Digital Insurance

Benchmark

Insurers should embrace new technologies to

differentiate themselves in the digital arena

I N S

U R A

N C E

The digital economy is here to stay. Today the world has 6.7 billion mobile phone users, 2.7 billion internet users and 1.7 billion social media users. In the Netherlands, with already high internet usage, the strongest growth is expected in usage on smartphone and tablets. The increased use of these devices and the willingness to rapidly adopt new technologies by consumers will be a catalyst for the development of new functionalities at phenomenal speed.

Continuous digital disruption in the insurance value chain is not a possibility, it’s a certainty. Digital has already changed the rules of the game in the insurance marketplace. Consumer behaviour has changed fundamentally with continued growth of the use of digital channels over traditional intermediaries and banks, increased use of online aggregators and strong growth in sharing consumer experiences through social media. Moreover, customers are influenced by a constant flow of new or enhanced digital experiences in other industries. While insurance needs may have stayed the same, customers have become more demanding with regards to their digital expectations for Insurance.

Our Digital Insurance benchmark shows that Dutch insurers have made good progress in supporting basic internet sales and service transactions and plugging into social networks. Most insurers however struggle with their mobile capabilities as only a few offer more than basic functionalities in the areas of claim notification. With the accelerated adoption rates of new technologies by consumers, NL Insurance companies need to speed up in increasing their digital capabilities to continue to meet the constantly increasing needs of online and especially mobile Insurance consumers. However quickly replicating internet capabilities to mobile will be costly and most likely have low chances of success as it will only create limited differentiation compared with other insurers. Successful use of mobile in an Insurance context requires more creativity to deal with the typical low interaction rate between Insurer and Consumers.

Adopting trends like gamification, telematics and the internet of things offer opportunities to create truly differentiating value propositions, which will enable insurers to regain customer loyalty and at the same time increase profitability. The insurers that have the vision, courage and endurance to take a step forward in the digital arena will be the ones that will truly reap the benefits of the digital megatrend.

Pieter Hofman Partner

Preface

Continuous digital disruption in the

insurance value chain is not a

possibility, it’s a certainty

Preface 2

Introduction 4

Insurance Benchmark Internet, Social & Mobile Capabilities 5

Internet transactions 6

Social & customer interaction 8

Mobile services & apps 10

Opportunities for improvement 12

Telematics 14

Gamification 15

New devices connected to the Internet (Internet of Things) 16

Contacts 18

Appendix 19

Deloitte e-Insurance maturity model 20

Assessed Insurance companies 22

Content

The Digital Economy is here to stay. Although digital distribution began in the 1990’s with the advent of the internet, it is only in the latter part of the last decade that the earlier predictions on its impact and explosive growth have become reality. ‘Digital’ is now a way of life. Today the world has 6.7 billion mobile phone users, 2.7 billion internet users and 1.7 billion Social Media Users1. Technology adoption

curves are becoming highly accelerated. Where the fixed line telephone took 110 years to reach 1 billion users, the Mobile phone reached the same milestone after 22 years and the smartphone after only 8 years. Mobile data traffic is expected to grow by 11 times by 2018 compared to 2013, of which 85% is caused by Smartphones and tablets2. This connected online

population forms a brand new market that cuts across borders and thinks fundamentally different about topics like information access, convenience, power of choice and communities.

Digital has already changed the rules of the game in the insurance marketplace and is expected to continue to create additional disruption in the upcoming years. Distribution of Insurance products in the Netherlands through direct channels has already reached > 80% for Health Insurance and > 50% for other Personal Lines Insurance and is expected to continue to grow in the upcoming years3. The

constant flow of new and enhanced features that consumers are being offered while shopping online for clothes or booking a holiday have raised expectations of what an insurance company should deliver.

Since the Netherlands is the frontrunner in both insurance penetration and distribution through direct channels4, it would be reasonable to expect

Dutch insurance companies to take a leading role in providing consumers with digital experiences. However, an initial assessment indicated low adoption rate of mobile capabilities of insurers. Subsequent interviews revealed many insurers struggle meeting constantly increasing needs of their digital consumers. This whitepaper aims to give an overview of current Internet, social and mobile capabilities of Dutch insurers and to support in understanding trends and required capabilities in digital distribution and – ultimately – in growing their online business.

For this whitepaper, Deloitte benchmarked the internet and mobile capabilities of 19 Dutch and 11 top international players in P&C and Health insurance. The benchmark was conducted on nearly 70 functional capabilities in 18 categories, using Deloitte’s e-Insurance maturity model. For each functional capability insurers were scored in a 6 level maturity scale (varying from non-existing to best in class). Please refer to the appendix for more details on the e-Insurance maturity model and scoring method.

The findings of this study are categorized in three sections: 1) facilitating internet transactions, 2) enabling social and online customer interaction and 3) providing mobile support. To conclude, future growth opportunities in digital insurance are explored.

Introduction

________________________________________________________ 1 Euromonitor, Ovum, eMarketer, IDC, EIU, 2014

2 Cisco VNI Forecast 2014

The constant flow of new and enhanced

features that consumers are being

offered while shopping online have

raised expectations of what an insurance

company should deliver

Insurance Benchmark Internet,

Social & Mobile Capabilities

Driven by improved retail shopping experiences, customers have started to expect insurance services to provide immediate response times and seamlessly access on any device, from desktop and laptop to tablet and mobile phone. So how are Dutch insurers dealing with these demands?

Well supported sales process

All Dutch insurers in our sample offer advanced capabilities for online premium calculations including recalculation for added or removed coverages, which can be saved for future use in 38% of the cases. The majority of Dutch insurers also support online acceptance of new policies with less than 24% requiring manual approval of an insurance employee. Best in class insurers, such as InShared, offer immediate acceptance and real-time confirmation of the insurance policy.

Greater differences occur in the area of self-service capabilities regarding policy and claims management. Policy related services, claims services and tracking of claims approval status are in general a lot less developed online than sales functionality. Within claims, 58% offers at least advanced capabilities in the area of first notice of loss, while tracking of claims approval status is only supported by 8%.

Insurance Benchmark Internet,

Social & Mobile Capabilities

Internet transactions

In the Netherlands

89%

of insurers offer

sophisticated online premium calculations

with online acceptance

After-sales support underdeveloped

Leading international insurers have made managing policies and making claims online a standard feature. However, in the Netherlands, 27% of insurers have nothing or very little in place to help customers manage their policies online. Changes can only be made by downloading forms from the website or by using traditional (non-digital) methods. On the other hand, ‘new kid on the block’ Ditzo let’s customers change their coverage online with immediate recalculation of prices and validation of changes, all without the help of a service employee.

Of the leading international insurers assessed in our benchmark, nearly all support the online submission of claims, enabling a complete online claims process in 58% of cases, and a partial online claims process in 38% of cases, with the final steps being confirmed by a service employee. This capability is less developed in the Netherlands, where 1 in 5 insurers does not support online claim submission at all.

Track & Trace of claims is the least developed capability across the board, with 46% of Dutch insurers and 43% of international insurers assessed not providing customers with an online overview of their claims’ status. In the Netherlands, Track & Trace is most commonly provided for health insurance, which has the highest claim volume and, therefore, the biggest need to reduce the number of calls. Zilveren Kruis for example provides insight into the healthcare costs and the parts that have been covered by insurance. International best practices let the customer see each stage of the claims process, with proactive notifications of changes in the claims status.

Chart 2 – Maturity of self-service on Dutch vs. International websites

27% of the Dutch insurers have very little

in place to help customer manage their

policies online

Consumers are becoming increasingly connected online, both professionally and personally, and they are collaborating within social networks to compare products, services and experiences. In online retail and online travel, the publication of reviews and ratings has become standard. For insurance companies, the fact that existing and potential customers communicate much more transparently about their experiences increases the pressure to improve levels of experience and reliability. Social networks primarily used for marketing Dutch insurers recognize the importance of social networks, with 84% of insurers assessed providing webcare on the major social networks and 73% using social networks and communities for product promotion. A few Dutch insurers go beyond this stage. Some insurers such as Zilveren Kruis offer special interest groups not only for various promotions but also the chance to discuss insurance-related topics. Some insurers such as FBTO go a step further by offering a co-creation platform on which customers can vote on how claims should be handled or which product terms & conditions should be changed. Dutch insurers take the lead in these best practices, which is in line with the chief role that Dutch consumers have in using social networks5.

Although peer reviews and ratings are very common in online retail and online travel, it is not a well-established practice within the Dutch insurance

sector. Price comparison site Independer.nl lets customers rate the customer service and claims handling of the insurers that it compares. However, the rating of insurance products and customer service on the insurers’ own websites has been adopted by only a few insurers such as InShared and AllSecur. Ratings can be viewed by visitors to the website, showing the score, age group and product concerned. The sense of reliability that this creates could be adopted by other insurers.

Social & customer interaction

Chart 3 – Maturity of social features on Dutch vs. International websites

________________________________________________________ 5 Euromonitor, Ovum, eMarketer, IDC, EIU, 2014

84 12 4

Customer service hardly digital

A recent study by GFK shows that consumers use the digital channel for information gathering, comparison and actual purchasing up to 75% of the time, which implies that personalized services and a rich digital customer interaction have become more important than ever6.

With more and more customer interactions taking place on digital channels, the demand for personalized online services and digital customer interaction through tools such as ‘webchat’ and ‘call me back’ has increased. Notably, over a quarter of Dutch insurance companies surveyed provide a call me back function, as opposed to only one international insurer in our benchmark.

The GfK survey also showed young age groups are most willing to buy insurance online. This correlates with the Dimension Data’s Global Contact Centre benchmark 2013/2014, which suggests this youngest age group prefers electronic messaging (42%) above social media, app and phone. The phone comes fourth as a contact channel (29%). For generation X, the preference for electronic messaging (44%) is closing in on telephoning (46%). Given this preference, insurers have a long way to go, with only

16% of Dutch insurers offering any form of webchat. A Dutch insurer that has implemented proactive webchat has apparently recorded a 50% increase in conversion after implementing a solution that prompts you to chat when analytics detect you are wandering around the website.

Another way of differentiating in the marketplace is by implementing a single point of contact strategy. Nationale Nederlanden has introduced a personal claims manager as the single personal contact during the process of handling a claim. A Swiss insurer takes this a step further and introduced a personalized web portal where the customer can always communicate with the same employee instead of contacting an anonymous call centre.

Chart 4 – Maturity of customer contact on Dutch vs. International websites

________________________________________________________ 6 GFK Insights, Online Insurance, March 2013

Only 16% of Dutch insurers offer any form

of webchat

As indicated earlier within the digital world the importance of the mobile channel (smartphone and tablet) has increased significantly in recent years and is expected to continue to grow strongly in the upcoming years. Our research shows that Insurance presence in the mobile world, through mobile websites and Apps, is limited and the functionalities currently offered are very basic.

Mobile websites at the adolescent stage When looking at mobile accessibility, only 36% of the insurers in the Netherlands offer a (partly) mobile website experience.

Features provided on the mobile websites of insurers are limited, once again focusing on effective sales (calculations, acceptance) rather than supporting self-service for policy management and claims. Only a few insurers such as Agis, InShared and Kroodle let customers manage their policies through the mobile website.

Moreover, the Track & Trace of claims is hardly supported in the Netherlands. This is the biggest difference with the best practices of international insurers. Less than 10% of the Dutch insurers in our data set provide Track & Trace functionality through their mobile websites versus more than 40% of international insurers. Health insurers such as Humana, Kaiser and Aetna, provide the option to claims bills through their mobile website with advanced Track & Trace capabilities.

Mobile services & apps

Apps focus on claims

Mobile apps could be the key to insurers becoming a greater part of their policyholders’ lives. However, most apps focus currently on the claim submission process, with 78% of Dutch insurers apps supporting this process. This is, without doubt, a vital capability as the claim is traditionally considered ‘the moment of truth’.

In our benchmark, none of the apps of Dutch insurers support claims aftercare or policy amendments. However, the international insurers in our benchmark have taken steps to develop apps in line with their websites, with 1 in 5 supporting policy changes through the app and 2 in 5 letting customers track their claims after submission through the app. Geico, that has one of the better known mobile insurance apps, provides quoting, policy management as well as an interactive accident guide to start the claims reporting process. However, these are simply the same features on a different channel.

Overall it can be concluded that both Dutch Insurers as well as International Insurers have not fully capitalized on the opportunity the new Mobile Channel offers them. Most NL Insurers don’t have an App at all and most of the ones that do have an App have only created functionalities in the area of First Notice of Loss. The lack of functionalities in combination with the low interaction level of consumers with their Insurance company results in a very low ‘success rate’ of Insurance Apps.

Chart 6 – Maturity of Dutch vs. International apps

36%

of Dutch Insurers offer a partly

mobile website experience, and most

apps focus only on claim submission

Our research has shown that most Dutch insurers are making progress in supporting online sales & service transactions but are struggling to provide truly mobile solutions. Given the market circumstances, insurers should carefully consider how to differentiate themselves in a world of continued digital disruption. Despite strong growth projections of especially mobile in combination with low maturity of Insurers in this area, it’s questionable if putting tremendous effort into ‘replicating’ current services to mobile is advisable as interaction levels and customer needs for mobile are substantially different than for other distribution channels.

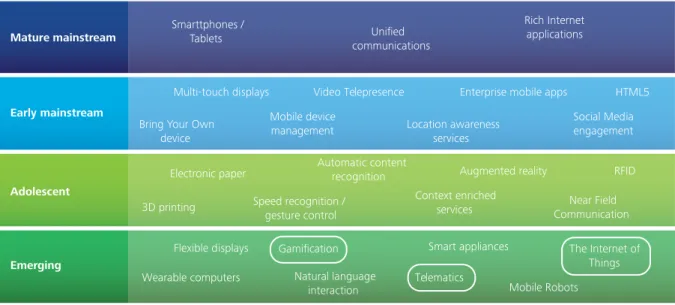

Inspiration with regards to the next steps in creating relevant and differentiating omni-channel capabilities can be found in Deloitte’s annual IT Trends & Innovation survey7 which identifies the most

important IT trends and technology enablers that can support revenue growth and business transformation across industries. In the area of IT trends for Mobile and User engagement 27 trends were identified in 4 levels of maturity. The most relevant emerging trends for Insurance are Gamifcation, Telematics and the Internet of things.

Opportunities for improvement

Figure 1 – Maturity of IT trends for Mobile and User engagement

________________________________________________________ 7 IT Trends & Innovation survey, Deloitte & CIO Magazine, 2014

Mature mainstream Early mainstream Adolescent Emerging Smarttphones / Tablets Multi-touch displays Bring Your Own

device Electronic paper 3D printing Flexible displays Wearable computers communications Video Telepresence Mobile device management Automatic content recognition Speed recognition / gesture control Natural language interaction Rich Internet applications Enterprise mobile apps Location awareness services Augmented reality Context enriched services Smart appliances Telematics HTML5 Social Media engagement RFID Near Field Communication The Internet of Things Mobile Robots

The idea behind telematics in car insurance (also known as Usage Based Insurance or Pay How You Drive) is that driving behaviour is actively monitored and used as a risk indicator to amend premiums accordingly. Especially for good drivers, telematics offers a more precise assessment of their skills and driving habits and associated risk profile ultimately resulting in lower Insurance premiums.

Using telematics devices to understand clients driving behaviour and provide a discount on car insurance dates back to 2005 but is now at the tipping point of large scale use. Exponential growth is expected in the upcoming years resulting in € 50 billion premium income by 2020 in Europe8 mainly due to

the reduced cost of technology, increased consumer demand and cross industry adoption. Telematics was initially predominantly enabled by monitoring devices installed in cars and still shows huge potential with Telematics unit sales in Western Europe expected to reach 25 million vehicles by 2016. Continuous growth of smartphone capabilities who nowadays offer GPS and G-force tracking has enabled App builders to create cheap and easy to use telematics based value propositions. Popularity of these apps in combination with strong smartphone growth will give an enormous boost to Telematics based Insurance policies. Telematics also offers opportunities for Insurance companies sharing their knowledge around e.g. ‘dangerous’ roads and pro-actively giving Telematics based drivers alternatives to further reduce their risk profile. Lastly in case of an accident, Telematics enables quick emergency services (e.g. automatically notifying police, towing truck and car rental company) as well as a reduction of error rates and costs for claims settlement.

Telematics based car insurance is already offered by major US insurers such as Progressive, AllState, StateFarm and Zurich. Their propositions are continuously being improved. Progressive, one of the first insurers to launch a Pay As You Drive proposition, uses a small SnapShot device that needs to be plugged into the car’s diagnostic port to collect data such as time of day, vehicle speed and braking tendencies, used for calculating personal discounts. Whoosz, introduced in the Netherlands, facilitated by T-Mobile and Zurich, uses a smartphone app to collect driving characteristics, giving more direct feedback while driving, providing a score per ride with leadership boards and shows accumulated savings based on (adjusted) driving style.

Telematics

________________________________________________________ 8 Global Insurance Telematics Study, Ptolemus, 2012

Popularity of Telematics Apps in

combination with strong smartphone

growth will give an enormous boost to

Usage Based Insurance policies

Gamification is the use of game thinking and game mechanics in a non-game environment to increase customer engagement and stimulate desired behaviour through challenges, incentives and rewards. These incentives can range from awarding achievement levels or badges to earning loyalty points and discounts.

In another industry, Dutch lease company Leaseplan provides benchmark data to their individual drivers showing fuel usage, damage profile and number of speeding tickets versus peers. Innovator Moven(bank) is actually built around providing customers with instant insights into their spending behaviour, providing incentives to improve their financial health over time. In a similar fashion, insurers could provide better insights, peer benchmarking, potential under- or over-insurance alerts and prevention tools. For life insurance, CUNA Mutual Group provides the

Retirement Radar App, which leverages ‘gamification’ techniques to help engage members in the complex process of retirement planning. For car insurance, Geico focuses on educational drivers with their Tricky Traffic App.

When gamification and telematics are combined Insurers could enable a virtual competition, by comparing the performance of individual ‘players’ (policyholders) with others in their peer group and providing real-time feedback in return for various benefits (discounts, loyalty points, coupons for external services, etc). Other options are Parental Guidance for young drivers, in which parents are alerted when a problem arises. Combining fun and value can help insurers enhance customer relationships by increasing the number of valuable customer interactions.

Gamification

Figure 2: Telematics and Gamification: from trend to opportunity9

Jon is 16 and just got his license. Dad is a little nervous.

Jon plays driving games on his smartphone

Jon gets real-time feedback in the car

Jon can share results with social network friends

Dad can see Jon’s trips and gets alerts if there is a problem

Dad gets a discount and renews his policy Jon’s driving quality is recorded and visible; good habits are rewarded

________________________________________________________ 9 Mills, H. Tubiana, B., Innovation in insurance, The path to progress. Deloitte University Press. (2013)

The number of people connected to the internet continues to grow from 2.7 billion in 2013 to 3.3 billion in 2017. Advanced but cheap sensor technology combined with available wireless communication will stimulate the growth of devices and smart objects connected to the internet to up to 50 billion by 202010. Sensors are already built into

smartphones for geolocation, Samsung equipped Washing machines with sensors enabling to shut of water supply automatically in case of leakage and Homewizard provides smart sensors for energy monitoring and control, fire prevention and burglary alarms. The range and use of Personal wearable devices will be booming in the incoming years varying from smart watches monitoring personal health (e.g. heart rate, movement, fat and cholestorel levels) to Google glass using Augmented reality to present an additional layer of information (e.g. traffic info, peer reviews and facial recognition linked to social media).

The real challenge for insurers is to capitalize on the tremendous opportunity provided by the enormous amount of additional data that will become available. Insurers can use external sensors to move from passive to proactive guidance. Consumers with high medical costs could be alerted by geolocation that additional coverages are required for travel or health insurance when they are about to cross the border. Analysing non-traditional insurance data could reveal new risk factors enabling pricing differentiation or new value propositions. With Google Glass, claims inspections can be made easier and cheaper, even better when facial expression recognition techniques are used to verify fraud. Information from health monitoring devices can be combined with loyalty programs for health insurance, creating a different kind of interaction and sense of belonging with an Insurance company. Pro-actively providing or supporting the purchase of home monitoring devices reduces risk. Therefore premium income is affected negatively at first, however, it builds trust and creates mental and financial exit barriers for consumers, positively influencing long term client relationships. Considering the law of Metcalfe that states that the value of a network increases quadratic with the number of objects added, the number of opportunities the Internet of things will create in general but also in an insurance context will only be limited by our own creativity and imagination.

New devices connected to the Internet (Internet of Things)

________________________________________________________ 10 IT Trends & Innovation survey, Deloitte & CIO Magazine, 2014

The real challenge for insurers is to

capitalize on the tremendous opportunity

provided by the enormous amount

of additional data that will become

available

INTERNET

of

THINGS

Insurers should embrace new technologies to differentiate themselves in the digital arena. The digital economy is here to stay. Whereas the world today has 6.7 billion mobile phone users, 2.7 billion internet users and 1.7 billion social media users, by 2017 these numbers have grown to 8 billion mobile phone users (1.2 for every human), 3.3 billion internet users and 2.5 billion social media users. In the Netherlands, with already high internet usage, the strongest growth is expected in smartphones and tablets. The increased use of these devices and the willingness to rapidly adopt new technologies by consumers will be a catalyst for the development of new functionalities at phenomenal speed.

Digital disruption in the insurance value chain is therefore not a possibility, it’s a certainty. Insurers shouldn’t deny this new reality but should embrace the opportunities these new digital technologies have to offer. In this way new areas of differentiation in the strongly commoditized and price competition dominated environment can be created. Adopting trends like gamification, telematics and the internet of things offer opportunities to create truly differentiating value propositions, which will enable insurers to regain customer loyalty and at the same time increase profitability. The insurers that have the vision, courage and endurance to take a step forward in the digital arena will be the ones that will truly reap the benefits of the digital megatrend, before others like aggregators or Google will take ownership of the majority of customer’s digital touchpoints.

The insurers that have the vision, courage

and endurance to take a step forward

in the digital arena will be the ones that

will truly reap the benefits of the digital

megatrend

Contacts

For more information on this research, please contact:

Pieter Hofman

Partner IT Strategy +31.88.288 5150 [email protected]

Frank Bovee

Director Strategy & Operations +31.88.288 7888

Raoul van de Hoef

Senior Manager Deloitte Digital +31.88.288 9709

Deloitte’s e-Insurance assessment methodology uses a framework of over 70 measurable and consumer-facing business capabilities to assess an insurer’s online maturity on their website and mobile site/app. The model was co-developed and validated with support of the University of Amsterdam.

A 6 level maturity score was assigned to each capability. Scores for each insurer’s website and mobile site/app are based on current consumer expectations and existing capabilities in the market. Deloitte used its business insights to assign maturity-level descriptions to each capability score to provide a guide for assessment. Using this methodology, benchmark data has been gathered for two different insurance segments: P&C and Health. Analysis of 30 insurers across three different countries (US, UK and NL) is included in this white paper. Maturity-level criteria

Maturity level Explanation

Does not exist Functionality is not present

Basic Functionality is very limited and mostly static

Moderate Functionality exists and is mostly interactive

Competitive Some advanced functionality exists within the capability

Advanced Almost all advanced functionality is offered

Best in Class Leading practices and all advanced functionality within the capability are offered

The Deloitte e-Insurance assessment results for each category identify key areas where insurance leaders differentiate themselves from their competition and score much higher than average. Examples of such categories include ‘Tracking’, ‘Claim’, ‘Manage policy’, and ‘Peer to Peer’.

Appendix

e-Insurance assessment categories

Category Category description

Design Does the interface conform to general design metrics of website or app use?

Usability The ease of use of website or app

Catalogue The completeness of the information provided on the website with respect to the market in which the website operates

Premiums: How mature are the possibilities to calculate premiums for products of the insurer? Acceptance Is the process of acceptance & confirmation mature within the insurer?

Manage policy Can customers manage their policies without the interference of a service employee?

Claim Can users claim damages and health care costs, and to what degree can it be done through the interface?

Tracking Is it possible to track progress on activities performed by the insurer?

Assurance Does the insurer provide assurance on the company, the products and the service? Security How secure is the interface and how secure is user data?

Customer service What is the maturity of the customer service?

Profile management Can users manage their own profile and to what extent does this have effect on the insurance policies?

Peer to Peer Does the insurer give users options to interact with one another with respect to the insurer of the products offered?

Multi-channel Does the insurer offer sales and services across multiple channels? Prevention Does the insurer offer advice or tips to prevent damage or health costs?

Guiding/advice Are customers guided through the process of buying insurance or is there no advice from the insurer?

Recommendations How mature are the recommendation systems within the insurers interface?

Mobility Does the insurer offer devices to track data and customer behaviour to influence, for example, premium rates and discounts?

For our assessment, we selected the majority of direct writers in the Netherlands, covering over 80% of the total GWP in Property & Claim and Health insurance. A selection of leading insurers from the US and UK was added that showed international best practices.

The following insurance companies were part of our assessment:

Dutch companies

Aegon Kroodle

Agis Menzis

AllSecur Nationale Nederlanden

Centraal Beheer OHRA

CZ Unive

Delta Lloyd Verzekeruzelf

Ditzo VGZ

FBTO Zekur

Inshared Zilveren Kruis

Interpolis

International companies

Aetna - US Humana – US

Allstate – US Kaiser Permanente – US

Aviva - UK Progressive Insurance – US

Axa - UK State Farm – US

Farmers – US Zurich - UK

Geico - US

The analysis was conducted in the last half of 2013 and early 2014.

Assessed Insurance companies

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.nl/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.