Volatility Modelling using ARCH and GARCH Models (A Case study of Exchange Rate in Sudan) (at the period from 2007-2018 )

Full text

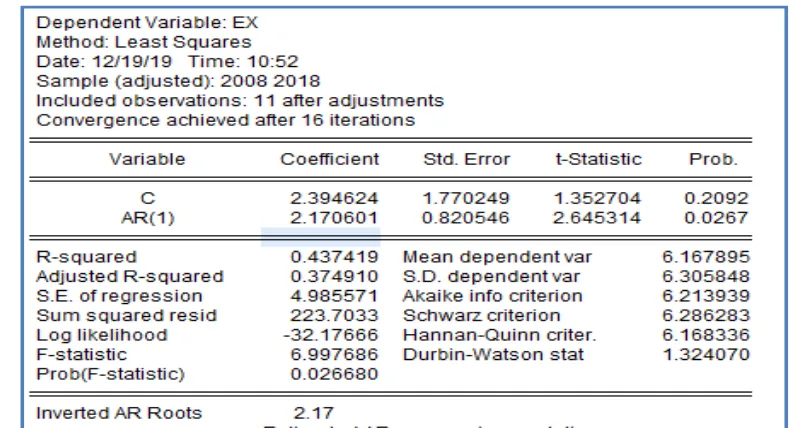

Figure

Related documents

Emperor International Journal of Finance And Management Research [EIJFMR] ISSN: 2395-5929. @Mayas Publication

(C) Comparison of the number of fNRBCs from maternal peripheral blood from abnormal pregnancy (Table S2) and normal pregnancy (Table S1) at 18 weeks of gestation. Fifteen

Results showed that liquidity, return on asset, firm size and previous year dividend has a positive relationship with dividend payout among banks involved in

In summary, Wnt5b gov- erns the phenotype of BLBC by activating both canonical and non-canonical Wnt signaling (Additional file 1: Figure S5), and should be a promising

This Chapter shall apply to the procurement of all construction services under CPC 51 procured by the procuring entities listed in Sections A, B and C, unless

• Based on the Kolmogorov-Smirnov and Anderson-Darling test criteria, the three-parameter Burr Type XII gives the best fit to the daily maximum ambient nitrogen dioxide

Toward a 3D coupled atomistic and discrete dislocation dynamics simulation: dislocation core structures and Peierls stresses with.. several character angles in FCC aluminum Jaehyun