P A R T 1

This part includes:

CHAPTER 1 The accounting environment 2

CHAPTER 2 Accounting reports: their nature and uses 26

CHAPTER 3 Classifi cation and analysis of transactions 50

CHAPTER 4 The structure and content of fi nancial statements 87

CHAPTER 5 Financial statement analysis 123

CHAPTER 6 Accounting and fi nancial management 176

BACKGROUND ENVIRONMENT

AND PRINCIPLES

Jackling Accounting ch01.indd 1

Jackling Accounting ch01.indd 1 18/3/10 2:22:38 PM18/3/10 2:22:38 PM

1

LEARNING OBJECTIVES

To defi ne accounting •

To identify the different uses of accounting information •

To describe how accounting aids economic decision making •

To describe the types of economic decisions made by users of accounting information •

To identify the types of entities that use accounting information •

To explain the roles of the regulatory environment, the economic decision-making •

environment and the international environment in society To evaluate how the international environment affects accounting •

The accounting

environment

C H A P T E R

Jackling Accounting ch01.indd 2

Jackling Accounting ch01.indd 2 18/3/10 2:22:39 PM18/3/10 2:22:39 PM

1

C H A P T E R 1 O V E R V I E W

Introduction

Have you ever purchased a car, chosen a mobile phone plan, or rented a house or fl at? If you answer yes to any one of these questions then you have probably used accounting information to help you make that decision, as well as many other daily decisions.

Nature of accounting Cash flow statement Statement of financial position Income

statement Partnerships Companies

Sole traders Public sector enterprises Environment of accounting Economic decision-making environment Regulatory environment International environment Key financial statements Types of accounting entities

Jackling Accounting ch01.indd 3

Jackling Accounting ch01.indd 3 18/3/10 2:22:39 PM18/3/10 2:22:39 PM

1

4

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

Looking forward

This chapter will introduce the reader to the ‘world of accounting’. It will examine the meaning of accounting, and how this meaning has changed over time. The chapter will also examine the roles and functions of accounting information in a number of social, economic and business contexts and settings. It will be seen that accounting information is not only an essential decision-making tool for business organisations, but it also has great signifi cance to the functioning of society.

The wider social signifi cance of accounting can best be understood and explained by reference to the diverse and sometimes complex environment in which accounting exists. Accounting both infl uences and is infl uenced by the environment in which it operates. Environmental factors that have shaped the development of accounting include:

• the regulatory environment (i.e. regulations related to accounting) • the economic decision-making environment

• the international environment.

It will be seen that each of these factors has had a unique infl uence on accounting developments. Furthermore, each has important implications for society. Together, they explain the relevance and the diversity of the impact that accounting has in society.

A large international company, Santos Ltd, has been chosen for illustrative purposes throughout this textbook. Santos is an acronym for South Australia Northern Territory Oil Search—a company involved in oil and gas exploration, which made its fi rst signifi cant discovery of natural gas in 1963.

Constant reference will be made to the company’s activities, including its fi nancial statements. Familiarise yourself with Santos through the web address www.santos.com and Appendix 1 in this textbook, where you will fi nd the Santos Ltd Annual Report 2008.

1.1

ACCOUNTING DEFINED

Traditionally, accounting has been defi ned as the process of ‘recording, classifying and reporting’ the

fi nancial activities and transactions of a business enterprise.1 The process of recording and classifying

business transactions is commonly referred to as ‘bookkeeping’. The bookkeeping function of accounting still forms the foundation of much accounting activity and the early part of this textbook presents a broad outline of the traditional manual recording process. An accountant is usually defi ned as ‘one who is skilled

in accounting’.2 At the beginning of the twentieth century, however, the role of the accountant did not

extend much beyond a bookkeeping function—that is, the keeping of records according to a set of well-defi ned rules and procedures. At this time, accountants were generally referred to as ‘bookkeepers’. In the business world of the twenty-fi rst century, the activities and responsibilities of accountants extend far beyond mere bookkeeping and the keeping of records. They include the interpretation and analysis of accounting reports, the design and operation of computer-based systems, the planning and conduct of business activities and the understanding of complex accounting regulations that have accumulated over many years.

Accountants serve a potentially wide variety of user groups. The many different users of accounting information include:

■ owners or shareholders of a business entity

■ people who have lent money to such an entity

■ the entity’s employees

■ government agencies

■ other social and political interest groups, such as environmental groups and trade unions.

Jackling Accounting ch01.indd 4

Jackling Accounting ch01.indd 4 18/3/10 2:22:39 PM18/3/10 2:22:39 PM

5

THE ACCOUNTING ENVIRONMENT

1

In providing information for these users, accountants frequently need to consider more than justfi nancial factors in the preparation of reports. For example, in recent years ethical considerations and environmental considerations have become particularly important. Accounting has a wide-ranging function and, hence, a broad defi nition of the fi eld of accounting is needed—one that embraces the variety of professional activities engaged in by accountants.

Several years ago a committee of the American Accounting Association (an infl uential body whose members include the leading academics and practitioners in accounting) provided a broader and more modern defi nition of accounting, beyond the ‘recording, classifying and reporting’ of transactions. The committee defi ned accounting as ‘the process of identifying, measuring and communicating economic

information to permit informed judgements and decisions by users of the information’.3 This defi nition has

continued to have widespread acceptance because it covers many of the essential facets of accounting.

1.1.1

Accountants: who are they and what do

they do?

Primarily, accountants are concerned with ‘communicating economic information’. As providers of information, they are similar to the newspaper or television reporter, the editor of a technical journal or the teacher. All must be skilful in conveying information concisely and accurately to their chosen audiences.

As communicators, accountants are mainly interested in conveying ‘economic information’—that is, the results of fi nancial transactions and events involving a fi rm. Using fi nancial statements, accountants are able to summarise the effects of a mass of seemingly unrelated fi nancial events on an individual or an organisation. Several million transactions can be summarised on one page of fi nancial results in a company fi nancial statement. In the Santos Ltd Annual Report 2008 in Appendix 1 at the end of the book, the 10-year fi nancial summary gives a one-page overview of fi nancial results, including sales and profi ts for the years from 1999 to 2008.

Classifi cation and summarisation are essential to communicate information effectively and effi ciently in a short space of time. On television, a 30-minute news telecast summarises events in distant places, each telecast consisting of many minor events that would take hours to relate in full.

In communicating economic data through fi nancial statements, the accountant acts in the same way. The approach adopted is discussed in the fi rst chapters of this book, which consider how relevant events are identifi ed, measured and communicated to users in summary form.

The second aspect to the American Accounting Association’s defi nition of accounting gives direction on what to communicate. The purpose of the information provided is to ‘permit informed judgements and decisions by users of the information’. The accountant must report on events that are useful to those who receive accounting reports.

To be useful, the information must be relevant to a decision the user is to make and it must help the user to choose between alternative courses of action. For example, to be told that it is raining in a neighbouring country is not useful unless, perhaps, one intends to travel there and suitable clothing must be selected. The accountant’s purpose may, therefore, be found in the decisions the users of accounting information must make.

1.2

KEY FINANCIAL STATEMENTS

The key fi nancial statements are:

■ the income statement (also known as the statement of profi t and loss and the statement of fi nancial

performance)

Jackling Accounting ch01.indd 5

Jackling Accounting ch01.indd 5 18/3/10 2:22:40 PM18/3/10 2:22:40 PM

1

6

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

■ the statement of fi nancial position (formerly known as the balance sheet)4

■ the cash fl ow statement.

Only the income statement and statement of fi nancial position will be introduced in this chapter. A more detailed discussion of the fi nancial statements is provided in Chapter 2 and Chapter 4.

■ The income statement reports the income, expenses and profi t (or the surplus of income over the expenses) that have been made during a given period. The statement shows how an entity’s income was obtained and how the expenses were incurred.

■ The statement of fi nancial position provides an important indication of the fi nancial performance of the entity. The statement of fi nancial position lists the assets or resources of value controlled by the enterprise, the entity’s debts and the owner’s claim on the entity. The statement of fi nancial position provides an indication of the fi nancial position of an entity at any given point in time.

Pause and refl ect

Reading fi nancial statements

Financial statements of large corporations are often complex documents. However, at this point, view the fi nancial statements of Santos in Appendix 1 at the end of the book. These reports may also be viewed at www.santos.com. Use the statement of fi nancial position for the last two years (known as the balance sheet in the 2008 Santos fi nancial statements; they include a list of the assets or resources of value controlled by the enterprise) to test your understanding and to answer the following questions.

1. State the total dollar value for assets listed in 2008.

2. Indicate whether assets have increased in total dollar value from 2007 to 2008.

3. Write three possible reasons for the change in the total dollar value of the assets from 2007 to 2008.

1.3

WHAT ARE ACCOUNTING ENTITIES?

This section examines the types of organisations (or accounting entities) for which accounting information, in the form of fi nancial statements, is prepared. It also examines the information needs of those external to the entity, including owners, lenders, government authorities and a wide range of other interested parties.

In accounting, the reporting (or accounting) entity is considered to be separate from its owners, who

are therefore regarded as external parties. An accounting entity is the area of activity in which users of

accounting information have an interest. Accounting entities may include an individual, a company, a company branch offi ce, a professional practice, a club, a government department or a small business

enterprise. The owners are variously called shareholders, partners or owners, depending on the form of

legal organisation they adopt. The emergence of greater interest in government enterprises, and in the public sector generally, has revealed that these entities have broadly similar information needs to private sector entities.

Jackling Accounting ch01.indd 6

Jackling Accounting ch01.indd 6 18/3/10 2:22:40 PM18/3/10 2:22:40 PM

7

THE ACCOUNTING ENVIRONMENT

1

1.3.1

Types of entities

Sole ownerships

A sole ownership is a business owned and operated by one person. It is the simplest form of ownership. Many small businesses are owned and operated by one person. No particular legal formalities are required to commence operations, although it is common practice to set up a business bank account and operate under a business name, which must, in certain circumstances, be registered. Amounts contributed to the

business by the owner are called capital.

Examples of small businesses include hairdressers, small general retail stores, butcher shops, cake shops, and fruit and vegetable shops.

As previously noted, for accounting purposes the business is considered to be a separate accounting entity from the owner, although, in law, the two are one and the owner remains liable for all business debts. The sole trader form of ownership is designed for the small business.

Most businesses exist to make profi ts. Owners may withdraw funds obtained from profi table trading for their personal use, or they may choose to reinvest them in the business. If desired, they may also withdraw previous contributions of capital.

Decision making by sole owners

The owner usually manages the business and the decisions of a sole ownership. The owner typically must decide:

■ whether to invest more capital or to withdraw capital from the business

■ how much profi t to withdraw

■ whether to expand the business, sell out or cease operations

■ whether the business is fi nancially stable.

These decisions overlap—for example, the owner might decide to invest more capital by leaving the profi t in the business. The decision to expand or discontinue must be based on expectations about the future fortunes of the business and the accountant can provide some information to aid in forming those expectations.

Partnerships

A partnership consists of two or more individuals who join as co-owners of a business. As with sole ownerships, partnerships are not separate legal entities from their owners and in law they remain ‘unincorporated’.

Examples of partnerships include many retail organisations as well as some professional businesses, such as those run by doctors, lawyers and accountants.

Why are partnerships formed?

These types of businesses are formed so that the skills of individuals are pooled in one business to maximise profi ts. For example, a legal fi rm operating as a partnership may bring together two or three solicitors, each with expertise in different aspects of the law, such as commercial law, criminal law and family law.

The accounting records of the partnership are treated as a separate accounting entity from the owners (partners). However, the partners are personally liable for any debts that are contracted by the partner-ship, and, if necessary, these debts may follow the partnership into bankruptcy. The partners are the partnership; if a partner dies, the partnership is normally dissolved.

Jackling Accounting ch01.indd 7

Jackling Accounting ch01.indd 7 18/3/10 2:22:40 PM18/3/10 2:22:40 PM

1

8

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

Decision making by partners

The decisions of partners are similar to those of the sole trader, with one important added responsibility— the partners must be able to assess their respective claims on the partnership.

■ The partners may agree on how much capital each will contribute.

■ The partners may agree on how much each may withdraw as a share of the profi t.

In the absence of a formal agreement, a Partnership Act—as enacted in Partnership Acts within

states and territories of Australia (e.g. see the Victorian Partnership Act at www.austlii.edu.au/au/legis/vic/

consol_act/pa1958154/), which requires the partners to share all profi ts equally, normally applies. For most partnerships, no more than 20 partners may be admitted.

The need for accounting information by partnerships

The desire to safeguard the individual claims of each partner creates an important need for accounting information. Records of capital contributions, withdrawals and the sharing of profi ts must be maintained so that the partners can decide how much they may withdraw or, alternatively, how much they will need to contribute as additional capital to maintain the partnership.

Companies

A company is a business owned by people with shares in the business. A business becomes a company when it meets certain legal requirements. A company is a legal entity and, as such, it is an ‘artifi cial person’ conducting a business in its own name.

Larger businesses are incorporated as companies, limited by share capital. Their shareholders enjoy

limited liability status. Capital is contributed by paying for shares in the company. The company is created as a separate legal entity from its owners who, in most cases, are not personally liable for the debts of the company beyond amounts unpaid on their shares. The term ‘Limited’ (Ltd) after a company’s name acknowledges that the liability of the shareholder is limited.

Types of companies include:

■ Unlimited liability companies: these exist, but they are rare.

■ Proprietary Limited (Pty Ltd): there are many companies of this type and they are generally small, privately owned companies or companies owned by other companies. There must be at least one but no more than 50 shareholders. The transfer of ownership shares is restricted and proprietary companies are generally not permitted to advertise for the contribution of funds, either by way of share capital or through loans.

■ Public companies: these are companies that are not proprietary companies. They must have at least one member, but there is no maximum number. They may advertise for funds and ownership shares may be bought and sold freely. The prices at which a company’s shares are traded will fl uctuate according to investors’ beliefs about the value of each share. Many public companies

are listed on stock exchanges, which are organised markets for the trading of shares and other

securities. As previously indicated, throughout this textbook reference will be made to Santos as an example of an international public company. Check the website www.santos.com for more information on this company.

Decision making in companies

What decisions must investors or shareholders in companies make?

■ In valuing shares, investors need to evaluate the progress of the company. This task is diffi cult, because

most investors in modern companies are remote from the day-to-day operations of the companies.

Jackling Accounting ch01.indd 8

Jackling Accounting ch01.indd 8 18/3/10 2:22:40 PM18/3/10 2:22:40 PM

9

THE ACCOUNTING ENVIRONMENT

1

■ A large company might have thousands of shareholders spread across the globe. Obviously, they

cannot all manage the company and, accordingly, the shareholders elect a board of directors to act for them. The directors, in turn, appoint managers to supervise the day-to-day operations of the company.

■ The directors retain responsibility to ensure that shareholders’ interests are always prominent when

decisions are being made.

The directors are required each year to call an annual general meeting of shareholders. The decisions to be made at this meeting include:

■ electing directors for the coming year

■ appointing an auditor to examine the income statement and statement of fi nancial position

■ determining the dividend, which is the proportion of the profi t to be paid out to shareholders as a

return for their investment.

In making these decisions, the investors require an account of the directors’ stewardship, meaning an account of their activities as care-keepers of the funds entrusted to them by the shareholders. This is contained in an annual report, which includes statements by the directors on the progress of the company and their expectations for the future. Also included in the annual report are the income statement and the

statement of fi nancial position.

Public companies, and proprietary companies that are owned by other companies, must make their reports available to the public. Other proprietary companies, which are called small proprietary companies, need not reveal their results to the public.

A company’s accountant prepares the annual fi nancial statements. It is the directors’ responsibility to ensure that these reports give a ‘true and fair’ representation of the company’s activities. However, since the company’s accountants, as employees, are responsible to the directors, and since the report will be used to evaluate the directors, a further step is taken to ensure that the reports are ‘true and fair’ and are not disguised to mislead the shareholders as to the achievements of the directors. In all public companies and in some proprietary companies an auditor must be appointed by the shareholders to make

an independent examination of the fi nancial statements. The auditor is usually a fi rm of public accountants.

Large international accounting fi rms, such as PricewaterhouseCoopers, Deloitte Touche Tohmatsu, Ernst & Young, and KPMG, provide a range of fi nancial services to companies, including independent auditing services. An auditor’s report is included in the annual report of Santos (see Santos Ltd Annual Report 2008 at Appendix 1 or www. santos.com). The auditor for Santos is currently Ernst & Young.

Decision making by shareholders

As owners, shareholders must make some important decisions, including the following:

■ Should the directors be reappointed? In making this decision, shareholders require an account of the

year’s fi nancial performance. This may be compared with performances in previous years or with the results of other companies.

■ What dividend should be paid? The dividend is the amount a shareholder receives in a distribution

of the profi ts. Dividends may not be paid unless the company has profi ts available for distribution. Otherwise, the dividend would amount to a return of capital. In practice, the full profi t is rarely distributed. Profi ts are retained in the company to cope with unexpected future commitments, to cope with higher costs due to infl ation, or to allow the company to grow. Re-invested profi ts are a major source of funds for expanding businesses.

■ In deciding how much dividend to pay, shareholders normally vote to endorse an amount

recommended by the directors. In approving a recommended dividend, a shareholder must know

Jackling Accounting ch01.indd 9

Jackling Accounting ch01.indd 9 18/3/10 2:22:41 PM18/3/10 2:22:41 PM

1

10

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

how much profi t was available for distribution and, if profi ts are to be retained, what purposes are to be served by the retained profi ts. Again, the shareholder needs fi nancial information that accounting reports are intended to provide.

■ If the management desires either to close down or to ‘liquidate’, the shareholder would want to know

what cash is likely to be received before agreeing to the liquidation.

These decisions, made at meetings of shareholders, are often left to those with major shareholdings in the company. When shares are traded on a stock exchange, a shareholder has a simpler way of expressing dissatisfaction with the company—that is, selling the shares and allowing a new shareholder to contend with the poor management or low dividends. The decision to sell shares, or to buy them if the prospects are good, is probably the only decision many shareholders will consider.

Public sector ownerships

The role of public sector ownerships differs in countries throughout the world and is identifi ed by the extent of government ownership of enterprises. The public sector in Australia refers to:

■ federal and state governments

■ local councils and all the associated structures that they own or control, such as departments,

statutory authorities, boards and commissions

■ business enterprises such as healthcare services—for example, public hospitals are public sector

enterprises that generate revenue from providing health care to the public, but they are also provided with funds from state and/or federal governments.

Many public sector business enterprises have broadly similar organisational structures to those in the private sector, and, therefore, have similar fi nancial statements.

The following list defi nes features of public sector enterprises that differ from private enterprises.

■ Public sector ownership is ownership on behalf of constituents—that is, taxpayers. Public sector

entities manage the resources available to them on the public’s behalf.

■ A public sector enterprise is not focused solely on making profi ts. Unlike private sector organisations,

which have in common the ‘profi t motive’, public sector business enterprises are generally set up to provide a service that, for a variety of reasons, would not be provided at an acceptable price, quantity or quality without government intervention. Public sector business enterprises are not ultimately dependent on profi t for their existence, and profi t generation is only one of many considerations for public sector entities.

Some of their other objectives may include effi ciency, effectiveness, equality, growth, stability, or the promotion of social welfare, culture, defence, history, education or environmental considerations. These are complex matters on which to report.

Formerly, it was commonly believed that a fairly simple form of accounting would suffi ce for public sector organisations. A statement of cash receipts and payments was often all that was available. However, as governments have become increasingly accountable as guardians of community resources, and as more sophisticated management has been adopted within public sector entities, the requirements for account-ing information to support decisions are now as demandaccount-ing as those of the private sector. Accountaccount-ing information needs to be combined carefully with other information (e.g. social and welfare information) to ensure that the most appropriate decisions are made.

While many of the accounting concepts discussed in later chapters are developed within a framework of private sector entities, it should be borne in mind that the principles are equally applicable in the public sector.

Jackling Accounting ch01.indd 10

Jackling Accounting ch01.indd 10 18/3/10 2:22:41 PM18/3/10 2:22:41 PM

11

THE ACCOUNTING ENVIRONMENT

1

1.4

THE ACCOUNTING ENVIRONMENT

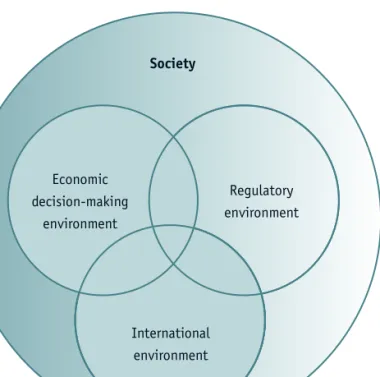

So far we have briefl y introduced the meaning of accounting, the nature of fi nancial statements and the types of accounting entities that prepare fi nancial statements. In this section we discuss how accounting infl uences, and is infl uenced by, its environment. The accounting environment has many aspects. These provide much of the richness and the diversity of the accounting discipline, as well as explaining its importance in society. As mentioned in the introduction to this chapter, the accounting environment includes:

■ the regulatory environment

■ the economic decision-making environment

■ the international environment.

These facets of the accounting environment are, to some extent at least, interdependent. Furthermore, all three impact on society more generally. These interdependencies are summarised in Figure 1.1.

We will fi rst discuss each of the ‘inner circles’ of Figure 1.1, the regulatory, the economic decision- making and the international accounting environments. We will then examine how each of these ‘inner circles’ impacts on the ‘outer circle’ (society).

1.4.1

The regulatory environment

Accounting regulations form the rules and principles that govern the structure, content, audit and disclosure of fi nancial information. The ethical responsibilities of accountants in performing their professional accounting duties are also governed by a number of regulations.

Society

Regulatory environment

Regulatory environment

FIGURE 1.1 The accounting environment

Economic decision-making

environment

International environment

Jackling Accounting ch01.indd 11

Jackling Accounting ch01.indd 11 18/3/10 2:22:41 PM18/3/10 2:22:41 PM

1

12

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

The role of regulation

Accounting regulations are principally designed to protect investors, creditors and other users from potential fi nancial losses associated with fraudulent, misleading or poor-quality fi nancial statements. High-quality fi nancial statements, which are deemed to refl ect a ‘true and fair’ view of an entity’s performance and fi nancial position, are not only essential for protecting individual investors against potential losses, but they play an important role in maintaining credibility and confi dence in our fi nancial systems and institutions, and in the business community more generally.

Professional accountants must follow regulations or they risk penalties imposed by the law and/or by the disciplinary processes of the accounting profession. In Australia, for example, there are essentially three main sources of accounting regulation:

1. requirements of company legislation

2. stock exchange listing requirements for public companies

3. accounting standards issued by the standard-setting body.

These sources of regulation are discussed in greater depth in Chapter 10, but they will be briefl y outlined here.

Requirements of company legislation

The relevant legislation governing accounting regulation in Australia is known as the Corporations Act 2001

(Cwlth). The Corporations Act is the highest level of regulatory authority over companies in Australia because

it is a statute passed by the federal parliament. The Corporations Act is a very lengthy statute covering a

great number of issues relating to the formation, conduct, administration and winding-up of companies in Australia. However, accountants are generally more concerned with the accounting requirements of the Act, which require that company directors present to shareholders at the annual general meeting an audited income statement and statement of fi nancial position. These fi nancial statements must comply with the detailed requirements for disclosure contained in relevant accounting standards (see the section below referring to accounting standards).

Stock exchange listing requirements

In most countries the ownership of shares in large public companies is traded via a stock exchange. For example, since 1998 the Australian Securities Exchange Ltd (ASX) has been a listed company. The

Corporations Act governs the conduct of the ASX and its members. A stock exchange is primarily concerned with the protection of investors as well as the promotion of an effi cient and ethical share market.

The ASX regulates the information conveyed via fi nancial statements through its listing requirements. That is, if a company wishes to list on the stock exchange, it must comply with the fi nancial disclosure (display) requirements of the ASX and other listing requirements. These requirements, like those of the

Corporations Act, have traditionally been concerned with information that should be disclosed to the public rather than with technical accounting issues—such as the different ways to measure and classify transactions in the fi nancial statements. Australian accounting standards provide detailed rules for measuring and classifying accounting transactions.

Accounting standards

Accounting standards provide detailed rules on how particular types of fi nancial transactions and other events should be dealt with in an entity’s accounting records. Some examples of how accounting standards provide rules for recording and reporting accounting information follow.

Jackling Accounting ch01.indd 12

Jackling Accounting ch01.indd 12 18/3/10 2:22:41 PM18/3/10 2:22:41 PM

13

THE ACCOUNTING ENVIRONMENT

1

■ Accounting standards explain how different types of assets should be valued and how they should be

set out and disclosed in the fi nancial statements.

■ Accounting standards help to ensure that an entity’s income statement and statement of fi nancial

position represent a ‘true and fair’ representation of its performance and fi nancial position.

International accounting standards

In a growing global economy, companies in different countries increasingly do business with each other. Many countries in the world, including Australia, prepare accounting standards. The International Accounting Standards Board (IASB) also sets accounting standards at the international level. As we will see in a later section of this chapter, a major objective of the IASB is to develop an internationally compatible set of accounting standards that all countries can readily adopt. At present, accounting standards around the world tend to differ from country to country and have varying degrees of enforceability.

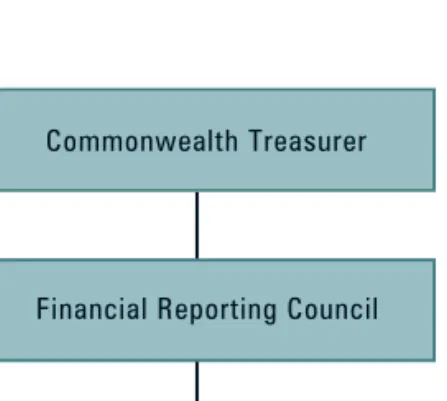

Despite the global economy, most countries continue to maintain a set of accounting practices that are unique to their individual circumstances. For example, the Financial Reporting Council (FRC) is the body responsible for the accounting standard-setting process in Australia for the private and the public

sectors. The FRC is a statutory body under the Australian Securities and Investments Commission Act 2001, as

amended by the Corporate Law Economic Reform Program (Audit Reform and Corporate Disclosure) Act 2004.

The FRC is responsible for providing broad oversight of the process for setting accounting and auditing standards as well as monitoring the effectiveness of auditor independence requirements in Australia and giving the Commonwealth Treasurer reports.

The FRC appoints the members of the Australian Accounting Standards Board (AASB), which issues

‘approved Australian accounting standards’. Under the Corporations Act, the governing board of a company

is required to comply with AASB accounting standards in preparing fi nancial statements. Failure to comply

with the accounting standards is an offence under the Corporations Act, and could lead to legal action. This

means that company directors and professional accountants who do not comply with these standards risk a variety of penalties which can be imposed under the law, such as fi nes and imprisonment. Figure 1.2 summarises current arrangements for accounting standard setting in Australia.

Because accounting standards deal with the detailed aspects of disclosure and measurement in the fi nancial statements, the release of a new accounting standard can have important consequences for an entity. For example, accounting standards often impact on the profi tability and the fi nancial position of companies, which in turn infl uence the economic decisions of users such as investors and lenders.

Commonwealth Treasurer

Financial Reporting Council

Australian Accounting Standards Board

FIGURE 1.2 A summary of the current arrangements for accounting standard setting in Australia

Jackling Accounting ch01.indd 13

Jackling Accounting ch01.indd 13 18/3/10 2:22:41 PM18/3/10 2:22:41 PM

1

14

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

1.4.2

The economic decision-making environment

As mentioned earlier in this chapter, the function of accounting is to communicate ‘economic information to permit informed judgements and decisions by users of the information’. The relationship between fi nancial statements, economic decisions and users is summarised in Figure 1.3.

Users of accounting information Decision required Relevant financial statements Economic events

e.g. owners and lenders e.g. whether to invest or lend money to the entity e.g. measures of risk, return

(profit), resources owned, relevant to user decisions e.g. financial transactions concerning the entity

FIGURE1.3 The relationship between fi nancial statements, economic decisions and users

Who then are the users of fi nancial statements, and what kinds of economic decisions do they make? There are several categories of users, and they make a variety of economic decisions based on company fi nancial statements. The users of the fi nancial statements include investors, lenders and others. (Note the reference to users of fi nancial statements, not users of accounting information, therefore excluding internal users.) Each user of fi nancial statements has special information needs depending on the types of decisions to be made. These decisions involve key questions, the answers to which are often available in fi nancial statements. This section describes several users of fi nancial statements and identifi es the types of decisions they seek to make from the statements.

Investors

Investors are usually the shareholders or owners of a company. Shareholders purchase a company’s share capital with the expectation of receiving a satisfactory return on their investment. Shareholders usually look for the return on their investment in two forms: dividend payments (distribution of profi ts of the

company to shareholders), and capital gain (increases in the share price of the company’s shares).

Jackling Accounting ch01.indd 14

Jackling Accounting ch01.indd 14 18/3/10 2:22:41 PM18/3/10 2:22:41 PM

15

THE ACCOUNTING ENVIRONMENT

1

The return on the shareholders’ investment needs to be consistent with the level of risk. The higherthe perceived risk of an investment (e.g. in a company’s shares), the higher will be the expected return required by investors, and vice versa. Shareholders need accounting information to help them to determine whether they should buy, hold or sell their share investments, and assess the ability of an entity to pay dividends.

Lenders

Lenders are of various types and are usually termed creditors (entities to whom money is owed). They may be long-term or short-term lenders and their loans may or may not carry a fi xed rate of interest. Lenders have priority over investors for repayment when an entity is wound up (i.e. discontinued). Lenders need accounting information in order to assess the risk of making loans: that is, the likelihood that the borrower will be able to meet the interest and principal repayment terms of the loan. Lenders may require a high interest and/or a greater security from a borrower who is perceived to possess high risk.

Short-term lenders

Suppliers of inventory commonly demand payment within 30 days. Normally, no interest is charged for the supply of inventory to be paid for within 30 days and a discount may be offered for early payment before the due date. Other short-term debts might be for electricity, telephone, other utilities and various services.

Short-term lenders need to assess whether the enterprise will remain stable for the period of the loan and whether future cash fl ows from earnings will be suffi cient to cover repayments of the loan plus interest.

Long-term lenders

Any entity may attempt to borrow long-term funds by offering its assets as security for the loan. Three types of long-term lending are outlined in this section.

1. Land and buildings may be purchased, for example, by giving the seller, or a bank or fi nance

company, a mortgage over the property in return for a loan. If repayments are not made, the property is forfeited.

2. Companies generally have greater borrowing opportunities than other forms of organisations.

Public companies may offer debentures for sale to the general public. Debentures are fi nancial

instruments offered to the public or to fi nancial institutions in exchange for large amounts of money for a number of years and secured by a fi xed or fl oating charge over the company’s assets. The issue of debentures must be accompanied by a prospectus. Debenture certifi cates normally carry a fi xed rate of interest. Debentures of large companies are listed on the stock exchange and may be traded at the market price.

3. Companies may also issue unsecured notes, which are effectively debentures without security, and

they are often issued for shorter periods of time. They may also issue notes that are convertible into shares at some later date, known as ‘convertible notes’.

Long-term lenders have a longer term perspective. They must determine the likelihood of the entity collapsing prior to repayment of the loan. They must also form an opinion about whether the future expected cash fl ows from trading activities will cover interest commitments. These concerns are close to those of the shareholder. Both parties are concerned with profi ts, but the lender is concerned solely that the return should be suffi cient to meet repayments, whereas the shareholder wishes to maximise future returns. Both are concerned with the risk of failure of the entity.

Jackling Accounting ch01.indd 15

Jackling Accounting ch01.indd 15 18/3/10 2:22:42 PM18/3/10 2:22:42 PM

1

16

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

Other external users

Accounting information is also used as the basis of taxation returns. These reports are prepared in accordance with taxation law, which differs in certain respects from the principles of valuation to be discussed in this book. Accounting is concerned with a measure of profi t useful for decision making, whereas taxation law is concerned with such principles as obtaining a fair distribution of the tax burden according to the taxpayer’s ability to pay. In many cases, therefore, taxable income differs substantially from accounting profi t. Taxpayers and ratepayers are also important users of accounting information. Ratepayers, for example, may wish to ascertain whether a special levy earmarked for a particular community project has been used for that purpose and used in an effi cient manner.

■ Other users of accounting information include employees, who are interested in knowing whether

the organisation is able to continue, or perhaps whether it can sustain higher wage payments without incurring losses.

■ Accounting information is also used in assessing tariffs and customs duties and in the deliberations of

investigatory commissions established to determine whether particular industries require government assistance.

■ Accounting information provides a host of statistical data for economic analysis, including the

calculation of the national income.

■ Environmental and social responsibility groups are also interested in the reports prepared by

organisations. With changing community values, business fi rms are increasingly accountable to a wide range of stakeholders with interests and values that go beyond the traditional reporting offered by fi nancial statements. Companies today need to be aware that environmental issues can directly impact on performance. Therefore, reporting issues of waste and emission control are important aspects of accounting information. This is evidenced in the Santos reports.

Pause and refl ect

Environmental impact

Go to the website of Santos and locate the company’s sustainability statement. As an energy company, Santos needs to acknowledge that while making economic progress it needs to operate in an environmentally responsible manner.

Describe what actions Santos has in place for oil spillage. Outline at least two other activities undertaken by Santos in 2008 as part of its sustainability policy.

1.4.3

The international accounting environment

The business and commercial environment of the twenty-fi rst century is, in many respects, very different from that of the twentieth century. The rapid globalisation of fi nance and consumer markets and the increasing internationalisation of business activities, particularly the proliferation of multinational corporations, have created numerous fi nancial and economic interdependencies in international commerce.

Countries around the world have different cultural, political, economic and legal systems; they also have different accounting regulations and practices. No two countries have produced an identical approach to accounting regulation and practice. For example, companies in Australia have in the past been permitted by accounting regulations to report changes in the value of certain assets such as land and

Jackling Accounting ch01.indd 16

Jackling Accounting ch01.indd 16 18/3/10 2:22:42 PM18/3/10 2:22:42 PM

17

THE ACCOUNTING ENVIRONMENT

1

buildings, and plant and equipment. In the US, companies have not been permitted to report changesin the value of such assets in their fi nancial statements. These differences highlight the difference in approaches to accounting.

At least four factors can contribute to differences in accounting regulations and practices in different countries. These include a country’s:

1. State of economic development: national economies around the world vary in terms of the extent of

their economic development.

2. State of business complexity: national economies vary in terms of their technological and industrial

know-how, creating differences in their business needs as well as their business output. This can also infl uence accounting diversity.

3. Shade of political persuasion: national economies vary in terms of their political systems, from the

centrally controlled economy to the market-oriented economy.

4. Reliance on a particular system of law: national economies vary in terms of their supporting legal

system. They may rely on either a common-law system or a code-law system; for example, they may have protective legislation and unfair trade and competition laws.

Harmonisation of accounting standards and international

convergence

To avoid and/or minimise international diversity in accounting standards, there have been many calls to

harmonise accounting standards. Harmonisation entails developing internationally compatible accounting

standards that every country can adopt. If successful, harmonisation of accounting standards will result in business entities in different countries preparing fi nancial statements on the same or a similar basis of accounting. Harmonisation would produce a number of benefi ts. For instance, some countries, particularly developing nations, have not fully developed their own set of accounting standards and principles. An internationally accepted set of accounting standards would allow developing nations to immediately become part of the mainstream.

Another benefi t of harmonisation is that companies needing to raise fi nance in foreign markets might fi nd the process easier if their fi nancial statements were consistent and comparable with a commonly accepted set of international accounting standards. In the case of Australia, it would enable foreign investors to more readily evaluate the performance and fi nancial position of Australian companies relative to other companies in the international business arena.

However, there are limitations to harmonisation as well. The previous section demonstrates that many countries around the world adopt different approaches to accounting regulation and practice. Such wide differences could render international harmonisation a diffi cult task.

In July 2002, the FRC decided to adopt a policy of international convergence and international harmonisation of Australian accounting standards. In this context, international convergence means working with other standard-setting bodies to develop new or revised standards that will contribute to the

development of a single set of accounting standards for worldwide use.5

From 1 January 2005 Australian companies have been required to prepare and present their fi nancial statements under the guidelines of the international harmonisation of accounting standards issued by the IASB.

Benefi ts of convergence and harmonisation

In adopting international accounting standards, the AASB envisages fi ve main benefi ts from convergence and harmonisation:

Jackling Accounting ch01.indd 17

Jackling Accounting ch01.indd 17 18/3/10 2:22:42 PM18/3/10 2:22:42 PM

1

18

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

1. Increasing the comparability of fi nancial statements prepared in different countries, thus providing

participants in international capital markets with better quality information for decision making.

2. Decreasing barriers to international capital fl ows and increasing the understanding by foreign

investors of Australian fi nancial statements.

3. Reducing the fi nancial reporting costs for Australian multinational companies and foreign companies

operating in Australia.

4. Facilitating more meaningful comparisons of the fi nancial performance of reporting entities and the

fi nancial position of reporting entities.

5. Moving fi nancial reporting in Australia towards best international practice.

1.5

ACCOUNTING AND SOCIETY

As indicated earlier in Figure 1.1, accounting has the potential to have a very important infl uence on society. The relationships expressed in Figure 1.1 indicate that society is affected by accounting through the regulatory environment, the economic decision-making environment and the international environment of accounting. Let us now briefl y consider the impact of each of these factors on society.

1.5.1

The regulatory environment and society

The pervasiveness and infl uence of accounting in society can be explained, at least in part, by the observation that the modern business corporation has become an increasingly integrated part of the social fabric. Companies provide much of the world’s employment, consumer products and services, and technology. The economic progress and the standards of living of the industrialised world have depended to a signifi cant extent on business enterprise. Companies are also a major source of government revenue, through company income tax and other taxes. This revenue is used to fund, among other things, social welfare and economic programs, and to maintain a satisfactory standard of living.

On the negative side, companies are a major contributor to pollution and environmental damage in the world. Furthermore, companies that fail (whether due to fraudulent or culpable managerial behaviour, mismanagement or poor business dealings) can cause enormous damage to local communities and economies and, in some circumstances, the national and international economies. For instance, as demonstrated in the global fi nancial crisis that began in 2008, the failure of companies can cause signifi cant social distress and dislocation through loss of employment to workers, loss of revenue for the government, loss of investment by shareholders and creditors, and loss of products and services for consumers.

These are some of the reasons companies have become more tightly regulated and closely monitored by government regulatory agencies in recent years. Just as the business corporation has become more embedded in the social fabric, so too has accounting. This is partly because accounting information is often likened to the ‘road map’ of the corporation. The linkages here between accounting and mapping are well founded. Accounting is widely recognised as the only viable information source that can display where an organisation is going in a fi nancial sense, how well it is achieving its profi t-making objectives, and whether managers are using resources in a manner consistent with organisational objectives.

Accounting information can display whether the performance of managers has been of the highest quality or otherwise and it can also signal warnings of impending business distress and, ultimately, collapse. The most visible signal of impending collapse is when the cash fl ow position of a company can no longer meet the cost of operations, particularly fi xed commitments such as interest payments on loans. It is mainly accounting records that are capable of communicating such precise and crucial fi nancial details to managers and users. A number of corporate failures, notably Enron and WorldCom in the

Jackling Accounting ch01.indd 18

Jackling Accounting ch01.indd 18 18/3/10 2:22:42 PM18/3/10 2:22:42 PM

19

THE ACCOUNTING ENVIRONMENT

1

US and HIH Insurance and One.Tel Ltd in Australia, demonstrate that failure to produce reliable andaccurate accounting information has a devastating impact on society. Company insolvencies can cause signifi cant fi nancial losses to individual investors, and dislocation and social distress to local communities. In the case of widespread corporate collapses, they can even bring recession to national and international economies.

As mentioned earlier in this chapter, the importance of accounting information to users has been recognised in company legislation and other forms of accounting regulation. Regulation imposes considerable responsibilities on accounting entities and professional accountants to produce relevant and reliable fi nancial statements for accountability and economic decision-making purposes. Considered historically, the purpose behind accounting regulation is to afford a framework of protection to society, particularly against the production of potentially fraudulent, misleading or poor-quality fi nancial statements which, among other things, can mask the true fi nancial position of a company.

Accounting in its regulatory context impacts on society in other important ways. We discussed above the users who rely on fi nancial information for economic decision making. These users collectively represent the stakeholders of a company. Many of these stakeholders participate, directly or indirectly, in an entity’s revenue or profi t. Stakeholders include:

■ investors or shareholders, who obtain their share of the profi t in terms of dividends

■ lenders, who obtain their share of the profi t in terms of interest and principal repayments

■ government, which obtains its share of the profi t in terms of tax collection

■ suppliers and other trade creditors, who obtain their share of the profi t in terms of payment of invoices

■ managers and employees, who obtain their share of profi t in terms of wages, bonuses and other

remuneration.

Each of the user groups is assumed to have a vested economic interest in maximising its share of an entity’s profi t. This can lead to confl icts of self-interest among the users, and perhaps even attempts by some parties (such as managers) to manipulate profi t information in order to achieve more of the profi t at the expense of other parties (such as the shareholders). Hence, accounting regulations and principles that guide the determination of an entity’s profi t fi gure could have an important role in the process of establishing social equity among potentially competing and confl icting interests in the business arena.

Accounting information can serve numerous other social equity functions. Consider the following examples.

■ Accounting information, particularly profi t information, is often an important factor in confl icts

between trade unions and employers in battles for wage increases and improvements in working conditions. Employer groups may support, resist or amend demands for wage increases by unions on the basis of an entity’s profi tability information.

■ Many large corporations provide essential services to the community, such as in the banking,

communications and transportation industries. Governments can, from time to time, exert infl uence over such organisations because of the essential nature of the services. The fi nancial position of large companies such as the National Australia Bank and Telstra, in the case of Australia, are often under public scrutiny. If companies in the banking industry and the telecommunications industry, for example, disclose high sustained profi ts in their fi nancial statements, the government can, among other things, put these industries under pressure not to increase the prices of their services. For example, the Australian Government has been known to put pressure on banks from time to time to not increase bank fees or interest rates at times when the banking industry has recorded record profi ts.

Jackling Accounting ch01.indd 19

Jackling Accounting ch01.indd 19 18/3/10 2:22:42 PM18/3/10 2:22:42 PM

1

20

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

■ Governments can subsidise struggling industries, such as farming and agriculture, in times of

drought, or banks and fi nancial institutions in times of fi nancial crisis and panic. Again, accounting records are the basis for determining the degree of fi nancial distress.

■ Many government services, such as public health, transportation and education, are provided on

a ‘user pays’ basis. The price charged for essential services to the community is often based on the fi nancial cost of providing the service. Accounting records invariably provide detailed cost information, notwithstanding that the assumptions in determining such costs are often contentious.

■ Accounting information has an important role in the redistribution of wealth throughout the

community. Companies must legally pay income tax on their net profi t fi gures. The taxation of company profi t provides a signifi cant source of income to government to fund crucial social and economic programs in the community, such as social security distributions, healthcare, education, and development and maintenance of infrastructure assets (such as roads and bridges). Determination of an entity’s net profi t is ascertainable only from the relevant accounting records.

■ Social and environmental information is increasingly sought from companies. Social responsibility

may include donations to charities. It can also include programs to reduce pollution, increase product safety, improve working conditions and enable better use of natural resources. For example, some organisations offer discounts to students and senior citizens, while others contribute to charitable organisations.

1.5.2

The economic decision-making environment

and society

We have seen that accounting’s regulatory environment impacts on society in many ways. The economic decision-making environment also infl uences society in a number of ways. Accounting’s decision-making environment is concerned with the effi cient allocation of scarce economic resources. The end goal of effi cient resource allocation is growth of the economy. As discussed above, all users of accounting information are concerned with the allocation of scarce economic resources. Needless to say, all users, assuming they are rational decision makers, are concerned about allocating their scarce resources as effi ciently as possible.

Typically, effi ciency is defi ned in terms of the performance of tasks to produce the best yield at the lowest cost from the resources available. This is an input to output relationship; in other words, what you get in return (output) for what is sacrifi ced or expended (input).

To an investor, this is translated into: What return do I get on my investment? Is the return satisfactory, given the relative riskiness of the investment?

To a lender, the question may be: Is the interest rate I get a suffi cient return on the funds advanced, given the risk of the loan?

Suppliers and other trade creditors are concerned with whether amounts owing to them will be paid on a timely basis. Their questions might be: Should I extend credit terms to company A or company B? From which of the two companies am I most likely to get timely repayment?

Importance of accounting in ensuring the effi cient use of

scarce resources

Accounting information is an important guide to users in making effi cient resource allocations.

■ Accounting information discloses vital information about the fi nancial condition and future prospects

of a company. A rational-decision emphasis would suggest that investors, lenders and other users

Jackling Accounting ch01.indd 20

Jackling Accounting ch01.indd 20 18/3/10 2:22:43 PM18/3/10 2:22:43 PM

21

THE ACCOUNTANTING ENVIRONMENT

1

are more likely to expend resources on companies with better fi nancial conditions and prospects than other companies, because they have a better chance of getting a higher return with less risk. Accounting information is relied on in making these assessments.

■ In the absence of fraud or error, accounting information can be used to identify prosperous,

high-performing companies over more mediocre or struggling companies. Stock market analysts and funds managers depend heavily on accounting information in making decisions to buy, sell or hold a company’s securities. Loan offi cers and managers also depend heavily on accounting information in making decisions about whether to extend loans to companies and in assessing the relative riskiness of the loan. Poor-quality accounting information could result in an investor making a potentially disastrous investment in a company, or a lending offi cer granting an equally disastrous loan. Hence, accounting plays an important role in the allocation of scarce resources throughout the economy. The effi cient allocation of resources in an economy is of great importance to society in general. An effi cient, well-functioning economy can deliver, among other things, higher standards of living for members of the community, including better technologies, higher employment levels, better healthcare and education, and a host of other social and economic services and programs.

1.5.3

The international environment and society

The international environment of accounting also impacts on society, particularly through the infl uence of foreign investment on the national economy. In Australia, for instance, it has long been recognised that it is in the country’s economic interests to encourage a strong regulatory accounting framework that will promote the production of high-quality company fi nancial statements. Many companies in Australia need to raise capital on overseas markets in order to grow their business or expand their operations. Financial statements that are perceived by foreign investors to be of high quality, and internationally comparable with other leading industrialised nations, are likely to assist in this process.

SUMMARY

Accounting is a communication system designed to provide economic information useful for decision making by users of the information. A primary user is the owner. Forms of ownership vary and consequently the needs for information vary. In general, however, owners must make decisions about:

• whether to continue or to expand their investments in the entity • how much profi t to withdraw as drawings or dividends

• how much revenue to allocate to the entity in the future (as in the case of government departments) • the size of the ownership claim on the entity’s assets.

In companies, where a board of directors represents the owners’ interests, shareholders require information enabling them to evaluate the stewardship and performance of the directors. Apart from these ownership interests, the shareholder may take the viewpoint of an investor, with the option of selling the shares if the selling price exceeds the value the investor places on the shares.

It was also shown in this chapter that accounting both infl uences and is infl uenced by its environment. There are principally three environmental factors that affect accounting:

• the regulatory environment

Jackling Accounting ch01.indd 21

Jackling Accounting ch01.indd 21 18/3/10 2:22:43 PM18/3/10 2:22:43 PM

1

22

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

• the economic decision-making environment • the international environment.

All three environments are to some extent interdependent, and all have a profound effect on society in general. With respect to the regulatory environment, fi nancial statements prepared by companies in Australia must be in accordance with the Corporations Act, the AASB series of accounting standards and ASX listing requirements. The purpose behind accounting regulation is to provide a measure of fi nancial protection to the various user groups, and society itself, against the potentially detrimental impacts of fraudulent, misleading or poor-quality fi nancial statements.

The economic decision-making environment stresses the importance of accounting information in assisting in the effi cient allocation of scarce resources in the economy. Here again, accounting information impacts on society in a profound way, in the sense that an effi cient, well-functioning economy is the basis for economic growth, including better living standards for the community.

Finally, the implications of the international accounting environment on society have been considered, particularly in relation to the harmonisation of accounting standards and the impact of foreign investment on the economy.

Looking forward

The next chapter examines the nature and use of accounting reports, which represent the prime means of communicating accounting information to a range of users. Whether these statements are adequate for decision making is an issue that will be taken up when the conventional basis of accounting has been addressed.

REVIEW QUESTIONS AND EXERCISES

Revise content

Multiple-choice questions

Provide the solution that gives the best answer to the question.

1.1 Which of the following statements best describes accounting and bookkeeping?

a Accounting and bookkeeping are the same.

b Bookkeeping is the process of recording and communicating fi nancial information. c Accounting is the process of recording, classifying and reporting fi nancial information. d Accounting is the process of recording and classifying fi nancial information.

1.2 John retires from his job as a manager to start his own lawn-mowing business. He decides that he wants to own and operate the business himself. This is an example of:

a A proprietary company b Public sector ownership c A partnership

d Sole ownership

1.3 John retires from his job as a manager to start his own lawn-mowing business. Because he owns and operates the business, he only uses one bank account for private and business use. Which of the following best describes the situation?

a Two accounting entities exist because a business is regarded as separate from the owner. b Two accounting entities exist because the owner is still liable for the business debts. c A single accounting entity exists because there is one shared bank account. d One accounting entity exists because it is a sole ownership.

Jackling Accounting ch01.indd 22

Jackling Accounting ch01.indd 22 18/3/10 2:22:43 PM18/3/10 2:22:43 PM

23

THE ACCOUNTANTING ENVIRONMENT

1

1.4 Although people involved in sole ownerships and partnerships make many similar decisions, which ofthe following decisions relates only to partnerships?

a How much profi t to withdraw

b Whether to expand or cease operations c Evaluating fi nancial stability

d Establishing respective claims on assets

1.5 Which entity produces accounting information and ceases on the death of a member, and which entity’s members are liable for any debts incurred?

a Group of companies b Partnership c Accounting entity d Subsidiary company

1.6 Which of the following provides the most important reason for accounting regulation?

a To enforce government legislation requiring ‘true and fair’ accounting reports b To maintain fairness by providing reports that are comparable between companies

c To protect users from fi nancial losses because of poor-quality or misleading fi nancial statements d To determine which companies are allowed to list on the stock exchange and to monitor their actions

1.7 The highest level of regulatory authority over companies in Australia is the:

a Corporations Act

b Australian Accounting Standards Board (AASB) accounting standards c Australian Securities Exchange (ASX) listing rules

d Financial Reporting Council (FRC)

1.8 Which of the following is the most likely basis for a short-term lender’s decision?

a Whether the entity’s future cash fl ows will be suffi cient to make repayments b Whether the entity has the liquidity to pay its dividends

c Whether increases in the share price will lead to permanent capital gains d Whether the entity can pay its debts in the next three to fi ve years

1.9 Which of the following is not a stated benefi t of international harmonisation of accounting standards?

a Harmonisation may make it easier for companies to raise funds overseas. b Financial statements in different countries could be prepared on a similar basis. c There would be an additional set of standards to refer to, providing more information. d Countries without their own standards could adopt international standards.

1.10 Which of the following is the most accurate?

a Accounting’s role of recording economic transactions has little impact on society.

b Companies are so large they are no longer part of the social fabric, but have become mega-states of their own. c Business entities have an impact on society because they consume vital and scarce resources in order to

deliver products.

d Accounting prevents major collapses of companies because it focuses on accountability, liquidity and solvency.

Short-answer questions

1.11 Defi ne accounting and explain why it exists.

1.12 State what the primary role of accounting is in society.

1.13 What type of information is communicated in an income statement?

1.14 State the purpose of a statement of fi nancial position.

1.15 Explain the entity concept and state how it affects communicating accounting information.

1.16 List and describe three main types of accounting entity.

1.17 Explain two ways in which public sector business enterprises differ from private sector businesses.

Jackling Accounting ch01.indd 23

Jackling Accounting ch01.indd 23 18/3/10 2:22:43 PM18/3/10 2:22:43 PM

1

24

PART 1

BACKGROUND ENVIRONMENT AND PRINCIPLES

ACCOUNTING

1.18 Outline the main sources of regulation of fi nancial reporting in Australia.

1.19 List and describe the three main components of the accounting environment.

1.20 Identify two main user groups of accounting information. Explain how the two groups may have different needs for information.

1.21 What is meant by the international harmonisation of accounting standards?

1.22 What is the role of the auditor in reporting fi nancial information?

1.23 Explain how the regulatory environment of accounting impacts on society.

Understanding and application

1.24 ‘An accounting entity may be, but is not necessarily, a legal entity.’ Discuss this statement in relation to the various types of business enterprises.

1.25 Compare the rights and obligations of: a Holders of shares in limited companies b Holders of debentures in limited companies c Partners in a partnership

d Sole traders

1.26