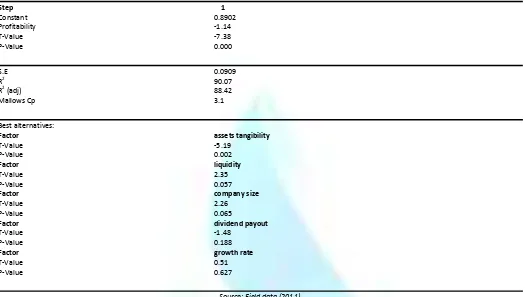

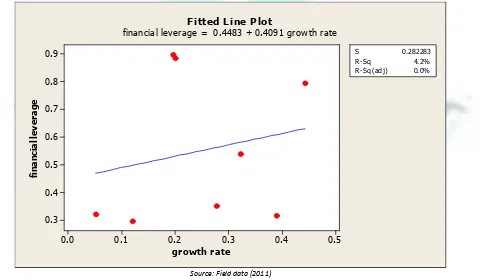

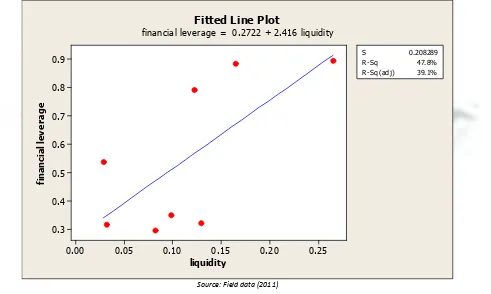

DETERMINANTS OF CAPITAL STRUCTURE: EVIDENCE FROM TANZANIA’S LISTED NON FINANCIAL COMPANIES

Full text

Figure

Related documents

In this paper, we study the Differentially Private Empirical Risk Minimization (DP-ERM) problem with non-convex loss functions and give several upper bounds for the utility in

Although man- datory disclosure obviously is superior to voluntary disclosure given the in- formation about product risks that firms have — since such information is valuable

However, since datagrams can be corrupted, discarded or duplicated, we need to define Send so that each datagram in the final state is derived from either the datagram being sent

Composite reliability coefficients and internal consistency values along with test-retest values computed for the reliability showed that the GBS was a reliable

Utilizing the rice straw in a solid-state fermentation process using Pleurotussajor-caju , laccase was produced and subjected to isolation and purification processes. The

If this product contains ingredients with exposure limits, personal, workplace atmosphere or biological monitoring may be required to determine the effectiveness of the ventilation

You can configure each port on a switch to be in a specific VLAN (access port) by using the interface switchport command.. You can also configure multiple ports at the same time

"Teaching Professionalism in the Law School Classroom"; Association of American Law Schools Annual Meeting, Section on Legal Research and Writing, Washington, D.C., January 4,