The Cash Paradox

∗

Janet Hua Jiang

†Bank of Canada

Enchuan Shao

‡University of Saskatchewan

March 15, 2019

Abstract

In many industrialized countries, cash usage at points of sale has been decreasing ow-ing to competition from alternative means of payment such as credit cards. At the same time, cash demand, measured as currency in circulation over GDP, fell only in earlier years but has remained surprisingly robust in the past two to three decades. This phe-nomenon, termed the “cash paradox,” poses a challenge to standard monetary models. We introduce two new features into the standard cash-credit model: the substitutability between cash and credit (as a stand-in for alternative means of payments) is uneven across different economic activities, and some agents actively manage cash flows across these activities. Calibration exercises show that the cash-flow channel is important for quan-titatively capturing the diverging trends in cash usage and demand. There is also some empirical support for our model’s prediction on cash velocity in the retail sector.

JEL codes: E41, E51

Keywords: Demand for Cash, Credit, Velocity, Cash Management

∗For their comments and discussions, we would like to thank the anonymous referee, the Associate Editor,

the Editor, Jonathan Chiu, Ben Fung, Pedro Gomis-Porqueras, Scott Hendry, Miguel Molico, Hector Perez-Saiz, Lukasz Pomorski, Francisco Rivadeneyra, Gerald Stuber, Liang Wang, Russell Wong, and Randall Wright, as well as participants at the African Search and Match Workshop in Marrakesh, the Spring 2014 Midwest Macro Meeting, the 2014 Chicago Fed Summer Workshop, the 2015 Econometric Society World Congress in Montreal, and seminars at the Bank of Canada, the University of Hawaii, the University of Iowa, the University of Saskatchewan, and the University of Windsor. The views expressed in the paper are those of the authors. No responsibility for them should be attributed to the Bank of Canada.

1

Introduction

The retail payment landscape has undergone significant changes in the past few decades with

the emergence of various new payment instruments. As a result, cash has been losing ground

to other means of payment at the point of sale. These developments can potentially impact

the demand for government currency. Given that currency in circulation (CIC) constitutes a

significant share of the balance sheet of a central bank, the shrinking demand for currency

will have critical implications on the central bank’s seigniorage revenue, its independence,

and its ability to conduct monetary policy (see Friedman, 1999; King, 1999; Freedman, 2000;

and Fung et al., 2014).1 It is therefore important to monitor and understand the trend in the

demand for cash.

Given that standard monetary models predict that cash usage and demand tend to move

in the same direction, one would naturally expect the demand for cash to decrease as it is

squeezed out by other payment methods at points of sale. However, surprisingly, the demand

for cash, measured as the value of CIC over GDP, after a steady decrease in earlier years, has

remained flat or even increased in the past two to three decades despite continuous declines

in cash usage; this phenomenon has been observed in various industrialized economies (see

Section 2 for more detailed documentation). Rogoff (2002) wonders at the surprising

popu-larity of paper currency in many industrialized economies. Bailey (2009) calls it the “paradox

of banknotes.” Williams (2012) terms this phenomenon of decreasing cash usage and robust

cash demand the “cash paradox.”2

1For example, CIC consisted of 93% of the Federal Reserve’s liabilities in 2007 just before the financial crisis. As a result of large-scale unconventional monetary policies such as quantitative easing, the share of CIC has decreased substantially since the financial crisis. However, CIC still consists of a significant share of the Federal Reserve’s balance sheet. As of the end of 2018, the share was 40%.

In this paper, we document the cash paradox and develop a parsimonious model that is

consistent with the phenomenon. To account for the cash paradox, we introduce two

inno-vations to standard cash-credit monetary models (where credit is a stand-in for alternative

payment methods to cash). The first innovation is that the substitutability between cash and

credit is uneven across different economic activities. Credit directly competes with cash in

many point-of-sale transactions. However, credit is a less-ideal substitute for cash as a store of

value and transactions in the underground economy, in bars and casinos, or in activities where

record-keeping or monitoring technology is not available, where agents desire anonymity, or

where unbanked or underbanked agents are involved. To capture the variation of

substitutabil-ity between cash and credit across different activities, we model a economy with two sectors:

a cash-credit sector and a cash-only sector. The cash-credit sector captures activities where

cash and credit are perfect substitutes for each other as a means of payment. The cash-only

sector captures activities where it is difficult or impossible for credit to replace cash.

The second innovation is the modelling of cash flows across different sectors. In our

model, some agents actively plan their cash inflows and outflows, receiving cash revenues

(in-flows) in the cash-credit sector to finance spending (out(in-flows) in the cash-only sector. Some

examples of these activities are taxi drivers acquiring cash from passengers to dine in

cash-only restaurants, bakeries receiving cash from customers to purchase ingredients at local

farm-ers’ markets, farmers selling produce in cash to pay unbanked temporary workers, firms using

cash revenues to pay suppliers, and all of them retaining some cash revenues as a store of

value.

With these two innovations, our model predicts that higher credit usage initially reduces

both the share of cash transactions and cash demand. However, once credit usage expands

beyond a certain level, the tight connection between cash usage and demand breaks down.

More specifically, agents adjust their cash management practices in response to further credit

expansions, so that the velocity of cash slows down and the demand for cash remains flat

despite further diminishing cash transactions. The intuition is as follows. With more credit

usage in the cash-credit sector, agents who are buyers in that sector lower their cash demand.

This change implies that agents who are sellers in the cash-credit sector will receive fewer

cash revenues or inflows. To finance their purchases or outflows in the cash-only sector, these

agents acquire more cash in advance to make up for the shortfall in cash receipts. The decrease

in cash demand by the first group of agents is offset by the increasing demand by the second

group, so that the total demand for cash remains flat despite shrinking cash transactions. As

for velocity, note that compared with cash acquired by the first group of agents, which is used

in both sectors, cash acquired by the second group of agents has a lower velocity because it

is used only in the cash-only sector. As credit usage expands, there is a redistribution of cash

demand from the first group of agents to the second group, implying that cash with a lower

velocity constitutes a higher fraction of the total demand for cash. As a result, the overall

velocity of cash decreases.

The decoupling of cash usage and demand in response to credit expansions enables our

model to capture the cash paradox successfully. In particular, the simultaneous decrease in

cash usage and robust cash demand in many industrialized countries can be explained as a

result of credit expansions together with falling nominal interest rates.

To quantify the importance of our new two modelling features in capturing the cash

para-dox, we carry out a series of calibration exercises. More specifically, we calibrate our model

and alternative models where these features are absent, to cash usage and demand in four

ad-vanced economies: Australia, Canada, the United Kingdom and the United States. We find

that both modelling features are important in capturing the cash paradox. The standard

mon-etary model, where both features are absent, cannot explain the robust cash demand. The

size of the cash-credit sector relative to the cash-only sector. In contrast, the model with the

cash-flow channel captures the trend in cash usage and demand well in all four countries with

much more reasonable parameterization. We also find some empirical support for our model’s

prediction on the cash velocity in the retail sector.

Our paper contributes to the literature on the cash paradox by developing the first

for-mal model to capture the phenomenon with plausible quantitative results. Our quantitative

exercises also formalize and deepen the popular indicative discussion that attributes the

para-doxical robust demand for cash in the face of credit expansion to increased demand in the

underground economy and/or as a store of value by either domestic or foreign agents, as these

demand categories are less sensitive to competition from other means of payment.3 We

be-lieve that this is an important first step to explain the cash paradox. The cash-only sector in

our model captures these demand categories as economic activities where it is difficult for

credit to replace cash (and our model predicts that cash is increasingly used for activities in

that sector). The next and more challenging step is to identify the forces that can plausibly

counteract the fall in cash demand driven by competition from other means of payment.

The increasing demand in less credit-sensitive activities can result from (1) structural

changes, which cause the money demand curve to shift, and/or (2) decreasing nominal interest

rates, represented by movement along the money demand curve. We think it is unlikely that

structural changes could (fully) account for the cash paradox. In general, there is no evidence

that the underground economy has experienced significant growth. According to Schneider

and Buehn (2012), from 1999 to 2010, the shadow economy as a percentage of GDP shrunk

slightly in 39 OECD countries. Another potential source of structural changes is increased

per-ceived uncertainty and distrust in the financial system, which induce agents to hold more cash

for precautionary motives or as a store of value (see, for example, Williams, 2012; Berentsen

and Schar, 2018). However, in many countries, the cash paradox phenomenon was observed

long before the financial crisis, with the CIC/GDP starting to level off or increase since the

1980s or 1990s. The financial crisis raised perceived uncertainty and distrust in the

finan-cial system and spurred the particularly strong cash demand afterward. Because of that, the

cash paradox phenomenon has drawn more attention following the crisis. However, we think

increased uncertainty and distrust in the financial system are unlikely to be the main force

be-hind the robust cash demand before the financial crisis. Foreign demand could be an important

factor for major international reserve currencies, such as the US dollar or euro. It is, however,

less applicable to other currencies. Given the ubiquity of the cash paradox, country-specific

factors, such as strong foreign demand, are unlikely to fully account for the phenomenon.

The critical question is then whether the fall in the interest rate can plausibly generate

a robust demand for cash as a store of value or in the underground economy to sufficiently

counteract the shrinking (transnational) demand for cash due to expanding credit usage. Our

calibration exercises suggest that the answer is “very unlikely” without additional channels

such as the cash-flow channel proposed in our paper, unless one is willing to make extreme

assumptions about the relative size of the cash-credit sector to the cash-only sector (the former

is less than 1/10,000 of the latter). The cash-flow channel that we emphasize strengthens the

role of the falling interest rate relative to credit expansion, and helps to capture the paradoxical

behavior of cash demand with much more plausible model parameterization.

Our model also closely relates to works that study credit in monetary economies within

the framework developed by Lagos and Wright (2005) and Rocheteau and Wright (2005).

Gu et al. (2016) and Araugo and Hu (2017) discuss the essentiality of credit in a monetary

economy. Berentsen et al. (2007), Rojas Breu (2013), Berentsen et al. (2014), and Chiu et al.

(2010) and Gomis-Porqueras and Sanches (2013) investigate the optimal monetary policy in a

model with money and credit. Bethune et al. (2014) study the relationship between unsecured

consumer credit and unemployment. Lotz and Zhang (2016) and Dong and Huangfu (2017)

model costly credit and examine how monetary policies affect credit adoption. Liu et al.

(2016) analyze the effects of inflation on price dispersion, markups, and welfare.

Our modelling innovation is to introduce cash flows between activities where cash and

credit have different extents of substitutability, and we apply this new model to explain the

paradoxical behavior of cash demand in response to increasing competition from credit usage.

We take a short cut in modelling credit expansion as the increasing fraction of agents having

access to credit (in our Bank of Canada Staff Working Paper version, Jiang and Shao 2014, we

model credit expansion along the intensive margin as increasing credit limits, and the results

are largely the same).4 One could endogenize credit expansion by introducing heterogeneous

preferences and a fixed cost of adopting credit, as in Dong and Huangfu (2017). In this setup,

agents with high marginal utilities tend to use credit. Financial innovations that reduce the

cost of adopting credit will induce more agents to use it. One could also endogenize credit

limits as in Kehoe and Levine (1993), and derive credit expansion along the intensive margin

as higher credit limits resulting from improvements in the monitoring technology to detect

defaults. Endogenizing credit usage would add an interesting interaction between inflation (or

nominal interest rate) and credit adoption or usage. However, given that the data on the cost of

using credit and the monitoring technology are not readily available, in the end, one still needs

to calibrate the cost or monitoring parameter to match observable data on credit adoption or

usage, such as the credit access rate used in our calibration.

Finally, by modelling the cash flows across different sectors where cash and credit have

different substitutability, our model generates a new channel through which credit and the

nominal interest rate affects cash velocity, as apposed to the traditional way of modeling

pre-cautionary demand (as in, for example, Hodrick et al., 1991; Jafarey and Masters, 2003;

Peter-son and Shi, 2004; Lagos and Rocheteau, 2005; Faig and Jerez, 2006; Ennis, 2008 and 2009;

Liu et al., 2011; Nosal 2011; Dong and Jiang, 2014; and Hu et al., 2017).

The rest of the paper is organized as follows. Section 2 documents in more detail the

long-term trend in cash demand and the recent puzzling phenomenon of continued

decreas-ing cash usage and robust cash demand. Section 3 describes the model and characterizes the

equilibrium. Section 4 derives the comparative statics and discusses the effect of credit

ex-pansions and the nominal interest rate on cash usage and demand. In Section 5, we calibrate

three models–the standard single-sector cash-credit model, the segregated two-sector model

where cash and credit have different substitutability across the two sectors, and the full model

where cash flows between the two sectors–to quantify the importance of the modelling

fea-tures. In that section, we also evaluate in detail existing alternative explanations about the cash

paradox and pinpoint the value-added of the cash-flow channel that we emphasize. Section 6

provides empirical support to our model’s predictions on cash velocity. Section 7 concludes.

In the appendices, we provide the proofs, document the data used in our quantitative analysis,

discuss different measures of nominal interest rates, lay out the standard single sector

cash-credit model and the segregated two-sector model for comparison, investigate the possibility

of unregistered economic activities to capture the cash paradox, and discuss model extensions.

2

Documentation of the Cash Paradox

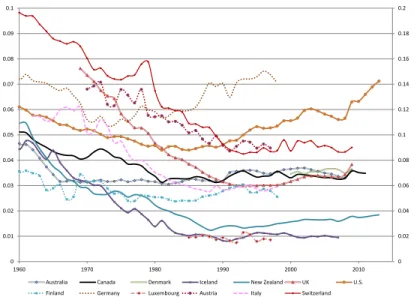

Figure 1 graphs the time series of CIC/GDP ratio for 13 industrialized countries from 1960

and onward: Australia, Canada, Denmark, Iceland, New Zealand, the United Kingdom, the

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2

0 0.01 0.02 0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.1

1960 1970 1980 1990 2000 2010 Australia Canada Denmark Iceland New Zealand UK U.S. Finland Germany Luxembourg Austria Italy Switzerland

Figure 1: Currency in circulation over GDP for selected countries

Notes: (a) Data source: IMF-IFS. (b)The series for Austria, Italy, and Switzerland are plotted against the right y-axis.

Luxembourg, subject to data availability.5 The demand for cash experienced a steady decrease

in earlier years, but the trend has stopped in the last two to three decades, in spite of a continued

decrease in cash usage at points of sales.6

There are in general two approaches to estimating the value of cash transactions. The

first proxies cash usage by cash withdrawals (see, for example, Gerdes et al., 2005) or by the

residual after subtracting non-cash payments from the total point-of-sales or from household

expenditures (see, for example, Humphrey et al., 2004). The second approach directly

cal-culates the share of cash payments from consumer payment survey or retailer scanner data.

Various studies have been conducted to investigate the substitution between cash and other

payment methods in many countries. A common result is that cash has been replaced by other

means of payment (to different extents in different countries).

For example, Arango et al. (2012) find that in Canada from the early 1990s to 2011, the

share of cash transactions at points of sale decreased from 80% to 40% in volume, and from

more than 50% to less than 20% in value. The Bank of Canada conducted two

methods-of-payment surveys, in 2009 and 2013. During the four-year intervening period, the share

of cash payments decreased from 54% to 44% in volume, and from 23% to 22% in value.

In the United States, Humphrey (2004) estimates that from 1980 to 2000, the share of cash

transactions in personal consumption expenditures fell from 33% to 20%. Citing two surveys

of payment method usage at US supermarkets conducted by the Food Marketing Institute,

Humphrey (2004) records that cash accounted for 36% of the value of sales in 1994 but fell

to 29% in 1997 and 17% in 2000. Wang and Wolman (2016) use the scanner data from a

large US discount chain store from April 2010 to March 2013 and find that the fraction of

cash transactions fell at a rate of between 1.3% and 3.3% per year, depending on the size

of transactions. In Australia, the Reserve Bank of Australia (RBA) Payments System Board

Annual Report (2013) shows that from 2004 to 2013, cash usage measured by the value of

cash withdrawals grew much more slowly than household consumption. In addition, RBA

conducted two consumer payment diary studies in 2007 and 2010. According to these studies,

the share of the number and value of cash transactions decreased by 6% and 5%, respectively,

during the three-year span (see Bagnall et al., 2016). In New Zealand, a study by Payments

NZ (2014) shows that cash payments as a percentage of total sales decreased by 10 to 20% in

all social-economic areas in New Zealand from 2006 to 2014.

Similar patterns have been observed in many European countries. Referring to data from

the Payments Council, Bailey (2009) documents that in the United Kingdom, the volume of

cash transactions fell from 87% in 1985 to 60% in 2009. In terms of value, the share decreased

from 9% to 4.2% from 1992 to 2008. In Austria, three payment diary surveys were conducted

in 1996, 2000, and 2005. The data show that in terms of volume, the share of cash payments

decreased from 94.9% in 1996, to 92.9% in 2000, and to 86.1% in 2000. The corresponding

payments accounted for about 80% of total purchases in value, whereas in 2002 the figure

dropped to below 50%. In Italy, Alvarez and Lippi (2009) use the Survey of Household

Income and Wealth to calculate the expenditure share paid with currency. For ATM card

holders, the share decreased from 62% in 1993 to 47% in 2004.7 Snellman et al. (2000) study

the substitution of noncash payment instruments for cash in 10 European countries–Belgium,

Denmark, Finland, France, Germany, Italy, Netherlands, Sweden, Switzerland, and the United

Kingdom–from 1987 to 1996. They find that cash was crowded out in all countries (although

the countries were at different stages of this substitution process).

As its name suggests, the cash paradox poses a challenge to standard monetary models.

Two major factors that affect cash usage and demand is the availability of alternative means

of payment (in this paper, we use credit as a stand-in for these alternatives), and the nominal

interest rate. In standard monetary models, cash usage and demand tend to respond in the

same (negative) direction to changes in credit expansion and the nominal interest rate. In

earlier decades, due to credit expansion and a high nominal interest rate, both cash usage and

cash demand decreased. However, in the past two to three decades, credit continues to expand

but the nominal interest rate starts to drop. The fall in cash transactions means that the effect of

credit expansion dominates, while the rise in cash demand requires the opposite. It is difficult

for standard monetary models to resolve the two conflicted requirements and therefore the

cash paradox.8 In the following sections, we show how we can modify the standard

cash-credit monetary models to resolve the conflict.

7Lippi and Secchi (2009) use the same data set as Alvarez and Lippi (2009), but calculate the cash expenditure ratio for non-durable expenditures. According to their calculation, the share of cash expenditure decreased from 85% in 1993 to 69% in 2004.

3

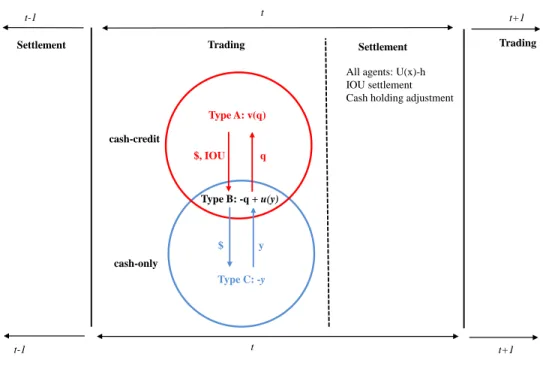

The Model

In this section, we build a cash-credit monetary model based on the framework by Lagos and

Wright (2005) and Rocheteau and Wright (2005) with two innovations: (1) the substitutability

between cash and credit is uneven across economic activities; and (2) some agents actively

manage cash inflows and outflows across these activities. We will start with a description of

the economic environment and then characterize the equilibrium. After that, we derive cash

usage and demand as functions of the credit access rate and the nominal interest rate.

3.1

Economic Environment

Time is discrete and continues forever. Each period consists of two stages: trading and

set-tlement. The trading stage consists of two parallel markets: the cash-credit market and the

cash-only market. In the cash-credit market, both cash and credit can be used for transactions.

In the cash-only market, only cash is accepted. As discussed in the introduction, the structure

reflects the different extents of substitutability between cash and credit across different

eco-nomic activities. Credit competes directly with cash only in the cash-credit market.9 In the

settlement stage, agents settle credit or debt balances and adjust money holdings. There are

three perishable goods, one in each of the three markets: good q in the cash-credit market,

goodyin the cash-only market, and goodxin the settlement stage. Agents are price takers in

all three markets.

The economy is inhabited by three types – A, B and, C – of infinitely-lived agents, each of

measure one. In the settlement stage, all agents can consume or produce goodx. The utility

from consumption isU(x)withU0 >0andU00 <0. Producing one unit ofxrequires one unit

cash-credit

Type C: -y

cash-only

Trading

t t+1

Type B: -q + u(y)

Type A: v(q)

$, IOU q

All agents: U(x)-h IOU settlement Cash holding adjustment

Settlement

t-1

Trading Settlement

t t+1

t-1

$ y

Figure 2: Model Environment

of laborh, which incurs disutility of one. There existsx∗such thatU0(x∗) = 1. In the trading

stage, type A agents are active only in the cash-credit market, type C agents are active only

in the cash-only market, while type B agents participate in both markets. In the cash-credit

market, type A agents are buyers who wish to consume but cannot produce, and type B agents

are sellers who can produce but do not want to consume. Type A’s utility from consumingq

units of the good is v(q), with v0 > 0, v00 < 0, and v0(0) = ∞. The coefficient of relative

risk aversion, σq = −qv00(q)/v0(q), is less than1 everywhere. Type B’s cost of producingq

units of goods is q. There exists q∗ such that v0(q∗) = 1. In the cash-only market, type B

are buyers who cannot produce but would like to consume; their utility from consumption is

u(y), withu(0) = 0,u0 >0,u00<0, andu0(0) =∞. The coefficient of relative risk aversion,

σy =−yu00(y)/u0(y), is less than1everywhere. Type C agents are endowed with a productive

technology and can produceyunits of good at a cost ofy, but do not want to consume. There

existsy∗ such that u0(y∗) = 1. Assumeq∗ > y∗, or the cash-credit sector is larger than the

The period utility functions of the three types of agents are, respectively,

UA = v(qA) +U(x)−hA, (1)

UB = −qB+u(yB) +U(xB)−hB, (2)

UC = −yC +U(xC)−hC. (3)

Agents discount the next period’s utility by0< β <1.

The structure of the economy implies that there are potential gains from trade between

type A and type B agents in the cash-credit market, and between type B and type C agents

in the cash-only market. There are two payment instruments: cash (used interchangeably

with currency or money) and credit. A fraction, δ ∈ [0,1], of type A agents have access to

credit, type B agents accept both money and credit for sales of goodq,and typeCagents only

accept cash for payments. The stock of moneyM grows at a constant gross rate,γ > β. The

expansion (contraction) of the money supply is implemented as lump-sum transfers to (taxes

on) agents in the settlement stage in the amount of τ = (γ−1)M/3. Credit is extended in

the cash-credit market, and credit balances are settled in the next period’s settlement stage.10

Credit expansion is represented by a higher fraction of type A agents holding credit cards.

In each trading cycle, type A agents engage in the following activities. In the cash-credit

market, they trade with type B agents for goodqusing cash, credit, or both. In the settlement

stage, they adjust their money holdings and settle debt balances incurred in the previous

cash-credit market. Type B agents do the following. In the cash-cash-credit market, they sell good q

to type A agents, accepting either cash or credit. In the cash-only market, they use cash to

purchase goodyfrom type C agents. In the settlement stage, they adjust their money holdings

and settle credit balances incurred in the previous cash-credit market. Type C agents sell good

yto type B agents in the cash-only market, and spend money earned in the cash-only market

to purchase goodxin the settlement stage.

3.2

Equilibrium Characterization

In this subsection, we characterize the equilibrium allocation. The following notations are

used. The value functions in the trading stage and the settlement stage areV andW,

respec-tively. Let φ, φq,andφy denote the value of money in terms of x, q,andy,respectively. We

will use “ˆ” to denote variables in the next period. We will focus on symmetric-stationary

equilibria where the real variables, including the real cash balance, φM, are constant over

time. The equilibrium inflation rate is equal to the money growth rate γ, and the nominal

interest rate isi=γ/β−1>0.

3.2.1 Settlement Stage

Agents settle credit balances and adjust money holdings in the settlement stage. The value

function of an agent holdingm units of money andaunits of credit (a > 0, if the agent is a

creditor, anda <0, if the agent is a debtor) is

W(m, a) = max

x,h,mˆ U(x)−h+βV ( ˆm)

s.t. x+φmˆ =φ(m+τ) +a+h,

which can be rewritten as

W(m, a) = max

The first-order conditions are

x : U0(x) = 1orx=x∗,

ˆ

m : β∂Vj( ˆm)

∂mˆ ≤φ, “=” ifm >ˆ 0. (5)

The marginal value of money and credit balances in the settlement stage are, respectively,

∂W(m, a)

∂m =φ,and

∂W (m, a)

∂a = 1.

We measure the demand for cash as the real cash holdings at the beginning of the trading

stageφˆmˆ. A well-known result from the literature is that those who do not need to use cash

for payment (i.e., type A agents with access to credit and type C agents) will not take cash into

the trading stage ifi >0.

3.2.2 Trading Stage

First, we characterize the decisions for agents who do not take cash into the trading stage.

Type A agents with access to credit (use the subscript 1to denote variables associated with

these agents) buy goodqon credit and solve

max q1

v(q1) +W(0, pq1),

where pis the price of q in terms of goodx. In words, in the cash-credit market, the agent

buysq1units of goodqwith credit and promises to repaypq1units of goodxin the settlement

stage. The first-order condition forq1 is

Type C agents choose the production of good y (we omit the subscript knowing that in

equilibrium the production of type C is equal to the consumption of type B) to solve

max

y −y+W(y/φy,0).

The first-order condition is

y:φ=φy, (7)

which says that the relative price between goodyand goodxis one.

The value function of type A cash users (use the subscript 2 to denote variables associated

with these agents) is

V2(m2) = max

q2

v(q2) +W2(m2−q2/φq,0)

s.t. q2 ≤φqm2.

The agent buysq2units of goodqand pays for it withq2/φqunits of cash. Combine the value

functionsW andV to derive type A cash users’ maximization problem as

W2(m,0) = φm+τ +βW(0,0) (8)

+max

ˆ m2,q2

(

−φmˆ2+β

"

ˆ

φ mˆ2−

q2

ˆ

φq

!

+v(q2) +λ2( ˆφqmˆ −q2)

#) ,

where λ2 is the Lagrangian multiplier associated with the cash constraint. The first-order

conditions are11

ˆ

m2 : φ =β( ˆφ+λ2φˆq)⇒i=λ2

φq

φ ,

q2 : v0(q2) =

φ φq

+λ2 =

φ φq

(1 +i). (9)

11Note thatmˆ

As is standard in the literature, the cash constraint binds (i.e.,λ2 >0) ifi >0.

The value function for type B agents is

VB(mB) = max

qBm,qBc,y

−(qBm+qBc) +u(y) +W(mB+qBm/φq−y/φ,−pqBc)

s.t.y≤φ(mB+qBm/φq).

In words, a type B agent sellsqBm units of good in cash andqBcunits of good in credit in the

cash-credit market, and buysyunits of good in the cash-only market, which can be financed

by cash brought by the agent from the previous settlement stage and cash revenue in the

cash-credit market. Combine the value functions for type B agents to get

WB(m, a) = φ(m+τ) +a+βW(0,0) (10)

+ max

ˆ

mB,qBm,y

−φmˆB+β

ˆ

φmˆB+qφˆBq

−qBm−qBc+pqBc

+u(y)−y+λB

ˆ

φ( ˆmB+ qBmφˆq )−y

;

where λB is the Lagrangian multiplier associated with the cash constraint. The first-order

conditions are12

ˆ

mB : −φ+βφˆ(1 +λB)≤0orλB ≤i, “=” ifmˆB >0, (11)

y : u0(y) = 1 +λB,

qBm : 1 = (1 +λB)

φ φq

⇒u0(y)φ

φq

= 1, (12)

qBc : p= 1. (13)

Conditions (6) and (13) imply

q1 =q∗,

12Note thatq

and conditions (9) and (12) imply

u0(y)v0(q2) = 1 +i. (14)

The left-hand side of equation (14) captures the marginal benefit of holding cash (which can

be used in both the cash-credit and cash-only markets), and the right-hand side captures the

marginal cost.

To solve (q2, y), we need to look at type B agents’ cash flows. Type B agents receive cash

from type A cash users selling good q and spend cash on goody. Type A cash users’ cash

holding can be derived from their cash constraint q2 = ˆφqmˆ2, which implies z2 = ˆφmˆ2 =

ˆ

φq2/φˆq=q2φ/φq, or

z2 =

q2

u0(y). (15)

Type B agents therefore receive (1−δ)z2 = (1−δ)u0q(2y) units of cash by selling q in the

cash-credit market. If they receive enough cash from type A cash users to purchasey∗units of

good in the cash-only market, then they consume y∗ and hold zero cash. If the cash revenue

lies betweenyi and y∗, then type B agents continue to setzB to zero, and exhaust their cash

revenue for the purchase ofy. If the cash revenue is not enough to buyyi, which solves

u0(yi) = 1 +i,

type B agents’ consumption ofyand real cash holdingzBsatisfy

y =

y∗ if (1−δ) q2

u0(y) ≥y∗,

(1−δ) q2

u0(y) ifyi <(1−δ)u0q(2y) < y∗,

yi if (1−δ)u0q(2y) ≤yi.

(16)

zB =

0 if (1−δ)z2 ≥yi,

yi−(1−δ)z2 if (1−δ)z2 < yi.

(17)

Type B agents’ production ofqcan be derived from the market-clearing conditions

qBc = δq∗, (18)

qBm = (1−δ)q2. (19)

3.2.3 Equilibrium

The symmetric-stationary competitive equilibrium is defined as follows:

Definition 1 Given credit condition δ and nominal interest rate i, a symmetric-stationary equilibrium consists of

(i) a settlement stage allocationx=x∗ for all agents;

(ii) a trading stage allocationq1 =q∗,(q2, y)such that equations (14) and (16) hold, and

(qBm, qBc) given by equations (18) and (19); and

(iii) a distribution of cash holdings at the beginning of each periodz1 = zC = 0, and

(z2, zB)given by equations (15) and (17).

After solving the equilibrium allocation, we derive four quantities–the total money demand

value of cash transactions at points of salezT, and GDPY–all measured in units ofx.

z = (1−δ)z2+zB,

S = (1−δ)q2+δq ∗

u0(y) +y,

zT = (1−δ)z2+y=

(1−δ)q2

u0(y) +y,

Y = S+ 3x∗ = (1−δ)q2+δq ∗

u0(y) +y+ 3x ∗

.

From these quantities, we derive three ratios to characterize the demand for cash: the velocity

of cashυ(at points of sale), the share of cash transactions at points of saleθand the CIC/GDP

ratioρ

υ = zT

z , θ = zT

S , ρ= z Y .

4

Theoretical Implications

In this section, we explore the effect of credit expansion,δ, and the nominal interest rate,i, on

cash usage and demand. We will focus more on the effect of credit expansions for two reasons.

First, our model has very different implications from standard cash-credit models regarding

credit expansions. Second, the main mechanism that contributes to our model’s success in

capturing the cash paradox is the breakdown of the tight connection between cash usage and

demand in response to credit conditions. Regarding the effect of the interest rate, our model’s

prediction is similar to that from standard models. We conclude this section by discussing

the intuition about why our model is likely to be more successful than standard models in

i: 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑖𝑖𝑟𝑟𝑖𝑖𝑖𝑖

δ: 𝑟𝑟𝑎𝑎𝑎𝑎𝑖𝑖𝑖𝑖𝑖𝑖 𝑖𝑖𝑡𝑡 𝑎𝑎𝑖𝑖𝑖𝑖𝑐𝑐𝑖𝑖𝑖𝑖 1 − 𝑦𝑦∗/𝑞𝑞∗

𝛿𝛿2= 1 − 𝑦𝑦𝑖𝑖𝑢𝑢𝑢(𝑦𝑦𝑖𝑖)/𝑞𝑞∗

𝛿𝛿1= 1 − 𝑦𝑦∗/𝑞𝑞𝑖𝑖

𝑖𝑖: 𝑞𝑞𝑖𝑖= 𝑦𝑦∗

o

Regime I

Regime II

Regime III

𝑧𝑧𝐴𝐴> 0

𝑧𝑧𝐵𝐵= 0

𝑦𝑦 = 𝑦𝑦∗

𝑞𝑞 = 𝑞𝑞𝑖𝑖

𝑧𝑧𝐴𝐴> 0

𝑧𝑧𝐵𝐵= 0

𝑦𝑦𝑖𝑖< 𝑦𝑦 < 𝑦𝑦∗

𝑞𝑞𝑖𝑖< 𝑞𝑞 < 𝑞𝑞∗

𝑧𝑧𝐴𝐴> 0

𝑧𝑧𝐵𝐵> 0

𝑦𝑦 = 𝑦𝑦𝑖𝑖

𝑞𝑞 = 𝑞𝑞∗

Figure 3: Regimes

4.1

Effects of Credit Expansion

As credit expands or asδincreases from 0 to 1, the economy will be in one of three regimes,

distinguished by whether or not type B agents consumey∗in the cash-only market and whether

or not they take cash into the trading stage. The threshold values ofδthat separate these three

regimes depend on the nominal interest rate. In Figure 3, we mark the border of each regime

in the(δ, i)space.

4.1.1 Regime I: Low Credit Regime

In regime I, type B agents receive enough cash revenue in the cash-credit market to purchase

y∗units of consumption in the cash-only market(y=y∗), and do not take cash into the trading

is given by

z2 = qi,

zB = 0,

z = zA = (1−δ)z2 = (1−δ)qi,

zT = (1−δ)qi+y∗.

If y∗ < qi, then the economy starts in regime I when δ = 0 and remains in this regime if

(1−δ)qi ≥y∗, or

δ≤δ1 ≡1−

y∗ qi

.

Ify∗ > qi, then the economy will not experience regime I and will be in regime II whenδ = 0.

The velocity of cash is

υ = zT

z = 1 +

y∗

(1−δ)qi

.

The share of cash transactions at points of sale is

θ = zT

S =

(1−δ)qi+y∗

(1−δ)qi+y∗+δq∗

.

The CIC/GDP ratio is

ρ= z

Y =

(1−δ)qi

(1−δ)qi+y∗+δq∗+ 3x∗

.

Proposition 1 The Effects of δ in regime I: dq1/dδ = dq2/dδ = dy/dδ = 0, dzT/dδ =

dz/dδ <0,dυ/dδ >0,dθ/dδ <0,anddρ/dδ <0.

Proof.See Appendix A.

In regime I, the allocation(q1, q2, y)is invariant to δ. Type B agents receive enough cash

from type A cash users to purchase y∗ and their demand for cash is zero. As more type A

A agents (which is also the total demand for cash), and the CIC/GDP ratio all decrease. By

construction, the velocity of cash at points of sale is between one and two. After type B agents

receive cash from their customers, a fixed amount (y∗) of it is spent in the cash-only sector

and this part of cash has a higher velocity of two. As type B agents receive less cash from

their customers in the cash-credit sector, the fraction of cash that travels twice in the trading

stage increases, resulting in a higher velocity.

4.1.2 Regime II: Intermediate Credit Regime

In regime II, type B agents do not have enough cash revenue in the cash-credit market to

support consumption of y∗ in the cash-only market. However, as long asy > yi, the benefit

of taking cash into the trading stage, u0(y), is lower than the cost, 1 +i, and type B agents’

cash demand is zero. They simply spend all the cash received from the cash-credit market to

purchaseyon the cash-only market. As a result,q2 andyjointly solve (14) and

y= (1−δ)q2

u0(y) ,

which follows from (15) and (16). Money demand is given by

zB = 0,

z2 =

q2

u0(y) =

y

1−δ,

z = zA= (1−δ)z2 =y,

zT =

(1−δ)q2

u0(y) +y= 2y.

This regime occurs when

whereδ2 solvesyi = (1−δ)q∗/u0(yi), or

δ2 ≡1−

yiu0(yi)

q∗ .

Note thatd[yu0(y)]/dy =u0(y) +yu00(y)>0under the assumptionσy =−yu00(y)/u0(y)<1.

Since yi < y∗, we have yiu0(yi) < y∗u0(y∗) = y∗ < q∗ and δ2 > 0, and the economy will

experience regime II for sure asδincreases from0.

In regime II, the cash taken by type A cash users into the trading stage is used twice: once

in the cash-credit market and once in the cash-only market. The velocity of cash is therefore

υ = zT

z = 2.

The share of cash transactions at points of sale is

θ = zT

S =

2y

2y+δuq0(∗y)

,

and the CIC/GDP ratio is

ρ= z

Y =

y

2y+ uδq0(∗y)+ 3x∗

.

In regime II, the effects of credit expansions is described in the following proposition.

Proposition 2 The effects ofδin regime II:dq1/dδ = 0,dq2/dδ > 0,dy/dδ < 0, dzT/dδ = 2dz/dδ <0,dυ/dδ= 0,dθ/dδ <0,anddρ/dδ <0.

Proof.See Appendix A.

In regime II, type B agents still choose not to take any cash to the trading stage. As the

fraction of type A credit users increases, type A agents’ (and therefore, the total) cash demand

CIC/GDP ratio continues to decrease.13

4.1.3 Regime III: High Credit Regime

As the fraction of credit card users continues to increase beyond δ2, type B agents do not

receive enough cash to purchaseyi. In this situation, type B agents start to accumulate some

cash to make up for the decreasing cash revenue in the cash-credit market (see equation 17).

The economy enters into regime III. In this regime, the marginal benefit of consuming y is

higher than that in Regime II and equal to 1 + i, the marginal cost of acquiring money in

the settlement stage. The cash-only market output is y = yi. Since type B agents are cash

constrained in the only market, they are willing to pay more to acquire cash in the

cash-credit market compared to the previous regimes. This leads toq2 =q∗; i.e., type A cash users

can afford the first-best consumption.14 The money demand is given by

z2 =

q∗ u0(y) =

q∗

1 +i,

zA = (1−δ)z2,

zB = yi−(1−δ)z2 =yi−(1−δ)

q∗

1 +i,

z = zB+zA =yi,

zT =

(1−δ)q∗

u0(y) +yi = (1−δ)

q∗

1 +i +yi.

13Gu et al. (2016) recently demonstrate that the increase in credit limits is neutral in a wide range of environ-ments. Our model provides a counter example. In our Bank of Canada Staff Working Paper version, Jiang and Shao (2014), we capture credit expansions along the intensive margin as increasing credit limits as in Gu et al. (2016), and find that when the economy is in regime II, a higher credit limit is not neutral: it expands cash-credit activities (q) and shrinks cash-only activities (y).

The velocity of cash, the share of cash transactions at points of sale and the CIC/GDP ratio

are, respectively,

υ = zT

z = 1 +

(1−δ)q∗

(1 +i)yi

, (20)

θ = zT

S =

(1−δ)1+q∗i +yi q∗

1+i +yi

, and (21)

ρ = z

Y =

yi q∗

1+i +yi+ 3x

∗. (22)

The effect of credit expansion in this regime is described in the proposition below. (The

proof is trivial and therefore omitted.)

Proposition 3 The effects ofδin regime III:dq1 =dq2/dδ=dy/dδ = 0,dzT/dδ =−q∗/(1+

i) <0, dz/dδ = 0, dυ/dδ =−q∗/[(1 +i)yi)]< 0,dθ/dδ = −q∗/[q∗ + (1 +i)yi] < 0, and

dρ/dδ = 0.

Once the economy enters into regime III, a further credit expansion reduces the value of

cash transactions, but the total money demand becomes flat. The reduction in type A agents’

money demand is exactly offset by the rise in type B agents’ money demand.

Figure 4 summarizes the effect of credit expansions on allocation(q2, y), money demand

(zA, zB), cash velocity υ, the share of cash transactionsθ, and CIC/GDPρ as the fraction of

type A agents with access to credit increases from0to1.

While a standard cash-credit model predicts continuous and synchronized falls in cash

usage and demand in response to credit expansions (see Appendix D), our model suggests

that this trend stops as credit expands beyond a certain level. In particular, onceδreachesδ2,

agents change their cash management practices and further credit expansions induce a

redistri-bution of cash demand. Buyers in the cash-credit sector hold less cash to spend in that sector,

while sellers in that sector acquire more cash in advance to make up for the shortfall of cash

δl 1

𝒒𝒒𝒊𝒊

𝒒𝒒∗

𝒚𝒚𝒊𝒊

𝒚𝒚∗

Figure 3: Effect of credit expansion

0 0

0 0

1

v

0

θ

0

2

δ2 δ

δl δ2 1 δ

δl δ2 1 δ δl δ2 1 δ

δl δ2 1 δ

δl δ2 1 δ

𝒒𝒒𝟐𝟐

y

𝒛𝒛𝑨𝑨; 𝒛𝒛𝑩𝑩 ρ

Figure 4: The effects of credit expansion

cash remains constant despite reduced cash usage. Compared with cash acquired by buyers,

which is used in both sectors, cash acquired by sellers has a lower velocity because it is used

exclusively in the cash-only sector. As a result, the redistribution of cash demand reduces the

overall velocity of cash.15

4.2

Effects of Interest Rate

Besides the credit access condition, the interest rate is another important parameter that affects

cash usage and demand. Our model’s prediction on the effect of the interest rate is similar to

that of standard cash-credit models, which we summarize in the following proposition.

Proposition 4 The effects ofi: dq1/di= 0;dq2/di <0in regimes I and II, and= 0in regime III;dy/di = 0in regime I, and<0in regimes II and III;dz/di < 0,dρ/di < 0,dθ/di < 0;

dυ/di >0in regimes I and III, and= 0in regime II.

Proof.See Appendix A.

As the interest rate rises, the cost of holding cash increases. Consumption financed by

cash, q2 and y, decreases (unless q2 = q∗ or y = y∗). Cash usage and cash demand both

decrease in response to higher interest rates.

In terms of velocity, our model provides a theory about the positive correlation between

the variable and inflation, the so-called hot potato effect of inflation. In particular, inflation

affects velocity by changing the fraction of money that sits idle in either the cash-only or the

cash-credit market.

The specification of our model implies that cash velocity lies between one and two. In

regime II, all cash is used in both markets so the velocity is fixed at the upper bound of two. In

regimes I and III, a fraction of cash sits idle in one of the two markets, and this fraction changes

in response to inflation. In regime I, type B agents use part of their cash revenues received

from type A cash users in the cash-credit market to finance a fixed level of purchase (y∗) in the

cash-only market, with the surplus cash sitting idle in the second market. As inflation rises,

type A cash users acquire less cash, which means that type B agents receive less cash and

have less idle balances in the cash-only market. As a result, velocity increases. In regime III,

both type A and B agents acquire money balances in advance. The amount acquired by type

B agents is spent only in the cash-only market and sits idle in the cash-credit market. The

amount acquired by type A cash users is spent in both markets and has a higher velocity. Both

types acquire less cash in response to higher inflation. However, type B agents reduce their

cash holdings more than type A cash users, causing the fraction of cash that sits idle in the

cash-credit market to fall. Consequently, the overall velocity of cash increases.16

Ro-5

Capturing the Cash Paradox

In the previous section, we develop a model that adds two new features into a standard

cash-credit model: different substitutability between cash and cash-credit across sectors, and cash flows

between the two sectors. In this section, we carry out a series of calibration exercises to

highlight the roles played by these two modelling features. First, we calibrate a standard

cash-credit model with a single sector. We then calibrate a model with two segregated sectors

that feature different substitutability between cash and credit (and label it the no-cash-flow or

“NCF” model) to identify the role played by this modelling feature. Finally, we calibrate the

full model with both modelling features to discuss the importance of the cash-flow channel.

For the calibration, we use constant-relative-risk-aversion (CRRA) utility functions

v(q) = sq

1−α

1−α andu(y) =

y1−η

1−η.

The curvature parameters α and η indicate the demand elasticity of the interest rate for the

cash users when they are liquidity constrained.17 In our calibration, we setα = ηso that the

two markets have the same interest rate elasticity.18 According to our theory, we setα∈(0,1)

in the full model, but do not restrict it to be less than 1 for the standard model and the NCF

model. The scaling parameter s >0captures the size of the cash-credit sector relative to the

cash-only sector.

Our calibration strategy is to use the time series of the credit access rate(δ)and the nominal

interest rate (i), and fit model parameters (α, s, x∗) to match the time series of CIC/GDP,ρ.

More specifically, for each parameter triplet (α, s, x∗), we plug(α, s, x∗)and (δt, it)into the

cheteau, 2005; Faig and Jerez, 2006; Ennis, 2008 and 2009; Liu et al., 2011; Nosal 2011; Dong and Jiang, 2013; and Hu et al., 2017). All these models feature a precautionary demand for money, while we identify a different mechanism that does not rely on the precautionary motive.

17When the cash users are liquidity constrained, the demand for type A cash user isq

iand the demand for type B cash user isyi. The demand elasticity is thenα(1+i)i andη(1+i)i , respectively.

expression forρto calculate the model’s prediction of CIC/GDP in periodt,ρˆt(δt, it|α, s, x∗).

We then do a grid search in the(α, s, x∗)space to minimize the sum of squared errors of the

predicted series of CIC/GDP from its actual path:

( ˆα,s,ˆ xˆ∗) = arg min

α,s,x∗

X

t

[ ˆρt(δt, it|α, s, x∗)−ρt] 2

.

In the case of the standard model, there is only one sector where cash and credit are perfect

substitutes (whereq is traded) and we sets = 1and grid search over the (α, x∗) space. Our

calibration strategy is in the same spirit as that in Lagos and Wright (2005) and follows the

tra-dition of Lucas (2000). The difference is that instead of fitting the model parameters to match

the money demand equation ρ(i), we fit the parameters to match the time series of money

demand over the sample period,ρt. After we acquire the model parameters, we calculate the

imputed series for cash usage and demand,θˆandρˆ.

We calibrate the models to the cases of four countries, Australia, Canada, the United

King-dom and the United States. The sample period spans from 1960 to 2014.19 We start from 1960

because it was not until 1958 that major banks issued credit cards. We use the (annualized)

short-term safe corporate bond rate to measure the nominal interest rate.20 To the best of our

knowledge, continuous time series data on the credit access rate are unavailable, so we have to

resort to various surveys to construct it. In each country over the sample period from 1960 to

2014, infrequent surveys that provide information on the fraction of households holding credit

cards were conducted. To fill in the missing years, we fit a polynomial function across the

available observations, together with an initial pointδ1960 = 0, to impute the series ofδfor the

entire sample period.

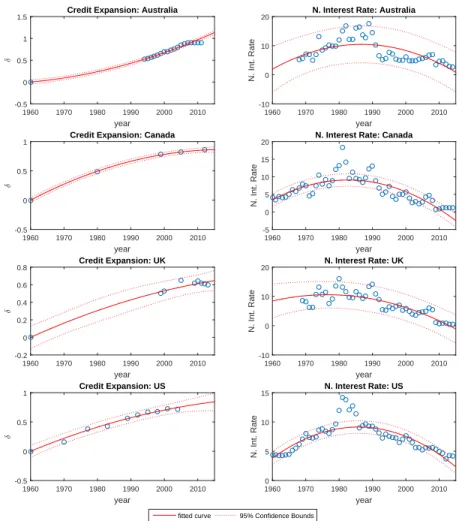

Figure 5 shows the trend in credit expansions and nominal interest rates in the data. There

19The sample period for Australia and the United Kingdom starts at 1968 and 1973, respectively, because the nominal interest rate data on these countries start from those years.

year

1960 1970 1980 1990 2000 2010

/

-0.5 0 0.5 1

1.5 Credit Expansion: Australia

fitted curve 95% Confidence Bounds

year

1960 1970 1980 1990 2000 2010

N. Int. Rate

-10 0 10

20 N. Interest Rate: Australia

year

1960 1970 1980 1990 2000 2010

/

-0.5 0 0.5

1 Credit Expansion: Canada

year

1960 1970 1980 1990 2000 2010

N. Int. Rate

-5 0 5 10 15

20 N. Interest Rate: Canada

year

1960 1970 1980 1990 2000 2010

/ -0.2 0 0.2 0.4 0.6

0.8 Credit Expansion: UK

year

1960 1970 1980 1990 2000 2010

N. Int. Rate

-10 0 10

20 N. Interest Rate: UK

year

1960 1970 1980 1990 2000 2010

/

-0.5 0 0.5

1 Credit Expansion: US

year

1960 1970 1980 1990 2000 2010

N. Int. Rate

0 5 10

15 N. Interest Rate: US

Figure 5: Time paths of credit access rate and nominal interest rate

is a clear upward trend forδdue to financial innovations. The nominal interest rate appears to

be hump-shaped, rising until the 1980s and declining afterwards. While calculatingρˆ, we use

the imputed series ofδand the actual series ofi(the trend curve foriis plotted for reference).

The upper panel from Table 1 summarizes the calibrated parameter values (α,ˆ ˆs,xˆ∗) for

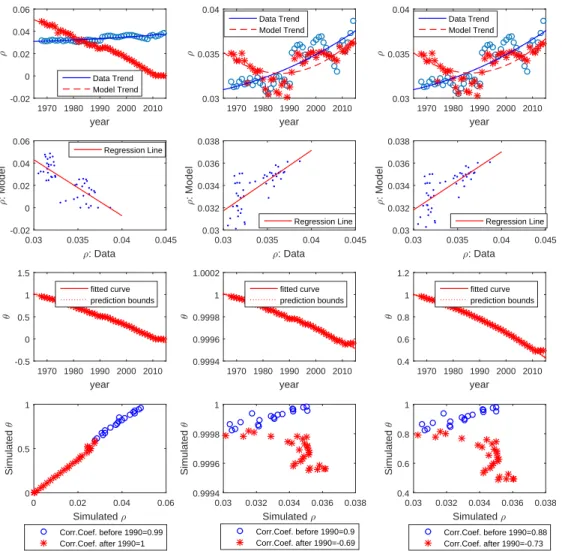

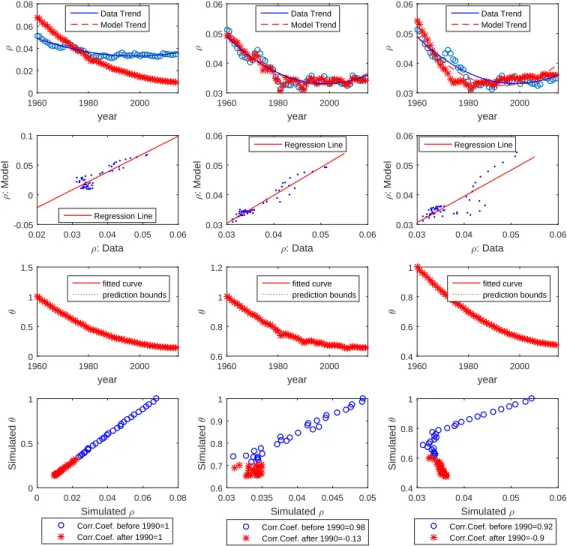

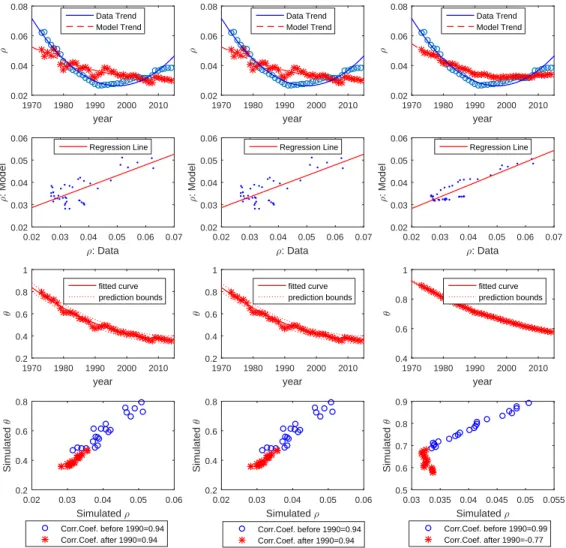

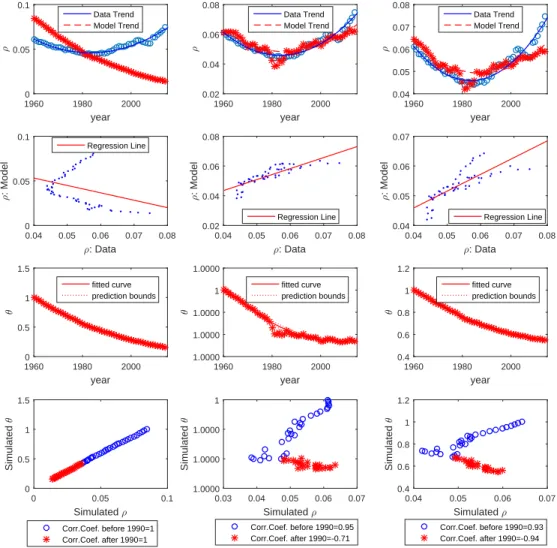

each country for each of the three models. Figures 6 to 9 plots the three models’ prediction

on ρ and θ. Each figure represents one country and has twelve panels. The left column of

actual and predicted series ofρalong with their corresponding (polynomial) time trends. The

second graph scatter plots actual versus predictedρ(together with a regression line). The third

panel plots the predicted series ofθand its trend. The fourth panel scatter plotsρversusθ; the

circles represent data before 1990, and the stars represent data from 1990.

The lower panel of Table 1 provides two statistics to measure the performance of the model

in capturing the long-run trend in cash demand. The first is the normalized root-mean-square

error (NRMSE) for the predicted path ofρ:

N RM SE =

q

1 N

P

t[ ˆρt(δt, it|α,ˆ ˆs,xˆ∗)−ρt] 2

¯

ρ ,

whereN is the sample size, andρ¯= 1

N

P

tρt is the average CIC/GDP in the sample period.

The second is the correlation between the predicted and actual series of ρ. The third and

fourth rows show the model’s prediction on the correlation between θ and ρ for two

subpe-riods, before 1990 and thereafter, respectively (note that the data suggest that the correlation

is positive before 1990 and negative after 1990).21 The last row reports the (NCF and full)

model’s implied relative size of the cash-credit sector, measured byq∗ (y∗is normalized to1).

Finally, Table 2 reports the share of cash transactions (calculated as the value of cash

transactions over the sum of cash and credit transactions) based on recent payment surveys:

the consumer payment diary surveys conducted in 2009 (Canada), 2010 (Australia), and 2012

(US), and the British Retail Consortium Payment Survey in 2016, which samples merchants.

For comparison, we calculate the average value ofθˆfrom 2005 to 2014 (which are the last 10

years for our calibration exercises) implied by each model.

21We also calculate the correlation betweenρˆandθˆ, splitting the sample at different time points between 1980

year

1970 1980 1990 2000 2010

; 0.03 0.035 0.04 Data Trend Model Trend

;: Data

0.03 0.035 0.04 0.045

; : Model 0.03 0.032 0.034 0.036 0.038 Regression Line year

1970 1980 1990 2000 2010

3 0.4 0.6 0.8 1 1.2 fitted curve prediction bounds

Simulated ;

0.03 0.032 0.034 0.036 0.038

Simulated 3 0.4 0.6 0.8 1

Corr.Coef. before 1990=0.88 Corr.Coef. after 1990=-0.73

year

1970 1980 1990 2000 2010

; -0.02 0 0.02 0.04 0.06 Data Trend Model Trend

;: Data

0.03 0.035 0.04 0.045

; : Model -0.02 0 0.02 0.04 0.06 Regression Line year

1970 1980 1990 2000 2010

3 -0.5 0 0.5 1 1.5 fitted curve prediction bounds

Simulated ;

0 0.02 0.04 0.06

Simulated

3

0 0.5 1

Corr.Coef. before 1990=0.99 Corr.Coef. after 1990=1

year

1970 1980 1990 2000 2010

; 0.03 0.035 0.04 Data Trend Model Trend

;: Data

0.03 0.035 0.04 0.045

; : Model 0.03 0.032 0.034 0.036 0.038 Regression Line year

1970 1980 1990 2000 2010

3 0.9994 0.9996 0.9998 1 1.0002 fitted curve prediction bounds

Simulated ;

0.03 0.032 0.034 0.036 0.038

Simulated 3 0.9994 0.9996 0.9998 1

Corr.Coef. before 1990=0.9 Corr.Coef. after 1990=-0.69

Figure 6: Model predictions–Australia

year

1960 1980 2000

; 0 0.02 0.04 0.06 0.08 Data Trend Model Trend

;: Data

0.02 0.03 0.04 0.05 0.06

; : Model -0.05 0 0.05 0.1 Regression Line year

1960 1980 2000

3 0 0.5 1 1.5 fitted curve prediction bounds

Simulated ;

0 0.02 0.04 0.06 0.08

Simulated

3

0 0.5 1

Corr.Coef. before 1990=1 Corr.Coef. after 1990=1

year

1960 1980 2000

; 0.03 0.04 0.05 0.06 Data Trend Model Trend

;: Data

0.03 0.04 0.05 0.06

; : Model 0.03 0.04 0.05 0.06 Regression Line year

1960 1980 2000

3 0.4 0.6 0.8 1 fitted curve prediction bounds

Simulated ;

0.03 0.04 0.05 0.06

Simulated 3 0.4 0.6 0.8 1

Corr.Coef. before 1990=0.92 Corr.Coef. after 1990=-0.9

year

1960 1980 2000

; 0.03 0.04 0.05 0.06 Data Trend Model Trend

;: Data

0.03 0.04 0.05 0.06

; : Model 0.03 0.04 0.05 0.06 Regression Line year

1960 1980 2000

3 0.6 0.8 1 1.2 fitted curve prediction bounds

Simulated ;

0.03 0.035 0.04 0.045 0.05

Simulated 3 0.6 0.7 0.8 0.9 1

Corr.Coef. before 1990=0.98 Corr.Coef. after 1990=-0.13

Figure 7: Model predictions–Canada

year

1970 1980 1990 2000 2010

; 0.02 0.04 0.06 0.08 Data Trend Model Trend

;: Data

0.02 0.03 0.04 0.05 0.06 0.07

; : Model 0.02 0.03 0.04 0.05 0.06 Regression Line year

1970 1980 1990 2000 2010

3 0.2 0.4 0.6 0.8 1 fitted curve prediction bounds

Simulated ;

0.02 0.03 0.04 0.05 0.06

Simulated 3 0.2 0.4 0.6 0.8

Corr.Coef. before 1990=0.94 Corr.Coef. after 1990=0.94

year

1970 1980 1990 2000 2010

; 0.02 0.04 0.06 0.08 Data Trend Model Trend

;: Data

0.02 0.03 0.04 0.05 0.06 0.07

; : Model 0.02 0.03 0.04 0.05 0.06 Regression Line year

1970 1980 1990 2000 2010

3 0.2 0.4 0.6 0.8 1 fitted curve prediction bounds

Simulated ;

0.02 0.03 0.04 0.05 0.06

Simulated 3 0.2 0.4 0.6 0.8

Corr.Coef. before 1990=0.94 Corr.Coef. after 1990=0.94

year

1970 1980 1990 2000 2010

; 0.02 0.04 0.06 0.08 Data Trend Model Trend

;: Data

0.02 0.03 0.04 0.05 0.06 0.07

; : Model 0.02 0.03 0.04 0.05 0.06 Regression Line year

1970 1980 1990 2000 2010

3 0.4 0.6 0.8 1 fitted curve prediction bounds

Simulated ;

0.03 0.035 0.04 0.045 0.05 0.055

Simulated 3 0.5 0.6 0.7 0.8 0.9

Corr.Coef. before 1990=0.99 Corr.Coef. after 1990=-0.77

Figure 8: Model predictions–UK

year

1960 1980 2000

; 0.02 0.04 0.06 0.08 Data Trend Model Trend

;: Data

0.04 0.05 0.06 0.07 0.08

; : Model 0.02 0.04 0.06 0.08 Regression Line year

1960 1980 2000

3 1.0000 1.0000 1.0000 1 1.0000 fitted curve prediction bounds

Simulated ; 0.03 0.04 0.05 0.06 0.07

Simulated 3 1.0000 1.0000 1.0000 1

Corr.Coef. before 1990=0.95 Corr.Coef. after 1990=-0.71

year

1960 1980 2000

; 0 0.05 0.1 Data Trend Model Trend

;: Data

0.04 0.05 0.06 0.07 0.08

; : Model 0 0.05 0.1 Regression Line year

1960 1980 2000

3 0 0.5 1 1.5 fitted curve prediction bounds

Simulated ;

0 0.05 0.1

Simulated 3 0 0.5 1 1.5

Corr.Coef. before 1990=1 Corr.Coef. after 1990=1

year

1960 1980 2000

; 0.04 0.05 0.06 0.07 0.08 Data Trend Model Trend

;: Data

0.04 0.05 0.06 0.07 0.08

; : Model 0.04 0.05 0.06 0.07 Regression Line year

1960 1980 2000

3 0.4 0.6 0.8 1 1.2 fitted curve prediction bounds

Simulated ;

0.04 0.05 0.06 0.07

Simulated 3 0.4 0.6 0.8 1 1.2

Corr.Coef. before 1990=0.93 Corr.Coef. after 1990=-0.94

Figure 9: Model predictions–US

Table 2: Cash shares relative to credit,θ

Australia Canada UK US

Data 0.64(1) 0.36(1) 0.52(2) 0.45(1)

Standard(3) 0.06 0.15 0.37 0.19

NCF(3) 1.00 0.66 0.39 1.00

Full(3) 0.52 0.49 0.60 0.56

Notes: (1) Data are based on payment diary surveys conducted in 2009 (Canada), 2010 (Aus-tralia), and 2012 (US); source: Bagnall et al. (2016). (2) The data on UK are from the 2016 British Retail Consortium Payment Survey. (3) The model’s cash share is the average value from 2005 to 2014.

5.1

The Standard Model

In the standard model, cash usage and demand are characterized by (see Appendix D for the

derivation)

θ = (1−δ)qi

(1−δ)qi+δq∗

, (23)

ρ = (1−δ)qi

(1−δ)qi+δq∗+ 2x∗

. (24)

Bothθandρdecrease withδandi. In earlier decades, the effect of the two parameters works

in the same direction (δand iboth increase). In more recent decades, however, the effect of

the two parameters works against each other (δcontinues to rise whileistarts to decrease). To

capture the cash paradox, the effect ofδ must dominate to capture the time trend inθ, while

the opposite is required to capture the trend in ρ. Although in theory it is still possible that

cash usage and demand can diverge from each other, these conflicted requirements imply that

it is difficult for standard cash-credit models to capture the cash paradox.

As shown in Table 1, the standard model is unable to resolve the cash paradox. Although

it generates continuously declining cash usage (θ), which is consistent with data, the predicted

40.7% for Canada, 17.8% for the United Kingdom, and 49.5% for the United States. The

correlation betweenρandρˆis even negative for Australia and the United States. In addition,

the standard model fails to account for the diverging trend in cash usage and demand in the

more recent decades: the correlation between θˆand ρˆis positive for all four countries after

1990.

5.2

The NCF Model

In the NCF model, cash usage and demand are given by (see Appendix E for the derivation):

θ = (1−δ)qi+yi

(1−δ)qi+δq∗+yi

,

ρ = (1−δ)qi +yi

(1−δ)qi+δq∗+yi+ 4x∗

.

Compared with the standard model, the NCF model is more flexible and allows the relative

effect of credit accessibility and the interest rate to differ in these two sectors. Note that δ

affects only the cash-credit sector, andiaffects both sectors. A smallerstends to increase the

relative importance ofi.

The NCF model’s performance is similar to the standard model for the United Kingdom

(and fails to capture the cash paradox). The model performs very well in terms of capturing

the cash demand series in the other three countries: the NRMSE forρshrinks substantially to

4.5% in Australia, 3.4% in Canada, and 7.0% in the United States.

The mechanism through which the NCF model captures the trend in money demand is as

follows. Note that the imputed value of s, which captures the size of the cash-credit sector

relative to the cash-only sector, is very small for Australia (at 0.003) and the United States (at

0.137). Together with the power of the utility functionα, it implies thatq∗is very close to zero

to the cash-only sector, which is hard to justify for advanced economies. For cash demand, a

negligible cash-credit sector means that the demand for cash is almost entirely driven by the

demand in the cash-only sector, which is shielded against credit expansions and has increased

in response to lower interest rates in the past two to three decades. However, the success

story for cash demand comes at a cost: the implied relative size of the cash-credit sector is

unreasonably low. In addition, although the model predicts that θ decreases over time, the

magnitude of changes is infinitesimal and the share of cash transactions has remained close to

1in the last six decades.

The NCF model does reasonably well for Canada. Although the cash-credit sector is still

smaller than the cash-only sector (q∗ = 0.648), the difference is not as extreme as in Australia

and the United States. The imputedθ averages at 66%from 2005 and 2014 (the survey data

suggest that the share of cash transactions is about 36% in 2009 in Canada).

5.3

The Full Model

The full model, which incorporates the cash-flow channel, generates continuous and

substan-tial declines in cash usage (θ) as suggested by the data. It also captures the time trend of

cash demand well. The NRMSE is small, ranging from 4.5% (in Australia) to 14.4% (in the

United Kingdom). It predicts that, despite continuing drops in cash usage, cash demand

de-clines only in earlier years, but stabilizes or increases in the more recent two or three decades,

successfully capturing the cash paradox. In all four countries, the correlation between cash

usage and demand is positive before 1990, but becomes negative afterwards. According to the

calibration, the cash-credit sector is larger than the cash-only sector in all four countries, and

the implied cash share is much more reasonable: the average cash share in 2005-2014 ranges

from 49% (in Canada) to 60% (in the United Kingdom).