Oil & Gas Exploration & Production

Morocco: Land Rush Leads to Drilling Surge

in 2013/2014

EQUIT

Y

RESEAR

C

H

GL

OB

AL

Laura Loppacher * Equity Analyst 44 (0) 20 7029 8276 lloppacher@jefferies.com Matthew Lambourne * Equity Analyst +44 (0) 20 7029 8705 mlambourne@jefferies.com Brendan Warn * Equity Analyst 44 (0) 20 7029 8670 bwarn@jefferies.com Iain Reid * Equity Analyst 44 (0) 20 7029 8691 ireid@jefferies.com Daniela Almeida * Equity Associate 44 (0) 20 7029 8258 dalmeida@jefferies.com * Jefferies International Limited Key TakeawayMorocco offshore emerged as one of the frontier exploration land grab hot spots in 2012 with numerous farm-ins, corporate acquisitions and new licence awards. This is expected to lead to an active drill program of 10+ wells in 2H13/2014. We believe new technologies and play ideas could unlock significant exploration upside in this Atlantic Margin region which has been largely overlooked for the past decade.

What’s causing all this fuss? Wide range of mid and large cap companies flocked to Morocco in 2012, planning active drill campaign of 10 or more wells. Companies which entered/increased interests in the region through licence awards, farm-ins and corporate acquisitions include: Chevron, Total, Kosmos, Cairn, Genel, Galp, Plafarm-ins and Chariot. The mid-caps are leading the charge for drilling, expected to kick off in 4Q13 and continue through 2014 with a multi-operator, multi-rig drilling campaign of at least 10 wells. We believe the well count could increase significantly in the event of any initial success. Scale: Friend and foe – licenced acreage is 2x entire US GoM. The entire licenced acreage position offshore Morocco is c.250,000km2, roughly double the size of the entire licenced US Gulf of Mexico. The average exploration licence is over 8,000km2 (over 2m acres), roughly the size of 360 standard GoM blocks. While this gives the advantage of very significant running room in the event of initial success, it also means drilling results read-throughs to other players is limited by the vast distances involved.

What are they targeting? Atlantic Margin Jurassic source rocks. Generally speaking, the companies are chasing the same Jurassic aged source rocks as other successful Atlantic Margin regions such as the North Sea and Canada and have been proven to exist in Morocco with the Cap Juby discovery. Some companies are also chasing source rocks that are believed to be more locally mature in the Cretaceous. Reservoir targets vary with the two primary plays being Jurassic aged carbonates in the shallower water and Cretaceous and Miocene aged channel/fans in the deeper water.

Who’s got exposure? Small caps with acreage include Chariot, Tangiers, Pura Vida, Fastnet, Serica, San Leon and Longreach. Of these, we see Pura Vida as the most attractive given its significant retained interest post farm-down with a carry on at least 2 wells. The mid-caps are largely the driving force behind the 2013/2014 drilling campaign and include Cairn, Genel, Kosmos and Plains. We like Cairn and Kosmos for their attractive valuations (trading at discounts to core SoP) with material upside potential which is not priced into the current valuations. Finally, large caps with exposure include Galp, Repsol, Total and Chevron. With the exception of Galp, we expect their drilling programs in 2015 and beyond. Attractive terms, indicative NPV over $10/bbl. Morocco has offered some of the most attractive terms available globally to incentivise investment. While we would expect tax creep over time if the region is successful, existing licence terms are protected with stabilisation clauses. Economics will be determined by size of discovery, water depths, reservoir quality and development plan but a Jubilee analogue in terms of costs and resource size could be worth $13/bbl at $100/bbl oil price.

In this note, we explore in detail: The geological fundamentals of the region, the recent licencing and corporate activity, the planned drilling program, the fiscal and regulatory environment and detailed assessments of each company's assets and plans.

We believe Morocco offers investors an attractive frontier exploration opportunity with a significant number of catalysts over the next 12-24 months.

Table of Contents

MOROCCO: LAND RUSH LEADS TO DRILLING SURGE IN 2013/2014 ... 3

Acreage map: Land rush in 2012/early 2013 ... 5

Summary of Licence holders, planned activities ... 6

10+ wells planned with multiple rigs, operators drilling ... 7

UNDERSTANDING THE ROCKS AND THE SCALE OF THE OPPORTUNITY ... 9

Basic geological setting ... 10

UNDERSTANDING THE POLITICAL AND COMMERCIAL ENVIRONMENT ... 11

Oil and gas regulation ... 12

Taxes ... 12

Indicative economics are attractive ... 13

Western Sahara dispute ... 14

Gas commercialisation? ... 15

COMPANY PROFILES... 17

Cairn Energy ... 17

Genel Energy... 20

Kosmos Energy ... 23

Plains Exploration & Pura Vida Energy ... 27

Galp Energia & Tangiers Petroleum ... 29

Chariot Oil & Gas ... 30

Chevron ... 32

Total ... 32

Repsol ... 33

San Leon Energy... 33

Serica Energy ... 33

Longreach Oil & Gas ... 33

Fastnet Oil & Gas ... 34

Morocco: Land rush leads to drilling

surge in 2013/2014

The offshore sector in Morocco has seen a recent surge in licencing and farm-in activity in 2012 with the entry or expansion of positions by Cairn, Genel, Kosmos, Plains, Galp, Chevron, Total and Chariot. The total area under exploration or reconnaissance licence is now over 250,000km2 (62m acres), or roughly 2 times the entire licenced

acreage in the US Gulf of Mexico (32m acres). In 2012 and 2013 to date alone, 84% of currently licenced acreage has had a change of ownership, either due to new licencing, farm-ins or corporate acquisitions. The players are now targeting a very active drilling program with 10 or more wells planned before the end of 2014, more than doubling the number of wells that have been drilled offshore since 2000.

Simplistically, the companies are targeting two primary play types, Jurassic aged carbonate shelf edge build ups and deepwater clastic channel/fan plays with sediments sloughed off the continent, largely in the Cretaceous but also some in the Tertiary. The primary source rock targeted is Jurassic in age, the same source rock that has proven prolific in other Atlantic Margin basins such as the North Sea and Canada and proven in Morocco at the Cap Juby discovery. There is also some potential for localised younger source rocks such as Cretaceous Cenomanian/Turonian.

The Jurassic carbonate play is the only proven play in Morocco but the very large volume potential sits in the deepwater fan plays.

For the purposes of this report, we focus on the offshore sector of Morocco only. There are a number of companies targeting both conventional and unconventional exploration onshore Morocco including Repsol, Anadarko, EOG, Vermillion, San Leon, Longreach, Circle Oil and Gulfsands. We will not address these onshore licences in this report.

Who’s got exposure to potential Morocco upside?

Small caps (up to $200m mkt cap): Includes Chariot, Tangiers, Pura Vida, Fastnet, Serica, San Leon and Longreach. Each of these have upside potential worth multiples of the current market cap if successful. With the exception of Chariot, all of these players are non-operated and have a carry on a portion of their planned program (seismic only for Fastnet, drilling of 1 well for Tangiers, 2 wells for Pura Vida, Serica, San Leon and Longreach). Of these small caps, we believe Pura Vida is the most attractively positioned given its significant (23%) retained interest with a carry on at least 2 wells. Serica, San Leon and Longreach all benefit from having both of the major play types in Morocco to be targeted on their blocks.

Mid caps ($1-10bn mkt cap): Includes Cairn, Genel, Kosmos and Plains. Each of these has an operated position and are targeting multiple wells in 2013/2014 although each is primarily targeting a different play type (Cretaceous reservoir, Jurassic source rocks for Cairn, Jurassic carbonates for Genel, Cretaceous reservoir and source rocks for Kosmos and Miocene reservoirs for Plains). We rate both Cairn and Kosmos as buys with both trading at discounts to core SoP with significant exploration upside not valued in current share price. Cairn’s core assets are cash, stake in Cairn India and North Sea developments, Kosmos’ core assets are its producing and developing assets in Ghana including Jubilee and the Tweneboa, Enyenra and Ntomme complex. We do not have a recommendation/target price for Genel (core assets in Kurdistan) or Plains (core assets in the US).

Large caps (over $10bn mkt cap): Includes Galp, Repsol, Total and Chevron. Galp is the only one of the large caps planning drilling in the near-term with 1 well planned before mid-14. Repsol has made a gas discovery but follow up drilling was disappointing. Total and Chevron have both taken large acreage positions and we expect seismic only in the next few years.

Over 250,000km2 licenced in

Morocco, 2x the entire US GoM Land rush in 2012/2013: c.85% of licence area saw changes in ownership – corporate acquisitions, farm-ins, new awards.

Two major play types targeted: Jurassic shelf edge carbonates and deepwater clastic channel/fans

Jurassic carbonates only proven play; Big volume upside is in the

channel/fan plays

Small caps: ‘Highest impact, highest risk upside’ – Chariot, Tangiers, Pura Vida, Fastnet, Serica, San Leon, Longreach

Mid-caps: ‘Material option value’ upside – Cairn, Kosmos, Genel, Plains

Large-caps: ‘Nice to have’ upside –

What could this exposure be worth?

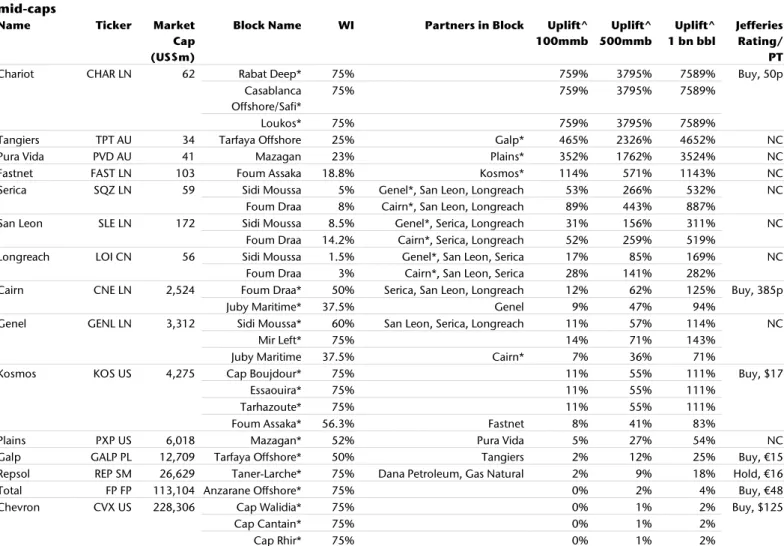

The table below shows estimates of potential upside for each of the companies for illustrative purposes of what a moderate (100mmb), large (500mmb) or very large (1 bn bbl) discovery could be worth unrisked relative to the current size of the company. Unsurprisingly, the smallest companies have the greatest relative exposure with Chariot, Tangiers and Pura Vida all having unrisked upside >10x the market cap in the event of a large discovery. A large discovery could be worth c.50% unrisked upside for our Mid-caps (Cairn, Genel, Kosmos and Plains) and up to 10% unrisked upside for our large-caps.

This table is for illustrative purposes only as it does not factor in any expected asset or equity level dilution, either pre- or post- drill and does not take into account the relative likelihood of a discovery in each block. It assumes a generic full cycle value of $7/bbl, less than what our modelling suggests a discovery could be worth if scale/costs similar to, for example, the Jubilee field in Ghana ($9-13/bbl at $100/bbl oil).

Table 1: Players targeting Moroccan upside: Transformative upside potential for small caps, material option value for mid-caps

Name Ticker Market

Cap (US$m)

Block Name WI Partners in Block Uplift^

100mmb Uplift^ 500mmb Uplift^ 1 bn bbl Jefferies Rating/ PT

Chariot CHAR LN 62 Rabat Deep* 75% 759% 3795% 7589% Buy, 50p Casablanca

Offshore/Safi*

75% 759% 3795% 7589% Loukos* 75% 759% 3795% 7589%

Tangiers TPT AU 34 Tarfaya Offshore 25% Galp* 465% 2326% 4652% NC Pura Vida PVD AU 41 Mazagan 23% Plains* 352% 1762% 3524% NC Fastnet FAST LN 103 Foum Assaka 18.8% Kosmos* 114% 571% 1143% NC Serica SQZ LN 59 Sidi Moussa 5% Genel*, San Leon, Longreach 53% 266% 532% NC

Foum Draa 8% Cairn*, San Leon, Longreach 89% 443% 887%

San Leon SLE LN 172 Sidi Moussa 8.5% Genel*, Serica, Longreach 31% 156% 311% NC Foum Draa 14.2% Cairn*, Serica, Longreach 52% 259% 519%

Longreach LOI CN 56 Sidi Moussa 1.5% Genel*, San Leon, Serica 17% 85% 169% NC Foum Draa 3% Cairn*, San Leon, Serica 28% 141% 282%

Cairn CNE LN 2,524 Foum Draa* 50% Serica, San Leon, Longreach 12% 62% 125% Buy, 385p Juby Maritime* 37.5% Genel 9% 47% 94%

Genel GENL LN 3,312 Sidi Moussa* 60% San Leon, Serica, Longreach 11% 57% 114% NC Mir Left* 75% 14% 71% 143%

Juby Maritime 37.5% Cairn* 7% 36% 71%

Kosmos KOS US 4,275 Cap Boujdour* 75% 11% 55% 111% Buy, $17 Essaouira* 75% 11% 55% 111%

Tarhazoute* 75% 11% 55% 111% Foum Assaka* 56.3% Fastnet 8% 41% 83%

Plains PXP US 6,018 Mazagan* 52% Pura Vida 5% 27% 54% NC Galp GALP PL 12,709 Tarfaya Offshore* 50% Tangiers 2% 12% 25% Buy, €15 Repsol REP SM 26,629 Taner-Larche* 75% Dana Petroleum, Gas Natural 2% 9% 18% Hold, €16 Total FP FP 113,104 Anzarane Offshore* 75% 0% 2% 4% Buy, €48 Chevron CVX US 228,306 Cap Walidia* 75% 0% 1% 2% Buy, $125

Cap Cantain* 75% 0% 1% 2% Cap Rhir* 75% 0% 1% 2%

Note: * denotes operatorship, assumed current working interest in blocks, does not adjust for anticipated farm-downs. Unless otherwise stated, ONHYM (State Oil Company) has a 25% WI which is carried during exploration.

^Uplift assumes $7/bbl, 10% risked currently in current mkt cap, no equity or asset level dilution required to achieved fully derisked valuation.

Source: Jefferies estimates

Chariot, Tangiers, Pura Vida all have unrisked upside 10x current mkt cap.

Cairn and Kosmos both trading below Jefferies core SoP with material upside potential not priced into current share price.

Acreage map: Land rush in 2012/early 2013

The map below shows the acreage position of each company and the table below provides key information on activity on the licence to date and what is planned for the block in the short to medium term. The total licenced area is c.2x the total licenced acreage in the US GoM.

84% of all of the licence area in Morocco has seen a change in ownership in 2012 and 2013 to date, either from new licence awards (including most notably Chevron and Total’s large positions), farm-ins (including most notably Cairn, Genel, Plains, Galp and Kosmos) or corporate acquisitions (Cairn, Genel).

Chart 1: Morocco’s awarded offshore licences: over 250,000km2 licenced, c.2x the entire US GoM

Source: ONHYM, Company reports, Jefferies

Huge block sizes: Average is equivalent to 360 standard GoM blocks.

Summary of Licence holders, planned activities

Table 1: Licence holders, key activities to date/planned, blocks with drilling in 2013/2014 shaded (roughly ordered from North to South)

Block Basin Participants Water Depth (m) Area (km2) Notes

Tanger-Larche Offshore Pre-ris/ Rharb

Repsol (36%), Dana Petroleum (15%), Gas Natural (24%)

2,744 Made Anchois gas discovery in 2009 (c.100bcf), 2 follow up wells in 2011 were unsuccessful, have now converted licence back into reconnaissance licence Loukos Offshore Pre-ris/

Rharb

Chariot (75%) 4-1446 1,925 Recently awarded (along with Rabat Deep and Casablanca/Safi blocks), current program is to reprocessing existing 2D seismic, acquire additional 2D. May move to acquire 3D in 2014, putting drilling on a 2016 timetable Rabat Deep Offshore Pre-ris/

Rharb

Chariot (75%) 136-3891 10,670 Same as Casablanca Offshore, Loukos and Safi Offshore blocks Casablanca Offshore I-II Doukkala Chariot (75%) 0-290 3,000 Same as Casablanca Offshore, Loukos and Rabat Deep blocks Safi Offshore Essaouira Chariot (75%) 60-1242 500 Same as Casablanca Offshore, Rabat Deep and Loukos blocks Cap Walidia 1-6 Doukkala Chevron (75%) 100-4500 11,768 Recently converted from Reconnaissance Licence, significant portion of blocks in ultra-deep water, includes seismic commitment

Cap Cantain I-VI Doukkala Chevron (75%) 100-4500 11,858 Same as Cap Walidia

Mazagan Offshore I-VI Essaouira Plains (52%), Pura Vida (23%)

967-3263 10,897 Plains farmed-in early 2013, pays $15m cash plus carry up to $215m on 2 wells (firm) and 3D seismic (optional).

Targetingfirst well in 2014

Cap Rhir Deep Offshore I-III

Doukkala Chevron (75%) 100-4500 5,591 Same as Cap Walidia

Essaouira Deep I-IV Essaouira Kosmos (75%)^ 157-2880 6,776 Awaiting approval of increase in licence interest from 37.5% to 75% with purchase of previous partner's interest.

Drilling planned for 2014

Tarhazout Offshore Essaouira Kosmos (75%)^ 990-2500 7,689 Recently converted from Reconnaissance Licence,

Drilling planned in 2014

Foum Assaka Essaouira Kosmos (56.25%), Fastnet (18.75%)

368-2268 6,473 Kosmos recently increased interest by carrying Fastnet's cost of seismic (up to cap) Mir Left I-II Aaiun -

Tarfaya

Genel (75%) 0-799 3,259 Genel recently awarded after previous licence expired. Currently finishing 3D seimic (1,200km2),

Targeting drilling in 2H14

Foum Draa Essaouira Cairn (50%), San Leon (14.2%), Serica (8.3%),

Longreach (2.5%)

197-2071 5,090 Cairn farmed-in in August 2012, carries first well (up to cap), first well in program once long term rig secured,

Targeting drilling in Sept/13

Sidi Moussa Aaiun - Tarfaya

Genel (60%), San Leon (8.5%), Serica (5%), Longreach (1.5%)

0-1,250 7,624 Genel farmed-in in August 2012, pays cost of first well (up to cap).

Targeting first well in 1H14. Tarfaya Offshore Aaiun -

Tarfaya

Galp (50%), Tangiers (25%) 0-800 15,041 Galp farmed-in in Dec/12, paid $7.5m cash and carries one well (up to cap).

Planning to drill by at least mid-14

Juby Maritime I-III Aaiun - Tarfaya

Cairn (35%), Genel (35%) 33-1542 5,606 Cairn acquired interest through acquisition of Nautical Petroleum, Genel through acquisition of Barrus, contains heavy oil Cap Juby field (tested >2kbopd), light oil shows seen in Middle Jurassic in the Cap Juby appraisal well.

Exploration/appraisal well planned for 4Q13

Bourjdour Offshore Shallow Teredo (75%) 7,244 Little is known about this company or its planned activities Cap Boujdour Aaiun -

Tarfaya

Kosmos (75%) 50-3,000 29,740 Portion of original 110,000km2 Boujdour Offshore, originally licenced by Kerr-McGee (Anadarko), offshore Western Sahara, 3D seismic acquired,

Drilling planned for 2014

Anzarane Offshore Aaiun-Tarfaya

Total (50%) 0-3504 100,927 Offshore Western Sahara, limited information available, reported to be acquiring seismic

Total acreage licenced 254,422

Total area of licences with change in ownership in 2012/2013 214,694

% of area with change in ownership in 2012/2013 84%

^Note: Kosmos’ increase in WI in Essaouira block and conversion of Tarhazout Offshore from reconnaissance licence awaiting government approval

10+ wells planned with multiple rigs, operators

drilling

Companies operating in Morocco are planning to drill at least 10 wells from 4Q13 to end 2014. We expect this to increase in the event of success at any of the wells. The mid-cap companies, Kosmos, Cairn, Genel and Plains are leading the charge.

Kosmos, Cairn and Genel are all stating their intention is secure long term rig capacity (1 year or more) to drill across their exploration portfolios, both in Africa and beyond. This gives them significant flexibility to follow up on any success with appraisal and follow on exploration drilling. None of these rigs have yet been formally contracted. Cairn believes they have line of sight that could begin drilling in September 2013 and Genel believes they have line of sight on a rig that could begin drilling in early 2014. Kosmos has not stated when they expect to have the rig secured but are targeting a multi-well campaign in 2014.

Plains and Galp also planning to drill in 2014, no details on rig strategy.

Chart 2: At least 10 wells planned before YE14, more wells likely added to program in the event of success

Note: Operator only is named. See above for other companies in licence. Source: ONHYM, Company reports, Jefferies

Planned drilling:

Foum Draa: 1 firm well on Prospect F. Cairn operated (50% WI, with San Leon 14.2%, Serica 8.3%, Longreach 2.5%). Dependent on rig, could start drilling in September 2013. Prospect F is a Lower Cretaceous fan. Cairn estimates prospective resources of 142mmb. Potential follow up in Prospect A (126mmb) in mid-year 2014 if successful. Cairn will carry the cost of the well up to $60m.

5 operators planning to bring in at least 3 rigs into the country to drill min 10 wells through to YE14. With LT rig capacity, program could be upscaled quickly to follow on any success with additional

Juby Maritime: 1 firm exploration/appraisal well, plus 1 likely exploration only well. Cairn operated (37.5% WI, with Genel 37.5%). Either second well in Cairn’s program for first well on Genel’s planned rig, late 4Q13 spud. First well is appraisal/exploration well near Cap Juby discovery, targeting light oil seen in Middle Jurassic. Cairn estimates 73mmb for exploration target only, Genel estimates 250mmb for exploration and appraisal target combined. Pure exploration well possible as follow up in 2H14, Genel estimates 200mmb prospective resources (no estimate from Cairn).

Essaouira, Tarhazoute, Foum Assaka: 2+ wells. Kosmos operated, plans to drill 2 or more wells on its northern acreage in the Agadir basin. Kosmos has 75% WI in Essaouira and Tarhazoute and 56.25% in Foum Assaka where it is partnered with Fastnet (18.75%). The company plans to farm-down its acreage before drilling and will begin that process shortly. It is currently looking for a long term contract on the rig. The company has not disclosed specific prospect sizes or which blocks will be drilled. The company believes it could have the rig secured and start drilling in late 2013 or 2014. Kosmos is targeting Cretaceous channel/fan plays with the primary source rock believed to be a locally mature Cretaceous source rock.

Cap Boujdour: 1+ well. Kosmos operated, plans to drill 1 or more wells on its Southern Aaiun basin acreage also in 2014. Like its northern acreage, Kosmos is running a farm-out process ahead of drilling and has not given any specific prospect sizes. Will be drilled as part of campaign in late 2013/2014.

Tarfaya Offshore: 1 well. Galp operated (50% WI), with Tangiers, 25% WI. First well is planned to be drilled by at least mid-2014 and given water depths, a jack up rig could be used. No specifics regarding timelines/rig contracting strategy has been disclosed. The first well targeted is Trident, a Jurassic carbonate with prospective resources of 450mmb. Galp will carry the cost of the well up to $33.5m.

Sidi Moussa: 1 well. Genel operated (60%WI), with San Leon (8.5%), Serica (5%) and Longreach (1.5%). Genel is looking to secure a long term rig which will also be used to drill in Malta. It currently expects the rig would be back in Morocco to drill on Sidi Moussa by March 2014. Genel carries the cost of the well up to $50m. The first prospect will be Nour, targeting a 200mmb Jurassic carbonate.

Mir Left: 1 well. Genel operated, 75% WI. May farm-down pre-drill. Currently finalizing acquisition of 1,200km2 3D seismic. Would drill after Sidi Moussa in mid-2H14.

Primary lead defined on 2D data only, currently estimated to have 200mmb, also primarily targeting Jurassic carbonates.

Mazagan: 1-2 wells. Plains operated, 52% WI, with Pura Vida 23%. Plans to drill in 2014, no details available on rig contracting strategy. The first prospect to drill is Toubkal, estimated to have 1.5bn bbl prospective resources in a Miocene fan. Plains to carry 2 firm wells up to a total cost of $215m. Second well prospect/timing not yet determined, may target deeper water Cretaceous fan play if 3D seismic is acquired over the area and is encouraging.

First 10 wells in area spanning equivalent of 75% of the US GoM acreage. Potentially material increase in activity in the event of success on some or all of the first 10 firm wells. While there is currently only 10 wells in the firm drilling program, in the event of success, there is very large running room possible given the acreage positions. The average block size of blocks that will have a well drilled in 2013/2014 is nearly 10,000km2 or 2.4m acres, equivalent to over 400 standard US GoM

blocks (9 square miles). The total size of acreage that will have a well is nearly 100,000km2, roughly 75% of the entire licenced area in the US GoM. As such, we see the

potential for the number of wells to drill to increase significantly in the event of success on the first 10 firm wells.

Understanding the rocks and the scale

of the opportunity

The Atlantic Margin has seen a material increase in interest from the industry recently with companies targeting a number of regions on both sides of the Atlantic, including, inter alia, Canada, Greenland, Ireland, Morocco, Mauritania, Senegal, The Gambia and Guinea. Generally speaking, the overriding thesis joining these regions together is the regionally significant development of source rocks in the Jurassic period during the early stages of Atlantic rifting. However, we note some companies are targeting source rocks believed to be only locally present. Proven source rocks typed to the same age include the Kimmeridge Clay in the North Sea and its regional equivalents in Canada (offshore Nova Scotia) and Morocco (Cap Juby discovery).

Chart 3: Jurassic source rock believed to be regionally extensive, deposited during the early stages of Atlantic rifting

Source: Pura Vida, RISC, Jefferies

Despite the recent surge in licencing in Morocco, this is not to say the country has seen no previous offshore exploration drilling with 36 offshore wells drilled offshore, only 9 since 1990. This equates to 1 well per 10,000km2 (vs world average of 80 wells/10,000km2). The majority of these wells were drilled in water depths of <200m and many of them targeted the Jurassic carbonate play which resulted in the Cap Juby heavy oil discovery. We believe new play concepts (including deeper targets than previously drilled) and new technologies could help unlock this region which has been largely overlooked for the past decade.

Morocco rush in 2012/2013...As mentioned above, Morocco has seen a rush of new entrants since the beginning of 2012 including: Cairn Energy (farm-in Foum Draa block, corporate acquisition of company with interests in Juby Maritime Block), Genel Energy

(farm-in Sidi Moussa block, corporate acquisition of Barrus Petroleum in Juby Maritime block, new licence award in Mir Left block), Kosmos Energy (acquisition of partner’s interest in Essaouira block, farm-in to increase interest in Foum Assaka block, conversion of Tarhazoute block from reconnaissance licence to exploration licence), Plains Exploration (farm-in to Mazagan block), Galp (farm-in to Tarfaya Offshore block),

Chevron (licencing 29,200km2 new acreage), Total (reconnaissance licence on

100,000km2 position) and Chariot (licencing 16,000km2 position).

Morocco targeting the same themes as seen along the Atlantic Margin.

36 wells offshore Morocco have resulted in only 1 discovery. Region has been largely overlooked for the last decade with only 9 wells in the last quarter century. New play ideas, new technologies could help unlock.

…follows surge in interest in Atlantic “sister” basin. One explanation for the recent surge in interest has been the multi-billion dollar commitments made for exploration acreage in Nova Scotia which is the conjugate margin sister basin to Morocco. Shell and BP were both awarded c.14,000km2 exploration licences in the deepwater

offshore Nova Scotia. Shell was awarded its package in January 2012 with a spending commitment over 6 years of $970m. BP was awarded its package in November 2012 with a spending commitment of $1.05 bn over 6 years.

Chart 2: The conjugate margin to Nova Scotia: BP and Shell were awarded blocks in 2012 with $2bn total spending commitment over 6 years

Source: Nova Scotia Department of Energy

Basic geological setting

Basic geological history of the region. Continental rifting began in the Middle to Upper Jurassic and sedimentation began during this period. Seaboard spreading began and a carbonate platform developed along the continental margins in the Early to Middle Jurassic with up to 4,000m of Carbonates forming. Fluctuations in sea levels alternatively eroded and then built the shelf basinward. During the Cretaceous, wrenching and lowering sea levels resulted in widespread and deep erosion of portions of the onshore and sediment dump into the basin. This caused significant halokinesis (salt movement) including the formation of salt diapers and salt pillows. Finally, during the Tertiary as the landmasses of Europe and Africa collided, the Atlas Mountains were uplifted in the north of Morocco and erosion into the basin began.

Source rocks: Jurassic primary target. The primary source rock being chased across the region are Jurassic aged, similar to the major source rocks seen in a number of Atlantic margin basins. The Jurassic is known to be a period when source rock development was regionally significant, for example the Kimmeridge Clay in the North Sea and its equivalents offshore Nova Scotia. Geochemical analysis by Shell suggested the oil in Cap Juby was sourced from Type I (Marine, oil prone) or Type II (Marine/Terrestrial mixed, oil or gas prone).

Potential for localised Cretaceous aged source rocks also. There are potentially other locally mature source rocks, such as the Cretaceous aged (specifically Aptian-Albian and Cenomanian-Turonian) which are by far the richest in organic matter with TOCs up to

Sable, Deep Panuke

(Gas)

2012 awards: BP and

Shell committed to

spend $1.1 bn over 6

years

$2bn exploration commitments made by Shell and BP in Morocco’s sister basin in Nova Scotia, Canada in 2012.Jurassic source rocks proven along the margin and in Morocco at Cap Juby. Areal extent/effectiveness in Morocco TBD.

Rich organic sections seen in Cretaceous: Key is finding areas were deeply buried to be in oil window.

20%. These are marine source rocks, implying they should be oil prone. However, the key challenge is finding these Cretaceous aged source rock buried sufficiently deeply to be oil mature. Kosmos is the main company chasing Cretaceous source rocks and state they have specifically targeted their blocks to where they believe they are most likely to be locally mature.

Reservoirs: Jurassic – proven but tricky: Along the shelf edge, the primary reservoir targets are carbonates with reefal build up estimated to be up to 4,000m. The successful discovery of Cap Juby proves this reservoir in the Upper Jurassic but its appraisal also highlights the key risk of the carbonate exploration. The Cap Juby-1 appraisal well was drilled in 1984 adjacent to the 1969 MO-2 discovery well which had porosities of 1-13% with natural fracturing. Cap Juby-1 found generally poor reservoir (porosity <5%, permeability <0.05mD). NSAI believe the proximity of these two wells indicates reservoir heterogeneity over relatively short distances. Companies primarily chasing these reservoirs include Galp and Genel (and Cairn to a lesser degree).

Reservoirs: Lower Cretaceous not well tested. In the deeper water, the Lower Cretaceous reservoirs have not been well tested as most of the deepwater wells have only gone as deep as the Upper Cretaceous. The two key deltas are the Tan-Tan and Boujdour. There is evidence of relative sea-level low-stands during the Lower Cretaceous which are believe to be responsible for the by-pass delivery of sands past the shelf edge and into the deepwater slope to base of slope areas. These reservoirs have been seen in DSDP wells in the area and in the Canary Island outcrops. Companies primarily chasing these Lower Cretaceous reservoirs include Kosmos (applying their expertise from its discoveries in Ghana) and Cairn.

Reservoirs: Tertiary potential in north from erosion of Atlas Mountains. The Atlas Mountains were uplifted along rifts created during the Mesozoic period primarily during the Miocene and Pliocene age. Erosional products at this time are believed to have provided reservoir for the main play of the Mazagan permit (Plains and Pura Vida). This is not a main reservoir target of other companies although its influence has been discussed by the other companies.

Understanding the political and

commercial environment

The Kingdom of Morocco is a constitutional monarchy with an elected parliament. It gained independence in 1956 from France. The King, King Mohammed VI, holds vast executive and legislative powers, including the power to dissolve parliament. In the wake of the Arab Spring in 2011, weekly rallies began in multiple cities to demand greater democracy and end to government corruption. Overall, the response of Moroccan security forces was assessed to be subdued compared to violence in other parts of the region and King Mohammed VI quickly responded with a reform package that included a new constitution and early elections. The constitution was approved by popular referendum in July 2011 and some new powers were extended to parliament and the prime minister.

Morocco’s economy is considered relatively liberal with privatizations of certain former public sectors since the early 1990s under King Mohammad’s rule. The main resources of the economy are agriculture, phosphates and tourism and its economy depends heavily on the weather. GDP growth has been steady in the 4-5% pa since 2000 although 2012 growth was lower (c.3%) due to a poor harvest and economic slowdown in Europe. In 2011 and 2012, high prices on fuel, which is subsidized and almost entirely imported, strained government budgets and widened the country’s current account deficit. Its debt is rated Baa1 by Moody’s.

Large carbonate sections built up in Jurassic period: Proven but reservoir heterogeneity is a risk.

Late Cretaceous reservoirs have not been targeted in previous drilling

Tertiary potential seen in the north caused by erosion of Atlas Mountains which were uplifted in the Tertiary period.

Oil and gas regulation

Wood Mackenzie states the regulatory regime in Morocco is currently the most favourable regime to international oil companies in North Africa.

The state’s interests in oil and gas are represented by the State Oil Company, L’Office National des Hydrocarbures et des Mines (ONHYM). ONHYM was formed in 2004 through the merger of the previous oil (ONAREP) and mining (BRPM) state companies. The hydrocarbon laws were amended significant in 2000 with the goal of attracting additional investment to the country. Under the new laws, ONHYM has the right to take up to 25% in all commercial discoveries (carried through exploration), down from 50% previously. The terms offered are attractive and licence awards surged offshore given the favourable terms, in particular for the deepwater. However, many of these licences were relinquished in the mid 2000’s after 8 unsuccessful offshore wells (notably before the Jubilee discovery in Ghana in 2007 brought attention to the potential of the Lower Cretaceous fan play offshore in the Atlantic Margin).

Licencing phases. Companies can first apply for reconnaissance licence for an initial period of 1 year, with extensions allowed. It allows for preliminary studies and seismic surveys but not drilling. Exploration permits have a duration of 8 years, extendable to 10 years if a discovery made in the last 2 years of the contract. The full duration is split into 3 periods of negotiable length with relinquishment requirements after the initial phase equivalent to 10% per year the licence has been held. Exploitation concessions are awarded to develop commercially valid deposits over 25 years with 10 year extensions possible through negotiation.

Taxes

Morocco has implemented one of the most attractive fiscal terms globally to attract investments. It is a tax/royalty system with a number of bonuses for various production thresholds. At least some of the contacts have tax stability clauses and international arbitration for any dispute settlement.

25% state participation. ONHYM, the state oil company, has a right to take up to 25% in all commercial discoveries. ONHYM must pay its share of costs for developments but is carried for the exploration phase.

7.5-10% royalty on oil. For offshore oil/gas fields, a royalty of 10% is payable on oil for fields in less than 200m water depth and 7.5% for fields over 200m. Royalties on gas are 5% and 3.5% respectively. In addition, the first 2.2mmb and 11 bcf are exempt from royalties in less than 200m and the first 4mmb, 18 bcf in water depths over 200m.

Surface rental fees. Current rates are 1000 Dirhams (c.$117) per km2, payable

annually in the exploitation phase (for example, average exploration licence is c.8,000km2, average surface rental fee would be c.$1m but exploitation licence likely be

smaller than exploration licence).

30% corporate income tax, 10 year holiday. The company pays 30% income tax with deductions allowed for surface rental fees, bonuses, training fees, royalties, development expenditure (over 10 years on straight line basis, ring fenced by field), operating expenses (year in which occurred) and exploration expenses (over 5 years, double declining balance basis).

Exploration expenses transferable between licences. Exploration expenses are deductible from income taxes. While development expenditures are ring fenced by field, companies can apply exploration expenses against any exploitation concession held.

No withholding taxes on profits remitted overseas.

Bonuses for commerciality, production thresholds. These bonuses are negotiable and vary by licence. For example, Pura Vida disclosed they are required to pay $1m on

Morocco has put in place a very attractive regulatory and fiscal regime for oil and gas exploration to incentivise investment.

Exploration licences last 8-10 years.

Morocco ranks as one of the most attractive fiscal regimes globally.

declaration of commerciality and granting of an Exploitation Concession and bonuses after production reaches certain thresholds for 30 days. These bonuses are $1m for 50kboep, $1.5m for 75kboep, $2m for 100kbeopd and $2.5m for 150kboepd.

Stability clauses, International arbitration. Pura Vida in their IPO disclosures state that the Petroleum Agreement provides compensation is payable to Pura Vida in the event of any adverse effect from a change in regulations. In addition, any dispute will be settled by arbitration in Paris before the International Centre for the Settlement of Investment disputes or the International Chamber of Commerce under internationally accepted rules. It is not known if this applies to all blocks in Morocco.

The chart below shows how attractive Morocco is on a global scale. Chart 26: Morocco ranks as one of the most attractive fiscal regimes in the world

Source: Journal of World Energy Law and Business

Indicative economics are attractive

It is far too early to estimate with any accuracy what a base case development scenario will look like given the significant variations in water depth, reservoir quality etc. However, as an illustration, we use the Jubilee field in Ghana as a recent deepwater development as an example to estimate what a Moroccan development could be worth.

Indicative NPV in a Jubilee like cost scenario: $13/bbl. We take key parameters from the Jubilee development and increase costs by c.20% to account for industry inflation since the time of its development. We estimate an NPV of c.$13/bbl at $100/bbl oil price.

Basic assumptions:

Discovery of 500mmb in water depth >200m, purchased FPSO based development 20% 30% 40% 50% 60% 70% 80% 90% 100% Ir el an d Pe ru M or o cc o N ew Z ea la nd Pa pu a N ew G u in ea Fr an ce N et he rl an d s So u th A fr ic a U S - O C S D ee p A rg en tin a A us tr al ia C an ad a A rc tic Ph ili p p in es In d ia U S - O C S Sh el f M au rit an ia Th ai la nd C o lo m b ia UK U S - A la sk a M oz am b iq u e Ec u ad or D en m ar k A ng ol a Sh el f N ig er ia JD Z In d on es ia M al ay si a Ru ss ia G ab o n Eg yp t N or w ay Bo liv ia C h in a - O ffs ho re U K P R T N ig er ia D ee p w ate r Tr in id ad & To ba go Tu ni si a A lg er ia N ig er ia S he lf O m an Ye m en Li by a EP SA IV -1 V en ez u el a H ea vy O il Li by a EP SA IV -2 V en ez u el a Ir an B u yb ac ks Go ve rn m e n t Ta ke (%)

Royalty & Tax System Production Sharing Contracts Service Contract Morocco's c.42%government take amongst

the most attractive in the world

At least some have stability clauses in the contract. Unconfirmed if all contracts benefit from this.

Using Jubilee as an analogue for size, production and costs indicates NPV of $13/bbl, IRR of 35%.

Discovery to first production takes 7 years (note Jubilee was 3), first production in 2020, reaches FPSO capacity of 100kbopd in 2023, 4 year plateau before declining at 10% pa, 30 year field life.

Development Capex: $4.7bn ($9.50/bbl), 20% more than forecast costs of Jubilee Phase 1 and 1a to recover a similar amount of oil. FPSO costs $1.7bn, drilling and subsea costs $3bn.

Operating costs: $8.50/bbl average over life of field (no FPSO lease costs as FPSO is purchased).

Base oil price $100/bbl, discount rate 10% real.

In this scenario, we estimate an NPV of c.$13/bbl and an IRR of 35%. We estimate a breakeven oil price of $34/bbl.

Indicative NPV if costs are circa double Jubilee is $9/bbl. Our basic assumptions are above but capex is $7.5 bn ($15/bbl), opex is $17/bbl. In this scenario, we estimate an NPV at $100/bbl of c.$9/bbl and an IRR of 25%. We estimate a breakeven oil price in this scenario of $55.

Relatively sensitive to change in oil prices. The structure of the tax regime is a flat tax rate, regardless of levels of profitability. This is in contrast with most African PSC structures which have a progressive tax rate (ie: as profitability increases, tax rate applied to those profits increase). As such, we estimate a 1% change in oil prices results in a c.1.5% change in NPV.

Chart 6: Indicative potential NPV/bbl and oil price sensitivity: $9/bbl if costs double Jubilee, $13/bbl if 20% above at $100/bbl

$0 $5 $10 $15 $20 $25 $70 $85 $100 $115 $130 US$ NPV/bbl

OIl price (US$/bbl) High Cost Jubilee costs +20%

Source: Jefferies estimates

Western Sahara dispute

The southern area of Morocco known as the Southern Provinces or the Western Sahara has been in a long term dispute over sovereignty. The area is claimed by Morocco and is largely administered by Morocco but has been on the UN list of non-self-governing territories since 1963. The area was originally a colony of Spain, which relinquished administrative control in 1975 to Morocco and Mauritania. After a war erupted, Mauritania withdrew in 1979 and Morocco secured effective control over the territory.

Increasing costs to roughly double that on Jubilee indicates NPV of $9/bbl, IRR of 25%.

Tax regime structure means higher than average flow through of oil price changes to the contractor.

Southern Provinces/Western Sahara claimed and de facto ruled by Morocco but is listed as a non-self-governing territory by the UN.

The Sahrawi national liberation movement of Polisario Front proclaimed the region to be the Sahrawi Arab Democratic Republic (SADR). A UN sponsored ceasefire was agreed in 1991 which included a planned referendum in 1992. This quickly stalled, largely over disputes over who is eligible to vote in the referendum (with the option between independence or affirming integration with Morocco). SADR has awarded several overlapping interests in this region although ratification requires the sovereignty dispute to be resolved (including Premier, Ophir, Tower, Wessex). There is currently no roadmap for any negotiations to resolve this dispute.

Licences offshore the disputed area include Total’s Anzarane block (reconnaissance licence), Kosmos’ Cap Boujdour block, Teredo’s Boujdour Offshore shallow block. The remainder sit north of the disputed border. Total was one of the first acreage holders in the region (from 2001) but withdrew in 2004, reportedly due to pressures over the region (including concerns over its relationship with Algeria which supports the Polisario Front and pressure from shareholders with a social responsibility mandate). However, Total was awarded its 100,000 km2 reconnaissance licence in 2012 and we believe it was extended

on its expiration in December. Industry reports suggest Total may acquire 3D seismic. Kosmos is confident in its ability to undertake exploration operations on its block as part of its planned upcoming drilling program.

Gas commercialisation?

All of the companies currently active offshore are targeting oil rather than gas. If a gas discovery was made, the companies would likely face many of the same challenges often faced in Africa for commercialising gas.

There is a very small amount of gas production in the onshore north-western part of the country which have been tied into infrastructure to supplement gas for the local industry. Morocco currently gets almost all of its gas from the Maghreb-Europe pipeline (GME) which links Algeria and Spain, going through the north-eastern part of Morocco. The pipeline was commissioned in 1996 and capacity is now 1.75bcf/d. Morocco has the right to access a set percentage of the gas transported on this pipeline as a royalty in kind fee transit fee but a number of the proposed projects to use this gas have been slow to start. There have also been reports of Morocco considering LNG import terminals with capacity of 0.5-1bcf/d.

In the event of a gas discovery, we believe there could be some gas supplied to the local industry. We think this is most likely to be an appropriate solution of small amounts of gas associated with an oil discovery. However, if a significant gas discovery was made, it would likely need an export solution. We believe it is most likely to be exported via pipeline to Spain and into the western Europe pipeline system. Whether Morocco could access capacity on the 1.75 bcf/d pipeline is unclear but at best, we believe volumes may be limited. Thus, we believe a significant gas discovery would likely require increasing/building additional pipeline capacity. While it clearly increases the minimum commercial threshold, given its proximity to western European gas markets, we do not believe it is unfeasible.

Companies have previously withdrawn from licences offshore Western Sahara reportedly due to pressure about the dispute. Kosmos believes it can drill there in its upcoming drilling campaign.

Companies targeting oil. Small gas discoveries could be utilised

domestically, crowding out currently imported gas. Large gas discoveries would require export solution, most likely by pipeline to Spain given distance. Feasible but increases minimum commercial threshold.

Chart 27: Maghreb-Europe pipeline connects Algerian gas with Western Europe via Morocco.

Company profiles

The sections below details the acreage position of each company, what their interpretation of the geology in their block is and what their future exploration programs are.

Operators

Cairn Energy

CNE LN, Buy, PT385p, Mkt Cap US$2.5bn, Covered by Laura Loppacher

Cairn holds a position in c.9,000km2across two block, Foum Draa (50%) and

Juby Maritime (37.5%). It operates both blocks.

Cairn farmed-in into the Foum Draa block Morocco in August 2012, earning a 50% WI by carrying the first well up to $60m and paying $1.5m back costs. Its partners on the block are San Leon 14.17% (SLE LN, 7.2p, NC), Serica Energy 8.33% (SQZ LN, 26.4p, NC) and Longreach Oil & Gas 2.5% (LOI CN, C$0.75, NC). Its 37.5% WI in the Juby Maritime block was acquired as part of the Nautical acquisition and is now partnered with Genel Energy (37.5%) after Genel bought out the previous owner, Barrus Petroleum (consideration not disclosed but media reports it was c.$50m, also had acreage in Cote D’Ivoire).

Cairn positioned for both of the key play types being chased. Cairn is targeting both late Jurassic/early Cretaceous aged clastic plays (deepwater slope/channel plays) as well as the Jurassic carbonate play in the Juby Maritime permit.

Late Jurassic/Early Cretaceous fan play

Cairn entered the Foum Draa block primarily for the sparsely drilled deep-water clastics fan play outboard of the Jurassic shelf edge carbonate play. The reservoir is believed to be sourced from the Tan-Tan Delta, a long lived drainage system in this region. The primary source rock interval is expected to be within the Jurassic, as established in the Cap Juby field. Cairn believes the Cenomanian/Turonian source rock targeted by Kosmos to the north is likely to be immature across the majority of their block as it is not sufficiently deeply buried. The RAK-1 well was drilled by Shell in 2001. Serica states the well found a highly condensed Upper Cretaceous section with thin sands in the Lower Cretaceous but only reached the Barremian level.

Chart 3: Tan-Tan delta believed to source reservoir

Source: Serica, Jefferies

Two primary plays being targeted – carbonate shelf and clastic

Cairn estimates mean resources of 142mmb in its “F” prospect, considerably smaller than estimates from its peers in block. Cairn has high-graded 2 prospects on the Foum Draa block as candidates for the first well. Both prospects are Late Jurassic/Early Cretaceous fans and Cairn estimate prospective resources of 142mmb in Prospect F and 126 mmb in Prospect A. These are equivalent to the prospects named ‚Fig‛ and ‚Apricot‛ in the NSAI report done for Longreach and featured in Serica’s public farmout data. NSAI estimated Apricot and Apricot Shallow had 584mmb, and Fig had 232mmb prospective resources, each at 10% GCoS. Serica estimated 552mmb in Apricot Deep and 338mmb in Apricot shallow (no GCoS given). Cairn has stated they believe all their frontier exploration prospects have 15-25% GCoS. We believe Cairn’s lower volume estimates but higher CoS is a result of additional study refining their estimates and more conservatism. We carry Prospect F at 4p/sh risked, 37p/sh unrisked. We carry Prospect A at 2p/sh risked, 33p/sh unrisked. We note using NSAI prospect sizes would suggest unrisked upside of >£2/sh unrisked for F&A.

Chart 4: Targeting late Jurassic/early Cretaceous fan prospects outboard of the shelf edge and carbonate prospects along the shelf edge

Source: Cairn

Chart 5: Amplitude response over F & A prospects

Source: Cairn

Jurassic Carbonates

The other major play being targeted in Morocco is the Jurassic Carbonate play. This play has the advantage of a proven discovery in the play, Cap Juby and lower migration risk as targeted reservoirs sit directly atop the targeted source rocks. However, as carbonates, it suffers from being unable to use seismic amplitudes to derisk charge and reservoir quality is more variable, as was seen on Cap Juby.

Cap Juby heavy oil discovery. The Cap Juby field was discovered in 1968 by Esso in c.100m water depth. It tested 2,400 bopd of heavy (12 deg API) from the Upper Jurassic. Whilst Esso drilled an additional well in 1972 and then Mobil in 1984, the field was deemed non-commercial at the time.

Heavy oil believed to be caused by localised biodegradation. The heavy oil at Cap Juby is believed to have occurred due to biodegradation. However, the specific cause of the biodegradation at Cap Juby is not well understood as the current depth of burial (c.2,000m sub-sea) does not suggest biodegradation should be expected. Several

competing theories have been proposed. One theory is that the oil was uplifted, biodegraded and then buried deeper due to later sedimentary deposits during the Tertiary period. Another theory suggests circulating sea water down dip of the oil cooled the reservoir sufficiently to allow microbial growth. These theories lead the companies to believe the biodegradation may be a localized phenomenon rather than widespread.

Light oil seen in Cap Juby. The 1972 MO-8 well tested 0.28 bbl of 38 degree API oil and 57.6 bbl of water from the Middle Jurassic. The partners believe this was perhaps close to the oil water contact. In addition, Cairn’s partner, Genel, now believe there is evidence from the crude samples of the Upper Jurassic discovery of 15-20% light oil very similar to the Middle Jurassic interval mixed in with the heavy oil.

Chart 6: Map of Cap Juby discovery

Source: Genel, Jefferies, company data

Cap Juby exploration: 73-250mmb prospect. Cairn and Genel will drill a exploration well on Cap Juby, primarily targeting the light oil seen in the Middle/Lower Jurassic and possibly partially appraising the Upper Jurassic discovery. The well location has yet to be finalised but one option under consideration is c.100m updip from the MO-8 well. This would also penetrate the Upper Jurassic closure which may have some commercial potential. Cairn estimates 73mmb in the Middle Jurassic only. Genel estimates 250mmb in the Upper and Middle Jurassic. The variance in estimates is partially due to including the shallower interval but we believe mostly due to the difficulty in predicting the heterogeneity of the carbonate reservoirs with limited data.

Potential running room is significant. The carbonate play is being pursued along trend from the Juby Maritime block to the northeast (Genel) and east (Galp) and the partners see additional exploration potential on the block. The partners recently acquired 680km2 over a carbonate edge prospect which could form part of a later drilling

campaign in 2014. Genel estimates 200mmb prospective resources in this prospect, Cairn will review the results of the 3D seismic before providing a resource estimate. In addition, Genel states they believe the block has a further 350mmb prospective resources in other potential follow on prospects/leads, both in the carbonate play but also in a sub-marine fan clastic play. Again, Cairn has not yet provided an equivalent estimate.

Forward program: Looking to secure rig for multi-well program

Cairn is currently looking for a long term rig (1 year) to drill a multi-well campaign across its portfolio, including at least 2 and up to 4 wells in Morocco. The first of these will be on Prospect F in Foum Draa block (50% WI, 142mm, Cairn carries full cost of well up to $60m) and the second will be the Cap Juby step-out on Juby Maritime block (37.5% WI,

Chasing smaller but low risk target updip of known light oil shows

M0-2

Cap Juby

M0-8

73mmb (CNE estimate), ONHYM’s interest carried so Cairn pays 50% of well cost). Dependent on the rig contract, Prospect F is expected to spud in September of this year, Cap Juby step out thereafter in 4Q13. Cap Juby is in shallow waters so may also be drilled by the long term rig which Genel is procuring. The follow on program will depend on the results of these 2 wells but the rig could return after a 1 well slot on its Senegal assets, returning to Morocco for another well(s) in 2Q14.

We like Cairn for its attractive valuation, trading at a significant discount to Core SoP and substantial upside potential which we do not see as being valued at current levels, not only in Morocco but also Senegal, Greenland and the North Sea.

Genel Energy

GENL LN, NC, Mkt Cap $3.3 bn

Genel acquired interests in 3 blocks in Morocco in 2012 through a combination of farm-in (Sidi Moussa Block, 60% WI), corporate acquisition (Juby Maritime Block, 37.5% WI) and licencing (Mir Left Block, 75% WI). These blocks cover c.16,500km2. Genel is primarily

focused on the Jurassic carbonate trend along the shelf edge. Genel believes this is most attractive as it is the only proven offshore play in Morocco and the target reservoirs sit directly atop the expected source rocks, lowering migration risk.

As reservoir risk is one of the key risks for carbonates, Genel is utilizing amplitude responses to help identify where the carbonates are mostly like to have good porosity, a technique not available in the 1980s when the majority of the unsuccessful wells were drilled in Morocco. Unlike sand bodies, it is not possible to use these techniques to attempt to identify hydrocarbon signatures.

Genel’s currently highgraded prospects are typically associated with domes of mobile salt features. This upward movement of the salt can help to break up the carbonates, increasing permeability. However, there is also some risk of this fracturing being significant enough to cause compartmentalisation within the reservoir and this is a key risk that would have to be addressed in the appraisal program.

Juby Maritime. Genel bought private Barrus Petroleum in summer 2012. Barrus held exploration interest in Juby Maritime (37.5% WI, with Cairn as operator) and Cote D’Ivoire. Terms were not disclosed but media reports stated consideration was $50m. The block is in water depths of 33-1550m and contains the existing Cap Juby discovery.

Sidi Moussa. Genel farmed into and took operatorship of the Sidi Moussa block in August 2012. It acquired a 60% WI in exchange for funding the first exploration well up to $50m and paying $1.3m in back costs. Remaining partners include San Leon (8.5%), Serica (5%) and Longreach (1.5%) with ONHYM holding a 25% carried interest. The block covers 7,625km2 in water depths up to 1,250m.

Mir Left. Genel licenced the Mir Left block in November, 2012 and has a 75% WI (with ONHYM 25%). The blocks cover 3,259km2 with water depths of 60-320m.

Genel’s key focus is on the Jurassic carbonates. Assembled acreage position in 2012 through corporate acquisition, farm-in and licencing awards.

Chart 7: Genel’s acreage position along the carbonate shelf edge

Source: Genel, Jefferies, company data

The Juby Maritime block is described in detail above under Cairn, who is the operator. The near term program involves drilling an exploration/appraisal well on the Cap Juby field with the main exploration target updip of the light oil shows seen in a previous well in the Middle Jurassic and will also appraise the heavy oil discovery in the Upper Jurassic. Genel sees a number of prospects in this block and have recently acquired an additional 680km2 3D seismic over its follow on target. They also see some potential for clastic fan

plays on the block.

On Sidi Moussa, Genel has identified multiple carbonate draped titled fault block structures along trend from the Cap Juby at the Jurassic level. The Nour prospect has been highgraded and Genel estimates 200mmb of prospective resources at 20% CoS. Once final reprocessing of the 3D seismic for depth conversion, Genel believes these estimates may increase. Genel believes there is 850mmb of prospective resource on the block. Most of this potential is identified in the carbonate play but there is some potential for the clastic fan plays as well.

Genel sees potential of up to 2 bn bbl or more on its 3 blocks. Planning to drill 3-4 wells initially and follow up quickly on any success.

Chart 8: Nour Prospect: Middle and Jurassic carbonates draped over a salt dome high

Source: Genel, Jefferies

Chart 9: Nour first of several prospects seen on block

Source: Genel, Jefferies

Mir Left is the most recent addition to the portfolio and has had the least amount of seismic done on it to date but sits directly along trend to Sidi Moussa and is targeting the same plays. However, it has the most existing well penetrations to date. 6 wells were drilled in the 1980s. Genel believes these wells failed for a variety of reasons including being drilled in an area without valid closures (porous interval above the carbonate seen extending all the way to sea floor) and not drilling deep enough within the Jurassic to hit the potential reservoir section in the carbonates.

A 1,200km2 3D seismic program is nearing completion and the company will use this data

to highgrade the leads seen on the block. The main lead seen is believed to be c.200mmb with 750mmb prospective resources on the block. However, interpretation of the 3D seismic is needed to further refine these estimates. Similar to its other blocks, Genel sees potential for a secondary play in the clastic channel/fan systems sitting on their block. Kosmos’ acreage sits to the outboard of this acreage and the reservoir Kosmos is targeting would have been transported from shore and across Mir Left to be deposited in Kosmos’ acreage.

Given its very high working interest on the block (75% participating, 100% paying during exploration), Genel states they may consider farming down upon interpretation of the finalised 3D data but will make that decision at a later date and has the financial capability to drill without a farm-in.

Chart 10: 1,250km2 3D seismic nearing completion. Main lead currently

estimated to have c.200mmb based on 2D Seismic

Source: Genel, Jefferies, company data

Previous well failures believed to be due to ineffective trap, not drilling deep enough within the section.

Genel may farm-down its Mir Left block pre-drill but has funding necessary to drill at 100% (75% after ONHYM back in).

Forward program: 4+ well program planned in Morocco in 2013/2014. Genel is looking to secure a rig for their exploration program across their portfolio in Morocco, Malta and Cote D’Ivoire (in addition to potential new ventures which they are continuously screening for). They are targeting a contract for the minimum of 10 well slots or 2 years, of which at least 4 would be for Morocco. This program is may begin with the well on Juby Maritime in 4Q14 if viewed more advantageous than operator Cairn’s rig option, before moving to Malta for a commitment well due by end of 1Q14. It would then bring the rig back to Morocco for drilling with the current most likely plan to drill a well in Sidi Moussa in 2Q14 and Mir Left in late 3Q14/early 4Q14 before returning for a second well in Juby Maritime in late 2014. Any success would be followed up with additional drilling in 2015. However, the exact well schedule will likely be adjusted in light of results from the program.

Kosmos Energy

KOS US, Buy, PT$17, Mkt Cap $4.2bn, Covered by Brendan Warn

Kosmos was one of the earliest (recent) entrants into Morocco, specifically looking for opportunities similar to their Jubilee field in Ghana. Kosmos states its strategy is to target area where they believe there is potential for good source rock and reservoir, lowering play risk. Kosmos state its primary focus is the potential of the rich Cenomanian/Turonian (CT) source rock with additional potential source rocks in the Jurassic. Given the highly variable burial history of the CT source rock in Africa, it specifically targeted areas which they believe had the thickest overburden above the Cretaceous, not only providing improved reservoir deposition but also increasing the likelihood of the CT source rock being buried sufficiently deeply to be oil mature.

Chart 20: Kosmos Morocco acreage position

* Essaouira WI increase from 37.5% upon government approval of acquisition of partner’s interest. Tarhazoute pending approval of conversion from Reconnaissance Licence; Upon approval, KOS will have 75% in both with ONHYM at 25%, initially carried)

Source: Kosmos, Jefferies

Genel and Cairn both looking at rigs which could drill on their shared block, Genel also looking for LT rig which could drill on Sidi Moussa, Mir Left.

Kosmos was the first of the current licence holders to see the potential of Morocco and has held acreage since 2007.

Kosmos applying its knowledge of Atlantic Margin Late Cretaceous petroleum systems gained from their Ghana (including Jubilee) success.

Kosmos now has 4 blocks covering >50,000km2, 3 in the Agadir basin to the north

(a sub-basin within what other often call the Essaouira basin) and 1 in the Aaiun Basin to the south. The Cap Boujdour block (75%) (29,740km2) is located offshore Western

Sahara. Kosmos is confident in its ability to undertake exploration operations as part of its upcoming drilling programs. In the northern area, it has 75% in the Essaouira and Tarhazoute (with ONHYM) and 56.25% of the Foum Assaka block (with Fastnet (18.75%), ONHYM). These blocks cover c.26,000km2 and the company has acquired nearly

5,000km2 3D seismic over the area. Agadir basin

Foum Assaka Block. Kosmos and Pathfinder Hydrocarbon were awarded the Foum Assaka block in May 2011, each with 37.5%. Kosmos later increased its WI to 56.25% by paying Pathfinder $1m cash and a carrying the initial exploration period work program up to $16m gross. The block covers c.6,500km2 in water depths of c.300-2,100m. Fastnet

acquired Pathfinder Hydrocarbon in mid-2012 for total consideration of $9m ($2m cash (including $1m which was contingent on the yet to close Kosmos farm-in) and 40.7m shares of Fastnet (19.8% of the company at the time).

Essaouira Block. Kosmos was awarded the block in Sept 2011 with a 37.5% WI, partnered with Canamens Energy. In 1Q13, Kosmos acquired Canamens interest, taking their total interest up to 75% (with ONHYM). Consideration was not disclosed. The block covers c.6,800km2 in water depths of 160-2,900m.

Tarhazoute block. Kosmos was awarded the Tarhazoute block in Dec 2011 as a reconnaissance licence. The block covers c.7,700km2 in water depths of c.1,000-2,500m.

The reconnaissance licence had an initial term of 1 year with possible 6 month extension and Kosmos is now in the process of converting it into an exploration contract. Once converted, Kosmos will have a 75% WI, carrying ONHYM’s 25% during exploration.

Chart 21: c.26,000km2 position in the Agadir basin

Source: Kosmos

Chart 22: Significant reservoir distribution from the Sous River Delta, targeting ponded slope channels and base of slope fans

Source: Fastnet

Looking for thick reservoir, deeply buried Cenomanian/Turonian source rock.

Kosmos states they high-graded the acreage selected due to the amount of overburden above their targeted CT source rocks which they believe should push them into the oil generating window. A secondary identified target which Kosmos believes also could be working for them includes the Jurassic source rocks which have been proven in the region. Reservoirs targeted include late Cretaceous/early Tertiary, partially influenced by the erosion of the uplifted Atlas Mountains to the north of Morocco.

While in country since 2007, Kosmos increased its position in 2012/2013 through licencing of the Tarhazoute block, farm-in on part of its partner’s interest in Foum Assaka and buying out its partner’s interest in Essaouira.

Kosmos focused on Late Cretaceous petroleum systems, specifically targeted areas which they believe organic rich Cenomanian/Turonian aged rocks are in the oil window.