Relationship marketing and CRM:

a financial services case study

SALLY DIBB AND MAUREEN MEADOWS

Warwick Business School, University of Warwick, Coventry CV4 7AL, UK

This paper considers the shift towards relationship marketing principles and the imple-mentation of CRM in the retail financial services sector. Many players offering personal banking and related products have now ‘bought in’ to the concepts behind relationship marketing, and are investing heavily (particularly in new information technology) to enhance customer relationships and improve retention rates. This trend is considered from the perspective of an organisation that is one of those leading the change. An in-depth case study reveals the progress made in recent years towards the company’s goals, focusing especially on the introduction of new systems and moves to enhance customer data. However, the analysis also suggests that major challenges remain if the benefits of CRM are to be fully realised. Issues involving the structure of the organisation and its approach to a range of staff issues such as recruitment and training are of particular concerns for the implementation of CRM principles.

KEYWORDS: Relationship marketing; services marketing; customer relationship management; financial services; case study

INTRODUCTION

This paper considers the shift towards relationship marketing principles and the implementation of CRM in the retail financial services sector. While other industries may have been quicker to adopt CRM ideas, many players offering personal banking and related products have now ‘bought in’ to the concepts behind relationship marketing and are investing heavily to enhance customer relationships and improve retention rates. This trend is considered from the perspec- tive of an organisation that has been one of those leading the change. An in-depth case study reveals the progress that the organisation has made towards its goals, and the challenges the business still faces if the benefits of CRM are to be fully realised.

The paper describes the application of relationship marketing in UK financial services by examining an organisation at the forefront of CRM thinking and implementation. The analysis is framed around a model of relationship marketing in the financial services sector developed by Dibb and Meadows in 2001. This model assesses the degree to which businesses are relationship marketing-oriented, based on a continuous scale from a low to high relationship marketing focus. In this paper it is suggested that the model can also be used to understand the progress which financial services companies have made towards CRM. This is achieved by applying the model using an extended case study to a business that is engaged in an ongoing organisation- wide exercise to implement CRM principles.

Journal of Strategic Marketing ISSN 0965–254X print/ISSN 1466–4488 online © 2004 Taylor & Francis Ltd http://www.tandf.co.uk/journals DOI: 10.1080/0965254042000215177 Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

The paper begins by reviewing the literature on relationship marketing and CRM. The methodology for the current research is then described and the results of the case study analysis are presented and discussed. Finally, conclusions are drawn about the progress made by financial services institutions towards the implementation of CRM and the difficulties that may lie ahead.

LITERATURE REVIEW

This review examines the theoretical basis for the shift towards a relationship marketing perspec- tive in the financial services industry (Buttle, 1996). The underlying principles of relationship marketing are explored and its linkages with CRM considered. Pivotal questions about the extent to which financial services companies have progressed towards a relationship marketing approach and whether the purported benefits are being achieved are raised.

Building relationships with customers helps marketers to better understand and satisfy custom- ers, objectives which are central to the marketing concept (Kotler, 2000; Reichheld and Sasser, 1990; Reichheld, 1993). The recent shift away from the transaction-based view of marketing has focused attention on the beneficial effects of managing customer relationships (Gronroos, 1989; Howcroft and Durkin, 2000). Many businesses now believe that long-term success is contingent upon customer retention as well as customer acquisition. By developing customer loyalty it seems that a steady stream of sales can be achieved from existing customers over the lifetime of their relationships with the company. This notion is especially pertinent in financial services, where the combination of product complexity and intangibility has tended to emphasise the importance of the relationship with the service provider (Berry, 1996; Meadows and Dibb, 1998; Spekman, 1988).

These principles are central to relationship marketing (RM) theory which focuses on buyer- seller interaction (Berry, 1995) and assumes that relationship longevity and business profitability are linked (Reichheld, 1993). The objective is to use the buyer-seller interaction to develop a marketing and service offer that assists customer acquisition and retention (Berry, 1983; Gronroos, 1994; Storbacka, 1997).

The roots of relationship marketing have been traced to services marketing, quality manage- ment and the network approach to business marketing (Gummesson, 1999; Edvardsson, Thomasson and Ovretveit, 1994; Hakansson, 1982). Moller and Halinen (2000), for example, identify inputs from four distinct theoretical areas: business marketing, services marketing, marketing channels, and direct/database marketing (see Table 1).

The underlying reasons for the current interest in relationship marketing are especially relevant to the financial services context. First, services marketing has matured and continues to grow in importance (Berry, 1995; Gummesson, 1999). The relative intangibility of the products has emphasised the need to build differential advantage through improved service quality (Perrien and Ricard, 1995). Second, as deregulation has heightened competitiveness in the financial services sector, relationship marketing’s ability to protect the customer base has come to the fore (Reichheld and Sasser, 1990; Turnbull and Valla, 1990). Third, there are clear customer benefits linked to a relationship marketing approach. By engaging with suppliers in a kind of ‘learning relationship’ (Peppers and Rogers, 1993, 1999), customers are more likely to be able to achieve suitable service delivery. This is a key consideration in a sector which is increasingly orientated to the life-time value of the customer. Finally, rapid and far-reaching technological change is improving businesses’ understanding of customers’ needs and buying behaviour. For financial services companies which have been at the forefront of implementing data capture and management systems, these insights enable the delivery of more tailored product and service offerings (Zielinski, 1994). Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

TABLE 1. The theoretical origins of relationship marketing

Developments in IT have also driven the adoption of customer relationship management (CRM). Despite the new terminology which is widely adopted across different sectors, CRM is simply a fresh perspective on relationship marketing ideas. Like relationship marketing, the costs of customer acquisition and desirability of customer retention are key features of CRM (Roberts, 2000; Zeithaml, 2000). However, the CRM perspective is particularly concerned with the impact of direct and database marketing on an organisation’s ability to create and build linkages with its customer base. CRM exponents explain that combining superior customer information and commitment to long-term relationships allows businesses to provide more tailored offerings. As a result, the concepts of the segment of one (or one-to-one) and mass customisation have come to the fore. As Chaffey et al., (2000, pp. 290–91) explain:

Relationship marketing theory provides the conceptual underpinning of one-to-one marketing since it emphasises enhanced customer service through knowledge of the customer, and deals with markets segmented to the level of the individual. Direct marketing provides the tactics that deliver the marketing communications and sometimes the product itself to the individual customers. Database marketing provides the technological enabler, allowing vast quantities of customer-related data to be stored and accessed in ways that create strategic and tactical marketing opportunities.

CRM is therefore a ‘new-old’ concept that is inextricably connected with more traditional relationship marketing principles. One implication of this connection is that it ought to be possible to adapt theoretical frameworks developed to explain different levels of relationship marketing as tools for measuring progress in CRM. This is the approach adopted in this paper, where a framework designed initially to assess relationship marketing is modified for CRM.

In the financial services sector the use of technology to implement CRM and enhance customer relationships has never been greater (Thurston, 2000; Sievewright, 2001). The connection between relationship marketing and business performance in the sector has already been demonstrated (Speed and Smith, 1993). The importance of investing in the ‘life time

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

1. Business marketing—the interaction and network approach (Ford, 1997; Hakansson and Snehota, 1995; Moller and Wilson, 1995). The approach examines the relationships built and resources exchanged between different actors (e.g., organisations and individuals). The evolution and functioning of relationships at the individual, dyadic and network level are of interest. A particular concern is the role of transactions as episodes in long-term relationships. 2. Services marketing (Bateson, 1995; Berry and Parasuraman, 1993; Gronroos, 1994; Parasuraman,

Zeithaml and Berry, 1985). This area is concerned with explaining, understanding and improving the efficiency of services management and services marketing relationships. Pertinent issues relate to the provision of service quality and customer value.

3. Marketing channels (Bogelund and Skytte, 1997; Moller, 1994; Joshi, 1995). The theoretical objective is to explain governance, relationships and balance of power between parties within the context of the channel. The normative objective is to identify more efficient relationships between parties, with a focus on structure rather than process.

4. Direct/database marketing (Peppers and Rogers, 1997; Shepard, 1995; Shaw and Stone, 1988). The approach is concerned with improving efficiency by targeting marketing activities more efficiently. Particular areas of concern relate to customer retention and loyalty, providing customer value and maximising customer lifetime value.

value’ of the customer has also been shown through studies examining the economic case for customer retention. Reichheld and Kenny (1990), for example, show that a small improvement in customer retention rates leads to higher margins, while Mitchell (1995) indicates that a 300% increase in customer profits can be achieved through a five-year extension to customer life cycles.

Despite these encouraging statistics, businesses seeking the benefits of a relationship approach face considerable challenges (Dibb and Meadows, 2001; Perrien and Ricard, 1995). The organisation’s structure may be insufficiently decentralised to encourage a relationship approach and too inflexible to adapt. The firm’s understanding of the customer base and/or technological resource for managing the information may be inadequate. Policies for managing human resources may impede the recruitment and training of suitable staff. The implication of these difficulties is that different organisations are implementing a relationship approach to varying degrees and with differing effectiveness.

Various frameworks have been developed to represent the different levels of relationship marketing which businesses have achieved. Some of these classification schemes compare traditional and interactive marketing approaches, relating marketing changes to developments in technology (Coviello, Brodie and Munro, 1997; Coviello, Milley and Marcolin, 2001; Day, 1998; and Iacoabucci and Hibbard, 1999). Dwyer, Schurr and Oh’s (1987) stepwise approach has five stages: awareness, exploration, expansion, commitment and dissolution. Kotler’s (1992) model, which proposes five levels of relationship marketing, is similar: basic, reactive, accountability, proactive and partnership. This latter model was adapted for the financial services sector by Dibb and Meadows (2001), who used it to review UK high street banks’ progress towards the relationship approach. Kotler’s (1992) model was chosen by Dibb and Meadows because it facilitated a detailed review of the seller and customer relationships at the heart of RM and CRM.

Dibb and Meadows’ (2001) examination of the state of relationship marketing in retail finan- cial services emphasised the need for relationship marketing models specific to the sector. They argued that generic models fail to reflect the diversity of relationship marketing sophistication exhibited by UK financial services companies or the routes taken to achieve it. Instead, Dibb and Meadows (2001) group companies according to whether they exhibit low or high RM focus in four areas: company, customers, technology and staff (see Table 2). In this research, two of these areas have been described as ‘softer’ (the company and its staff), while the other two are described as ‘harder’ areas (technology, and the customer perspective). This terminology is reflected in the analysis and discussion of the case material.

According to the scheme, ‘Type A’ businesses tend to offer typical service interactions while ‘Type B’ businesses have a more strategic commitment to relationship marketing. ‘Type B’ businesses are further divided into three sub-categories, according to their progress along a continuous scale towards a high relationship marketing focus. The first sub-category is quick fix, where businesses attempt to realign existing practices to place more emphasis on relationship marketing. The second is radical fix, where more substantive changes are made to existing practices, often linked with significant investment in staff and/or technology. The third and final sub-category is strategic set-up, which applies primarily to new operations with a belief in the one-to-one future.

This framework is used as the basis for the case study reviewed in this paper. The semi-structured interviews used to collect the data were structured around the issues described in Table 2. Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

TABLE 2. Research framework: characteristics of a high and low relationship marketing focus

Low RM focus High RM focus

Company: Company:

More likely to use traditional distribution channels More likely to use new distribution

channels

Stated desire for RM Believe in one-to-one future Develop high relationship products Believe better relationships lead to competitive advantage

Customer-driven and event-led marketing

No stated desire for RM

Not convinced about one-to-one future

Focus on customer groups rather than the individual Transaction driven marketing

Staff:

Rewards for new accounts Staff: Emphasis is on excellent communication

with customers to ‘connect’ and spot opportunities

Empowered, self-managed staff who can make quick decisions for customers Reward customer retention, not just new accounts

Most decision-making authority does not rest

with front-line staff

Pay structures may lack incentives or be transaction based

Technology: Technology:

Primary role of information is to record transactions Information is powerful and vital to

strategy

Highly integrated systems and processes Computer screens shared with customers Full access to customer information when dealing with enquiries

Focus on rich attitudinal/buying behaviour data used to identify ‘life events’

Databases used for contact management purposes

All dealings with customer logged allowing continuity between each transaction

Customer contacts used as market research opportunity

Systems often not very well integrated

Account driven rather than customer driven systems Front-line staff only have access to simple profile of customers with little attitudinal data

Some are starting to think about customer emphasis in their systems

Systems may not have ability to identify ‘lifeevents’

Information used to mail customers with literature

Direct mail often handled remotely from front-line

staff with little co-ordination

Customers: Customers:

Emphasis on the value to be achieved from

customers today through the sale of an additional product

Contact with company instigated by the customer

Emphasis on current and potential value of customers, with lifetime value focus

Relationship achieved through integrating

technology and the human face Focus on easy, regular contacts with customers

Use contact to regularly update systems Anticipate needs through events-based marketing

Use contact to conduct transactions and sell

additional products

Collection of customer information often carried out remotely

Adapted from Dibb and Meadows, 2001.

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

METHODOLOGY

This paper applies the model outlined to a case study of a financial services company with a publicly stated commitment to relationship marketing and to implementing CRM. Adopting a case study approach allowed a detailed understanding of the organisation and the issues facing it to be achieved. The case study approach has been widely used by researchers seeking such an understanding of complex phenomena (Yin, 2003). For example, Crittenden and Wilson (2002) have used a qualitative case-based methodology based on personal interviews and archive data to explore success factors in non-store retailing.

The case study in this paper, which is based on a UK building society, uses a combination of personal observation, interviews and secondary data (Blaxter, Hughes and Tight, 1996). A case study approach was particularly appropriate here because a detailed understanding of the application of relationship marketing was needed. In addition, Yin (2003, p. 5) argues that the case study method is suitable when the following conditions are met:

1. The form of the research question is ‘how?’ and/or ‘why?’ This condition is clearly met in the research described here, as the issues of concern are around how and why the approaches of relationship marketing and CRM are being applied in financial services organisations, why barriers to progress are being encountered, how these are being overcome, and so on.

Behavioural control of events is not required. The current research meets this criterion, as the researchers were not part of the decision-making process within the organisation being studied.

The research focuses on contemporary events. Again, there is a good fit with the study described here, as the decisions and actions under discussion had either occurred very shortly before the research intervention or, in some areas, were still unfolding at the time of the research.

2. 3.

The rationale for a single case design is similarly well supported in this context. First, the company was chosen because of its publicly stated commitment to RM, and its aim to position itself ‘at the cutting edge’ of CRM. Yin (2003, pp. 40–2) describes critical cases, extreme or

unique cases, and revelatory cases as worthy of documentation and analysis in their own right, as provid- ing opportunities crucial for testing theories and models under development, and as situations for observing and analysing phenomena that are normally inaccessible. In addition, this analysis is one element of a longitudinal case (Yin, 2003, p. 42), with the researchers gaining access to the case company, and observing its ‘journey’ towards CRM, over an extended time period.

The data used in the case study were obtained from a combination of secondary and primary sources. The secondary data included internal documentation from the case company and a selection of general reports on the financial services industry. Primary data gathering followed, involving semi-structured interviews with senior managers from the case organisation. The interviewees were selected on the basis of their experience and involvement in relationship marketing and related issues. Table 2 was used as a checklist to guide the semi-structured interviews. Interviewees were invited to discuss the position of the case company on each of the dimensions shown. Precise measurements on a quantitative scale were not deemed to be appropriate at this stage of the research programme. Instead, the aim was to use the notion of low to high RM focus proposed by Dibb and Meadows (2001).

The case study analysis is organised around the four areas described in Table 2 in the following order: company, staff, technology and customers. This approach means that the

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

analysis begins by explaining the context of the company as whole before addressing its staff (the two ‘soft’ areas), then moving on to consider the two ‘harder’ areas of technology and customer data.

In order to protect the identity of the organisation, the company’s name and certain other details have been changed. The aim of the case study is to describe the strategies and plans that are being adopted by the business from the perspective of the personnel involved. The opinions of these interviewees are expressed in the ‘Case Study Analysis’ section of the paper. These views are then synthesised and discussed in relation to the Dibb and Meadows (2001) model.

CASE STUDY ANALYSIS

Bsoc is one of the largest mutual building societies in the UK with a history stretching back around 150 years. With assets totalling £15 billion and more than two million members, Bsoc has around 200 branches spread widely across the UK.

Company

Bsoc has an energetic Customer Relationship Management (CRM) team which sits between the Corporate Planning team and the Marketing team. The CRM team has responsibility for the customer databases (see below) and carries out customer data analysis. This analysis leads to an increased understanding of customer profitability, segmentation of the customer base and other important issues. The result is that the CRM team is involved in Bsoc’s marketing planning and targeting and has substantial inputs to the corporate plan and strategic issues. It is clear that this organisational structure could create practical day-to-day problems if effective co-ordination between the teams is not a priority. For example, sharing of data is needed with the Marketing team which retains control of advertising, branding and product design. Strong linkages with the Corporate Planning team and the Marketing team are therefore crucial if Bsoc is to pursue its strategic goals in a well co-ordinated manner.

Bsoc is currently broadening the range of distribution channels that it offers to its customers. For instance, significant investment has been made in telesales. Web-based projects are also under development, but it seems that Bsoc has been slower than many other players in the industry to establish itself on the Internet.

Staff

Bsoc has a number of staff related issues to consider including training, recruitment and incentive schemes. The CRM programme has involved the company in a range of CRM- related training initiatives involving all staff with direct customer contact roles. Levels of training for branch and call centre staff have been increased so that new working practices associated with the new computer systems can be established. Bsoc sees this as a sizeable and difficult challenge to implement which will be ongoing for some time.

Bsoc does not have a centrally directed staff employment programme. The traditional approach to recruitment has allowed branch managers considerable freedom over who is recruited. The view is that these managers are able to use their local knowledge to tailor recruit- ment and how jobs are advertised to suit local media and the needs of their branch. This empowerment of branch managers also extends to some locally targeted marketing activity, with managers given access to customer data and discretionary budgets.

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

Staff targets and incentives have historically been based on product-based sales targets and on customer retention. Interviewees expressed two concerns about the schemes which are currently in place. The first relates to whether the levels of bonuses are sufficient to change staff behaviour. The second concerns whether the schemes need to be reviewed to reflect the Bsoc’s CRM initiatives. In other words there is a view that the current schemes may not be the most appropriate given Bsoc’s interest in customer lifetime value.

Technology

The CRM team sponsors a range of new technology projects. A major exercise was recently undertaken to clean up Bsoc’s customer data and set up a new database. The new systems allow Bsoc to merge data across their product range and create a detailed overview of each customer relationship. Significant efforts invested in data modelling are also increasing Bsoc’s understand- ing of its customers. Individuals with certain profiles on the database can now be pinpointed and targeted with relevant direct marketing.

In branches, screen prompts have been created that encourage staff to cross-sell new products to existing customers. The same mechanism informs staff about any direct mail which customers have recently received. Branch staff now have access to a complete, up-to-date picture of each customer’s business. Staff performance (for instance, in cross-selling in response to screen prompts) can also be monitored through the system. Cross-sales of new products to existing customers have doubled since the introduction of the new systems. Maintaining this progress in an Internet banking environment is a challenge which Bsoc might face in the future.

Customers

A loyalty scheme is in place to reward customers according to the length of their relationship with Bsoc, the number of products held and the monetary sums involved. The scheme, which is believed to be unique among Bsoc’s competitors, helps the business to retain and build in-depth relationships with customers. It may also help Bsoc to retain its mutual status as it gives customers a greater sense of involvement and demonstrates the tangible benefits of mutuality.

Bsoc operates a customer segmentation approach which is critical to its medium and long term planning. The segmentation is based on the estimated present and future value of custom- ers, as well as the length and depth of the customer relationship. Profitability data helps Bsoc to decide where future resources should be focused. It also highlights customer behaviour, such as movements between segments.

Picture portraits of each segment have been developed to help staff more easily relate to the segmentation. The CRM team is aware that the segmentation may need updating as customers make greater use of new delivery channels. Although Bsoc has not regarded Internet banking as a strategic priority, a fresh look at customer segmentation will be required if its pilot projects in this area are rolled out.

DISCUSSION

This section reviews the company, staff, technology and customer evidence for Bsoc and con- siders the organisation’s progress towards a relationship marketing focus. As the literature review has established, a number of barriers can impede the process (Dibb and Meadows, 2001; Perrien and Ricard, 1995). These relate to the organisation’s structure, its understanding of the customer

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

base, the technological resource at its disposal and human resource policies for recruitment and training.

Like other organisations striving to implement relationship marketing, Bsoc must deal effectively with these issues if progress is to be made. Overall, the company has been helped by the fact that it is large enough to devote the required technological resource but small enough to ensure that implementation is manageable. Bsoc is also aided by its mutual status which drives members’ loyalty and encourages ‘closeness’ between both parties. However, some aspects of implementation, particularly those associated with ‘softer’ issues such as people and organisational structure, have been more difficult to handle. The progress that Bsoc has made is therefore not consistent across each of the company, staff, technology and customer areas.

Judging Bsoc’s overall progress involves reviewing the discrepancies in progress across the ‘softer’ and ‘harder’ areas. The discussion therefore commences by considering the ‘softer’ issues relating to the company and its staff where some serious implementation problems remain. As will become apparent, greater steps have so far been taken with the ‘harder’ areas of technology and

customer data. In order to progress its relationship marketing and CRM goals Bsoc must continue to address concerns in the ‘softer’ areas.

‘Softer’ areas: the company and its staff

The importance that Bsoc attaches to relationship marketing is reflected by the powerful role of CRM within the business. The CRM function uses its rich data sources to drive marketing strategy and planning. However, it is less clear to what extent the belief in one-to-one and relationship marketing prevails at all levels in the organisation. For the underlying principles to permeate the entire company it will be necessary for all departments to adopt a consistent approach. Yet there is evidence that a lack of interfunctional co-ordination, primarily between CRM and marketing, is causing problems. The relationship between these functions is crucial if the one-to-one future is to be reflected in the brand. However, at the present time the market- ing programmes being devised by the marketing function do not always reflect the relationship marketing message and may be a poor fit with the company’s stated strategy.

In the staff area, Bsoc has been considering a range of recruitment and training issues. A particular focus has been the training of branch staff to use the new computer systems. Although this initiative is ongoing and its success cannot yet be judged, an outcome is that training levels are receiving greater emphasis. Once finalised, the new systems will allow the performance of individual staff to be tracked so that further training needs can be assessed. The implementation of the CRM initiative may have implications for staff recruitment, which currently is primarily handled by branch managers. The absence of a centrally driven recruitment policy may become problematic if decisions are made to empower staff further. In such circumstances Bsoc would need to ensure that new recruits have the appropriate personal skills to cope.

Staff incentive schemes have not yet been modified to reflect relationship marketing prin- ciples. Current reward schemes are based on product targets rather than on customer lifetime value. If Bsoc is serious about relationship marketing and the one-to-one future, it must press ahead with its review of incentive packages so that customer lifetime value becomes the focus.

‘Harder’ areas: technology and customer data

The ‘harder’ areas that must be addressed relate to technology and the handling of customer data. Bsoc has responded effectively to the need for investment in these areas, with considerable

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

resource being ploughed into technology developments. The role of information in planning and the need for clean data and fully integrated, customer-facing systems are clearly recognised by the company.

Bsoc’s commitment has ensured that an excellent mix of attitudinal/buying behaviour data is available and sophisticated data modelling is possible. For those dealing with customers, either through the branch network or over the telephone, access to data is better than ever. The new systems have resulted in fuller customer records containing details of all interactions with customers. This greatly assists the process of cross-selling and also allows customer records to be updated whenever contact is made.

The implementation of the new systems is still underway. The effectiveness of these improve- ments in the integration of technology and the human face is dependent upon the success of the training programme for branch staff. From a customer data perspective there is no doubt that Bsoc has made substantive inroads towards a relationship marketing approach. The current and potential value of customers is strongly emphasised and has been used as the basis for the segmentation approach underlying Bsoc’s strategy. This approach, which involves the company in anticipating customer needs, is consistent with relationship marketing principles.

Bsoc’s technological commitment means that customer relationship marketing principles can be used to implement the tactics associated with this strategy. In other words, Bsoc is using its high quality customer data to anticipate and respond to needs on a one-to-one basis. Ultimately the key to success lies in Bsoc’s ability to implement the approach at all levels in the organisation.

The literature indicates that overly centralised or inflexible organisations may find it difficult to adapt to a relationship marketing approach. There is no doubting Bsoc’s desire to invest in relationship marketing. The company believes that better customer relationships lead to competitive advantage. This is demonstrated by Bsoc’s commitment to its sophisticated and well-established customer loyalty programme. The company’s belief in the one-to-one future is being supported by substantial investment devoted to implementing the required technology and processes. These investments are helping the company move towards a more customer- driven and event-led marketing approach.

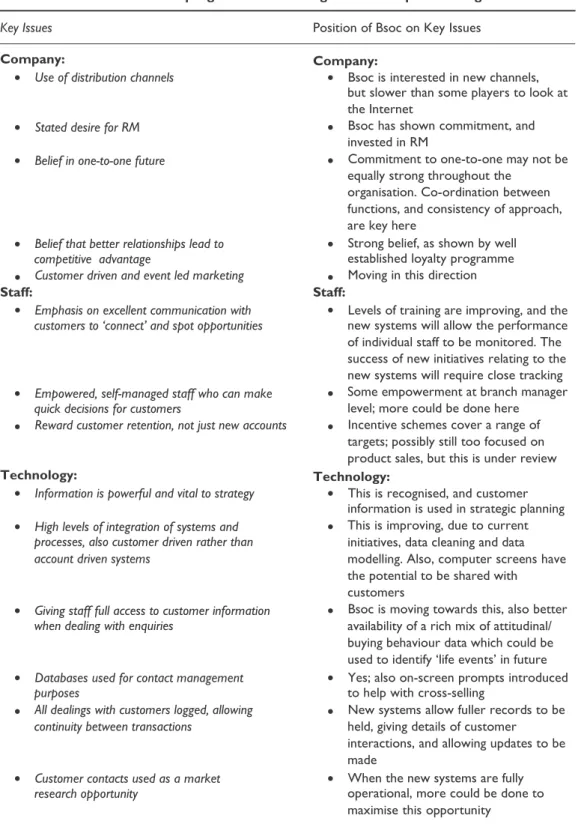

Where is Bsoc now?

As Table 3 illustrates, Bsoc is achieving a high relationship marketing focus in terms of ‘harder’ issues (technology and customers), but still needs to make progress with the ‘softer’ issues (com- pany and staff). Change management literature notes that these softer areas are often the most problematic but that they are also crucial to overall project success. For example, Blennerhassett and Galvin (1993) describe the 1980s IT industry as being focused on technology first and people second, before recognising that any technological solution must recognise the people dimension. Similarly, Peppard and Rowland (1995, p. 99) observe that ‘processes can only perform as well as the people who operate them’. Obeng and Crainer (1994, p. 6) argue that BPR type projects fail because of their focus on ‘hard’ issues such as processes and systems; ‘the “soft” issues—people, skills, behaviour, culture and values—are at least as critical, often more so, but have tended to be relegated in importance’.

In terms of the Dibb and Meadows’ (2001) classification of financial services providers Bsoc is a ‘Type B’ business, because it is demonstrating a strategic commitment to relationship marketing. Of the three different ‘Type B’ scenarios Bsoc can be regarded as fitting the radical fix

category because it is effectively ‘re-engineering’ its strategic approach to embrace relationship

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

TABLE 3. Research results: progress towards a high relationship marketing focus at Bsoc

Key Issues Position of Bsoc on Key Issues

Company: Company:

Use of distribution channels Bsoc is interested in new channels,

but slower than some players to look at the Internet

Bsoc has shown commitment, and invested in RM

Commitment to one-to-one may not be equally strong throughout the

organisation. Co-ordination between functions, and consistency of approach, are key here

Strong belief, as shown by well established loyalty programme Moving in this direction

Stated desire for RM

Belief in one-to-one future

Belief that better relationships lead to

competitive advantage

Customer driven and event led marketing

Staff: Staff:

Emphasis on excellent communication with

customers to ‘connect’ and spot opportunities Levels of training are improving, and thenew systems will allow the performance

of individual staff to be monitored. The success of new initiatives relating to the new systems will require close tracking Some empowerment at branch manager level; more could be done here

Incentive schemes cover a range of targets; possibly still too focused on product sales, but this is under review

Empowered, self-managed staff who can make

quick decisions for customers

Reward customer retention, not just new accounts

Technology: Technology:

Information is powerful and vital to strategy This is recognised, and customer

information is used in strategic planning This is improving, due to current initiatives, data cleaning and data modelling. Also, computer screens have the potential to be shared with customers

Bsoc is moving towards this, also better availability of a rich mix of attitudinal/ buying behaviour data which could be used to identify ‘life events’ in future Yes; also on-screen prompts introduced to help with cross-selling

New systems allow fuller records to be held, giving details of customer interactions, and allowing updates to be made

When the new systems are fully operational, more could be done to maximise this opportunity

High levels of integration of systems and

processes, also customer driven rather than account driven systems

Giving staff full access to customer information

when dealing with enquiries

Databases used for contact management

purposes

All dealings with customers logged, allowing continuity between transactions

Customer contacts used as a market

research opportunity Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

TABLE 3. (Con’t)

Key Issues Position of Bsoc on Key Issues

Customers: Customers:

Emphasis on current and potential value

of customers, with lifetime value focus This emphasis is well established, and thecurrent investment in new information

systems is part of this commitment Attempts to improve this integration are underway, with greater data availability and a commitment to the required staff training

Many different opportunities are used to improve data quality

In theory, this in now possible. However, many implementation issues will need to be addressed

Relationship achieved through integrating

technology and the human face

Focus on easy, regular contacts with the

customer, and use these to update systems Anticipate needs through events-based marketing

Adapted from Dibb and Meadows, 2001.

marketing and one-to-one principles. Even so, there is progress to be made in relation to the ‘softer’ issues.

These findings raise interesting questions about how the behaviour of businesses at the high- end of the framework is changing. Comparing the approach of Bsoc to financial services organisations at the high-end of the original framework brings the changing nature of relation- ship marketing into focus. A period of three years has elapsed between the creation of the framework and the current study. During this time various developments have been noted. First, the language being used to describe the relationship marketing approach is changing. CRM, which previously was rarely mentioned, now seems to be a preferred term for financial services organisations. Second, a wider range of customer channels is generally now being used. Curi- ously Bsoc, which has been slow to establish an Internet presence, has not been particularly proactive in this regard. Third, the concept of customer lifetime value is becoming increasingly entrenched, with considerable coverage in the marketing and financial services literature. This has been matched by a desire by organisations to upgrade their technological capability to manage customers at this level.

There is a growing realisation that it is impossible to avoid this kind of technological invest- ment. Once the infrastructure is in place, the needs and wants of customers naturally come to the fore. Once again this emphasises that considerable progress has been made in the ‘harder’ areas of technology and customer analysis. However, in some cases (and Bsoc is typical) staff training may be slow to catch up and there may be difficulties ensuring the smooth implementation of new approaches at all levels of the business. This is consistent with suggestions that in periods of change staff and company structure issues may take longer to resolve.

CONCLUSION

The detailed financial services case study outlined in this paper has provided a vehicle for examining the application of relationship marketing by an industry leader. In particular, the analysis has pinpointed the recent progress of relationship marketing in retail financial services.

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

The study has used an existing framework of relationship marketing in financial services as the basis for the analysis.

The findings of the research highlight various barriers which can impede an organisation’s progress towards a relationship marketing focus. These relate to the organisation’s structure, its appreciation of its customer base, level of technological resource and human resource policies. The analysis demonstrates that in practice it may be simpler to manage the ‘harder’ areas of technology and customer analysis. Dealing with the ‘softer’ aspects of staff and company structure can take longer and may be more complex. Even though Bsoc can be classified as a ‘Type B’ business with a high relationship marketing focus adopting a

radical fix approach to relationship marketing, human resource policies have been slow to catch up. As a result, the progress of implementation has been somewhat impeded by certain structural constraints.

An important outcome of this application has been to identify key changes in the behaviour of businesses at the high-end of the relationship marketing framework. Key differences have emerged in the use of language, the application of different customer channels and the use of lifetime value as a basis for assessing the worth of customer relationships. There is also an acceptance that technology and systems are required that are capable of handling this change. Nonetheless, the ultimate success or failure of organisations pursuing a relationship marketing vision lies in their ability to manage implementation at a much more human level.

REFERENCES

Bateson, J.E.G. (1995) Managing Services Marketing: Text and Readings, Fort Worth: The Dryden Press. Berry, L.L. (1983) Relationship marketing. In: L.L. Berry, G.L. Shostack and G. Upah (eds) Emerging

Perspectives on Services, Chicago: American Marketing Association.

Berry, L.L. (1995) Relationship marketing of services—growing interest, emerging perspectives. Journal of the Academy of Marketing Science 23(4), 236–45.

Berry, L.L. (1996) Retailers with a future. Marketing Management 5, Spring, pp. 39–46.

Berry, L.L. and Parasuraman, A. (1993) Building a new academic field—the case of services marketing.

Journal of Retailing 69, Spring, 13–60.

Blaxter, L., Hughes, C. and Tight, M. (1996) How to Research, Buckingham: Open University Press. Blennerhasset, L. and Galvin, E. (1993) The strategic dimension. In: J. Peppard (ed) I.T. Strategy for

Business, London: Pitman.

Bogelund, J.N. and Skytte, H. (1997) A review and integration of socio-political processes in marketing channel relationships, MAPP Working paper, No. 46, Aarhus School of Business, Denmark.

Buttle, F. (1996) Relationship Marketing: Theory and Practice, London: Chapman.

Chaffey, D., Mayer, R., Johnston, K. and Ellis-Chadwick, F. (2000) Internet Marketing, Harlow: Pearson Education.

Coviello, N.E., Brodie, R.J. and Munro, H.J. (1997) Understanding contemporary marketing: development of a classification scheme. Journal of Marketing Management 13(6), 501–22.

Coviello, N.E., Milley, R. and Marcolin, B. (2001) Understanding IT-enabled interactivity in contemporary marketing, Working Paper, University of Calgary.

Crittenden, V.L. and Wilson, E.J. (2002) Success factors in non-store retailing: exploring the Great Merchants Framework. Journal of Strategic Marketing 10, 255–72.

Day, G. (1998) Organizing for interactivity. Journal of Interactive Marketing 12(1), 47–53.

Dibb, S. and Meadows, M. (2001) The application of a relationship marketing perspective in retail banking. The Service Industries Journal 21(1), 169–94.

Dwyer, F.R., Schurr, P.H. and Oh, S. (1987) Developing buyer-seller relationships. Journal of Marketing 51, 11–27.

Edvardsson, B., Thomasson, B. and Ovretveit, J. (1994) Quality of Service: Making it Really Work, London: McGraw-Hill. Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

Ford, D. (1997) Understanding Business Markets: Interaction, Relationships and Networks, London: Academic Press.

Gronroos, C. (1989) Defining marketing: a market-oriented approach. European Journal of Marketing 23(1), 52–9.

Gronroos, C. (1994) From scientific management to service management. A management perspective of the age of service competition. International Journal of Service Industry Management 5(1), 5–20.

Gummesson, E. (1999) Total Relationship Marketing, Rethinking Marketing Management: From 4Ps to 30Rs, Oxford: Butterworth-Heinemann.

Hakansson, H. (1982) International Marketing and Purchasing of Industrial Goods, Chichester: Wiley. Hakansson, H. and Snehota, I. (1995) Developing Relationships in Business Networks, London: Routledge. Howcroft, B. and Durkin, M. (2000) Reflections on bank-customer interactions in the new millennium.

Journal of Financial Services Marketing 5(1), 9–20.

Iacoabucci, D. and Hibbard, J. (1999) Towards an encompassing theory of business marketing relationships (BMRs) and interpersonal commercial relationships (ICRs): an empirical generalization. Journal of Interactive Marketing 13(3), 13–33.

Joshi, A.W. (1995) Long-term relationships, partnerships and strategic alliances: a contingency theory of relationship marketing. Journal of Marketing Channels 4(3), 75–94.

Kotler, P. (1992) Marketing’s new paradigm: what’s really happening out there. Planning Review Special Issue, September–October, 50–2.

Kotler, P. (2000) Marketing Management, Englewood Cliffs: Prentice Hall.

Meadows, M. and Dibb, S. (1998) Assessing the implementation of market segmentation in retail financial services. The International Journal of Service Industry Management 9(3), 266–85.

Mitchell, A. (1995) The ties that bind. Management Today, June, 60–4.

Moller, K. (1994) Interorganizational marketing exchange: metatheoretical analysis of current research approaches. In: G. Laurent, G. Lilien and B. Pras (eds) Research Traditions in Marketing, Boston: Kluwer, 348–82.

Moller, K. and Halinen, A. (2000) Relationship marketing theory: its roots and direction. Journal of Marketing Management 16(1), 29–54.

Moller, K. and Wilson, D.T. (1995) Business Marketing: An Interaction and Network Perspective, Boston: Kluwer.

Obeng, E. and Crainer, S. (1994) Re-engineering: back to earth. directions—The Ashridge Journal, July, 4–9.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1985) A conceptual model of service quality and its implications for future research. Journal of Marketing 49, Fall, 41–50.

Peppard, J. and Rowland, P. (1995) The Essence of Business Process Re-engineering, Hemel Hempstead: Prentice Hall International.

Peppers, D. and Rogers, M. (1993) The One-to-One Future, London: Piatkus.

Peppers, D. and Rogers, M. (1997) Enterprise One-to-One. Tools for Competing in the Interactive Age, New York: Currency Doubleday.

Peppers, D. and Rogers, M. (1999) The One-to-One Manager, New York: Currency Doubleday. Perrien, J. and Ricard, L. (1995) The meaning of a marketing relationship: a pilot study. Industrial Marketing

Management 24, 37–43.

Reichheld, F.F. (1993) Loyalty-based management. Harvard Business Review 71, March–April, 64–73. Reichheld, F.F. and Kenny, D.W. (1990) The hidden advantages of customer retention. Journal of Retail

Banking 12(4), 19–23.

Reichheld, F.F. and Sasser, W.E., Jr. (1990) Zero defections: quality comes to services. Harvard Business Review 68, September–October, 105–10.

Roberts, J.H. (2000) Developing new rules for new markets. Journal of the Academy of Marketing Science

28(1), 31–44.

Shaw, B. and Stone, M. (1988) Competitive superiority through data base marketing. Long Range Planning

21(5), 24–40. Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4

Shepard, D. (1995) The New Direct Marketing: How to Implement A Profit-Driven Database Marketing Strategy,

New York: Irwin.

Sievewright, M. (2001) Charting the future of financial services. Credit Union Magazine 67(4), S4–S6. Speed, R. and Smith, G. (1993) Customers’ strategy and performance. International Journal of Bank Marketing

11(5), 3–11.

Spekman, R.E. (1988) Strategic supplier selection: understanding long-term relationships. Business Horizons

31, July–August, 75–81.

Storbacka, K. (1997) Segmentation based on customer profitability—retrospective analysis of retail bank customer bases. Journal of Marketing Management 13, 479–92.

Thurston, C. (2000) Financial services lead the way. Global Finance 14(1), 114–16.

Turnbull, P.W. and Valla, J.-P. (1990) Strategic planning in industrial marketing—an interaction approach. In: D. Ford (ed) Understanding Business Markets: Interaction, Relationships and Networks, London: Academic Press.

Yin, R.K. (2003) Case Study Research: Design and Methods, 3rd Edn, Thousand Oaks, CA: Sage. Zeithaml, V. (2000) Service quality, profitability, and the economic worth of customers: what we know

and what we need to learn. Journal of the Academy of Marketing Science 28(1), 67–85.

Zielinski, D. (1994) Database marketing: with costs down, more use it to pinpoint promotions, create customer bonds. The Service Edge 7, February, 1–3.

Questions:

1. Discuss briefly the reasons supporting the utilization of CRM as a vehicle for the development of service providers’ marketing strategy

2. Discuss in brief the differences between low RM focus and high RM focus service providers 3. Describe in brief the current conditions of Bscoc.

4. Please indicate and discuss the points that Bsoc have achieved towards becoming a relationship-oriented company and the points that need to further improve in the future.

Your assignment must follow these formatting requirements:

• Be typed, double spaced, using Times New Roman font (size 12), with one-inch margins on all sides; citations and references must follow APA or school-specific format.

• Include a cover page containing the title of the assignment, the student’s name, the professor’s name, the course title, and the date. The cover page and the reference page are not included in the required assignment page length.

Do wn lo ad ed b y [T E I of Ath en s] at 00 :0 3 24 Dec em ber 2 01 4