Research

Publication Date: 25 May 2006 ID Number: G00139568

© 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved. Reproduction and distribution of this publication in any form without prior written permission is forbidden. The information contained herein has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or adequacy of such information. Although Gartner's research may discuss legal issues related to the information technology business, Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner shall have no liability for errors, omissions or inadequacies in the information contained herein or for interpretations thereof. The opinions expressed herein are subject to change without notice.

Magic Quadrant for Storage Services, 2Q06

Adam W. Couture, Robert E. Passmore

Use Gartner's storage service Magic Quadrant to evaluate providers' vision and ability to execute their services, and to determine which providers can best address your

Publication Date: 25 May 2006/ID Number: G00139568 Page 2 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

WHAT YOU NEED TO KNOW

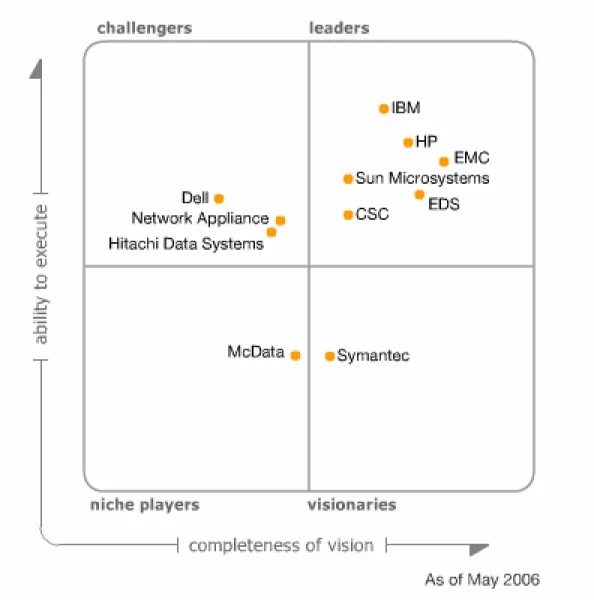

Gartner's 2Q06 storage service Magic Quadrant is a useful starting point to identify and evaluate storage services from a variety of vendors. Selection should be based on a detailed evaluation of an enterprise's storage needs and objectives compared to a service provider's capacity to fulfill those requirements and expectations. Just because a service provider falls into the Leaders quadrant doesn't automatically make it the right choice. For example, service providers in the Challengers quadrant are extremely capable of delivering the day-to-day storage services required by most enterprises and frequently provide exceptional value. A visionary vendor can deliver competitive advantages through its approach to service technologies, best-in-class strategies and services tied to technology innovation. Niche players deliver excellent service for exceptional value in their particular geographies or technological focus areas. All the vendors ranked in Gartner's 2Q06 storage service Magic Quadrant (see Figure 1) provide good services in their respective areas. Therefore, enterprises need to determine which storage service provider (or providers) can best address their particular requirements.

Publication Date: 25 May 2006/ID Number: G00139568 Page 3 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

MAGIC QUADRANT

Figure 1. Magic Quadrant for Storage Services, 2Q06

Source: Gartner (May 2006)

Market Overview

In 2005, the worldwide storage service market was worth more than $24 billion. Depending on worldwide economic conditions, compound annual growth rates for storage services were approximately 8 percent (2004 to 2009), bringing the worldwide opportunity to more than $30 billion by 2009. North America accounts for the largest portion of the storage service market; however, the Asia/Pacific region is experiencing the fastest growth.

Publication Date: 25 May 2006/ID Number: G00139568 Page 4 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Market Definition/Description

The following services comprise Gartner Dataquest's core storage service segmentation, which serves as the baseline for all market sizing and market share assessments. All these service categories were taken into account when we evaluated storage service providers for this Magic Quadrant. However, the most emphasis was given to professional services, such as consulting, implementation and management services and the vendors' abilities to integrate these services in multivendor environments. (Note: Vendor customer services, such as break/fix, are evaluated by Gartner in individual Vendor Rating research).

Storage hardware maintenance and support services — preventive and remedial services that physically repair or optimize hardware, including contract maintenance and per-incident repair. Hardware support also includes online and telephone technical troubleshooting,

assistance for setups and fee-based hardware warranty upgrades. Exclusive of parts bundled into maintenance contracts, sales of all parts are also included. This segment includes only external customer spending on these services.

Storage software maintenance and support services — include revenue derived from long-term and pay-as-you-go (incident-based) support contracts. Software support contracts include remote troubleshooting and support conducted via telephone and online means, installation assistance and basic usability assistance. In some cases, software support services may include new product installation services, installation of product updates, migrations for major releases of software and other types of proactive or reactive on-site services. Software products and

technologies covered under this category include operating systems and infrastructure software. Storage software support services do not include revenue derived from purchasing subscriptions that provide entitlements and rights to use future minor versions (point releases) or future major releases of software. Gartner Dataquest does not include revenue associated with product license updates and upgrades in vendor revenue reports and forecasts. However, we cover entitlements and publications for software support services.

Storage consulting services — help organizations assess different technology and

methodology strategies and align their storage strategies to their business or process strategies. These services support customers' IT initiatives by providing strategic, architectural, operational and implementation planning related to storage. Strategic planning includes advisory services that help organizations assess their IT needs and formulate system implementation plans. Architecture planning includes advisory services that combine strategic plans and the knowledge of emerging technologies to create the logical design of the storage environment and the

supporting infrastructure to meet customer requirements. Operational assessment and benchmarking includes services that assess the operating efficiency and capacity of an

organization's storage environment. Implementation planning includes services aimed at advising customers on the rollout and testing of new storage deployments.

Storage implementation services — support the implementation and rollout of new storage infrastructure, including consolidating the storage infrastructure. Activities may include hardware or software procurement, configuration, tuning, staging, installation and interoperability testing. Storage management services — transfer all or part of the day-to-day management

responsibilities for a customer's storage environment — including storage area networks (SANs), network-attached storage (NAS) and tape libraries — as well as the ownership of the technology or personnel assets to an outside vendor. These services may include system operation or support, capacity planning, asset management, availability management, performance

management, administration, security, remote monitoring, technical diagnostics/troubleshooting, configuration management, system repair management and generation of management reports.

Publication Date: 25 May 2006/ID Number: G00139568 Page 5 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Storage-on-demand services (the storage utility), as well as backup and recovery services, also fall into this category when some degree of management is included in the service.

Inclusion and Exclusion Criteria

To be considered for our Magic Quadrant, vendors had to deliver at least two of the storage services defined above and serve clients throughout North America. Only large service providers with annual storage service revenue of $100 million or more were considered, exclusive of revenue from physical tape vaulting. Additionally, the provider had to cater to multiple market segments. For example, an independent software vendor (ISV) providing software support and no other storage services would not qualify.

Qualifying companies ranged from hardware manufacturers and ISVs to large outsourcing providers. Although some storage resellers and integrators deliver a level of storage services, they were excluded from consideration because the focus of this Magic Quadrant is on storage original equipment manufacturers, outsourcers and ISVs. Additionally, this assessment does not include many specialty or regional service providers that offer varying levels of storage services from consulting to implementation services to managed storage services.

Added

• Symantec and McData

Dropped

• CNT (acquired by McData) and Storage Technology (acquired by Sun Microsystems)

Evaluation Criteria

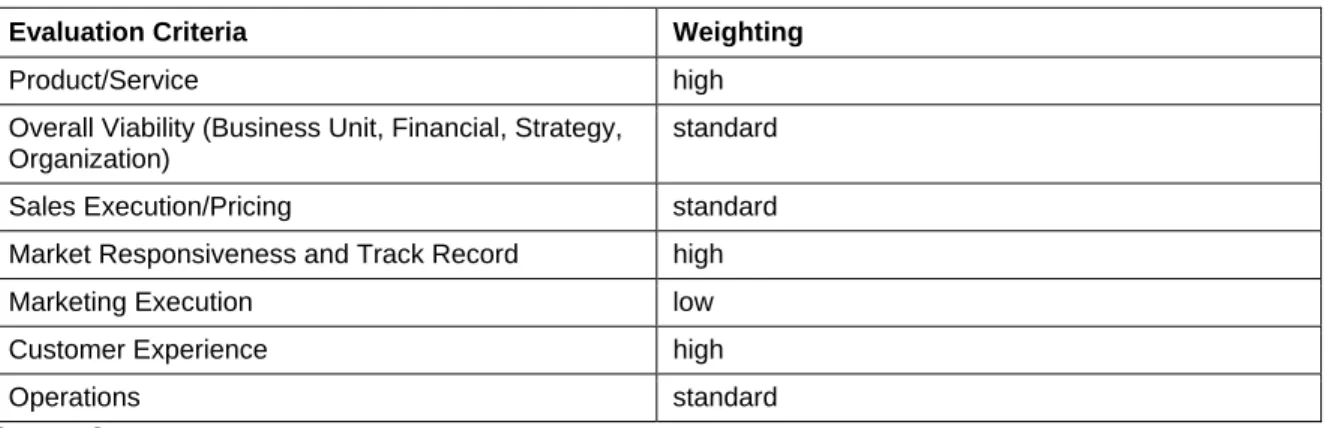

Ability to Execute

The Ability to Execute score includes ratings on the strength of corporate management; the vendor's offering in terms of execution, including partnerships, functionality, technology, and service and support; and the vendor's overall stability and viability. The offerings are rated on service breadth and maturity, as well as customer satisfaction.

Table 1. Ability to Execute Evaluation Criteria

Evaluation Criteria Weighting

Product/Service high Overall Viability (Business Unit, Financial, Strategy,

Organization)

standard Sales Execution/Pricing standard Market Responsiveness and Track Record high Marketing Execution low Customer Experience high

Operations standard

Publication Date: 25 May 2006/ID Number: G00139568 Page 6 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Completeness of Vision

The Completeness of Vision score is based on the vendor's value proposition, service technology vision, market presence and growth plans, as well as its fit into enterprise sourcing operations. We rate an offering's likely development in functionality, service and support, and how the vendor plans to keep the offering viable in a challenging marketplace.

Table 2. Completeness of Vision Evaluation Criteria

Evaluation Criteria Weighting

Market Understanding standard Marketing Strategy high Sales Strategy standard Offering (Product) Strategy standard

Business Model low

Vertical/Industry Strategy low

Innovation high Geographic Strategy standard

Source: Gartner

Leaders

Leaders are performing well today, have a clear vision of market direction and are actively building competencies to sustain their leadership position in the market.

Challengers

Challengers execute well today, but they have a less-defined view of market direction and, therefore, they may not be aggressive in preparing for the future.

Visionaries

Visionaries have a clear vision of market direction and are focused on preparing for that, but they still can improve in terms of optimizing service delivery.

Niche Players

Niche Players focus on a particular segment of the client base, as defined by characteristics such as size, vertical or project complexity. Their ability to outperform or be innovative may be affected by this narrow focus. Niche Players concentrate on particular market segments and often only support applications that apply to those targeted segments.

Vendor Comments

CSC

CSC is a worldwide outsourcer, with few storage services delivered outside the scope of outsourcing or managed hosting. Hitachi Data Systems (HDS) is the primary CSC storage platform for managed hosting solutions, but the company also partners with EMC and Network Appliance (NetApp). As an outsourcing and managed service provider, CSC understands the benefits of effective storage management, including storage security, policy-based management

Publication Date: 25 May 2006/ID Number: G00139568 Page 7 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

and storage-on-demand alternatives. It has made considerable strides in these areas during the past two years. A new tape encryption offering heralds the company's focus on storage security, and a tape tracking service is slated for the second half of 2006.

CSC created its Global Solutions and Technology Group in 2005 to develop standardized bundled offerings. One of the group's priorities has been to expand information life cycle management (ILM) storage tiering offerings to more customers. In April 2006, CSC engaged Goldman Sachs to put the company up for sale and announced that it will cut 4,700 jobs in 2006 and 2007. Although CSC contends that its storage service delivery capabilities will be unaffected by the downsizing, if the company were to be acquired and split up, as is speculated, then its storage service capabilities could be affected.

Dell

During the past year, Dell has focused on developing service consistency across geographies. In 2006, the company opened its fifth worldwide Enterprise Command Center in Malaysia.

Additionally, premium service offerings are available worldwide, with consistent service processes worldwide. Dell continues to invest in and enhance its delivery and support capabilities. For example, the company independently developed proprietary SAN discovery and assessment tools. Additionally, the company's focus on service metrics has resulted in a unique tool to scope customer serviceability. Focusing on implementation and consolidation services, Dell's storage service objective is to drive down costs through automation technology and standardized repeatable services that can be consistently delivered worldwide.

As a consequence, Dell's storage service vision is also operational, striving to reduce variance in execution through process innovation and rigorous service operations management, leveraging automation technology and flexible service process design. Dell uses a mixture of Dell field engineers and independent service organizations to provide break-fix service and support, but the company always remains the point of customer contact. Dell's storage professional services focus on infrastructure areas, such as consolidation and implementation. In mid-2006, Dell plans to revamp service offerings, metrics and management for enterprise customers.

EDS

Most of EDS' storage-related revenue is derived from managed hosting and outsourcing. EDS claims 14 petabytes of storage under management, with two petabytes delivered through use-based pricing. The company continues to be proactive in migrating customers to managed SANs, and it is implementing tiered storage options, including NAS on-demand offerings.

Although EMC remains the company's primary storage technology provider as an "agility alliance" partner, options for NetApp solutions were rolled out in 2005. Products from these two companies constitute EDS' five primary storage tiers complemented by five backup options. New backup options include remote server backup and virtual tape libraries. Continuous data protection is one of the backup initiatives for 2006 and beyond. In late 2005, EDS consolidated storage services with hosting services to create a combined data center service organization.

EMC

EMC is a market leader in direct and fabric-attached storage, with an extensive service customer base. In 2005, EMC grew service revenue to more than $2.65 billion, contributing more than one-fourth of the company's overall revenue. Professional services, which have been an emphasis for EMC for the past several years, account for 16 percent of the company's overall revenue. The launch of EMC Consulting in 2005 formalized a number of professional service offerings in the areas of ILM, consolidation, storage management and data protection.

Publication Date: 25 May 2006/ID Number: G00139568 Page 8 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

The company's Microsoft practice was enhanced in 2006 with the acquisition of Internosis. In 2005, EMC standardized software support services across product lines and improved e-support. The company considers storage security a major initiative and rolled out security assessment services in early 2006. It announced a security consulting unit in April, with intentions to grow it to 90 people. In May 2006, EMC replaced its traditional four-hour, same-day hardware support with a variety of tiered offerings on newly announced CLARiiON products. On-site CLARiiON support will continue to be delivered primarily through authorized service partners. Gartner anticipates more on-demand pricing alternatives and additional managed services from EMC in late 2006.

Hitachi Data Systems

HDS provides hardware and software support directly via its high-end storage line. Midrange products are supported directly or through authorized service providers. During the past two years, HDS has placed substantial emphasis on growing its service capabilities and revenue. During that time frame, the company has developed standardized professional services that can be consistently delivered through these channel partners. Professional services are delivered directly and through strategic partners, such as Glasshouse Technology and Novus Consulting Group. Management services are predominantly delivered through partners.

In 2005, HDS undertook a major training program for field sales and support personnel to teach them how to develop and sell service-led engagements. In 2006, HDS' professional services focus on virtualization, application alignment and data classification enabled by its TagmaStore Universal Storage Platform and Network Storage Controller virtualization capabilities. During the past year, HDS has experienced major leadership changes in its service organization, including the senior vice president of Global Solutions Strategy and Development. The new leadership team, plus a yet-to-be-named vice president of Global Solutions and Services, will define HDS' professional service directions for 2006 and 2007.

HP

HP aligns its storage service investments and portfolio to major infrastructure initiatives, such as adaptive infrastructure and ILM (seven new ILM services were announced in 2005). The

company is investing heavily in managed services to offset lower margins in commodity services, such as break/fix. Outsourcing capabilities were strengthened in 2005 as HP delivered on its Proctor and Gamble engagement. HP seems committed to on-demand capabilities but customer demand remains slow.

HP is also investing in storage management and automation, and announced services to

implement and manage them, including new remote monitoring and management services. HP is incorporating IT Infrastructure Library (ITIL) into internal and external service delivery. Gartner does not anticipate any major changes in HP's storage service direction resulting from new executive leadership; however, anticipated cost cutting and head-count restrictions could limit some service investments.

IBM

IBM's storage service vision is focused on information on-demand initiatives and, more recently, ILM. Its service portfolio includes business continuity and recovery services, infrastructure and system management services, networking services, technical-support services and IT education services. In the past year, IBM announced a number of new professional services, such as data classification services and managed services for e-mail compliance. New managed backup services announced in 2005 target the midmarket.

Although IBM does not track storage services as a separate business, Gartner acknowledges IBM as the market share leader. In the past, IBM's storage service initiatives were largely driven

Publication Date: 25 May 2006/ID Number: G00139568 Page 9 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

by a broader set of IT services to enable outsourcing, managed hosting or customer-enabled solutions. In March 2006, the company began realigning its technology service organizations along product lines, including storage. The new IBM Global Technology Services product lines span outsourcing, integrated technology and maintenance. Although the product lines' business plans are still under development, Gartner believes this realignment has the potential to improve how storage services are created and delivered.

McData

McData is a midsize vendor of storage networking technology and fiber channel switching solutions. Prior to the company's acquisition of CNT in June 2005, McData put little emphasis on storage services. Since the acquisition, McData has integrated CNT's considerable storage service capabilities and is attempting to make services a strong contributor to the company's bottom line. The company's two major service areas focus on distance networking, and backup and recovery. McData storage infrastructure products are sold worldwide, but consulting, implementation and management services are delivered primarily in the U.S., with capabilities being expanded in Europe. Services in Asia/Pacific are expected to be rolled out in late 2006. McData's storage service vision mirrors CNT's former vision and includes remote storage

management and automation. The company has invested in tools to automate processes such as infrastructure assessments, long-distance migrations, service delivery, and remote infrastructure monitoring and management. McData's consulting organization of 120 is down from the 180 professional service people employed prior to the acquisition. It is still too early to determine whether McData can for the first time successfully enter into and manage a storage service business, particularly in the area of storage professional services.

Network Appliance

NetApp leads the NAS/unified storage market and continues to lead in Internet Small Computer System Interface arrays. In 2005, the company grew service revenue by nearly 50 percent. Part of this growth was attributable to NetApp's emphasis on its small but growing professional service capabilities during the past two years. Still, some larger customers believe that NetApp needs to prove itself in this area. Servicing reseller channels and a growing cadre of service delivery partners bolster NetApp's service organization of 300.

In 2005, NetApp consolidated its help desk operations, but local-level support is available in more than 80 countries. This should help relieve customer-reported lack of help desk depth. NetApp continues to invest in its self-service Web portal and service automation capabilities, and it has built a reputation for some of the best e-support capabilities in the storage industry. Although NetApp has been slow to adopt ITIL internally, all internal service processes and procedures are being developed within the ITIL framework. In 2005, the company formalized standardized consulting services with the launch of ConsultEdge Services, which focuses on SAN design, data migration, storage consolidations, and backup and recovery. 2006 service initiatives include strategic business consulting services, expanded reseller service programs and enhanced storage service offerings.

Sun Microsystems

Through its acquisition of StorageTek, Sun Microsystems strengthened its storage service capabilities on a number of fronts. The net result of the acquisition increased Sun's geographic reach and storage service revenue market share, although the majority of StorageTek's service revenue came from break/fix services. Moreover, the addition of StorageTek's professional service head count reinforced the ranks of Sun's professional service organization, which had been plagued by attrition and reductions. StorageTek's multivendor service capabilities provide Sun with the heterogeneous product support needed to deliver on major Sun service initiatives,

Publication Date: 25 May 2006/ID Number: G00139568 Page 10 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

such as Sun Preventive Services. However, these support services tend to be subcontracted to smaller local service providers or maintenance contract management, so they are not on par with IBM or HP for multivendor support and outsourcing.

Organizational and integration issues have improved but still represent work in progress. When Sun acquired StorageTek, the StorageTek organization melded into Sun’s Data Management Group. The storage service delivery organization, headed by StorageTek's Eula Adams, is now integrated into Sun's service organization, which is also under new leadership as Sun Services Executive Vice President Don Grantham was promoted to executive vice president of Sun's Global Sales and Services Organization. Gartner believes that Sun's storage service organization is properly aligned in the service organization, where it can best influence and integrate service investments and deployments. Although the storage service portfolios of the two organizations have yet to be fully integrated, Sun anticipates that this will be resolved in the second half of 2006.

Symantec

Symantec enters the storage service Magic Quadrant in 2006 following its acquisition of Veritas Software in July 2005. Software support is segmented according to consumer and business products. Symantec personnel support business software from three major support hubs, while consumer product support is outsourced. Business software support is a strength for Symantec, with support tiers spanning basic, extended and business-critical support. Business-critical support was extended to all business products in early 2006 and includes fly-to-site services and priority case handling.

Symantec's consulting services span business continuity, storage management, utility computing and security. Professional and support services are supplemented through authorized partner programs. Symantec leverages its strong capabilities in security consulting, managed security and security intelligence as key market differentiators. Of Symantec's 700-person consulting organization, 415 are aligned with storage services. Symantec's managed service offering is dedicated to security services, but Gartner anticipates that managed services will be extended to storage in the near term, initially in the area of managed backups.

RECOMMENDED READING

"Magic Quadrant for Storage Services, 2Q05" "Storage Service Market Leaders Hold Their Ground" "Magic Quadrant for MSSPs, North America, 2H05"

"Magic Quadrants and MarketScopes: How Gartner Evaluates Vendors Within a Market"

Acronym Key and Glossary Terms

HDS Hitachi Data Systems

ILM information life cycle management ISV independent software vendor ITIL IT Infrastructure Library NAS network-attached storage SAN storage area network

Publication Date: 25 May 2006/ID Number: G00139568 Page 11 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Evaluation Criteria Definitions

Ability to Execute

Product/Service: Core goods and services offered by the vendor that compete in/serve the defined market. This includes current product/service capabilities, quality, feature sets, skills, etc., whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability (Business Unit, Financial, Strategy, Organization): Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood of the individual business unit to continue investing in the product, to continue offering the product and to advance the state of the art within the

organization's portfolio of products.

Sales Execution/Pricing: The vendor’s capabilities in all pre-sales activities and the structure that supports them. This includes deal management, pricing and negotiation, pre-sales support and the overall effectiveness of the sales channel.

Market Responsiveness and Track Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message in order to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional, thought leadership, word-of-mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements, etc. Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the Web site, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling product that uses the appropriate network of direct and indirect sales, marketing, service and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Publication Date: 25 May 2006/ID Number: G00139568 Page 12 of 12 © 2006 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature set as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition. Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including verticals.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.

REGIONAL HEADQUARTERS

Corporate Headquarters

56 Top Gallant Road Stamford, CT 06902-7700 U.S.A. +1 203 964 0096 European Headquarters Tamesis The Glanty Egham Surrey, TW20 9AW UNITED KINGDOM +44 1784 431611 Asia/Pacific Headquarters

Gartner Australasia Pty. Ltd. Level 9, 141 Walker Street North Sydney

New South Wales 2060 AUSTRALIA +61 2 9459 4600 Japan Headquarters Gartner Japan Ltd. Aobadai Hills, 6F 7-7, Aobadai, 4-chome Meguro-ku, Tokyo 153-0042 JAPAN +81 3 3481 3670

Latin America Headquarters

Gartner do Brazil

Av. das Nações Unidas, 12551 9° andar—World Trade Center 04578-903—São Paulo SP BRAZIL