A

Diffe

Usin

Receive doi:10.5

Abstra In today strategi dynami really d market. to the l feasibil Indian s Black - market. the opti expecte price ha Merton of timin

A Feasi

erential

ng Histo

E-mai

ed: June 29, 5296/ajfa.v4

ct

y’s financia c decisions ic and unce difficult. Ma

The certain level of mi ity of Black stock excha

Scholes – Further the ion price an ed price as c

ave any sig model is m ng is more r

ibility A

l Equat

orical V

Stock

Dr. Shyam Associate

School il: shyamlal

, 2012 A 4i2.2022

al world the s can be ma

rtain nature any models nity of these

inimum dev k - Scholes anges. The r Merton diff e regression nd anova tes omputed by gnificant di more usefull relevenat fo

Analys

tion Mo

Volatili

k Optio

Dr. R Prof

m Lal Dev e Professor

of Busines dev@gmail

Accepted: J URL: htt

ere is a grea ade to mak e of the fina

have been d e models to

viation is q – Merton d result of thi ferential equ n analysis ha st has been y Black - Sc

ifference. T in call optio r put option

sis of B

odel for

ity : Wi

ons Tra

Rekha Kala fessor of Fin

Pandey (Co of Finance s, Bangalor l.com, shya

July 25, 201 tp://dx.doi.o

at need to pr ke short term

ancial mark developed t

predict the questionabl differential e

s study can uation mod as been use used to che choles – Mer The result o on pricing t n pricing tha

lack-Sc

r Stock

ith Ref

aded in

A.M. nance

orrespondin , Alliance U re, Karnatak amlal.pandey

12 Pub org/10.5296

redict the va m or long t kets, the pre to predict th

option pric e. This stu equation mo n be used to del to predic ed to see the eck whether rton differen of analysis

han the put an for call o

choles-Option

ference

NSE

g Author) University ka, India

y@alliance

blished: Dec /ajfa.v4i2.2

alue of the term capital ediction of t he option pri es to the mo udy is aime

odel for stoc predict the ct stock opti e impact of r the mean ntial equatio

found that option pric option pricin

-Merton

n Pricin

to Sele

.edu.in

cember 1, 2 2022

assets, usin l gains. Du the asset pr ices in the f ost accurate ed at analyz

ck option pr suitability ion prices in

time to exp difference b on model an

Black - Sc cing and also

ng.

n

ng by

ected

2012

ng which ue to the rices are financial e level or zing the ricing in

Introdu Finance cornerst financia to shift markets derivati tax-ded The day finance In the l product market particip to deter option p to the Black-S model u model i constan In the m promine the Nob one of t

Black– The dat rate and hedge p The hed will alw be deter factors, portfoli

BLACK uction e is one of th

tone of the al instrumen ts in econo s have conti ives, altern ductible equ

ys have gon now area o last 30 year ts serve the and risk m pants. Pricin

rmine call a prices in the

most accur Scholes mod uses ideas f involves cer nt volatility modern finan

ent place sp bel prize for the receipien

–Scholes mo ta inputs to t d time to ex portfolio com

dge portfoli ways be equ rmined by t the portfol io and the ac

K – SCHOL

he most dyn e free enter nts have bec

mic conditi inued to pro native risk

ity.

ne when sim of finance is

rs derivativ vitally imp managemen ng is very im

and put opt e financial m

rate level del is consid from the Bro rtain inheren during the t nce theory B pecially afte r economics nt of the pri

odel

this model a xpiry. In thi

mprising a l io will be co ual to the opt the Black-S lio mix has ct of mainta

LES FORM

namic area i rprise syste come comp ions. In tod oduce a mul

transfer p

mple busine s controlled ves have be portant econ

t tools by mportant in o tions prices market. The or to the dered as a v ownian mot nt assumptio tenure of th Black - Sch er 1997 whe s. Sadly, Fis

ize (Hull &

are current s s model pri long positio onstituted in

tion’s price Scholes form

to be const aining the p

MULA FOR ∗

∗

in the mode em. Due to plex and it i

day’s highl ltitude of ne products, ex

ess graduate by mathem ecome incre nomic funct facilitating options cont s. Many mo

certainity o level of m very elegant tion and oth ons such as he option, in holes – Mert en Robert M scher Black

Basu 2010

stock price, icing of an on in stock a n such a wa e at that time mula.As the tantly adjus portfolio in b

R OPTION

1 ∗

∗ 2

ern corporat high volat s undergoin ly volatile ew products xchange tra

es were ma maticians and

easignly im tions of pric

the tradin tract. Option odels have b of these mod minimum de t piece of re her theories

log-normal nterest rate, ton differen Merton and k died in 199

).

exercise pri option invo and a short p ay that at an e. The propo e formula c sted. So the

balance is c

N PRICING

∗ 2

∗

e arena and tility and u ng constant and dynam s including m

aded funds

anaging the d computer mportant in f ce discovery

g of risks ns traders us been develo dels to predi eviation is esearch into s based on ‘

l distribution exercise pr ntial equatio Myron Sch 95, otherwis

ice, expecte olves constru position in a ny given poi ortion of sto onsists of c

portfolio is alled as hed

G: 2

1

d in a real se uncertain be

change in r mic world, f many new f s, and vari

world of c r scientists. finance. De ry in the un

among the se a pricing oped to pre ict the optio questionab o option pric

random wa n of the stoc rice and stoc on model (19 holes were a se he too ha

ed volatility, ructing a rep a zero-coupo int of time i ocks and bo constantly c s called as d dge rebalanc

ense, it is ehaviour response financial forms of iants of

orporate

erivative derlying e market

formula edict the on prices ble. The

ces. The alk’. The ck price, ck price. 970) has awarded ave been

Here in N(.) = c ln = Na S = Spo X = Exe r = Ann t = Tim = An One of t dividen analysis paymen

BLACK

Here in d = Ann

Problem Using th prices f compar Merton

Objecti 1.

n this formul cumulative n atural logarit

ot price of st ercise price nual risk fre me to expiry nnual volatil the assumpt nd. This can s of Black & nts. So this h

K – SCHOL

n this case, nual dividen

m Statemen he Black – for various e re it with t (B-S-M) m

ives

To test the la,

normal dist thm tock

e of the optio e rate of ret

of the optio lity of the st tions and lim nnot be the & Scholes m helped in ov

LES – MER

nd yield

nt

Scholes – M expiry dates

the actual odel is feas

viability of

1 ln

2

ribution fun

on turn on

tock mitations of

case with model in wh ver coming

RTON FO

∗ ∗

∗ ∗

1 ln

2

Merton mod s through da

stock optio ible in pred

f Scholes –

∗ √

1 ∗

nction

f the Black – all the asse hich he sugg

one of the l

ORMULA: 1

2

∗ √

1 ∗

del to calcula ata gathered on price, t dicting optio

Merton mo

2 ∗ √

∗ √

– Scholes m ets. In 1973 gested adjust limitations

∗ ∗

∗ ∗

2 ∗ √

∗ √

ate the expe d from NSE o find out on prices in

odel using re

model is that 3, Robert M

tments to ta of Black – S

2

1

∗

ected call op E website fo whether B Indian mark

eal time data

t the asset p Merton prov

ake care of d Scholes mo

ption and pu or stock opti Black – Sc rket.

a from NSE

ays zero vided an dividend odel.

ut option ions and choles –

2.

3.

4.

Resear In this r Black – expecte compar Black-S

Data C This res (NSE) d similar ending differen trade.

Tools o Study i derivati ANOVA ratio etc

Hypoth H1: The model b H2: Th actual o H3: Bla otion pr

Literat Numbe Black a bias wi

To test the real time d To measur Scholes – M To test the actual price

ch Design research pap – Scholes - M ed price of o re it with the Scholes-Me

Collection M search is ba derivative s

subject. Re with 29/9/2 nt industries

of Analysis s based upo ive segment A has been c.

heses ere is no sig by taking hi ere is no im options price ack- Schole

rice.

ture Review er of studie and Scholes ithin the B

feasibility data from NS

re the impac Merton mod

significanc e.

per, real tim Merton mod option. We e calculated rton model

Methods an ased on rea egment. Ot al time data 2011. To m s has been

on applicati t. For the t used. Othe

gnificant dif istorical vol mpact of len

e.

- Merton m

w

es can be t s (1973) stu lack-Schole

of Black – S SE.

ct of change del. ce of the dif

me values ar del are calcu

also take t d price of op

is feasible f

d Sources al time seco

her relevant a has been ta make this st

picked up o

ion of black testing purp er statistical

fference bet latrility and

ngth of tim

model gives i

traced out udy that was

es model in

Scholes – M

es in time to

fference betw

re taken from ulated and s the actual p ption. Throu

for option p

ondary data nt informatio aken for eac tudy more f on the basi

k scholes m pose Paired l tools used

tween the ex actual price me to expiry

identical res

on black s s based on n terms of

Merton mod

o expiry on t

ween the m

m the NSE w substituted i

rice of the ugh this we pricing in In

collected fr on has been ch trading d feasible 5 d

s of market

model and t Samples T in study in

xpected opti e determine y on the diff

sult for both

scholes mod an empirica moneyness

del in Indian

the option p

mean of estim

website and in formula a

option from come to a c ndia.

from Nation collected fr day starting w

different sto t capitalizat

testing of th Test, Regres clude Stand

ions price c ed by marke fference betw

h call option

del. Here w al investiga s and matu

n scenario b

prices using

mated price

d the compo and we arriv m NSE web

conclusion

nal Stock E from past stu

with 16/8/2 ocks represe

tion and vo

his model in ssion Analy dard deviatio

computed by et forces. tween expec

n price as we

we are starti ations and c urity. MacB

y using

Black –

and

onents of ve at the bsite and whether

xchange udies on 2011 and enting 5 olume of

n indian ysis and on, beta,

y B-S-M

cted and

ell as put

Mervill (CEV) m Gonede In the m promine the Nob one of t Bhattac ideal co applicat Radu, T STOCK type: ∂V constan dividen Heston, Black-S differen provide elasticit solution arbitrag satisfied lookbac Ross. Scott M investig evaluate

1 MacBe models.

2

Blattb statistica

3

Bhatta Journal

4

Turcan p795-79

5

Heston Mar200 6 McKen model:e Journal,

le (1980)1 t model, whi es (1974)2 s modern finan

ent place sp bel prize for the receipien charya, M. (

onditions, e tions in the Turcan(2010 KS OPTION V/∂t + 1/2σ² nt and conti nd are depen , Steven L Scholes-Me ntial equatio e new solut

ty of varian ns reflect a ges. We pro d, put-call p ck calls hav

McKenzie, gation of th

es the prob

eth, J. D., an Journal of fi berg, R. C., a

al models for

acharya, M. of financial

n. (2010) An 99,

n, Steven L.; 7, Vol. 20 Iss nzie, S.; Gera

vidence from , 1(4), 2007.

ested the B ch assumes suggest vola

nce theory B pecially afte r economics nt of the pri 1980)3 in h xamined th 21st centur 0)4,in their NS” mentio ²S²∂²V/²S² + inue dividen ndent on tim L.; Loewen rton option on (PDE). B

ions for the nce (CEV) asset pricin ovide condi parity might

e infinite va

Dionigi Ge he Black-Sc bability of

nd Merville, L finance, 35(2) nd Gonedes, r stock prices

(1980). Emp and quantita

nals of the U

Loewenstein sue 2, p359-3 ace, D.; and m the Austral

lack – Scho volatility c atility of the Black - Sch er 1997 whe s. Sadly, Fis

ize (Hull & his paper Em he "Black-S

ry economy paper “BL oned that Pa

rS ∂V/∂S - r nds or in ev me.

nstein, Mar n valuation But this met

e Cox-Inger model, an ng bubbles,

itions to rul t not hold, A alue. We cla

erace, Zaff choles mod

an exchang

L. J. (1980). ), 285-301.

J. (1974). A s. Journal of

pirical proper ative analysis

University of

n, Mark; Wil 390, 32p d Subedar, Z.,

lian Stock Ex

oles model changes whe e underlying holes – Mert en Robert M scher Black

Basu 2010 mpirical prop

choles" me y.

LACK-SCH artial differ rV=0 is use valuate opt

rk; Willard n method i thod can ge rsoll-Ross ( nd the Hest dominated le out bubb

American c arify a long

far Subedar del: Eviden ge traded E

Tests of the B

A comparison f business, 4

rties of the B s, 15(5), 108

f Oradea, Eco

llard, Gregor

, (2007)An e xchange, Aus

against the en the stock g stock is st

ton differen Merton and k died in 199

).

perties of th ethod for pr

OLES MOD rential equa ed in evaluat ions in whi

d, Gregory involves de enerate mul

(CIR) term ton stochas d investmen bles on und calls have n standing co

r, (2007)6 nce from th

European ca

Black-Schole

n of the stabl 7(2), 244- 28

Black Scholes 81-1105.

onomic Scien

ry A.(2007),

mpirical inve stralasian Ac

constant el k prices chan

ochastic and ntial equatio

Myron Sch 95, otherwis

he Black Sch icing, its fu

DEL USED ation, parab

ting equity o ich interest

A (2007) eriving and

tiple values structure m tic volatilit nts, and (p erlying pric no optimal e onjecture of

in their pa he Australia all option b

es and Cox c

le and studen 80.

s formula un

nce Series, 2

Review of

estigation of ccounting Bu

lasticity of v anges. Blattb nd random. on model (19

holes were a se he too ha

holes formu undamentals

D TO EVA bolic

Black-options, tha rate, volati

5 found th d solving a

s for an opt model, the ty model. M possibly inf

ces. If they exercise pol f Cox, Ingers

aper ‘An em an stock ex

being exerc

call option va

nt distributio

nder ideal co

010, Vol. 19

f Financial St

f the Black-S usiness and F

variance berg and

970) has awarded ave been

ula under s and its

ALUATE -Scholes at paying ility and

hat The a partial tion. We

constant Multiple feasible) y are not licy, and soll, and

mpirical xcahnge’ cised on

aluation

ns as

onditions.

Issue 2,

tudies,

ASX20 this pap that the the use of the u model. Espen G Used th finance neither traders manner differen can be u model t used to Scholes saying o

Chaudh Black-S option p two GA options bearing the othe the dire

Heston for a sp returns volatilit shows t are sub volatilit

7 Espen the Blac http://ch ack-Scho 8 Heston valuatio

00 Option In per utilises q B & S mod of implied v underlying

Gaarder Hau he Black-Sc

theory and philosophy copying oth r. This stud ntial equatio used to pre to predict st check whe s – Merton d of Espen Ga

hury and J Scholes mod price is not ARCH (1,1) are an exc g on the mag er hand, det ection of the

and Nand ot asset who

of the spot ty model a that the out-bstantially lo

ty for each o

n Gaarder Ha ck-Scholes-M hineseactuary

oles-Merton_ n, SL; Heston on model, Rev

ndex. Using qualitative r del is statisti volatility an lognormal

ug & Nassi choles-Mert d practicle. T

y nor mathe her traders) dy is aime on model fo dict the sui tock option ether the me differential

aarder Haug

Jason (199 del bias wh preference ) process p ception. Th gnitude of th

ermines the e Black-Sch

di (2000)8 in ose varianc t asset. The as a continu of-sample v ower than option to fit

Haug & Nassi

Merton Option y.groupsite.c _Option_Pri n, Steven L.; view of Fina

g single-par regression a ically signif nd a jump-d distribution

m Nicholas ton Option They furthe ematics. It i and tricks d d at analyz or stock opti

tability of u prices in In ean differen equation mo g & Nassim

96) examine hen stock re neutral and arameters ( e variance he Black-Sc e so called “ holes model n their pape e follows a e single lag uous-time li valuation err the ad hoc t to the smir

im Nicholas n Pricing Fo com/uploads/f

icing_Formu Nandi, S; N ncial Studies

rameter estim and a maxim ficant at the diffusion app n, improves

s Taleb (200 Pricing Fo er narated th is a rich cra developing

zing the fe ion pricing using Black ndian marke nce between odel and ctu m Nicholas T ed the beh eturns follow d depends o (a1 ,b1). De

persistence choles mode “leverage ef

bias. er developed

GARCH(p g version of

imit. Empir rrors from th Black-Sch rk/smile in t

Taleb (2008) ormula, can b

/files/x/000/0 ula.pdf Nandi, Saikat

s, Fall2000,

mates of fa mum likelih 1% level an proach, whi

the statisti

08)7 in their ormula” em hat Option h aft with tra

under evolu easibility o

in Indian C k - Scholes et. Further t n expected ual price hav Taleb is corr avior of Eu w a GARC on the unit r

eep-out-of e parameter el bias. The r

ffect” and ca

d a closed-f , q) process f this mode rical analys he single lag holes model the implied

) in their pap be download 00e/45c/Why

(2000) A clo Vol. 13 Issue

ctors within ood approac nd it also pr ich increase cal signific

r paper “Wh mphasized o

hedging, pri aders learnin

ution pressu f Black - ontext. The – Merton d the indipend

price as co ve any signi rect. uropean op

H (1,1) pro risk premium

the-money , g = a1 + risk preferen an be impor

form option that can be el contains sis on S&P g version of l that uses volatilities

per “Why We ded from: y_We_Have_N

sed-form GA e 3

n the B & S ch. Results rovide evide es the tail pr cance of the

Why We Hav on the gap b

icing, and tr ng from tra ures, in a bo Scholes – e result of th differential e ndent t test h omputed by ificant diffe

ption price ocess. The G um (l) as we

and short m b1, has a nce parame rtant in dete

n valuation e correlated Heston's st P500 index f the GARCH

a separate .

e Have Never

_Never_Used

ARCH option

S model, indicate ence that roperties e B & S

ve Never between rading is aders (or ottom-up Merton his study equation has been Black - erence or

and the GARCH ell as the maturity material eter, l, on ermining

formula with the tochastic options H model implied

r Used

d_the_Bl

Lehar, commo volatilit Christo differ in-the-m by thes returns as cond pricing Barone-new me In an i historic prices. A outperfo

Singh, sample option Black-S price us the para the nex outperfo between as comp reduces

Rotkow

Volatili

9 Lehar,

Option p p323, 23 10 Chri skewnes 11 Baro Model w p1223-1 12 Sing

and Pra (0304-09

13

Rotko Examine

Scheicher on extension

ty option pr ffersen, Pet systematica money call p se empirical

with Invers ditional hete formula co -Adesi, Gio ethod for pr

incomplete cal and the p

An extensiv forms other

Ahmad an forecasting pricing m Scholes mod sing error m ameters of th

xt-day opti forms the oth n model and pared to Pra s price bias

wski, Aaro

ity in the B

, Alfred; Sch

pricing and r 3p,

istoffersen, P ss, Journal of one-Adesi, G with Filtered 1258,

gh, Vipul Kum ctitioner Bla 941), Aug20 owski, Aaron er, Nov/Dec2

and Schitte ns of the B ricing mode

ter; Heston ally from

prices) are l facts, the se Gaussian eroskedastic nsistent wit ovanni; Eng icing option

market fra pricing retur ve empirical competing

nd Pachori g performan model with del for prici metrics, mon

he models a ion prices. her two mod d market gre actitioner Bl

significantl

on M.(2011

Black-Schol

heicher, Mar

risk managem

Peter; Heston

f Econometri Giovanni; Eng

Historical S

mar; Ahmad

ack-Scholes M 11, Vol. 38 Is n M.(2011), E

2011, p13-19

enkopf (200 Black-Schol el.

n, Steve; Ja Black-Sch relatively h authors de innovation city and a le

th this stock

gle, Robert F ns based on amework th rn dynamics l analysis ba GARCH pr

i (2011)12 nce of clos h benchma ing S&P CN

eyness-mat analytically, . The resu dels. It is no eatly, despit lack-Schole y, in 12 out 1)13, in the

les-Merton

rtin; Schitten

ment, Journa

n, Steve; Jac

ics, Mar/Apr

gle, Robert F Simulation., R

d, Naseem; P

Model for pr ssue 2, p51-6 Estimating Stock 9, 7p,

02)9 examin les framewo

acobs, Kris holes price high compar evelop a new ns. The mod

everage effe k return dyn

F.; Mancin n GARCH m

he authors s enhancing ased on S& ricing mode The researc sed-form di ark Black-NX Nifty 50 turity wise. I

, and then us ults show ot only outp te the fact th es and Black t of 15 mon eir research

Model fou

nkopf, Christ

al of Banking

cobs, Kris. (2 r2006, Vol. 1 F.; Mancini, Review of Fin

Pachori, Push

ricing S&P C 67,

k Price Volatilit

ned the out-ork, namely

(2006)10 f

es. Out-of-red to the B

w discrete-el allows fo ect. The pap namic.

ni, Loriano.

models with allow for g the model

P 500 index els and ad ho

ch work em iscrete time -Scholes a 0 index opti In this resea sed them to that Pract performing b

hat executio k-Scholes. T eyness-matu h paper ent und that Th

tian. (2002) g & Finance,

2006), Option 31 Issue 1/2

Loriano(200 nancial Stud

hkar(2011), E CNX Nifty 50

ty in the Black-S

of-sample p y a GARCH

found that I the-money Black-Schole

time dynam or condition

per presents

(200811 the filtered his different d flexibility t x options sh

oc Black-Sc mpirically i e Heston an and its ve

ion of India arch work, t

produce rel itioner Bla but also redu on of GARC The Practitio urity groups titled Estim

he BSM mo

GARCH vs. s Mar2002, V

n valuation w , p253-284, 08), A GARC dies, May200

Empirical an index option

Scholes-Merton

performanc H and a st

Index optio put price es price. M mic model nal skewness

s an analyti

eir work an storical inno distributions to fit marke hows that thi choles mod

investigates nd Nandi G ersion Pra a, relative to the authors f liable predic ack-Scholes ducing the pr

CH is very c oner Black-s.

mating Stoc

model is a c

stochastic vo Vol. 26 Issue

with conditio

CH Option P 08, Vol. 21 Iss

nalysis of GA ns of India., D

n Model, Val

e of two tochastic

n prices es (and Motivated

of stock s as well c option

nalyzes a ovations. s of the et option

is model els. s out of GARCH

ctitioner o market first find ctions of s model

rice bias complex -Scholes

ck Price

common

olatility: 2/3,

onal

Pricing sue 3,

ARCH Decision

approac options option t

Limitat Though results assump i. ii ii iv v

Data A Data ob Black-S has bee and 30-by usin using fo Annual Annual 2010-20

ch used by made by cl time to expi

tions of Stu h study is b

for Indian ption can be

. There

i. Daily

ii. Divid

v. Vola

v. Rate

Analysis – R btained fro Scholes-Me en computed -Jun-2011. F ng ln(St/St-1 ollowing for Volatility ( dividend y 011 and con

valuation a losely held b iration, risk

udy:

ased upon t n market si regarded as e is no diffe y fluctuation dend yield i atility remain

of interest (

Real Time om F&O se

rton Model d by consid For the com 1) then daily

rmula: (σ) = Daily yield has bee

nsidering th

analysts to c businesses. -free interes

the analysis ituatio. Stu s the limitat erence betw n of option is annual div

n same for s (repo rate) d

egment of in Indian c dering the st mputation of y standard

σ *√Days i en compute he market pr

compute the This model st rate, and

s of real tim udy is base tion of study ween historic

prices betw vidend yield study period does not ch

NSE has context. For

tock prices f annual vola deviation h

in a Year ed by consid

rice of the s

e fair marke l consists of

current pric

me data and ed upon ce

y. These are cal volatility ween periods d and remai d .

ange during

been tested r the analys

movement atility first d has been con

dering the t tock on

31-et amount o f 5 fundame ce of the und

d aim to pro ertain assum e:

y and implie s have not ta in same for

g the analys

d for the f is purpose H

between th daily return

nverted in a

otal dividen -Mar-2011.

of non-trade ental parts in nderlying sto

oduce most mptions an

ed volatility aken in the

study perio

sis period.

feasibility s Historical v he dates 1-J has been co annual vola

nds paid in

ed stock ncluding ock.

feasible nd these

y. study. od.

study of volatility

Jul-2010 omputed atility by

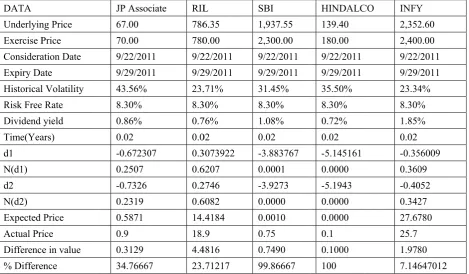

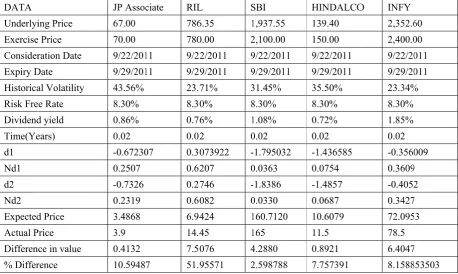

Table 1 DATA Underlyin Exercise P Considera Expiry Da Historical Risk Free Dividend Time(Yea d1 N(d1) d2 N(d2) Expected Actual Pri Difference % Differe

Source: c

Table N 7 days. which i free rate in case option p price is case of

. Difference

ng Price Price ation Date ate l Volatility

Rate yield ars)

Price ice e in value ence

computed on t

No. 1 shows Expected p is based on e of return, T

of short per price. The d absent due INFY Call

e between a JP Assoc 67.00 70.00 9/22/201 9/29/201 43.56% 8.30% 0.86% 0.02 -0.67230 0.2507 -0.7326 0.2319 0.5871 0.9 0.3129 34.76667

the basis of re

difference rice has bee

5 factor viz Time to exp riod (7 days difference is to zero valu option i.e. R

an expected ciate RIL

786 780 11 9/2 11 9/2 23. 8.3 0.7 0.0 07 0.3 0.6 0.2 0.6 14. 18. 4.4 7 23.

ealtime data ob

between an en computed

z. Spot pric piry of the op s) there is si s m,aximum ue of N(d1) Rs. 1.9780

d and actual L

6.35 0.00 22/2011 29/2011

.71% 30% 76% 02 3073922 6207 2746 6082 .4184 .9 4816

.71217

btained from N

n expected a d by using U ce of stock,

ption, Annu gnificant di m in case of H

and N(d2), (27.6780-25

price of a c SBI

1,937.55 2,300.00 9/22/2011 9/29/2011 31.45% 8.30% 1.08% 0.02 -3.883767 0.0001 -3.9273 0.0000 0.0010 0.75 0.7490 99.86667

NSE Derivati

and actual pr Using the Bl Exercise pr ual volatility ifference be Hindalco ca while the co 5.7) 7.15%

call option e HINDALC 139.40 180.00 9/22/2011 9/29/2011 35.50% 8.30% 0.72% 0.02 -5.145161 0.0000 -5.1943 0.0000 0.0000 0.1 0.1000 100

ve segment.

rice of a cal lack – Scho rice of the o y of the stoc etween expe all option pr omperative

only .

expiring in 7 CO INFY 2,352 2,400 9/22/ 9/29/ 23.34 8.30% 1.85% 0.02 -0.35 0.360 -0.40 0.342 27.67 25.7 1.97 7.146

ll option exp oles – Merto

option, Ann ck. Table sh ected and ac rice where e difference i

7 days Y

2.60 0.00 /2011 /2011 4% % %

56009 09 052

27 780

80 647012

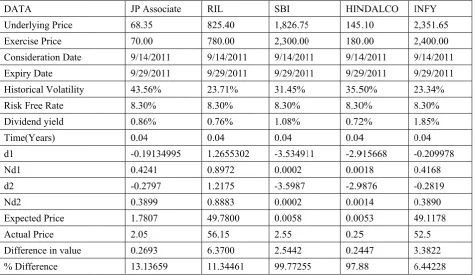

Table 2 days DATA Underlyin Exercise Consider Expiry D Historica Risk Free Dividend Time(Ye d1 Nd1 d2 Nd2 Expected Actual Pr Differenc % Differ

Source:

Table 2 of all se incresed differen highest with .24 SBI cal

2. Price diffe

ng Price Price ration Date Date

al Volatility e Rate d yield ears)

d Price rice ce in value

ence

: computed

2 indicates th elected und d because o nce between

in case of R 447 as a perc l option pri

ference betw

JP A 68.3 70.0 9/14 9/29 43.5 8.30 0.86 0.04 -0.1 0.42 -0.2 0.38 1.78 2.05 0.26 13.1

on the basis

hat increase erlaying sto f time value n expected RIL call opt

centage diff ce with 99.7

ween an exp

Associate 35 00 4/2011 9/2011 56% 0% 6% 4

9134995 241

797 899 807 5 693

3659

s of realtim

e in the time ock. Due to e of option a price and tion price w ference in In

77%.

pected and a

RIL 825.40 780.00 9/14/2011 9/29/2011 23.71% 8.30% 0.76% 0.04 1.2655302 0.8972 1.2175 0.8883 49.7800 56.15 6.3700 11.34461

me data obta

e to expiry b increase in and relative actual pric with Rs. 6.37

nfosys Call

actual price

SBI 1,826.75 2,300.00 9/14/201 9/29/201 31.45% 8.30% 1.08% 0.04 -3.53491 0.0002 -3.5987 0.0002 0.0058 2.55 2.5442 99.77255

ained from N

brings positi n time to exp

difference h ce. The diff

7 While low option is low

of a call op

HIN 5 145 0 180 11 9/14 11 9/29 35.5 8.30 0.72 0.04 11 -2.9 0.00 -2.9 0.00 0.00 0.25 0.24 5 97.8

NSE Deriva

ive impact o piry call op has been mi ference in t west in HIND

west with 6

ption expirin

NDALCO I

.10 2

.00 2

4/2011 9 9/2011 9

50% 2

0% 8

2%

4 0

915668

-018 0

9876

-014 0

053 4

5 5

447 3

88 6

ative segmen

on call optio ption price h inimized in the value h DALCO cal .44% and hi

ng in 15

INFY 2,351.65 2,400.00 9/14/2011 9/29/2011 23.34% 8.30% 1.85% 0.04 -0.209978 0.4168 -0.2819 0.3890 49.1178 52.5 3.3822 6.44228

nt.

on prices has been terms of has been

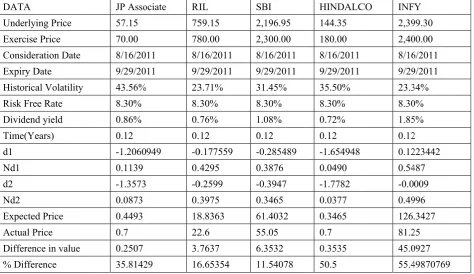

Table 3 30 days DATA Underlyin Exercise Consider Expiry D Historica Risk Free Dividend Time (Ye d1 Nd1 d2 Nd2 Expected Actual Pr Differenc % Differ

Source:

Table 4 43 days DATA Underlyin Exercise Consider Expiry D Historica Risk Free Dividend Time(Ye d1 Nd1 d2 Nd2 Expected Actual Pr Differenc % Differ

. The price s

ng Price Price ration Date Date

al Volatility e Rate d yield ears)

d Price rice ce in value

ence

: computed

4. The price s

ng Price Price ration Date Date

al Volatility e Rate d yield ears)

d Price rice ce in value

ence

difference b

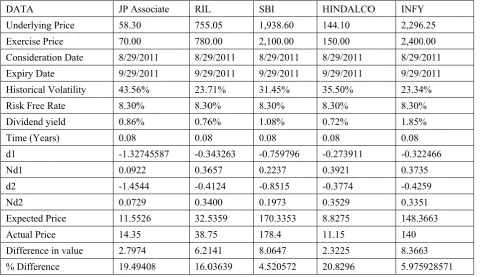

JP Asso 58.30 70.00 8/29/20 9/29/20 43.56% 8.30% 0.86% 0.08 -1.3274 0.0922 -1.4544 0.0729 0.3018 0.45 0.1482 32.9333

on the basis

difference b

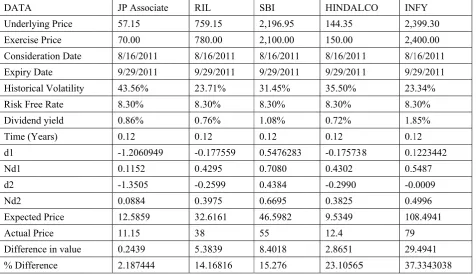

JP Asso 57.15 70.00 8/16/20 9/29/20 43.56% 8.30% 0.86% 0.12 -1.2060 0.1139 -1.3573 0.0873 0.4493 0.7 0.2507 35.8142

between an

ociate RI 75 78 11 8/ 11 9/

% 23

8. 0. 0. 45587 -0 0.

4 -0

0. 12 16 3. 33 21

s of realtim

between an

ociate RI 75 78 11 8/ 11 9/

% 23

8. 0. 0. 0949 -0 0. -0 0. 18 22 3. 29 16

expected a

IL 55.05 80.00 /29/2011 /29/2011 3.71%

30% 76% 08 0.343263

3657 0.4124

3400 2.5778 6

4222 1.38875

me data obta

expected a

IL 59.15 80.00 /16/2011 /29/2011 3.71%

30% 76% 12 0.177559

4295 0.2599

3975 8.8363 2.6

7637 6.65354

nd actual pr

SBI 1,938.60 2,300.00 8/29/2011 9/29/2011 31.45% 8.30% 1.08% 0.08 -1.752344 0.0399 -1.8440 0.0326 2.7623 6.5 3.7377 57.50308

ained from N

nd actual pr

SBI 2,196.95 2,300.00 8/16/2011 9/29/2011 31.45% 8.30% 1.08% 0.12 -0.285489 0.3876 -0.3947 0.3465 61.4032 55.05 6.3532 11.54078

rice of a cal

HINDALC 144.10 180.00 8/29/2011 9/29/2011 35.50% 8.30% 0.72% 0.08 -2.036193 0.0209 -2.1397 0.0162 0.1109 0.5 0.3891 77.82

NSE Deriva

rice of a cal

HINDALC 144.35 180.00 8/16/2011 9/29/2011 35.50% 8.30% 0.72% 0.12 -1.654948 0.0490 -1.7782 0.0377 0.3465 0.7 0.3535 50.5

ll option exp

CO INF 2,29 2,40 8/29 9/29 23.3 8.30 1.85 0.08 -0.3 0.37 -0.4 0.33 57.8 47.1 10.7 22.7

ative segmen

ll option exp

CO INF 2,39 2,40 8/16 9/29 23.3 8.30 1.85 0.12 0.12 0.54 -0.0 0.49 126. 81.2 45.0 55.4

piring in

Y 96.25 00.00 9/2011 9/2011 34% 0% 5% 8

22466 735

259 351 8701 15 7201 73616119

nt.

piring in

Y 99.30 00.00 6/2011 9/2011 34% 0% 5% 2 223442 487

009 996

Source:

Observ In the c achieve Associa differen followe expiry o Rs.0.14 option w associat Table 5 days.

DATA Underlyi Exercise Consider Expiry D Historica Risk Fre Dividend Time(Ye d1 Nd1 d2 Nd2 Expected Actual P Differenc % Differ

Source:

: computed

vations case of call ed in Hinda ates with Rs nce in price ed by JaiPra of 30 days, 482 and fol with time to tes which is . The price

ing Price Price ration Date Date

al Volatility e Rate d yield ears)

d Price Price

ce in value rence

: computed

on the basis

l option wi alco Indust s.0.3129. In e was achi akash Asso the least di lowed by H o expiry of 4 s Rs.0.2507

difference b

JP Assoc 67.00 70.00 9/22/201 9/29/201 43.56% 8.30% 0.86% 0.02 -0.67230 0.2507 -0.7326 0.2319 3.4868 3.9 0.4132 10.5948

on the basis

s of realtim

ith time to tries limited n the case of ieved in Hi ociates with

fference in Hindalco In

43 days, the and follow between an

ciate RIL 786 780 11 9/2 11 9/2 23.7 8.30 0.7 0.02 07 0.30 0.62 0.27 0.60 6.94 14.4 7.50 7 51.9

s of realtim

me data obta

expiry of 7 d which is f call option indalco Ind h Rs.0.2693

price was a ndustries lim

e least diffe wed by Hind expected an

L S

6.35 1

0.00 2

2/2011 9 9/2011 9

71% 3

0% 8

6% 1

2 0

073922

-207 0

746

-082 0

424 1

45 1

076 4

95571 2

me data obta

ained from N

7 days, the Rs.0.1000 n with time dustries lim . In the cas achieved in

mited with erence in pri dalco Industr

nd actual pri

SBI 1,937.55 2,100.00 9/22/2011 9/29/2011 31.45% 8.30% 1.08% 0.02 -1.795032 0.0363 -1.8386 0.0330 160.7120 165 4.2880 2.598788

ained from N

NSE Deriva

least diffe and follow to expiry o mited which se of call o JaiPrakash Rs.0.3891. ice was ach ries limited ice of a put o

HINDALCO 139.40 150.00 9/22/2011 9/29/2011 35.50% 8.30% 0.72% 0.02 -1.436585 0.0754 -1.4857 0.0687 10.6079 11.5 0.8921 7.757391

NSE Deriva

ative segmen

erence in pr wed by Jai of 15 days, t h is Rs.0.24 option with associates w .In the case hieved in Jai d with Rs.0.3

option expi

O INFY 2,352.6 2,400.0 9/22/20 9/29/20 23.34% 8.30% 1.85% 0.02 -0.3560 0.3609 -0.4052 0.3427 72.095 78.5 6.4047 8.1588

ative segmen nt.

rice was iPrakash the least 447 and

time to which is e of call iPrakash 3535 ring in 7

60 00 011 011 %

009 9

2 7 53

7 853503

Table 6 15 days DATA Underlying Exercise P Considerat Expiry Da Historical Risk Free Dividend y Time (Yea d1 Nd1 d2 Nd2 Expected P Actual Pric Difference % Differen

Source:

Table 7 30 days DATA Underlying Exercise P Considerat Expiry Dat Historical Risk Free R Dividend y Time (Yea d1 Nd1 d2 Nd2 Expected P Actual Pric Difference % Differen

6. The price s

g Price Price

tion Date ate

Volatility Rate yield ars)

Price ce e in value

nce

: computed

7. The price s

g Price Price

tion Date te Volatility Rate yield ars)

Price ce e in value

nce

difference b

JP Assoc 68.35 70.00 9/14/201 9/29/201 43.56% 8.30% 0.86% 0.04 -0.191349 0.4241 -0.2797 0.3899 3.2165 3.85 0.6335 16.45455

on the basis

difference b

JP Assoc 58.30 70.00 8/29/201 9/29/201 43.56% 8.30% 0.86% 0.08 -1.32745 0.0922 -1.4544 0.0729 11.5526 14.35 2.7974 19.49408

between an

iate RIL 825 780 1 9/14 1 9/29 23.7 8.30 0.76 0.04 995 1.26 0.89 1.21 0.88 1.98 9.75 7.76 5 79.6

s of realtim

between an

iate RIL 755 780 1 8/29 1 9/29 23.7 8.30 0.76 0.08 587 -0.3 0.36 -0.4 0.34 32.5 38.7 6.2 8 16.0

n expected a

L S

5.40 1

0.00 2

4/2011 9 9/2011 9

71% 3

0% 8

6% 1

4 0

655302

-972 0

175

-883 0

818 2

5 2

682 0

67385 0

me data obta

n expected a

L S

5.05 1

0.00 2

9/2011 8 9/2011 9

71% 3

0% 8

6% 1

8 0

343263

-657 0

4124

-400 0

5359 1

75 1

141 8

03639 4

and actual p

SBI 1,826.75 2,100.00 9/14/2011 9/29/2011 31.45% 8.30% 1.08% 0.04 -2.108033 0.0175 -2.1718 0.0149 267.6310 267 0.6310 0.23633

ained from N

and actual p

SBI 1,938.60 2,100.00 8/29/2011 9/29/2011 31.45% 8.30% 1.08% 0.08

0.759796 0.2237

0.8515 0.1973 170.3353 178.4 8.0647 4.520572

rice of a pu

HINDALCO 145.10 150.00 9/14/2011 9/29/2011 35.50% 8.30% 0.72% 0.04 -0.382229 0.3511 -0.4542 0.3248 6.8076 7.85 1.0424 13.27898

NSE Deriva

rice of a pu

HINDALCO 144.10 150.00 8/29/2011 9/29/2011 35.50% 8.30% 0.72% 0.08 -0.273911 0.3921 -0.3774 0.3529 8.8275 11.15 2.3225 20.8296

ut option exp

O INFY VALU 2,351 2,400 9/14/2 9/29/2 23.34 8.30% 1.85% 0.04 -0.209 0.416 -0.28 0.389 91.08 103.3 113.4

ative segmen

ut option exp

O INFY 2,296 2,400 8/29/2 9/29/2 23.34 8.30% 1.85% 0.08 -0.322 0.373 -0.425 0.335 148.3 140 8.366 5.975

piring in

Y UE

.65 0.00 2011 2011 4% % %

9978 68

19 90

26 5 4684341

nt.

piring in

Y 6.25 0.00 2011 2011 4% % %

2466 5 59

1 663

Source:

Table 8 43 days DATA Underlyin Exercise Consider Expiry D Historica Risk Free Dividend Time (Ye d1 Nd1 d2 Nd2 Expected Actual Pr Differenc % Differ

Source:

Observ In the ca in JaiPr Rs.0.89 was ach with Rs price w JaiPrak the leas followe cases Ja providin It is als and hin than the

: computed

8. The price s.

ng Price Price ration Date Date

al Volatility e Rate d yield ears)

d Price rice ce in value

ence

: computed

vations ase of put op rakash assoc 921. In the c

hieved in St s.0.6335 In was achieve kash Associa st differenc ed by Hinda

aiPrakash A ng least diff so observed ndalco Indus e historical

on the basis

difference b

JP Asso 57.15 70.00 8/16/20 9/29/20 43.56% 8.30% 0.86% 0.12 -1.2060 0.1152 -1.3505 0.0884 12.5859 11.15 0.2439 2.18744

on the basis

ption with t ciates which case of put o

ate Bank of the case of ed in Hind ates with Rs

e in price w alco Industr Associates an

fference from d that JaiPra

stries limited annual vola

s of realtim

between an

ociate R 75 78 011 8/ 011 9/

% 23

8. 0. 0. 0949 -0 0.

5 -0

0.

9 32

38 5. 44 14

s of realtim

ime to expir h is Rs.0.41 option with t f India whic

put option w alco Indust s.2.7974. In was achieve ries limited

nd Hindalco m the actual akash associ d has got a h atility of oth

me data obta

n expected a

RIL 59.15 80.00 /16/2011 /29/2011 3.71% .30% .76% .12 0.177559

.4295 0.2599

.3975 2.6161 8 .3839 4.16816

me data obta

ry of 7 days 132 and foll time to exp ch is Rs.0.63

with time to tries limite n the case of ed in JaiPra

with Rs.2.8 o Industries

l price. iates has go historical an her three com

ained from N

and actual p

SBI 2,196.95 2,100.00 8/16/2011 9/29/2011 31.45% 8.30% 1.08% 0.12 0.5476283 0.7080 0.4384 0.6695 46.5982 55 8.4018 15.276

ained from N

s, the least d lowed by Hi

iry of 15 da 310 and foll o expiry of d which is f put option akash assoc 8651. So it limited has

ot a historic nnual volati mpanies.

NSE Deriva

rice of a pu

HINDAL 144.35 150.00 8/16/201 9/29/201 35.50% 8.30% 0.72% 0.12 -0.17573 0.4302 -0.2990 0.3825 9.5349 12.4 2.8651 23.10565

NSE Deriva

ifference in indalco Indu ays, the least

lowed by Ja 30 days, the s Rs.2.3225 with time to ciates which can be seen occupied th

cal annual v ility of 35.5

ative segmen

ut option exp

LCO IN 2,3 2,4 1 8/1 1 9/2 23 8.3 1.8 0.1 8 0.1 0.5 -0. 0.4 10 79 29 5 37

ative segmen

n price was a dustries limi

t difference aiPrakash as e least diffe 5 and follo o expiry of

h is Rs.0.2 n that most he first two

volatility of % which ar

nt.

piring in

NFY 399.30 400.00 16/2011 29/2011

.34% 30% 85% 12 1223442 5487

0009 4996

8.4941

.4941 .3343038

nt.

achieved ited with e in price ssociates erence in owed by

43 days, 438 and tly in all ranks in

It can al all com prices m volatilit and actu Market State B limited Rs.24,7 It can b JaiPrak compan predicti

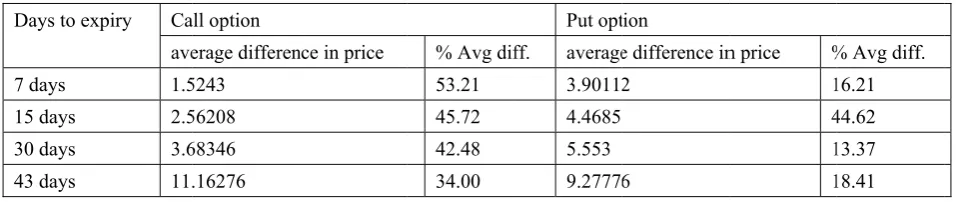

Table 9 Days to e

7 days 15 days 30 days 43 days

Observ From th values. decreas Black-S days to options average percent Black-S analysis

lso be seen mpanies in ca

mostly when ty, the Black ual value of

capitalizati Bank of Ind is Rs.2,68 725.59 crore be seen tha kash associa nies. So Bl ion for the c

9. Table sho expiry Ca ave 1.5 2.5 3.6 11.

vations he above an

In the Table sing as the Scholes-Me expiry incre

are mostly e percentag

age differen Scholes-Me

s of differen

that Infosys ase of histo n compared

k-Scholes-M f call and pu

ion of Infos dia is Rs. 1 8,533.75 cro

es and Mark at the avera ates is nea lack-Schole companies w

wing the av all option

erage differen 5243

56208 68346 .16276

nalysis it is f e 9, it can b

number of rton model eases. It can y lower than

e differenc nces compa

rton model nce in follow

s Limited w rical annual to other com Merton mod ut options o

sys Limited ,11,013.7 c ores, Marke ket capitaliz

age market arly 8.7 tim

es-Merton m with lower m

verage differ

nce in price

found that t e found that

days to ex in computa n also be fou n the avera e is not sim ared to put

for a call op wing section

which has hi l volatility a mpanies. Th del can prov of that stock

d is Rs. 1,4 crores, Mar et capitaliz zation of Jai t capitalizat mes lower

model seem market capi

rence in opt

% Avg dif 53.21 45.72 42.48 34.00

the expected t the percen xpiry increa ation of call und that the age differen milar in all option pric ption is high n makes ou

istorical vol and it has s he companie vide least di k.

46,532.7 cro rket capital zation of H iPrakash ass tion of Hin than the m ms to prov

italization.

tion prices o Put opt ff. average

3.90112 4.4685 5.553 9.2777

d values var ntage averag ses. This sh l option pric e average dif nce in rupee l four cases e. This show her than tha ur inference

atility of 23 hown the hi es which ha ifference be

ores , Mark ization of R Hindalco Ind

sociates is R ndalco Indu market capi vide least d

of five stock tion

e difference in 2

6

ry significan ge difference hows that t ces increase fference in r e prices for s as call op ws that the at of the put

more valid.

3.34% is the highest diffe ave higher h etween the e

ket capitaliz Reliance In dustries Lim Rs.15586.76 ustries Limi

italization o difference

k options

n price % 1 4 1 1

ntly from th e in prices k the accurac es as the nu rupee prices r put option

ption shows prediction t option. Re

.

e least of erence in historical expected

zation of ndustries mited is 6 crores. ited and of other in price

% Avg diff. 16.21 44.62 13.37 18.41

he actual keeps on y of the umber of s for call ns, while

Regress Model 1

a Predic

Mod 1

a Predic b Depen

Model

1

a Depen

Model 1

a Predic

Model 1

a Predic b Depen

sion Analys R .9

ctors: (Cons

del Regressi Residua Total

ctors: (Cons ndent Varia

(Constant) Days

ndent Varia

(i

R .939(a)

ctors: (Cons

Regression Residual Total

ctors: (Cons ndent Varia

sis: Regress

R R

905(a) .8

stant), Days

Sum Squa ion 47.0 al 10.3 57.4

stant), Days able: ECPRI

Unstanda

B -1.151 .248

able: ECPRI

ii) Regressi

R Square .881

stant), Days

Sum of 15.455 2.079 17.534

stant), Days able: EPPRI

ion Value o Square A

19 .

s

ANO

m of ares df 059 1 393 2 452 3

s

ICEDIF

Coeffic

ardized Coeffi

Std. Err 2.263 .082

ICEDIF

on Value o

Adjusted R .822

s

ANO

Squares d

2 3

s

ICEDIF

of Differenc Adjusted R Sq

729

OVA(b)

Mean 47.05 5.196

cients(a)

ficients S C

ror B

.

of Differenc

Square

OVA(b)

df 1 2 3

ce in Call Op quare St

2.

n Square F

9 9.

6

Standardized Coefficients

Beta

905

ce in Put O

Std. Error of 1.01955

Mean Squa 15.455 1.039

ption prices td. Error of the

27955

Si 056 .0

t

B -.508 3.009

ption price

f the Estimate

are F 14.8

s

e Estimate

ig. 095(a)

Sig.

Std. Err .662 .095

es:

e

Si 868 .0

ror

Model

1

a Depen

Mod 1

a Predic

Model 1

a Predic Regress depende indepen expiry. option p model. differen Similar Square to expir to expir Greek u B-S-M says tha increase So far a freedom call opt the case

(Constant) Days

ndent Varia

Model Sum

del R .973(a)

ctors: (Cons

Model Sum

R .323(a)

ctors: (Cons sion analysi

ent variable ndent variab

On the basi prices have Here R valu nce that say

relationship value .881 w ry. Based on ry is more st under the B model, thou at it is not e in time to anova is con m of denom

tion price an es.

Unstandar

B 2.428 .142

able: EPPRI

mmary: Re

R Squa .946

stant), Days

mmary: Re

R Squa .104

stant), Days is is a metho e, in this s ble while ca is of outcom e positive re

ue is .905 a ys that if tim

p has been o which indic n the regress

trong than t B-S-M mode

ugh when it necessary t expiry will ncern the tab minator for 5

nd 14.868 fo

C

rdized Coeffic

Std. Error 1.012 .037

ICEDIF

gression Va

are

s

egression V

are Adjus -.344

s

od to deal w study days all and put o

me of regres elationship

nd R Squar me to expir observed in cate close re sion value w the call opti el. Our stud

comes to pe that always

increase pu ble value fo 5 % level of for put optio

oefficients(

cients Sta Co

Bet

.93

alue of % D

Adjusted R .920

Value of %

sted R Square 4

with the relat to expiry option prices

ssion analys as it has b re .819 in ca ry decreases case of put elation ship we can say t on price. Th dy based on

ercentage d s reduction ut option pric

or 1 degree f significanc on price, the

(a)

andardized efficients

ta

9

Difference

Square

Difference

e Std.

16.7

tionship betw i.e. 7, 15, s are depend sis we can s been one of ase of Europ s call prem

option beha between the that put opti

his relations n regression difference in in time wil ce as the Ad of freedom ce is 18.5 a erefore null

t

B 2.399 3.856

in Call Op

Std. Erro 2.25733

in Put Opt

Error of the E 76026

ween indep 30 and 43 dent over th say that tim f the basic p

pean Call O ium decrea aviour with e put option ion price rel ship is also n analysis pr n the put opt

ll reduce pu djusted R Sq for numera and compute hypothesis

Sig.

Std. .139 .061

ption prices

or of the Estim

tion prices:

Estimate

pendent vari are consid he change in me to expiry

principle of Option price ases and vic h R value .93 n premium a lationship w explain by t rove the va tion prices a ut option p quare value ator and 2 d ed value is is accepted

Error 9 1

:

mate

:

able and dered as n time to

and call f B-S-M average ce versa. 39 and R and days with time theta (θ) alidity of analaysis rice and is -.344. degree of

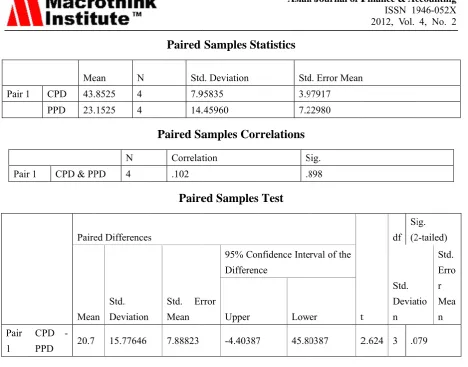

Pair 1

Pair 1

Pair 1

C PP

CPD: C PPD: Pu Table v indicate accepte Hypoth H1: The Model Accept H2: Th actual o corelati H3: Bla option p

Recom

Me CPD 43. PPD 23.

CPD & PP

Paire

Mean CPD -

PD 20.7

Call price Av ut price Av value at 5% es that B-S-ed.

hesis can be ere is no sig by taking h ed.

ere is no im options pric ion between ack Schole M

price. Accep

mendation Traders nee price of put compared t

ean N 8525 4 1525 4

N PD 4

ed Differences

n Std. Deviation

15.77646

verage % D erage % Di % significanc

-M model is

concluded gnificant dif historical vo

mpact of len ce. Rejecte n time to exp

Merton mod pted

ns for the A ed to be cau t option as t to call optio

Paired

Std 7.9 14.

Paired Sa

Correlat .102

Paire

s

Std. Er Mean

7.88823

Difference w fference wi ce level for s identical f

in the follow fference bet

olatrility an

ngth of tim d/ Not Acc piry and pri del gives id

Application utious while

the averge v on.

Samples S

d. Deviation 95835

.45960

amples Cor

tion

ed Samples

rror

95% Co Differen

Upper

-4.4038

with Actual P ith Actual P r 3DF is 3.1

for both cal

wing manne tween the ex nd actual pr

me to expiry cepted bec ice.

dentical resu

of Model: e using Blac

variation in

tatistics

Std 3.9 7.2

rrelations

S .8

s Test

onfidence Inte nce

Low

7 45.80

Price Price

182 while c ll and put op

er:

xpected opti rice determ

y on the diff ause for bo

ult for both

k-Schole-M the prices a

d. Error Mean 97917 22980

Sig. 898

t rval of the

er

0387 2

computed t ption pricin

ions price c ined by ma

fference betw oth call and

call option

Merton mode are higher in n

t

df Si (2

Std. Deviat n

2.624 3 .0

value is 2. ng hencefor

computed by arket forces

tween expec d put there

price as we

el for predic n case of pu

ig. 2-tailed)

tio Std. Erro r Mea n

079

624 that rth H3 is

y B-S-M s. Result

cted and is stong

ell as put

Conclu On the b prices o stock o results volatilit increase Black-S options From th options Black-S model w is driven investor Indian s

Refern Black, efficien Black, F

politica

Blattber as sta http://dx Burasch markets Chen, R Empiric http://dx Copelan New Yo

Traders sho nearer as th in number o are less wil actual value Traders sho seem to pro

usion basis of the of stock opti options. The of Black-S ty and the m es as the n Scholes-Me

.

he research trading Scholes-Me would lead t

n by large n rs. Therefor stock option

ces

F., & Scho ncy. Journal

F., & Schol

al economy,

rg, R. C., & atistical m

x.doi.org/10 hi, A., & Ja s. Review of

R., & Palm cal Eviden

x.doi.org/10 nd, T., Wes ork: Pearson

ould avoid u he relative /

of days to e ll lead to hig

es of call an ould use Bla ovide better

real time da ions have be e difference choles-Mer market capit number of rton model

h it is found in NSE I rton model the possibil number of m

re there is n n products.

oles, M. (1

l of finance,

les, M. (197

81(4),

637-& Gonedes, models for

0.1086/2956 ackwerth, J.

f financial s

mon, O. (20 nce. Review

0.1007/s111 ston, J., & S

n Addison W

using Black percentage expiry. Usin gh percentag nd put optio ack-Scholes

results.

ata collected een compute e between t rton model alization of days to ex

provides b

d that the fe India mark seems to va lity of price macro econo need to brin

1972). The

, 27(3), 399

73). The pr -659. http:// J. (1974). A

stock p 634 . (2001). Th

studies, 14(2

005). A No

w of Quan

156-005-633 Shastri, K. (2

Wesley.

k-Scholes-M difference ng Black-Sc age differenc ons

s-Merton mo

d from the d ed and com the expecte have certai f the stock. I xpiry decrea

better result

feasibility o ket is ver ary highly fr differencia omic factors ng more ref

valuation 9-417. http:/

ricing of op /dx.doi.org/ A comparis prices. Jou

he price of 2), 495-527 on-Paramet

ntitative Fi

33-2 2005). Fina

Merton mode in prices inc holes-Merto ce in prices

odel when d

derivative se mpared with t ed and actu

in relations It is also fou ases and it ts for call o

of Black-Sch ry low. A rom the actu ation in Indi

s as well as form in this

of option //dx.doi.org/ ptions and c /10.1086/26 son of the s

urnal of

a smile: He . http://dx.d tric Options

nance and

ancial theory

el when day creases high on model w between th

days to expir

egment of N the actual ca al values w hip with th und that the also has b options whe

holes-Merto As the pri

ual values. A an derivativ the emotion model to m

contracts in /10.2307/29 corporate lia 60062

table and st

business,

edging and doi.org/10.1 s Pricing M

d Accountin

ry and corpo

ys to expiry hly with the when days to

he expected

ry are more

NSE, the call all and put p were found he historica

difference i been observ en compare

on model f ices predic At present u ve market as ns of the tra make it feas

n a test of 978484 abilities. Jo

tudent distr

47(2), 2

spanning in 1093/rfs/14. Model: The

ng, 24(1),1

orate policy

are e decrese

o expiry and

e, as they

l and put prices of and the l annual in prices ved that

d to put

for stock cted by

sing this s market ders and sible for

f market

urnal of

ributions 244-280.

n option 2.495 eory and

115-134.

Das, S.

Journal

http://dx Draper, Duffie, jump-di http://dx Dumas, tests. Jo

Finnerty

of finan

Galai, D

of busin

Geske, 63-81. h Geske, and “B http://dx Hull, J.

Journal

Johnson

financia

Macbet option http://dx MacBet valuatio http://dx Naik, V with http://dx Peiro, A

econom

www.ns

R., & Sund

l of

x.doi.org/10 , N., & Smit D., Pan, J., iffusions. x.doi.org/10 , B., Flemin

ournal of fin

y, J. E. (197

nce and qua

D. (1977). T

ness, 50(2),

R. (1979). http://dx.do R., R, Roll. Biases” in t x.doi.org/10

, & White,

l of finance

n, H., & Sh

al and quan

th, J. D., & pricing x.doi.org/10 th, J. D., &

on m

x.doi.org/10 V., & Lee M

discontinu x.doi.org/10 A. (1994). T

mics, 4(6), 43

seindia.com

daram, R. K

financial

0.2307/2676 th, H. (1981 , & Singleto

0.1111/1468 ng, J., and

nance, 53(6

78). The Ch

antitative an

Tests of mar 167-197. h The valuati oi.org/10.10

., & Shastri the Black-S 0.1111/j.154 A. (1987).

42(2), 281–

hanno, D. (1

ntitative ana

Merville, L g mode 0.1111/j.154 &Merville, models.

0.1111/j.154 M. (1990). G uous retu

0.1093/rfs/3 The distribu 31-439. http m

K. (1999). O

and

6279 1). Applied R

on, K. J. (20

Econome

8-0262.001 Whaley, R ), 2059-210 hicago Boar

nalysis, 13(1

rket efficien ttp://dx.doi. ion of comp 16/0304-40 , K. (1984). Scholes mo 40-6261.19

The Pricin –300. http:// 987). Optio

alysis, 22(2)

L. J. (1979).

el. Jour

40-6261.19 L. J. (1980

Journal

40-6261.19 General equ urn. Revi

3.4.493 ution of sto

p://dx.doi.or

Of Smiles an

quantitati

Regression

000). Trans

trica,

64 R. E. (1998

06. http://dx rd Options 1), 29-38. ncy of the C

.org/10.108 pound optio 05X(79)900

. Over-the-c odel: A no 83.tb02295 ng of Optio /dx.doi.org/ on pricing w ), 143-151.

An empiric

rnal of

79.tb00063 0). Tests of

of

80.tb02157 uilibrium: P

iew of

ck returns: rg/10.1080/

nd Smirks:

ive ana

Analysis (2

sform analy

68

). Implied x.doi.org/10 Exchange a

Chicago Boa 86/295929

ons. Journa

22-9 counter opti ote. Journa

5.x ns on Asse /10.1111/j.1 when the va http://dx.do cal examina

f financ

.x f the Black

finance

7.x Pricing of o

financial

Internation /758518675

A Term Str

alysis, 3

2nd edn). Ne sis and asse

8(6),

volatility fu .1111/0022 and market

ard Options

al of financi

ion market d

l of financ

ts with Stoc 1540-6261.1 ariance is ch oi.org/10.23

ation of the

ce, 34(5

-Scholes an

e, 35(

ptions on th

studies,

nal evidence 5

ructure Pers

34(2), 2

New York: W et pricing fo 134

functions: em 2-1082.0008

efficiency.

Exchange.

ial econom

dividend pr

ce, 38, 127

chastic Vol 1987.tb0256 hanging. Jo

07/2330709 Black-Scho 5), 117

nd Cox cal

(2), 2

he market p

, 3, 4

e. Applied f

spective. 211-239.

Wiley. or affine 43-1376.

mpirical 83

Journal

Journal

ics 7(1),

rotection 71-1277.

latilities. 68.x

ournal of

9 oles Call 73-1186.

ll option 285-301.

portfolio 493-521.