Kennesaw State University

DigitalCommons@Kennesaw State University

Faculty Publications2018

Interpersonal Affect, Accountability and

Experience in Auditor Fraud Risk Judgments and

the Processing of Fraud Cues

Jennifer Schafer

Kennesaw State University, [email protected]

Brad Schafer

Kennesaw State University, [email protected]

Follow this and additional works at:https://digitalcommons.kennesaw.edu/facpubs Part of theAccounting Commons

This Article is brought to you for free and open access by DigitalCommons@Kennesaw State University. It has been accepted for inclusion in Faculty Publications by an authorized administrator of DigitalCommons@Kennesaw State University. For more information, please contact

Recommended Citation

Schafer, Jennifer and Schafer, Brad, "Interpersonal Affect, Accountability and Experience in Auditor Fraud Risk Judgments and the Processing of Fraud Cues" (2018).Faculty Publications. 4231.

Interpersonal Affect, Accountability and Experience in Auditor Fraud Risk Judgments and the Processing of Fraud Cues

ABSTRACT

This paper examines whether auditors’ affect toward client management influences fraud likelihood judgments and whether accountability and experience with fraud risk judgments moderate this effect. This research also explores the process by which affect influences fraud judgments by examining affect’s influence on the evaluation of fraud evidence cues. Results indicate that more positive affect toward the client results in lower fraud likelihood judgments. Accountability is found to moderate this effect, but only for experienced auditors. These findings have implications for fraud brainstorming sessions where all staff levels provide input into fraud risk assessments and because client characteristics are especially salient during these

assessments. Importantly, results also support the proposition that affect impacts inexperienced auditors’ fraud assessments through errant attribution of client likeability to evidence cues that refer to management, rather than biasing all client-related evaluations. Together, these findings suggest that education and training can be improved to better differentiate relevant and irrelevant cues in fraud judgment.

INTRODUCTION

“One cannot be introduced to a person without experiencing some immediate feeling of attraction or repulsion and without gauging such feelings on the part of the other. We evaluate each other constantly, we evaluate each others’ behavior, and we evaluate the motives and the consequences of their behavior” Zajonc (1980, p. 153).

One of the cornerstones of the audit profession is the objective evaluation of evidence (Kinney 1999). A critical source of audit evidence comes from the interactions between auditors and their clients (Public Company Accounting Oversight Board [PCAOB] 2004). As discussed by Bennett and Hatfield (2013), characteristics of the audit work environment, including client management, have the potential to affect auditor behavior. Individuals have an automatic, emotional evaluation of others, which has been shown to influence one’s interpretation of subsequent facts and impressions (Regan et al. 1974, Fiske and Taylor 1991). Research has shown that interpersonal affect influences financial decisions (Kida, Moreno, and Smith 2001, Moreno, Kida and Smith 2002), juror judgments (Kadous 2001), and auditor judgments

(Bhattacharjee and Moreno 2002, Bhattacharjee et al. 2012). Reviews of the auditing literature note the dearth of research on how interpersonal relationships influence audit judgments (Nelson and Tan 2005) and call for research examining the effect of task experience and/or other

interventions that may serve to minimize the effects of affect on auditor judgments

(Bhattacharjee and Moreno 2013). Further, there is little research on how affect may affect fraud judgments even though client characteristics may be more salient in a fraud setting.

The purpose of this paper is to examine whether interpersonal affect (client likeability) impacts auditors’ assessments of fraud risk. Further, this study extends prior research by examining two potential moderating factors, accountability and experience, which have been shown to eliminate certain judgment biases (Kennedy 1993, Bhattacharjee and Moreno 2002).

Importantly, the professional standards require inclusion of inexperienced auditors in fraud brainstorming discussions (AICPA 2002b). These professionals may be the most susceptible to client affect (Bhattacharjee and Moreno 2002), and they tend to have significant interactions with clients (Bennett and Hatfield 2013). However, even those with general audit experience may not have experience in assessing fraud risk. As discussed by Hammersley (2011), task experience may be more useful than general audit experience in explaining effectiveness on fraud tasks. Therefore, this study specifically examines the moderating influence of task experience

(experience with fraud risk assessments) on fraud risk judgments. Further, within the fraud risk setting, interpersonal affect may be more salient since client factors (i.e. attitudes, honesty, competence) need to be attended to in assessing management characteristics. Accountability is particularly important in this case as it enables auditors to evaluate information more

systematically to distinguish between relevant and irrelevant information. Finally, this study explores the process by which interpersonal affect impacts fraud judgments by examining how client likeability influences the assessment of specific fraud evidence cues.

An experiment in which client likeability and accountability were manipulated was conducted with professional auditors as participants. A self-report measure of direct fraud risk experience was also collected. Auditors judged the likelihood of fraud for a company and then assessed the extent to which ten evidence statements were indicative of fraud. Results indicate that client likeability impacts overall fraud likelihood judgments with auditors assessing a higher (lower) likelihood of fraud for dislikeable (likeable) clients. A three-way interaction indicates that accountability mitigates this effect for the auditors who have relevant task experience. Further, the paper finds differences in the manner in which experienced versus inexperienced auditors assess independent fraud cue statements. Inexperienced auditors make errant attributions

of likeability to the fraud cue statements that reflect management characteristics and attitudes, while experienced auditors exhibit no affect bias in their assessments of the fraud cue statements.

This paper contributes to both practice and academia by providing a first step to

identifying the boundary conditions of the combination of experience and accountability on fraud judgments. These findings provide support for the profession’s use of accountability tools

(requiring documentation/justification) to encourage effortful thought, but highlight the need for task-specific knowledge in fraud judgments. Brainstorming and group discussions of fraud can provide a venue for experiential training for inexperienced auditors to learn to distinguish relevant from irrelevant information in their judgment process.

The remainder of the paper is organized as follows. The next section of the paper presents the theory and hypotheses. The third section describes the experimental design. Finally, the last two sections present the results and conclusions, and offer some directions for future research.

THEORY AND HYPOTHESES

Evidence received from the client may be one of the most pervasive (Koonce 1992) and cost-effective types of audit evidence (Wright and Mock (1985)). While evidence collected from independent sources is considered more reliable, personnel within the client organization possess valuable knowledge (Haynes 1999). In some instances, such as assessing client integrity and competence, management may be the only practical source of evidence (Anderson and Marchant 1989; Anderson, Koonce and Marchant 1994). The auditing standards require auditors to conduct interviews with client personnel pertaining to potential fraudulent activity, but they also require the auditor to maintain professional skepticism “regardless of any past experience with the entity and regardless of the auditor’s belief about management’s honesty and integrity” (AICPA

the auditor-client relationship and its influence on evidence evaluation, evidence reliability, and professional skepticism.

Auditing research has investigated several characteristics of client personnel that are relevant to auditing judgments, including competence (Hirst 1994; Bhattacharjee et al. 2012), source reliability (Anderson et al. 1994), and “tone at the top” (Marden, Holstrom, and Schneider 1997). In the discussion of their results, Anderson et al. (1994) suggest that the social context of the audit environment may contain some dimensions not captured in their experiment. The auditor-client social context is an important aspect that has been largely neglected by research (Waller 1989). Hoffman and Patton (1997) suggest the social interaction is immediate as auditors begin forming impressions of the client during initial meetings. The auditors surveyed by

Gibbins and Wolf (1982) consistently rated client service matters and people involved in the audit as important environmental factors for the auditor to consider. In fact, of the thirteen most important factors identified, five were directly related to the social environment of the audit, including references to personnel (client and auditor), client service, and client wishes. The professional standards implicitly acknowledge this social context by cautioning the auditor to maintain professional skepticism in client interactions despite any previous experience with the client (AICPA 2002b). While some client characteristics (integrity, trust, competence) are relevant to auditing judgments, client likeability (disposition) is an irrelevant factor for fraud judgment.

Research finds that auditors do include some evidence that is not relevant in their judgments, and that experience may moderate this effect. Hackenbrack (1992) provided auditor participants with both evidence relevant to the experimental judgment and evidence relevant to other aspects of the audit but not the judgment task. Hackenbrack suggests that auditors may

include irrelevant information in judgments due to “similarity based inference processing.” Similarity based inferences are based on evidence that is similar but not a substitute for relevant evidence in a judgment.1. Hoffman and Patton (1997) argue that the professional guidance omits the important hazard of auditors attending to irrelevant evidence in fraud judgments. The

discussion of professional skepticism in the standards suggests that client likeability (disposition) should not be mistaken as a relevant cue, such as client integrity, in a fraud judgment. While a few accounting studies have examined the impact of face-to-face human (affective) interaction in audit judgments (i.e. Bhattacharjee and Moreno 2002; Bhattacharjee et al. 2012), researchers note the importance of, and need for, future research in this area (i.e. Nelson and Tan 2005; Bhattacharjee and Moreno 2013). Further, fraud provides an important setting for the examination of the influence of affect. Interpersonal affect cues may be more salient in this environment as auditors assess management characteristics and attitudes in order to detect fraud red flags.

Affect

The affective evaluation of others is automatic and immediate (Zajonc 1980). That is, people immediately feel attraction or avoidance toward others. One way this affective evaluation can impact future judgments is through errant attribution (e.g., Regan, Straus and Fazio 1974). Attribution relates to the mental processes employed in a particular judgment used to draw causal inferences (Fiske and Taylor 1991). For example, Regan et al. (1974) demonstrate that a simple manipulation of likeability toward a target person in the introduction of a videotaped skill-test impacts the overall skill rating of the target person. That is, a likeable (dislikeable) person will receive higher (lower) skill rating despite demonstrating equivalent skill on a task. Specifically,

1 The term “similarity based inference” is consistent with judgment errors described as errant attribution. While

attribution is looking for a cause on an event (Hastie 1984), errant attribution is errantly attributing someone’s behavior to disposition qualities rather than the appropriate factor (Fiske and Taylor 1991).

the performance of a liked (disliked) target was attributed to the target’s ability when the

performance was good (bad), but attributed to external situational factors when the performance was bad (good)2. Thus, auditors should be aware that client likeability established in an initial client meeting may impact future judgments related to the client attributes, such as competence and integrity, causing suboptimal fraud judgments.

Affect in Accounting

While accounting research finds that auditors develop an attitude toward evidence, which may include an affective component (e.g., Bamber, Ramsay and Tubbs 1997), relatively little research has specifically investigated affect in the judgments of accountants. Kida and Smith (1995), Kida, Moreno, and Smith (2001), Bhattacharjee and Moreno (2002), and Bhattacharjee et al. (2012) are some notable exceptions.

Kida and Smith (1995) provide a theoretical model of cognitive processing that includes affect, which was supported empirically in a study by Kida, Smith and Maletta (1998). Kida, Moreno, and Smith (2001) examine the systematic impact of affect on accountants’ capital budgeting decisions. Business managers reject capital budgeting projects that elicit negative affect even though they have higher expected returns. This demonstrates that business managers do not make judgments in a strictly rational economic manner. Instead, they include in their judgment a cost or avoidance utility function associated with the negative affect of persons related to the judgment.

Bhattacharjee and Moreno (2002) find that staff and seniors rate inventory obsolescence risk assessments higher when they have negative affect toward the client than when no affective

2 The experimental task was to assess the skill of a student performing a skill test. Participants viewed a two-part

videotape including an introduction (likeability manipulation) and the target student performing the test. The current research follows the Regan et al. (1974) protocol and is discussed further in the method section below.

information is provided. Conversely, affect does not influence the judgments of managers and partners. Their findings support the hypothesis that general audit experience may limit the impact of negative affect toward a client during an audit judgment task. Bhattacharjee, Moreno and Riley (2012) extend this research by examining whether affect influences auditors’ sensitivity to client competence. They find that when client competence is low, auditors rate the risk of

obsolescence higher for dislikeable clients than likeable clients. However, the effect is eliminated for high competence clients.

The current study extends the literature on affect toward the client to a fraud judgment task. Fraud provides an important and distinct setting for the examination of the influence of affect. Fraud continues to be a concern to the auditing profession with large resources being devoted to litigation (See Hammersley 2011). Auditors must attend to specific client

characteristics as they assess fraud risk in their communications with management in order to evaluate the client’s attitudes and assess whether the client may be concealing information. These interpersonal interactions are potentially more susceptible to the influence of affect than other general audit tasks. Auditing standards note the importance of fraud judgments and specify that fraud discussions should continue throughout the audit (AICPA 2002, SAS 99). Although client likeability should not be considered relevant evidence in fraud judgments, we expect that since prior research has shown that affect toward the client has erroneously been included in other accounting judgments, it will also be included in fraud judgments. On the other hand, since fraud has serious implications for an audit client, it is possible that auditors use more systematic (versus heuristic) thinking and are thus better able to exclude irrelevant information. Stated as a testable hypothesis:

H1: Positive (negative) affect toward a client will result in a lower (higher) overall likelihood judgment of fraud.

Accountability and Experience as Moderators

Bhattacharjee and Moreno (2013) call for the examination of factors that may moderate the impact of client likeability. This study examines accountability and fraud risk assessment experience as potential moderating factors. Accountability has been shown to influence what evidence the judge attends to and how that evidence is weighted (Tetlock 1992; Hirst 1992; Messier and Quilliam 1992; Peecher 1996; Hoffman and Patton 1997). In practice, auditors are held accountable to superiors, and are generally required to explain their judgments through workpaper documentation.

The framework for accountability’s debiasing effect is that judges have available two mental processes: heuristic/low effort (system 1 thinking) and systematic/high effort (system 2 thinking) to evaluate judgment criteria. High effort judges pay closer attention to the message cues rather than environmental cues such as the person sending the message (Chaiken 1980). The high accountable judge is motivated to balance efficient and effective processing based on the audience preferences and demands (Fiske and Taylor 1991; Tetlock 1992). In this study we posit that greater accountability will cause more effortful thinking, which will enable individuals to exclude the irrelevant environmental cues (client affect) from their decision. An explicit justification requirement is a common and salient accountability manipulation (e.g. DeZoort, Harrison, and Taylor 2006; Agoglia, Kida, & Hanno, 2003) that has been shown to lead to more complex and careful analysis of information. To vary accountability, participants in the high (low) accountability condition will be informed of an explanation requirement for their judgment before viewing the case materials (at the time of recording their judgment). Pre-knowledge of the explanation requirement should lead to more effortful analysis of information (process

accountability), whereas asking for an explanation at the time of the judgment should result in lower accountability (outcome accountability). Formally stated:

H2: As accountability increases, the impact of affect toward the client on the overall likelihood of fraud judgment will be reduced.

Accountability has been shown to reduce effort-related biases such as primacy (Tetlock 1983) and recency (Kennedy 1993) for individuals with relevant experience. Conversely for those with less experience, accountability has been shown to exacerbate certain judgment biases or result in less extreme judgments when the judgment environment includes irrelevant evidence (Nisbett, Zukier and Lemley 1981; Tetlock and Boettger 1989; Hackenbrack 1992; Kennedy 1995; Shelton 1999). Because accountability may induce effort-based thinking where knowledge and experience are essential, this study also considers the auditor’s task experience. Knowledge gained from experience can create knowledge structures that differentiate experienced auditors from novices (Frederick 1991). Prior accounting research has considered differences in novices and experienced professionals in making audit judgments (Bonner and Lewis 1990; Libby and Frederick 1990; Bonner and Pennington 1991; Libby and Tan 1994; Bonner 1990; Shelton 1999; Bhattacharjee and Moreno 2002). Shelton (1999) finds that auditors with less experience include irrelevant evidence in a going concern judgment, but experienced audit partners do not use irrelevant audit evidence in the going concern judgment. Similarly, Davis (1996) finds that more experienced audit seniors attend to more relevant information than inexperienced audit seniors in a control risk assessment task. In addition, he reports that the experiential knowledge of audit seniors leads them to view fewer pieces of evidence, and make judgments in less time.

Specifically related to affect, Bhattacharjee and Moreno (2002) find that general audit experience moderates the influence of affect on auditors’ risk assessments of inventory obsolescence.

Auditor experience can be general or task-specific. While general audit experience is relevant in many audit judgments, Hammersley (2011) points out that it is a noisy proxy for fraud experience given the high variance of field experience with actual fraud among auditors. That is, general audit experience does not ensure that an auditor has gained experiential fraud knowledge. Thus, she suggests that fraud experience is a more useful measure for explaining performance on fraud tasks. Hammersley further discusses the importance of measuring

experience with financial reporting fraud specifically. However, she notes two studies that find the typical auditor has less than one encounter with financial reporting fraud. Since the setting in the current study is a fraud risk assessment in the client acceptance/planning stage, the

experience measure chosen is a self report of whether the auditor has been “directly involved in judging the likelihood that a firm may have material fraudulent financial reporting”.3 Although lower ranking audit staff may have little experience in directly assessing fraud risk, they are an important part of the fraud risk assessment process. SAS 99 requires audit teams to conduct brainstorming sessions during the audit planning stage related to fraud, and all levels of

experience (rank and task experience) are expected to provide input. Thus in a fraud risk task, it is important and relevant to determine whether experience has an effect on whether auditors are susceptible to affect biases.

This research specifically examines the influence of task-specific-knowledge gained through experience (Bonner 1990). Because auditors that have experience in direct assessment of fraud risk have developed stronger knowledge structures of the fraud risk they are more apt to select authoritative cues and objectively weight cues leading to a reduced impact of affect.

3 Participants were asked a debriefing question of “What proportion of these firms did have a material irregularity

(fraud in their financial statements)?” Consistent with other studies, partners with over 20 years of experience reported encountering 0-2 actual material fraudulent misstatements.

Therefore, it is expected that auditors who have fraud risk assessment experience will be less likely to include client likeability in a fraud judgment. Formally stated:

H3: Fraud risk assessment experience will mitigate the impact of client affect on the overall likelihood of fraud judgment.

Affect and Evidence Evaluation

A second focus of this paper is to explore the process by which affect toward the client impacts fraud likelihood judgments. Client likeability could impact the overall judgment directly, or it may impact fraud judgments indirectly through the auditor’s processing of the fraud

evidence cues that are more susceptible to attribution error.

Psychology research suggests that placing a stereotype or label on a person, such as socioeconomic background, can impact all future judgments related to that person (e.g., Darley and Gross 1983). Darley and Gross (1983) provide that individuals could maintain a predisposed position when receiving future information by discounting inconsistent future information or reinterpreting the valence of new information to maintain the predisposed position. Thus, the predisposed like or dislike position leads to a global bias in the fraud judgment.

Conversely, affect can impact assessments of individual fraud statements through attribution or errant attribution. That is, affect can influence certain types of related, but not relevant, evidence in future evaluations (Regan et al. 1974). As Hackenbrack (1992) proposes, individuals may use “similarity based inference” to link an irrelevant fact to an evaluation. Regan et al. (1974) find that likeability of a target impacts the future skill rating of the target person. Similarly, this research posits the auditors will link client likeability to the specific evidence being interpreted. That is, a personal characteristic of client likeability may be erroneously attributed to other characteristics or attitudes of the client, but it is less likely that errant attribution will occur to non-personal evidence, such as industry competitiveness.

Auditors who are experienced with fraud presumably possess the task-specific knowledge to exclude client likeability in evidence assessments. Conversely, auditors who are not

experienced with fraud may be more susceptible to making errant attributions. Thus, we posit that client likeability will be more likely to impact inexperienced auditors’ assessments of evidence cues through the errant attribution of client likeability. We also expect this errant attribution to be more prevalent in the evaluation of evidence cues that are related to the characteristics or attitudes of the client (management characteristics) than for other types of evidence cues. Formally stated:

H4: Errant attributions of client likeability are more likely to occur for evidence cues concerning management characteristics than for evidence unrelated to management characteristics, and this effect will be mitigated for auditors with fraud risk

assessment experience.

METHOD Participants

The participants in this study included 140 audit professionals from staff to partner from all of the Big 4 firms, another large international firm, and several regional firms located in two cities representing the mountain west and southeast geographic areas of the United States. The auditors were asked to voluntarily commit 30 minutes to complete a fraud likelihood judgment task in mini-case format.

Procedure

The quasi-experiment was a 2x2x2 between-subjects design with two levels of affect toward the client (like/dislike), two levels of accountability (low /high), and one measured variable, experience assessing financial reporting fraud risk (no experience/experience). The participants were asked to judge the likelihood of fraud for the company based on the

Partners of the contacted offices sent an email to audit professionals in their respective office containing a request to participate in the study. The email included the purpose of the study, the steps necessary to complete the study, the time commitment, and the voluntary nature of participation. The email also contained a link to the research website. In addition, each

participant received a CD that contained the video portion of the study, which manipulated client likeability. Participants were randomly assigned to one of the experimental treatments of

accountability as they entered the case materials on the website. After reviewing the case, the participants made an overall fraud judgment, completed their explanation requirement, performed a distracter task, and completed an assessment of ten potential red flag cues. An overview of the steps in the experiment is presented in Figure 1.

<Insert Figure 1 here>

Independent variables

Participants first viewed the video of a hypothetical client, who participants were told had agreed to be taped for firm training purposes during the client acceptance interview. The client acceptance setting was chosen to minimize the potential for participants to consider prior year judgments made by firm colleagues. The client in both conditions expressed a desire to get the audit change completed. The company background, such as industry classification, was omitted to avoid a potential alternative explanation that auditors could systematically differ on the judgment of a particular industry’s inherent risk4.

4 Because the case intentionally omitted many factors of client acceptance procedures that could inform a fraud

judgment, the introduction included the following statements, “You have been asked to assess the probability of fraud based on limited information about the company. The case you are provided purposely omits information related to client acceptance discussions of other members of the firm. You are being asked to consider the potential for fraudulent financial reporting based on a taped interview by a colleague with the client’s controller/CFO. The video was recorded during initial discussions of considering the engagement.”

The video contained two segments. The first segment included the introduction of the auditor to the client CFO, which contained the manipulation of client likeability.5 One group viewed a pleasant, considerate, and interested client (likeable) while the other group viewed an abrasive, rude/unpleasant, and inconsiderate client (dislikable).The second portion of the video (consistent for all participants) portrayed the client answering the auditor’s questions. This portion of the video contained the fraud cues (seven statements) adapted from Eining, Jones, and Loebbecke (1997), which represented a moderate risk of fraud for the client. The moderate risk case was selected to avoid floor or ceiling effects. The second segment was appended to each version of the first segment to create the two video versions, which were randomly distributed to the participants.

Accountability was manipulated between subjects, with one group being informed that they would later be required to explain their fraud judgment and one group receiving no advance instructions regarding the explanation requirement. Fraud experience was measured with a dichotomous (yes/no) self-report of whether the auditor has ever been directly involved in judging the likelihood that a firm has fraudulent financial reporting.

Dependent variable

After viewing the video, participants provided their overall fraud judgment on an eleven-point fraud judgment scale adapted from Hoffman and Patton (1997). The scale endeleven-points were 1 (fraud extremely unlikely) and 11 (fraud extremely likely). Next, all participants provided an

5The video was produced using a 50-year-old white male with management experience as the hypothetical

client’s CFO. Because of potentially lengthy download time related to the video, the video was burned onto CDs for distribution to the participant pool. All other material, the introduction, overall judgment,

individual cues, manipulation check questions, and demographic questions were placed on a research web site managed by the author.

explanation for their judgment (recall that only the accountable group was informed that this explanation would be required).

Fraud Evidence Statements

In an effort to provide information about the process by which affect influences fraud judgments, participants were given ten additional independent statements made by the hypothetical client. After recording their fraud judgment and completing a distractor task, participants were asked to assess each additional statement on an 11-point scale of whether it was (or was not) indicative of fraud. The statements were adapted from the 37 red-flag cue examples in SAS 82 and SAS 99.6 Cues from Loebbecke et al. (1989), Hoffman and Patton (1997) and Bell and Carcello (2000) were evaluated in developing the statements to present to participants.7

Ten original red-flag fraud cues were selected and worded as a statement from the client in this case. The negative wording of each statement was then positively worded to create ten non red-flag statements. Each participant’s set of statements included five of the original red-flag statements and five non red-flag statements. Two versions of the ten statements were created such that the five red-flag (non red-flag) statements for half of the participants were the five non red-flag (red flag) statements for the other half of the participants. The statements are presented in Figure 2, and are categorized into statements relating to industry, management motivation, management attitudes, operations, or external auditor relationship (two cues from each category).

<Insert Figure 2 here>

6Statement on Auditing Standards (SAS) 82 provides five categories including management characteristics (attitude

and motivation), operating conditions, industry characteristics, and auditor relations (AICPA 1997). SAS 99

provides three categories based on the fraud triangle (pressure, opportunity and rationalization) developed to identify characteristics of fraud perpetrators.

7 We gratefully acknowledge Vicky Hoffman’s willingness to share her experimental materials and notes on fraud

Pretest

Several audit professors and several practicing auditors reviewed the materials. The practicing auditors were from a variety of firms and represented different levels of experience (staff, senior, and senior manager). The auditors unanimously agreed that the materials were of similar quality to firm training materials, and that the video accurately portrayed a likeable and dislikeable client similar to those they had encountered in practice. A pretest was conducted with students enrolled in an auditing class who had already covered the standard on fraud. The student participants completed the entire case for the non-accountable condition. The pretesting provided evidence that the likeability manipulation was salient, but not overwhelming. The mean rating for the dislikable client was 4.02 versus 5.52 for the dislikeable client on a scale from 1 (strong dislike) to 9 (strong like). The pretest also supported that the case represented a moderate risk of fraud, with participants rating the risk of fraud at a mean of 7.02 on a scale from 1 (fraud

extremely unlikely) to 11 (fraud extremely likely).

Because likeability is considered a central construct encompassing many psychological constructs (Brewer and Crano 1994), the pretest asked participants to rate the confederate CFO in the video on several personality characteristics. These included likeability (two questions), competence, honesty, and cooperativeness. Of the five questions, only the two likeability and the cooperativeness questions were significantly correlated to the assigned likeability condition. This provides evidence that, although the confederate CFO differed in likeability across conditions, he was not viewed differently in terms of honesty (means of 5.26 and 5.62 for dislike and like conditions, respectively) or competency (means of 4.74 and 4.62 for dislike and like conditions, respectively).

Demographics

The participants in this study were professional auditors from international and regional audit firms at levels from staff to partner.8 The participants’ fraud risk experience and rank demographics are presented in Table 1. Of the 140 auditor participants, 80 reported no

experience, and 60 reported having experience assessing fraud in their professional duties. One person with 6.5 years of experience who reported experience with fraud judgments did not report his professional rank, and one staff level with no fraud judgment experience answered all

questions except the overall fraud judgment question. <Insert Table 1 here>

Manipulation Checks

To evaluate the experimental manipulation of affect, auditor participants were asked several questions related to the client in the video. Following the Regan et al. (1974) protocol, two questions asked the participant to rate the client’s likeability from dislike to like and whether the participant would like to work with the client. Both questions were scaled from 1 (strong dislike) to 9 (strong like). The means for the two questions for the dislikeable and likeable conditions were 3.44, 2.84, and 5.78, 5.50, respectively. Both manipulation check questions indicate a significant effect of affect for the hypothetical client in the video (F = 139.258, p < .001 and F = 137.198, p < .001 respectively). That is, when the hypothetical client appeared rude (pleasant), the participants rated his likeability lower (higher) and would not (would) like to work with the person in the video. Six participants’ perceptions were not consistent with the

8 Approval for the use of human subjects was granted from the IRB at the institution where the experiment took

intended manipulation. That is, five (one) participants in the likeable (dislikeable) condition rated the CFO on the dislikable (likeable) end of the scale.9

Overall Judgment

After viewing the interview of the hypothetical client, participants made an overall initial fraud judgment. An eleven-point fraud likelihood scale adapted from Hoffman and Patton (1997) was used for the judgment. Recall that the case facts were intended to present a moderate risk of fraud. The mean rating for fraud risk for all subjects was 7.73 suggesting the case elicited a slightly higher than average risk of fraud.

The auditors’ overall fraud judgment was analyzed using a full factorial ANOVA, and the results are presented in Table 2. The results indicate a three-way interaction between likeability, experience and accountability (F= 2.869, p = .047); a two-way interaction of likeability and experience (F = 4.183, p = .022); and a main effect of client likeability (F = 17.294, p < .001). All p-values are one-tailed. To further explore the three-way interaction, specific simple main effects were analyzed. These results along with the mean fraud judgment by condition are reported in Table 3. The accountability manipulation did not reduce likeability for inexperienced participants. These participants rated the fraud likelihood judgment higher (lower) for the

dislikeable (likeable) client in both the low-accountable and high-accountable conditions (t = 3.049, p < .01 and t= 3.377, p < .01 respectively). For the experienced auditors, accountability mitigated the effect of likeability (lowaccountable: t = 1.817, p = .040; highaccountable: t = -0.012, p = .495), partially supporting H2. In summary, the main effect results support hypothesis one that client likeability does influence fraud judgments. However, it appears that task

9 The results are presented using all participants based on assigned likeability condition. An analysis without the six

experience alone is not sufficient to moderate its effects. Accountability in combination with task experience eliminates the bias in judgment caused by client likeability.10

<Insert Table 2 here> <Insert Table 3 here>

In the dislike (like) condition, the video included a statement by the client expressing displeasure (pleasure) about the audit process. It is possible that this statement may have influenced participants’ perceptions of management’s attitudes about internal controls or may convey poor source reliability (i.e. signal that management may be trying to conceal a fraud). This would be a relevant fraud risk factor as discussed under rationalization in SAS 99. SAS 99 describes rationalization as an “attitude, character, or set of ethical values that allows

management to knowingly and intentionally commit a dishonest act” (AU 316.07). The pretest ratings of the case client on the characteristics of honesty and competency were not different between the affect conditions, which provides evidence that the manipulation did not impact participants’ perceptions of management as it relates to relevant fraud factors. Further, when partners’ (all of whom had experience assessing fraud risk) judgments are examined

independently, likeability has no influence on fraud judgments, suggesting that experts did not view the information in the dislike condition as relevant to the fraud assessment.11

Fraud Statement Assessments

In addition to examining whether client likeability impacts overall fraud judgments, we also examine whether and how client likeability influences participants’ assessments of

10 As indicated in Table 1, the most variability in fraud experience existed among the senior and manager levels.

While the sample size is not large enough to examine the three-way interaction within this group, it should be noted that there is an overall main effect of likeability within this group (like mean = 7.67 vs. dislike mean 8.39, p=.045, two-tailed), indicating that general audit experience alone is not sufficient to eliminate the effect of likeability.

11 Seven partners, all with fraud assessment experience, judged the fraud risk to be similar regardless of the

likeability condition (like condition mean = 8.33 (n=3); dislike condition mean =8.0 (n=4)). This provides evidence that there were no additional relevant fraud risk cues in the dislike manipulation.

individual fraud evidence statements made by management. Recall that participants assessed ten independent statements made by management (see Figure 2), which included five red-flag and five non-red-flag statements. The shaded statements in Figure 2 comprise the ten statements used in the primary analysis discussed and presented below. The non-shaded statements comprise statement set version two, and produced similar results.12

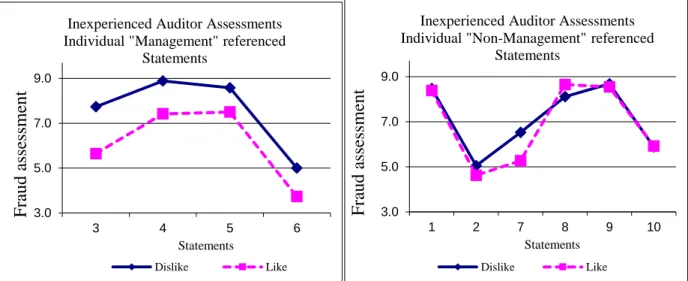

A statistical comparison of means was used to test likeability’s impact on the statement assessments for both the inexperienced and experienced auditors. For the inexperienced auditors, results indicate that five of the ten statements are impacted by client likeability. Statements 3, 4, 5, 6, and 7 are statistically different for the likeable versus dislikeable client conditions.13

Statements 3, 4, 5, and 6 all refer to management characteristics, while statement 7 relates to an operational characteristic. Conversely, for the experienced auditors there is no difference for nine of the ten statements.14 The dislike condition resulted in a higher fraud rating than the like

condition (p = .065) for statement 8, a related party evidence cue. Table 4 presents the means for the statement assessments across likeability condition and the corresponding t-test for the

inexperienced auditors only. The results provide support for Hypothesis 4. That is, client

likeability influences the assessments of evidence cues related to management characteristics for inexperienced (but not experienced) auditors. Inexperienced auditors rate statements that

represent management characteristics as more indicative of fraud for the dislikeable client than the likeable client. This provides evidence that, for inexperienced auditors, likeability impacts overall fraud judgments partially through its impact on the assessment of statements made by

12 Because the negatively worded red-flag statement may not be completely parallel to its positively worded non-red

flag statement counterpart, the statement sets were analyzed separately. The primary analysis (version one) includes 45 inexperienced and 27 experienced auditors.

13 For version 2 (where red-flag and non-red flag statements were reversed), statement 5 was not significantly

different between conditions, and two statements were significantly different at p < .10.

management. Since these ten statements were independent of (and assessed after) the fraud judgment, we are not able to test for a mediating effect, but inexperienced auditors do appear to exhibit attribution error of client likeability to evidence cues related to management

characteristics.

<Insert Table 4>

Of the five statements assessed by the inexperienced auditors differently for the likeable versus dislikeable client, two statements were red-flag statements (statements 4 and 5), and three were non-red-flag statements (statements 3, 6, and 7). Together, the results generally support the prediction that client likeability impacts the statements referring to management characteristics, regardless of whether or not the statement was a “red-flag” statement. Figure 3 presents a graphical representation of the fraud evidence assessments between likeability conditions for experienced and inexperienced auditors.

<Insert Figure 3>

CONCLUSIONS

As Bazerman et al. (2002) state: “We will need to embrace practices and regulations that recognize the existence of bias and moderate its ill effects.” Affect is one area of bias where there is still much to learn (Nelson and Tan 2005; Bhattacharjee and Moreno 2013). This research provides evidence that affect influences overall fraud judgments, and that this effect persists for auditors who are inexperienced with fraud judgments even when they are held accountable. One explanation for this result is that experienced auditors who anticipate having to explain their judgment have the requisite knowledge to enable systematic processing (system 2 thinking), which leads to the use of only relevant evidence in their judgments. These findings support the profession’s use of accountability tools (requiring documentation/justification) to

encourage effortful thought, but highlight the need for task-specific knowledge in fraud judgments. The professional standards encourage brainstorming and group discussions in discussions of fraud, which can provide a venue for experiential training for inexperienced auditors to learn to distinguish relevant from irrelevant information in their judgment process.

This paper provides a first step to identifying the boundary conditions of the combination of experience and accountability’s impact. Our paper supports the suggestion by Hammersley (2011) that since fraud experience is highly varied among auditors, task experience is potentially gained through firm training or fraud-related tasks, such as risk assessments. Future research could investigate a larger set of mid-level experienced participants (i.e. seniors/managers) and various training and practice factors that can improve fraud risk judgments to provide further evidence.

This paper also provides insights into how affect toward the client biases the processing of fraud cues for inexperienced auditors differently than experienced auditors. The results demonstrate that the inclusion of client likeability may not transcend all evidence evaluation. Client likeability impacts evidence statements that represent management characteristics, but it does not influence the assessment of fraud cues related to industry characteristics, related party transactions, or even past auditor relationships. This supports the notion that client likeability, which is irrelevant in fraud judgments, is errantly attributed to certain cues that are relevant to a fraud judgment. If the experiment had manipulated management’s honesty or integrity, it would have been appropriate for participants to differentially assess fraud cues related to management. However, the manipulation checks show that honesty, integrity, and competence were held constant across likeability conditions. This result is particularly important given that inexperienced auditor have significant interactions with audit clients. Bennett and Hatfield

(2013) find that 86 percent of staff level auditors report interacting with client management three or more days during a typical week of fieldwork, and senior and staff-level auditors reported interacting with the client more than managers or partners. Further, prior research shows that documentation by lower level staff has the potential to reduce the effectiveness of the subsequent judgments of reviewers (Libby and Trotman 1993; Anderson and Koonce 1998; Agoglia, Brazel, Hatfield 2009).

LIMITATIONS AND FUTURE DIRECTIONS

As with all experimental research, this paper may not generalize to other audit judgments, such as internal control effectiveness and going concern judgments. It only addresses a fraud judgment within a client acceptance procedure for a client with a moderate fraud risk. The experimental design provided for the randomization of accountability and affect between participants. However, experience with fraud was a measured variable. Thus, it is possible that experience is correlated with an unmeasured variable (i.e. client size, industry). Specific details about the client (i.e. industry) were intentionally not provided to mitigate these concerns. Because this is an experimental setting, it is possible that other factors present in the audit environment were omitted in the study that could impact the results. However, care was taken to ensure the experimental materials represented the true audit environment, and discussions with practicing auditors indicate that the scenario was realistic.

The results of this paper highlight the need for future research to investigate the impact of client environmental factors to other areas of auditor judgment and for varying fraud risk clients. Further, more research is needed on the types of evidence most likely to be impacted by client characteristics, the importance of relevant versus irrelevant affect in judgment, and the

example fraud cues from the professional standards, future research should investigate if evidence can be better categorized to identify the specific characteristics of evidence that are influenced by client likeability (i.e. objective versus subjective), to further refine when inexperienced auditors might use errant attribution in their judgment process.

This paper characterizes client likeability as an irrelevant factor for the fraud judgment. Bamber et al. (1997) find that auditors develop an “attitude toward the evidence” in the audit process (Bamber et al. 1997); thus, emotion toward some evidence is appropriate. In gathering evidence and formulating a fraud judgment, auditors must learn to appropriately utilize emotion to accurately select and weight evidence in their judgment process. Future research could further investigate how expert fraud examiners differentiate relevant and irrelevant emotion to assist the training of inexperienced auditors. Other methods for improving inexperienced auditor judgment include experiential training and electronic aids. Providing inexperienced auditors the knowledge possessed by experienced auditors could improve their judgment (e.g., Carpenter, Durtschi, and Gaynor 2006). Training material development would benefit from an examination of factors that both should and should not be included (cue selection) in the judgment beyond guidance that is provided by the current auditing standards. Electronic aids used as training tools and might also improve the information used and weight allocated to auditor judgments, such as decision

support systems and expert systems (Eining et al. 1997, Bell and Carcello 2000). Future research could investigate how affect impacts interactions in brainstorming sessions within the team. Further, the effects of general affect (i.e. engagement team anxiety/stress from looming or prior PCAOB inspections) versus targeted affect (i.e. affect toward the client) should be examined.

Finally, while the current paper examines the influence of the auditor’s affect toward the client, it may be fruitful for future research to examine whether management’s affect toward the

auditor is a relevant fraud signal that indicates an attempt to conceal fraud from the auditor. In our case, the dislikeable client expressed displeasure with the audit process, but we find no evidence that this was viewed as a relevant fraud cue. However, it is possible that a direct manipulation of client affect toward the auditor might be a relevant fraud cue. We know of no research that has examined this link. There are several anecdotal cases of clients with noteworthy personalities (i.e. Jeff Skilling at Enron), which may influence how auditors assess fraud risk.

REFERENCES

Agoglia, C. P., Hatfield, R. C., & Brazel, J. F. (2009). The effects of audit review format on review team judgments. Auditing: A Journal of Practice and Theory 28 (10), 95-111. Agoglia, C., Kida, T. & D. Hanno. (2003). The effects of alternative justification memos on the

judgments of audit reviewees and reviewers. Journal of Accounting Research, 41, 33–46. American Institute of Certified Public Accountants (AICPA). (1997). Consideration of Fraud in

a Financial Statement Audit. Statement on Auditing Standards No. 82. New York, NY, AICPA.

American Institute of Certified Public Accountants (AICPA). (2002a). AICPA Professional Standards. Chicago, American Institute of Certified Public Accountants.

American Institute of Certified Public Accountants (AICPA). (2002b). Consideration of Fraud in a Financial Statement Audit. Statement on Auditing Standards 99. New York, NY, AICPA.

Anderson, U., & Marchant, G. (1989). The auditor's assessment of the competence and integrity of auditee personnel. Auditing: A Journal of Practice and Theory 8(Supplement): 1-16. Anderson, U., Koonce, L. & Marchant, G. (1994). The effects of source-competence information

and its timing on auditors' performance of analytical procedures. Auditing: A Journal of Practice and Theory 13 (1), 137-148.

Anderson, U., & Koonce, L. (1998). Evaluating the sufficiency of causes in audit analytical procedures. Auditing: A Journal of Practice and Theory 17 (1), 1-12.

Bamber, E. M., Ramsay, R. & Tubbs, R. M. (1997). An examination of the descriptive validity of the belief-adjustment model and alternative attitudes to evidence in auditing.

Accounting Organizations and Society 22 (3/4), 249-268.

Bazerman, M., Loewenstein, G. F. & Moore, D. (2002). Why good accountants do bad audits. Harvard Business Review (November), 1-8.

Bell, T. B., & Carcello, J. V. (2000). A decision aid for assessing the likelihood of fraudulent financial reporting. Auditing: A Journal of Practice and Theory 19 (1), 169-184.

Bennett, G. B., & Hatfield, R. C. (2013). The effect of the social mismatch between staff auditors and client management on the collection of audit evidence. The Accounting Review 88 (1), 31-50.

Bhattacharjee, S., & Moreno, K. (2002). The impact of affective information on the professional judgment of more experienced and less experienced auditors. Journal of Behavioral Judgment and Decision Making 15 (August), 361-377.

Bhattacharjee, S., Moreno, K. & Riley, T. (2012). The interplay of interpersonal affect and source reliability on auditors' inventory judgments. Contemporary Accounting Research 29 (4), 1087-1108.

Bhattacharjee, S., & Moreno, K. (2013). The role of auditors' emotions and moods on audit judgment: A research summary with suggested practice implications. Current Issues in Auditing 7 (2), 1-8.

Bonner, S. E. (1990). Experience effects in auditing: The role of task-specific knowledge. The Accounting Review 65 (1), 72-92.

Bonner, S. E. & Lewis, B. L. (1990). Determinants of audit expertise. Journal of Accounting Research 28 (Supplement), 1-20.

Bonner, S. E. & Pennington, N. (1991). Cognitive processes and knowledge as determinants of auditor expertise. Journal of Accounting Literature 10, 1-50.

Brewer, M. B. & Crano, W. D. (1994). Social Psychology. St. Paul, MN, West.

Carpenter, T., Durtschi, C. & Gaynor, L. (2006). The effects of training methodologies in assessing both fraud risk and the relevance of fraud risk factors. Working Paper, University of Georgia, Athens Georgia.

Chaiken, S. (1980). Heuristic versus systematic information processing and the use of source versus message cues in persuasion. Journal of Personality and Social Psychology 39 (5), 752-766.

Darley, J. M. & Gross, P. H. (1983). A hypothesis-confirming bias in labeling effects. Journal of Personality and Social Psychology 44 (1), 20-33.

Davis, J. T. (1996). Experience and auditors' selection of relevant information for preliminary control risk assessments. Auditing: A Journal of Practice and Theory 15 (1), 16-37. DeZoort, T., Harrison, P. & Taylor, M. (2006). Accountability and auditors’ materiality

judgments: The effects of differential pressure strength on conservatism, variability, and effort. Accounting, Organizations, and Society 31, 373-390.

Eining, M. M., Jones, D. R. & Loebbecke, J. K. (1997). Fraud reliance on decision aids: An examination of auditors' assessment of management fraud. Auditing: A Journal of Practice and Theory 16 (2), 1-19.

Fiske, S. T. & Taylor, S. (1991). Social Cognition. New York, McGraw-Hill.

Frederick, D. (1991). Auditors' representation and retrieval of internal control knowledge. The Accounting Review (April), 240-258.

Gibbins, M. & Wolf, F. M. (1982). Auditors' subjective decision environment: The case of a normal external audit. The Accounting Review 57 (1), 105-124.

Hackenbrack, K. (1992). Implications of seemingly irrelevant evidence in audit judgment. Journal of Accounting Research 30 (1), 126-136.

Hammersley, J. S. (2011). A review and model of auditor judgments in fraud-related planning tasks. Auditing: A Journal of Practice and Theory 30 (4), 101-128.

Hastie, R. (1984). Causes and effects of causal attribution. Journal of Personality and Social Psychology 46 (1), 44-56.

Haynes, C. M. (1999). Auditors' evaluation of evidence obtained through management inquiry: A cascaded-inference approach. Auditing: A Journal of Practice and Theory 18 (2), 87-104.

Hirst, D. E. (1992). Discussion of "The effects of accountability on judgment: Development of hypotheses for auditing. Auditing: A Journal of Practice and Theory 11 (Supplement), 139-145.

Hirst, D. E. (1994). Auditors' sensitivity to source reliability. Journal of Accounting Research 32 (1), 113-125.

Hoffman, V. B. & Patton, J. M. (1997). Accountability, the dilution effect, and conservatism in auditors' fraud judgments. Journal of Accounting Research 35 (2), 227-237.

Kadous, K. (2001). Improving jurors' evaluation of auditors in negligence cases. Contemporary Accounting Research 18 (3), 425-444.

Kennedy, J. (1993). Debiasing audit judgment with accountability: A framework and experimental results. Journal of Accounting Research (Autumn), 231-245.

Kennedy, J. (1995). Debiasing the curse of knowledge in audit judgment. The Accounting Review 70 (April), 249-270.

Kida, T. & Smith, J. F. (1995). The encoding and retrieval of numerical data for decision Making in accounting contexts: Model development. Accounting Organizations and Society 20 (7/8), 585-610.

Kida, T., Smith, J. F. & Maletta, M. (1998). The effects of encoded memory traces for numeric data on accounting decision making. Accounting, Organizations and Society 20 (5/6), 451-466.

Kida, T., Moreno, K. & Smith, J. F. (2001). The influence of affect on managers' capital-budgeting decisions. Contemporary Accounting Research 18 (3), 477-494.

Kinney, W. R. J. (1999). Auditor independence: A burdensome constraint or core value? Accounting Horizons 13 (1), 69-75.

Koonce, L. (1992). Explanation and counterexplanation during audit analytical review. The Accounting Review 67 (1), 59-76.

Libby, R. & Frederick, D. (1990). Experience and the ability to explain audit findings. Journal of Accounting Research (Autumn), 348-367.

Libby, R. & Trotman, K. T. (1993). The review process as a control for differential recall of evidence in auditor judgments. Accounting Organizations and Society 18 (August), 559-574.

Libby, R. & Tan, H. (1994). Modeling the determinants of audit expertise. Accounting Organizations and Society 19 (8), 701-716.

Loebbecke, J. K., Eining, M. M. & Willingham, J. J. (1989). Auditors' experience with material irregularities: Frequency, nature, and detectability. Auditing: A Journal of Practice and Theory 9 (1), 1-28.

Lord, A. T., Lepper, M. R. & Preston, E. (1984). Considering the opposite: A corrective strategy for social judgment. Journal of Personality and Social Psychology 47 (6), 1231-1243. Marden, R. E., Holstrum, G. L. & Schneider, S. L. (1997). Control environment condition and

the interaction between control risk, account type and management's assertions. Auditing: A Journal of Practice and Theory 16 (1), 51-68.

Messier, W. F. & Quilliam, W. C. (1992). The effect of accountability on judgment:

development of hypotheses for auditing. Auditing: A Journal of Practice and Theory (Supplement), 123-138.

Moreno, K., Kida, T. & Smith, J. F. (2002). The impact of affective reactions on risky decision making in accounting contexts. Journal of Accounting Research 40 (5), 1331-1349. Nelson, M. & Tan, H. T. (2005). Judgment and decision making research in auditing: A task,

person, and interpersonal interaction perspective. Auditing: A Journal of Practice and Theory 24 (Supplement), 41–71.

Nisbett, R. E., Zukier, H. & Lemley, R. E. (1981). The dilution effect: Nondiagnostic

information weakens the implications of diagnostic information. Cognitive Psychology 13, 248-277.

Peecher, M. E. (1996). The influence of auditors' justification processes on their decisions: A cognitive model and experimental evidence. Journal of Accounting Research (Spring), 125-140.

Regan, D. T., Straus, E. & Fazio, R. H. (1974). Liking and the attribution process. Journal of Experimental Social Psychology 10, 385-397.

Shelton, S. W. (1999). The effect of experience on the use of irrelevant evidence in auditor judgment. The Accounting Review 74 (2), 217-224.

Tetlock, P. E. (1983). Accountability and the perseverance of first impressions. Social Psychology Quarterly 46 (4), 285-292.

Tetlock, P. E. (1992). The impact of accountability on judgment and choice: Toward a social contingency model. Advances in Experimental Social Psychology 25, 331-376.

Tetlock, P. E. & Boettger, R. (1989). Accountability: A social magnifier of the dilution effect. Journal of Personality and Social Psychology 57 (3), 388-398.

U.S. House of Representatives. (2002). The Sarbanes-Oxley Act of 2002. Public Law 107-204 [H.R. 3763]. Washington, D.C.: Government Printing Office.

Waller, W. S. (1989). Discussion of the auditor's assessment of the competence and integrity of auditee personnel. Auditing: A Journal of Practice and Theory 8 (Supplement), 17-21. Wright, A. & Mock, T. J. (1985). Towards a contingency view of audit evidence. Auditing: A

Journal of Practice and Theory 5 (1), 91-100.

Zajonc, R. B. (1980). Feeling and thinking: Preferences need no inferences. American Psychologist 35 (2), 151-175.

FIGURE 1

Participant Steps in Experiment

1. Receive email from office partner requesting participation and CD (video) in office mail folder

2. Open link to the research website and read an introduction to the study that includes the purpose and a modified consent form.

3. Review hypothetical company and fraud likelihood scale example with explanation of midpoint being average client for the audit firm.

4. Receive accountability treatment manipulation

5. Watch video of an interview with the client containing affect (likeability) manipulation 6. Make an overall likelihood judgment of fraud

7. Document reasons for their judgment

8. Complete distracter task: remove the CD and record the CD key number (to identify likeable/dislikable group membership)

9. Make an assessment of ten additional CFO statements related to fraud likelihood. 10.Complete a demographic survey and manipulation check questions

FIGURE 2

Independent Fraud Statements

“Red-Flag” “Non- Red-Flag”

Industry Conditions

1

As you know, our industry is very competitive with fairly saturated product markets. It’s so tough that we haven’t been able to maintain our profit margins over the last few years.

As you know, our industry is not very

competitive; our product markets are far from saturated. We’ve had no trouble maintaining our profit margins over the last few years.

2

The industry is changing so fast,

particularly product technology. We’ve had to handle a great deal of product

obsolescence.

The industry doesn’t change very fast,

particularly product technology. We haven’t had to deal with much product obsolescence.

Management Motivation (Pressures)

3

Our new executive team tries to maintain our share price with some fairly aggressive accounting practices.

Our new executive team manages to maintain our share price without resorting to aggressive accounting practices.

4 Our new executive team gives analysts what appear to be very optimistic forecasts.

Our new executive team gives analysts what appear to be very achievable forecasts.

Management Attitudes

5

Because of budget constraints we continue to struggle with the effectiveness of our IT system as well as our internal audit staff.

Since we don’t have tight budget constraints we are quite happy with the effectiveness of our IT system and our internal audit staff.

6

In my view, the new executive team has not communicated its vision in terms of values and ethics very effectively.

In my view, the new executive team has communicated its vision in terms of values and ethics very effectively.

Operating Conditions

7

We have barely managed to generate cash flows from operations, while reporting earnings growth.

We have easily managed to generate cash flows from operations, while reporting earnings growth.

8

The significant related-party transactions we have are not in the ordinary course of business.

We have not had any significant related-party transactions in the ordinary course of business.

External Auditor Relationship

9 I must admit that we did have some disputes with our previous auditor. I’m happy to say that we did not have any disputes with our previous auditor.

10

I don’t think that our previous auditor understood our need for a quick audit and issuance of their report.

I think that our previous auditor understood that we didn’t need a quick audit and issuance of their report.

NOTE: Participants viewed five red-flag and five non red-flag statements after their fraud judgment was recorded. Two versions were created such that the five red-flag (non red-flag) statements for half of the participants were the five non red-flag (red flag) statements for the other half of the participants. Shaded statements indicate the ten statements used in version 1. The non-shaded statements were used in version 2.

FIGURE 3 Panel A

No Experience with Fraud Judgment

Statements 3, 4, 5, and 6 refer to management characteristics (see Figure 2, version one), and each assessment is significantly different based on the client likeability condition (all p < .05). Statements 3 and 6 are non-flag statements, and statements 4 and 5 are red-flag statements. For version 2, there is no significant difference for statement 5. All p-values are one-tailed.

For the non-management statements (1, 2, 7, 8, 9 and 10) five of the six assessments are not statistically different based on the client likeability condition. Statement 7 is an “operating” cue, and fraud is rated statistically higher for a dislikeable client than a likeable client. Statements 2, 7, and 10 are non-red-flag

statements, and statements 8 and 9 are red-flag statements.

Panel B

Experience with Fraud Judgment

For auditors with fraud judgment experience, there is no difference in the assessment of nine of the ten individual statements based on client likeability in version 1. Likeability influenced the assessment of Statement 8, a related party evidence cue (p = .065). There is no significant difference for any statement for the experienced auditors for version 2 of the statements.

3.0 5.0 7.0 9.0 3 4 5 6 F ra ud assessment Statements

Inexperienced Auditor Assessments Individual "Management" referenced

Statements Dislike Like 3.0 5.0 7.0 9.0 1 2 7 8 9 10 F ra ud assessment Statements

Inexperienced Auditor Assessments Individual "Non-Management" referenced

Statements Dislike Like 3.0 5.0 7.0 9.0 3 4 5 6 F ra ud assessment Statements

Experienced Auditor Assessments Individual "Management" referenced

Statements Dislike Like 3.0 5.0 7.0 9.0 1 2 7 8 9 10 F ra ud assessment Statements

Experienced Auditor Assessments Individual "Non-Management" referenced

Statements

TABLE 1

Participant Task Experience by Professional Rank

Experience a Staff Senior Manager Senior

Manager Partner Total

No 55 19 4 1 0 79

Yes 8 22 8 14 7 59

63 41 12 15 7 138 b

aSelf-reported experience of the auditor’s direct experience assessing the likelihood of fraud for an

audit client.

b One participant with 6.5 years of experience (with fraud experience) did not provide professional

TABLE 2

Univariate ANOVA of auditor’s overall judgment a

Source of variance DF Mean Square F-value Sig.b

Likeable (Like) c -H1 1 32.959 17.294 .000 Accountability (Acct) d 1 .148 .078 .391 Experiencee 1 2.236 1.173 .141 Acct * Like -H2 1 .369 .193 .331 Experience * Like –H3 1 7.971 4.183 .022 Acct * Experience 1 2.580 1.354 .124 Like*Acct*Experience 1 5.468 2.869 .047 Error 131 1.906

aThe overall judgment is measured on an eleven-point fraud judgment scale adapted from Hoffman and Patton

(1997). Eleven indicates a high likelihood of fraud, and one indicates a low likelihood of fraud.

b All statistical test significance values are one-tailed.

cClient likeability (Like) is manipulated through a video recording of the auditor-client introduction, with the

client represented as likeable or not likeable.

dAccountability is manipulated through a forewarning of a required post-judgment explanation (high accountable)

or by omitting this instruction (low accountable).

eExperience is a self-report measure of the auditor’s experience with making a fraud risk judgment in their