European Cluster Mapping Project “Identifi-cation, analysis, and monitoring of business clusters in Europe”

Case study for the Commission of the Euro-pean Communities Enterprise and Industry Directorate-General*

22 January 2008

*The opinions expressed are those of the authors, the con-sultancy Competitiveness (www.competitiveness.com ), and do not represent the Commission's official position.

Table of contents

1. Objectives of the case studies ... 4

Addressing the European innovation gap ... 4

Understanding if clustering efforts are helping to close the gap... 4

Why the Irish example can be useful... 4

2. The clustering effort in the Ireland shared services cluster6 Description of the activity and context ... 6

The Shared Services Cluster in Ireland ... 8

History of success ... 8

The favourable factors that led to success in Ireland ... 10

The Challenge of Low Cost Competition ... 12

Responses to the Challenges... 13

Strategy ... 13

Structure ... 15

Actions ... 16

Implications of Actions ... 16

Measuring and Evaluating Results ... 18

3. Have the clustering efforts been a driver for innovation in the Irish shared services cluster? ... 21

Contribution to the development of lead markets... 21

Help in focusing R&D&I resources ... 21

Contribution to an increased mobility of knowledge ... 21

4. Successes and failures of the clustering efforts in the Irish

shared services industry ... 23

In defining the perimeter for the clustering effort ... 23

In setting the strategies to build a sustainable competitive advantage ... 23

In managing the clustering efforts jointly ... 23

In applying the learning to the whole economy ... 23

5. Bibliography ... 25

Table of figures

Figure 1 Location cost versus location quality positioning ... 81.

Objectives of the case studies

Addressing the European innovation gap

Many countries have intended position themselves on the market of shared services. Even though these shared services centres seemed to have a very autonomous activity within a territory where they are implemented, their development has a strong impact on the capacity of the region to develop high level services such as financial, HR, or IT services. In other words, they contribute in a positive manner to the increase of the qualification of their inhabitants and the competi-tiveness of the region. Thus these centres would prepare better the regions, where they were implemented to the shift to services activ-ity.

Understanding if clustering efforts are helping to close

the gap

The clustering effort performed by the member of the shared ser-vices cluster in Ireland during the 80’s and 90’s was first the result of a necessity: the necessity to continue to deliver high-level services to their client usually the large headquarters in the US. The quality of their services was jeopardized by the scarcity of the human re-sources and its consequence on their cost. So the first efforts of the members of the cluster were first focusing on increasing the visibility of the shared services centres in Ireland in order to attract more peo-ple to come to work with them. After having experienced successful actions in this field, they could work together on the ways to improve their productivity. These efforts definitely contributed to create a cul-ture of services in Ireland and thus favouring the entrance of Ireland in the knowledge economy.

Why the Irish example can be useful

Ireland serves as a valuable case study to illustrate how large the payoffs can be from better economic policies in the presence of fa-vourable external factors. The lessons learned may have particular relevance for smaller countries and for regions within larger ones, where the dependence on “external markets” is extremely high and monetary policy in large part is determined elsewhere. After the

suc-cessful experience in services centre, Ireland is now evolving to-wards more specialized strategic activities in Life Science for exam-ple. This way they are applying their experience in dealing with com-plex processes in even higher level.

2.

The clustering effort in the Ireland

shared services cluster

Description of the activity and context

Shared service centres allow companies to combine back office processes in order to achieve increased efficiency and higher quality services. The functions often included are finance and treasury, cus-tomer support, human resources, IT and IT support, supply chain management and purchasing. With standardisation, there are more opportunities to automate, capitalise on technological innovations, and realise cost savings. This activity originally started in the US be-fore to be implemented as well by US companies in their European subsidiary.

According to Oxford Intelligence the main driver for the multinational companies to choose one city from another to implement their shared services centres are the following:

Availability of qualified people

Grants and incentives

Labour costs

Property costs

Established corporate presence

Tax issues

Communications and infrastructure

Quality of life

It has been estimated that the shared services market is the fastest growing segment of the IT service sector. It is expected to increase 40% from $112.1 billion in 2005 to $144 billion in 2008, by 2008 will account for 22% of all IT services revenues globally.TP

1

PT

Some of the attributes of a shared service operation are (independ-ently of whether it is internal or outsourced):

It operates as a stand-alone organisation,

TP

1

PT

It is process-oriented and focuses on specific activities within processes,

It is driven by market competitiveness as their organisation is focusing on delivering services that were not traditionally a real priority in a competitive way with the same constraints than producing a “product”.,

It leverages technological investments,

It focuses on continuous improvement.

Through consolidation and standardisation, the shared service cen-tres in Ireland typically achieve cost savings of 30% to 40% with a pay back period between two and three yearsTP

2

PT

.

3 successive waves of countries that have all evolved similarly but with differences in time can be identified.

Ireland was the first European country to propose such services because of a combination of factors such as: being culturally close to the US decision makers or being one the lowest cost country of the EU, etc.

Then other European cities deployed efforts to attract this activ-ity, such as Amsterdam, Madrid, Barcelona, Copenhagen. The general conditions were to have a qualified work force espe-cially in language and at a relatively low cost.

Another wave of smaller cities around Europe joined them such as Bordeaux, Belfast, Maastricht, Newcastle and indented pro-posing such administrative services.

Later in the 90’s as these cities developed their services and increased the quality and thus their cost, they let space for a third wave of low cost cities outside of Europe to enter the mar-ket such as: Bangalore, Tallinn, Bratislava, Budapest, Lisbon, Prague, Kuala Lumpur, Johannesburg, etc.

So after profiting of the first mover advantage by having a clear lead-ership, the position of Ireland in this sector has been challenged strongly by different actors around Europe and Asia.

TP

2

PTShared Services: how Irish shared services centres are adding value by

In February 2004, the different shared service regions have been ranked by the Oxford Intelligence as illustrated here below:

Figure 1 Location cost versus location quality positioning

Today, the competitive advantage of Ireland in the shared services sectors is constantly challenged by other regions, but Ireland has been using its supremacy to capitalize and react accordingly propos-ing higher value services before the others.

The Shared Services Cluster in Ireland

History of successIn 1978, Apple located its European manufacturing headquarters in Cork. Raw materials were imported to Ireland, assembled into com-puters, and then shipped to customers in Europe. Over time, most of the raw materials began to be sourced from Ireland and Europe. Ap-ple located a full printed circuit board (PCB) manufacturing facility at its Cork site. In the mid 1980s through the mid 1990s, the building PCBs and systems was subcontracted in order to leverage subcon-tracting capacity and maintain cost competitiveness.

This was part of a larger trend that started when Digital Equipment Corporation established a mini-computer manufacturing facility in Ireland, followed by Amdahl, Apple, Wang and others. Most were similar to Apple in that they were just sub-assembly plants. Raw ma-terials were sourced from elsewhere and often final assembly was done in other countries as well.

The Irish Industrial Development Agency (IDA) actively solicited for-eign investment. This was a big reversal after a long history of

pro-tectionism. The United States was the primary target for cultural and language reasons. IDA frequently offered substantial incentives such as capital grants, ready-made facilities, training and research and development grants. This was often a source of controversy. In 1982 report, the government found that the IDA’s promotion activities were “overly generous towards multinationals – relative to what was needed to attract them – and providing the wrong kind of incen-tives.”3 Furthermore, there were few penalties for firms that did not meet their projections for employment or outsourcing to Irish firms. In the mid-1980s, IDA began to shift away from industries requiring capital-intensive investment, such as chemicals and pharmaceuti-cals, to service-oriented industries such as software and data proc-essing. By 1985, IBM, Lotus and Microsoft had also made

invest-ments in Ireland. In the 1980s, IDA also became an active lobbyer for

telecommunica-tions reform and upgrading. From 1979 till 1987, with the pressure of the IDA, the government succeeded in improving “to such a degree that it is now a major contributing factor to present day successes in wooing foreign firms to our shores” as said in the Daily Parliamentary Debates on May 24th, 1988. Most countries traditionally charge higher rates on international calls to subside domestic service. Tele-com Eireann, on the other hand, offered highly Tele-competitive rates on international services. By 1987, Telecom Eireann installed digital switching throughout the country and began laying optical fibre lines. Between 1985 and 1991, Ireland exceeded the average OECD de-cline in international call rates of 3% with a 28% dede-cline. By 1994, charges for leased lines for business were half the OECD average.4 IDA also encouraged the regional technical colleges to emphasize electrical engineering and IT in order to deliver on promises being made to companies like Apple. By 1993, Ireland led the OECD on the share of science and technical graduates in the 24-35 age group of the labour force.5 Modern languages were also emphasized at the secondary level.

3 “Why Ireland Boomed” by James B. Burnham in The Independent Review 4

“Why Ireland Boomed” by James B. Burnham in The Independent Review 5 OECD, Communications Outlook 1999

The consequences of these decisions were the transformation of Ireland into a country with low tax, a good infrastructure, a qualified workforce and a favourable image among the US decision makers. These elements provide an excellent location for pan-European op-erations. So when the US headquarters were considering consolidat-ing their administrative services into one location for Europe, Ireland won most of their votes. This is illustrated by several methods: first the traditional emigration stops in the mid-90’s and for the first time since the early 70’s, a sustained inflow occurred as job opportunities in Ireland became abundant. Then if we look further in the type of sector that benefited most of the growth we observe that more than 165,100 jobs were created between 1987 and 19976 in the “market services” (which exclude government, health and education employ-ments). That represents a 37% increase in which much of the growth - perhaps 75% - was internationally mainly in the shared services centres.

Forfas, the national policy and advisory board for enterprise, trade, science, technology and innovation, as well suggested that nearly 70% of employment gains in the 1990s took place thanks to the US and global investment boom. The Celtic Tiger was born.

The favourable factors that led to success in Ireland

Ireland has benefited of several favourable conditions simultaneously in order to attract shared services sector to the territory:

Ireland benefits of the most attracting taxation conditions in Europe with a company tax at 12,5%. This has obviously contributed to at-tract shared services centres in the country. In addition, the decision to spend 20% of public budget on education has contributed to raise the level of services provided.

Demand Conditions

During the 70’s, the first companies to implement the concept of con-solidated services were the US based, culturally related to Ireland. The US companies constituted the main source of clients for this ac-tivity in Europe. Later, when the consolidation process were decided to be applied in Europe, most of the large groups were already hav-ing closed links with Ireland through their manufactures. We should

note as well that the chance of Ireland is as well due to the fact that a lot of decision makers of these large US group were of Irish origin. Later Ireland kept its attraction as being the only English speaking country in the EU and using the Euro.

Factor Conditions

Like the demand factors, the local factor conditions were favourable to attract these kinds of foreign investments due to the availability of young overqualified workforce ready to work for a modest salary, the key for the successful development of a shared services centre. Dur-ing the 80’s, Ireland was still at the bottom rang of Europe’s eco-nomic ladder and the unemployment rate was hitting some 19%. The advantage of having a flexible and qualified workforce has survived during more than 20 years as the area has succeeded in attracting young students from all over Europe to work in these centres with the promise of finding a job easily combined with a relatively low cost of living. Ireland was chosen the best country to live according to Economist Intelligence Unit’s Quality of Life Index for 111 countries. This quality of life is as well profiting to the shared services cluster as it makes their task of attracting foreign young workforce easier. Today Ireland is still having the youngest population in Europe with 40% under 25 years. According to IMD World Competitiveness Year-book 2005, Ireland has the most flexible, adaptable, motivated work-force out of 60 economies surveyed. It is the only English speaking country in the Euro zone and 65% of secondary school students and 18% of tertiary students study a foreign language.

Firm Strategy, Structure and Rivalry

In fact, the shared services centres are completely dedicated to in-crease the productivity of their employees and the level of service delivered to their collaborators and customers all around the world. This continuous pressure to innovate has greatly contributed to force these centres to develop exceptional competitiveness that has spilled over other sectors in Ireland. This, from more global perspective, has also prepared the evolution of the developed economies towards the services.

Related and Supporting Industries

Considering the related and supporting industries of the shared ser-vices sector, as these centres are more in contact at the international

level rather than with their immediate environment, very often the suppliers have been chosen directly by the headquarters in the US and not in function of the local capabilities. Still the technological requirements are extremely high so that the productivity of the em-ployee is optimized and the presence of Microsoft, Dell and Apple from very early on has insured the presence of qualified work force to deploy the technological solutions within the shared services cen-tres. In addition we have to note that Ireland benefits of one of most advanced telecom networks in Europe with the lowest annual rental for international leased lines and the lowest cost in Europe for in-bound international toll-free services, thanks to the aggressive price policy of Telecom Eireann. The decrease of the cost of telecommuni-cation during the 90s contributed greatly to the consolidation of the service in one location. These elements are as well key drivers for the location of the implementation of a centre. The telecom budget represents about 10% of a budget of a centre.

In addition to these favourable conditions, we should as well con-sider that Ireland benefited from the first mover advantage. In this sector, being able to demonstrate to newcomers the success of pre-vious experiences has played an important role. It has generated the venue of numerous followers.

The Challenge of Low Cost Competition

During many years, Ireland and the Dublin shared services cluster had benefited disproportionately from the “death of distance”7 and the digitization of the information by investing very early on their tele-communication infrastructure. But, the phenomenon started rapidly benefit to other countries.

The sector’s main driver is low costs as the shared service compa-nies act as a cost centre for the headquarters. 80% of the costs are spent in human resources, and the availability of qualified human resource at a low cost is a key success factor. The other 20% is spent in infrastructure and ITC. So while Dublin became more and more attractive for multinational investments, the demand for shared services accelerated and the shared service centres started to lack low cost employees, making it difficult to fight with low prices. This was the problem that confronted Dublin and Cork as they

fully attracted many shared services centres such as Pfizer, Black & Decker, Microsoft, Accenture, Wirlpool, etc.

In the mid-1990s, Ireland began to face competition from Eastern Europe and Asia, which could offer greater scale and lower cost. These regions started to challenge the position of Irish centres by offering mainly lower cost and a qualified workforce and available. Sector per sector, regions intended to take market share away from Ireland: Bangalore for the IT support, Prague, Bratislava for account-ing, Amsterdam, Barcelona for the customer relationship to name a few. These countries inspired by the Irish example reoriented their efforts that were directed towards attracting manufactures into at-tracting shared services centres. And they did it with a notable suc-cess.

Besides within Apple after a strategic assessment in 1998, the manu-facturing of Printed Circuit Boards (PCB) was moved to Indonesia, portable product manufacturing to Taiwan, and low-end desktop manufacturing to the Czech Republic. Employment at the Apple’s Cork facility dropped from 1,500 to 500 people. This move signal the start of the decline of the manufactures of Ireland to low cost coun-tries and put even more pressure on the services centres as they were identified as the relay of growth of Ireland. This was a negative challenge for the industrial activity at that time but it gave a addi-tional positive kick off to the shared services cluster.

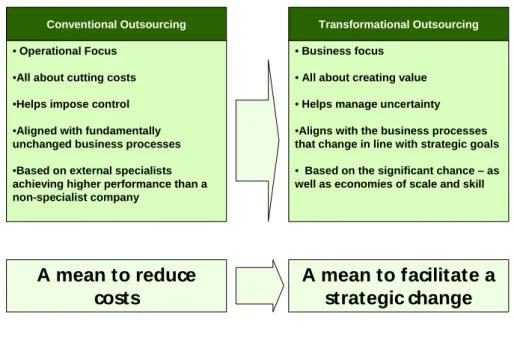

Observing these difficulties, the shared services centres together with the public sector players (IDA, Enterprise Ireland and Forfás) had to encounter the way to evolve and offer alternative that other regions could not offer. The chosen strategy was to transform the shared services centres from “cost centres” to “profit centres”, de-tailed in the following chapter.

Responses to the Challenges

StrategyIreland’s strategy to move towards higher-value activities, in other words from basic manufacturing to shared services and again from shared services to added-value shared services (see the Figure 2 below) benefited fully from the inherent factors presented in the first

chapter: the demand coming from the US, the availability of qualified workforce at a low cost, a good telecom infrastructure, the continu-ous pressure to increase the productivity of the centres that forced them to improve and innovate, the low tax rate and finally the high quality of life.

Each of these elements played a positive role and permitted the pro-vided services to evolve. At the beginning, the shared services cen-tres were processing such operations as insurance claims and magazine fulfilment. By the late 1980s, the economics of interna-tional call centres for marketing, technical assistance, and regular servicing to customers such as reservation appeared. The long term vision then became clear: The shared services centres should evolve from cost centres to autonomous profit centres.

Under constant pressure, the shared services operations increased their levels of quality and service and at the same time added further value to their organisation by bringing other activities such as HR, administration, sales order processing, strategic procurement sup-port and contract management ... Increased regulatory and control requirements such as Sarbanne Oxley have presented new chal-lenges and opportunities for these actors. The challenge of moving up the value chain and embracing activities that were traditionally reserved to the headquarters permitted these shared services cen-tres to resist to the competition. Ultimately by working at more and more complex and strategical services, they successfully attracted EMEA decision centre. They even directly attracted strategic centres like the EMEA headquarters of Microsoft or Dell.

Conventional Outsourcing

•Operational Focus •All about cutting costs •Helps impose control •Aligned with fundamentally unchanged business processes •Based on external specialists achieving higher performance than a non-specialist company

Transformational Outsourcing

•Business focus •All about creating value •Helps manage uncertainty •Aligns with the business processes that change in line with strategic goals •Based on the significant chance – as well as economies of scale and skill

A mean to reduce

costs

A mean to facilitate a

strategic change

Figure 2 Trends of the shared services

Structure

In 1998, was established under the initiative of Whirlpool and the IDA the first “Shared Service Forum”: Its objective was to create a space where the companies and the administration could exchange on the issues they were facing via regular meetings, specific studies and a web. This initiative was created first to deal with the impressive growth of the sector and this forum became the main tool that permit-ted to all the actors to exchange on operational issues such as proc-esses and quality management, regulation especially on the use and protection of the data bases, European legislation, project manage-ment, staff recruiting, training, use of effective technology like VOIP or CRM, etc.

This informal structure of the Shared Services Forum financed by both IDA and the private sector has allowed an open communication between the members and allowed them to share specific issues and raise the level of their services all together.

One of the motivations of the members of this association and what made its success is to resist and innovate rapidly in front of the strong market forces that are threatening them: Namely the cost competitiveness of Eastern Europe and Asia and the smarter use of technology to automate activity.

Actions

Beyond the specific actions that have had the opportunity to take place within the Shared Services Forum, the main drivers of the boom of the shared services centres in Ireland are macroeconomic decisions taken by the government coupled with the technological revolution that was well exploited. Furthermore the common under-standing of the shared services centre of the strategy to added-value services made the rest.

The decisions taken by the government during the 80’s:

To invest in education by expanding the Regional Technical Colleges (RTCs) as well as to construct new universities,

To invest in telecommunication as the network was completely renewed from 1979 till 1990,

and to cut tax and generally to improve spending policies that encouraged investment and work

under the active advice of IDA, have prepared the ingredients of the future and dazzling success. Other actions, such as the exploitation of the links including the cultural links between the US leaders and Irish have as well played a role, and again IDA has its shared of the success.

These actions combined with the technological discontinuity, which brought down the cost of telecommunication and the digitalization of the information favoured specifically the development of shared ser-vices activity in Ireland. Ireland was best prepared at that time to profit of this radical change first. Then the creation with Whirlpool of the Shared Service Forum permitted to communicate the vision of the future of the sector and foster innovation within the shared ser-vices centres.

Implications of Actions

IDA Ireland is the agency responsible for industrial development in Ireland. The agency was founded in 1949 as the Industrial Develop-ment Authority and placed on a statutory footing a year later. During the 60’s the authority changed its role greatly and took a central role in reform and industrialisation of the economy. In 1994 the authority

became the Industrial Development Agency (Ireland) or more com-monly, IDA Ireland.

Today IDA Ireland is responsible for the attraction and development of foreign direct investment in Ireland. The promotion of Irish compa-nies is the responsibility of Enterprise Ireland and national policy and advisory matters are handled by Forfás. These agencies are respon-sible to the Minister for Enterprise, Trade & Employment in the Irish Government.

In recent years many countries and regions have created industrial development authorities modelled on the agency to encourage for-eign direct investment and economic growth.

Being well prepared to take advantage of this technological disconti-nuity was largely the happy result of prior decisions centred on edu-cation and telecommuniedu-cation investment, combined with signifi-cantly improved government tax and spending policies that encour-aged investment and work.

These decisions were largely piecemeal and driven more by pragma-tism than by a widely shared consensus on redefining the role of government. Historical trends and decisions also contributed to Ire-land’s propitious preparation: demographic patterns, the legacy of English law and language, and a series of decisions going back to the 1950s that opened the economy to foreign trade and investment and culminated with entry into the Common Market in 1973.

When Ireland joined the EU, it was one of the poorer members, and much has been made of the country’s access to the EU’s various transfer programs. As illustrated below, these transfer represented up to 6.2% of the GDP in 1991.

Figure 3 Net receipts from European Union, 1973-200 as Percent of GDP

However, a recent study of the overall impact of “structural” EU transfers in 1990s concluded that their contribution to income growth was lower than one percentage point a year8.

Measuring and Evaluating Results

As an illustration of the results of the clustering effort

Pfizer has located its financial shared services in Dublin. This centre combines the financial processing activities of nineteen European countries into one single-platform, including services like reconciling bank account, short term cash management, preparation of all VAT and transaction based tax return, credit card administration, reconcil-ing profit and loss accounts.

Accenture employs over 300 people in Dublin to provide internal ser-vices at European level such as general accounting, billing, cash management, HR, customer relationship management and IT ser-vices that were previously performed in 16 different European coun-tries.

Whirlpool has located its financial centre in Dublin to provide general accounting, fixed asset/inventory accounting, account payable and

8 Barry, Breadley, and Hannan 1999,114

reporting consolidation among other services to its European branches.

Microsoft has first implemented its European Operations Centre in 1985, now it employs now 1500 people and provides key support for company sales and customer support activities across 85 different countries. Microsoft European Product Development Centre is also located in Ireland as well as Microsoft Sales and Marketing.

Hertz first implemented its financial shared services centre in 1998. Today the company employs a total of 1,197 people between its res-ervation centre, its financial services centre and its customer support services.

UPS implemented its customer service contact centre first in 1995 in Tallaght then a back-office data processing facility in Ballymount. Today they employ 650 people.

IBM is the pioneer in ebusiness solution. They now employ more than 3,500 people in Dublin providing Marketing, sales support, and technical support to 28 countries in EMEA.

Oracle opened their first office in Ireland in 1997 then implemented successfully there their first model of telesales operation outside of the USA to service the entire EMEA region. Oracle Ireland now em-ploys 900 people.

At last Apple’s Cork management team was successful in marketing the benefits of Ireland. In 1998, all of Apple’s European financial ac-counting functions were centralised at Cork. In 1999, they added ca-pability for manufacturing computers with customized configurations for the European market. In 2000, the decision to outsource technical and customer support and back office functions was reversed and the European call centre was moved back to Apple’s Cork facility. This facility incorporates the following activities: Telesales (Inbound and Outbound Calls), treasury and supply chain management, back office accounting support for accounts payable, intercompany ac-counting and fixed asset acac-counting among others.

In 2003, Apple’s European Operations Headquarters employed ap-proximately 1,200 people, 15% of which are engaged in manufactur-ing and 85% in value-added activity.

Cathy Kearney, Senior Director, European Operations, Apple Ireland mentioned "We have taken a lot of functions and processes into this facility that were previously all over Europe. Our move up the value chain is due to our success at integrating all of these into a world-class, lean, cost-effective model that really adds value."

According to the European Cluster Observatory, the shared services cluster is present in business services as well as IT and financial services companies so that it is difficult to evaluate its size. The fol-lowing table presents the current data on these activities in Ireland.

NUTS II REGION

CLUSTER

CATEGORY EMPLOYEES SIZE SPEC FOCUS STARS

Ireland Business

Services 39 237 0,91% 1,05 2,47% 0

Ireland IT 30 353 1,48% 1,71 1,91% 1

3.

Have the clustering efforts been a driver

for innovation in the Irish shared

ser-vices cluster?

Contribution to the development of lead markets

This case is an illustration of the apparition of services cluster on a market that did not exist in Europe before the 80’s. Only the US large companies were consolidating their activity in a central place. The investments made by the government under the wise advices of IDA in education and in telecommunication combined to their geographi-cal favourable factor (being part of Euro, English speaking popula-tion…) has contributed greatly to the apparition of this new shared services market successfully in Ireland. In addition the success of Ireland in shared services has contributed to the implementation of other knowledge intensive services activities even more innovative such as R&D centres in Life Science.

Help in focusing R&D&I resources

The decision taken by the Irish government to invest in education by expanding the Regional Technical Colleges (RTCs) as well as the pressure that was continuously exercised by the competition’s cen-tres to increase their productivity has forced the cencen-tres to improve their it infrastructure and the sophistication of their solution. Thus the investment done in R&D in IT in order to increase the productivity of their employees has been important. We can illustrate the success of these investments by mentioning that today the European headquar-ters of Apple and Dell are in Ireland as well as the product develop-ment centre of Microsoft.

Contribution to an increased mobility of knowledge

The results of this combination of favourable factors on Irish soil are impressive: during the 90’s Ireland has successfully attracted the shared services centres (back office) or contact centres (front office) from the main US multinational across all sectors (see the examples below). In 1988, more than 40,000 Irish were emigrating whereas after 1997, Ireland was facing a net migration of more than 20,000 people per year. By 2001, the Irish economy was in effect operating

at full employment, less than a decade after rates of joblessness had been among the highest in the EU. The recorded unemployment rate of 3,7% for 2001 represented little more than “frictional” unemploy-ment, as individuals moved between one job and the next.

Reinforcing entrepreneurship in the area

As the shared services centres are for most of them constituted of branch of multinational groups that are consolidating their activity, it is difficult to evaluate any impact on the entrepreneurship. It is fair to say that the majority of the jobs created within this cluster are not issued by entrepreneurs but by the multinational when they are opening and growing their own shared service centres. The entre-preneurship might have benefited of secondary effect of the shared services though.

4.

Successes and failures of the clustering

efforts in the Irish shared services

in-dustry

In defining the perimeter for the clustering effort

Defining the business of these industries as “shared services” is definitely a success. In fact it was not obvious as they were part of groups that were already belonging to other sector such as tourism (starwood), transportation (Hertz), IT (Apple) or finance (Amex). But they realized that they were facing similar challenge for there core activity, which was to assist international customers and created this new name for their business.

In setting the strategies to build a sustainable

com-petitive advantage

After answering to their first necessity, which was to access qualified and cheap labour, the member of the shared services forum actually defined their strategy to target advanced services (as explained be-low) together with the support of a consulting firm. This way they re-sponded to their challenge successfully in ad equation with a set strategy defined early on.

In managing the clustering efforts jointly

This case is as well an illustration of how the public administrations intervene successfully in the development of a specific business. They jointly with whirlpool develop the community of actors involved in the shared services. And they contributed greatly to the attractivity of the region for these kind of services.

In applying the learning to the whole economy

The lessons learned by the shared services centres in recruiting, in delivering complex services and in increasing the productivity of their employees and the visibility given to these capabilities by the cluster have benefited to the whole image of the economy of Ireland. So the

economy has greatly benefited of this cluster that could be consid-ered as one of the locomotives of Ireland.

5. Bibliography

“Why Ireland Boomed” by James B. Burnham

Ireland Country Profile by The Economist Intelligence Unit

“Ireland’s coming of Age with Lessons for Developing Countries” by Paul P. Tallon and Kennet L. Kraemer

“Services FDI and Offshoring into Ireland” by Frank Barry and De-siree van Welsum, 2005