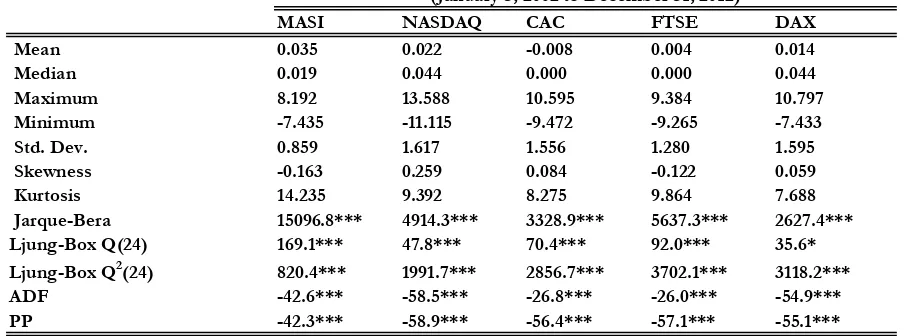

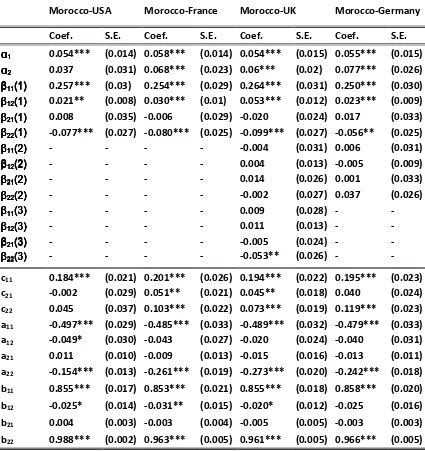

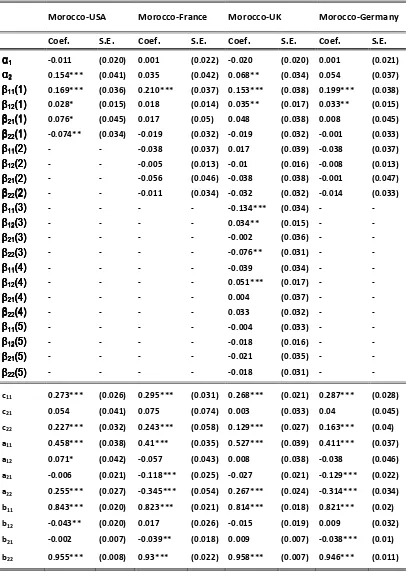

Return and Volatility Spillovers in the Moroccan Stock Market During The Financial Crisis

Full text

Figure

Related documents

The population of interest will be derived from primary care, through the clinical practice research data-link (CPRD, n=10M) and the student will use electronic linkage to

A second difference between our model and most of the screening literature starting from Rothschild and Stiglitz (1976) is that we conduct our analysis in the contract space as

specialty marks, 0.807 in learning by rote, 0.527 in guided learning, 0.595 in independent learning and 0.463 in meaningful learning) with 65 0.05 degrees of freedom, indicating that

a) The survey of Institutions started with an enquiry to those State Organizations responsible for the articulation and decentralization of Plans and Programmes of Development

After skin contact: solid carbon dioxide may cause redness, frostbite and serious.

Note that the selection of a 10-min rain rate is not necessarily reflected by the overall performance of the rain gauge network (Table 2) mainly due to the high number of

Faculty members regularly work as consultants for business, government and not-for-profit organizations, serve on regional and national boards and contribute regularly to the