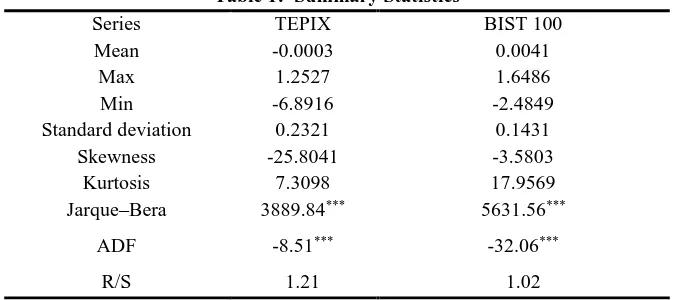

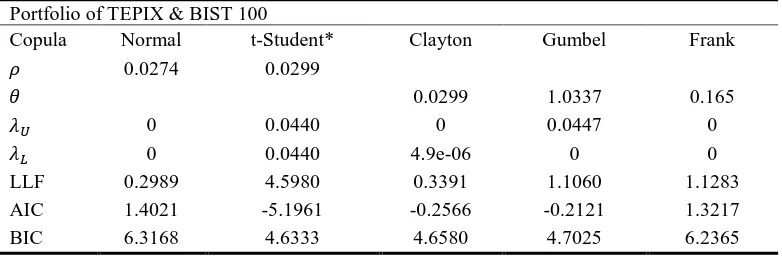

GJR-Copula-CVaR Model for Portfolio Optimization: Evidence for Emerging Stock Markets

Full text

Figure

Related documents

AIDS Healthcare Foundation CONTACTS FOR ADMINISTRATION: Medical Case Management (MCM) Address for Agency's Headquarters (HQ): Official Contact for Programmatic, Day-to-Day and

It provides a summary or snapshot of important health and wellbeing issues for same/both-sex attracted young people from Youth’12: The National Health and Wellbeing Survey of New

Simultaneous perturbation stochastic approximation (SPSA) (Spall,1987) as a simple yet powerful search technique is used to drive the dominant particles to approach to the

A comprehensive technical and tecno-economic feasibility and environmental impact assessment framework is used to illustrate that this approach for supplying renewable

Therefore, specifically aims, are as follows ( 1) to construct a hypothetical model for enhancing effective change management in universities, (2) to verify the model for

2012 School of Art Institute Chicago, Fashion Scholarships, Chicago Carl Sandburg High School Student Art Show, Chicago 2011 School of Art Institute Chicago,

Our algorithm is based on DBSCAN [EKSX 96], [SEKX 98] which is an efficient clustering al- gorithm for metric databases (that is, databases with a dis- tance function for pairs

Muhasebe Meslek Mensuplarının Sundukları Hizmetin Müşteri Tarafından İlişkisel Pazarlama Anlayışı Doğrultusunda.. Değerlendirilmesine Yönelik Ampirik