ANNUAL REPORT 2013

REGISTRATION DOCUMENT INCLUDING ANNUAL FINANCIAL REPORT

Advanced batteries.

Designed for industry.

1 Group

presentation

5

1.1 Group profi le 6

1.2 Group strategy and competitive advantages 7

1.3 Activities 8

1.4 Sustainable development 13

1.5 Organisation and locations 14

1.6 Key fi gures 16

1.7 Shareholders and stock market information 18

2 Risk

Factors

21

2.1 Risks related to the market environment

and the Group’s activities 22

2.2 Operational risks 25

2.3 Credit and counterparty risks 27

2.4 Liquidity risk 27

2.5 Market risks 27

2.6 Contractual and legal risks 28

2.7 Risks related to the impact of the Group’s business on the environment, human health and safety 29

2.8 Insurance 32

3 Sustainable

Development

33

3.1 Environmental responsibility 35

3.2 Social responsibility 40

3.3 Corporate social responsibility 45

3.4 Statutory Auditors’ independent third-party report on consolidated social, environmental and societal information published

in the management report 47

4 Corporate

Governance

51

4.1 Management and Supervisory Boards 52

4.2 Remuneration and shareholding of the Management and Supervisory

Board members 58

4.3 Report of the Chairman

of the Supervisory Board 70

4.4 Statutory Auditors’ report, prepared in compliance with article L.225-235 of the French Commercial Code on the report prepared by the Chairman of the Supervisory Board of Saft Groupe SA 79

4.5 Main provisions of the Supervisory Board

bylaws 80

5 Comments

on the 2013

fi nancial year

83

5.1 Activity and consolidated results 84

5.2 Earnings per division 86

5.3 Other items of consolidated income 89

5.4 Research and development 90

5.5 Investments and fi xed assets 91

5.6 Cash fl ow and fi nancing 91

5.7 Statement of fi nancial position 92

5.8 Other key events in fi nancial year 2013 92

5.9 Related-party transactions 93

5.10 2013 Change in scope 93

5.11 Basis of preparation of the consolidated

fi nancial statements 93

5.12 Recent events and 2014 outlook 94

5.13 Saft Groupe SA activity and results 94

5.14 Activity of Saft Groupe SA

subsidiaries and controlled entities 95

Contents

labeltransparence.com

TRANSPARENCE

LABEL

This label recognises the most transparent Registration Documents according to the criteria of the Annual Transparency Ranking.

6

2013 consolidated fi nancial

statements 97

6.1 Consolidated statement of fi nancial position 986.2 Consolidated income statement and consolidated statement

of comprehensive income 100

6.3 Consolidated statement of cash fl ows 102

6.4 Statement of changes in equity 103

6.5 Notes to the consolidated fi nancial

statements 104

6.6 Statutory Auditors’ report

on the consolidated fi nancial statements 151

7

Parent company Certifi ed

Financial Statements

153

7.1 Balance sheet – Assets 154

7.2 Balance sheet – Equity and liabilities 154

7.3 Income statement 155

7.4 Notes to the parent company

Financial Statements 156

7.5 Parent company – Financial summary

for the last fi ve years 165

7.6 Statutory Auditors’ report on the fi nancial statements for the year ended

31 December 2013 166

8

Information about the

Company and its share capital 169

8.1 General information about the Company 1708.2 Group history 171

8.3 Group organisation chart 172

8.4 Signifi cant contracts and commitments 173

8.5 Main statutory provisions 174

8.6 Capital and shareholding of SAFT Groupe SA 178

9 Annual

General Meeting

181

9.1 Overview of key resolutions 182

9.2 Statutory Auditors’ special report

on regulated agreements and commitments with third parties 183

10 Additional

information

185

10.1 Documents accessible to the public 186

10.2 Offi cers responsible for the annual report 188

10.3 The Saft Group Auditors and related fees 189

10.4 Registration document cross-reference Table 190

10.5 Annual fi nancial report cross-reference table 192

10.6 Management report cross-reference table 193

10.7 Cross-reference table for environmental,

social and corporate social information 194

The information contained in the management report relating to the financial year ended December 31, 2013, presented in this document has been prepared by the Management Board and approved by the Supervisory Board of Saft.

Certain statements contained herein are forward-looking statements relating, in particular, to future events, trends, plans or objectives. By their nature, these forecasts are subject to known or unknown risks and uncertainties could cause Saft’s actual results and objectives to diff er materially from those expressed or implied in these forward-looking statements.

The French version of the 2013 Registration Document has been registered with the AMF. It is therefore the only version that is binding in law.

This Registration Document was registered with the Autorité des marchés fi nanciers (AMF) on February 18 , 2014, in accordance with the article 212–13 of the AMF’s General Regulations. It may be used in support of a fi nancial transaction if accompanied by a transaction circular approved by the AMF.

Chairman’s message

2013

was a year of contrasts for Saft. During the fi rst half the performance was rather

disappointing with no sales growth and reduced profi tability.

This reduction of profi tability was due to a number of factors; unfavorable product mix,

planned increases in research and development costs, and the purchase of a Li-ion cell production facility in France

which added costs. This purchase was the fi nal part of the agreement signed with Johnson Controls Inc. in 2011

to resolve the dispute on the future of Johnson Controls-Saft.

However, after this slow start the Group reported signifi cant commercial successes which drove excellent sales

growth in the second half-year and which had a positive impact on H2 profi tability.

Finally the Group achieved sales growth of 7.5% in the year at constant exchange rates and a strong recovery in

profi tability in H2.

Among the noteworthy successes in 2013 were the major breakthroughs we made in the telecoms market for our

nickel-based batteries in the US and the Evolion® lithium-ion batteries in India.

During the year as a whole the transportation activity, batteries for trains and aviation, registered strong growth,

with numerous successes in the Chinese rail market.

Of course, there were some markets where progress was slower than we had expected, notably in the emerging

energy storage business where we encountered delays in securing contracts. In addition, our Specialty Battery

division had a challenging year notably in the US where demand for our products was lower than expected. The

year ended on a stronger note in civil markets.

In June last year we completed our sale of the Small Nickel Battery business based in Nersac, France, which marked

our fi nal exit from this activity, which is now operating under the name of Arts Energy.

Looking forward, our strategy is to secure growth through continued commercial success for our nickel and primary

lithium products which have been key to our past successes coupled with the rapid growth in sales of our new

technology lithium-ion battery systems.

These new systems are targeted at new applications, energy storage for electricity utilities and vehicles and as

a high performance option in many existing applications, telecom back-up power, motive power, satellites and

launchers, and longer term for aircraft and new rail applications.

I am confi dent that Saft is well-positioned with its products and market experience to be one of the most successful

advanced battery manufacturers in the world in the years to come.

John Searle

Chairman of the Management Board Saft Groupe SA

1

Group presentation

1.1 Group

profi le

6

Saft, the world leader in advanced and innovative battery systems 6

1.2

Group strategy and competitive

advantages 7

1.3 Activities

8

1.3.1 Technologies 8

1.3.2 Applications and markets 8

1.3.3 Research & development 11

1.4 Sustainable

development

13

1.5

Organisation and locations

14

1.5.1 An organisation and international presence supporting

the Group’s development 14 1.5.2 Corporate governance ensuring the balance of powers 15

1.6 Key

fi gures

16

1.7

Shareholders and stock

GROUP PRESENTATION

1

Group profi le1.1 GROUP

PROFILE

Saft in brief

€

624.2

m

sales in 20133,856

staff worldwide18

countries around the world

9.3

%

of sales invested in Research and Development in 2013

14

manufacturing sites worldwide

SAFT, THE WORLD LEADER IN ADVANCED AND INNOVATIVE

BATTERY SYSTEMS*

Created in 1918, Saft is the world’s leading designer, developer and manufacturer of advanced technology batteries for industry. Its multi-technology battery systems meet the needs of a wide variety of customers worldwide:

nickel-based and primary lithium batteries in industrial infrastructure, transportation, civil and military electronics;

lithium-ion solutions in energy storage, telecoms, marine, vehicles, space and defence.

Saft’s customers include original equipment manufacturers (OEMs), distributors, and fi nal end users. Saft manufactures batteries to meet the requirements of specifi c applications, developing batteries in close cooperation with the industrial clients who use Saft batteries in their equipment. Saft continues to develop new generations of batteries for new applications, helping customers develop innovative products and services. On most of the advanced-technology battery markets targeted by Saft, the Saft brand is a key criterion in the customers’ purchase decisions. However, Saft also markets products under other well-known brands: Alcad, Tadiran, Eternacell, Nife and Ferak. This strategy enables the Company to leverage its position on certain specialized markets throughout the world and meet the diverse needs of its customers.

With a consolidated turnover of €624.2m in 2013, Saft operates through two divisions:

the Industrial Battery Group (IBG), which manufactures rechargeable batteries for transportation, stationary backup power and energy storage systems. In 2013, IBG sales represented 59% of the Group consolidated turnover;

the Specialty Battery Group (SBG), which manufactures primary and rechargeable batteries for civil and military electronics activities, space and defence. In 2013, SBG sales represented 41% of the Group consolidated turnover.

2013 key events are presented in the management report in chapter 5 of the Registration Document. Key dates of Saft history are presented in chapter 8 of the Registration Document.

GROUP PRESENTATION

1

Group strategy and competitive advantagesBecause energy consumption in the world is increasing and its production cost is also growing, the energy storage market and therefore the battery market have a promising future. Its potential has also increased thanks to the awareness of the need for a more responsible economic growth, in which energy wastage is limited and emissions of greenhouse gases are reduced.

Saft’s strategy is to address the market segments where its advanced technologies provide a signifi cant advantage over alternative technologies. This strategy is therefore based on: the focus on Research and Development. Saft invests

signifi cant resources in its research and development activities. Saft employs approximately 465 engineers and technicians working in applied research, development of new battery technologies, and optimization of existing products and the adaptation of various batteries to specifi c customer specifi cations;

a wide range of technologies. The Group fi led ten new patents in 2013 divided into 141 patent families related to its battery technologies;

the identification of markets and advanced industrial

applications with a high growth potential where customers require products designed for their specifi c needs. To this eff ect Saft works in close collaboration with its key customers;

a requirement for high quality products. Saft supplies batteries for applications where the cost of failure can be high to end users, particularly in the aviation, defence, and space industries. With nearly one hundred years’ experience in the battery market, Saft’s reputation for making reliable, safe, and high performance products represents a signifi cant competitive advantage in these markets;

the development of solid customer relationships. Those relationships have enabled Saft to work with its main customers in the development phase for new applications which in turn leads to opportunities for new supply contracts;

global c apabilities. Saft is present in 18 countries. Its 14 manufacturing facilities worldwide at sites in nine countries, and its broad sales network, enable Saft to service customers all over the world. The Group’s ability to service its customers in strategic markets on a local basis is also a key competitive advantage.

These principles of the Group’s strategy are competitive advantages and enable the Group to achieve high margins justifi ed by the technology used and the technical know-how. In addition, this strategy enables the Group to have diversifi ed customers and to limit its exposure to cyclical fl uctuations which may aff ect certain industries.

Finally, it enables the Group to hold signifi cant market shares worldwide in most of its markets and to implement a premium pricing policy for its products.

Saft intends to maintain this strategy and take full advantage from its competitive advantages, in order to increase its market shares in the strategic markets where it operates, to gain new markets and new industrial applications with lithium-ion technology developed by the Group, to increase sales and, fi nally, to increase its operating margins.

To achieve these objectives, Saft implements the following strategies:

investment in lithium-ion technology and in new markets; continue to expand its commercial presence with regards

to the market’s needs. Thus, Saft has opened a commercial unit in Brazil in 2010 and Russia in 2013;

exited non-core markets. With the sale of the SNB activity in June 2013, the Group has left the small nickel battery market;

cut production costs. Saft is continuously seeking opportunities to reduce component and manufacturing costs in order to improve its competitiveness. Among others, through its World Class Manufacturing Program for continuous improvement, Saft employs an effi cient methodology to continue reducing its costs while maintaining a high level of quality.

GROUP PRESENTATION

1

ActivitiesSaft‘s strategy is to propose a portfolio of advanced technologies to multiple industrial markets.

1.3.1 TECHNOLOGIES

Batteries are stand-alone power sources that convert chemical energy into electrical energy through a chemical reaction when the battery is discharged.

There are two main types of batteries produced by Saft: non rechargeable batteries (primary) and rechargeable batteries (secondary):

the active materials in a non-rechargeable battery are irreversibly converted during the chemical reaction which produces energy. The principal primary battery technologies Saft’s uses are lithium-based;

rechargeable batteries are batteries which can be used (charged and discharged) repeatedly. The achievable number of recharge cycles varies among technologies and is an important competitive factor. The main rechargeable battery technologies used by Saft are nickel and Li-ion. Rechargeable batteries based on these advanced technologies off er better and more reliable performance, especially under extreme conditions, and have a longer life, reducing replacement frequency and related costs, than batteries based on lead acid technology, an alternative technology used in industrial batteries.

A description of the main technologies used by Saft is set forth below:

nickel-based technology was developed in 1910 and remains, with lead acid, the main technology for industrial batteries. Nickel technology based batteries accounted for approximately 48% of the Group’s combined revenues in 2013;

primary lithium. Non-rechargeable lithium batteries, which were fi rst developed in the 1960s, possess high end storage and performance capabilities over a large range of formats. Primary lithium batteries accounted for approximately 30% of the Group’s combined revenues in 2013;

rechargeable lithium (Li-ion). Li-ion is a rechargeable lithium technology, developed in the early 1990s, that Saft expects will be increasingly used in advanced applications

in the aviation, defence and hybrid vehicle markets. Li-ion technology based batteries accounted for approximately 18% of the Group’s combined revenues in 2013;

other technologies. Silver-based technologies are used to manufacture batteries used in missiles and torpedoes. These batteries accounted for approximately 4% of the Group’s combined revenues in 2013.

1.3.2

APPLICATIONS AND MARKETS

Industrial Battery Group (IBG)

Presentation

Nickel-based batteries represent the traditional expertise of Saft’s Industrial Battery Group (IBG). On the foundations of this long heritage, the Group has successfully developed lithium-ion technology in order to meet the ever diversifi ed requirements of its customers, whose applications benefi t from the smaller, lighter, longer-life and versatile batteries that Li-on off ers. IBG is now going that extra mile in satisfying customer needs by off ering not only systems integration, for example in energy storage systems, but also full turnkey solutions that include services such as installations, commissioning and training across all its markets and segments.

Industrial Battery Group in 2013

The industrial Battery Group is the division which provided the growth for Saft in 2013. The telecom network back-up power segment made major breakthroughs with Li-ion batteries in India and a high level of sales of nickel batteries to US operators. The transportation activity also registered strong growth in both rail and aviation. Rail batteries destined for the Chinese mass transport and high speed train market were particularly successful in 2013.

The Energy storage battery market experienced contract delays this year although this segment remains very attractive for Saft for the future.

The Group’s growth strategy for the IBG division is based on continued success in nickel-based batteries and faster growth in new technology Li-ion battery systems which are opening up new opportunities in many of Saft’s industrial markets.

1.3 ACTIVITIES

GROUP PRESENTATION

1

ActivitiesMarket segments Stationary backup power

Industrial standby

Saft designs and manufactures batteries for industrial standby applications. These batteries are generally robust, have a long life and can perform under extreme conditions. Product applications are principally emergency power back-up systems in the following markets: oil and gas, power generation and distribution, railway signalling systems, in which the Group delivers the products directly to the end customers.

Growth in this sector is generally correlated with GDP growth, and in particular with capital expenditures in the industrial sector.

Telecommunications networks

Saft manufactures backup power stationary nickel or Li-ion batteries, in case of grid failure. Installed mostly in outdoor telecommunications terminals, these batteries face extreme conditions and/or for which maintenance is diffi cult and costly due to their remote location.

Growth in this market is generally driven by levels of capital expenditure in the telecommunications industry.

Energy storage systems (ESS)

Essential for the stability of the grid, energy storage also helps to smooth the peaks and troughs of renewable energy generation. Saft off ers battery solutions to ensure the constant reliability required to better integrate this intermittent energy. With high energy effi ciency, the range of Saft Li-ion batteries for these applications off ers high performance, long life and a limited maintenance.

Transportation

Rail transport

Saft supplies railway and mass transit operators as well as train manufacturers primarily with nickel-based batteries for back-up power communication, lighting, air-conditioning and critical safety applications such as emergency bracking and for door opening systems. Batteries supplied to the rail market must be reliable and able to withstand extreme conditions. They generally have a life of 10 to 15 years. The rail market is also demanding increasingly compact batteries with reduced maintenance requirements.

The replacement and refurbishment of rolling stock as well as investments in mass transport systems drive growth in this market.

Aviation

Saft is the world’s leading supplier of battery systems for the aeronautics industry (OEMs, distributors and airlines) and its batteries on board two thirds of the worldwide fl eet of civil and military aircraft. Saft nickel batteries are utilized mainly for power back-up and emergency systems, as well as for engine and turbine starting and fl ight preparation. Since the consequences of power failure are signifi cant for aircraft operators, batteries supplied to the aviation market must be highly reliable and durable, especially in extreme conditions. Although most of the batteries used in the aviation market are nickel-based batteries, Li-ion is an emerging technology in this market.

Vehicles

In this innovative sector, Saft develops and provides Li-ion battery solutions for both motorsports and industrial vehicles, such as forklift trucks in industrial infrastructure. Both sectors require high performance and effi ciency and Saft battery systems are particularly well suited to these innovative vehicles to optimize their duty cycle.

IBG competitive environment

For its nickel battery activity, Saft IBG is the leader on all its markets and faces competition mainly coming from Europe and India with smaller production capacity than Saft. However the main competition the Group faces is from lead-acid technology which has lower performance and a shorter life than nickel batteries, especially in diffi cult climatic conditions but also a lower initial cost.

For Li-ion, the range of competitors is wider and comes mainly from US and Asia. The Group’s fi nancial strength gives it the power to constantly develop new products and be present worldwide to keep its leadership position.

With its deep knowledge of high value-added markets for nickel-based activities, exciting new Li-ion opportunities, two new world class factories and its extensive sales network, Saft has a unique multi technology off er of high performance and competitive products.

Specialty Battery Group (SBG)

Presentation

Saft’s Specialty Battery Group is acknowledged as the world’s leader in the design, development and manufacture of high-performance primary lithium and lithium-ion (Li-on) battery systems. Those systems tend to be small, lightweight, resistant, reliant, powerful and long lasting, and they are developed to meet customer needs in the civil and military electronics industry, defence and space industries. Saft

GROUP PRESENTATION

1

Activitiesdevelops batteries for applications in cooperation with OEMs, which typically leads to a supply contract with an OEM and subsequent replacement sales to end users. The division also supplies silver-based batteries for conventional defence applications such as electric torpedoes.

Specialty Battery Group in 2013

The Specialty Battery Group had a more challenging year in 2013, with the civil electronics activity encountering lower demand for Saft’s high performance primary and rechargeable batteries for the utility meter markets, in particular in the US, and lower sales to the space and defence segment.

This division is also very well-positioned to benefi t from new opportunities opening up for new technology lithium-ion battery systems, in the space and defence markets, the o il and g as markets, marine applications and medical equipment for example.

Saft’s strategy for growth in this division is also based on off ering a range of high performance battery systems to multiple end markets requiring the technological advantages Saft’s products bring.

Market segments Civil electronics

With its two major brands, Saft and Tadiran, the Saft Group continues to be the world’s leading supplier of primary lithium technologies for the main targeted market segments. Generally speaking, Saft designs and manufactures lightweight, high-performance, highly reliable batteries tailored to the demands of OEMs.

Customers in this market include both specialized OEMs and distributors. Temperature resistance, long life, reliability and small size are among the most valued technical capabilities for batteries in this market. In general, prototypes are prepared to meet the specifi cations of the application and there is a period of tests before the batteries are selected by the OEM client. The qualifi cation and testing period can take up to two years before production begins. Given these requirements, once a battery manufacturer is qualifi ed as the supplier, it is generally in a strong position to remain the supplier for the life of the product. Sales to distributors involve standardized products and permits wider geographic coverage of sales. Space

Saft is the world’s leading company for the design, development and manufacture of Li-ion batteries for satellites used in communications, scientifi c and defence applications

and is continually breaking new ground in this area. Satellites represent the major share of Saft’s space activity. However, the Company also equips satellite launchers, where it has pioneered solutions based on lithium-ion technology combining lighter weight with improved thermal management. Saft remains the only manufacturer with a complete range of battery technologies for the space market.

Satellites require batteries that can withstand extreme conditions such as temperature variations and vibrations, operate reliably throughout the entire mission, and comply with strict size and weight constraints. Saft produces specialized batteries customized for the particular needs of each satellite. The development and production of a satellite battery typically takes approximately three years from initial inquiry to launch of a satellite. Demand is driven by telecommunications investment, defence budgets and scientifi c and special projects. Since it is impossible to replace a faulty item on a satellite, reliability and long life are the most important characteristics valued by customers.

Military activities

Saft is a leading designer, developer and manufacturer of high-performance lithium solutions for defence applications. These batteries power equipment ranging from communications systems, night-vision goggles to thermal-imaging cameras, missile launchers and military vehicles.

Military lithium (batteries used in portable devices) requires highly technical batteries that provide reliable power under extreme conditions with strict size and weight constraints. Sales of lithium batteries to the defence market are predominantly driven by sales of replacement batteries directly to armed forces. Once a battery supplier has qualifi ed with an OEM for an initial sale, replacement sales are made directly to the end-user, generally pursuant to multi-year contracts which are submitted for bids to qualifi ed suppliers. Long term customer relationships are particularly important because there is a need to collaborate with OEM customers to continually reduce the size and weight of batteries for these mainly portable applications. In the defence market, Saft designs and manufactures

silver-based batteries. These batteries are required to be robust, have a long shelf life and be resistant to shocks, and must be customized to each application:

Saft has a strong position in the silver based applications market, mainly silver-zinc batteries for torpedoes and missiles. Saft’s customers for applications using silver based batteries are mainly European OEMs that manufacture

GROUP PRESENTATION

1

Activitiestorpedoes, and with whom the Group has concluded long-term sales contracts. Shelf life and reliability are key purchasing considerations in this market.

I n the new defence systems market, Saft is developing batteries, in collaboration with OEMs, for advanced applications in the defence market based upon high performance Li-ion technology. Advanced defence systems are typically applications that require reliable, lightweight and high-energy power sources, such as smart weaponry, hybrid military vehicles and mini-submarines. By working with OEMs to develop applications for new defence systems, Saft, as a general rule, is able to secure supply contracts with OEMs for successful applications.

SBG Competitive environment

In primary lithium products, lithium batteries division of Saft SBG off ers a wide portfolio of technologies and has a leading position in its strategic markets. It faces competition mainly from Asian companies – a Korean company plus more than a dozen of small or middle sized Chinese companies - off ering a signifi cantly smaller choice of technologies with more limited performance. Only one or two of them are qualifi ed suppliers and all of them stay behind Saft’s brands in terms of technical capacity. In the military market segment, Saft has only one smaller competitor with a rather limited off er. Saft’s brands are leaders in all key segments of this market.

In rechargeable Li-ion, Saft SBG mainly addresses technically-driven niche markets, off ering complete battery solution. Competition varies depending on the market and is based in the United States, Europe and Asia. Asia, including Korea, China and Japan, has many manufacturers of cells dedicated to consumer products with which Saft does not compete. Saft has positioned itself on the segments with technically complex products and the highest requirements in terms of battery capacity or cell performance. Unlike many of its competitors who must incorporate cells into their products from various manufacturers, Saft can provide its strategic markets with complete in-house battery solutions, ensuring a strong position on the market.

In space activities, Saft is mainly competing with a large Asian company and a small European manufacturer. Its market share illustrates the weakness of these two competitors, Saft holding a position forefront with its higher technology and its capability to manufacture complete cells and batteries both in Europe and the United States.

In defence activities, Saft has no major competitor able to reach all regions and markets, but two serious competitors in the silver-based technology. However, Saft remains the leader through its technical expertise and signifi cant productivity eff orts. In Lithium-ion products, Saft faces multiple small to medium sized manufacturers of cells and batteries, most of the time regional manufacturers. With its two manufacturing centres of large capacity in Nersac and Jacksonville, Saft is able to off er competitive prices in this segment for high-volume operations using their cells or their complete battery solutions.

1.3.3

RESEARCH & DEVELOPMENT

If Saft has succeeded in establishing itself as a world leader in cell and battery systems, it is in large part thanks to the company’s long-term commitment to research and development.

Almost 500 engineers work on multiple R&D programs – basic electrochemistry research, new materials, improved production processes, design, development and enhancement, systems and software, data management, maintainability, and more.

A major portion of Saft’s R&D work is dedicated to creating new, cost-competitive products meeting specifi c customer application needs and off ering very near-term benefi ts. In 2013, Saft again invested more than €55 million in research and development, representing more than 9% of sales. R&D headcount further increased to 465. In 2013, ten new patents were fi led, adding to Saft’s portfolio of patent families of around 141.

Li-ion technologies, the major growth area for Saft, represent some 70% of the Company R&D investment, in the quest for new chemistries and new cell formats for next generation solutions and systems integration.

P rimary lithium represents another area of signifi cant growth opportunities for Saft in the future. Therefore the R&D team also works on improving traditional primary lithium products as well as bringing new products to market.

F inally, R&D engineers continue to enhance Saft’s nickel-based products to bring greater benefi ts to customers. To be effi cient, R&D teams work closely with the Group’s sales and marketing services that are deployed in 30 sales offi ces located on fi ve continents.

GROUP PRESENTATION

1

ActivitiesLi-ion, a promising future

Thanks to its R&D advances, Saft is now a multi-chemistry lithium-based battery provider. Our lithium-ion chemistries are now in production and shipping from the Jacksonville and Cockeysville plants in the USA and from the Bordeaux and Nersac factories in France. So today, Saft is meeting multiple needs thanks to its portfolio of technologies.

Other Li-ion chemistries are under development and coming out of the pipeline. Considerable development eff ort has gone into Super-PhosphateTM lithium-ion technology, including software to predict and manage performance, lifetime and safety.

Cell and system development

Of Saft’s overall R&D investment, around 10% is dedicated to long-term research, where the Company continues to focus on new materials, new chemistries and new processes. This will lead to improved performance and lower cost products for the future. In addition, research is also expanding the work on models and algorithms to support system development. In the shorter term, the R&D teams have further intensifi ed their systems development activity to integrate power

electronics and software so as to off er customers complete, customised solutions. The Systems Development Unit (SDU based in Bordeaux) is the fastest growing team in Saft’s R&D community, and a SDU unit has also been created at the Jacksonville lithium-ion plant in the United States, whose engineers have the task of integrating specifi c US needs into the systems. SDU continues to work on several programmes to improve the system content of Energy Storage Systems, off ering more energy and more power at a more competitive price in the market. In further developing systems, the R&D teams enable Saft to deliver more content to more applications, and therefore expand the product portfolio.

Turnkey solutions, which customers increasingly demand, are high on the priority list of Saft R&D. Much of the focus here is on maintainability. With systems that have a service life of 20 years or more, maintenance is important. Maintainability needs to be integrated in initial design – so that the electronics are easily accessible for service technicians and safe to handle. This requires new and more stringent modular design criteria that the R&D engineers are developing for future products.

GROUP PRESENTATION

1

Sustainable development1.4 SUSTAINABLE

DEVELOPMENT

In designing and manufacturing products that contain chemicals, Saft strives to make effi cient use of resources and reduce the environmental impact to a minimum. This is achieved by improving performance, extending lifetime and reducing the weight and footprint of the products. It can also be enhanced by saving energy and minimising the CO2 emissions of its factories. Saft supports end-of-life battery recycling and the use of recycled materials. These actions are all included in programmes Saft has introduced to preserve the environment.

Saft continues to make every eff ort to protect people and the planet, while bringing benefi ts to the users of its products. The Group uses a set of Key Performance Indicators (KPIs) to monitor the environmental performance. These KPIs assist the Group in monitoring the impact of its activity on the environment and the results of the Group’s eff orts. In most cases, these KPIs show the Group is making good progress. In addition, all Saft sites in Europe and China are now ISO 14001 certifi ed.

The Company contributes to protecting the environment through its end-of-life programmes, where Saft is fully compliant with national laws. An important element is the Saft “take-back” programme. For many years, Saft has encouraged, on a voluntary basis, that used Saft nickel-based batteries be returned by end users to bring-back points for recycling. Now that this is an EU wide requirement, Saft goes beyond the legal demands. The programme has been extended geographically to cover 31 countries, well beyond the EU-27 area.

Re-cycling and life cycle assessment

Recycling has long been a policy at Saft. All products are recycled back into the manufacturing process. With nickel-based batteries, for example, recycled cadmium is used to produce new batteries, while nickel is re-used either in batteries or in other industries.

The Group also carried out a full Life Cycle Assessment (LCA) on primary lithium batteries for metering devices. LCA involves

measuring impacts at diff erent phases of a component or system life to detect where improvements are needed to reduce (inter alia) CO2 emissions or energy usage. This can lead to changes in design or materials or in the manufacturing process. Saft is the fi rst battery supplier to conduct such an LCA, and utility companies appreciate the initiative.

Plants and products

Saft actively promotes the principles of sustainable development, organised into three areas: society, economy and environment. A reporting process on indicators has been set up to measure the Group’s performance in these areas. Data is collected on these non-fi nancial indicators every year and published in this Registration Document. In order to show its commitment and give more weight to these indicators, Saft began in 2011 to have them audited externally. In 2012, Saft has completed a greenhouse gas audit on its French sites. This audit covers direct emissions and indirect emissions linked to energy. In 2013, Saft had the 42 social, societal and environmental indicators audited as part of the French Grenelle 2 law.

Saft is also very involved in the practice of eco-design. Product developers are co-operating with recyclers to understand the constraints and costs of design to recyclers. Developers are seeking to include recycling-related constraints in initial design without impacting products performance. In 2013, Saft joined the new programme of the European Commission which aims at establishing a single market for green products and to facilitate improvement of information on the environmental performance of products and organizations. Saft is expert and very active in the Rechargeable Batteries project, led by the Association RECHARGE.

Health and safety

The Group makes every eff ort to fully comply and exceed legal health and safety requirements to reduce risks and uses a number of indicators which demonstrate risks are controlled. These indicators continue to show progress year on year.

GROUP PRESENTATION

1

Organisation and locations1.5 ORGANISATION AND LOCATIONS

1.5.1

AN ORGANISATION AND INTERNATIONAL PRESENCE SUPPORTING

THE GROUP’S DEVELOPMENT

The Group is organised around the holding “Saft Groupe SA”. The Group organisation chart at December 2013 is detailed in chapter 8 of the Registration Document.

AN INTERNATIONAL PRESENCE AND AN ORGANISATION ADAPTED TO CUSTOMERS’ NEEDS

Specialty Battery Group production site Industrial Battery Group production site Saft sales network

ASB (50% Saft, 50% EADS)

In total, Saft employs 3,856 people across 18 countries, with: 14 production sites;

30 sales offi ces.

Saft has been historically present in Europe and the United States, but is constantly developing in emerging countries, including Asia, South America and Russia.

Each Saft division has its own sales team, though if the customer situation demands, one division can work with the other in certain markets. The Industrial Battery Group (IBG) sales and marketing teams comprise 213 people. They are organised by geographic zone, whereas the Specialty Battery Group (SBG) sales teams of 77 people are structured by brand. In certain markets or regions, the sales teams are complemented by agents or distributors with whom the Company has been working for several years.

GROUP PRESENTATION

1

Organisation and locations1.5.2

CORPORATE GOVERNANCE ENSURING

THE BALANCE OF POWERS

The Saft Group has governance bodies whose operating principles are transparency and dialogue. It is guided by the applicable recommendations and stipulations of Afep-Medef consolidated Code of Corporate Governance for listed companies issued in June 2013 and of AMF.

The Saft management team is driven by a long-term vision. It is recognised for its stability and its international experience. Since Saft has been listed on the Eurolist market of Euronext in June 2005, the Group has had a Supervisory Board and a Management Board:

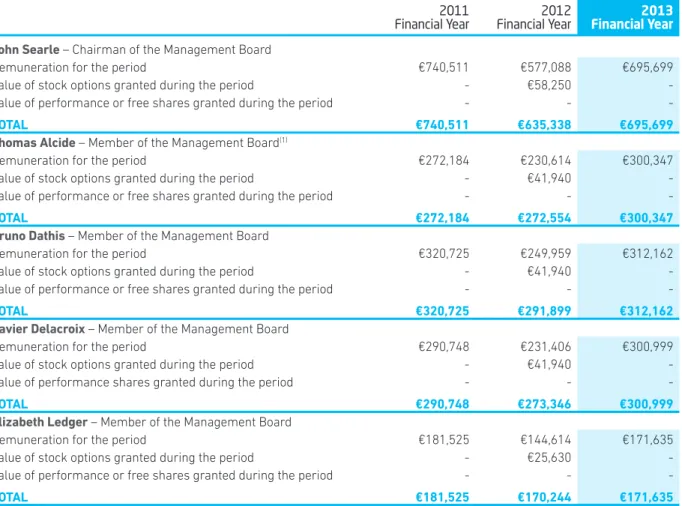

The Management Board is appointed by the Supervisory Board. It has the most extensive powers to act under any circumstances in the Company’s name. It decides the strategy and priorities for Saft’s activities. It is composed of fi ve members:

John Searle, Chairman;

Thomas Alcide, General Manager of SBG and President of Saft America Inc.;

Eliz abeth Ledger, Director Corporate Communications & Institutional Relations;

Bruno Dathis, Chief Financial Offi cer; Xavier Delacroix, General Manager of IBG.

The Supervisory Board exercises permanent control over management of the Board of Directors and its members are appointed by the Shareholders’ General Meeting for a three-year term. It is composed of fi ve members:

Yann Duchene, Chairman;

Jean-Marc Daillance, Vice-chairman; Charlotte Garnier-Peugeot;

Bruno Angles; Ghislain Lescuyer.

The Supervisory Board is assisted in its functions by an Audit Committee, a Remunerations and Nominations Committee and a Strategy and Technology Committee. A Management Committee also exists within the

Group, which serves as a forum for discussing and for implementing the Group’s strategy. In addition to the members of the Management Board, the Management Committee comprises:

François Bouchon, Director of the Energy Storage Unit; Igal Carmi, General Manager of Tadiran Batteries Ltd.; Franck Cecchi, Director Li-ion Operations;

Kamen Nechev, Chief Technology Offi cer.

Information relating to Saft Group governance is described in chapter 4 of this Registration Document.

GROUP PRESENTATION

1

Key fi guresCONSOLIDATED SALES BY ACTIVITY

(in € million) 298.9 320.5 367.9 2011 2012 2013 Industrial Battery Group 271.1 277.5256.3 2011 2012 2013 Specialty Battery Group2013 CONSOLIDATED SALES BY MARKET SEGMENT

22%

Transportation

16%

Space & defense

37%

Stationary*

25%

Civil electronics

*Including sales of electrodes to Arts Energy

1.6 KEY

FIGURES

ANNUAL SALES GROWTH OF 7.5% AT CONSTANT PERIMETER AND EXCHANGE RATES.

NET INCOME UP 5.2% TO €36.5 MILLION.

SALES

(in € million)577.4 598.0624.2

GROUP PRESENTATION

1

Key fi guresEBITDA

(in € million) 108.9 102.5 92.5 2011 2012 2013NET INCOME

(in € million) 75.2 34.7 36.5 2011 2012 2013EBIT

(in € million) 80.9 69.8 54.5 2011 2012 2013SHAREHOLDER’S

EQUITY

(in € million) 405.0 394.4415.5 2011 2012 2013NET INCOME FROM

CONTINUING OPERATIONS

(in € million) 51.6 42.0 41.7 2011 2012 2013NET DEBT

(in € million) 71.8 103.0111.6 2011 2012 2013GROUP PRESENTATION

1

Shareholders and stock market information1.7 SHAREHOLDERS AND STOCK

MARKET INFORMATION

IDENTIFICATION

Listing: Euronext Paris

Market: Eurolist Compartiment B

Indexes: SBF 120, CAC Mid 60, CAC IT, CAC Industrial Index ISIN code: FR 0010208165

Eligible security for French equity saving plan (PEA) and for deferred settlement service (SRD) for long positions.

FINANCIAL

CALENDAR 2013

Q1 turnover April 24, 2014 Shareholders general annual meeting May 12, 2014 Q2 turnoverand half year earnings July 23, 2014

Q3 turnover October 23, 2014

CAPITAL DISTRIBUTION*

THE SPLIT BY REGION IS AS FOLLOWS:% 6 . 4 8 Institutional shareholders % 1 . 5

1 Individual shareholders including management of the Group

0.3% Treasury stock 33.4% North America 14.6% United Kingdom 32.0% France 18.9% Other Europe 1.1%

Rest of the world

* Based on an analysis of shareholdings as of January 2, 2014.

MAIN SHAREHOLDERS

Harris Associates: 8.42%

Schroders

Investment Mgt: 5.98%

Carmignac Gestion: 4.34%

Caisse des Dépots

et Consignation: 4.10%

DIVIDEND

FOR THE YEAR

2012 0.75 2011 1.72 2010 0.70Saft will propose an ordinary dividend of €0.78 per share to shareholders at their annual General Meeting in May 2014.

SAFT SHARE PRICE INCREASED BY MORE THAN 41% IN 2013,

OVER PERFORMING MAJOR PARIS STOCK EXCHANGE INDICES.

GROUP PRESENTATION

1

Shareholders and stock market informationSTOCK MARKET INFORMATION

(in euros)SHARE PRICE

0 50 100 150 200 250 300 350Base 100 on January 1, 2013 (in thousand shares)Share volume

January 2013

Feb. March April May June July Aug. Sept. Oct. Nov. Dec. January 2014 90 100 110 120 130 140 150 160

Saft SBF 120 CAC 40 CAC Mid 60 Volume

Share price (in euros) 2013 2012 2011

Highest 25.000 24.900 31.600

Lowest 16.670 16.335 18.995

Closing price for the year 25.000 17.700 21.850

Change in the year 41.24% (18.99)% (20.69)%

Change in the CAC 40 index during the year 17.99% 15.23% (16.95)%

Change in the SBF 120 index during the year 19.49% 16.50% (16.21)%

Change in the CAC Mid 60 index during the year 26.83% 23.00% (21.58)%

Stock market capitalisation at December 31 (in million euros) 646 446 550

Annual transaction volume (millions of shares) 11.52 12.34 21.31

Number of shares comprising the share capital at December 31 25,853,811 25,174,845 25,174,845

GROUP PRESENTATION

2

Risk Factors

2.1

Risks related to the market

environment and the Group’s activities 22

2.1.1 Risks related to exposure to a high level of competitionand price pressure 22

2.1.2 Risks related to technologies used 22

2.1.3 Risks related to development of new markets in which Saft

is making a signifi cant investment 23 2.1.4 Risks related to the Group’s dependence on certain customers

or core sectors 24 2.1.5 Risks related to the geopolitical environment 24

2.2 Operational

risks

25

2.2.1 Risks related to defective or poor quality products 25 2.2.2 Risks related to the ability to recruit and retain qualifi ed staff 25 2.2.3 Risks related to potential disagreements between Saft

and its partners relating to their joint subsidiaries 25 2.2.4 Risks related to purchases and suppliers 26 2.2.5 Risks of Internal Control failure and risks of fraud 26

2.2.6 Risks linked to information systems 26

2.3

Credit and counterparty risks

27

2.3.1 Credit risks 27

2.3.2 Counterparty risks 27

2.4 Liquidity

risk

27

2.5 Market

risks

27

2.5.1 Raw material price risks 27

2.5.2 Foreign exchange risks 27

2.5.3 Interest rate risks 28

2.5.4 Share price risk 28

2.6

Contractual and legal risks

28

2.6.1 Risks related to products sold 28

2.6.2 Risks related to export control 28

2.6.3 Litigation risks 29

2.6.4 Risks related to intellectual property 29

2.7

Risks related to the impact

of the Group’s business

on the environment, human health

and safety 29

2.7.1 Environmental risks related to operating factories 29 2.7.2 Risks related to the availability and use of chemical substances 30 2.7.3 Risks related to the end of life of products sold 30RISK FACTORS

2

Risks related to the market environment and the Group’s activities This section describes the signifi cant risks which the Groupconsiders it is exposed to through its activities and environment, as well as the steps taken to lower the probability of such risks materialising and to reduce their potential impact.

At the time that this annual report was prepared, the Company performed a review of risks that could have a material adverse eff ect on its business, fi nancial position or results and its ability to achieve its objectives, and it feels there are no risks, other than those listed below, that the Company deems relevant and meaningful.

Since 2004, the Saft Group has established a risk mapping process to identify the major risks to which it is exposed.

The risk mapping, which is updated regularly, ranks all risks identifi ed based on their potential impact, on the probability that they will occur and on an assessment of the level of control for each one of them. The process of evaluating risks is described in the report prepared by the Chairman of the Supervisory Board, presented hereafter in chapter 4 “Corporate Governance” of this annual report.

The most recent risk mapping update, conducted at the end of the 2012 fi nancial year, showed that the major risks to which the Group is exposed are those listed below in paragraphs 2.1.2, 2.1.3 and 2.2.1.

2.1 RISKS RELATED TO THE MARKET ENVIRONMENT

AND THE GROUP’S ACTIVITIES

2.1.1

RISKS RELATED TO EXPOSURE

TO A HIGH LEVEL OF COMPETITION

AND PRICE PRESSURE

Types of risks

Certain segments of the Group’s activities are exposed to competition from low-cost battery producers, mainly in Asia. The pressure that this competition exerts on prices could force the Group to reduce its prices, leading to a contraction of its margins.

Moreover, the possible relocation of some of the commercial or manufacturing operations of the Group’s customers to Asia or other lower labour cost countries could lead to these customers deciding to source their batteries from competitors of the Group already located in these territories. This could have a considerable negative impact on the Group’s business and its results.

Risk management

In order to minimise this risk, the Group prioritises its innovation strategy, with the aim of diff erentiating itself from its competitors in terms of the products it off ers, while also seeking to improve its competitiveness. The Group has therefore implemented an investment policy in some low labour cost countries, such as the Czech Republic, China, India and Brazil, by setting up commercial units and/or manufacturing facilities there. In 2013, the Group created a subsidiary in Russia in order to develop sales of its products, then in the future to perform assembly of certain of its products.

2.1.2

RISKS RELATED TO TECHNOLOGIES

USED

Loss of the Group’s competitive advantage

in an environment of fast changing

technological development

Types of risks

Saft’s business is focused on specialised markets for advanced technology batteries. Saft holds leading positions(1) in many of these markets because it provides high value-added products based on innovative technologies and its ability to customise its products according to changes in the specifi cations of its customers. However, the batteries market involves rapidly evolving technology. Therefore, it cannot be ruled out that the technological advances in the manufacture of batteries will not aff ect the competitiveness of the products made by Saft and lead to a loss of the competitive advantages currently held by the Group.

Risk management

To develop and gain access to new technologies, the Group channels signifi cant resources into Research and Development. Accordingly, over the last three fi nancial years, the Group has invested the equivalent of 9.5% in 2011, 9.0% in 2012 and 9.3% in 2013 of its revenue in Research and Development.

RISK FACTORS

2

Risks related to the market environment and the Group’s activitiesUncertainties with regard to the success

of lithium-ion technology

Types of risks

The Group currently develops and sells lithium-ion battery components and systems, which it believes will enable it to meet a range of requirements in a number of evolving sectors, notably those regarding storage of renewable energy and traction batteries. Saft has thus invested in the construction of a manufacturing plant for lithium-ion cells and batteries in Jacksonville, Florida (USA) and acquired the lithium-ion cell-manufacturing unit located in Nersac, France from Johnson Controls on 1st January 2013.

The Group cannot guarantee that this technology will be a success, and it cannot be ruled out that diff erent technologies will meet the same needs. Thus, some companies have recently developed batteries using emerging technologies that are likely to be in competition with the lithium-Ion technology developed by the Group.

Risk management

The Group has established a multi-year continuous development plan for this technology to best meet the expectations of the various markets addressed by the Group. In addition, it is pursuing Research and Development work in other technologies, while maintaining a forward-looking approach to its research activities at all times, and constantly monitoring the development of technologies that could potentially compete with lithium-ion.

2.1.3

RISKS RELATED TO DEVELOPMENT

OF NEW MARKETS IN WHICH

SAFT IS MAKING A SIGNIFICANT

INVESTMENT

Types of risks

The outlook for growth of the Group’s activities involving products to be manufactured at the Jacksonville, Florida (USA) and Nersac (France) facilities is, as with all commercial activities, subject to a certain number of risks. These risks are principally the following:

uncertainties related to the development of emerging markets in which Saft is positioning itself, with lithium-ion products: Those emerging markets have currently low production volumes, as for example, those relating to storage of renewable energy, as well as the markets for traction batteries for utility vehicles or buses. Moreover,

although the prospects for development of these markets over the next few years are generally considered as signifi cant, estimates relating to the level that these markets could reach vary signifi cantly and the exact pace of this development remains uncertain. Accordingly, the growth of these markets might not reach the expected levels, and the future profi tability of Saft’s investments therein could be aff ected;

dependence on national and international energy policies: The markets for energy storage are partly dependent on political decisions, both at the national and international level. These decisions may involve the introduction of subsidies and/or tax incentive mechanisms, or the adoption of various pieces of legislation;

impact of commodity and fossil energy prices: The development of certain new markets for which Saft is investing in new Li-ion production facilities in Jacksonville (USA) and Nersac (France) could be aff ected by fl uctuations in prices, supplies of raw materials and/or fossil energies (oil and natural gas, for example). A large decrease in the price of fossil energies could thus cause a fall in demand for lithium-ion batteries to be used for energy storage; exposure to competition: In certain new markets, and in

particular the markets for energy storage and traction batteries, Saft is exposed to strong competition:

some competitors, already present in these markets or seeking to establish themselves therein, may have more signifi cant commercial, fi nancial, technical or human resources than those of the Group,

some customers in these markets may consider insourcing the design or production of the type of components and products off ered by the Group. The pressure that this competition may exert on prices could force the Group to limit its prices and reduce its margins, and consequently could aff ect its ability to generate the expected profi tability in the anticipated timeframe. This could have a considerable negative impact on the Group’s business, fi nancial position and results.

Risk management

In order to limit these risks, the Group strives:

fi rst, to maintain a balance between existing profi table activities and markets and developing activities and markets that generally consume cash;

and secondly, to identify other markets or applications that can benefi t from the advantages of lithium-ion products for which Saft has made signifi cant investments.

RISK FACTORS

2

Risks related to the market environment and the Group’s activities2.1.4

RISKS RELATED TO THE GROUP’S

DEPENDENCE ON CERTAIN

CUSTOMERS OR CORE SECTORS

Types of risks

Saft’s sales are made to many industrial customers present in very diverse sectors such as the aeronautics and rail industries, road infrastructure, public transport, oil industry, telecommunications, gas and electricity production, defence and space. However, the Group makes a signifi cant portion of its sales to a few strategic customers. Thus, for the 2013 fi nancial year, the Group’s sales to its top 10 customers accounted for 26% of the Group’s consolidated revenue. The Group’s top customer in terms of revenue in 2013 accounted for less than 5% of consolidated revenue, as compared to less than 3% in 2012 and 2011.

Moreover, the Group’s revenue and operating profi t are partly related to the cyclical nature of certain activities. In particular, a signifi cant portion of the Group’s consolidated revenue is made from the Defence sector. In 2013, this represented 12.7% of consolidated revenue.

Defence spending for each country depends on a complex mix of geopolitical considerations and budgetary constraints. It may therefore vary signifi cantly from year to year. Accordingly, a reduction in defence spending or the postponement of particular programmes could have a negative eff ect on the Group’s sales, operating profi t and cash fl ow, as well as having signifi cant repercussions for certain production facilities.

Risk management

To limit this risk, Saft, on the one hand, constantly seeks to diversify its customer portfolio to avoid depending on a single client or on too limited a number of clients and, on the other hand, implements a global strategy aimed at striking a balance in its portfolio of activities.

2.1.5

RISKS RELATED TO

THE GEOPOLITICAL ENVIRONMENT

Types of risks

The Group carries out a signifi cant portion of its commercial and manufacturing operations in emerging countries, which have recently undergone or are likely to undergo periods of political or economic instability. In 2013, revenue recorded outside of the “Europe” and “North America” zones represented 35% of consolidated revenue. Moreover, some countries in which the Group operates have underdeveloped or un-protective legal frameworks, which can aff ect the Group’s ability to enforce contractual rights.

Saft is therefore exposed to risks that could aff ect its fi nancial position, notably:

a more restrictive control of foreign exchange that could limit or block a currency leaving a customer country and in turn its ability to honour its debts;

discriminatory measures taken against Saft that could pose a threat to the Group’s business in a particular country (expropriation, nationalisation, etc.);

an unexpected breach of contract or commitment; diffi culties in protecting the Group’s intellectual property.

Risk management

Although Saft’s growing internationalisation enables it to spread geopolitical risk, the Group makes every eff ort to identify ways of limiting the fi nancial impact of this risk. Where necessary, it may turn to insurers to take out appropriate insurance policies or resort to fi nancial payment hedging instruments for certain countries (bank guarantees, Coface guarantees, etc.).

RISK FACTORS

2

Operational risks2.2 OPERATIONAL

RISKS

2.2.1

RISKS RELATED TO DEFECTIVE

OR POOR QUALITY PRODUCTS

Types of risks

The success of Saft’s business depends on the quality of its products and its relationships with customers. As the batteries manufactured are often complex and are mostly used in critical applications, Saft cannot guarantee that its customers will not encounter defects or quality problems with its products. In the event that its products or services fail to meet its customers’ standards, Saft’s reputation could be harmed, which could adversely aff ect its marketing and sales eff orts, and therefore have an impact on its competitive position.

Risk management

In order to mitigate these risks, Saft operates detailed development, manufacturing and testing processes, as well as quality control procedures, at all times.

Furthermore, Saft has brought all of its continuous improvement processes for quality and performance under a global umbrella programme called Saft World Class. Proven quality management procedures are thus deployed at all group sites:

quality standards: all of the Group’s sites have ISO 9001 certifi cation and most of them have supplementary certifi cations depending on the requirements of their markets;

the 5S and visual management: each Saft production facility employs this type of management so that any anomaly can be rapidly identifi ed and corrected. The methods for problem resolution such as the 8D are also implemented in the Group;

process management: relies on various tools, such as equipment design standards, error-proofi ng systems and Statistical Process Control (SPC).

2.2.2

RISKS RELATED TO THE ABILITY

TO RECRUIT AND RETAIN QUALIFIED

STAFF

Types of risks

Saft’s success is highly dependent on the quality and experience of its management team, and of key employees responsible for manufacturing processes and Research and Development. These highly qualifi ed employees have generally been at the Group for a number of years, and have an excellent knowledge of its business and the sectors in which it operates. The departure of one or more managers or

key employees could lead to a loss of expertise and aff ect the Group’s ability to grow some of its businesses or attain certain strategic objectives.

The Group’s future success will partly depend on its ability to attract, train, motivate and retain highly qualifi ed employees and managers. However, given the intense competition to attract employees with such qualifi cations, there can be no assurance that Saft will be able to do so.

Risk management

In order to limit the impact of this risk, Saft has put in place a number of human resource management programmes based on anticipating needs and retaining staff :

drafting of a succession plan for key employees;

implementing a process for rewarding performance and retaining staff such as:

development of geographical and functional mobility, implementation of a skills development and support for

change policy through trainings,

implementation of an attractive remuneration system. These measures are described in more detail in section 3.2 “Social Responsibility” of this annual report.

2.2.3

RISKS RELATED TO POTENTIAL

DISAGREEMENTS BETWEEN SAFT

AND ITS PARTNERS RELATING

TO THEIR JOINT SUBSIDIARIES

Types of risks

As part of its manufacturing and commercial activities and in line with its strategic goals, Saft may decide to enter into joint venture agreements with specifi c partners. Should the relationship between Saft and any of its partners deteriorate, or the terms of their agreement no longer be respected, Saft’s assets and commercial activities could be aff ected. Furthermore, any dispute between the parties, management disagreement or any decision to terminate the joint venture agreement could have a material adverse impact on the Group’s commercial activities.

Risk management

In order to limit the risk inherent in any partnership and to safeguard its interests as best as it can, Saft endeavours to ensure that any such agreements contain a certain number of governance rules regarding the joint management of the Company including, for example, the need for the two parties to agree on all important decisions.

RISK FACTORS

2

Operational risksAt present, the Saft Group’s only joint venture is ASB, in which it holds a 50% interest, the same as the EADS group. This company mainly produces thermal batteries for military use. Shareholder relations are governed by a shareholder agreement, which was renewed in 2006. This agreement contains provisions designed to protect the Group’s interests, notably in the event of a change in control, as described in the “Additional information” section of the annual report.

Note 28 to the consolidated fi nancial statements details the key fi nancial data concerning the Saft Group’s joint venture as at the end of the 2013 fi nancial year.

2.2.4

RISKS RELATED TO PURCHASES

AND SUPPLIERS

Regulatory risks related to purchases

Types of risks

The Group is subject to a large number of regulations at the local, European and international levels in relation to its purchasing activities.

Non-compliance with these requirements would entail legal and fi nancial risks and in some cases restrictions on access to public sector contracts. Saft therefore takes particular care in ensuring it complies with these regulations.

Risk management

In order to mitigate these risks, the Group’s buyers are regularly informed of changes in the legal and regulatory framework in which they operate. Moreover, compliance with certain legislation is subject to specifi c monitoring, for example, the European regulation on chemical substances, “REACH” programme (Registration, Evaluation, Authorisation and Restriction of Chemicals).

Supplier risks

Types of risks

As with any manufacturing company, Saft is exposed to a risk related to the quality and durability of its raw materials and components supplies. Like any company that manufactures high technology products, Saft regularly uses a number of suppliers of specialised products. If one or more of these suppliers were to fail, it could have a signifi cant impact on the Group’s business and fi nancial performance.

Risk management

In order to limit these risks, each unit has supplier risk evaluation procedures in place, at least annually, as does the management of the Group’s Purchasing Department. In addition, progress plans and specifi c action plans are regularly drawn up and implemented according to the risk levels identifi ed.

2.2.5

RISKS OF INTERNAL CONTROL

FAILURE AND RISKS OF FRAUD

Types of risks

Saft’s international profi le means that its administrative, fi nancial and operational processes are managed in various legal and regulatory environments, with varying degrees of Internal Control and risk management sensitivity from one entity to another. Moreover, they may be managed with diff erent information systems.

In this context, Saft cannot rule out a failure of Internal Control or an instance of fraud that could have a signifi cant fi nancial impact and/or harm the Group’s reputation.

Risk management

In order to mitigate these risks, Saft has set up a review process of its Internal Control, based on a set of rules and procedures that it has circulated to all its subsidiaries. In addition, regular audits of diff erent group sites or audits of processes are carried out according to a programme established and approved annually by General Management and the Audit Committee. Lastly, Saft has implemented a number of initiatives to raise the awareness of employees of risks relating to fraud, corruption or non-compliance with the Group’s rules of ethics.

The process of evaluating risks is described in greater detail in the report prepared by the Chairman of the Supervisory Board, presented hereafter in section 4 “Corporate Governance” of this annual report.

2.2.6

RISKS LINKED TO INFORMATION

SYSTEMS

Types of risks

Daily management activities include purchasing, production and distribution, billing operations, reporting and consolidation as well as exchange and access to internal information. It is based on a proper functioning of technical infrastructure and applications. The risk of failure or shutdown of systems and the risk of cybercrime or industrial espionage can not be ruled out, which could lead to signifi cant fi nancial impact and / or damage the image of the Group.

Risk management

To minimize the impact of these risks, the Direction of Information Systems of Saft Group has established strict rules on data backup, protection and access to confi dential data, security of materials and applications. In addition, the Group has implemented and released an IT charter that defi nes best practices and responsibilities to contribute to IT security.