Alternatives

Benefiting from Merger

Arbitrage

Dr Tim Wooge

Senior Product Developer – Liquid Alternatives Allianz Global Investors

A typical acquisition deal involves the acquirer offering a premium acquisition price for the target company in order to win approval from the target company’s shareholders and board. When an M&A transaction is announced the target company’s stock typically trades at a discount to the price offered by the acquiring companies. The difference between the target’s share price and the offer price is known as the M&A arbitrage spread (“arbitrage spread”). Typically, as the M&A transaction progresses towards a successful close, the target’s share price and the offer price converge and the arbitrage spread shrinks. If, however, the transaction fails the arbitrage spread rises quickly and the target’s share price usually drops to a pre-announcement level. The arbitrage spread is therefore an indicator of the market’s expectation of deal failure.

Accessing the merger arbitrage

risk premium

Merger arbitrage (also known as risk arbitrage) refers to an investment strategy that aims to systematically extract this arbitrage spread from the markets by investing in a diversified portfolio of takeover targets shortly after the announcement of the M&A deal1. The strategy compensates the merger arbitrageur for bearing the risk of deal failure which other investors in the target firms might not be willing to accept. The supply and demand imbalance between deal risk “insurance” providers and takers results in structural market inefficiencies2 that can be exploited by merger arbitrage strategy investors.

1 This does not include

strategies that invest in companies based on M&A speculation or rumoured deals. It also does not include hedge funds in this space, which usually employ a fundamental approach and invest in much more concentrated portfolios of targets.

Risk diversification with conventional assets has become increasingly

difficult in light of a low yield environment and relatively expensive

equity markets (as highlighted in our recent publication on “Volatility

as an Asset Class”). As investors try to identify alternative sources

of return, they are increasingly looking towards unconventional

but liquid risk premia, such as the volatility risk premium. The M&A

(Mergers & Acquisitions) arbitrage spread also represents one such

alternative risk premium that is sufficiently liquid and can provide

attractive returns and diversification effects for investors.

The upside for the investor in merger arbitrage strategies equals the arbitrage spread of the portfolio of takeover targets. However, if one deal fails or a transaction is withdrawn, the downside for this single position can be significant. In most cases the target’s share price will fall back to the levels prior to the announcement of the transaction and the shares begin to trade again based on fundamentals rather than the expectation of a deal. Considering that historically the average premium has been approximately 30 %, this can be a significant drawdown3. However, constructing diversified portfolios of a number of different takeover targets can considerably reduce the likelihood of deal failure as well as the impact of one failed transaction on the profitability of merger arbitrage strategies. The following M&A transaction examples illustrate the dynamics of the arbitrage spread.

When the EUR 2.4bn acquisition of the Norwegian pharmaceutical Algeta ASA by Bayer AG was proposed on 26 November, 2013, the target’s share price jumped 30 %, but it remained below the offer price (see Figure 1) until the completion of the transaction. A merger arbitrage investor could have taken a long position in the target on 26 November (at NOK 345.2) and would have received cash (at NOK 362) in exchange for the shares at the close of the transaction in March 2014, resulting in an arbitrage spread of 4.8 % (over 3 months).

Figure 1: Acquisition of Algeta ASA by Bayer AG in 2014

370 26.11.2013 07.03.2014 330

350 310 290

11-Nov

Arbitrage-Spread Share Price Algeta ASA Price at announcement

Proposal Date Deal Offer

Share Price in NOK

25-Nov 9-Dec 23-Dec 6-Jan 20-Jan 3-F

eb

17-F

eb

3-Mar

270 250

Sources: Bloomberg, Allianz Global Investors. This is for illustrative purpose only and no recommendation or solicitation to buy or sell any particular security. Past performance is not a reliable indicator of future results.

Figure 2, on the other hand, shows the downside potential of a single transaction and reveals that the main risk associated with merger arbitrage strategies is deal failure. On 28 July, 2015, it was announced that Zurich Insurance Group agreed to acquire RSA Insurance, but the deal was abandoned in September 2015 due to Zurich’s financial difficulties at its general insurance unit. RSA’s share price immediately dropped 20 %, causing the arbitrage spread to widen and resulting in a loss on position.

Figure 2: Failed Acquisition of RSA Insurance Group PLC by Zurich Insurance Group

600 28.07.2015 18.09.2015 400

500 300 200

21-Jul

Arbitrage-Spread

Share Price RSA Insurance Group PLC Price at announcement Deal Offer

Share Price in GBP

28-Jul 4-Aug 11-Aug 18-Aug 25-Aug 1-Sep 8-Sep 15-Sep 22-Sep

100 0

Proposal Date

Sources: Bloomberg, Allianz Global Investors. This is for illustrative purpose only and no recommendation or solicitation to buy or sell any particular security. Past performance is not a reliable indicator of future results.

2 See Shleifer and

Vishny (1997), Baker and Savasoglu (2002).

3 The average bid

premium has declined from 45 % (1996 – 2001) to 36 % in the period between 2002 – 2007 (Jetley and Ji). Dieudonné, Cretin, and Bouacha have also found significant regional differences: the average bid premium in North America in their 1998 – 2012 sample is 29 % and 20 % in Europe.

The risk in merger arbitrage –

risk of deal failure

As seen in the example above, deal failure can have a significant impact on the profitability of the respective position in the merger arbitrage portfolio. Failure to close a transaction usually does not have much to do with the broader market environment, but rather with very specific risks instead.

Accordingly, each transaction is independent from the other and the risk of large drawdowns for a merger arbitrage strategy can be reduced by diversifying the investment over a large set of M&A transactions. The reasons why M&A transactions fail can be grouped into the following categories: • Shareholder resistance: target or acquirer

shareholders, board of directors or the

management team might reject the acquisitions (e.g. hostile vs. friendly takeover).

• Regulatory / legal opposition: competition authorities/industry bodies or governments can reject the acquisition.

• Change in market conditions and/or financing:

the buyer can no longer finance the transaction due to a tightening of the borrowing conditions. • Major events: poor quarterly results, regulatory

changes, or due diligence reveal problems at the target company which have an impact on valuations.

Historically, the deal failure rate has fluctuated between 2 % and 13 %, with a plateau of over 20 % for several months in the US and Canada during the financial crisis in 2008 – 2009. The average failure

rate in Europe is 8.3 % based on data from 1998-2013. Specifically, some deal parameters have been identified that have an impact on the failure rate.4 They are as follows:

• Hostile takeovers are far more likely to fail (30 % vs. 5.9 % failure rate)

• Private equity deals are more likely to fail than strategic deals (15.3 % vs. 6.1 % failure rate) • Deals with an initial arbitrage spread between

5 % and 10 % have the lowest failure rate (3.4 % vs 10.6 % of deals with a spread between 15 % and 20 %)

• Deals with small acquirers (in relation to the targets) have higher probabilities of failure(17 % failure rate where acquirers are smaller than targets vs 4.2 % where acquirers are five times the size of the target)

Actively considering these parameters during the deal selection process and carefully constructing diversified portfolios can considerably reduce the likelihood of deal failure and reduce the drawdown potential of merger arbitrage strategies.

Merger arbitrage strategies provide

diversification potential

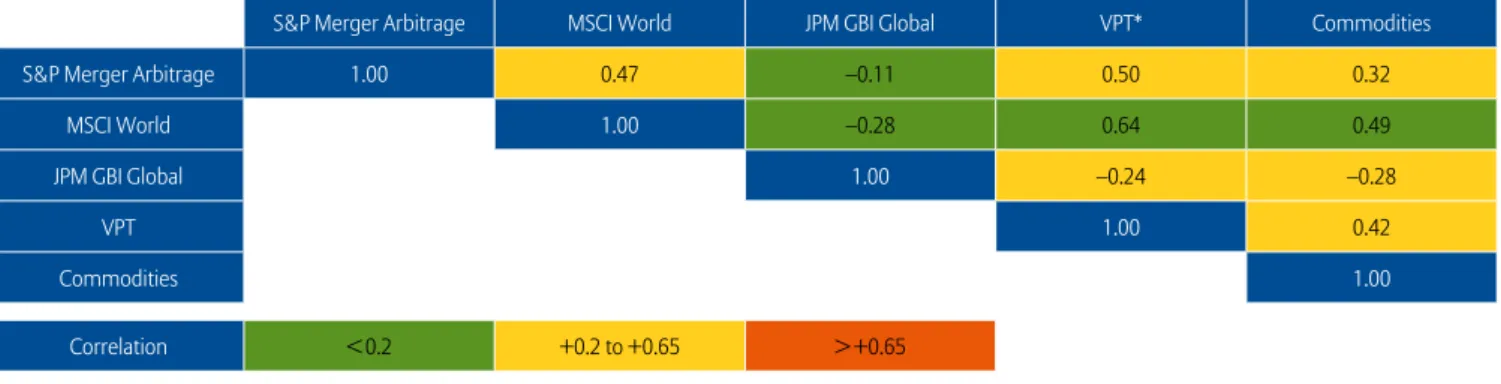

As merger arbitrage strategies are primarily dependent on deal risk, they show low to moderate correlation with broader equity markets. Compared to other asset classes, they display attractive diversification potential that investors can explore (see Figure 3).

Figure 3: Correlation analysis of monthly returns shows diversification potential of merger arbitrage strategies

S&P Merger Arbitrage Index from 31/01/2006 – 31/08/2015

S&P Merger Arbitrage MSCI World JPM GBI Global VPT* Commodities

S&P Merger Arbitrage 1.00 0.47 –0.11 0.50 0.32

MSCI World 1.00 –0.28 0.64 0.49

JPM GBI Global 1.00 –0.24 –0.28

VPT 1.00 0.42

Commodities 1.00

Correlation < 0.2 +0.2 to +0.65 > +0.65

Sources: Bloomberg, Allianz Global Investors. Calculation based on monthly total returns from Bloomberg. The VPT Index represents the Variance Premium Trading IndexTM

developed by risklab GmbH. risklab GmbH is a subsidiary of Allianz Global Investors. Past performance is not a reliable indicator of future results.

4 See Cretin, Bouacha,

and Dieudonné (2010) and (2013).

In market downturns, the correlation between merger arbitrage strategies and broader markets can increase, which is mainly caused by index ETF providers or risk-averse investors who will sell index constituents indiscriminately, even if they are subject to a takeover bid. As the macroeconomic environment for M&A transactions might become less favourable during market downturns, the risk of deal failure may increase as well. Furthermore, transactions that involve a stock-for-stock or other hybrid forms of payment can increase the correlation with the markets and cause higher levels of volatility because of their sensitivity to the target and acquirer share price.5

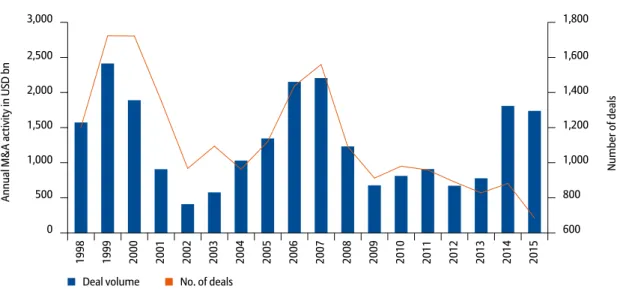

Large opportunity set available in

M&A market

The current M&A market environment is very buoyant and provides merger strategies with a large pool of investable transactions from which the arbitrage spread can be extracted. Because of an upturn in strategic activity (i.e. non-private equity) due to strong corporate balance sheets and high CEO confidence, the M&A market may be moving back towards the peaks of 2007 (see Figure 4). This trend is expected because companies still have large amounts of cash available to fund corporate activity. Moreover, inorganic growth via acquisitions is an excellent way of improving earnings.

Understand. Act.

• In light of a low-yield environment and relatively expensive equity markets, risk diversification with conventional assets has become increasingly difficult. Investors are therefore increasingly looking towards unconventional but liquid risk premiums, such as the M&A arbitrage spread, which can provide both attractive returns and diversification potential.

• Merger arbitrage refers to an investment strategy that aims to systematically extract the arbitrage spread from markets – i.e. the difference between the target’s share price and the offer price – by investing in diversified portfolio of takeover targets shortly after the announcement of the M&A deal.

• The upside for the investor in merger arbitrage strategies equals the arbitrage spread of the portfolio of takeover targets. However, if one deal fails or a transaction is withdrawn, the downside for this single position can be significant. Constructing diversified portfolios of a number of different takeover targets can considerably reduce the likelihood of deal failure as well as the impact of one failed transaction on the profitability of merger arbitrage strategies, though. As merger arbitrage strategies are primarily dependent on deal risk they show little correlation with broader equity markets. Compared to other asset classes they display attractive diversification potential that investors can explore.

• The current M&A market environment is very buoyant and provides merger strategies with a Sources: Bloomberg, Allianz Global Investors. Included are transactions where the target is a public company, the value of the transactions is known and where the acquirer holds less than 50 % of the target’s shares before the transaction and seeks more than 50 % with the transaction.

Figure 4: Breakdown of M&A transactions per annum

3,000

2,000 2,500

1,500 1,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Deal volume No. of deals

Annual M&A activity in USD bn

Number of deals

500 0

1,800

1,400 1,600

1,200 1,000 800 600

5 To extract the

arbitrage spread in stock-for-stock transactions, long positions in the target and short position in the acquirer have to be set up. Glans and Vo (2013) find that both value- and equal-weighted portfolios of stock-for-stock transactions experience significantly higher levels of volatility than portfolios of cash transactions.

Imprint

Allianz Global Investors GmbH Bockenheimer Landstr. 42 – 44 60323 Frankfurt am Main

Global Capital Markets & Thematic Research Hans-Jörg Naumer (hjn), Ann-Katrin Petersen (akp), Stefan Scheurer (st)

Allianz Global Investors

www.twitter.com/AllianzGI_VIEW

Data origin – if not otherwise noted: Thomson Financial Datastream.

Calendar date of data – if not otherwise noted: October 2014

Literature:

1) M. Baker and S. Savasoglu (2002). Limited arbitrage in mergers and acquisitions. Journal of Financial Economics.

2) M. Mitchell and T. Pulvino (2001). Characteristics of Risk and Return in Risk Arbitrage. Journal of Finance, vol. 56, no. 6 (December): 2135 – 2175. 3) A. Shleifer and R. Vishny (1997). The Limits

of Arbitrage. Journal of Finance, vol. 52, no. 1 (March): 35 – 55.

4) G. Jetley and X. Ji (2010). The Shrinking Merger Arbitrage Spread: Reasons and Implications. Financial Analysts Journal (66 / 2). Pages 54 – 68. 5) F. Cretin, S. Bouacha, S. Dieudonné: Risk Arbitrage,

a probabilistic approach over 1998 – 2010 in the US and Canada. SSRN. October 2010

6) F. Cretin, S. Bouacha, S. Dieudonné: MAGMA Europe, a tool to analyse the European M&A market. SSRN. October 2013

7) C. Glans and P. Vo (2013). Merger Arbitrage Opportunities left for financial mavericks in the new millennium?

References to specific securities are not intended to be, and should not be interpreted as an offer, solicitation or recommendation to purchase or sell any financial instrument, an indication that the purchase of such securities was or will be profitable, or representative of the composition or performance of any AllianzGI product. Any such references are only made to illustrate the concept of merger arbitrage.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered

Active Management

→ “It‘s the economy, stupid!”

→ The Changing Nature of Equity Markets and the Need for More Active Management → Harvesting risk premium in equity investing → Active Management

Alternatives

→ Volatility as an Asset Class

Financial Repression

→ Shrinking mountains of debt → QE Monitor

→ Between a flood of liquidity and a drought on the government bond markets

→ Liquidity – The Underestimated Risk

→ Macroprudential policy – necessary, but not a panacea

Strategy and Investment

→ Equities – the “new safe option“ for portfolios? → Dividends instead of low interest rates

→ “QE” – A starting signal for euro area investments?

Capital Accumulation – Riskmanagement – Multi Asset

→ Smart risk with multi-asset solutions

→ Sustainably accumulating wealth and capital income → Strategic Asset Allocation in Times

of Financial Repression

Behavioral Finance

→ Behavioral Risk – Outsmart yourself! → Reining in Lack of Investor Discipline:

The Ulysses Strategy

→ Behavioral Finance – Two Minds at work