ORGANIC

ADVANTAGE

Transition to higher profits

Field

crops

1

Organic advantage

Transition to higher profits

Are you a field crop producer looking for a new business opportunity? Whether you grow grain, pulses or oilseeds, there is an opportunity for you to gain a market and business advantage by switching your conventional acres into organic production. No matter where you farm in Canada, making the transition can be easily navigated with support from organic experts.

Opportunities in Canada’s organic sector

The Canadian organic sector has experienced rapid growth for the past decade and is well positioned for continued expansion. To meet growing consumer demand with Canadian supply, however, the sector needs to significantly increase production capacity. Substantial transition of conventionally farmed lands and processing facilities to organic practices is required to supply both the quantity and variety of products that are demanded by consumers in both the domestic and international markets.

This brochure is intended to highlight the business case for organic field crop production. It will provide conventional producers with a better understanding of the market opportunity, economic benefits, investment requirement, marketing possibilities, and available resources and expertise to support a successful transition into the sector.

Market advantage – Consumer demand for organic food products is

outpacing Canadian production capacity.

Business advantage – Field crop producers who transition from

conventional to organic production are rewarded with increased profitability.

Transition advantage – There is a significant knowledge base and

numerous resources available to navigate a smooth transition from

conventional to organic production.

Organic Value Chain Roundtable

The Organic Value Chain Roundtable (OVCRT) is an industry-led partnership working

collaboratively with government on strategies to address regulations, increase Canadian

organic capacity, support development of markets and help guide research and innovation

for Canada’s organic sector. Increasing the organic share of domestic retail sales from 1.7%

to 5% by 2018 is a key strategic priority for the OVCRT. This will be accomplished through

increased production, improved production efficiencies and greater economies of scale.

Photo courtesy of Barnyard Organics in PEIOrganic producers’ input

costs are about half of their

conventional counterparts

There are nearly 5,000 certified

organic farms, processors and

handlers in Canada

North America accounts for 50% of the

global organic demand but only produces

7.5% of the global organic production

For every

$100

earned per acre an

organic farmer keeps

$58

while a

conventional farmer keeps

$31

Demand for organic

has increased 170%

since 2002 in Canada

Canadian organic

food sales are

$2.8 billion

Canadian organic

exports are valued at

$458 million

More than 20 million (60%)

Canadians buy organic

products weekly

ORGANIC CONSUMER 2002

ORGANIC CONSUMER 2013

ORGANIC

ADVANTAGE

50% Demand

7.5% Supply

There is significant room for growth

in organic beef – only 0.4% of the

U.S. cow herd is certified organic

3

Organic producers’ input

costs are about half of their

conventional counterparts

There are nearly 5,000 certified

organic farms, processors and

handlers in Canada

North America accounts for 50% of the

global organic demand but only produces

7.5% of the global organic production

For every

$100

earned per acre an

organic farmer keeps

$58

while a

conventional farmer keeps

$31

Demand for organic

has increased 170%

since 2002 in Canada

Canadian organic

food sales are

$2.8 billion

Canadian organic

exports are valued at

$458 million

More than 20 million (60%)

Canadians buy organic

products weekly

ORGANIC CONSUMER 2002

ORGANIC CONSUMER 2013

ORGANIC

ADVANTAGE

50% Demand

7.5% Supply

There is significant room for growth

in organic beef – only 0.4% of the

U.S. cow herd is certified organic

4

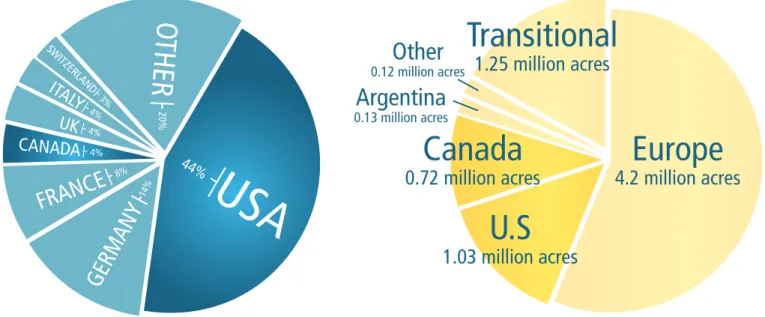

USA

USA

44% 20%GE

RM

AN

Y

OT

HER

14%FRAN

CE

8% CANADA 4% ITALY 4% SW ITZERLA ND 3% UK 4%Global market: Distribution of total retail sales value by country

Source: FiBL-AMI-IFOAM Survey 2013

Figure

2

Market advantage

Strong consumer demand for organic products

Sales of organic food and beverages in Canada increased from $2 billion in 2008 to $3 billion in 2012. Since 2006, the value of the Canadian organic food market has tripled, far exceeding the growth rate of other agri-food sectors. The significant increase in industry value is driven by consumers – more than 58% of Canadians buy organic products on a weekly basis. Many consumers are choosing organic grain-based products because of perceived health benefits, including increased antioxidants.1

On track to triple market share

While organic sales in Canada are growing much faster than food sales in general, they still account for only a 1.7% share of total food sales. In comparison, U.S. organic market share is 5% and Germany’s is 8%. The OVCRT’s goal is to grow the organic share of food sales in Canada to 5% by 2018, tripling its current market share.

There is a significant opportunity for growth in organic breads and grains, a category worth $360 million at retail in Canada. As well, market share for organic grains and cereals in the U.S. has steadily increased over the last decade (see Figure 1), and 36% of U.S. organic food businesses sourced ingredients from Canada in 2012.

Access to 96% of the global organic market

Organic food demand is also on the rise globally. The reduction of trade impediments puts the Canadian organic sector in an ideal position for growth. Canada currently has five equivalency arrangements in place with the United States, Europe, Costa Rica, Japan and Switzerland, and more in development. These arrangements recognize the Canadian organic standard and help facilitate trade. As a result of these arrangements, Canada has access to 96% of the current global organic market, valued at $US63 billion annually.

Building on a solid foundation

An established base of organic production and processing also positions Canada well for growth. The country is home to 3,732 organic farms, 870 organic processors (at least 356 process grain and oilseed) and 245 organic handlers (see Figure 2). These numbers are steadily increasing. Between 2001 and 2011 the Census of Agriculture shows Canadian organic

operations increased by 66.5% and the number of certified organic processors and handlers increased by 194%.

Consumer demand for organic food products is outpacing Canadian production

capacity. This gap in supply and demand offers field crop producers the opportunity to

convert conventional acres to organic and benefit from an untapped market.

Mark

et Adv

antage

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 19 97 19 98 19 99 20 00 20 01 20 02 20 03 20 04 20 05 20 06 20 07 20 08 20 09 20 10 % market shar eChange in Consumer Market Share for Organic Breads and Cereals in the United States from 1997-2010 Figure 1

1. The Organic Center. With the Grain: A closer look at the nutrient quality of grain, grain based products, and the role of organic agriculture. July 2012

Organic Grain Processors in Canada Figure 10

Food processing

212Seed

processing

62 Feed processing 19 Alcohol processing 15Brokers

48 Figure 1Change in Consumer Market Share for Organic Breads and Cereals in the United States from 1997-2010

Source: Organic Trade Association

Figure 2

Organic Grain Processors in Canada

5

Opportunity to expand organic field crop acreage

North America represents nearly half (48%) of the global demand for organic products (see Figure 3).

Currently, however, the continent has approximately 25% of global organic grain and oilseed production acres (see Figure 4).

Established track record in all major regions and crops

Organic acreage is between 0.5% and 1.3% of total acres across the country. There is significant opportunity to increase production on an already solid base of acres. Canada’s organic sector has an established track record on a significant acreage distributed across the country and across the range of major crops grown in each region (see Figure 5). .

USA

USA

44% 20%GE

RM

AN

Y

OT

HER

14%FRAN

CE

8% CANADA 4% ITALY 4% SW ITZERLA ND 3% UK 4%Global market: Distribution of total retail sales value by country

Source: FiBL-AMI-IFOAM Survey 2013

Figure

2

Wheat/

durum

Oats

Barley

Flax

Peas

Soybeans

Lentils

Corn

Rye

Area of selected grain and oilseed crops (Canada, 2012)

Figure 4

205,097 ac 128,495 ac 81,545 ac 66,718 ac 42,008 ac 42,008 ac 29,653 ac 22,239 ac 22,239 acUSA

Organic cereal grain and oilseed production, 2011

Source: 2011 data from IFOAM and FiBL

Figure 3

Europe

4.2 million acres

Transitional

1.25 million acres

U.S

1.03 million acres

Canada

0.72 million acres

Other

0.12 million acresArgentina

0.13 million acresMark

et

Adv

antage

Organic Grain Processors in Canada Figure 10

Food processing

212Seed

processing

62 Feed processing 19 Alcohol processing 15Brokers

48 Figure 3Global Market: Distribution of Total Retail Sales Value by Country

Source: FiBL-AMI-IFOAM Survey 2013

Figure 5

Area of Selected Grain and Oilseed Crops (Canada, 2012)

Source: MAFRD

Figure 4

Organic Cereal and Oilseed Production, 2011

Source: COG and USDA

Figure 2

Organic Grain Processors in Canada

6

Business advantage

Lower costs, increased profitability

Best management practices associated with producing an organic crop can significantly reduce cost of production as compared to a conventional crop. For instance, inputs such as fertilizer and pesticide are not relied upon in this crop production system. In other words, less investment is required per acre to grow an organic crop. As well, between 30% and 50% less energy is required per acre when all sources of energy are accounted for.1

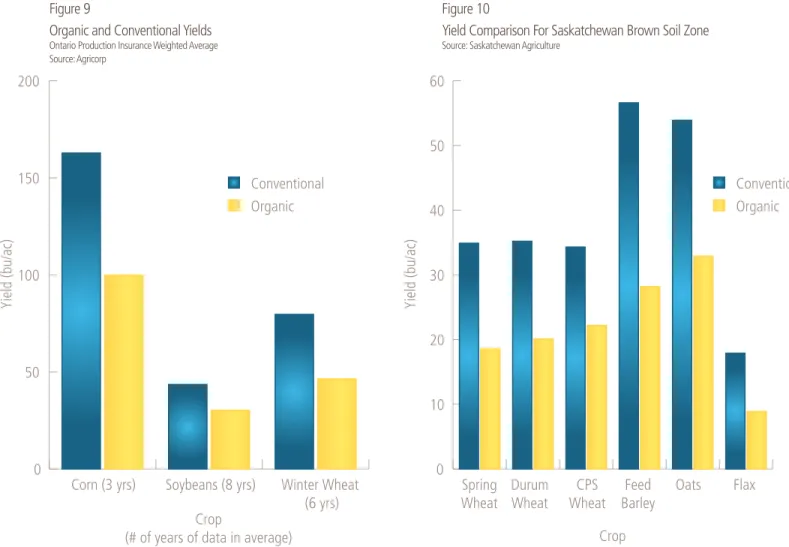

And while yields may be lower than with conventional crops, better prices are offered for organic crops making margins higher (see Figures 6 & 7). When you combine lower costs with price premiums, the result is a healthier bottom line.

The projected returns for 2014 for five crops (i.e. hard spring wheat, durum, oats, barley, flax) in the brown soil zone in Saskatchewan shows:

• Average operating expenses per organic acre were 32% less than conventional production. • Average gross margin per acre was

300% higher in the organic crops. • Maximum gross margin

advantage was 840% (oats) and minimum gross margin advantage was 189% (brown flax).

The projected returns do not factor in the effect of a field being planted to a non-revenue generating green manure crop to build nitrogen and fertility (generally one year in four on prairie soils).

Field crop producers who transition from conventional to organic

production are rewarded with increased profitability.

Business Adv

antage

Soybeans (Food) Soybeans (Feed) Flax $ /b u 10 15 20 25 30 35 40 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Organic Oilseed Prices

Figure 6 Corn HRS Wheat Feed Barley Milling Oats $ /b u 0 5 10 15 20 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Organic Grain Prices

Figure 5Figure 6

Organic Grain Prices

Source: Saskatchewan Agriculture & USDA

Figure 7

Organic Oilseed Prices

Source: Saskatchewan Agriculture & USDA

Figure 8

Comparison of Average Revenue, Expense and Gross Margin for 5 Crops in Brown Soil in SK

Source: Saskatchewan Agriculture 1. Organic Agriculture Centre of Canada and York University. Carbon and Global Warming Potential Footprint of Organic Farming.

Gross Revenue Comparison of Average Revenue, Expense and Gross Margin for 5 Crops in Brown Soil in Sask

Figure 7 Gross Margin Operating Expense Gross Revenue Gross Margin $60.05 $132.26 $189.49 $77.89 Operating Expense $0 $50 $100 $150 $200 $250 Conventional Organic $ per acre

7

Business Adv

antage

Price transparency

Historically, price transparency for organic crops has been challenging. In contrast to conventional marketing, there are no organic Chicago Board of Trade (CBOT) futures contracts. Today, however, organic producers have reliable price information to make good planting and selling decisions. Up-to-date prices for major commodities are now published at the following sites:

• United States Department of Agriculture (USDA) publishes biweekly organic price information: www.ams.usda.gov

• Homestead Organics lists buy and sell prices on its website: www.homesteadorganics.ca/Buy-and-Sell-Grain.aspx

• Mercaris started tracking organic grain prices in fall 2013: www.mercaris.com/weekly_price_reports

• The Manitoba government compiles a monthly organic grain price report: contact Laura.Telford@gov.mb.ca

Setting yield expectations

Organic yields can vary depending on the crop. During the transition from conventional to organic, production yields are lower than conventional levels, but after a three- to five-year transition period, the organic yields typically increase, and increased experience with growing organics helps to optimize yield. Price premiums also tend to compensate for any yield shortfall.

HRS Wheat Feed Barley Miling Oats Yield (bu/ac ) 0 5 10 15 20 25 30 35 2003/ 2002 2004/2003 2005/2004 2006/2005 2007/2006 2008/2007 2010 2012 2013/2014 Prairie Organic Grain Prices

Corn (3 yrs) Soybeans (8 yrs) Winter Wheat (6 yrs)

Figure 5

Organic and Conventional Yields Ontario Production Insurance Weighted Average

Figure 8 0 50 100 150 200 Conventional Organic Crop

(# of years of data in average) HRS Wheat Feed Barley Miling Oats Yield (bu/ac ) 0 5 10 15 20 25 30 35 2003/ 2002 2004/2003 2005/2004 2006/2005 2007/2006 2008/2007 2010 2012 2013/2014 Prairie Organic Grain Prices

Spring Wheat Durum Wheat CPS Wheat Feed Barley Oats Crop Flax Figure 5

Yield Comparison For Saskatchewan Brown Soil Zone

Figure 9 0 10 20 30 40 50 60 Conventional Organic

Business

Adv

antage

Figure 9Organic and Conventional Yields

Ontario Production Insurance Weighted Average Source: Agricorp

Figure 10

Yield Comparison For Saskatchewan Brown Soil Zone

8

Business Adv

antage

Increasing organic crop research

A significant investment in organic research will have an impact on the sector’s profitability, sustainability and competitiveness. The Organic Science Cluster II (OSCII) was announced in 2014 with support of up to $8 million from Agriculture and Agri-Food Canada (AAFC) under its Growing Forward 2 AgriInnovation Program, $2.4 million from industry, and in-kind contributions of $346,000. This follows on the heels of OSCI, which provided $8 million and funded 28 organic research activities and one communication activity.

Managed by the Organic Federation of Canada, and administered by the Organic Agriculture Centre of Canada, OSCII is supported by over 75 contributing partners on 37 research activities. OSCII includes nearly 200 collaborating researchers and institutions across Canada.

OSCII consists of industry-led research and development, and its outcomes are centred on competitiveness, market growth, adaptability and sustainability. This will be accomplished by using innovation to drive ‘ecological intensification’ through the following:

A. Field crops: Optimizing productivity and competitiveness through adaptable systems for field crops

B. Horticultural crops: Advancing the science of vegetable, fruit and novel horticultural crops

C. Crop pests: Innovation in sustainable pest management strategies

D. Livestock: Optimizing animal health and welfare for productivity and quality

E. Value Adding: Adding value to capture markets through innovative processing solutions

OSCII includes a number of examples of innovation that will help the organic crop sector grow and prosper. This includes: breeding for improved cultivars; reduced tillage systems under organic management; use of biological soil amendments to improve plant health; development of new management products and practices for crops pests (insects, diseases and weeds) in field and storage; technological advances in greenhouse production; management targeting optimization of the nutritional value of crops; and utilizing advanced processing techniques to develop value-added products.

OSCII, which continues until March 2018, will help producers capture opportunities by supporting the

development of emerging organic production in Canada that is responding to market demand.

OSCII numbers at a glance

• $10,705,908 total funding

• Over 200 collaborating scientists,

including graduate students

• 36 research institutions/facilities

• 15 AAFC research centres

• 15 university/educational institutions • 6 others

• Over 70 industry partners committed

to cash or in-kind contributions

9

Business Adv

antage

Transition advantage

Strategies for a successful transition

The transition period is 36 months from the last application of a prohibited substance until a certified organic crop can be harvested. This can mean either two or three years of transitional crops between the last conventional crop and the first certified organic crop depending on when during the growing season the prohibited substances were applied. This is the most challenging period in organic production. However, there are effective transition strategies.

While the economics of various crops during transition vary from region to region, one of the best options for maintaining positive returns through this period is a perennial hay crop. Not only does it provide a positive economic return during transition, it also sets the farm up for success in the first years of certified organic production – it builds soil nitrogen levels, assists with weed control, and increases soil biological activity. Another strategy is a gradual transition into organic production, which can offset the transition costs. As current Canadian organic regulations do not require immediate total conversion, a conventional operation can diversify into organic production over time.

Certified organic

Your decision to certify will depend on marketing plans and the crops you produce. Many organic growers sell their crops to buyers or processors that require certification. This process involves contracting with a third-party certifier to provide the official certification that your farm and its products are in compliance with the Canada Organic Regime. The Canadian Food Inspection Agency maintains a list of accredited certifying bodies in Canada at:

www.inspection.gc.ca

Organic agronomics 101

Organic agriculture has the same primary goal as conventional agriculture – create the best possible conditions for a crop to thrive. Much of the knowledge and techniques from conventional agriculture apply. Proper seedbed preparation, timing of seeding, crop monitoring and harvest are all key practices. While well-planned crop rotations are a beneficial management practice in conventional production, they are critical to success in organic production. Using legumes to fix nitrogen is a method of increasing margins in conventional agriculture; it is essential to supplying the nitrogen needs of crops in organic agriculture.

The organic sector is well established in Canada. There is a significant

knowledge base and numerous resources available to navigate a smooth

transition from conventional to organic production.

Transition resources

There are several Canadian resources for helping in the transition from conventional to organic agriculture.

• Ontario Ministry of Agriculture and Food (OMAF) Factsheet: Transition to Organic Crop Production:

www.omafra.gov.on.ca/english/crops/ facts/10-001.pdf

• Saskatchewan Agriculture: Organic Crop Planning Guides (including returns for transition crops):

www.agriculture.gov.sk.ca

• Gaining Ground: Making a Successful Transition to Organic Farming, Canadian Organic Growers, 2005 • Western Canadian Organic Business

Directory: www.organicalberta.org/

business-to-business

Tr

ansition Adv

antage

10

Thinking differently about inputs

In organic agriculture, inputs tend to have longer-term impact – there aren’t any quick fixes. Of the three macronutrients, phosphorus is generally the most challenging to adequately supply under organic cropping systems. However, a

combination of judicious use of phosphorus sources (including animal manure, compost and mineral phosphate) and improved soil biological activity has proven successful. The following chart shows the key sources of organic phosphorus:

Table 1. Available Phosphorus in Organic Fertilizer

Sources Pounds of Fertilizer/acre to provide X pounds of P

2O5 per acre

20 40 60 80 100

Bonemeal 15% P2O5 130 270 400 530 670 Rock Phosphate 30% total P2O5

(X4 because of slow release) 270 530 800 1100 1300

Fish Meal, 6% P2O5 (also contains 9% N) 330 670 1000 1330 1670

Source: Cornell University Cooperative Extension, NYS IPM Publication No. 133. 2013.

It’s important to remember that all inputs have to be approved under organic regulations. A database of approved inputs for organic agriculture is maintained at: www.organicinputs.ca.

Reduced tillage and no-till techniques are also utilized in organic production and research is ongoing in this area.

Increasing organic seed supply

Organic seed breeding trials are being conducted across the country. Funded by the W. Garfield Weston Foundation, USC Canada’s Bauta Family Initiative on Canadian Seed Security is conducting seed trials across the country to determine whether organically adapted seeds perform better in organic systems than conventionally bred seeds.

The organic seed supply in Canada is growing. More than 50% of grain growers reported using 100% organic seed in 2011 and 64% had increased their use of organic seed in the previous three years. Provincial organic associations include lists of organic seed suppliers on their websites.

Planning is key to marketing

As with any crop, it is best to have a plan for marketing it before you plant the seed.

Refer to the Western Canadian Organic Business Directory (www.organicalberta.org/business-to-business) for a list of buyers. During your transition period, you will need to take the opportunity to seek out buyers for your future organic

production. The organic grain handling sector is well established across Canada but requires advance planning on the part of the seller. Many buyers offer forward contracts for post-harvest delivery.

Canadian growers are supplying both domestic and international markets. Complete value chains for many organic crops exist in Canada, including: • Malt barley to organic beer • Flax, canola, camelina, and soybeans to organic oils

• Soybeans to organic tofu • Organic grains to breakfast cereals • Wheat to organic flour and baked goods

Tr

ansition Adv

antage

Success Story

Homestead Organics

Berwick, OntarioHomestead Organics celebrated 25 years in business in 2013. The journey began in the mid-1980s when Murray and Carrie Manley went organic ‘cold turkey’ on 400 acres, producing their first certified organic crops in 1988.

In 1997, the family business was re-organized with Murray and Carrie keeping the land and their son Tom and his wife Isabelle taking over the processing. That year, Homestead Organics was moved to an old abandoned feed mill in Berwick. The mill was re-tooled and it received 500 tonnes in its first year. The business grew every year, with new grain bins, more equipment, extra staff and expanding markets.

Today, Homestead Organics employs 14 people serving hundreds of farmers, with $1 million in infrastructure, offering multiple products and services to organic farmers from Ontario to Nova Scotia. It handles over 7,500 tonnes of grains annually in feed manufacturing, precision cleaning of grains for food markets, seed and brokering. In late 2013, Homestead Organics announced the purchase of a property in Morrisburg with a 27,000 square foot building on 2.2 acres. The site represents the next step in the growth of Homestead Organics.

11

Tr

ansition Adv

antage

Tr

ansition Adv

antage

Insuring your high-value organic crop

Organic producers in Saskatchewan, Manitoba and Ontario have the same ability to insure their crops against weather perils as conventional growers for most major crops. The list of crops covered under provincial AgriInsurance

programs is growing.

Crop

Saskatchewan

Manitoba Ontario

Wheat CPS x x Extra Strong x x Hard Red x x Hard White x x Durum x x Feed x Winter x x x Khorasan/Kamut x Barley x Oats x x Flax x x

Other crops insured under an organic plan

Canary Seed, Canola, Faba Beans, Field Peas,

Lentils (large green, red, other), Mustard (brown, oriental,

yellow), Rye (fall, spring), Sunflowers,Triticale

Corn, Soybeans,

Spelt

For more information on insurance programs specific to your province: • Saskatchewan: www.saskcropinsurance.com

• Manitoba: www.masc.mb.ca/masc.nsf/program_organic.html

• Ontario: www.agricorp.com/SiteCollectionDocuments/ PI-Guide-Organics-en.pdf

It’s time to grow organic

Consider switching your conventional field crop

acres to organic and gain several advantages:

Market advantage – Tap into a market with

outstanding potential.

Business advantage – Get rewarded with lower

expenses, price premiums and increased profitability.

Transition advantage – Gain knowledge from

numerous resources for a smooth transition.

Success Story

Farmer Direct Co-op

Regina, Saskatchewan

Farmer Direct Co-op (FDC) started in sum-mer 2002 with three organic family farms and a handful of sales. Now FDC has 66 organic family farm members with sales in excess of $5 million per year and 7,000 metric tonnes of grain shipped annually. In 2012, FDC launched the FDC brand of retail bulk bin grains, oilseeds, pulses and value-added products in western Canada and the Pacific Northwest. Products in-cluded flaxseeds, lentils, beans, split peas, hulled hempseed and rolled oats. In May 2013, the FDC brand launched nationally in the U.S. with Whole Foods Market. In FDC’s current fiscal year, sales of the FDC brand are forecast to represent 30% of total sales of over $6 million.

Demand for FDC products is driven by organic consumers wanting their pur-chases to support family farms, organics and fair trade. With FDC they don’t have to choose, they can support all three with one purchase. Farmer Direct Co-op is the first brand in North America to be certi-fied to domestic fair trade standards and the only brand that can claim all three attributes of 100% farmer ownership, 100% domestic fair trade and 100% organic. Future plans include consumer packaged goods and developing further joint ventures with toll processors and organic food manufacturers.

Agri-Insurance is a Growing Forward 2 Federal/Provincial/Territory Business Risk Management Program www.agr.gc.ca. Information on other programs and services are available on AAFC’s website at: www.agr.gc.ca/eng/programs-and-services

12

To start your transition to higher profits,

contact one of the following organizations for more information on organic crop production:

National

Agriculture and Agri-Food Canada

(AAFC) 1-855-773-0241 info@agr.gc.ca www.agr.gc.ca/organic

Canadian Organic Growers (COG)

1-888-375-7383 office@cog.ca www.cog.ca

Canada Organic Trade Association (COTA)

East: 613-482-1717 West: 250-335-3423 otacanada@ota.com www.ota.com

Organic Agriculture Centre of Canada (OACC)

902-893-7256 oacc@dal.ca www.oacc.info

British Columbia

Certified Organic Associations of B.C. (COABC)

250-260-4429

office@certifiedorganic.bc.ca www.certifiedorganic.bc.ca

British Columbia Ministry of Agriculture (BCMAGRI)

Susan Smith, Industry Specialist, Vegetables and Organics

604-556-3087 Susan.L.Smith@gov.bc.ca www.agf.gov.bc.ca/organics

Alberta

Organic Alberta 1-855-521-2400 info@organicalberta.org www.organicalberta.orgAlberta Agriculture and Rural Development

Keri Sharpe, Organic Business Development Specialist 403-556-4218

keri.sharpe@gov.ab.ca

Saskatchewan

Saskatchewan Organic Directorate

Marla Carlson, Administrator 306-535-2710

admin@saskorganic.com

Organic Connections

Marion McBride, Coordinator 306-543-8732

b.mcbride@sasktel.net

Saskatchewan Agriculture

Chantal Jacobs,

Provincial Specialist: Alternative Cropping Systems

306-798-0945

chantal.jacobs@gov.sk.ca

Manitoba

Manitoba Organic Alliance (MOA)

(204) 546-2099

info@manitobaorganicalliance.com www.manitobaorganicalliance.com

Manitoba Agriculture, Food and Rural Development (MAFRD)

Laura Telford, Business Development Specialist, Organic Marketing 204-871-6600

Laura.Telford@gov.mb.ca

Tr

ansition Adv

13

Tr

ansition Adv

antage

Ontario

Organic Council of Ontario (OCO)

519-827-1221

info@organiccouncil.ca www.organiccouncil.ca

Ecological Farmers of Ontario (EFAO)

1-877-822-8606 info@efao.ca www.efao.ca

Ontario Ministry of Agriculture and Food (OMAF)

Agriculture Development Branch 519-826-4587

www.ontario.ca/organic

Québec

L’Union des producteurs agricoles (UPA)

450-679-0530 upa@upa.qc.ca www.upa.qc.ca

La Filière biologique du Québec

418-838-4747 info@filierebio.qc.ca www.filierebio.qc.ca

Le ministère de l’Agriculture, des Pêcheries et de l’Atimentation du Québec (MAPAQ)

Nicolas Turgeon, Organic Consultant 418-380-2100, ex 3801

nicolas.turgeon@mapaq.gouv.qc.ca

New Brunswick

Atlantic Canadian Organic Regional Network (ACORN)

1-866-32-ACORN admin@acornorganic.org www.acornorganic.org

New Brunswick Department of Agriculture Fisheries and Aquaculture

Claude Berthélémé, Organic Production Specialist

506 453-3046

claude.bertheleme@gnb.ca

Prince Edward Island

Atlantic Canadian Organic Regional Network (ACORN)

1-866-32-ACORN admin@acornorganic.org www.acornorganic.org

PEI Certified Organic Producers Co-Operative (PEI COPC)

902-894-9999 www.organicpei.com

PEI Department of Agriculture and Forestry

Susan MacKinnon, Organic Development Officer 902-314-0825

sdmackinnon@gov.pe.ca

Nova Scotia

Atlantic Canadian Organic Regional Network (ACORN)

1-866-32-ACORN admin@acornorganic.org www.acornorganic.org

Perennia Food & Agriculture Inc.

Av Singh, Organic & Rural Infrastructure Specialist 902-896-0277, ex 228 asingh@perennia.ca www.perennia.ca

Newfoundland and Labrador

Atlantic Canadian Organic Regional Network (ACORN)

1-866-32-ACORN admin@acornorganic.org www.acornorganic.org

Newfoundland Department of Natural Resources, Agrifoods Development Branch

Jane White, Industry Development Officer (Crops)

709-729-6867 janewhite@gov.nl.ca