MICRO INSURANCE IN INDIA: A POWERFUL TOOL TO EMPOWER POOR

DEEPAK KUMAR ADHANA

Research Scholar, Institute of Mgt. Studies & Research, M.D. University, Rohtak

MAYANK SAXENA

Assistant Professor, J.S. (PG) College, Sikandrabad, Bulandshahr (INDIA)

ABSTRACT

Poor people are the most vulnerable to shocks arising from sickness, accidents, death or loss of assets due to natural calamities and riots, etc. Micro insurance is the protection of such low-income people against specific perils in exchange for regular premium payments proportionate to the likelihood and cost of the risk involved. Micro insurance is recognized as the terrain where innovation in insurance can be and indeed is being experimented. The strongest drive to understand more about micro insurance comes from the realization that insurance is an essential tool in improving the protection of low income persons against the financial exposure due to life cycle events, economic activity, environmental issues and political issues. Insurance cannot resolve any of the major underlying issues;

it can however provide the tools that delimit the financial exposure of single individuals when adverse, cost generating events occur.

With the liberalization of the Indian economy in the 1990s, and the government's stance of inclusive growth, the Insurance Regulatory and Development Authority Act were passed in 1999, and the insurance sector was opened for the private sector. Subsequently, micro insurance regulations were introduced in 2005. With these government initiatives to provide risk coverage to the poor, there has been a significant increase in insurance penetration and density in India.

Though there is a growth in the Micro Insurance but still India has very low Insurance penetration. The main objectives of the study are to study Micro Insurance market in India, regulations pertaining to Micro Insurance and analyses the initiatives taken and progress made so far by Micro Insurance in India.

KEY WORDS: Micro Insurance, Social Insurance, Social Security, IRDA I. INTRODUCTION

The term micro insurance is comprised of two words “Micro” which means “Affordable to the poor” and

“Insurance” means “Risk pooling to compensate to individual and group”. Micro insurance, a recent concept in the field of micro finance, helps reduce vulnerabilities of microfinance clients and saves them from disastrous liabilities.

The last decade has seen several myths being exploded about the repayment capacity of the poor. With the recognition of the fact that “Poor are Bankable” micro finance came into play. Several players came forward with a view to make the poor financially sustainable. But it was felt that the effect of the microfinance intervention would get eroded in absence of a comprehensive risk mitigation tool. This gave birth to the idea of Micro- Insurance.

The term "Micro insurance” typically refers to insurance services offered primarily to clients with low income and limited access to mainstream insurance services and other means of effectively coping with risk. More precisely, Micro insurance is a means of protecting low income people against specific risks in exchange for a regular payment of premiums whose amount is proportional to the likelihood and cost of the relevant risk. Thus “Micro insurance is a financial tool that helps low-income households mitigate risk and plan for the future. It enables them to cope with unpredictable and irregular incomes, while also preparing them for financial emergencies that threaten their livelihood.”

DEFINITIONS

CONSUMER BASED DEFINITIONS: These definitions use “micro” in reference to the consumers of micro insurance products. The clients are “micro” in the sense that they have low net worth, low income, little property or assets, etc.

PRODUCT BASED DEFINITIONS: These definitions apply the term micro to characteristics of the products, such as having low premiums, low levels of coverage, being affordable and accessible, etc.

QUALITATIVE: “Micro insurance is the protection of low-income people against specific perils in exchange for regular premium payments proportionate to the likelihood and cost of the risk involved.”

QUANTITATIVE: In 2007 in Peru, micro insurance was defined as massive, cheap and low coverage insurance. Regulation was applied to any insurance that didn’t exceed USD 3,300 coverage limit or USD 3, 3 monthly premiums and required certain policy features such as minimum requirements for group policies, an application certificate to begin the insurance coverage, simple coverage, minimum number

of exclusions, no previous evaluations of policyholders or insured values necessary, no deductibles and copayments, and payment of claims must be done in 10 days (in reality, 3 days).

In principle, micro-insurance works like any typical insurance business. But there are several things that differentiate it from normal insurance. First, it is group insurance that can cover thousands of customers under one contract. Second, micro-insurance requires an intermediary between the customer and the insurance company. Preferably, this intermediary is a non-governmental organization (NGO) or microfinance institution, for example a rural bank that can handle the whole distribution and most of the administration process. The few differences between traditional insurance and micro-insurance are as follows:

Traditional Insurance Micro-insurance Clients Low risk environment.

Established insurance culture

High risk exposure/ high vulnerability,

Weak insurance culture Distribution

model

Sold by licensed intermediaries or by insurance companies directly to wealthy clients or companies that understand insurance

Sold by non-traditional intermediaries to clients with little experience of insurance

Policies Complex policy documents with many exclusions

Simple language

Few ,if any exclusion

Group policies Premium

calculation

Good statistical data

Pricing based on Individual risk

Little historical data,

Group pricing

Very price sensitive market Premium

collection

Monthly/quarterly/semi or annually collection

Frequent or irregular payment adapted to volatile cash flow of clients

Often linked with other transaction (e.g. loan repayment

Control of insurance risk (adverse selection,

Limited eligibility,

Significant documentation required

Screening such as medical test is

Broad eligibility

Limited but effective control

Insurance risk included in premium

moral hazards, frauds)

required rather than exclusion

Linked to other service (like credit) Claims

handling

Complicated process

Extensive verification documentation

Simple and fast procedure of small firms.

Efficient fraud control Premium

Interval

Regular premium payments Premiums should be designed to accommodate customers’ irregular cash flows

Mode of

Premium Payment

Premium collected mostly from deductions in bank account

Premium often collected in cash or associated with another financial transaction

Insurance Sale Agents and brokers are primarily responsible for sales

Distribution channel may manage the entire customer relationship, perhaps including premium collection and claims payment

Insured Sum Large sums insured Small sums insured Premium

Based on

Priced based on age/specific risk Community or group pricing

TYPES OF MICRO INSURANCE 1. LIFE INSURANCE

Life insurance pays benefits to designated beneficiaries upon the death of the insured. There are three broad types of life insurance coverage: term, whole-life, and endowment. Term life insurance policies provide a set amount of insurance coverage over a specified period of time, such as one, five, ten, or twenty years. This insurance is appropriate when the policyholder's need for coverage is temporary.

Compared with other life insurance policies this is not very complicated for the provider to offer. This is the most widely used life insurance policy in low-income communities in developing countries.

Whole life insurance is a cash-value policy that provides lifetime protection. This is hardly offered in low- income markets in the developing countries Endowment life insurance pays the face value of insurance if the policyholder dies within a specified period. It thus has a longer time horizon that the term life insurance. This is also not offered widely in developing countries.

2. HEALTH INSURANCE

Health insurance provides coverage against illness and accidents resulting in physical injuries. While actual coverage varies, many health insurance providers cover for limited hospitalization benefits for certain illnesses, and for costs of physician visits and medicine. Some insurance providers also make available primary health care services such as immunization and contraceptives.

3. PROPERTY INSURANCE

Property insurance provides coverage against loss or damage of assets. SEWA in India, for example, provides insurance against damage to home and productive assets.

4. DISABILITY INSURANCE

Disability insurance in most cases is tied to life insurance products. It provides protection to the policy holder and her family, should she or some of her family suffers from a disability.

5. CROP INSURANCE

Crop insurance typically provides policy holders protection in the event their crops are destroyed by natural calamities such as floods or droughts.

6. UNEMPLOYMENT INSURANCE

Unemployment insurance is typically offered by the public sector. Private insurance companies are usually not involved in it. This insurance provides cash relief to individuals who become unemployed involuntarily and who meet certain government requirements. It also helps unemployed workers find jobs. Unemployment insurance attempts to stabilize the economy by enabling people to maintain their purchasing power.

7. REINSURANCE

Reinsurance is the shifting of part or all of the insurance originally written by one insurer to another.

This is a central feature of the operations of all commercial insurers.

II. NEED AND OBJECTIVES OF STUDY

Insurance segment is mainly engaged in serving only the people who have regular income. The sector by no means seeks to uplift the rural poor who are most prone to risk and mostly cope up with risk by selling their assets or reducing their consumption. The poor felt the need for pecuniary gear to protect their families as well as themselves against risks that arise in course of life. There is a strong need to make sure that that they have access to appropriate products, and have a positive experience with insurance. Hence, the need for micro insurance comes here to protect the poor from a hotchpotch of

risks. The need of the study is an attempt to understand the progress made by the micro insurance sector, the regulations followed by the sector and initiatives taken so far to promote this sector in India.

Based on these, the main objectives of the study are:

1. To study Micro Insurance market in India

2. To study regulations pertaining to Micro Insurance

3. To analyses the progress made so far by Micro Insurance in India III. RESEARCH METHODOLOGY

Analysis is done using secondary resources collected from the authentic sources and regulatory bodies such as IRDA. The scope of study is limited to growth in micro insurance sector post liberalization and is mainly in context of India.

IV. REVIEW OF LITERATURE

The present study embodies a brief review of the research done in the area of micro insurance. The purpose of reviewing the earlier studies is to economize the historical and present prospective of the present work and the related studies which have been taken cognizance of one or more variables includes in the study.

Kirti Singh, Vijay Kumar Gangal (2015), Micro Insurance is a Vehicle for Economic Development by alleviating Poverty and Vulnerability and Micro-insurance increases and has increased the chances of economic growth for poor (Apostolakis, 2015).

Ratna Kishore (2013) in his article “Micro Insurance in India – Protecting the Poor” has pointed out that the market for micro-insurance in India is enormous and remains untapped. The potential market size for micro insurance in India is estimated to be between Rs.62, 000 and Rs.84, 000 million. He has given a micro insurance business model for the existing insurers. He explains micro insurance as social security cover for the poor and brought out the problems and challenges in micro insurance.

Syed Abdul Hamid & Roberts & Paul Mosley (2010)1 in the study shows that there is a positive impact of micro health insurance in the reduction of poverty among rural households of Bangladesh. Micro health insurance has a significant beneficial effect on food sufficiency of poor’s and has a dynamic improvement in the health status of poor rural households.

Ito and Kono (2010) observed that there are common problems associated with micro insurance (1) low take-up rates, (2) high claim rates, and (3) low renewal rates. This is explained on the basis of prospect

theory, hyperbolic preference, and adverse selection. The prospects theory makes an assumption that people are risk averse while evaluating gains and they become risk loving when it comes to loss.

Venkata Ramana Rao (2008), the study reveals that micro insurance is not an opportunity but a responsibility and to serve this responsibility good awareness campaign is needed. Micro insurance is offering real solutions to the billions of rural poor that raises the awareness of micro insurance as a key issue in coming future.

V. MICRO- INSURANCE MARKET IN INDIA

Insurance Regulatory and Development Authority (IRDA) has created a special category of insurance policies called micro-insurance policies to promote insurance coverage among economically vulnerable sections of society. The IRDA Micro-insurance Regulations, 2005 defines and enables micro-insurance.

A MICRO-INSURANCE POLICY IS

A general or life insurance policy with a sum assured of Rs 50,000 or less A GENERAL MICRO-INSURANCE PRODUCT IS ANY

Health insurance contract

Any contract covering belongings such as

Hut, Livestock, Tools or instruments or Any personal accident contract

They can be on an individual or group basis A LIFE MICRO-INSURANCE PRODUCT IS

A term insurance contract with or without return of premium

Any endowment insurance contract or

A health insurance contract

They can be with or without an accident benefit rider and

Either on an individual or group basis

There is flexibility in the regulations for insurers to offer composite covers or package products that include life and general insurance covers together

INTERMEDIARIES

Micro- insurance business is done through the following intermediaries:

Non-Government Organizations : A Non-Government Organization (NGO) shall be a registered non- profit organization under the Society’s Act, 1968

Self-Help Groups: Self Help Group (SHG) may be an informal group or registered under Societies Act, State Co-operative Act or as a partnership firm

Micro-Finance Institutions

MICRO-INSURANCE DELIVERY MODELS

One of the greatest challenges for micro-insurance is the actual delivery to clients. Methods and models for doing so vary depending on the organization, institution, and provider involved. In general, there are four main methods for offering micro-insurance the partner-agent model, the provider-driven model, the full-service model, and the community-based model. Each of these models has their own advantages and disadvantages.

A. Partner agent model: A partnership is formed between the micro-insurance scheme and an agent (insurance company, microfinance institution, donor, etc.), and in some cases a third-party healthcare provider. The micro-insurance scheme is responsible for the delivery and marketing of products to the clients, while the agent retains all responsibility for design and development. In this model, micro- insurance schemes benefit from limited risk, but are also disadvantaged in their limited control.

B. Full service model: The micro-insurance scheme is in charge of everything; both the design and delivery of products to the clients, working with external healthcare providers to provide the services.

This model has the advantage of offering micro-insurance schemes full control, yet the disadvantage of higher risks.

C. Provider-driven model: The healthcare provider is the micro-insurance scheme, and similar to the full-service model, is responsible for all operations, delivery, design, and service. There is an advantage once more in the amount of control retained, yet disadvantage in the limitations on products and services.

D. Community-based/mutual model: The policyholders or clients are in charge, managing and owning the operations, and working with external healthcare providers to offer services. This model is advantageous for its ability to design and market products more easily and effectively, yet is disadvantaged by its small size and scope of operation.

MICRO-INSURANCE PRODUCTS IN INDIA

As on 1st July 2015, there are 17 companies offering micro insurance products in 26 categories. Broadly micro insurance products are classified into two categories discussed below:

A. GENERAL MICRO-INSURANCE PRODUCT

A “general micro-insurance product” means any health insurance contract, any contract covering the belongings such as hut, livestock, any personal accident contract, or tools or instruments, either on individual or group basis, as per terms

B. LIFE MICRO-INSURANCE PRODUCT

A “life micro-insurance product” means any term insurance contract with or without return of premium, any endowment insurance contract or health insurance contract, with or without an accident benefit rider, either on individual or group basis, as per terms stated.

Below is the list of micro insurance products along with the name of companies:

Micro insurance Product list Updated list as on 1st July, 2015

Product list updated as on 1st July, 2015 Financial

Year Name of Insurer Name of the Product Product UIN

In operation from

(opening date*) 2014-15 AVIVA Life Ins. Co. India Pvt. Ltd.

Aviva Nayi Grameen Suraksha-Micro Insurance Product

122N108V01 20-Mar-15 2013-14 AVIVA Life Ins. Co. India Pvt. Ltd. Credit Plus 122N009V02 15-May-13 2013-14 Bharti AXA Life Insurance Co. Ltd. Bharti AXA Life Jan Suraksha 130N040V02 16-Jul-13 2001-02 Birla Sun Life Insurance Co. Ltd. BSLI Bima Kavach Yojana 109N005V01 21-Sep-01 2007-08 Birla Sun Life Insurance Co. Ltd. BSLI Bima Suraksha Super 109N032V01 13-Aug-07 2007-08 Birla Sun Life Insurance Co. Ltd. BSLI Bima Dhan Sanchay 109N033V01 13-Aug-07 2013-14 Birla Sun Life Insurance Co. Ltd. BSLI Grameena Jeevan Raksha

Plan 109N086V01 21-May-13

2013-14

Canara HSBC Oriental Bank of Commerce Life Insurance Company Ltd.

Canara HSBC-Sampoorna

Kavach Plan 136N022V02 27-Jun-13

2013-14 DHFL Pramerica Life Insurance

Co. Ltd DHFL Pramerica Sarv Suraksha 140N007V02 28-Jun-13 2013-14 Edelweiss Tokio Life Insurance

Co. Ltd

Edelweiss Tokio Life - Raksha

Kavach (Micro Insurance Plan) 147N012V02 20-Sep-13 2013-14 Edelweiss Tokio Life Insurance

Co. Ltd

Edelweiss Tokio Life - Dhan

Nivesh Bima Yojana 147N013V02 20-Sep -13 2013-14 HDFC Standard Life Insurance Co.

Ltd.

HDFC SL Sarvgrameen Bachat

Yojana 101N069V02 3-Jul-13

2013-14 ICICI Prudential Life Insurance

Co. Ltd. ICICI Pru Sarv Jana Suraksha 105N081V02 11-Sep-13 2013-14 ICICI Prudential Life Insurance

Co. Ltd. ICICI Pru Anmol Bachat 105N139V01 11-Dec-13

2013-14 IDBI Federal Life Insurance Co.

Ltd.

IDBI Federal Group

Microsurance Plan 135N004V02 29-Jul-13 2014-15 IDBI Federal Life Insurance Co.

Ltd

IDBI Federal Termsurance Sampoorn Surksha Micro Insurance Plan

135N037V01 31-Oct-14

2014-15 Kotak Mahindra OM Life Insurance Ltd.

Kotak Sampoorn Bima Micro-

Insurance Plan 107N092V01 2-Mar-15 2013-14 PNB MetLife India Insurance Co.

Ltd. Met Grameen Ashray 117N063V02 28-Jan-14

2013-14 Sahara India Life Insurance Co.

Ltd.

Sahara Surakshit Pariwar

Jeevan Bima 127N032V01 14-Mar-14

2013-14 SBI Life Insurance Co. Ltd. SBI Life Grameen Shakti 111N038V02 29-Jul-13 2013-14 SBI Life Insurance Co. Ltd. SBI Life Grameen Super

Suraksha 111N039V02 17-Jul-13

2012-13 SBI Life Insurance Co. Ltd. SBI Life Grameen Bima 111N087V01 27-Nov-12 2006-07 Shriram Life Insurance Co. Ltd. Shri Sahay 128N011V01 7-Feb-07 2014-15 TATA AIA Life Insurance Co. Ltd.

TATA AIA Life Insurance Navkalyan Yojna - Micro Insurance Product

110N115V01 20-Nov-14

2013-14 Life Insurance Corporation of

India LIC's New Jeevan Mangal 512N287V01 2-Jan-14

2014-15 Life Insurance Corporation of

India LIC's Bhagya Lakshmi 512N292V01 21-Oct-14

Source: www. irdai.gov.in VI. REGULATIONS PERTAINING TO MICRO – INSURANCE

MICRO INSURANCE REGULATIONS IN INDIA

Some of the measures taken by Insurance Regulatory development of India (IRDA) along with government are as:-

Mandate: ‘Rural areas and the social sector’ obligations for the private insurance industry

During the nationalized insurance phase approximate 48% of LIC‟s customers were from rural and semi-urban areas. After liberalization, the industry regulator was concerned about inclusive insurance growth and rural exposure for insurance companies. IRDA, therefore, mandated the insurance companies through rural and social sector obligation 2002 to safeguard certain percentage of polices to be sold in rural areas and certain number of lives are covered in the social sector.

Permitting self-help groups (SHGs), NGOs, and MFIs as new micro insurance delivery channels.

Entering into various Private Public Partnerships (PPP) agreements between the Indian government and the insurance Companies.

MICRO INSURANCE REGULATIONS, 2005

Micro Insurance Regulations 2005 clearly conveys the clarity on:

Product guidelines for Distribution, Design and Issuance of policy contracts

Guidelines for Agents Appointment, Remuneration, Code of conduct, Capacity Building etc.

Guidelines for Life & non -life tie-ups: A life insurer may offer general micro insurance products &

vice versa

Mandate on covering Rural and Social sectors CHANGES IN MICRO INSURANCE REGULATIONS (2015) The main highlights are:

Capacity building exercises are expanded by introducing additional 25 hours of training for micro agents licensed to distribute general insurance MSME policies with mandatory refresher training in every three years.

Appointment of Micro agents is expanded through tie ups with AIC and other health insurers are also permitted now.

Minimum 5 people from earlier cap of 20 is allowed for group policies

Definition of micro-agents is expanded with inclusion of Regional Rural banks, Primary agricultural and other co-operative Societies, Bank correspondents of scheduled commercial banks etc.

Rural and Social Sector Obligation: Life Insurers are required to cover a certain % of the total number of policies in rural areas and to insure a given number of lives in the social sector.

VII. RESEARCH ANALYSIS

The social security lies in: Who pays the premium: Govt. or Subscriber? Who underwrites the risk: Govt.

or Insurer? Based on this classification, the model of India predicting the differences between commercial/ conventional insurance and social insurance is as follows:

Figure 1: Differences between commercial/ conventional insurance and social insurance Some of Government sponsored micro insurance schemes are as follows:

WEATHER BASED CROP INSURANCE SCHEME (WBCIS) Some of the key features of WBCIS are:

Was launched initially by the private sector but gradually is adopted by the State and was subsidized in 2007.

In 2009-2010, private sector firms were allowed to compete with the public insurer Agriculture Insurance Company of India (AIC) to offer subsidized WBCIS products at a state level.

In 2015-16, the Weather-based Crop Insurance Scheme (WBCIS) is being implemented as component of National Crop Insurance Programme (NCIP).

As on May 2015, 34,136,419 farmers were covered and 46 million hectares insured RASHTRIYA SWASTHYA BIMA YOJANA (NATIONAL HEALTH INSURANCE SCHEME) The key points of this scheme are:

The scheme started enrolling on April 1, 2008 and has been implemented in 25 states of India. A total of 36 million families have been enrolled as of February 2014.

Implemented by different insurers in different districts

Governments can shift contracts between commercial insurers and thus, competition allows the government to drive the programme at low cost.

As of 19th October, 2015, around 50% of BPL Population is covered.

Social Security Schemes

• Risk is insured by the Government

• like Mahatma Gandhi National Rural

Employment Guarantee Act

Social Insurance Schemes

• Insurer is the Underwriter and Government Subsidises the premium

• like Aam Admi Bima Yojna

Micro Insurance

• Entire

Contribution is by Insurer with

limited direct subsidy

• Like Pradhan

Mantri Suraksha

Bima Yojna

PRADHAN MANTRI JAN DHAN YOJANA (PMJDY)

PMJDY is India's National Mission for Financial Inclusion to ensure access to financial services, namely Banking Savings & Deposit Accounts, Remittance, Credit, Insurance, and Pension in an affordable manner. This financial inclusion campaign was launched by the Prime Minister of India Narendra Modi on 28 August 2014. By 19 April 2017, over 28 crore (283 million) bank accounts were opened and almost 639 billion (US$10 billion) were deposited under the scheme.

Pradhan Mantri Jan - Dhan Yojana (Statistics as on 19 April 2017) (All Figures in Crores)

S.

N o

No Of Accounts No Of

RuPay Debit Cards

Aadhaar Seeded

Balance In Beneficiary Accounts

% of Zero Balance Accounts Rural Urban Total

1

Public Sector Banks

12.45 10.36 22.80 17.76 14.45 49, 999.02 24.86

2

Regional Rural Banks

3.97 0.69 4.65 3.53 2.89 11, 853.55 21.13

3 Private

Banks 0.56 0.37 0.93 0.86 0.45 2, 107.60 36.54

Total 16.97 11.41 28.38 22.15 18.79 63, 960.17 crore

(US$9.9 billion) 24.63 Table 1: Pradhan Mantri Jan - Dhan Yojana (Statistics as on 19 April 2017)

The scheme has been started with a target to provide 'universal and clear access to banking facilities' starting with "Basic Banking Accounts" with overdraft facility of Rs. 5,000 (US$74) after six months and RuPay Debit card with inbuilt accident insurance cover of Rs. 1 lakh (US$1,500) and RuPay Kisan Card.

Figure 2: PMJDY and its associated Yojana A. PRADHAN MANTRI SURAKSHA BIMA YOJANA (PMSBY)

Pradhan Mantri Suraksha Bima Yojana is available to people between 18 and 70 years of age with bank accounts. It was formally launched by Prime Minister Narendra Modi on 9 May 2015 in Kolkata. As of May 2015, only 20% of India's population has any kind of insurance, this scheme aims to increase the number.

It has an annual premium of Rs. 12 (18¢ US) excluding service tax, which is about 14% of the premium.

The amount will be automatically debited from the account. In case of accidental death or full disability, the payment to the nominee will be Rs. 2 lakh (US$3,000) and in case of partial Permanent disability Rs.

1 lakh (US$1,500). Full disability has been defined as loss of use in eyes, hands or feet. Partial Permanent disability has been defined as loss of use in one eye, hand or foot. This scheme will be linked to the bank accounts opened under the Pradhan Mantri Jan Dhan Yojana scheme.

As of 24th April 2017, 10 crore people have already enrolled for this scheme. 9,705 claims have been disbursed against 12,975 claims received. In April 2017, Haryana Government has announced that all Haryana residents in the age group of 18-70 years will be covered by PMSBY, wherein the state government would reimburse the premium to the beneficiary.

B. PRADHAN MANTRI JEEVAN JYOTI BIMA YOJANA (PMJJBY)

Pradhan Mantri Jeevan Jyoti Bima Yojana is a government-backed Life insurance scheme in India. It was originally mentioned in the 2015 Budget speech by Finance Minister Arun Jaitley in February 2015. It

Pradhan Mantri Suraksha Bima Yojana

-banking & financial inclusion

Atal Pension Yojana -Retirement Plan PMJDY

-Social Security through Financial inclusion Pradhan Mantri Jeevan

Jyoti Bima Yojana

-life insurance

was formally launched by Prime Minister Narendra Modi on 9 May in Kolkata. As of May 2015, only 20%

of India's population has any kind of insurance, this scheme aims to increase the number

Pradhan Mantri Jeevan Jyoti Bima Yojana is available to people between 18 and 50 years of age with bank accounts. It has an annual premium of Rs. 330 (US$4.90). The Service tax is exempted on Pradhan Mantri Jeevan Jyoti Bima Yojana. The amount will be automatically debited from the account. In case of death due to any cause, the payment to the nominee will be Rs. 2 lakh (US$3,000). This scheme will be linked to the bank accounts opened under the Pradhan Mantri Jan Dhan Yojana scheme.

As of 24 April 2017, 3.11 crore people have already enrolled for this scheme. 60,422 claims have been disbursed against 63,767 claims received.

C. ATAL PENSION YOJNA (APY)

Atal Pension Yojana is a government-backed pension scheme in India targeted at the unorganized sector. Originally mentioned in the 2015 Budget speech, it was formally launched by Prime Minister Narendra Modi on 9 May in Kolkata. As of May 2015, only 11% of India's population has any kind of pension scheme, this scheme aims to increase the number.

BACKGROUND OF APY: NEW UNIVERSAL PENSION SCHEME

The new pension scheme can be analyses better with the help of following chart:

Figure 3: Emergence of Atal Pension Yojana National Pension

Scheme (NPS)

• Introduced in 2004 for new entrants to Central Government service, except for the Armed Forces

• NPS was then opened to all citizens from 1st May, 2009 on a voluntary basis

NPS Swavalamb an (NPS-S) launched in 2010

• Voluntary pillar of NPS was extended to cover the unorganised sector

• Temporary subsidy provided when member contributes towards NPS-S

Atal Pension Yojana (APY) launched in 2015

• Successor of NPS Swavalamban

• The older a subscriber, the lower the guaranteed rate of return

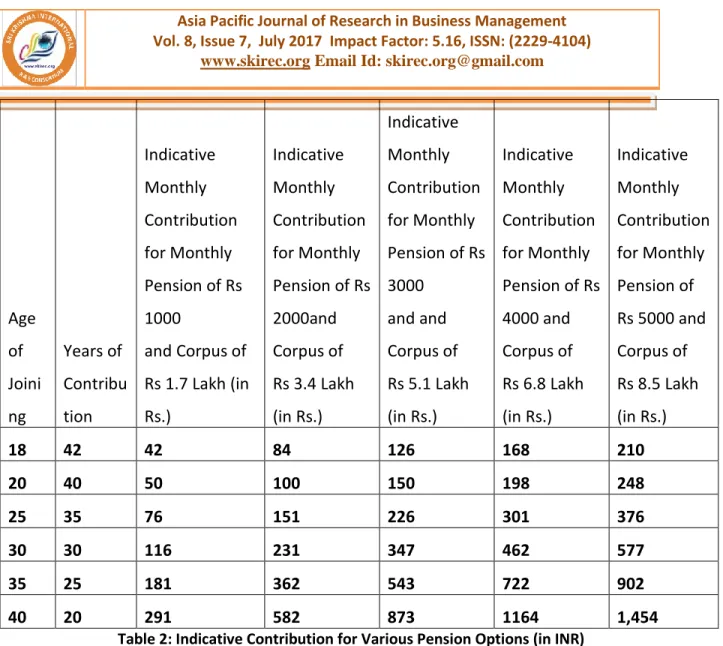

Table 2: Indicative Contribution for Various Pension Options (in INR)

Status of the above mentioned schemes based on Enrolment under APY, PMJJBY and PMSBY as on March 21, 2016 is as:

Scheme Name

Rural Male

Rural Female

Urban Male

Urban Female

Grand Total APY 7,07,475 3,77,295 7,13,172 4,52,727 22,50,669

PMJJBY 91,34,052 56,49,707 94,17,101 53,33,187 295,34,047

PMSBY 296,02,859 199,01,811 280,92,347 163,68,331 939,65,348 Grand

Total

394,44,386 259,28,813 382,22,620 221,54,245 1257,50,064

Age

of Joini ng

Years of Contribu tion

Indicative Monthly Contribution for Monthly Pension of Rs 1000

and Corpus of Rs 1.7 Lakh (in Rs.)

Indicative Monthly Contribution for Monthly Pension of Rs 2000and Corpus of Rs 3.4 Lakh (in Rs.)

Indicative Monthly Contribution for Monthly Pension of Rs 3000

and and Corpus of Rs 5.1 Lakh (in Rs.)

Indicative Monthly Contribution for Monthly Pension of Rs 4000 and Corpus of Rs 6.8 Lakh (in Rs.)

Indicative Monthly Contribution for Monthly Pension of Rs 5000 and Corpus of Rs 8.5 Lakh (in Rs.)

18 42 42 84 126 168 210

20 40 50 100 150 198 248

25 35 76 151 226 301 376

30 30 116 231 347 462 577

35 25 181 362 543 722 902

40 20 291 582 873 1164 1,454

Table 3: Enrolment status under APY, PMJJBY and PMSBY as on March 21, 2016 VIII. SWOT ANALYSIS OF MICRO-INSURANCE SCHEMES

STRENGTHS

1. Elimination of fake claims: false and exaggerated claims put a pressure on the profitability of insurance companies. SHGs are small and close knit formal groups of individuals living in close vicinity and are known to each other. It helps in eliminating the chances of false and exaggerated claims.

2. High Speed Claim Settlement: Since all members of SHGs are known to each other, the complexity of investigation about genuine claims is pretty less. This enables the SHGs for speedy claim settlement.

3. Affordability: Small installments of premium amounts are affordable for the members of SHGs who live below poverty line.

4. Reach: it gives a great outreach for micro insurance products.

WEAKNESSES

1. Small corpus: Due to small amount of premiums, the corpus money collected does not have a large pool of funds prevent them from scaling up.

2. Designing Micro: Designing insurance products that suits to the individual needs and requirement is a difficult task.

OPPORTUNITIES

1. Government Support: The Government of India has supported Micro Insurance. Any innovative scheme is likely to be encouraged.

2. Market Potential: The large number of population qualifies as consumer of these products. It offers huge business opportunities for the organizations operating in this area.

3. Lack of Competition: Many insurance companies are reluctant to enter into this market; providing wider space for existing players.

THREATS

1. New Entrants: As the insurance sector is being liberalized, so there is a threat of new entrants.

2. Lack of Professionals: Many a times NGOs lack specialized professionals to run these types of schemes.

IX. SUGGESTIONS

Innovations are required at all stages for products, in pricing policy and in delivery channels

Success of marketing micro insurance depends on understanding the social and cultural needs of the target population

Integrating micro finance activities with micro insurance for a most beneficial outcome.

Claim settlement to be timely, simple and transparent.

Simplification of products and bundling where requires making them easy to understand, easy to use, sill and service.

Simplifying and making premium payment plans flexible to suit the needs.

Focus on volumes by targeting large groups.X. CONCLUSION

Micro insurance in India can be compared to a glass of water either half empty or half full. If one is optimistic, there is a huge scope for developing the segment in the country. Small firms should make a compulsory contribution from the employer to actively take and participate in an insurance cover. The real problem lies with the corporate because they are still not ready to give importance to the rural market. There is a need of well laid out strategy to target rural market at corporate level. Many NGOs and MFIs are already doing commendable work for betterment of the deprived people in villages. They can be recognized as agents and their infrastructure can be used by insurance companies governed by IRDA. Many companies—through their trusts and CSR activities—are extending their support for betterment of villagers.

Even some banks through their rural branches are selling micro insurance products. State governments are also coming out with various schemes to improve the earnings and protect the poor from natural calamities. The extensive expansion of pioneering micro insurance product holds much significance in outreaching the concept of micro insurance to the grass root level.

If micro insurance schemes are rightly implemented, it could bring sea change in the living standard of rural population living below poverty line. The customization of products could better suit to the need and requirement of individual customers and hence could favorably impact the demand for micro- insurance products.

REFRENCES

Kirti Singh, Vijay Kumar Gangal (2015), Micro Insurance in India: A Gizmo to Vehicle Economic Development & Alleviate Poverty and Vulnerability, IOSR Journal of Economics and Finance, Volume 6, Issue 2. Ver. I (Mar.-Apr. 2015), PP 14-20.

N. Ratna Kishor, “Micro Insurance in India-Protecting the Poor”, Journal of Business Management and Social Sciences Research, Vol.2, No.3, March 2013, pp.39-44.

Syed Abdul Hamid, Jennifer Roberts & Paul Mosley (2010), Can micro health insurance reduce poverty:

Evidence from Bangladesh. Sheffield economic research paper series no. 2010001

Ito Seiro and Kono Hisaki (2010), “Why Is the Take-Up of Micro insurance So Low? Evidence from a Health Insurance Scheme in India”, the Developing Economies, Vol. 48, No. 1, pp. 74–101

Venkata Ramana Rao “Life insurance awareness in rural India: Micro insurance lessons to learn and teach” Bimaquest- Volume VIII issue I, 2008

https://www.irdai.gov.in/ADMINCMS/cms/NormalData_Layout.aspx?page=PageNo271&mid=26.2 http://www.policyholder.gov.in/economically_vulnerable.aspx