of being independent of the underlying contract/transaction that brought it into being. This situation where the documentary credit contract is detached from the underlying contract is aptly captured by the autonomy doctrine. To emphasize this autonomy, a documentary credit is stated to be documentary in character. In this circumstance, the paying bank is prepared to pay the seller/beneficiary because it holds the documents as collateral security and would be prepared to make payment once the documents are conforming regardless of issues in the underlying transaction. Put differently, it is irrelevant to the bank whether the underlying contract involves the purchase of corn, machinery or oil.6 The only exception traditionally recognized where the bank should refuse to pay under the credit occurs if it is proved to the appropriate standard that the documents, though apparently conforming on their face, are in fact fraudulent and the seller/beneficiary or his agent was involved in such fraud.7

The emergence of fraud as an exception to the principle of autonomy has had its own legal implications. One of such implications is that the scope of the fraud rule varies from one common law jurisdiction to the other. Jurisdictions like Australia and Canada, in terms of enforcement of the principle, have developed a more robust and

5

The point here is that the documentary credit contract is established because there is an underlying contract on the basis of which the documentary credit contract was established. This underlying contract sometimes relates to goods which are being exchanged between the buyer and the seller in an international business transaction. However, despite the credit contract taking its life from the underlying transaction, it is assumed to operate independently of the underlying contract that gives its life.

6 But the irrelevance of the underlying contract as to the right of a beneficiary to payment under the credit contract does not mean that where the exceptions operate, a beneficiary’s right to payment under the credit is unaffected.

3 wider ground of interference. Jurisdictions like Singapore, while insisting on the restrictive approach of English law to the fraud rule, have developed some further exceptions like nullity and unconscionability. The primary implication of the fraud rule is that the perceived impregnability of documentary credits is no longer absolute with some circumstances justifying interference with the autonomy doctrine. These circumstances which could displace an otherwise absolute principle by way of being exceptions to this autonomy principle are central to the analysis undertaken in this thesis.

1. 1. Overview of the Research

As its main goal, the thesis examines critically the exceptions to the principle of autonomy in documentary credit transactions. The analysis, as reflected in the title of the thesis, centres fundamentally on documentary credits. However, bearing in mind that documentary credits and demand guarantees are both abstract payment instruments8 that share similar characteristics,9 the thesis, for the purposes of sustaining its arguments, at times analyses case law and secondary data10 dealing with both documentary credits and demand guarantees. The approach adopted in this thesis of treating documentary credits and demand guarantees as payment instruments sharing similar characteristics has the support of not only English jurisdiction but other common law jurisdictions like Canada, Singapore and Malaysia that have

8

The position that documentary credits and demand guarantees are abstract payment instruments is properly reflected in case law. Its abstract nature arises because the credit contracted is said to be autonomous to the underlying contract or transaction upon which it is based. See Hamzeh Malas &

Sons v British Imex Industries Ltd [1958] 2 QB 127; Howe Richardson Scale Co. Ltd v Polimex-Cekop

[1978] 1 Lloyd's Rep 161; R D Harbottle (Mercantile) Ltd. v National Westminster Bank Ltd [1978] QB 146.

9 See Howe Richardson Scale Co. Ltd v Polimex-Cekop [1978] 1 Lloyd's Rep 161165 and Bolivinter Oil S A v Chase Manhattan Bank N.A. [1984] 1 WLR 392, 393.

10

In this case, I refer to opinion expressed in books, articles and other published materials that are different from case law and statutes.

4 regularly maintained that the relevant legal principles applicable are the same in both types of case and judicial authorities have sustained this assumption by using authorities interchangeably.11

To facilitate the discussion necessary to deal with the topic, the thesis analyses: (a) Documentary credits, the autonomy doctrine and the rationale behind it, (b) The established fraud exception to the principle of autonomy in documentary

credit;

(c) The rationale and scope of the exception;

(d) The reason why it established itself as a defence capable of breaching the autonomy doctrine;

(e) The other exceptions to the principle of autonomy in documentary credits; (f) Arguments in support of and against their recognition and whether their

recognition in any way affects documentary credit practice.

In addressing the above issues, the thesis aims to answer some crucial research questions viz:

(a) How satisfactory is the present approach of English law with respect to the scope of the fraud exception and to what extent does it defeat or facilitate the letter of credit instrument?

11

Edward Owen Engineering Ltd v Barclays Bank International Ltd [1978] QB 159; Howe Richardson Scale Co Ltd v Polimex- Cekop [1978] 1Lloyd’s Rep161.

5 (b) To what extent is illegality a defence to the principle of autonomy in documentary credits and to what extent is the scope of the exception properly defined?

(c) Apart from fraud and illegality, are there convincing reason(s) for the judicial recognition of some other exceptions to the principle of autonomy in documentary credits? In addressing this question, the thesis investigates such other exceptions as nullity, beneficiary’s recklessness, unconscionability, and finally discusses contractual restrictions on a beneficiary’s right to draw on a credit.

(d) Taking into consideration that documentary credit law represents an area of law that is constantly changing and embracing wisdom that did not previously exist, the thesis, as part of its conclusion, suggests approaches to the exceptions that the author deems preferable. Put differently, the thesis explores whether a change of attitude from the current predominant approach that emphasizes the supremacy of the autonomy doctrine even in the face of strong countervailing consideration(s) ought to be revisited. The recommendation offered is based on the information gathered from the detailed and critical analysis of issues under consideration.

1. 2. Methodology of the Research

The thesis adopts an approach that is analytical and not simply descriptive of the issues discussed. It critically examines the research topic and the issues raised there in,

6 by principally analysing case laws, statutes and other legal instruments related to the issues under consideration. It also makes an extensive use of other secondary literature related to the topic.

The thesis, for the purposes of ensuring that the issues analysed are clear, adopts a method that analyses the exceptions in the order that simplifies the understanding of the exceptions. In this regard, fraud as a primary exception to the principle of independence is analysed first. After examining fraud, exceptions, which though not based on fraud but are perceived to be an extension of the fraud exception, are examined. Here the thesis investigates the extent to which it is appropriate to say that issues that are detached from the fraud of the beneficiary or his agent could in fact provide a good defence that could displace the autonomy principle. Specific issues, emerging as separate exceptions, which seem to have evolved or are still evolving in the course of judicial pronouncement on the fraud exception are nullity, unconscionability or bad faith and beneficiary’s recklessness. Other exceptions whose operations are predicated on some other legal considerations that are different from fraud are considered. The exceptions considered here include illegality and express contractual restrictions on beneficiary’s right to draw on the credit.

Finally, the thesis addresses the research questions by comparatively analysing the legal positions (but not in all circumstances) in other common law jurisdictions namely Canada, United States, Australia, Singapore and Malaysia. The objective is to analyse the legal practices in other common law jurisdictions with respect to the exceptions and use it as a yardstick for judging the merits or satisfactoriness of the

7 arguments that have been advanced mostly in English law against the widening of the exceptions.

1. 3. The Thesis Outline

The thesis chapter structure reflects a sequential presentation of arguments that address the key research questions. It is divided into nine chapters. Overall, the thesis begins with a general introduction and ends with a general conclusion.

Chapter One is the introductory chapter. The chapter highlights the general overview of the thesis, the research methodology adopted and overall structure of the thesis.

Chapter Two deals with the nature of documentary credits and analyses the relevance of the principle of autonomy. The chapter looks at the general components of documentary credits. It introduces the various contracts involved in a documentary credits transaction and also outlines the basic features of each layer of contract. It highlights the cardinal principle evident in documentary credits known as the autonomy principle and the role it plays in documentary credits. This chapter also examines the nature and relevance of this doctrine. It explains how the strict adherence to the doctrine of autonomy has shaped the practice and perception of documentary credits in the different legal jurisdictions. It also analyses the extent to which the strict interpretation of the autonomy doctrine is well founded. Finally, the chapter closes with a discussion of the functions of documentary credit and the different ways in which it can be utilized.

8 Chapter Three analyses the issues relating to the fraud exception to the principle of autonomy in documentary credits. It is divided into two parts. Part One analyses the general issues relating to fraud. In this respect, it notes that the autonomy principle is central to documentary credit. However, the autonomy principle admits of an important exception if the beneficiary of the undertaking fraudulently seeks payment when he has no right to payment. Courts of different legal jurisdictions have in a long line of cases acknowledged fraud as an exception to the principle of autonomy in documentary credits. But the parameters or scope of the fraud exception to the autonomy principle remain largely imprecise. The reason for this lies in the way that the different national courts have defined the scope of fraud that is capable of constituting an exception to the principle of autonomy in documentary credits. Also the standard of proof required to establish such fraud has been a subject of different treatment from the various jurisdictions. The chapter takes a comparative approach to the issue of fraud with the objective of establishing if the English approach to the fraud rule is in the main satisfactory. It ends with a question as to whether there is room for some other exceptions to the principle of autonomy. The second part of the analysis relating to the fraud rule concentrates on fraud in deferred payment and the effect of the current UCP 600 in relation to such fraud. It seeks to address the question whether the problems created by the Banco Santander Case has been resolved by this latest edition of the UCP 600.

Chapter Four assesses the nullity exception in documentary credits which is an extension of the fraud rule. Nullity as an exception that is distinct from fraud has been recognised by the Singapore courts. But in England it has been held that the nullity exception is not part of the English law. The chapter considers the Singapore

9 approach to the exception and the extent to which its recognition is founded on sound legal principle bearing in mind the autonomy rule. It also considers the scope and rationale for the exception. Finally the chapter concludes with an examination of the arguments for or against the nullity exception with the objective of assessing whether it should be recognised in other jurisdictions.

Chapter Five considers whether recklessness of the beneficiary in tendering a document forged by a third party is an exception to the autonomy principle and capable of excusing payment where his dishonesty could not be established. Beneficiary’s recklessness traces its origin from the dictum of the court in the Singapore case of Lambias and has been favourably commented on by the English Court of Appeal in Montrod’s case. The chapter considers to what extent the enthusiasm generated by the dicta of the courts in the case of Lambias and Montrod regarding beneficiary’s recklessness as a possible exception to the autonomy principle should be welcomed or whether its recognition runs contrary to accepted documentary credit practice. In addressing the question relating to beneficiary’s recklessness, consideration is given to the question whether the beneficiary owes a duty to act carefully so as to safeguard the issuing bank and/or the applicant against being defrauded by a third party who may be involved in the preparation of the documents stipulated in the credit.

Chapter Six deals with the unconscionability exception and the focus of this chapter is a consideration of whether unconscionability can constitute a separate ground upon which the independent undertaking in documentary credits can be breached. It then explores the question whether unconscionability should be recognised in English law.

10 Chapter Seven examines the illegality exception to the principle of autonomy in documentary credits. Under English law, the illegality exception is gradually gaining ground as an exception to the autonomy rule in letters of credit. This is evident from prevailing judicial pronouncements. The chapter looks at the nature of the illegality exception. It analyzes the authorities that are a pointer in the direction of its recognition as well as decisions that have acknowledged it. It aims to define and analyse the scope of the exception and the standard for establishing it. It also weighs the exception by analysing the arguments for or against it. The chapter concludes by addressing in a comparative manner illegality issues in letter of credit from other jurisdictions with the view to understanding the law and practice in place in other jurisdictions.

Chapter Eight deals with contractual restrictions on the beneficiary’s right to draw on the credit. It discusses the exception to ascertain to what extent it is accurate to argue that the principle of autonomy is undermined in a case where the beneficiary had expressly agreed with the applicant for the credit not to draw down the credit unless certain conditions are fulfilled and a draw down is sought to be prevented on the grounds of non-fulfilment.

Chapter Nine summarizes the issues and conclusions arrived at. It aims to take a position based on the issues raised and discussed in the preceding chapters. It endeavours to point out issues that probe the current thinking (accepted practice of documentary credits law exceptions) with a view to assessing the satisfactoriness of the current position of the law.

11 Chapter Two

2.0. Nature of Documentary Credit and Principle of Autonomy

2. 1. Introduction

Amidst the various ways in which the price of exported goods may be paid, documentary credit12 plays a vital role in international sales. Its origin is traceable to the activities of merchants concerned with the ways of resolving the conflicting interests between the parties to a contract of sale. On the one hand, the seller does not want to give up the control of the goods before he has received the purchase price. On the other hand, the buyer of goods, for the purposes of hedging his own position, does not want to pay the price for the goods until the goods are no longer at the disposal of the seller. It is to resolve this conflict between the buyer and the seller arising from their interest in the goods that the documentary credit was developed.13

The primary concern of this chapter is to spell out the fundamental issues relating to documentary credits, whose understandings are necessary for a proper appreciation of the issues subsequently discussed in later chapters. The chapter is divided into sections and generally deals with the meaning of documentary credit, the mechanism

12 Documentary credit has already occasioned one of the greatest outpourings of legal writings. Notable textbook in the area include: Richard King, Gutteridge and Megrah’s Law of Bankers Commercial

Credits (Europa Publication 2001); Peter Ellinger, Benjamin’s Sale of Goods (10th edn, Sweet & Maxwell 2002); Michael Brindle & Ray Cox Law of Bank Payment (Sweet &Maxwell 2004) Ch 8; Mark Hapgood, Paget’s Law of Banking (Lexis Nexis 2007) ch. 34; Ewan McKendrick, Goode on

Commercial Law (Penguin 2009) Ch. 35; Ali Malek and David Quest Documentary Credits (4th edn, Tottel Publishing 2009); Raymond Jacks, Documentary Credit (Trottel 2009); Peter Ellinger & Dora Neo, The Law and Practice of Documentary Credit (Hart Publishing 2010).

12 of operations and the parties to it. It discusses the principle of autonomy which together with the doctrine of strict compliance form the cardinal rules that underpin the law and practice of documentary credits. Some aspect of the sections, deal with the different legal instruments that regulate and govern documentary credit practice.

2. 2. The Concept of Documentary Credits

The documentary credit was once described by Professor Kozolchyk14 as a type of mercantile currency embodying an abstract promise of payment, which possesses a high, though not total, immunity from attack on the ground of breach of duty of the seller to the buyer. This apt definition of documentary credits raises a further question inherent in the definition itself as to the circumstance(s) contemplated in the definition under which the high immunity evident in the abstract promise to pay will not be total.15 Another eminent academic,16 referred to a documentary credit as ‘a money promise which is independent of the transaction that gives it birth and which is considered binding when received by the beneficiary without acceptance, consideration, reliance, or execution in solemn form.’17

In similar vein, the Uniform Customs and Practice for Documentary Credits (UCP 600) defines documentary credit as an arrangement, however named or described, that

14 See Kozolchyk, ‘Letters of credit’, (1973)in IX International Encyclopaedia of Comparative Law (ed K zweigert and Ulrich Drobnig, 1973) Chapter 5 at pp138-143; Roy Goode ‘Abstract Payment Undertakings’ in Peter Cane and Jane Stapleton (ed), Essays for Patrick Atiyah (OUP 1991) 1079, 1098. See also the definition offered by Professor Ellinger, where he argued that documentary credits should be treated as a sui generis instrument embodying a promise which by mercantile usage is enforceable without consideration. E P Ellinger, Documentary Credit (1970) ch.IV cited in Ewan McKendric Goode on Commercial Law ( Penguin 2009) 1078.

15 It has to be noted that these circumstances albeit restricted to those situation where they displace the autonomy principle remain the major interest pursued in this thesis.

16 See Roy Goode ‘Abstract Payment Undertakings’ in Peter Cane and Jane Stapleton (eds), Essays for Patrick Atiyah (OUP 1991).

13 is irrevocable and thereby constitutes a definite undertaking of the issuing bank to honour a complying presentation.18 In this regard, a complying presentation is also defined in the UCP 600 as ‘a presentation that is in accordance with the terms and conditions of the credit, the applicable provisions of this rule and international standard banking practice.’19

From the foregoing definition of documentary credits, some issues are worth pointing out. The first is that the contracts of documentary credits though having a binding force20 does not follow the normal rules of contract. It still remains binding in the absence of the normal contract law rules of consideration and acceptance.21 The explanation logically given for its binding force in the absence of such ingredients like consideration (being ingredients required to make a contractual obligation binding) is that its application is based on mercantile usage.22 Secondly and more importantly, is that the undertaking is independent. The nature of the independence of the undertaking is captured by the Professor Kozolchyk23 who described its independence in terms that reflect documentary credits as possessing a high, though not total immunity from attack on the ground of breach of duty of the seller to the buyer. As will be reflected later in the subsequent chapters, the thesis analyses the circumstances

18 Article 2, UCP 600, note also that only irrevocable credit is described as credit and is different from the UCP 500 that describes both revocable and irrevocable credit.

19 ibid.

20 Article 7 (b) where the UCP 600 stated that an issuing bank is irrevocably bound to honour as of the time it issues the credit.

21

Consideration and acceptance are essential ingredients that make a contract binding in ordinary rules of contract.

22 EP Ellinger, Documentary Letters of Credit- A Comparative Study (University of Singapore Press 1970); Roy Goode, ‘Abstract Payment Undertakings’ in Peter Cane and Jane Stapleton (eds), Essays

for Patrick Atiyah (OUP 1991) 225.

23

See Kozolchyk ‘Letters of Credit’ (1973)in K Zweigert and K Drobnig (eds), IX International

14 under which the high immunity24 on the ground of breach of duty of the seller to the buyer could be displaced.

2. 3. Parties to Documentary Credit

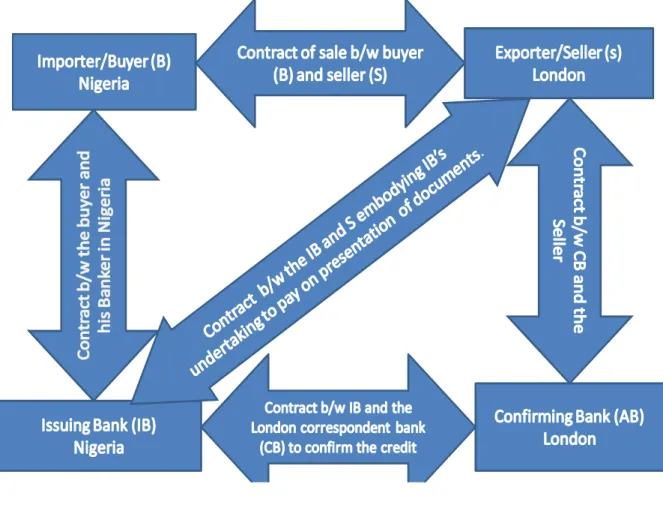

In line with the current definition of documentary credits, 25 five contractual relationships26 arise in a transaction in which an irrevocable documentary credit is issued.27 These basic contractual relationships exclude the addition of parties through negotiation of drafts or the transfer of credit.28 The five contractual relationships which arise in a typical transaction involving an irrevocable credit are: (1) a contract of sale between the buyer (the applicant for the credit) and the seller (the beneficiary), (2) a contract between the buyer and the issuing bank containing the terms on which the letter of credit is opened, (3) a contract between the issuing bank and the bank which confirms or advises the credit (the confirming or advising bank) embodying the advising or confirming bank’s mandate to advise and/or confirm the credit, collection of documents and payment on acceptance or negotiation, (4) a contract between the issuing bank and the seller containing the issuing bank’s undertaking to the seller to pay him or accept or negotiate his draft(s) provided that the seller has presented the stipulated documents in accordance with the terms of the credit and (5) a contract between the confirming bank and the seller containing the confirming bank’s additional undertaking to the seller to pay him or accept or negotiate his draft(s)

24

High immunity in this case referring to the impregnability of documentary credits as reflected in the doctrine of autonomy of the credit.

25 See the definition of the UCP 600 in article 2.

26 For more detailed analysis of the parties to a documentary credit, see Ewan McKendrick (ed), Goode on Commercial Law (4th edn, Penguin 2009) 1087.

27 Note that in United City Merchant (Investment) Ltd v Royal Bank of Canada [1983] 1 AC 168, 182, Lord Diplock identified only four autonomous but interconnected contract in a documentary credit sales. Lord Diplock here excluded the contract between the issuing bank and the seller/beneficiary embodying the issuing bank’s undertaking to pay upon presentation of complying documents. 28 Roy Goode, Commercial Law (Penguin 2004) 978.

15 provided that the seller has presented the stipulated documents in accordance with the terms of the credit.29

Figure 2: The Diagram below illustrates the five parties to documentary credits. (Own Illustration)

The above diagram represents (barring the addition of other parties in the contract through negotiation of draft or transfer of credit) the five main parties to a

29 See Standard Chartered Bank v Pakistan National shipping corporation (No 2) [1998] 1 Lloyd’s Rep 218 and [2001] 1QB 167; Bank of Credit & Commerce Hong Kong Ltd (in Liquidation) v Sonali Bank [1995] 1Lloyd’s Rep 227.

16 documentary credit in a hypothetical case of a Nigerian importer/buyer and an English Exporter/seller in London. Note the double-arrowed lines showing the two-way relationship between the parties to documentary credits –leading to the five contractual relationships that arise in a typical transaction in which an irrevocable documentary credit is issued.

2. 3.1. The Underlying Contract of Sale

Basically, the contract between the buyer and seller is the root contract from which all contracts stem. The seller’s right to demand a letter of credit, and the nature of the credit to which he is entitled, depends on the terms of the contract of sale. On the other hand, the buyer must ensure that the letter of credit issued to the seller is that prescribed by the contract. Fulfilment of this obligation is a condition precedent to the seller’s duty to perform his delivery obligations.30 For example if the letter of credit stipulates a bill of lading as one of the shipping documents when the contract permits seller to tender a delivery order, the letter of credit will be defective and can be rejected by the seller.31 If a nonconforming letter of credit is tendered and rejected, the buyer may cure the defect by procuring the issue of a new and conforming letter of credit if still within the time limit.32 However, if he fails to do so or is out of time, he commits a repudiatory breach, which entitles the seller to treat the contract as discharged33and to recover damages from him. It may also be noted that if the seller

30 Garcia v Page & Co Ltd (1936) 55 LI L Rep 391; Etablissments Chinbaux SARL v Harbourmaster Ltd [1955] 1 Lloyd’s Rep 303.

31 See Roy Goode Commercial Law (3rd edn, Penguin 2004) 979, (4th edn, Pengiun 2009) 1087. 32

Forbes, Forbes, Campbell & Co v Stanley & Co (1921) 9 LI L Rep 202. 33 Trans Trust SPRL v Danubian Trading Co Ltd [1952] 1Lloyd’s Rep 348.

17 elects to waive the breach and accept a nonconforming letter of credit, he loses his right to complain of breach34

It should be noted that a term in the contract of sale providing for payment by letters of credit is for the interest of both parties. Hence, the seller is not ordinarily entitled to demand payment in any other way nor to sue for the price during the pendency of the credit or complain of non-payment by the buyer during this period.35 The letter of credit, like the bill of exchange, is considered to be taken as conditional payment unless otherwise agreed, and during the lifetime of the credit, the seller’s right to sue for the price is suspended. If the credit is honoured, that constitutes payment under the contract of sale. If it is dishonoured, the seller’s right to sue the buyer for the price or for damages revives.36

In the same vein, the buyer is generally not entitled to call for the tender of documents in a manner inconsistent with the letter of credit arrangements prescribed by the contract of sale. So, if pursuant to that contract (or a later arrangement or understanding by the parties) the letter of credit issued to the seller calls for the tender of document to the advising bank, the seller is not obliged to tender the documents directly to the buyer or to the issuing bank or to anyone other than the advising bank.37

34 In this regard, no question of damages as for breach of warranty arises; by waiving the breach, the seller assents to the letter of credit in the form in which it is issued.

35 See exception as expressed in Mann (E D and F) Ltd v Nigerian Sweets and Confectionery Co Ltd [1977] 2 Lloyd's Rep 50, in situation where the letter of credit has failed due to the issuing bank going into administration. In this case, the claimant/ beneficiary could proceed against the buyer directly for the price agreed in the contract of sale or sue for damages for breach of their contractual promise to pay by letter of credit. See also WJ Alan &Co v L Nasr Export [1972] 1 Lloyd’s Rep 313.

36

See EP Ellinger, ‘Does an Irrevocable Credit Constitute Payment’ (1977) 40 MLR 91. 37 Roy Goode, Commercial Law (3rd edn, Penguin 2004) 980.

18 As to the time of the opening of the credit, subject to any express provisions in the contract which gives the parties the liberty to contract according to their own terms, the letter of credit has to be opened within reasonable time38 This means a reasonable time calculated back from the date of the shipment, not calculated forward from the date of conclusion of the contract.39 Taking the first date of shipment as the starting point, the buyer has, it is thought, to open the credit a sufficient time in advance of that event to enable the seller to know before he sends the goods to the docks that his payment will be secured by the credit for which it is stipulated.40

The duration of credit or the date of expiration is a very vital statement in the letter of credit. In the absence of such a statement, the implication is merely that the credit endures for a reasonable time, a somewhat vague concept that leaves the seller in a state of uncertainty as to whether he is covered for the full shipment period and as to the latest date by which a tender of document is acceptable.

The UCP 600 re-emphasized the crucial nature of this statement in letter of credit. Article 6(d)(i)41 provides:

‘A credit must state an expiry date for presentation. An expiry date stated for honour or negotiation will be deemed to be an expiry date for presentation’

39 This is an implied term of the contract. See Diamond Cutting Works Federation v Triefus & Co Ltd [1956] 1 Lloyd’s Rep 216, 225.

40 Sinaison- Teicher Inter-American Grain Corporation v Oilcakes and Oilseeds Trading Co Ltd [1954] 1WLR 935.

19 The UCP further contains detailed provisions for the ascertainment of the expiry date and its extension should it fall on a day when the bank is closed42 or in case of interruption of the bank’s business. 43

Finally, in terms of rejection of the goods, the acceptance of documents under a letter of credit does not preclude the buyer from subsequently rejecting the goods themselves if on arrival they are found not to conform to the contract of sale.44

2.3.2. The Contract between the Buyer and the Issuing Bank

Here, pursuant to the contract of sale, the buyer requests his own bankers to open a documentary credit in favour of the seller. The relationship between the issuing bank and the buyer is that of a banker and customer. The buyer completes an application form provided by the banker. The terms of the contract are set out in details in the Issuing Bank’s standard form of application, which normally incorporates the UCP. In English practice, the contract is usually a unilateral contract in which the buyer’s submission of the application constitutes an offer which the issuing bank accepts by conduct in issuing the letter of credit.45 The issuing bank owes the usual duties of a banker strictly to observe the terms of the mandate,46 and to act in other respects with reasonable care and skill in relation to the credit, except so far as these duties are

42

See Art.29 (a) and (b), UCP 500 Art.44. 43 UCP 600, Art.36, UCP 500 Art. 17.

44 Here, the buyer’s right to reject defective or nonconforming goods is not affected by the fact that the defect or nonconformity was apparent on the face of the documents accepted by the issuing bank. One rational explanation for this is that in accepting the documents, the paying or confirming bank acts as principal, not as the buyer’s agent. Hence, it would seem that the buyer is entitled to reject even for defect apparent on the face of the documents, which he would not be entitled to do if the documents had been accepted by him or his agent.

45

Ewan McKendrick (ed), Goode on Commercial Law (4th edn, Penguin 2009) 1089. 46 ibid 1089.

20 effectively qualified by the contract. In particular, the issuing bank is responsible for ensuring that the letter of credit issued to the seller complies strictly with the instructions contained in the application for the credit and that payment, acceptance or negotiation is effected only on presentation of documents which fully accord with the terms of the credit.

It need not be over-emphasized that the letters of credit issued by the issuing bank to the seller constitutes an autonomous engagement in which the issuing bank acts as principal, not as the agent of the buyer.47 It simply follows from the above that the buyer is not entitled to give instructions to the issuing bank to withhold payment or to deviate from the terms of the credit. The issuing bank is both entitled and obliged to ignore any such instructions so long as the documents are presented within the period of the credit and duly comply with its provisions.

Also, if the credit is not honoured, the issuing bank is obliged to indemnify the buyer against any liability he may incur from the seller.48 On the contrary, where the issuing bank makes payment without authority against non-complying presentation,49 the buyer, though not entitled to reject conforming goods from the seller, may as between himself and the issuing bank decline to adopt the transaction, on account of breach of mandate.50 In this case, the issuing bank cannot debit the buyer with the price paid or with remuneration for its services, while the buyer for his part is taken to have

47RM Goode, Commercial law (3rd edn, Penguin 2004) 982. Note also that in some authorities like Bank Melli Iran v Barclays Bank [1951] 2 Lloyd’s Rep 267, a relationship between the issuing bank

and the instructing bank which is similar to the relationship between an issuing bank and applicant was referred to as that of agency. Note also the dictum of Devling J. in Midland Bank v Seymour [1955] 2 Lloyd’s Rep 147, 153.

48 Ewan McKendrick (ed), Goode on Commercial Law (Penguin 2009) 1090. 49

If he acts promptly, the buyer may be able to obtain an injunction to restrain such payment. 50 Ewan McKendrick (ed), Goode on Commercial Law (Penguin 2009)1090.

21 rejected (abandoned) the goods to the issuing bank, in whom they will then vest51 In addition, the buyer may claim damages for any loss reasonably foreseeable by the issuing bank as likely to flow from the breach.52

The buyer as an alternative to rejecting the documents may waive the breach or accept the documents without prejudice to his right to damage for any resulting loss. Here the buyer will be deemed to have waived any nonconformity if he obtains delivery of the goods from the carrier without production of the bill of lading53 in circumstances where this needs to be tendered under the credit. Where this is the case, it may be noted that the buyer has no right to take the goods from the carrier and it would be fraud on the seller from the buyer, having wrongfully procured the goods, to prevent payment under the credit. At the moment, there seems not to be any English case law on the subject of acceptance of documents under reservation of the right to damages54 and thus no adequate guide to the measure of damages.

2. 3.3. The Contract between the Issuing Bank and the Advising Bank

The issuing bank begins the inter-bank contractual relationships when it asks another bank, usually in the seller’s country, to advise the seller (beneficiary) of the credit or to confirm the credit. The contract is made between the issuing bank and the advising

51

R Goode, Commercial Law (Penguin 2004) 980.

52 Here damages are recoverable under the rule in Hadley v Baxendale (1854) 9Exch341.

53 It may be noted that at present, carriers sometimes agree to release goods without the bill of lading against guarantees and warranties. This takes care of situations where the preparation and delivery of the bill of lading is delayed with the result that goods arrive before it. See generally RM Goode,

Proprietary Rights and Insolvency in Sales Transactions (2nd edn 1989); For latest edition, see Roy Goode and Simon Mills, Proprietary Rights and Insolvency in Sales Transactions (3rd edn, Sweet and Maxwell 2009).

54

This may be due to allegation of wrongful honour of credit being resolved mainly through out of court settlement.