In-vehicle Enabler Considerations

3

Considerations with Smartphones Solutions

5

Considerations

with

OBD-II

Solutions

6

Considerations

with

Hybrid

Solutions

8

Factors to Consider When Comparing Mobile, OBD-II, and Hybrid Solutions

10

Data Quality

10

Continuity of the Data Record

12

User Experience

12

Accident Data

13

Summary: Data Collection Trade-offs

14

Choosing a Telematics Partner

16

Executive Summary

As insurance telematics gains momentum and nears a tipping point in the insurance market, connected car technologies continue to emerge and evolve, face the challenges of real-world implementations, and gain acceptance or rejection based on their merit. Acceptance hinges on a variety of factors—some financial and some related to how well the technology meets technical challenges and suits market requirements in daily practice. Solutions that deliver effectively on promised capabilities must also be measured in terms of cost effectiveness. Inexpensive solutions that seem attractive initially need to measure up in terms of general usability, including reliability, precision, and the overall user experience.

Usage-based Insurance (UBI) has experienced whirlwind growth over the last few years, and the technology choices that gain favor in the near term will influence the direction of the market for years to come. One of the key areas of focus is data collection. Techniques for collecting, consolidating, and analyzing the data required to assess driver behavior continue to be refined as the technologies for accomplishing this undergo an inevitable evolution. At the moment, a fundamental question is being debated throughout the industry: what is the right solution for my program? Should connectivity rely on data captured with a standalone, cellular-based OBD device? Or rely on technology brought into the vehicle (smartphones)? Or use a hybrid solution consisting of multiple technologies.

Accurate, timely data is an essential commodity in the telematics-based insurance market— both in commercial and personal lines applications—so the methods, costs, and precision of collecting data are prime factors in the viability of UBI programs. Many of the current leading products in this market connect directly to a vehicle’s on-board diagnostics port and use different mechanisms for transmitting driving data to the insurer’s back-office servers (or other collection point). More recently, UBI products and services based on smartphones have been introduced as alternatives to OBD-II solutions for capturing and delivering driver and vehicle data. Hybrid solutions, consisting of a device that connects to the car by means of an OBD port but leverages the smartphone for data transmission, have been positioned as cost-effective solutions for insurers. This paper compares the relative strengths and trade-offs of three leading data collection solutions used in telematics programs: mobile, OBD-II, and hybrid solutions. Fundamentally, a knowledgeable telematics service provider (TSP) is imperative in explaining the various options and helping you select the technology to meet insurance program goals and requirements. The perspective provided in this paper draws on field research performed by IMS through pilot programs and actual deployments with customers, as well as surveys and research conducted by organizations in the telematics industry.

UBI Data Collection Techniques

The insurance industry has always been data-centric, but telematics adds extra dimensions of volume and large-scale processing to the equation. The challenge of capturing, processing, and analyzing information from telematics devices on hundreds of thousands of vehicles is substantial. Telematics devices typically produce a data record every second, which can include G-force values, date, time, speed, location, cumulative trip mileage, fuel consumption, and more. The quality, scope, and precision of the data depend on the type of telematics device that is capturing and transmitting it. Ultimately, the goal is to correlate the driver and vehicle data collected with insurance claims data, performing analysis to determine which variables relate to increased driver risk and claims losses.

From the perspective of the insurer, particular types of information are vital to assessing and grading driver behavior—regardless of the equipment that collects that data. Each of the solutions discussed in this paper—OBD-II, mobile, and hybrid—have varying strengths and weaknesses. Rather than choosing any one approach over another, this paper discusses how each solution may work effectively for a particular type of insurance program, based on its inherent characteristics and features. The goal is to provide an overall understanding of the choices in the telematics market. We recommend that you consult an experienced telematics service provider to help critically evaluate trade-offs and capabilities before committing to any one solution over another.

One technology commonly used for vehicle telematics data collection is the OBD-II interface, a federally mandated feature on all US vehicles since model year 1996. The equivalent standard in Europe is called EOBD (European On-Board Diagnostics). For simplicity, this paper will refer to OBD-II throughout, with the understanding that the term also includes EOBD.

OBD-II is a vehicle standard that includes specifications for diagnostic coding, electrical signaling protocols, and messaging protocols for exchanging information with other devices. Although not originally designed with vehicle telematics in mind, OBD-II provides access to data indicating vehicle speed, engine rpms, calculated fuel consumption, general trip data, and other information (in addition to the diagnostic data for which the port was designed). All of the relevant information can be transmitted into a telematics data collection system. OBD-II relies on the standardized vehicle hardware port—tied directly to the built-in monitoring and diagnostics system and generally supplemented with data loggers and data transmission equipment. This approach has provided the framework underlying much of the insurance telematics market today, and it has a number of clear and compelling differences from smartphone data collection.

Another option to consider: telematics data collection by smartphone has been generating increased interest in the UBI sector. Hardware costs are eliminated for the insurer—since the approach relies on the consumer’s smartphone instead of add-on hardware. There are, however, a number of limitations that offset the cost advantages to some degree.

Rather than the unified infrastructure surrounding OBD-II connectivity, smartphones today rely on several different operating systems and platforms, each of which can change at an

accelerated rate as new phones are introduced. Collecting data from these individual platforms in a consistent manner to a central system can be problematic, particularly keeping track of the different versions of both smartphones and operating systems and adapting to their changing connectivity standards. Another consideration is that the consumer-grade sensors used in smartphones are specifically designed for phone applications, not telematics data collection. With the diversity of smartphone makes and models, and different sensors, to account for these differences, algorithms must be applied to normalize the data that is collected, stored, and analyzed. Once the data is normalized and the other considerations addressed, smartphone telematics solutions can be successfully incorporated into a variety of UBI programs. Because of the unified nature of the solution, the cost effectiveness of smartphone-based solutions can provide an effective introductory telematics offering. Presenting data to the driver through the smartphone is also a natural and intuitive way to receive information, as well as to perform data collection and transmission.

Hybrid solutions represent another approach that has gained popularity in the marketplace. A hybrid solution combines an OBD-II device installed in the vehicle with Bluetooth capabilities for data collection and a smartphone to relay data using its wireless connection and data plan. As discussed later in this paper, this approach offers a high degree of data integrity related to vehicle operation and provides the benefits of cost-effective smartphone data transmission. It does, however, present added complexities for the end user.

Telematics programs differ widely, and the appropriate set of options and optimal solution to use should be based on client needs and program objectives. For example, commercial programs present very different needs and requirements than a personal lines program. A telematics solution focused on lead generation and customer acquisition will by nature differ from a complete implementation (and might initially use a smartphone for collection later to be replaced by an OBD-II device). Other factors—such as a different client consumer segments— can impact the evaluation and suggest the most appropriate telematics data collection technique. This paper explores the range of considerations that can impact various programs.

In-vehicle Enabler Considerations

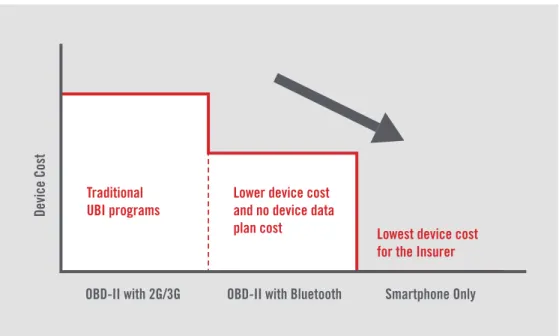

Costs for all forms of telematics data collection are steadily declining as technologies improve, with smartphone solutions leading the pack, as shown in Figure 1. Most current OBD-II solutions rely on 2G or 3G mobile telecommunications technology for data transmission, but OBD-II with Bluetooth offers a lower cost alternative, and this approach does not require a separate data plan. From the point of view of the insurer, smartphone-only solutions present the lowest cost because the insured individual has already invested in the smartphone and also pays for the cellular data plan by which the collected data is transmitted (no additional hardware device is required).

Figure 2 shows the basic components of telematics solutions based on OBD-II and mobile phones. Although there are other approaches to the hardware used for data collection, these examples show most common implementations.

OBD-II OBD-II

(with Bluetooth) SMARTPHONE

Device Cost

OBD-II with 2G/3G

Traditional UBI programs

Lowest device cost for the Insurer Lower device cost

and no device data plan cost

OBD-II with Bluetooth Smartphone Only

Figure 1. UBI Device Costs

The options shown in Figure 2 have these characteristics:

> OBD-II: As the longest running and most prevalent solution in the marketplace, permanently plugged-in OBD-II devices have a proven track record and level of acceptance.

> Hybrid solution - OBD-II with Bluetooth and Smartphone: This approach is gaining popularity in the telematics market. OBD-II device functionality can be extended and enhanced by coupling communication with a smartphone by means of a Bluetooth connection. Data transmission can be performed using the smartphone communication and data plan capabilities (saving on the need for setting up separate communication through the OBD-II device).

> Smartphones: Telematics solutions based on smartphones lower installation costs, can provide a variety of custom features through apps, and offer a straightforward path to telematics data collection through the smartphone’s data transmission capabilities (i.e., data plan, WiFi, and so on).

Considerations with Smartphones Solutions

The excitement around smartphones for telematics data collection stems from the possibilities offered by these devices—many of which are well suited to the insurance telematics business model. Current smartphones feature a number of built-in sensors and capabilities that equip them to collect data for telematics analytics. The typical, current-generation smartphone includes a precision global-positioning system (GPS) receiver, accelerometers for detecting G-forces, and multiple data connectivity mechanisms. These capabilities can be complemented with additional sensors, such as a magnetometer, proximity sensor, and ambient light sensor. Used as the hub of a telematics solution, the smartphone offers the advantages and challenges shown in Table 1.

Table 1. Advantages and Challenges of Smartphone Solutions

SMARTPHONE ADVANTAGES

SMARTPHONE CHALLENGES

Inexpensive alternative: The solution relies on a device that the individual already has and the provider does not assume this cost. Vehicle installation is not required, so the solution can be quickly implemented with no additional hardware.

Regular capture of quality trip data: Solutions must include a mechanism to ensure that trip data is captured on a regular basis (beyond the basic assurance that the insured driver has the phone charged and turned on to register trips in a reliable way). Ensuring that the data collected by accelerometers and GPS is high quality data is also a consideration.

Portability: Smartphones allow driving behaviors to be assessed among several different vehicles used by the driver. This differs from an OBD-II solution, in which several different drivers may be using the same car, but typically only the car, not the driver, is assessed.

Deliberate fraud: Solutions need to address the possibility of deliberate fraud, where the driver disables the app or turns off the phone to hide risky trips from the data record.

Custom apps tailored to smartphone capabilities: Custom apps offer a way to provide training, coaching, social interaction, and useful advice to drivers through their smartphones.

Regulatory approvals: Obtaining necessary approvals for smartphone data collection from those regulatory bodies involved in vehicle insurance is necessary in some cases.

Vehicle compatibility not an issue: Smartphone solutions can be used with any type of vehicle.

Battery life: Optimizing smartphone battery life requires balancing telematics data collection with the overall lifespan of the smartphone battery to avoid excess power drainage.

Lack of direct vehicle information: No value-added services can be created that relate to vehicle information, such as maintenance tips and operational warnings, because the smartphone does not have direct access to diagnostics and internal vehicle data.

Considerations with OBD-II Solutions

Telematics solutions based on OBD-II feature dedicated, secure connections between a vehicle and the back-office server consolidating the data (whether located at the insurer’s site or a service provider). OBD-II is well established and in widespread use by many insurance companies that offer UBI programs. The OBD-II connection ensures positive vehicle identification. It reduces the possibility that the insured party will turn off the data collection at any stage and identifies those time periods when the device is disconnected. This is a necessary requirement for many state insurance regulators and insurance carriers. Table 2 shows the advantages and challenges associated with OBD-II telematics solutions.

Table 2. Advantages and Challenges of OBD-II Solutions

OBD-II ADVANTAGES

OBD-II CHALLENGES

Uniformity: Using OBD-II in this manner ensures that the data collected will be fair and unbiased across all demographics, vehicle types, vehicle uses, and drivers. Insured drivers within this type of program will be treated equitably, and measurements made will use equivalent values.

Limited to a single port: Each vehicle has only a single OBD-II port that supports only one device at a time. Fleet providers, road-charging entities, and consumer applications all have begun to come up with special-purpose add-ons using this port. These add-ons could compete with availability for UBI telematics applications unless a service provider is selected to deliver both UBI and the additional service available from the special-purpose add-ons.

High reliability: Solutions based on OBD-II hardware are highly reliable, using proven methods to establish the necessary vehicle- to-insurance carrier connectivity and to transmit all data to the insurer quickly and accurately.

Higher hardware costs: Although the required hardware to equip a vehicle for UBI telematics use and data collection is less expensive than less permanent solutions, such as smartphones, the costs to equip the vehicle are covered by the insurance carrier as opposed to the smartphone that is paid for by the driver. Costs for hardware continue to be reduced as design improvements and mass commoditization have been introduced, but still represent a potential obstacle for insurers who are seeking to implement UBI telematics at

the lowest possible cost.

Value-added services: Integration with internal vehicle information opens opportunities to provide particular enhanced types of value-added services, such as maintenance reminders, roadside assistance, crash notification, and more. Value-added services are available with mobile solutions, but not as closely integrated with the vehicle itself (such as automated roadside assistance or captured collision data).

Vehicle compatibility concerns: OBD-II availability is limited to light duty vehicles manufactured later than 1995 in North America, and light duty vehicles later than 2000 in Europe. There are still a few vehicles, particularly in areas outside of North America, that do not fit into these categories and may not have an OBD-II (EOBD) connection port.

Exceptional security: The nature of an OBD-II hardware-based solution minimizes possibilities for fraudulent acts and eliminates the potential for individuals to circumvent the monitoring system. Many solutions immediately detect the deliberate removal of the OBD-II device.

Considerations with Hybrid Solutions

In some ways, Bluetooth-linked hybrid telematics solutions exhibit the best characteristics of individual OBD-II and smartphone solutions from an insurer’s perspective. As is the case with OBD-II, the hybrid solution provides excellent data quality, standardized information capture that is always associated with a single vehicle, and a higher degree of precision and reliability because of the fixed mounting of the OBD-II device in the vehicle. Also, because the insured individual contributes the smartphone to the solution and already pays the monthly costs of the data plan, leveraged for data transmission, the insurer does not bear device costs or data expenses. As with all the solutions discussed in this paper, however, there are tradeoffs to the advantages associated with hybrid solutions, detailed in Table 3.

Table 3. Advantages and Challenges of Hybrid Solutions

OBD-II ADVANTAGES

OBD-II CHALLENGES

Delivers consistent, high-quality data: Because the hybrid solution relies on data collected from an OBD-II device using in-vehicle sensors, information about VSS, RPM, fuel levels, trip delineation, and so on, are extremely precise. Accelerometer data is equivalent to OBD-II solutions that directly offer data links through cellular services.

Requires more involvement from the policyholder: Each insured individual must provide a compatible smartphone, complete the steps for Bluetooth pairing with the OBD-II device, and install the telematics application on his or her phone. The insured parties must also regularly bring along their smartphone when driving, with Bluetooth enabled, to complete the data transmissions. If any steps are omitted, no data can be accessed or transmitted.

Provides enhanced FNOL: The hybrid solution offers superior First Notice of Loss (FNOL) reporting, because of the close correlation with second-by-second vehicle data that can detect accidents and hasten claim responses. The solution also offers deeper insight into the nature of incidents based on precision data captured by the OBD-II device.

Presents data loss possibilities: If a phone is not available on the Bluetooth link within a reasonable amount of time, data collected by the OBD-II device could overflow before it is transmitted. This creates a potential for data loss (less loss potential, however, than for a standalone smartphone application).

Opens opportunities for value-added services: Insurers can craft custom programs that use smartphone applications to provide additional value for the insured individual. These value-added services might include automotive service reminders, vehicle and weather warnings, traffic updates, geolocation services, and more.

Uses policyholders wireless plan for data transmission: Hybrid solutions require that the insured individual have an active wireless data plan and maintain it in good standing over the course of the policy term.

Reduces operational costs for insurers: Policyholders already incur the cost of the data plan that transmits collected data from the smartphone, removing this operational cost from the insurer. Typically, OBD devices used in hybrid solutions are lower in cost than their cellular counterparts, as they require fewer internal components (relying on the smartphone) for data transmission.

Introduces a greater need for support: Insurers will need to provide more support for insured individuals, who may need help with smartphone installations, Bluetooth pairing, application use, data communication issues, and so on.

Raises possible compatibility issues over time: Vehicle compatibility with hybrid solutions is not automatically assured. Also, the frequent nature of smartphone technology updates and operating system releases could pose ongoing compatibility issues that would require testing and validation. Early adopters with solutions already installed may face the challenge of keeping the solution current and operable.

Factors to Consider When Comparing Mobile, OBD-II, and Hybrid Solutions

When assessing the relative merits of data collection by mobile, OBD-II, and hybrid solutions, consider these primary factors in your evaluation.

> Data quality: Many different factors affect data quality, all of which have a bearing on the quality of the solution.

> Continuity of the data record: Data that is captured continuously and is accessible as needed improves the value and utility of the driver evaluation.

> User experience: Solutions that are transparent to the user and don’t require active engagement typically yield better collection results.

> Accident data: A smartphone-only solution is not quite as good as a black box or any device attached to the vehicle in providing a picture of an accident.

Data Quality

To satisfy data quality standards—for smartphone, hybrid, and OBD-II solutions—continuous, calibrated measurements must be captured from the smartphone or vehicle sensors. This can be easier to accomplish with in-vehicle, cellular-based OBD-II solutions and hybrid solutions because of the direct connection to the vehicle’s engine control module. In mobile applications, the use of data fusion techniques can enhance the quality of collected sensor data, as well as exclude poor quality data that cannot be verified or validated. In some instances, data fusion techniques have also been applied to OBD-II solutions to enhance data results.

Vehicle speed can be determined precisely with solutions consisting of an OBD-II device, based on data from the Vehicle Speed Sensor (VSS) in the automobile and GPS-based speed. In smartphone solutions, vehicle speed can only be calculated based on the GPS signal, which can be inaccurate in certain conditions and also requires that a strong GPS signal is being received. The VSS data values can also provide insights into certain types of driving behavior by detecting indications of wheel spin and loss of vehicle traction.

Although positional and speed data collected from smartphone-only solutions can come quite close to the quality of positional and speed data from OBD-II-equipped options, it cannot entirely match the same degree of precision and reliability, especially in terms of capturing data relevant to accidents. Because the smartphone is not physically secured, the data collected can be affected by movement within the vehicle, such as the phone sliding off a seat into the footwell during hard braking, which creates potentially confusing data (see the section that follows titled “Accident Data”).

As shown in Figure 3, in dense urban areas with strong GPS signals, positional data accuracy is very good. In marginal areas where signal strength is less reliable, positional accuracy may suffer.

The degree of accuracy is also dependent on the quality of the GPS receiver, which can vary from device to device.

Under optimal conditions, data collected from GPS speed calculations compares favorably to captured data from OBD-II vehicle speed sensors, as shown in Figure 4.

Figure 3. GPS Positional Data Accuracy in Urban Settings

Continuity of the Data Record

An OBD-II-equipped solution essentially connects a vehicle to the data collection mechanism (not the actual driver), while mobile device solutions rely on the owner of a smartphone bringing that phone along in whatever vehicle is being driven.

There are pros and cons to each approach. For younger drivers without their own vehicle, the use of a smartphone can track that driver’s performance regardless of whose car is being driven, letting them establish a driving record that can help keep premiums low. Success of this approach depends on whether the mobile application being used can automatically activate in driving situations and minimize ways that the driver can circumvent the monitoring process. The more contiguous the data record tracked for the driver, the more precise the ratings that can be calculated based on driver performance (with subsequent adjustments made to the insurance rates). If the solution depends on the driver selectively turning the app on or off during trips or travel, the potential for fraud is much greater. Authentication models for smartphones can be used to keep track of when the ignition is turned on or off, so insurers have a means to determine how frequently drivers are using the software.

OBD-II solutions and hybrid solutions using OBD-II provide a more stable, permanent solution (that can’t be turned off without detection). These solutions are mounted in place and ready to record data from the moment the car moves. However, they typically lack any mechanism for identifying individual drivers in situations where more than one person often drives the vehicle. If, for example, a father loans his vehicle that he uses for a daily commute to his less-experienced son on the weekend, data collection cannot distinguish between the father’s driving habits and the son’s without additional input at this point.

User Experience

Different user demographics have different expectations of an insurance telematics solution, and insurers should be aware of these differences when crafting solutions. Younger drivers, particularly those in the millennial generation (born between 1980 and 2000) are highly adapted to smartphone use. They are digital natives and use social networking heavily. They are open to new technologies and would be likely to respond positively to a smartphone app that highlights metrics that determine the driver’s premium while offering tips on how to improve one’s rating. The social aspects of smartphones could also be used by the insurer in innovative ways to create a dialog with the drivers. Incentivized programs or gamification could be used to influence the millennial’s driving behavior, encouraging safer practices and generally creating greater engagement from the drivers. Active use of smartphones to make calls while driving, for example, could be discouraged, depending on the insurer’s policies. Using transparent algorithms to assess driving behavior and encourage better driving practices would likely be positively received by this generation. Other age groups could be responsive to these incentives as well.

Older drivers may not own smartphones or may prefer solutions that are built into the vehicle and require no interaction from them. This is where the transparency of an OBD-II-equipped solution tends to gain favor. Older drivers may also be less inclined to engage in incentive programs that

offer only slight improvements in their rates and prefer solutions that operate completely in the background, not requiring their engagement or interaction in any way.

For mobile applications, power management is another critical aspect of the overall user experience. If the sensors are active continuously and drain the smartphone’s battery so that it’s not available for use when needed, most users won’t be inclined to use this solution over the long term. Developing algorithms to selectively engage sensors and manage power use proactively can extend the smartphone battery life and improve the user experience.

Hybrid solutions offer a more flexible approach to the user experience by developing the program features around a smartphone application, but they also place greater demands on the user, who must successfully complete the Bluetooth pairing with the OBD-II device, install the required application, and ensure that cellular communication is available on a regular basis to complete the data collection cycle.

Accident Data

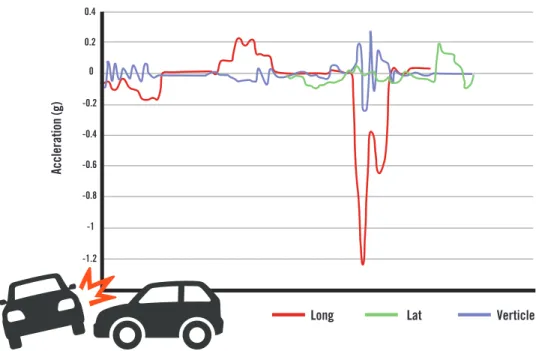

Because the smartphone in a mobile data collection application is often not securely fastened to the vehicle, it delivers less relevant accident data in collisions. For example, the smartphone may be lying on the seat beside the driver or loosely resting in a cup holder so that during a collision, the accelerometers may not provide precise data. Secure mounting enables better calibration of the positioning of the unit and better data results.

In comparison, OBD-II solutions and OBD-equipped hybrid solutions rely on a telematics device mounted in a permanent position in the vehicle. This provides much more data fidelity from the accelerometers. Overall precision and sensitivity to low-energy impacts offer a level of data useful in assessing accident scenarios. As shown in Figure 5, the data fidelity provides a deeper view into the nature of the accident and a much better picture of what actually happened. This level of data collection can’t be ensured with a smartphone-based solution

– Denise Carth, Insurance Experts’ Forum1

Summary: Data Collection Trade-offs

By all indications, vehicles are quickly advancing beyond their primary role as transportation devices and are now becoming full-featured mobile communication platforms. As a part of this trend, drivers can voluntarily transmit information about their driving behavior—to have their insurance premiums more accurately linked to their behavior—and they can also receive real- time feedback to reinforce positive driving habits and minimize risks during travel. Numerous other benefits result from improved communication, including maintenance reminders, social media interaction, weather and road-condition warnings, accident reconstruction, theft recovery, and more.

At the moment, telematics solutions based on OBD-II are leading the market in terms of sheer numbers. However, for select programs, smartphones are satisfying certain market requirements

1 http://www.insurancenetworking.com/blogs/telematics-auto-insurance-innovation-group-32742-1.html

“ Furthermore, many insurers are beginning to look at telematics and vehicle data for claims

to help assess what happened, who was at fault, damage, and more. By doing so, they are able to

potentially eliminate fraud and make sure the right driver in the accident is paying for the damage.”

Accleration (g)

Long Lat Verticle

-1.2 -1 -0.8 -0.6 -0.4 -0.2 0 0.2

and establishing their own niche. Hybrid solutions are also gaining popularity because of their ability to capture rich vehicle data while offsetting some of the traditional costs of standalone cellular-based OBD options.

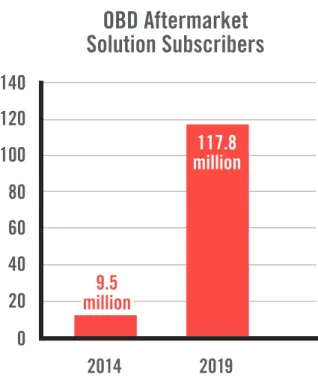

By most indicators, OBD-II devices will still be a dominant presence in the market well beyond 2025. As shown in Figure 6, ABI research predicts there will be 117.8 million subscribers to OBD aftermarket solutions by 2019.

Ultimately, it’s essential to work with an experienced telematics service provider that understands the full range of options and can help you assess the trade-offs in choosing the most appropriate in-vehicle technology to meet the specific segmentation goals of your program. OBD-based options, smartphone options, and hybrid solutions are not necessarily in opposition to each another, but can be complementary in meeting the diverse needs of a comprehensive behavior-based assessment program. Cost savings can be a valuable consideration, but extended capabilities, data quality, and flexibility are important factors as well. OBD-based, smartphone-based, and hybrid telematics solutions have a place in the market, depending on the requirements of the insurers and the preferences and habits of the insured. Strong growth in each of these sectors seems assured.

The trade-offs among smartphones, hybrid, and OBD-II for data collection are largely linked to the overall objectives of a given insurance program and should always be considered in this context.

OBD Aftermarket

Solution Subscribers

2014

2019

100

120

140

40

20

0

60

80

117.8

million

9.5

million

Some factors seem clear-cut on initial analysis, and they reveal greater complexity after more analysis. For example, the inexpensive initial cost (to the insurer) of smartphone data collection can be countered by the long-term trade-offs. In comparison, OBD-II solutions have a higher initial cost (to the insurer), but, since the hardware is fixed and stays in the car, additional costs over the term of the insurance program are less likely. Hybrid solutions provide data accuracy, and opportunities for value-added services, but require greater support by the insurer and more intervention by the policyholder to establish communication and ensure the data collection is taking place as needed.

Geographical considerations are also a factor. Regulatory bodies in the insurance industry set the standards by which a given technology will be accepted or rejected in each region. Legislative and regulatory bodies in some regions prefer one approach over another. For example, in the European market, mobile solutions are less restrictive and fit within the regulatory frameworks in many regions. The US market is still in flux with some states rejecting use of mobile solutions, and others not explicitly supporting mobile solutions yet. Solutions using aftermarket OBD-II devices are supported by insurance regulatory bodies in both the European and US markets.

Choosing a Telematics Partner

The selection of a technology and a strategy to deploy telematics-based UBI can be a fairly complex process—the options are numerous and the technology features required are closely linked to the type of product that the insurer wants to offer. The insurer’s program goals will often determine the optimal hardware platform and software components, so each insurer should have a clear picture of the insurance product at the very beginning of the planning process. If you select solution components before evaluating the capabilities of the product to be offered, you may discover too late that the choice of data collection hardware does not suit the objectives of the program. An experienced telematics partner will be able to provide services and facilitate your project goals supporting whichever combination of technologies you decide on.

Partner integration is an important part of the mix as well, and this factor should be included when making a selection. Look for solutions that are modular and flexible with well-defined interfaces and an automated process for performing machine-to-machine integration. Ideally, the solution infrastructure should integrate data collection from both mobile applications and telematics hardware mounted in-vehicle—favoring simple, straightforward deployments and minimal maintenance. Technologies don’t need to be considered in isolation, but should be evaluated as to how well suited to overall program objectives they are. In many cases, these technologies can be used in complementary ways that strengthen the objectives of the program. For example, an insurer can initiate a customer acquisition/trial program—based on an easy- to-implement smartphone solution to gather data or UBI leads. This trial period can then be upgraded to a more permanent OBD-II or hybrid solution after the trial period ends. Opportunities to integrate smartphone-based solutions with embedded OEM telematics features in automobiles will also increase as these technologies mature and become increasingly available.

Ideally, the selected partner should be able to support a number of different program types without the need to re-engineer any part of the solution. For example, specialized programs might include:

> Programs to support young drivers and encourage teen driver safety

> Customer acquisition/lead generation telematics solutions that offer a free trial period to get started

> Different forms of incentivized UBI packages designed to appeal to different groups, such as seniors, daily commuters, or occasional vehicle users

While this paper has contrasted and compared the capabilities of smartphones, hybrid, and OBD-II solutions, in real-world implementations recent innovative approaches are combining the best ideas from new and emerging technologies to create solutions that meet customer expectations. Knowledgeable TSPs should stay abreast of these developments to be ready to take advantages of the latest technologies when the time is right.

– Telematics Update2

2 http://analysis.telematicsupdate.com/infotainment/connectivity-enables-new-paradigm-auto-mobility

“ There’s still a disconnect between consumer expectations and the reality of automotive telematics.

While consumer awareness of telematics is still relatively low, those drivers who are aware of it expect

higher reliability from automakers than they do from phone makers while expecting connected car

services to be as fully featured as their phones are.

When the auto industry gets this right, the car will take its place as part of the consumer’s digital

lifestyle and the connected society. Cars will be less prone to failures; issues will be addressed more

quickly; and major recalls will be reduced or even avoided. At the same time, cars will work harder

for their drivers. They’ll not only get them where they’re going while avoiding bad traffic conditions,

but they’ll also help them keep in touch with family, friends and co-workers; offer them just-in-time

information; and enable them to take care of little chores while driving.”

About IMS

Intelligent Mechatronic Systems Inc. (IMS) is a leader in connected car technology that enables drivers to be safer, smarter, and greener. The unique approach of converging in-car infotainment, automotive telematics, and data intelligence has resulted in an impressive range of connected car solutions and services. From insurance and government, to fleets and everyday drivers, IMS technology revolutionizes industries.

From early success in developing automotive safety products, IMS is dedicated to vehicle safety and intelligence, evolving beyond vehicle component applications to include industry-leading, award-winning connected vehicle solutions that greatly enhance driver behavior, improve productivity, and make it safer for drivers to acquire and manage critical information efficiently whenever required.

For more information on how you can approach the commercial or personal UBI market with full-featured telematics support and powerful analytical tools, visit www.intellimec.com/ CommercialLinesUBI or www.intellimec.com/usage-based-insurance-telematics.